Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

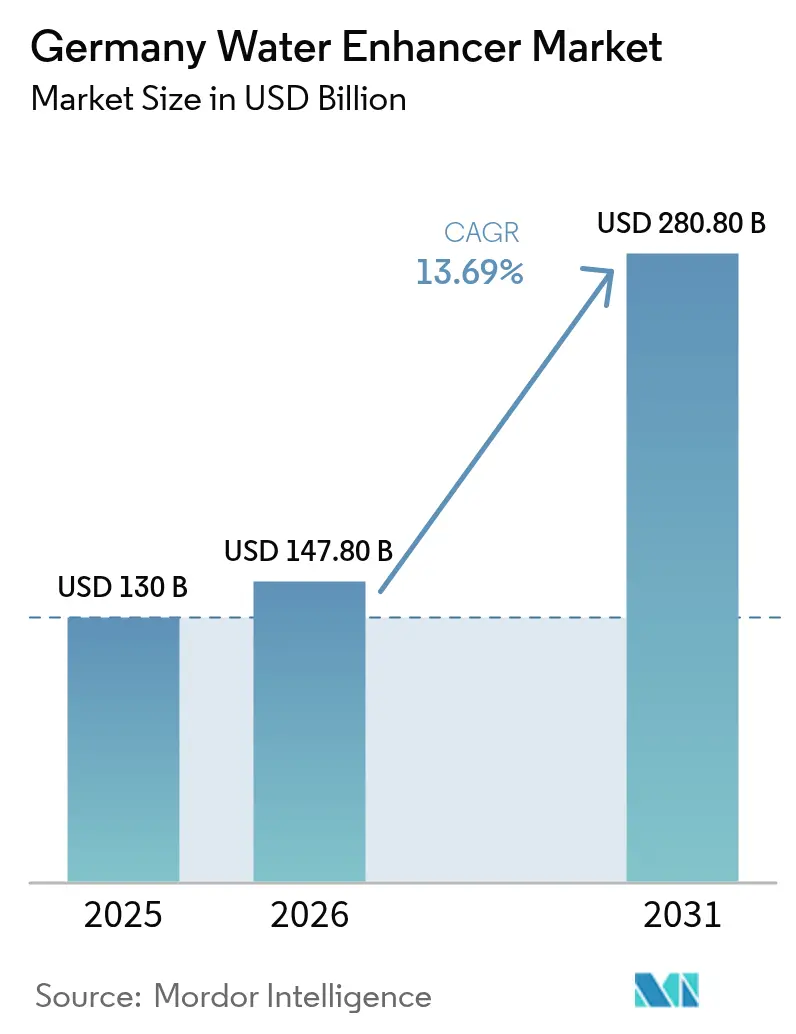

| Base Year Market Size (2025) | USD 130 Billion |

| Market Size (2026) | USD 147.8 Billion |

| Market Size (2031) | USD 280.8 Billion |

| Growth Rate (2026 - 2031) | 13.69% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Water Enhancer Market Analysis by Mordor Intelligence

The German water enhancer market size is expected to grow from USD 130 million in 2025 to USD 147.8 million in 2026 and is forecast to reach USD 280.8 million by 2031 at 13.69% CAGR over 2026-2031. This growth stems from changing consumer preferences, increased health awareness, and continuous product development. German consumers are shifting toward healthier, low-calorie alternatives to traditional soft drinks, making water enhancers an attractive option for personalized hydration. The market expansion is supported by growing wellness consciousness, with products containing vitamins, minerals, electrolytes, and natural extracts gaining consumer interest. The demand for functional beverages offering energy enhancement, immune support, and cognitive benefits has strengthened the water enhancer segment. Urban consumers, particularly younger demographics, prefer portable formats, including liquids, powders, and tablets. The market growth is further supported by expanded distribution through online channels and supermarkets, providing consumers with easy access to various flavors and product formats.

Key Report Takeaways

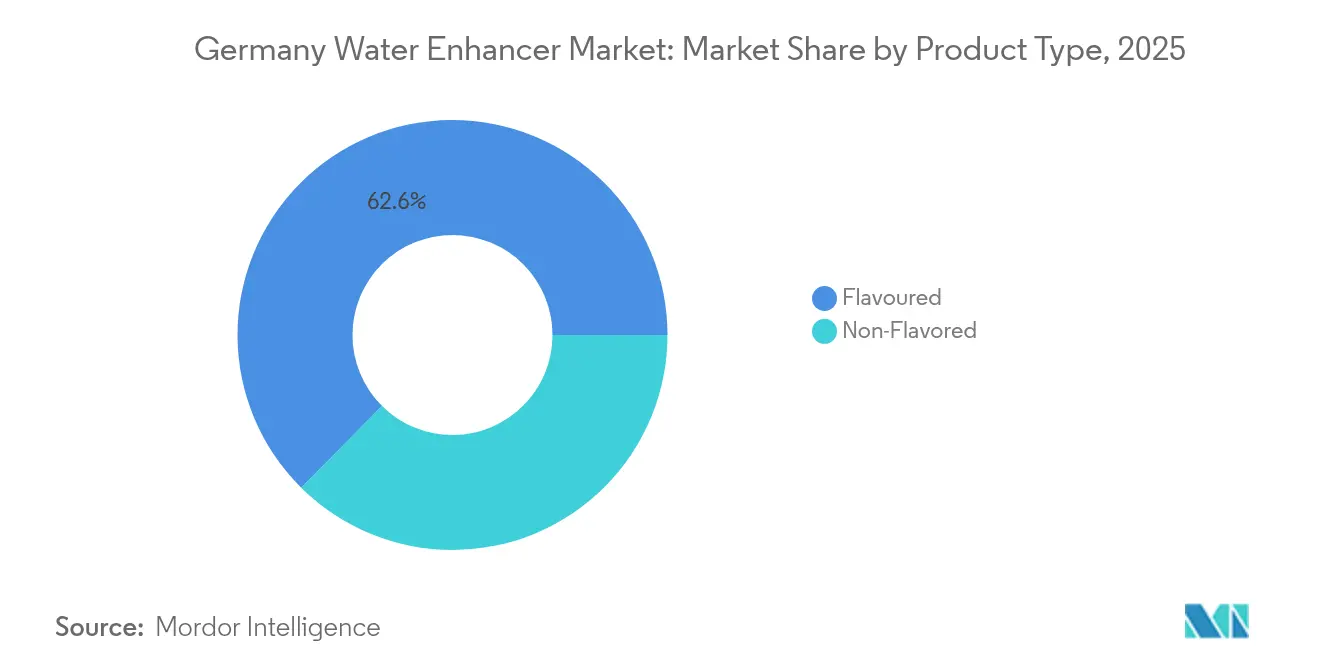

- By product type, Flavoured led with 62.58% of the German water enhancer market share in 2025, and Non-Flavored is projected to post the fastest 13.70% CAGR through 2031.

- By ingredient source, Artificial/Synthetic variants accounted for 64.12% share of the German water enhancer market size in 2025, while Natural/Organic formulations are advancing at 14.42% CAGR to 2031.

- By sweetener type, Without Sugar products captured 65.20% share of the German water enhancer market size in 2025, and With Sugar lines are set to expand at 13.41% CAGR through 2031.

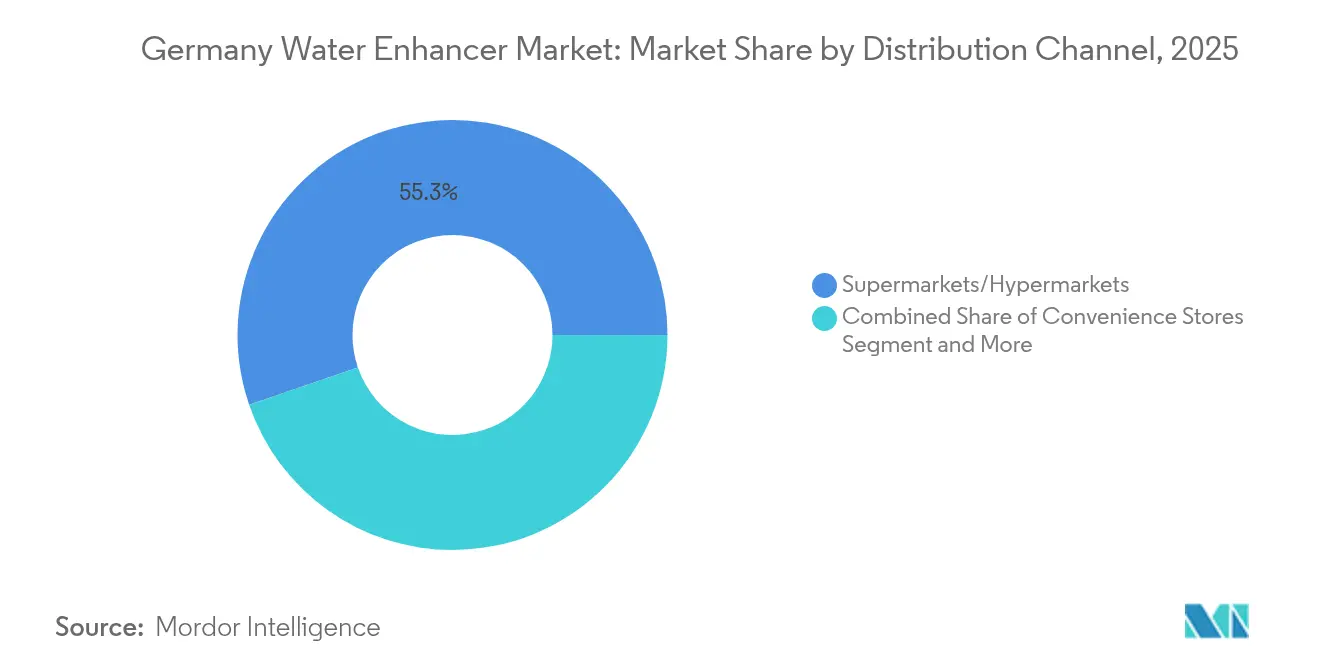

- By distribution channel, Supermarkets/Hypermarkets commanded 55.25% share in 2025, and Online Retail Stores are forecast to grow fastest at 16.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Water Enhancer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban lifestyles and on-the-go consumption support compact, portable enhancer formats | +2.8% | Major German cities (Berlin, Munich, Hamburg) and metropolitan areas | Medium term (2-4 years) |

| Rising health consciousness boosts demand for low-calorie, sugar-free beverages | +3.2% | Nationwide, with strongest impact in Bavaria, Baden-Württemberg, and North Rhine-Westphalia | Long term (≥ 4 years) |

| Growth of fitness and wellness trends increases demand for functional water products | +2.1% | Urban centers and affluent regions | Medium term (2-4 years) |

| Expanding e-commerce channels make enhancers more accessible to consumers | +1.9% | Tech-forward cities like Berlin and Hamburg | Short term (≤ 2 years) |

| Innovation in natural and organic formulations attracts health-focused buyers | +2.4% | Premium markets in southern Germany (Bavaria, Baden-Württemberg) | Long term (≥ 4 years) |

| Marketing by global brands improves product awareness and trial rates | +1.3% | Nationwide, with emphasis on major retail chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urban Lifestyles and On-The-Go Consumption Support Compact, Portable Enhancer Formats.

Urban population density drives demand for space-efficient hydration solutions, as city residents seek convenient alternatives to traditional beverage formats. In Germany, the increasing urbanization and fast-paced lifestyle of consumers have created a strong market for portable water enhancers. Water enhancer drops align with micro-dosing preferences, enabling consumers to adjust hydration intensity while reducing storage space requirements. In October 2024, Mio, a Kraft Heinz brand, launched its "Bottle Boards" campaign, which transforms reusable water bottles into advertising platforms. The campaign, targeting Gen-Z consumers, showcases how brands utilize urban environments for marketing purposes. The urbanization trend particularly benefits liquid formats compared to powder alternatives, as drops integrate easily into fast-paced lifestyles without requiring mixing preparation.

Rising Health Consciousness Boosts Demand for Low-Calorie, Sugar-Free Beverages.

The increasing emphasis on health consciousness serves as a primary catalyst for the expansion of the water enhancer market in Germany. According to the IfD Allensbach, as of 2024, approximately 24.26 million people in Germany have shown a strong inclination toward healthy eating and maintaining a healthy lifestyle, which has significantly influenced their beverage consumption patterns [1]Source: IfD Allensbach, "Number of people interested in healthy eating and a healthy lifestyle in Germany", www.ifd-allensbach.de. This transformation has generated increased demand for beverages characterized by low caloric content, absence of sugar, and functional properties, positioning water enhancers as an optimal solution. German consumers are demonstrating a diminishing preference for conventional soft drinks and sugar-laden beverages, attributed to enhanced awareness regarding the correlation between sugar consumption and health conditions, including obesity, diabetes, and cardiovascular diseases. Water enhancers present a pragmatic alternative, enabling consumers to incorporate flavor into water without sugar or excessive caloric content, while simultaneously delivering supplementary benefits through vitamins, electrolytes, or herbal extracts.

Growth Of Fitness and Wellness Trends Increases Demand for Functional Water Products.

The rising fitness and wellness trends in Germany are driving increased demand for functional water products, particularly water enhancers that offer nutritional benefits beyond hydration. As Germans increasingly incorporate physical activities like gym workouts, running, yoga, and cycling into their daily routines, the demand for hydration solutions supporting performance, recovery, and health has grown. For instance, according to Europe Active, Germany recorded approximately 11.3 million fitness club members in 2023 [2]Source: Europe Active, "European Health & Fitness Market Report 2024", www.europeactive.eu, representing an increase of one million members from the previous year. Water enhancers containing electrolytes, B-vitamins, antioxidants, and adaptogens have become essential for fitness enthusiasts seeking enhanced hydration options. These products address various wellness objectives, including energy enhancement, immune support, digestive health, and fatigue reduction. The growing preference for personalized health routines has led consumers toward customizable beverage options, making water enhancers particularly attractive due to their adjustable dosage and flavor intensity.

Expanding E-Commerce Channels Make Enhancers More Accessible to Consumers.

E-commerce growth has made water enhancers more accessible to German consumers, contributing to market expansion. Digital shopping has become integral to daily life, particularly after the pandemic, with German consumers increasingly purchasing beverages and health products online due to convenience, variety, and competitive prices. According to the Federal Statistical Office, 77.5% of Germans aged 25-45 made online purchases in 2024 [3]Source: Federal Statistical Office, "online shoppers who ordered and purchased products on the internet", www.destatis.de. E-commerce enables water enhancer brands to reach health-conscious consumers nationwide without traditional retail constraints. This benefits smaller and emerging brands, which can target specific consumer segments through digital marketing, influencer collaborations, and social media. Online platforms provide educational resources, including usage instructions, health benefits information, and consumer reviews, helping new customers understand the products. Features like subscription services, product bundles, and automatic reordering improve customer retention and encourage consumers to try different flavors and variants. Online-focused brands also develop and launch new formulations and wellness products more quickly due to reduced operational costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product development and approvals hampered by stringent food and beverage regulations | -1.8% | Nationwide, with strongest impact due to strict German food law compliance requirements | Long term (≥ 4 years) |

| Market share curtailed by intense competition from flavored bottled water and soft drinks | -2.3% | Major retail markets across all German states | Medium term (2-4 years) |

| Trust in some products reduced by consumer concerns over artificial sweeteners and additives | -1.5% | Nationwide, with heightened sensitivity in health-conscious regions | Medium term (2-4 years) |

| Eco-conscious consumers impacted by environmental worries about plastic packaging | -1.1% | Nationwide, with strongest impact in environmentally progressive cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Product Development and Approvals Hampered by Stringent Food and Beverage Regulations.

The German water enhancer market faces growth limitations due to strict regulatory requirements for food and beverage products. As a member of the European Union, Germany follows comprehensive food safety and consumer protection standards through the European Food Safety Authority (EFSA) and the Federal Office of Consumer Protection and Food Safety (BVL). These regulations govern product composition, health claims, labeling, additives, and advertising. Water enhancer manufacturers must obtain pre-market approval for new ingredients, including botanical extracts, sweeteners, and functional additives. This approval process requires extensive testing, which is both time-intensive and expensive, particularly affecting smaller companies with limited resources. Additionally, manufacturers must provide scientific evidence to support any claims about health benefits, energy enhancement, or hydration, which restricts marketing capabilities and extends product launch timelines. These regulatory requirements can deter market entry and slow innovation due to high compliance costs and financial risks.

Market Share Curtailed by Intense Competition from Flavored Bottled Water and Soft Drinks.

The Germany water enhancer market faces significant competition from flavored bottled water and soft drinks, which maintain dominance in the hydration and refreshment categories. Despite offering customization, portability, and functional benefits, water enhancers struggle to compete with the convenience and familiarity of ready-to-drink beverages. Flavored bottled water has established a strong market presence by providing zero or low-calorie options that appeal to health-conscious consumers without requiring preparation. Soft drink manufacturers, particularly those offering sugar-free or "light" variants, maintain substantial brand loyalty and marketing influence, limiting the growth of water enhancers. The extensive distribution networks and large promotional budgets of major beverage companies enable them to secure prime shelf space and achieve economies of scale that water enhancer brands cannot replicate. This competitive landscape affects pricing, product visibility, and consumer retention for water enhancers, which remain a niche category in Germany compared to established beverage segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flavoured Segment Drive Market Leadership

The flavoured segment maintains a dominant 62.58% market share in 2025, demonstrating substantial consumer preference for enhanced beverage taste profiles. This significant market presence is attributed to addressing the inherent challenge of water's neutral taste, which presents a notable barrier to optimal hydration levels. The Non-Flavored segment, despite its smaller market presence, demonstrates robust growth potential with a projected 13.70% CAGR through 2031, primarily driven by health-conscious consumers seeking unadulterated hydration enhancement. This segment's expansion correlates with increased consumer awareness regarding artificial additives, particularly following the World Health Organization's 2023 health advisory regarding sucralose consumption.

The market penetration of flavor drops has been significantly enhanced through social media platforms, where consumer-generated content showcasing hydration formulations influences product adoption and consumption patterns. Non-flavored variants have established a strong presence among fitness practitioners and medical professionals who emphasize electrolyte supplementation without flavor modifications, indicating distinct market segmentation opportunities based on consumption occasions rather than demographic classifications.

By Ingredient Source: Natural Formulations Reshape Premium Positioning

Artificial/Synthetic ingredients currently constitute 64.12% of the market share in 2025, primarily attributed to operational cost efficiencies and well-established supply chain infrastructure that facilitates mass-market pricing strategies. Natural/Organic formulations demonstrate significant market expansion with a 14.42% CAGR through 2031, driven by consumer acceptance of premium pricing structures for products offering health-oriented benefits and environmental sustainability. This market transformation indicates fundamental shifts in consumer preferences, specifically within millennial and Generation-Z demographics who emphasize ingredient transparency and sustainability metrics.

Waterdrop's micro-drink strategic implementation exemplifies natural product positioning through its emphasis on environmental sustainability and reduced ecological impact in comparison to conventional bottled beverage alternatives. The regulatory environment for artificial ingredients continues to intensify, with increased oversight potentially advantaging natural alternatives that require less extensive regulatory documentation. The natural segment experiences substantial growth through clean label initiatives and enhanced consumer understanding of ingredient procurement processes, presenting strategic opportunities for organizations that implement transparent supply chain communication protocols.

By Sweetener Type: Sugar-Free Dominance Faces Premium Challenge

In Germany's water enhancer market, sugar-free products hold a dominant position, accounting for approximately 65.20% of the market share in 2025. This aligns with the country's shift toward healthier consumption patterns and increasing regulatory and public health pressure to reduce sugar intake across beverage categories. The adoption of artificial and non-nutritive sweeteners, including sucralose, stevia, and acesulfame-K, enables brands to meet consumer demands for flavorful, low-calorie hydration solutions. German consumers favor sugar-free formulations, prioritizing calorie reduction, weight management, and metabolic health. This preference is particularly strong among fitness-oriented and health-conscious demographics.

While sugar-free enhancers dominate the market, products containing sugar are growing at a CAGR of 13.41% through 2031. This growth indicates an emerging segment driven by demand for premium, naturally sweetened options without artificial additives. Consumers seeking clean-label products are selecting water enhancers that contain natural sweeteners such as cane sugar, honey, or fruit extracts in moderate quantities. This trend creates opportunities for brands to develop premium water enhancers that focus on organic ingredients, transparency, and minimal processing.

By Distribution Channel: Digital Commerce Disrupts Traditional Retail

Supermarkets/Hypermarkets hold a dominant 55.25% market share in 2025, benefiting from established consumer shopping patterns and opportunities for impulse purchases of water enhancers. These retail channels support product adoption through in-store demonstrations and sampling programs that encourage first-time purchases among consumers.

Online Retail Stores demonstrate substantial growth potential with a projected CAGR of 16.25% through 2031. This distribution channel facilitates direct manufacturer-to-consumer relationships and enables the implementation of data-driven subscription services and personalized product recommendations. Furthermore, e-commerce platforms serve as strategic entry points for international market expansion, allowing companies to evaluate market demand prior to establishing physical distribution infrastructure.

Geography Analysis

Germany represents a strategic market for water enhancer drops, driven by the nation's environmental consciousness and acceptance of premium products that align with sustainable hydration solutions. The country's retail infrastructure, supported by major chains including Edeka, Rewe, Aldi, and Lidl, provides comprehensive distribution coverage across urban and rural markets while maintaining competitive pricing that benefits mass-market adoption. German consumers show high sensitivity to ingredient transparency and natural formulations, creating favorable conditions for brands focusing on clean labels and organic certifications.

The market operates within strict European Union food safety regulations that enhance consumer trust in approved products and create barriers for inferior formulations. Urban concentration in major metropolitan areas, including Berlin, Munich, Hamburg, and Frankfurt, drives demand for portable hydration solutions as commuting patterns and fast-paced lifestyles increase the need for convenient products. These cities demonstrate higher disposable incomes and greater willingness to pay premiums for functional beverages, with health consciousness reaching peak levels among German regions.

Germany's aging population prioritizes wellness and preventive health measures, creating opportunities for water enhancers positioned as daily nutrition supplements rather than occasional flavor additions. Regional preferences vary, with northern regions showing greater acceptance of innovative formats like tablets and effervescent solutions, while southern areas prefer traditional liquid concentrates and natural ingredient profiles. Competition increases as international brands target Germany as a gateway to European markets, driving innovation in product formulations and sustainable packaging that meets the country's environmental standards.

Competitive Landscape

In Germany, the water enhancer drops market sees a moderate consolidation, featuring local and regional players such as The Kraft Heinz Company, Waterdrop Microdrink GmbH, BRITA SE, and BOLERO GmbH, all leveraging strong distribution networks. Meanwhile, fresh entrants are honing in on digital strategies and niche segments. Dominating the German market, Kraft Heinz leverages its Mio brand, driving continuous product innovation and tailoring offerings to local tastes.

German market entrants and international players like Waterdrop compete through sustainability initiatives and direct-to-consumer sales channels, particularly resonating with the environmentally conscious German consumer base. Waterdrop's micro-drink cubes align with Germany's strict environmental regulations and consumer preferences, emphasizing reduced plastic waste and CO2 emissions compared to bottled alternatives. Companies operating in Germany, including Stur, leverage social commerce platforms for product launches and consumer engagement, adapting to the digital-savvy German market.

The German water enhancer market presents significant opportunities in personalized nutrition and subscription services, reflecting the country's growing health consciousness and digital adoption. Companies in the German market increasingly focus on developing region-specific formulations and sustainable packaging solutions while building recurring revenue streams through online platforms. This digital transformation enables companies to gather valuable consumer data from the German market for product optimization and targeted marketing strategies.

Germany Water Enhancer Industry Leaders

-

The Kraft Heinz Company

-

Waterdrop Microdrink GmbH

-

BRITA SE

-

BOLERO GmbH

-

Holy Energy GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Liquid I.V. expanded its product portfolio by introducing a Tropical Punch flavor, which combines tangerine, pineapple, and cherry to address the increasing consumer demand for diverse flavors in hydration products.

- April 2024: Kraft Heinz rebranded its Mio water enhancer with new packaging, brand colors, and logo. The rebranding aligns with Mio's focus on offering customizable beverage options for consumers seeking functional drinks.

Germany Water Enhancer Market Report Scope

Germany water enhancer market features revenue generated through hypermarket/ supermarket, convenience store, online channel, and others

By Product Type

| Flavoured |

| Non-Flavored |

By Ingredient Source

| Natural/Organic |

| Artificial/Synthetic |

By Sweetener Type

| With Sugar |

| Without Sugar |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Pharmacy and Health Stores |

| Other Distribution Channels |

| By Product Type | Flavoured |

| Non-Flavored | |

| By Ingredient Source | Natural/Organic |

| Artificial/Synthetic | |

| By Sweetener Type | With Sugar |

| Without Sugar | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Pharmacy and Health Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the current value of the Germany water enhancer market?

The Germany water enhancer market size reached USD 147.8 million in 2026 and is projected to grow rapidly toward USD 280.8 million by 2031.

Which product type leads in Germany?

Flavored water enhancer dominated with 62.58% share in 2025, reflecting consumer appetite for taste-driven hydration options.

How fast are online sales of water enhancers growing in Germany?

Online Retail Stores are forecast to expand at a brisk 16.25% CAGR through 2031, outpacing all other channels.

Are natural ingredients gaining preference?

Yes. Natural/Organic formulations are advancing at 14.42% CAGR, faster than synthetic counterparts, as shoppers seek clean labels.

Page last updated on: