Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 14.46 Billion |

| Market Size (2026) | USD 15.05 Billion |

| Market Size (2031) | USD 18.70 Billion |

| Growth Rate (2026 - 2031) | 4.43% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain 3PL Market Analysis by Mordor Intelligence

The Spain third-party logistics (3PL) market size is expected to grow from USD 14.46 billion in 2025 to USD 15.05 billion in 2026 and is forecast to reach USD 18.70 billion by 2031 at a 4.43% CAGR over 2026-2031.

A steady rebound in the national manufacturing PMI, the mandatory shift to electronic freight documentation, and the expansion of free-trade-zone incentives all lift demand for outsourced logistics that bundles transport, warehousing, and light manufacturing services. Early adoption of hydrogen trucks and trailer-based IoT maintenance cuts operating costs and positions providers to win sustainability-linked contracts. E-commerce and temperature-controlled food exports enlarge the customer base, while duty deferment inside Barcelona, Valencia, and Algeciras zones keeps Spain on shippers’ shortlists for Iberian and North African distribution. Technology-forward operators, therefore, widen the service gap against paper-based rivals that struggle with higher cyber-insurance costs and chronic port container imbalances.

Key Report Takeaways

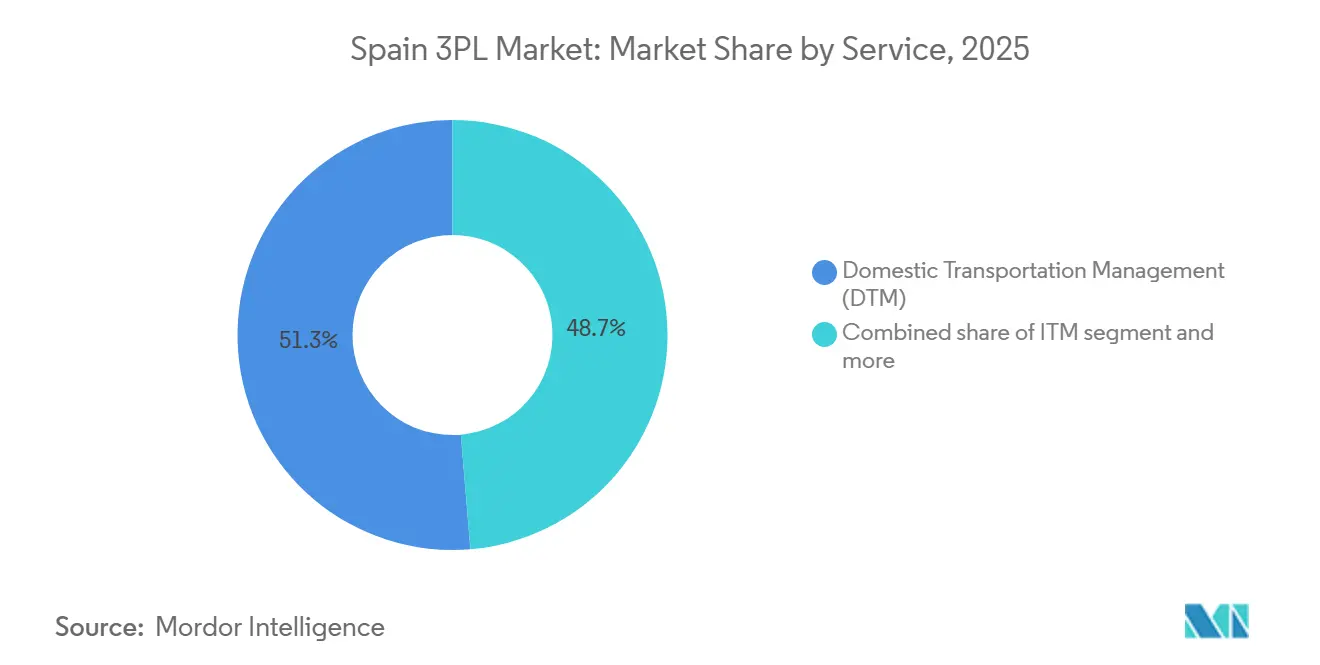

- By service type, domestic transportation management held 51.33% of the Spain third-party logistics (3PL) market share in 2025, while value-added warehousing and distribution is projected to expand at a 7.54% CAGR through 2031.

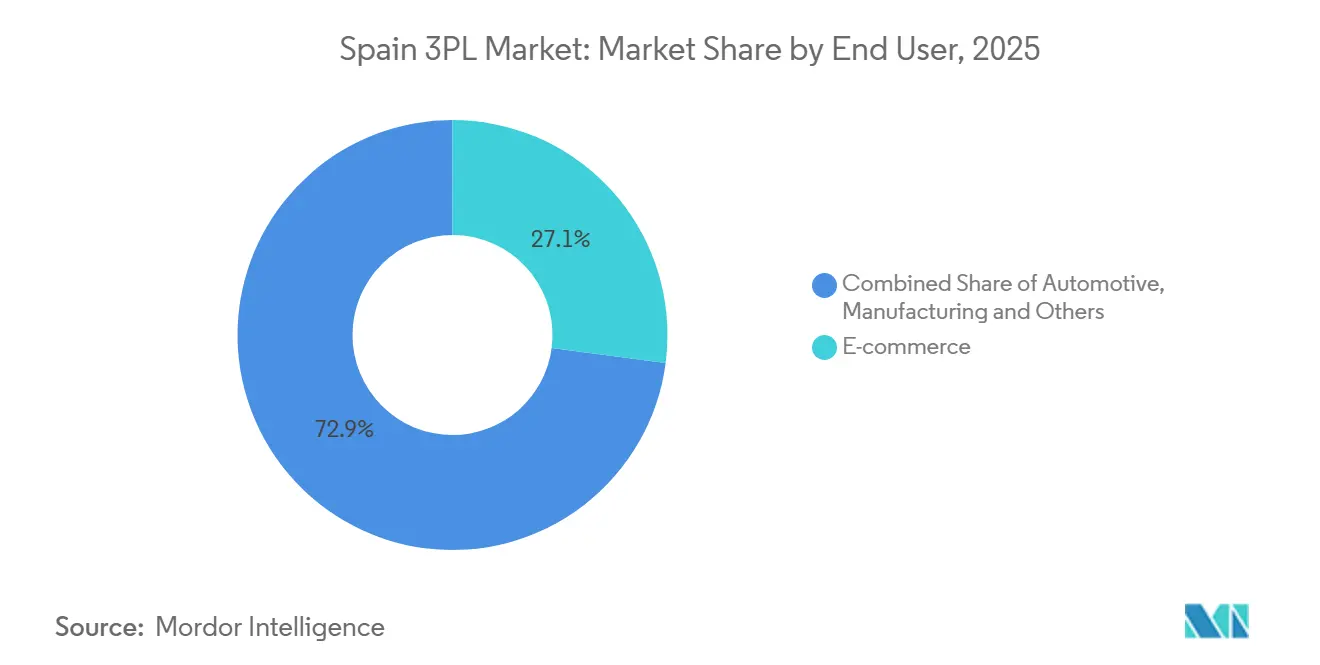

- By end-use industry, e-commerce accounted for 27.07% of the Spain third-party logistics (3PL) market size in 2025, whereas food and beverages is forecast to post a 6.25% CAGR to 2031.

- By logistics model, asset-light providers retained a 41.70% share in 2025, yet hybrid models are advancing at a 6.69% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain 3PL Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Manufacturing PMI rebound is fueling contract logistics demand | +1.1% | National, concentrated in the Basque Country, Catalonia, and Valencia | Medium term (2-4 years) |

| EU eFTI regulation pushing end-to-end digital freight data | +0.7% | National, with cross-border corridor emphasis | Short term (≤ 2 years) |

| Expansion of the Iberian free-trade zone, warehousing incentives | +0.9% | Barcelona, Valencia, Algeciras, and Vigo free-trade zones | Medium term (2-4 years) |

| Tax credits for hydrogen-truck pilots are lowering haulage costs | +0.5% | National, with priority corridors Madrid-Barcelona, Valencia-Zaragoza | Long term (≥ 4 years) |

| "Farm-to-port" consolidation hubs for Andalusian produce | +0.6% | Andalusia, Murcia, with export flows to Northern Europe | Short term (≤ 2 years) |

| IoT-enabled trailer uptime through predictive maintenance | +0.4% | National, higher adoption among large fleet operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Manufacturing PMI Rebound Fueling Contract-Logistics Demand

Spain’s PMI climbed to 50.8 in January 2025, ending a four-quarter contraction streak and signaling higher raw-material inflows and finished-goods outflows that require time-critical logistics. Industrial modernization grants worth EUR 10.6 billion (USD 12.29 billion) steer factory upgrades that embed vendor-managed inventory and postponement assembly inside 3PL warehouses close to production sites. Performance-based pricing, pegged to inventory turns rather than pallet counts, tightens operational alignment between shippers and providers. Medium-sized manufacturers lean on 3PL partners to digitize inbound visibility because in-house systems remain fragmented. As a result, the Spain 3PL market wins incremental volumes from reshoring suppliers that now treat Iberia as a European gateway.

EU eFTI Regulation Pushing End-to-End Digital Freight Data

Full enforcement of Regulation (EU) 2020/1056 in August 2025 obliges carriers to submit 106 transport documents electronically, trimming border clearance times by up to 40% on Spain-France and Spain-Portugal lanes. Compliance outlays of EUR 50,000-200,000 (USD 57,975–231,900) hit mid-tier providers, yet early adopters win new tenders from multinationals that insist on real-time milestone feeds. Interoperability rules ease blockchain pilots that auto-release freight payments once delivery events are trigger, shortening cash conversion cycles. The mandate also propels control-tower platforms that aggregate carrier data into a single customer dashboard, heightening switching costs and reinforcing market stickiness.

Expansion of Iberian Free-Trade-Zone Warehousing Incentives

Spain’s 11 free-trade zones cut working-capital needs by 15-25% via duty and VAT suspension, with Barcelona’s Zona Franca already channeling EUR 24 billion (USD 27.82 billion) in goods yearly. Valencia’s 2024 land-bank addition adds 500,000 square meters of rail-connected plots, luring pan-European retailers to position Iberian inventory closer to fast-growing Maghreb end-markets. Algeciras offers transshipment proximity to Africa, letting 3PL firms consolidate LCL flows into full containers and capture scale economies. Light industrial activities allowed inside the zones mean contract logistics now covers kitting and final labelling, giving operators a margin lift over pure storage.

Tax Credits for Hydrogen-Truck Pilots Lowering Haulage Costs

The MOVES III extension funds up to 40% of fuel-cell truck costs, slashing the EUR 300,000-400,000 (USD 347,850-463,800) price gap versus diesel and placing 50 high-capacity refueling sites on core routes by end-2025. Early pilots show total cost of ownership parity by 2028 once green hydrogen falls to EUR 3-4/kg. Providers piloting zero-emission vehicles gain preferential access to urban low-emission zones and capture sustainability-linked financing at interest savings of 50-75 bps. These economics underpin long-term contracts that lock in fleet utilization, bolstering the Spain 3PL market[1] “Low-Carbon Fuels,” repsol.com .

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Container imbalance at ports is inflating repositioning charges | -0.8% | Major container ports: Valencia, Barcelona, Algeciras | Short term (≤ 2 years) |

| Warehouse rents surging in tier-1 logistics hotspots | -0.6% | Madrid Corredor del Henares, Barcelona Zona Franca, Valencia | Medium term (2-4 years) |

| Rising cyber-insurance costs after 3PL ransomware incidents | -0.4% | National, affecting all digitized 3PL operators | Short term (≤ 2 years) |

| Scarce sustainable aviation fuel is limiting green air-cargo lanes | -0.3% | Madrid-Barajas, Barcelona-El Prat air cargo hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Container Imbalance at Ports Inflating Repositioning Charges

Valencia and Barcelona show import-export ratios above 1.3, generating up to three million empty container moves each year and pushing repositioning fees to EUR 200-400 (USD 231.90-463.80) per TEU. Terminal congestion from empties extends dwell to 8-12 days and ties up chassis capacity. Carriers levy imbalance surcharges that many shippers refuse, forcing 3PL firms to absorb the hit, a drag on Spain's 3PL market margins.

Warehouse Rents Surging in Tier-1 Logistics Hotspots

Prime rents climbed 15% year-on-year to EUR 7.50-9.00 (USD 8.70–10.44)/m² a month in Madrid and Barcelona during 2025, while Valencia vacancies dipped below 3%. Lengthy build-to-suit lead times and CPI-plus escalators squeeze providers locked into multi-year fixed-price contracts. Many seek cheaper space in Zaragoza or Tarragona, but longer trunk-haul distances offset savings, challenging the Spain 3PL market's profitability[2]CBRE, “Spain Industrial and Logistics Market Outlook 2025,” cbre.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Warehousing Complexity Drives Premium Growth

Domestic transportation management still anchors 51.33% of revenue, while value-added warehousing and distribution, reflecting a 7.54% CAGR that outpaces the overall Spain 3PL market size. Demand continues to shift from simple storage toward postponement assembly, kitting, and return-merchandise processing. Providers invest in voice-directed picking, automated sortation, and multi-temperature chambers that raise revenue per square meter. International Transportation Management benefits from 4.8 million TEU of Mediterranean transshipment flows.

Intermodal offerings that splice short-sea links with rail shorten transit by 12-18 hours compared with all-road routes, easing driver shortages and cutting emissions. Rail’s momentum accelerated after Spain and Portugal launched gauge-compatible freight services in mid-2024. Airways remains niche, reserved for pharma and electronics time-critical consignments where carriers can command premiums that lift the Spain third-party logistics market size for high-value segments[3]International Union of Railways, “Interoperable freight traffic between Spain and Portugal,” uic.org.

By End-Use Industry: Food Sector Cold Chain Sophistication

The e-commerce segment accounted for 27.07% of Spain 3PL market share in 2025, while food and beverages will post a 6.25% CAGR through 2031 as online grocery and export produce rely on GDP-compliant, temperature-controlled nodes. Spain’s EUR 28 billion (USD 32.47 billion) food export base pulls dense reefer truck demand from Andalusia farms to Northern Europe supermarkets.

Automotive volumes stabilized once vehicle output rebounded to 2.3 million units in 2024, and just-in-sequence supply calls for sub-two-hour delivery windows around assembly plants. Life Sciences demand builds on Spain’s EUR 18 billion (USD 20.87 billion) pharmaceutical manufacturing cluster, where serialization and 2-8 °C storage add service premiums. Technology and electronics distributors relocate inventory from Northern hubs to Iberia to tap shorter shipping windows into the Maghreb, spreading the Spain third-party logistics market across adjacent regions.

By Logistics Model: Hybrid Approaches Balance Flexibility and Control

Asset-light operators kept a 41.7% of Spain 3PL market share in 2025 while hybrid players mix owned strategic warehouses with outsourced haulage, achieving 6.69% CAGR and widening the Spain third-party logistics market footprint.

Asset-heavy models prevail in pharma, cold chain, and ADR cargo, where compliance and risk transfer mandate direct infrastructure control. Technology invests blur boundaries, since even asset-light providers deploy WMS and TMS suites that match asset-heavy visibility. Commercial terms grow flexible, with shippers blending models across product lines to optimize cost and service.

Geography Analysis

Madrid, Barcelona, and Valencia form an industrial triangle that concentrates 65% of national warehouse stock and trucking activity. Madrid’s central hub supports 24-hour deliveries nationwide, while Barcelona’s 3.6 million TEU port and France rail link unlock 200 million-consumer coverage within 48 hours. Valencia’s sub-3% vacancy forces longer lease tenors or spill-over development in Sagunto.

The Basque Country dominates high-value machinery and automotive exports through Bilbao, where 3PL firms bundle pre-delivery inspection with export packing. Andalusia’s cold-chain corridor moves 3.2 million tons of produce annually via Algeciras, Almería, and Huelva consolidation hubs, enlarging the Spain third-party logistics market size in perishables.

Galicia’s Vigo and A Coruna ports bridge seafood imports and vehicle exports to Latin America, while Zaragoza offers sub-EUR 6 (USD 6.96)/m² rents that attract cost-focused operators, even with two-hour longer line-hauls to consumption centers. Combined, these emerging corridors diversify the Spain third-party logistics market away from overheated tier-1 nodes.

Competitive Landscape

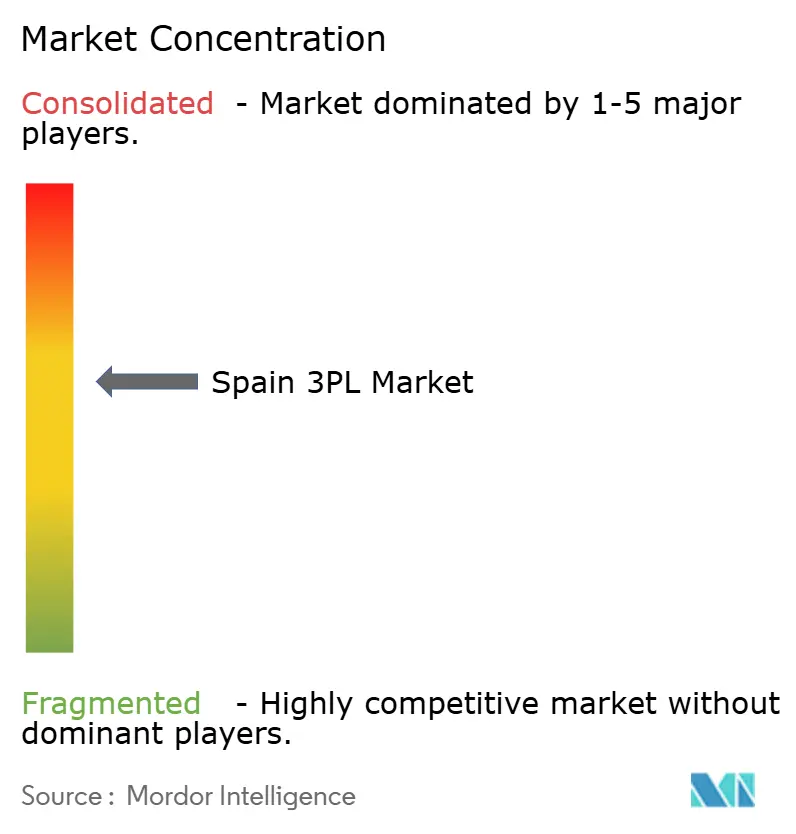

No single company commands more than 10% revenue, leaving the Spain 3PL market moderately fragmented. DHL, GEODIS, and Kuehne + Nagel leverage global networks and real-time visibility suites, while Grupo Sese and Logista employ regional know-how to serve blue-chip clients. STEF Iberia focuses on temperature-controlled chains, and Rhenus Logistics leads in automotive after-market deliveries that promise four-hour drop-offs.

Technology adoption-including autonomous mobile robots, AI route optimization that saves 8-12% fuel, and predictive ETAs, creates new competitive moats. Scale helps large fleets keep 90-95% load factors, versus 70-75% for sub-regional carriers. Sustainability now shapes tender awards, with providers offering carbon reporting and hydrogen truck pilots fetching 5-10% price uplifts.

M&A remains active: GEODIS bought PEKAES to widen East-West reach in 2024, CEVA opened a green 18,000 m² Tarragona site, and DSV sustained EBIT margins above 13% in 2024 despite soft volumes. Such moves are compressing mid-tier space and nudging the Spain third-party logistics market toward consolidation[4]GEODIS, “Acquisition of PEKAES,” geodis.com.

Spain 3PL Industry Leaders

DSV

DHL

Kuehne + Nagel

CMA CGM

XPO

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Logista lifted adjusted EBIT 5% to EUR 202 million and confirmed an M&A-driven growth path

- January 2025: Schmitz Cargobull purchased a majority stake in Atlantis Global System to deepen refrigerated-trailer IoT coverage.

- December 2024: DHL eCommerce and CTT Expresso merged Iberian parcel networks, targeting EUR 1 billion combined revenue.

- December 2024: GEODIS unveiled “Ambition 2027,” committing to fleet electrification and advanced analytics.

Spain 3PL Market Report Scope

By Service

| Domestic Transportation Management (DTM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| International Transportation Management (ITM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| Value-Added Warehousing & Distribution (VAWD) |

By End User

| Automotive |

| Energy and Utilities |

| Manufacturing |

| Life Sciences and Healthcare |

| Technology and Electronics |

| E-commerce |

| Consumer Goods and FMCG |

| Food and Beverages |

| Others |

By Logistics Model

| Asset-Light (Management-Based) |

| Asset-Heavy (Own Fleet and Warehouses) |

| Hybrid |

| By Service | Domestic Transportation Management (DTM) | Roadways |

| Railways | ||

| Airways | ||

| Waterways | ||

| International Transportation Management (ITM) | Roadways | |

| Railways | ||

| Airways | ||

| Waterways | ||

| Value-Added Warehousing & Distribution (VAWD) | ||

| By End User | Automotive | |

| Energy and Utilities | ||

| Manufacturing | ||

| Life Sciences and Healthcare | ||

| Technology and Electronics | ||

| E-commerce | ||

| Consumer Goods and FMCG | ||

| Food and Beverages | ||

| Others | ||

| By Logistics Model | Asset-Light (Management-Based) | |

| Asset-Heavy (Own Fleet and Warehouses) | ||

| Hybrid | ||

Key Questions Answered in the Report

What CAGR is forecast for Spain third-party logistics through 2031?

The market is projected to grow at a 4.43% CAGR between 2026 and 2031, driven by manufacturing rebound, e-commerce, and digitization mandates.

Which service type is expanding fastest?

Value-Added Warehousing and Distribution is set for a 7.54% CAGR as clients shift toward kitting, labeling, and returns processing.

How large is the e-commerce segment?

E-commerce generated 27.07% of 2025 revenue and benefits from roughly 800 million parcel movements each year.

What hampers green air-cargo offerings?

Spain lacks sustainable aviation fuel, with only 50,000 tons of capacity against a 2030 need of 500,000 tons, limiting carbon-neutral lanes.

Why are cyber-insurance costs rising for 3PLs?

A high-profile ransomware attack in November 2024 prompted insurers to hike premiums 30-50% and raise deductibles, lifting IT compliance spend.

Which regions outside Madrid-Barcelona are attracting logistics investment?

Zaragoza and Galicia offer lower warehouse rents and port access, while Algeciras and Andalusian hubs support fast-growing cold-chain exports.

Page last updated on: