Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

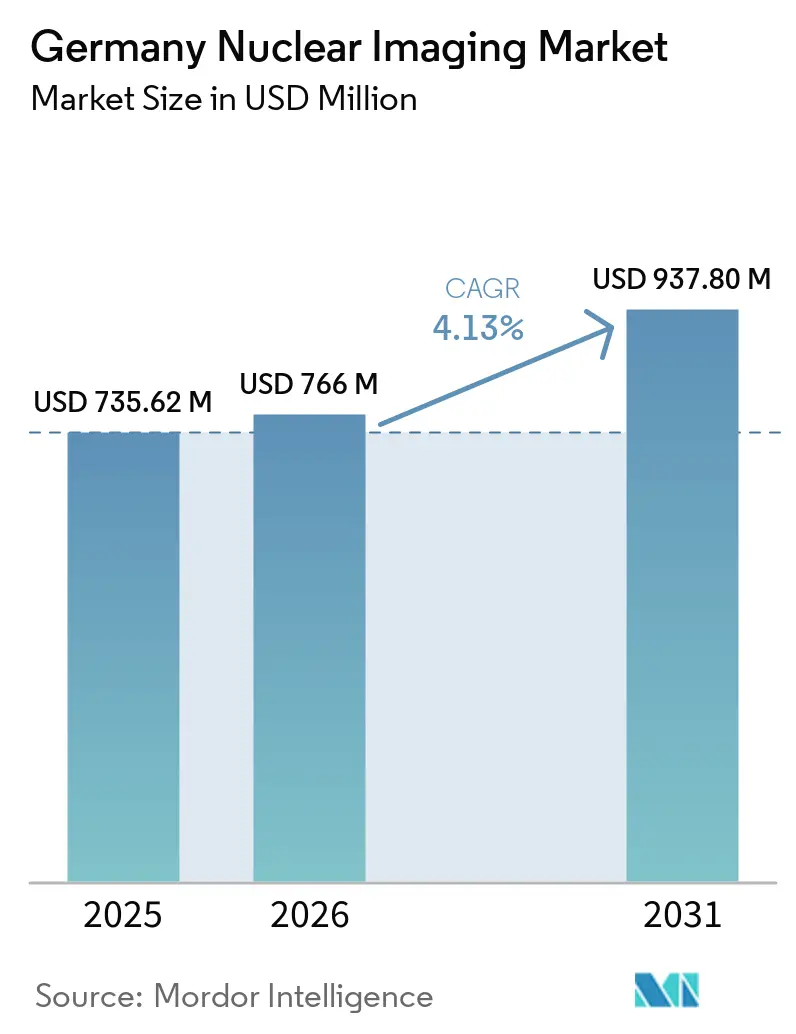

| Base Year Market Size (2025) | USD 735.62 Million |

| Market Size (2026) | USD 766 Million |

| Market Size (2031) | USD 937.80 Million |

| Growth Rate (2026 - 2031) | 4.13% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Nuclear Imaging Market Analysis by Mordor Intelligence

The Germany Nuclear Imaging Market size was valued at USD 735.62 million in 2025 and is estimated to grow from USD 766 million in 2026 to reach USD 937.80 million by 2031, at a CAGR of 4.13% during the forecast period (2026-2031).

Structural change is underway as theranostic workflows intertwine diagnostic scans with radionuclide therapy, boosting repeat PET volumes, especially for prostate and neuroendocrine tumors. Federal capital-equipment grants are refreshing hospital fleets with digital PET/CT systems that cut radiation dose by up to 40% while lifting sensitivity by 1.6 times. Parallel expansion of on-site cyclotrons is improving gallium-68 and fluorine-18 tracer availability, reducing downtime caused by reactor or generator interruptions. The Germany nuclear imaging market is also benefitting from total-body PET roll-outs paired with AI workflow tools that double patient throughput and justify premium pricing.

Key Report Takeaways

- By application, oncology led with 61.52% revenue share of the Germany nuclear imaging market in 2025, while it is projected to expand at a 5.12% CAGR through 2031.

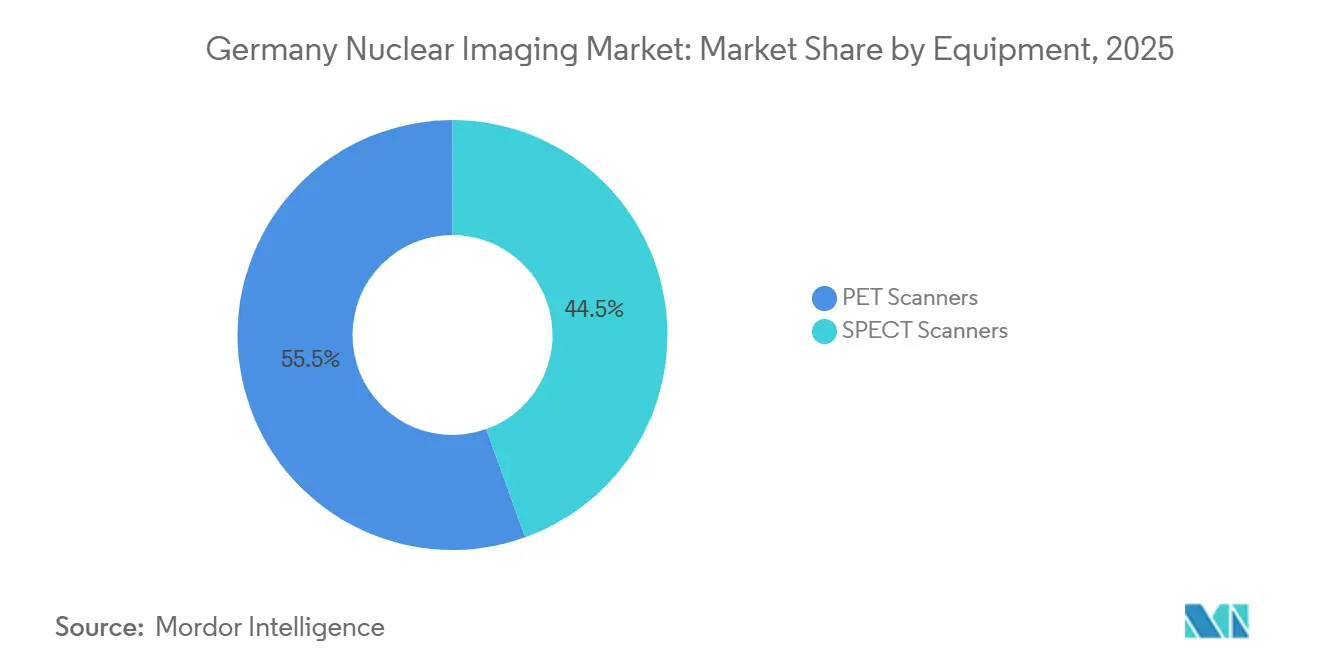

- By equipment type, PET scanners accounted for 55.55% Germany nuclear imaging market share in 2025; SPECT scanners record the highest projected CAGR at 5.85% through 2031.

- By modality, PET/CT systems held 60.53% of the Germany nuclear imaging market size in 2025, whereas PET/MRI systems are forecast to grow at 6.75% CAGR to 2031.

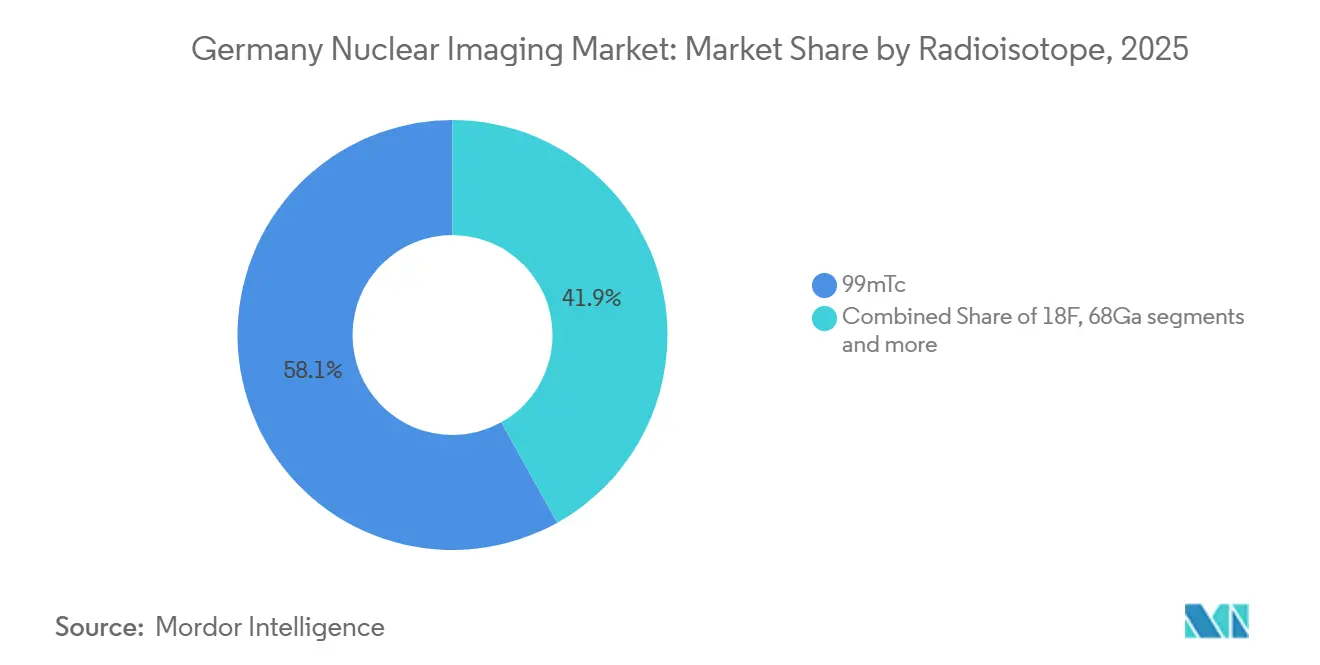

- By radio-isotope, technetium-99m commanded 58.15% share of the Germany nuclear imaging market size in 2025, but lutetium-177 is set to advance at a 5.82% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Nuclear Imaging Market Trends and Insights

Driver Impact Analysi*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cancer & CVD prevalence surge | +0.8% | National, concentrated in urban centers | Long term (≥ 4 years) |

| Federal PET/CT-CapEx grants (German Cancer Aid) | +0.6% | National, prioritizing mid-tier hospitals | Medium term (2-4 years) |

| On-site cyclotron expansions improve tracer supply | +0.5% | National, early gains in Munich, Hamburg, Berlin | Medium term (2-4 years) |

| Theranostic Lu-177-PSMA adoption boosts imaging volumes | +0.9% | National, spill-over to Austria, Switzerland | Short term (≤ 2 years) |

| Roll-out of total-body PET + AI workflow optimization | +0.7% | National, led by university hospitals | Medium term (2-4 years) |

| DRG 39301 outpatient reimbursement uplift | +0.4% | National, immediate effect on outpatient imaging centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cancer & CVD Prevalence Surge

Growing incidence of oncology and cardiac disease keeps scan volumes on an upward trajectory. Broader reimbursement for PET/MRI in neurology and cardiology is unlocking pent-up demand while technetium-99m myocardial perfusion SPECT maintains dominance for ischemia work-ups. Novel tracers such as fluorine-18-florbetaben for cardiac amyloidosis and PSMA agents for prostate cancer further widen clinical utility, underpinning sustained growth across modalities through 2031. Aging demographics ensure a continuous flow of complex cases that require follow-up imaging, embedding multiphase PET protocols into routine care. As guideline updates recommend earlier PET staging, scan frequency per patient continues to rise, reinforcing recurring revenue for equipment vendors and isotope suppliers.

Federal PET/CT-CapEx Grants (German Cancer Aid)

Targeted grants are narrowing the technology gap between university and regional hospitals. Recipients must install digital PET/CT with dose-tracking software and convene multidisciplinary tumor boards, structurally embedding PET scans into care pathways. Digital detectors deliver up to 40% dose reduction, enabling pediatric protocols while supporting higher patient throughput that improves return on investment. The grant mechanism also stipulates public reporting of utilization metrics, increasing transparency and spurring peer adoption. With Germany’s National Cancer Plan prioritizing precision oncology, additional rounds of funding are anticipated, keeping the capital pipeline flowing for the Germany nuclear imaging market.

On-Site Cyclotron Expansions Improve Tracer Supply

Compact cyclotrons such as MINItrace Magni allow hospitals to make gallium-68 and fluorine-18 onsite, insulating them from generator or reactor disruptions. Decentralized production permits evening and weekend imaging sessions, uplifting equipment utilization rates. Siemens Healthineers’ PETNET network now reaches Hamburg, Munich and Berlin, delivering tracers within 90 minutes of synthesis[1]Siemens Healthineers, “FAST PET Workflow,” siemens-healthineers.com. Reliable isotope access is especially critical for theranostics, where diagnostic gallium-68-PSMA scans and therapeutic lutetium-177-PSMA infusions must be coordinated tightly. By lowering logistical risk, cyclotrons expand viable use cases and sustain scan volumes, fortifying growth prospects for the Germany nuclear imaging market.

Theranostic Lu-177-PSMA Adoption Boosts Imaging Volumes

Each lutetium-177-PSMA therapy cycle requires baseline and post-therapy PET/CT, effectively doubling per-patient scan counts and lifting tracer demand. ITM’s 7,000 m² Munich-Neufahrn plant assures large-scale lutetium-177 supply ahead of its lead candidate’s 2026 FDA decision. Favorable cost-effectiveness studies position the therapy competitively versus systemic oncology drugs, supporting broader payer coverage. German university hospitals are already embedding theranostic boards that jointly plan imaging and therapy, institutionalizing demand. Spill-over adoption in Austria and Switzerland provides regional export potential for domestic isotope suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High equipment CAPEX & maintenance costs | -0.5% | National, acute in rural and mid-tier hospitals | Long term (≥ 4 years) |

| Tc-99m & Ga-68 supply interruptions | -0.4% | National, spill-over from European reactor outages | Short term (≤ 2 years) |

| Stricter 2024 Radiation Protection Act licensing | -0.3% | National, disproportionate burden on small clinics | Medium term (2-4 years) |

| Workforce shortage in rural nuclear-imaging sites | -0.3% | Rural regions, particularly eastern Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Equipment CAPEX & Maintenance Costs

List prices of USD 2-3.5 million for digital PET/CT and more than USD 4 million for PET/MRI strain hospital budgets, while service contracts add 8-10% of purchase value annually[2]Federal Office for Radiation Protection, “Radiation Protection Act 2024,” bfs.de. Retrofitting legacy facilities to comply with new shielding rules can exceed USD 1 million. These economics concentrate capacity at university centers and large private chains, curbing geographic penetration of the Germany nuclear imaging market. Pay-per-scan leasing offers relief yet demands guaranteed volumes that small clinics struggle to achieve.

Tc-99m & Ga-68 Supply Interruptions

Outages at aging European reactors periodically curtail technetium-99m, forcing postponement of elective SPECT studies. Cyberattacks in 2025 paused gallium-68 generator shipments, spotlighting supply fragility. Although hospital cyclotrons provide insurance, capital outlays of USD 3-5 million confine adoption to larger sites. Any protracted isotope shortfall can dampen scan volumes and temper revenue expansion in the Germany nuclear imaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment: Digital Detectors Redefine PET Economics

PET platforms delivered 55.55% of the Germany nuclear imaging market share in 2025, anchored by oncology staging and follow-up. Transitioning to digital silicon photomultipliers pushes time-of-flight resolution below 200 ps, slicing dose 30-40% without losing contrast. The Germany nuclear imaging market size for digital PET scanners is forecast to widen further as total-body models amortize faster by doubling throughput. SPECT systems currently trail yet are projected to outpace PET growth at a 5.85% CAGR through 2031 as quantitative platforms like xSPECT Quant provide dosimetry for lutetium-177 therapy.

Hybrid SPECT/CT is now the de-facto specification, displacing standalone cameras. GE’s StarGuide integrates deep-learning reconstruction that halves acquisition time while improving lesion conspicuity. Regulatory insistence on automated dose tracking tips buyer preference toward premium vendors, consolidating share among Siemens, GE and Philips. These trends pivot capital budgets toward systems that support theranostic workflows, reinforcing revenue momentum across the Germany nuclear imaging market.

By Modality: PET/MRI Gains Ground Despite Cost Premium

PET/CT dominated with 60.53% of modality revenue in 2025, yet PET/MRI is set to grow 6.75% CAGR as simultaneous anatomical-functional acquisition avoids CT dose—vital for pediatrics and neurology. Reimbursement gaps persist, but advocacy could unlock wider uptake by 2028. The Germany nuclear imaging market size attributable to PET/MRI remains modest, but expanding neurology protocols and prostate workflows indicate accelerating penetration.

Hybrid SPECT/CT maintains a stable cardiology and bone-scan niche. Rising cardiac amyloidosis awareness may reinvigorate SPECT growth via iodine-123-MIBG studies, while PET/CT challengers from Canon and United Imaging compete on price and service, appealing to regional hospitals. Survey data show 92% of new German installs since 2023 are hybrid, signaling an irreversible market shift toward multimodal scanners that future-proof clinical versatility.

By Radio-Isotope: Lutetium-177 Theranostics Drive Fastest Growth

Technetium-99m still anchored 58.15% of isotope demand in 2025, but growth lies with lutetium-177, forecast at 5.82% CAGR as gallium-68-PSMA PET/CT guides therapy. The Germany nuclear imaging market size attributable to lutetium-177 will therefore expand rapidly as university centers roll out radioligand therapy suites. Fluorine-18 holds ground through FDG but is conceding share to PSMA and DOTATATE tracers. Cyclotron-produced gallium-68 is gaining traction where generator supply proved unreliable, tightening the diagnostic-therapeutic continuum central to theranostics.

Emerging isotopes such as actinium-225 create optionality for next-generation alpha therapies. Eckert & Ziegler’s European CDMO unit can supply GMP-grade material by mid-2025. Although commercialization timelines extend beyond the forecast window, pipeline visibility supports sustained isotope-segment momentum within the Germany nuclear imaging market.

By Application: Oncology Dominates, Neurology Emerges

Oncology captured 61.52% of 2025 revenue on routine FDG-PET in lung, esophageal and head-and-neck cancers together with rising PSMA scans in prostate workflows. Serial imaging around lutetium-177 therapy amplifies follow-up volumes, lifting oncology’s share further by 2031. Neurology, although smaller, is the fastest grower outside oncology as PET/MRI proves invaluable in dementia and epilepsy focus localization. Cardiology remains steady through technetium-99m perfusion SPECT, while endocrinology gains from gallium-68-DOTATATE adoption.

These divergent growth rates illustrate how clinical breadth and reimbursement evolution shape segment revenue distribution. Sustained oncology dominance combined with neurology ascent ensures a diversified demand foundation underpinning the Germany nuclear imaging market.

Geography Analysis

Urban university hospitals in Munich, Berlin and Hamburg account for the lion’s share of equipment installs and tracer consumption thanks to consolidated theranostic programs and access to cyclotron supply nodes. Their aggregated share of the Germany nuclear imaging market size exceeded 55% in 2025 and is projected to inch higher as smaller clinics cede complex cases post-2024 Radiation Protection Act. Mid-tier regional hospitals are closing the gap through German Cancer Aid grants that fund digital PET/CT replacements, yet maintenance cost burdens could temper long-term utilization if reimbursement fails to keep pace.

Rural regions, especially in eastern Länder, lag due to physician shortages and high shielding retrofit expense[3]German Society of Nuclear Medicine, “Workforce Survey 2024,” nuklearmedizin.de . Mobile PET/CT fleets now cover some underserved areas on rotating schedules, adding incremental scan volume but only modestly lifting the Germany nuclear imaging market size because daily capacity per mobile truck remains limited. Cross-border referrals to Austrian or Czech centers are observed for specialized peptide receptor radionuclide therapy when local facilities lack licensing.

Decentralized cyclotron deployment reduces isotope delivery gaps between north and south. Hamburg’s new PETNET cyclotron, operational since late 2025, has shaved average tracer transit time by 30%, supporting evening session expansion and lifting scan throughput in Schleswig-Holstein. In aggregate, geographic distribution continues to skew toward populous metropolitan corridors, yet incremental capacity gains elsewhere widen overall access, sustaining the inclusive growth profile of the Germany nuclear imaging market.

Competitive Landscape

Market concentration is moderate; Siemens Healthineers, GE Healthcare and Philips together control a significant installed base of hybrid scanners. Siemens leverages domestic manufacturing and service density, retaining leadership in system sales and service contracts. GE competes on digital detector performance and through PETNET’s tracer network, bundling equipment with isotope supply, while Philips differentiates via AI reconstruction inside IntelliSpace Portal.

Radiopharmaceutical suppliers are vertically integrating. ITM, Eckert & Ziegler and Curium co-locate cyclotrons at hospital sites and bundle multi-year supply with therapy support, shifting competition from one-time isotope sales toward annuity-style service revenue. Eckert & Ziegler’s new CDMO unit positions it to capture pipeline manufacturing for biotech startups, expanding beyond diagnostic supply. Software disruptors such as Hermes Medical Solutions and SurgicEye are embedding quantitative analytics and augmented reality into vendor-neutral workstations, attracting providers eager to maximize return on premium scanners.

White-space opportunities persist in rural imaging, though economics remain challenging. Mobile scanning and cloud-based AI reading may mitigate access gaps, yet capital intensity, isotope logistics and staffing hurdles still constrain footprint expansion. Overall, competitive intensity is expected to remain moderate, with alliances between equipment makers and isotope suppliers consolidating share within the Germany nuclear imaging market.

Germany Nuclear Imaging Industry Leaders

Siemens Healthineers

GE Healthcare

Philips

Curium Pharma

Eckert & Ziegler AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Siemens Healthineers folded PETNET Solutions and AdAcAp Molecular Imaging under the Siemens Healthineers brand, streamlining its radiopharmaceutical portfolio.

- June 2025: Telix Pharmaceuticals’ Illuccix (Ga-68 gozetotide) received German marketing authorization for prostate cancer lesion detection.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Germany nuclear imaging market as the annual value generated inside Germany from equipment sales and on-label diagnostic use of radiopharmaceutical tracers in positron-emission tomography (PET), single-photon emission computed tomography (SPECT), and hybrid PET/SPECT systems that deliver clinical images for oncology, cardiology, neurology, and endocrine assessments.

Scope exclusion: veterinary nuclear imaging, pre-clinical scanners, purely therapeutic radioisotopes, and any recurring service contracts are kept outside this study.

Segmentation Overview

- By Equipment

- PET Scanners

- SPECT Scanners

- By Modality

- SPECT Cameras

- PET/CT Scanners

- PET/MRI Scanners

- Hybrid SPECT/CT

- By Radio-isotope

- 99mTc

- 18F

- 68Ga

- 177Lu

- Others (64Cu, 89Zr, etc.)

- By Application

- Oncology

- Cardiology

- Neurology

- Endocrinology

- Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts supplement desk work with structured discussions involving German radiologists, hospital procurement managers, isotope distributors, and academic PET center heads across Bavaria, NRW, and Baden-Wuerttemberg. Interviews test utilization ratios, average selling prices, and upcoming capital budget intentions, letting us close information gaps and adjust preliminary desk findings.

Desk Research

Our analysts begin with public pillars such as the Federal Statistical Office hospital procedure files, German Society of Nuclear Medicine audit notes, Euratom reactor supply reports, and reimbursement tariffs disclosed by the Federal Joint Committee. Trade bodies like the European Association of Nuclear Medicine, peer-reviewed journals (e.g., European Journal of Nuclear Medicine & Molecular Imaging), and import/export generator logs accessed via Volza further refine tracer flow assumptions. Company 10-Ks collected through D&B Hoovers and news archived in Dow Jones Factiva help trace vendor revenues and installed-base refresh cycles. These references illustrate, not exhaust, the wider desk research canvas consulted.

Market-Sizing & Forecasting

We anchor totals through a top-down reconstruction of diagnostic scan volumes reported by hospitals, multiplied by tracer consumption rates and validated average tariffs, which are then checked with selective bottom-up roll-ups of major vendor equipment shipments. Key variables feeding the multivariate regression forecast include PET/CT installed base growth, technetium-99m generator imports, reimbursement tariff revisions, oncology incidence rates, and tracer ASP progression. ARIMA smoothing handles seasonality in scan counts, while missing device data are bridged through weighted extrapolation from confirmed hospital cohorts.

Data Validation & Update Cycle

Outputs face multi-layer reviews: automated anomaly flags, peer analyst cross-checks, and a senior sign-off meeting. We refresh the model every twelve months, with interim revisions triggered when major reimbursement or reactor-supply events occur, ensuring clients always receive a current baseline.

Credibility Behind Mordor's Germany Nuclear Imaging Baseline

Published estimates rarely match; divergent scopes, price bases, and refresh cadences frequently explain the spread. Mordor's disciplined filter, clinical imaging only, Germany-only revenue, and annual tariff alignment, keeps the lens tight and comparable.

Key gap drivers include some studies folding in service contracts or therapeutic isotopes, others inflating totals by applying list prices without hospital-level discounts, and a few relying on partial vendor shipment samples. Our annual refresh and dual-level validation guard against such drifts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 524.39 million (2025) | Mordor Intelligence | - |

| USD 2.5 billion (2024) | Regional Consultancy A | Bundles radiopharmaceutical sales, hybrid modality service revenues, and cross-border imaging volumes |

| USD 850 million (2024) | Trade Journal B | Counts devices only, applies inflation-adjusted list prices, omits tracer revenue and public hospital discounts |

The comparison shows that when scope is widened or price realism is ignored, numbers swing widely. Mordor's narrowly defined clinical revenue base, verified variables, and yearly update cadence produce a balanced, transparent benchmark that decision-makers can confidently rely upon.

Key Questions Answered in the Report

How fast is demand for theranostic imaging growing in Germany?

Theranostic workflows centred on gallium-68-PSMA imaging and lutetium-177-PSMA therapy are pushing oncology scan volumes at a 5.12% CAGR through 2031.

Which equipment type is expanding quickest?

Quantitative SPECT scanners lead with a 5.85% CAGR as they support personalized dosimetry for radionuclide therapy.

What limits wider adoption of PET/MRI?

A 30-40% price premium and inconsistent reimbursement outside oncology constrain PET/MRI uptake despite its radiation-sparing advantages.

How are isotope supply risks being addressed?

Hospitals are installing compact cyclotrons and suppliers are spreading production across multiple German sites to buffer technetium-99m and gallium-68 shortages.

Where are the largest unmet needs geographically?

Rural eastern regions face physician shortages and high retrofit costs, prompting deployment of mobile PET/CT units to extend access.

Page last updated on: