Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.45 Billion |

| Market Size (2026) | USD 3.65 Billion |

| Market Size (2031) | USD 4.84 Billion |

| Growth Rate (2026 - 2031) | 5.82% CAGR |

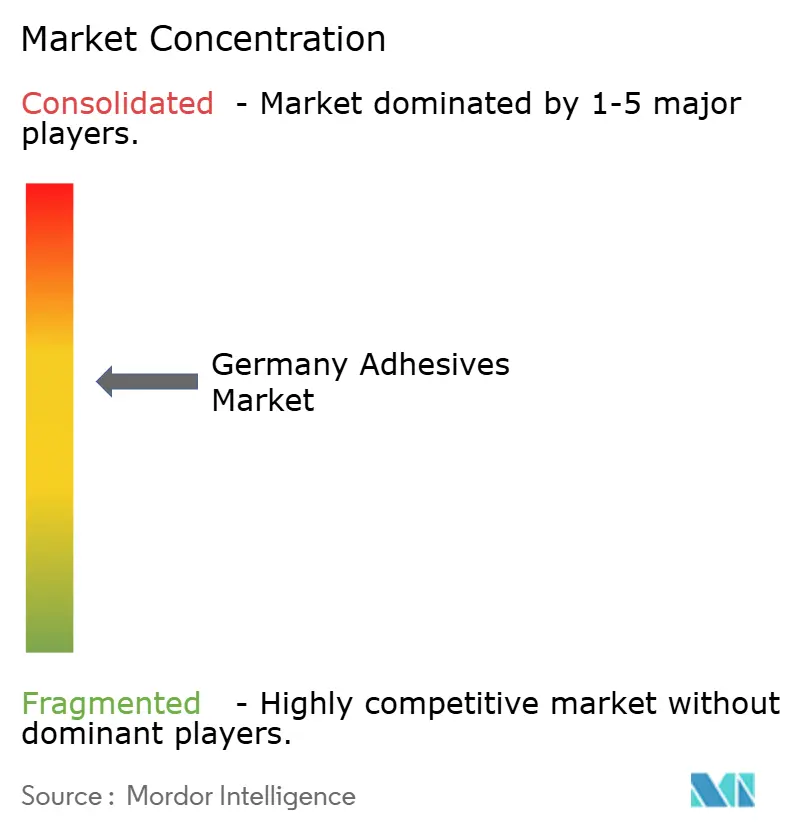

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Adhesives Market Analysis by Mordor Intelligence

The Germany Adhesives Market size is projected to grow from USD 3.45 billion in 2025 to USD 3.65 billion in 2026, and reach USD 4.84 billion by 2031, growing at a CAGR of 5.82% from 2026 to 2031. Growth stems from renovation-led construction demand, rising electric-vehicle output, and packaging reforms that oblige converters to switch to low-VOC and debondable chemistries. Domestic formulators sharpen export focus because energy prices remain two to three times U.S. levels and cumulative regulation costs approach 13% of value-added, eroding home-market margins. Water-borne technology maintains a lead on the back of EU mid-2026 VOC caps, while hot melts gain traction as automation and bio-based initiatives accelerate. Meanwhile, global players consolidate specialty niches through large acquisitions, leaving small and medium-sized enterprises (SMEs) to defend regional pockets through customization and service intensity.

Key Report Takeaways

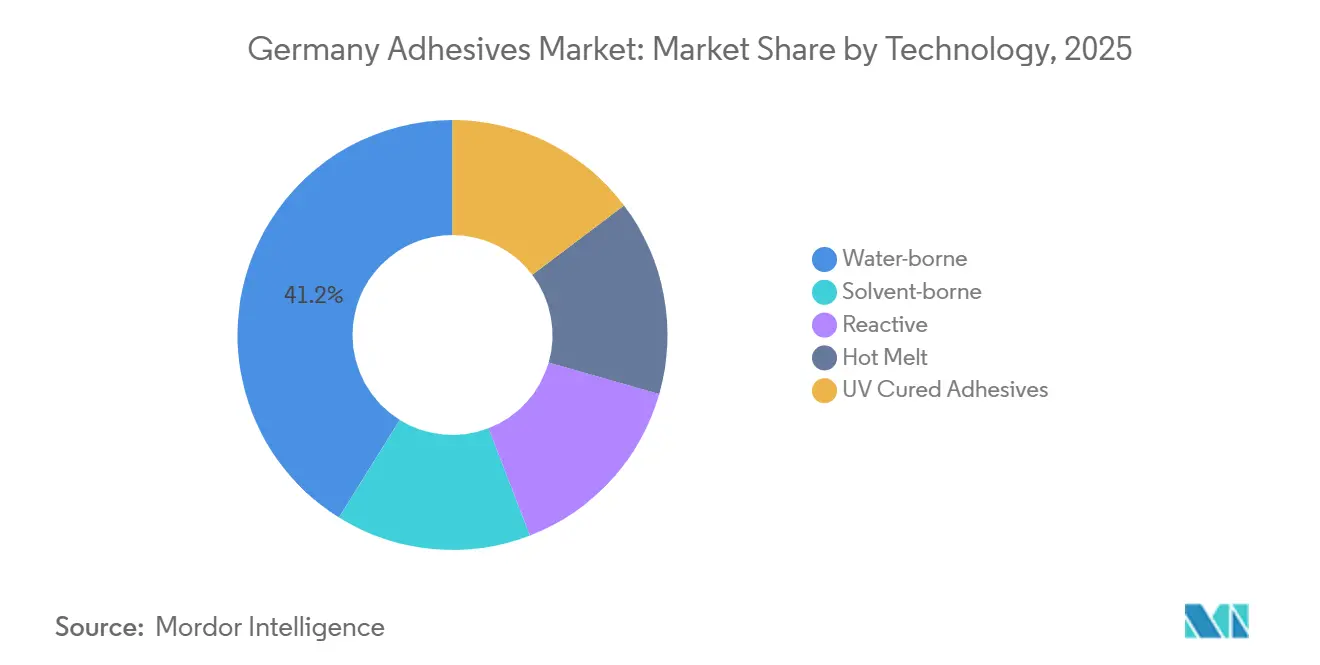

- By technology, water-borne adhesives commanded 41.15% of the Germany adhesives market share in 2025, while hot-melt adhesives are projected to grow at 6.67% CAGR through 2031.

- By resin, acrylic adhesives held 25.67% of the Germany adhesives market size in 2025, while VAE/EVA resins are forecast to expand at 6.43% CAGR through 2031.

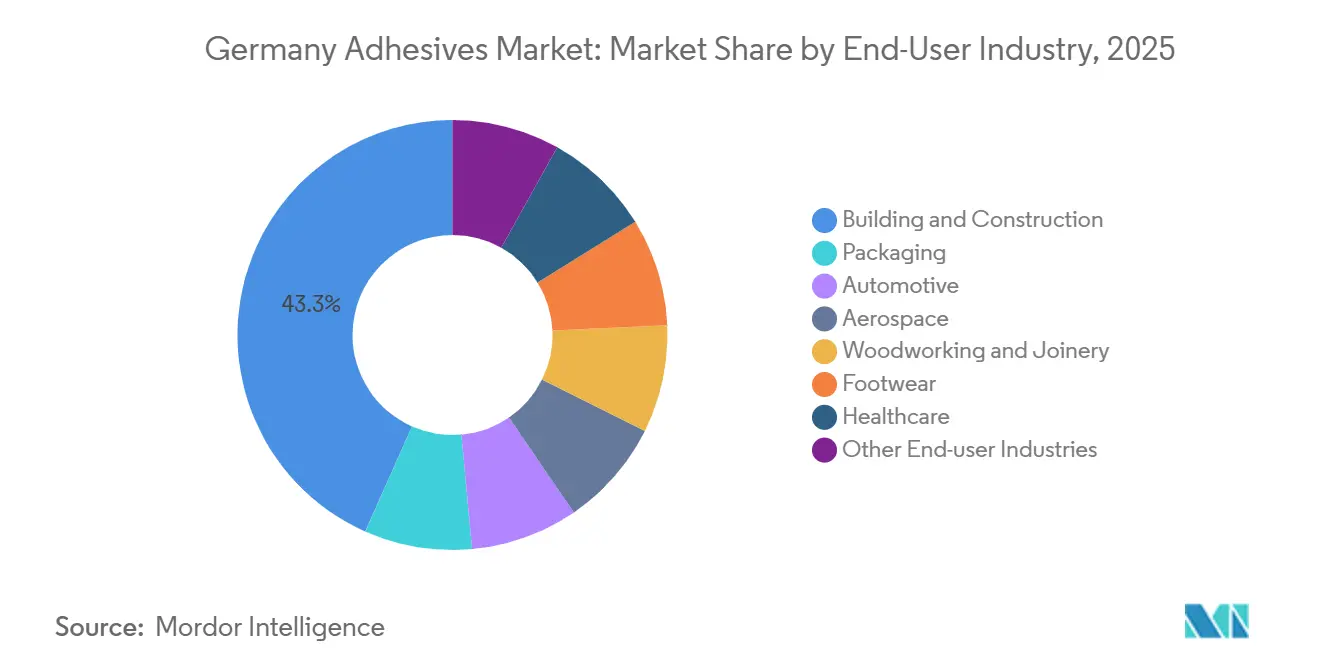

- By end-user industry, building and construction accounted for 43.35% of Germany adhesives market demand in 2025, while the automotive segment is expected to register the highest CAGR of 6.47% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction-sector renovation boom | +1.8% | Germany-wide, concentrated in urban centers (Berlin, Munich, Hamburg) | Medium term (2-4 years) |

| Shift toward flexible and recyclable packaging | +1.5% | Germany-wide, spillover to EU27 via VerpackDG harmonization | Short term (≤ 2 years) |

| Thermal-conductive adhesives for EV battery cells | +1.2% | Germany automotive clusters (Baden-Württemberg, Bavaria, Lower Saxony) | Medium term (2-4 years) |

| Bio-based adhesives backed by German Bioeconomy Strategy | +0.9% | Germany-wide, with R&D hubs in Braunschweig, Stuttgart | Long term (≥ 4 years) |

| Healthcare and medical-device bonding growth | +0.7% | Germany-wide, concentrated in medical-device manufacturing hubs (Bavaria, Baden-Württemberg, Hesse) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Construction-Sector Renovation Boom

Energy-efficiency retrofits dominate demand as pre-1990 structures require multilayer insulation, window sealing, and façade cladding to meet the federal 55% emissions-reduction target by 2030. Construction adhesives volume rose 15.4% in 2024 while wood and paper end-markets shrank, reflecting higher adhesive intensity per square meter in renovation projects. Formulations such as VINNAPAS VAE powders enable lower-clinker CEM II tile systems without sacrificing freeze–thaw durability. Project execution risk remains as skilled-labor shortages delay installations and lift costs, particularly for precision façade bonding.

Shift Toward Flexible and Recyclable Packaging

The amended Packaging Act (VerpackDG) forces 90% recyclability of plastic packs by 2029, incentivizing mono-material films and debondable adhesives to avoid extended producer responsibility penalties[1]Packaging Europe, “Germany Sets 90 % Recyclability Target,” packagingeurope.com. Water-borne and hot-melt systems are preferred for polyethylene and polypropylene structures because they remove solvent emissions and allow mechanical recycling. Henkel’s wash-off labels, launched in April 2025, preserve PET flake quality during bottle-to-bottle loops and require only six months of customer validation, accelerating market uptake.

Thermal-Conductive Adhesives for EV Battery Cells

Fast-charging EV packs create heat flux above 1,000 W/m², driving adoption of gap-filler adhesives with ≥1.5 W/mK conductivity that cure at room temperature and retain electrical isolation. Evonik’s ORTEGOL DA 801 bonds cylindrical and prismatic cells to cooling plates, aligning with gigafactory ramp-ups planned through 2028. Combined with multi-material lightweighting, structural adhesives replace welds and cut car body mass 10-15%, extending range per charge.

Bio-Based Adhesives Backed by German Bioeconomy Strategy

The EUR 6 million BioRUHM consortium develops 100% bio-based, isocyanate-free reactive hot melts that enable reversible bonding for end-of-life disassembly, targeting automotive interiors and wood-metal hybrids. VAE/EVA emulsions allow up to 50% renewable content while maintaining low-VOC profiles, supporting the federal goal of doubling bio-based material use by 2030. Certification complexity and a 10-20% cost premium remain adoption challenges.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC and REACH regulations on solvents | -1.1% | Germany and EU27, with enforcement concentrated in industrial clusters | Short term (≤ 2 years) |

| Specialty-polymer supply-chain disruptions | -0.8% | Germany, with upstream exposure to Middle East and Asia feedstocks | Short term (≤ 2 years) |

| Skilled-labor gap in precision adhesive application | -0.5% | Germany-wide, acute in automotive assembly (Baden-Württemberg, Bavaria) and construction sectors (urban centers) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC and REACH Regulations on Solvents

The EU slashed allowable VOC content to 30 g/L for interior products in 2026 and imposed workplace formaldehyde exposure limits of 0.3 ppm, forcing SMEs to spend EUR 2-5 million on reformulation and equipment upgrades[2]European Coatings, “Revised EU VOC Directive 2026,” european-coatings.com. Dual inventories during the transition squeeze working capital, while water-borne chemistries still face performance gaps in aerospace and high-temperature automotive bonding.

Specialty-Polymer Supply-Chain Disruptions

The March 2026 Strait of Hormuz crisis lifted European natural-gas futures 70% and added up to USD 4,000 per container in freight surcharges. Dow Europe passed through EUR 250/ton price increases on polyether polyols, exposing non-integrated German formulators that rely on just-in-time Asian imports. With 11 million tons of European chemical capacity shut since 2023, supply shocks have become systemic, compelling buyers to carry 60-90 days of stock and explore bio-polyol options that raise costs and tie up cash.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-Borne Dominance Amid Hot-Melt Acceleration

Water-borne systems captured 41.15% of Germany adhesives market share in 2025 on the strength of EU VOC limits that cap interior emissions at 30 g/L, steering woodworking, packaging, and construction users toward low-solvent options. Their dominance in Germany adhesives market size reflects mature production infrastructure and improved VAE copolymer performance, including less than or equal to 1 g/L VOC content and up to 50% bio input. Yet hot melts post the fastest 6.67% CAGR to 2031 as packaging lines demand instant tack, and BioRUHM’s bio-reactive grades broaden application reach beyond cartons into automotive wood-metal structures.

Solvent-borne volumes continue to shrink but retain critical roles where water uptake, slow cure, or high-temperature stability preclude aqueous systems, particularly in aerospace interiors. Reactive chemistries - epoxies, polyurethanes, cyanoacrylates - anchor aerospace composites, medical devices, and electronics, commanding premium margins because of high lap-shear strength and precise cure profiles. UV-cure and hybrid reactive hot melts blend instant handling with final cross-linking, a convergence likely to redefine category boundaries and sharpen Germany adhesives market competitiveness.

By Resin: Acrylic Leadership, VAE/EVA Fastest Growth

Acrylics led the Germany adhesives market size with 25.67% share in 2025, supplying pressure-sensitive tapes, façade sealants, and automotive display bonding where optical clarity and UV stability matter. VAE/EVA resins, however, deliver the swiftest 6.43% CAGR through 2031 because they satisfy low-VOC mandates and support up to half renewable content without major line modifications. Polyurethanes address dynamic-load joints in footwear and vehicle bodies but face growing scrutiny over isocyanate emissions, spurring development of isocyanate-free systems under the BioRUHM program.

Epoxies dominate high-temperature composite bonding in aerospace, backed by qualifications that deter new entrants. Cyanoacrylates occupy specialty medical niches requiring instant cure on small bonding areas. Silicone volumes remain niche but irreplaceable in electronics encapsulation at over 150 °C, though supply risk from Asian upstream dominance has prompted Wacker to invest in hybrid silane-terminated polymers that marry silicone flexibility with polyurethane strength.

By End-User Industry: Construction Leads, Automotive Accelerates

Building and construction drew 43.35% of Germany adhesives market demand in 2025, reflecting a renovation-heavy pipeline that uses multi-layer insulation and structural bonding to avoid thermal bridges. Water-borne high-solid powders like VINNAPAS enable low-clinker tile adhesives that trim CO₂ by 20% while weathering freeze–thaw cycles. Automotive usage records a 6.47% CAGR to 2031, propelled by EV battery assembly and multi-material bonding that trims vehicle curb weight 10-15%.

Packaging shows a split trajectory: flexible mono-material films grow under recyclability quotas, while rigid paper boards stagnate amid digitization. Aerospace and woodworking demand remains cyclical but benefits from high-value structural and bio-based innovations. Healthcare advances, such as wearable sensors and catheter assemblies, adopt biocompatible acrylic and silicone adhesives certified to ISO 10993.

Geography Analysis

Germany’s southern automotive clusters in Baden-Württemberg and Bavaria generate outsized demand for structural, thermal-conductive, and UV-curable grades, reinforcing local supply chains around Munich, Stuttgart, and Nuremberg. Northern ports of Hamburg and Bremen import bulk polyols and EVA, serving SME blenders that ship to Scandinavia and the Benelux. Eastern states leverage lower labor costs to host packaging-adhesive operations linked to Poland and Czechia end-markets. Western NRW, anchored by Düsseldorf and Cologne, remains the research and regulatory hub thanks to Henkel, Covestro, and the IVK headquarters, concentrating compliance expertise needed to navigate REACH and MDR rulemaking.

About 55% of Germany's adhesive market output is exported, with France, Poland, and Italy leading destinations for construction and packaging grades. In reverse, solvent-borne specialty imports from the U.S. and Japan supply aerospace and electronics niches where domestic capacity is limited. The energy-price gap persists despite renewables expansion, prompting firms in eastern Germany to pilot biomass and green-hydrogen boilers that can shave 15-20% off thermal-energy costs. Regional clusters now compete for federal hydrogen subsidies set to roll out in 2027, a policy likely to rebalance production footprints toward low-carbon zones.

Competitive Landscape

The Germany adhesives market is moderately consolidated. Wacker Chemie expanded hybrid-polymer output at Nünchritz in 2025, underlining its bet on silane-terminated polymers with tin-free catalysts. Sika integrates MBCC’s German assets to deepen construction-sealant offerings, while 3M pivots toward medical and electronics tapes. Competitive intensity rises as Chinese silicone giants seek downstream entry; however, aircraft, automotive, and medical validations that run 12-36 months delay their incursion. Digitization and AI-assisted formulation emerge as differentiators: Henkel reports a 25% cut in lab iterations by simulating polymer cross-link density before pilot production. Supply-chain resilience gains board-level attention; integrated players hedge feedstock risk with captive propylene-oxide or vinyl-acetate chains, whereas non-integrated SMEs build 75-day inventories, tying up working capital.

Germany Adhesives Industry Leaders

Henkel AG & Co. KGaA

Sika AG

H.B. Fuller Company

3M

Jowat SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Henkel completed the acquisition of Stahl Group, adding EUR 725 million specialty-coatings sales to its Adhesive Technologies unit.

- January 2026: Henkel purchased ATP Adhesive Systems, a German water-based tape specialist generating EUR 270 million in revenue, to boost its medical and electronics portfolio.

Germany Adhesives Market Report Scope

Adhesives are materials designed to bond surfaces together effectively, ensuring durability and resistance to separation. Various industries, including building and construction, packaging, automotive, aerospace, woodworking and joinery, footwear, healthcare, and other end-user sectors, rely on specific types of adhesives tailored to their composition and functional requirements.

The Germany adhesives market is segmented by technology, resin, and end-user industry. By technology, the market is segmented into water-borne, solvent-borne, reactive, hot melt, and UV cured adhesives. By resin, the market is segmented into polyurethane, epoxy, acrylic, cyanoacrylate, VAE/EVA, silicone, and other resins. By end-user industry, the market is segmented into building and construction, packaging, automotive, aerospace, woodworking and joinery, footwear, healthcare, and other end-user industries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Technology

| Water-borne |

| Solvent-borne |

| Reactive |

| Hot Melt |

| UV Cured Adhesives |

By Resin

| Polyurethane |

| Epoxy |

| Acrylic |

| Cyanoacrylate |

| VAE/EVA |

| Silicone |

| Other Resins |

By End-User Industry

| Building and Construction |

| Packaging |

| Automotive |

| Aerospace |

| Woodworking and Joinery |

| Footwear |

| Healthcare |

| Other End-user Industries |

| By Technology | Water-borne |

| Solvent-borne | |

| Reactive | |

| Hot Melt | |

| UV Cured Adhesives | |

| By Resin | Polyurethane |

| Epoxy | |

| Acrylic | |

| Cyanoacrylate | |

| VAE/EVA | |

| Silicone | |

| Other Resins | |

| By End-User Industry | Building and Construction |

| Packaging | |

| Automotive | |

| Aerospace | |

| Woodworking and Joinery | |

| Footwear | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the adhesives market.

- Product - All adhesive products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms