Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 5.82 Billion |

| Market Size (2026) | USD 6.14 Billion |

| Market Size (2031) | USD 8.06 Billion |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany In-Vitro Diagnostics Market Analysis by Mordor Intelligence

The Germany In-Vitro Diagnostics Market size is expected to grow from USD 5.82 billion in 2025 to USD 6.14 billion in 2026 and is forecast to reach USD 8.06 billion by 2031 at 5.58% CAGR over 2026-2031.

Underlying this steady headline growth is a structural shift from routine clinical chemistry to high-value molecular testing, an evolution propelled by the genomDE genome-sequencing program, the approaching May 2026 IVDR recertification deadline, and Germany’s sweeping Health Data Usage Act, which mandates nationwide interoperability of electronic patient records. Manufacturers are pruning legacy portfolios to fund IVDR-compliant innovation, while laboratories channel capital into automation and middleware that can surface clean, FHIR-formatted results to national data hubs. At the same time, statutory insurers reward preventive screening for an aging population in which 25-27% of citizens will be ≥67 years by 2038, steering demand toward diabetes, cardiovascular and oncologic panels. Together, these forces position the Germany in-vitro diagnostics market at the intersection of policy, demography, and precision-medicine technology adoption.

Key Report Takeaways

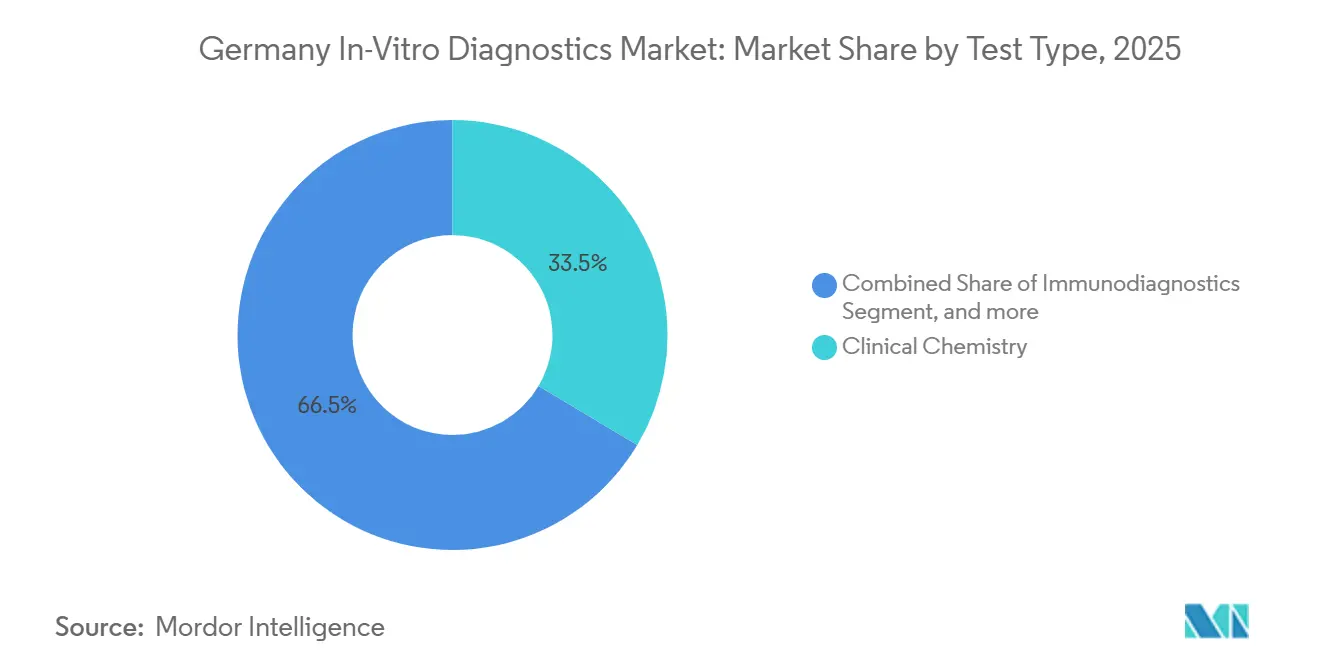

- By test type, clinical chemistry led with 33.54% of Germany in-vitro diagnostics market share in 2025, while molecular diagnostics is projected to expand at a 7.87% CAGR through 2031.

- By product & service, reagents and consumables commanded 55.65% share of the Germany in-vitro diagnostics market size in 2025, yet software and services are advancing at an 8.65% CAGR to 2031.

- By usability, disposable devices held 65.76% share in 2025, whereas reusable platforms are forecast to post a 7.99% CAGR between 2026-2031.

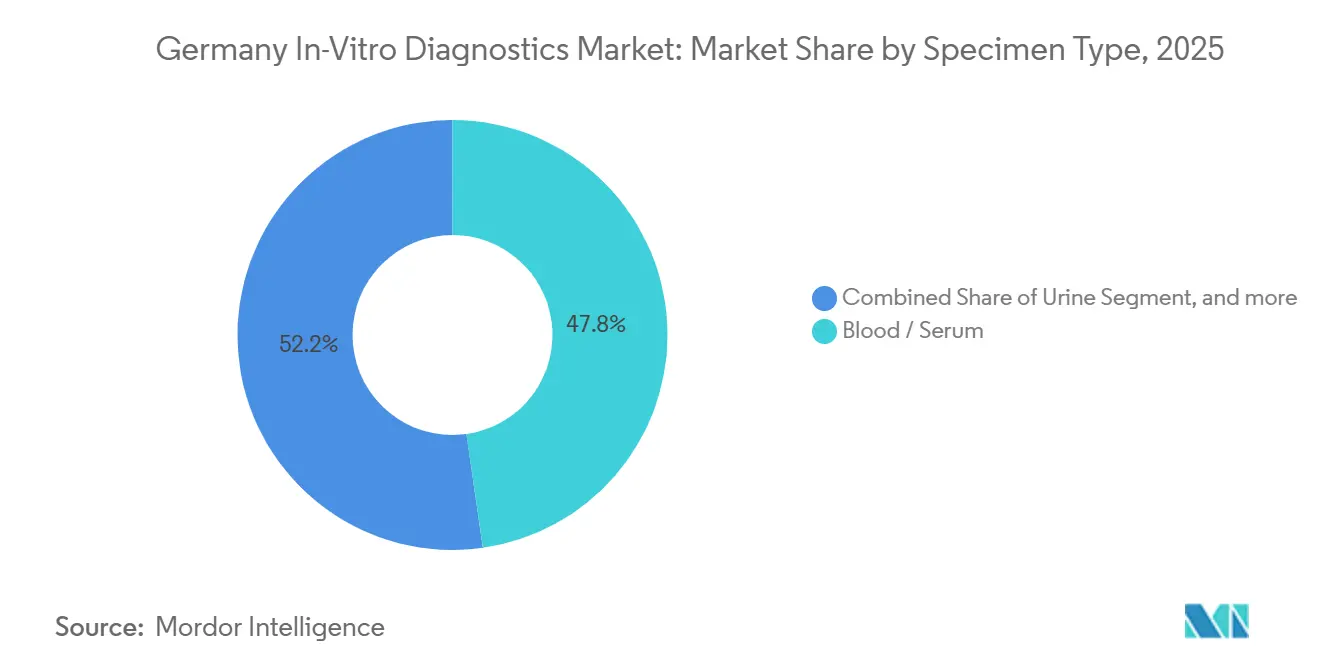

- By specimen type, blood and serum represented 47.76% of Germany in-vitro diagnostics market share in 2025, and urine-based testing is climbing at 7.54% CAGR through 2031.

- By application, infectious diseases captured 30.65% revenue share in 2025; diabetes monitoring is set to record the fastest 8.88% CAGR to 2031.

- By end user, diagnostic laboratories generated 45.32% revenue in 2025, while home-care and point-of-care centers are expanding at 8.65% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany In-Vitro Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Chronic Disease Burden | +1.2% | National, with acute pressure in aging regions (Bavaria, Baden-Württemberg) | Long term (≥ 4 years) |

| Expansion Of Precision Medicine Initiatives | +1.5% | National, concentrated in university hospital networks (Berlin, Munich, Heidelberg) | Medium term (2-4 years) |

| Government Funding For Digital Health Infrastructure | +1.0% | National, accelerated deployment in urban centers | Medium term (2-4 years) |

| Shift Toward Decentralized Testing Models | +0.9% | National, early gains in ambulatory care and rural areas | Short term (≤ 2 years) |

| Continuous Technological Advancements In IVD | +1.3% | Global, with German leadership in automation and AI integration | Long term (≥ 4 years) |

| Aging Population And Preventive Health Focus | +1.1% | National, pronounced in eastern states with higher median age | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Chronic Disease Burden

Chronic pathology anchors baseline test volumes in the Germany in-vitro diagnostics market. More than 53.7% of adults live with at least one long-term condition, including 8.4% with diabetes and 6.8% with cardiovascular disease, driving continuous demand for chemistry panels, immunoassays and glucose monitoring[1]Robert Koch Institute, “Gesundheitsberichterstattung 2025,” rki.de. Statutory insurers have widened HbA1c screening intervals under the Disease Management Program to intercept pre-diabetes early, and oncology testing is buoyed by 510,000 new cancer diagnoses recorded in 2024. Cardiovascular biomarker panels are migrating into outpatient cardiology because 2025 guidelines recommend annual troponin, BNP and D-dimer checks for citizens ≥50 years, opening a recurring preventive market.

Expansion of Precision Medicine Initiatives

The EUR 700 million genomDE pilot seeks to sequence 100,000 genomes by 2027, embedding next-generation sequencing into daily practice at 33 comprehensive cancer centers. Companion diagnostics now sit under IVDR Rule 3d, meaning clinical utility must be proven prospectively, but once certified they enjoy reimbursement certainty. Illumina’s NovaSeq X Plus has pushed whole-genome sequencing costs down to USD 200 per run, making population scale feasible. Prenatal NIPT penetration jumped to 18% of births in 2024 after blanket GKV coverage, underscoring how policy unlocks latent precision-testing demand.

Government Funding for Digital Health Infrastructure

Germany’s Health Data Usage Act makes electronic patient records mandatory for 73 million citizens by 2025, compelling every laboratory to transmit results in interoperable FHIR structure. Middleware sales therefore outpace the broader Germany in-vitro diagnostics market, growing at 8.65% CAGR as labs retrofit legacy LIS estates. The European Health Data Space extends interoperability across 27 member states, and new EBM billing codes pay physicians for algorithm-assisted remote monitoring, further monetizing digitized data streams.

Shift Toward Decentralized Testing Models

Section 64e of the Social Code Book V now reimburses point-of-care pilots, catalyzing CGM, pharmacy-based respiratory panels and mobile lab vans that travel rural districts. Abbott’s FreeStyle Libre counts 1.2 million German users; Cepheid’s GeneXpert network in 450 hospitals cuts sepsis pathogen turnaround to 90 minutes, and Bavarian Red Cross vans deliver on-site results to 200 underserved towns. These quick-response modalities capture the fastest 8.65% CAGR slice of the Germany in-vitro diagnostics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory Compliance Requirements | -1.8% | EU-wide, acute bottleneck in Germany due to notified body concentration | Short term (≤ 2 years) |

| Pricing And Reimbursement Pressures | -1.2% | National, intensifying in high-volume commodity tests | Medium term (2-4 years) |

| Supply Chain Vulnerabilities For Critical Components | -0.7% | Global, with German exposure via reagent imports from Asia | Short term (≤ 2 years) |

| Data Privacy And Security Concerns | -0.5% | National, heightened scrutiny under GDPR and IT Security Act 2.0 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Compliance Requirements

The IVDR transition forces around 25,000 legacy assays through only 35 notified bodies able to review ~8,000 files a year, leaving a backlog that drives some mid-tier suppliers from the Germany in-vitro diagnostics market. Average recertification cost per product line ranges EUR 200,000-500,000, and companion diagnostics must fund 200-patient prospective trials, extending launch timelines by up to two years. BfArM tracking shows 18% of manufacturers have already dropped at least one low-margin test, thinning choice in niche pathogen panels.

Pricing and Reimbursement Pressures

The EBM schedule trimmed reimbursement on high-volume chemistry panels by 8-12% between 2022-2024 even as reagent inflation ran 6%, compressing gross margins. G-BA health technology assessments now demand cost-utility evidence before listing novel molecular assays, a process costing up to EUR 1.5 million and adding multi-year uncertainty. Private insurers meanwhile introduce pre-authorization for tests priced above EUR 200, creating administrative drag.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Molecular Momentum Beside Clinical Chemistry Scale

Clinical chemistry underpinned 33.54% of Germany in-vitro diagnostics market share in 2025 on the back of millions of metabolic and lipid panels processed each day. Still, molecular diagnostics is clocking a brisk 7.87% CAGR from 2026-2031 as oncologists, geneticists and infectious-disease teams pivot to NGS and rapid PCR. The Germany in-vitro diagnostics market size tied to molecular assays benefits directly from the EUR 700 million genomDE pipeline and IVDR companion-diagnostic mandates that guarantee reimbursement once clinical utility is proven. Laboratories continue to run chemistry platforms for population-wide screening, but capital budgets increasingly favor sequencers and syndromic PCR stations that condense multi-day culture workflows into one-hour runs. Microbiology culture’s share erodes as 450 German hospitals rely on Cepheid GeneXpert for 90-minute sepsis panels, while immunodiagnostics hold steady with hormone, tumor-marker and autoimmune workloads.

Automated hematology analyzers such as Sysmex XN-Series embed AI morphology modules, reducing manual slide reviews and elevating hematology to a higher-margin, insight-driven service line. Point-of-care rapid tests that flourished during the pandemic are now repurposed for flu and streptococcus screening in community pharmacies. Over the next five years, genomDE feeder projects at 38 university hospitals will lift germline and somatic variant testing penetration, locking molecular diagnostics into double-digit revenue share by the end of the forecast horizon.

By Product & Service: Digital Layers Outpace Reagent Core

Reagents and consumables generated 55.65% of Germany in-vitro diagnostics market size in 2025 because every assay cycle demands single-use chemicals and cartridges. Yet software and services revenue rides an 8.65% CAGR through 2031 as laboratories rush to install middleware that converts legacy LIS outputs into IVDR-mandated FHIR messages. Germany’s Health Data Usage Act, European Health Data Space linkage and real-time upload to EUDAMED all hinge on this digital layer. The Germany in-vitro diagnostics market share for instruments is under cyclical lift as labs replace aging analyzers with IVDR-validated platforms like Roche cobas 8000 or Siemens Atellica, which integrate QC automation to satisfy stricter post-market surveillance.

Service lines diversify beyond maintenance into regulatory consulting, with midsize manufacturers outsourcing technical documentation writing for EUR 80,000-150,000 per SKU. Near-shoring of reagent production strengthens continuity; Thermo Fisher’s Freiburg expansion will reduce Asian dependency, and Siemens’ AI process manager cuts waste 15%. Together, these investments ensure reagent dominance persists, even as digital revenues compound from a smaller base.

By Usability: High-Throughput Reusables Climb

Disposable cartridges, strips and lateral-flow cassettes held 65.76% revenue in 2025, meeting consumer demand for easy home and pharmacy testing. Still, reusable high-throughput analyzers are forecast to grow 7.99% CAGR because hospitals deploy large systems to offset workforce shortages and to log every QC event for IVDR compliance. The Germany in-vitro diagnostics market size addition from reusable analyzers is amplified by greener purchasing rules that favor lower plastic consumption within the German Hospital Federation’s Green Lab Initiative.

Abbott’s FreeStyle Libre proves disposables’ continued pull—1.2 million active diabetic users in Q3 2024 alone—yet laboratories processing >500 specimens daily achieve cost-per-test parity only with reusable cobas or DxH series analyzers. Vendors therefore design modular layouts where shared reagent packs can run thousands of cycles before disposal, reducing hazardous-waste bills and aligning with sustainability targets.

By Specimen Type: Blood Rules, Urine Rises for CKD Watch

Blood and serum samples underwrote 47.76% of Germany in-vitro diagnostics market share in 2025, indispensable for chemistry, immunoassay, hematology and molecular workflows. Urine testing is, however, the fastest climber with 7.54% CAGR as quarterly albumin-creatinine ratio monitoring becomes compulsory for 2 million diabetics at risk of chronic kidney disease. The Germany in-vitro diagnostics market size linked to ctDNA rises too, as liquid-biopsy assays secure reimbursement for lung and colorectal cancers.

Saliva now serves rapid respiratory panels and oral HIV screens; Euroimmun’s saliva-IgA celiac test entered German labs in 2024. Tissue biopsies remain critical for complex oncology profiling although liquid biopsy trims invasive procedures. Blood screening remains regulated tightly by Paul-Ehrlich-Institut NAT testing for every donation, ensuring safety while adding steady NAT kit demand.

By Application: Diabetes Surges Beyond Infection Normalization

Infectious diseases remained the largest slice at 30.65% in 2025, but COVID-volume retrenchment flattens growth. Diabetes monitoring posts an 8.88% CAGR to 2031, buoyed by CGM reimbursement for all insulin-treated Type 2 patients. This pivot positions diabetes as the pre-eminent growth engine inside the Germany in-vitro diagnostics market. Oncology gains from liquid biopsy adoption; Roche’s FoundationOne Liquid CDx now reimbursed for NSCLC illustrates payers’ appetite for minimally invasive monitoring that fits value-based frameworks. Cardiology panels hold steady on aging demographics, and autoimmune multiplex assays shorten diagnostic journeys for lupus or Sjögren’s patients. Prenatal NIPT acceptance expands as blanket coverage makes trisomy screening routine.

By End User: Labs Consolidate While POC Networks Bloom

Diagnostic laboratories generated 45.32% of 2025 revenue, yet their growth lags that of home-care and point-of-care centers, which accelerated at a 8.65% CAGR. Synlab’s 120-site network processed 180 million tests in 2024, leveraging AI to keep staffing flat, proving that scale is the core route to lab survival. Contrastingly, pharmacies, GP clinics and mobile vans now capture patients who favor on-site answers within minutes. The Germany in-vitro diagnostics market size attached to hospitals shows hybrid behavior: high-acuity assays stay in-house, routine panels outsource to mega-labs. Academic centers drive frontier NGS research, funded by genomDE grants, and their in-house lab-developed tests maintain discovery agility under IVDR’s LDT carve-out.

Geography Analysis

Germany accounts for almost 30% of total European IVD revenue thanks to its 84 million population, EUR 474 billion in health spending, and a dense laboratory grid[2]. The Germany in-vitro diagnostics market size therefore dwarfs peers such as France and Italy, and its forward CAGR of 5.58% edges above their 4.8-5.2% trajectories. Precision-medicine leadership flows from Berlin and Munich university-hospital corridors where genomDE funnels capital and talent. Bavaria and Baden-Württemberg outpace national averages in liquid biopsy and CGM adoption, reflecting higher disposable income and private clinic density. Eastern Länder struggle with clinician shortages; hence, mobile diagnostic units and tele-connected point-of-care hubs are most impactful there.

Urban hubs—Berlin, Hamburg, Frankfurt—benefit from 95% household high-speed internet coverage, making cloud-LIS, AI triage, and home-monitoring integration seamless. Cross-border care is rising because the European Health Data Space gives 449 million EU residents digital access to German lab results; ISO 15189 upgrades and multilingual reports thus become export enablers for German reference labs. Germany also hosts eight of Europe’s 35 IVDR notified bodies, cementing its role as certification hub; foreign manufacturers often enter the Germany in-vitro diagnostics market first to navigate audits on local turf before rolling out EU-wide.

Surrounding markets react: Scandinavian countries push point-of-care adoption, Southern Europe remains price-sensitive toward clinical chemistry, while Eastern Europe imports German automation expertise. Collectively, this reinforces Germany as trendsetter whose policy moves—data sharing, reimbursement, regulatory rigor—set de facto standards for continental diagnostics practice.

Competitive Landscape

The Germany in-vitro diagnostics market exhibits moderate concentration: the top five suppliers—Roche, Siemens Healthineers, Abbott, Danaher and Qiagen—hold about 55-60% revenue. Roche dominates chemistry and immunoassay through the cobas ecosystem; Siemens leads workflow automation with high-throughput Atellica lines; Abbott commands CGM with FreeStyle Libre; Danaher’s Beckman Coulter plus Cepheid blanket hematology and syndromic PCR; Qiagen steps up with QIAstat molecular panels. Mid-tier brands—bioMérieux, Thermo Fisher, BD, Werfen—specialize in infectious-disease syndromic panels, life-of-patient coagulation, and niche reagent franchises.

IVDR recertification has become a competitive wedge: well-capitalized multinationals shoulder EUR-million documentation bills more readily than small firms, allowing them to consolidate share as niche rivals exit. Synlab and Limbach illustrate a parallel service-provider land grab; scaling to 180 million tests enables Synlab to negotiate reagent discounts and invest EUR 40 million in AI interpretation to offset staffing gaps. Technology road-maps converge on digital adjacency: Roche’s Navify cloud trims tumor board turnaround by half; Siemens’ AI process manager prunes reagent waste; Illumina’s NovaSeq X slashes WGS cost 60%, enabling insurer-funded screening.

Acquisition remains key: Danaher’s USD 5.7 billion Abcam deal arms it with 200,000 antibodies; Thermo Fisher buys upstream peptide producers to buffer supply. Competitive intensity also plays out in home-care where Abbott pushes Libre 3 Plus into pump integration, while Roche and Ascensia chase with G7 and Eversense respectively. Overall, the Germany in-vitro diagnostics market rewards scale, digital fluency and regulatory foresight.

Germany In-Vitro Diagnostics Industry Leaders

Qiagen N.V.

Abbott Laboratories

Roche Diagnostics

bioMerieux SA

Becton Dickinson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Biotech start-up Amplifold, based in Martinsried, Germany, completed an oversubscribed EUR 5 million seed financing round to support the market launch of its highly sensitive lateral flow diagnostics. The start-up combines DNA origami nanotechnology with cost-effective lateral flow assays (LFAs).

- January 2025: Medix Biochemica, one of the global leaders in the supply of critical raw materials for the in vitro diagnostics (IVD) industry, acquired CANDOR Bioscience GmbH, a Germany-based developer and manufacturer of premium immunoassay solutions.

Germany In-Vitro Diagnostics Market Report Scope

As per the scope of this report, the in-vitro diagnostics market includes medical devices and consumables that are utilized to perform in vitro tests on various biological samples. They are used to diagnose various medical conditions, such as diabetes, cancer, and other diseases.

The Germany In-Vitro Diagnostics Market is Segmented by Test Type (Clinical Chemistry, Immunodiagnostics, Molecular Diagnostics, Hematology, Microbiology & Lateral Flow, Coagulation, Point-Of-Care Tests, and Other Tests), Product & Service (Reagents & Consumables, Instruments/Analyzers, and Software & Services), Usability (Disposable IVD Devices and Reusable IVD Devices), Specimen Type (Blood/Serum, Urine, Saliva, Tissue/Biopsy, and Other Specimen Types), Application (Infectious Diseases, Diabetes, Cancer/Oncology, Cardiology, Autoimmune Disorders, Nephrology & Renal Panels, Prenatal/Genetic Screening, Blood Screening, and Other Applications), and End User (Academic & Research Institutes, Diagnostic Laboratories, Home-Care/POC Centers, Hospitals & Clinics, and Other End Users). The report offers the value (in USD) for the above segments.

By Test Type

| Clinical Chemistry |

| Immunodiagnostics |

| Molecular Diagnostics |

| Hematology |

| Microbiology & Lateral Flow |

| Coagulation |

| Point-Of-Care (Rapid) Tests |

| Other Tests |

By Product & Service

| Reagents & Consumables |

| Instruments / Analyzers |

| Software & Services |

By Usability

| Disposable IVD Devices |

| Reusable IVD Devices |

By Specimen Type

| Blood / Serum |

| Urine |

| Saliva |

| Tissue / Biopsy |

| Other Specimen Types |

By Application

| Infectious Diseases |

| Diabetes |

| Cancer / Oncology |

| Cardiology |

| Autoimmune Disorders |

| Nephrology & Renal Panels |

| Prenatal / Genetic Screening |

| Blood Screening |

| Other Applications |

By End User

| Academic & Research Institutes |

| Diagnostic Laboratories |

| Home-Care / POC Centers |

| Hospitals & Clinics |

| Other End Users |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Test Type | Clinical Chemistry |

| Immunodiagnostics | |

| Molecular Diagnostics | |

| Hematology | |

| Microbiology & Lateral Flow | |

| Coagulation | |

| Point-Of-Care (Rapid) Tests | |

| Other Tests | |

| By Product & Service | Reagents & Consumables |

| Instruments / Analyzers | |

| Software & Services | |

| By Usability | Disposable IVD Devices |

| Reusable IVD Devices | |

| By Specimen Type | Blood / Serum |

| Urine | |

| Saliva | |

| Tissue / Biopsy | |

| Other Specimen Types | |

| By Application | Infectious Diseases |

| Diabetes | |

| Cancer / Oncology | |

| Cardiology | |

| Autoimmune Disorders | |

| Nephrology & Renal Panels | |

| Prenatal / Genetic Screening | |

| Blood Screening | |

| Other Applications | |

| By End User | Academic & Research Institutes |

| Diagnostic Laboratories | |

| Home-Care / POC Centers | |

| Hospitals & Clinics | |

| Other End Users | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Germany in-vitro diagnostics market by 2031?

It is forecast to reach USD 8.06 billion, expanding at a 5.58% CAGR from 2026-2031.

Which segment is growing fastest within German IVD?

Molecular diagnostics leads with a 7.87% CAGR, fueled by the genomDE sequencing program and IVDR companion-diagnostic rules.

How are German reimbursement policies influencing home-care testing?

Section 64e of the Social Code Book V reimburses decentralized pilots, driving 8.65% CAGR for home-care and point-of-care centers.

Why are software revenues rising in German laboratories?

Mandatory FHIR data exchange under the Health Data Usage Act and IVDR post-market surveillance needs push software and services at 8.65% CAGR.

What impact will IVDR have on market supply?

High compliance costs and limited notified-body capacity may remove low-margin assays, but larger players able to certify early can gain share.

Page last updated on: