Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

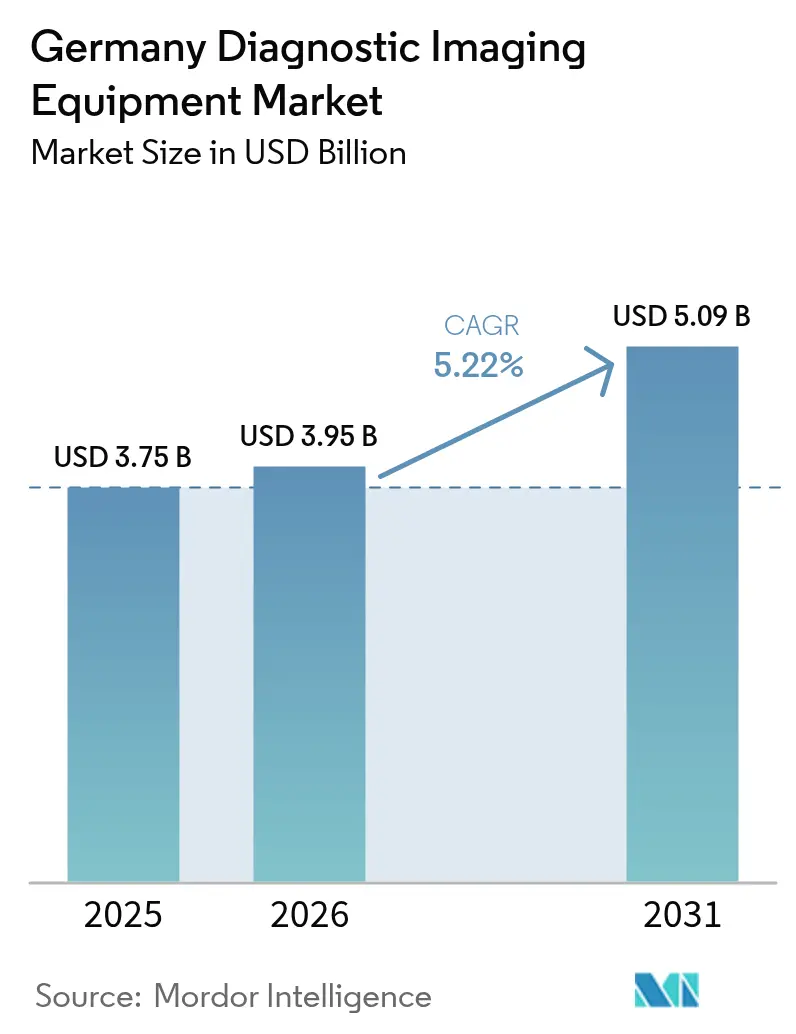

| Base Year Market Size (2025) | USD 3.75 Billion |

| Market Size (2026) | USD 3.95 Billion |

| Market Size (2031) | USD 5.09 Billion |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Diagnostic Imaging Equipment Market Analysis by Mordor Intelligence

The Germany diagnostic imaging equipment market size was valued at USD 3.75 billion in 2025 and estimated to grow from USD 3.95 billion in 2026 to reach USD 5.09 billion by 2031, at a CAGR of 5.22% during the forecast period (2026-2031). Growth builds on Germany’s position as Europe’s largest healthcare economy. Technology adoption accelerates because 1,874 hospitals now connect radiology equipment to new data backbones, while artificial-intelligence (AI) software offsets persistent radiologist shortages. Demographic pressure magnifies demand: Germany’s population aged 65 and older continues to rise, pushing oncology and cardiology screening volumes higher and supporting steady equipment replacement cycles. Consolidation among private imaging chains and hospital capacity reductions intensify competition, yet regulatory barriers created by the Medical Device Regulation (MDR) reward vendors that maintain robust quality processes.

Key Report Takeaways

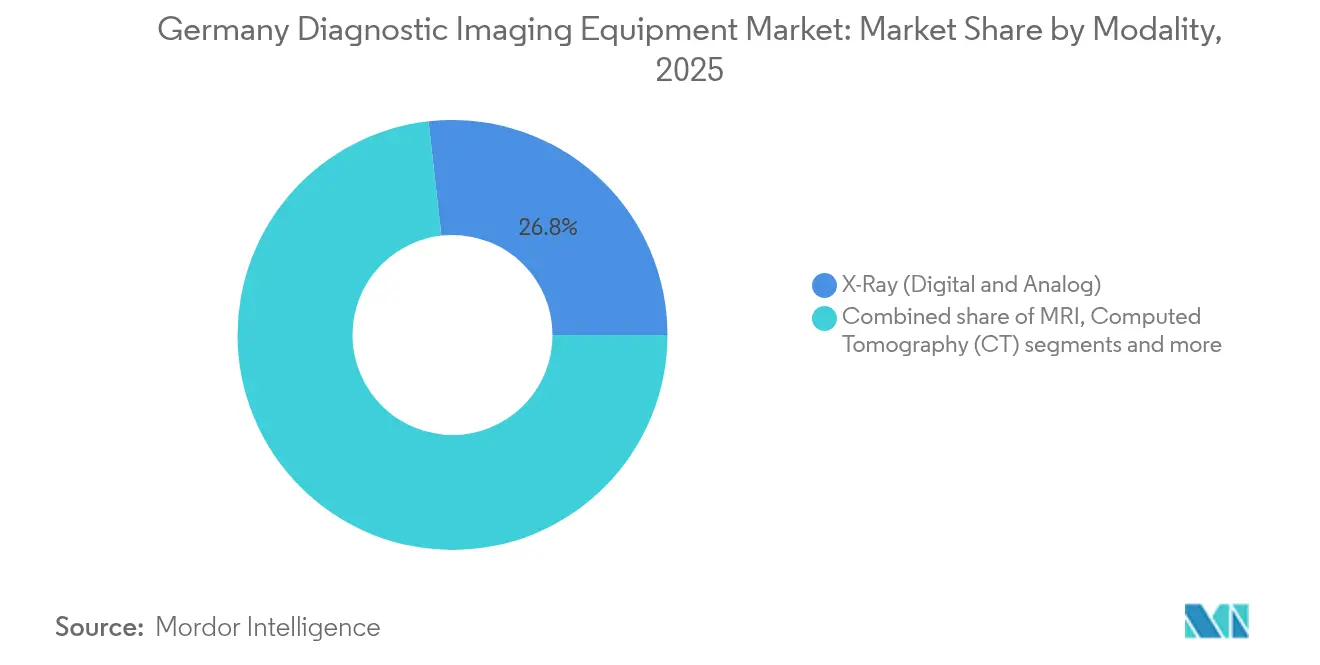

- By modality, X-Ray systems led with 26.78% of Germany's diagnostic imaging equipment market share in 2025, while MRI is projected to grow at a 6.18% CAGR to 2031.

- By 2025, fixed systems accounted for 79.65% of the German diagnostic imaging equipment market size, whereas mobile and handheld platforms are expected to advance at a 6.55% CAGR through 2031.

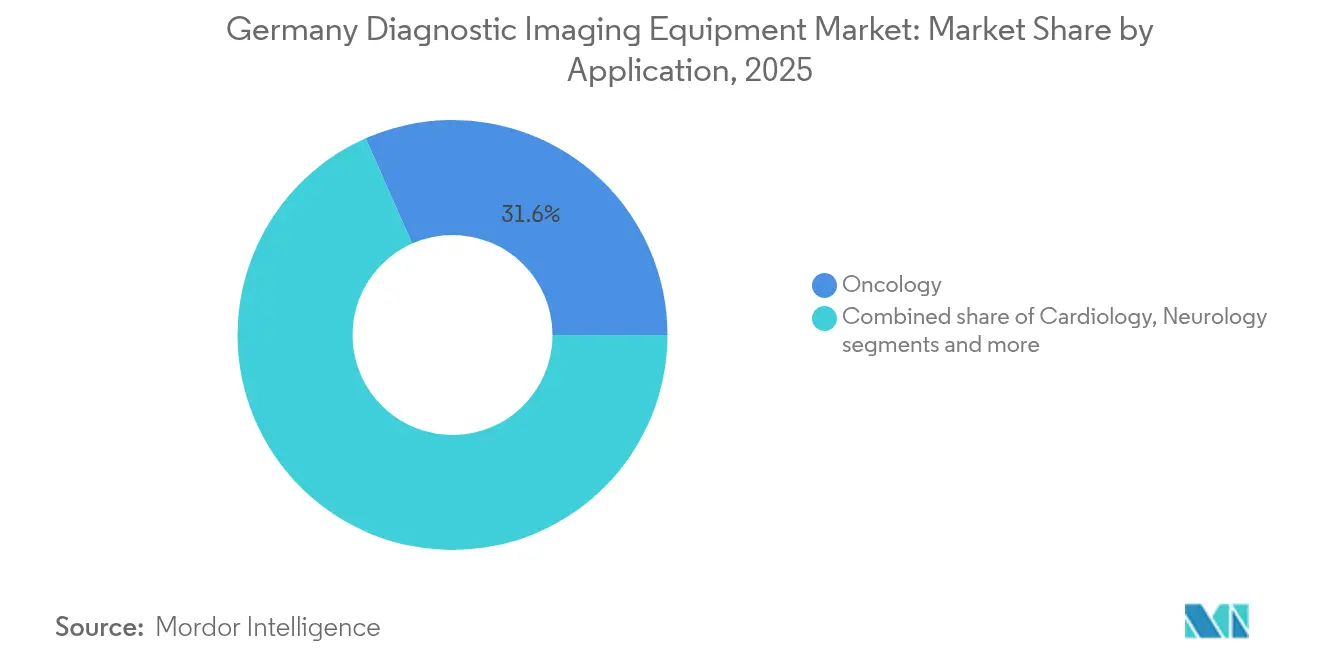

- By application, oncology captured 31.62% of the revenue in 2025; cardiology is poised for the fastest growth, with a 6.78% CAGR between 2026 and 2031.

- By end user, hospitals maintained a 65.08% share of the German diagnostic imaging equipment market in 2025, but diagnostic imaging centers are expected to expand at a 6.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Diagnostic Imaging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of chronic diseases | +1.2% | National, concentrated in urban centers | Long term (≥ 4 years) |

| Increased adoption of advanced technologies | +1.8% | National, led by university hospitals | Medium term (2-4 years) |

| Rapidly ageing population demanding early diagnosis | +1.1% | National, acute in rural areas | Long term (≥ 4 years) |

| Government grants for rural teleradiology roll-out | +0.7% | Rural regions, eastern states priority | Short term (≤ 2 years) |

| Private-equity consolidation of imaging centres | +0.4% | Metropolitan areas, outpatient facilities | Medium term (2-4 years) |

| Expansion of national cancer-screening programs | +0.6% | National, focus on mammography networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing burden of chronic diseases

Rising prevalence of cancer, diabetes, and cardiovascular disease secures long-run imaging demand across the market. Cervical cancer illustrates the dynamic: 4,666 new diagnoses appear annually, and HPV-16/18 infections account for 76.5% of invasive tumors, making precise screening indispensable. National mammography sensitivity between 69.9% and 71.7% underscores the need for AI-enabled enhancement that improves lesion detection and reduces false-negatives. Chronic-disease care pathways now rely on longitudinal imaging, securing recurring equipment upgrades. Hospitals and outpatient centers therefore consider imaging hardware as revenue-protective infrastructure rather than discretionary capital, reinforcing steady orders even during broader economic volatility

Increased adoption of advanced technologies

The EUR 4 billion Hospital Future Fund accelerates digital infrastructure purchases that integrate AI, interoperability, and cloud architectures. DigitalRadar benchmarking of 1,624 hospitals revealed a mean digitization score of 33.3/100, exposing significant upgrade headroom. Philips’ HealthSuite cloud imaging platform and NEXUS/CHILI’s distribution pact with deepc confirm that scalable AI pipelines now influence procurement. Institutions adopt advanced modalities not merely for image quality but for seamless data exchange with electronic patient records mandated by the 2024 Digital-Gesetz.[1]Source: Bundesministerium für Gesundheit, “Digital-Gesetz (DigiG),” bundesgesundheitsministerium.de

Rapidly ageing population demanding early diagnosis

Germany’s nursing-workforce requirement is projected to rise 33% by 2049, signaling broader strain on diagnostic throughput. Physicians exhibit 79.2% positive attitudes toward teleradiology, yet 80.4% record limited usage, evidencing implementation hurdles rather than acceptance gaps. Preventive screening drives imaging volumes before symptom onset, demanding high-resolution modalities that reveal subtle lesions. Such demographic resilience shields equipment sales from cyclical hospital budget constraints and continues to underpin the Germany Diagnostic Imaging Equipment market.

Government grants for rural teleradiology roll-out

Federal policy removes teleradiology quantity caps and provides flat-rate reimbursement for digital services, boosting installation rates in underserved eastern states. Nearly 59.5% of referring physicians identify teleradiology as the pivotal lever for rural access, incentivizing vendors to offer portable CT and hand-held ultrasound solutions that travel between sites. Early projects demonstrate network effects: once initial gateways are in place, additional centers prefer equipment compatible with the established data backbone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Radiation-dose concerns & stricter regulation | -0.8% | National, enforced by BfS | Short term (≤ 2 years) |

| High equipment cost & reimbursement gaps | -1.1% | National, acute in smaller facilities | Medium term (2-4 years) |

| Radiologist shortage causing under-utilisation | -0.7% | National, severe in rural areas | Long term (≥ 4 years) |

| Data-privacy hurdles hindering large-scale AI training & image sharing | -0.5% | EU-wide, GDPR compliance focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Radiation-dose concerns & stricter regulation

Germany’s Strahlenschutzverordnung enforces annual dose limits that require justification and optimization for every examination, pushing providers toward premium scanners with automated dose-tracking. Siemens Healthineers’ photon-counting CT illustrates how vendors differentiate through low-dose performance while preserving diagnostic fidelity. Compliance adds cost and operational complexity, especially for facilities without integrated informatics, and may reduce examination frequency for low-value indications.

High equipment cost & reimbursement gaps

Germany’s shift from per-case funding toward guaranteed income models by 2029 clouds return-on-investment calculations for capital purchases. The Hilfsmittelverzeichnis forces manufacturers to demonstrate both quality and price competitiveness before a scanner receives insurance coverage, favoring incumbents with established dossiers. Smaller clinics therefore postpone upgrades, dampening adoption curves despite clear clinical need.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: MRI momentum challenges X-Ray dominance

X-Ray retained 26.78% of Germany Diagnostic Imaging Equipment market share in 2025 because every hospital relies on radiography for trauma and routine chest studies. MRI, however, is boosting volumes in cardiac and neuro applications, and its 6.18% CAGR positions it as the primary growth engine through 2031. Siemens Healthineers expands its Magnetom Flow platform in the popular 1.5 Tesla segment, adding AI-enabled workflow automation that cuts exam times and broadens referral indications. PET/SPECT resurrection through theranostics further diversifies modality mix as GE Healthcare builds a dedicated center in Germany.

The Germany Diagnostic Imaging Equipment market now values modalities not only for image clarity but for how they integrate with electronic patient records and AI decision support. Ultrasound adoption benefits from hand-held devices that bring imaging to emergency rooms and rural clinics, while mammography modernizes through digital detectors and computer-aided detection that lift program sensitivity. Overall, modality portfolios continue to split between high-throughput X-Ray rooms that secure baseline service levels and premium MRI suites that capture incremental reimbursement, sustaining balanced capital investment profiles across provider types.

By Portability: mobile systems mitigate staffing gaps

Fixed systems commanded 79.65% of the Germany Diagnostic Imaging Equipment market size in 2025 because large institutions still favor room-based CTs and MRIs for throughput efficiency. Nonetheless, mobile and hand-held systems post a 6.55% CAGR as workforce shortages make point-of-care diagnostics attractive. Siemens Healthineers’ SOMATOM On.site CT allows intensive-care imaging without patient transport and provides remote control options that save technologist time.

Hand-held ultrasound units embedded with AI now generate automated measurements and share results directly to cloud archives, aligning with Germany’s digital-health reimbursement framework for telematics infrastructure. Portable scanners complement rather than cannibalize fixed installations, revealing a dual-track procurement trend where hospitals purchase both categories to match case-mix variability.

By Application: Cardiology overtakes Oncology in growth speed

Oncology captured 31.62% of revenue in 2025 underpinned by national screening programs for breast, colorectal, and prostate cancer. Cardiology is set to outpace with a 6.78% CAGR as guidelines recommend earlier coronary assessment for patients with metabolic syndrome and as AI-enhanced cardiac MRI protocols slash scan times. Germany Diagnostic Imaging Equipment market size in cardiology is therefore projected to expand predictably, attracting vendor R&D toward myocardial tissue characterization and post-processing automation.

Neurology expands through stroke triage networks supported by the EUR 26.9 million UMBRELLA project, which installs AI algorithms for real-time decision support. Orthopedics and obstetrics present steady volumes, while gastro-urology gains from hybrid imaging that combines diagnosis and minimally invasive treatment. Application diversification secures utilisation across hospital departments, spreading revenue risk.

By End User: Outpatient centers accelerate

Hospitals held 65.08% of the Germany Diagnostic Imaging Equipment market size in 2025 because they remain the gatekeeper for high-complexity procedures. Diagnostic imaging centers, however, record a 6.24% CAGR as outpatient reimbursement models reward same-day service and as private equity finances chain consolidation. Evidia exemplifies this expansion: formed via merger of MRH and Blikk, it manages over 100 locations and 1,800 staff.

Ambulatory surgery centers adopt in-house imaging to streamline patient journeys, while specialty clinics such as orthopedics invest in 3-D scanners that feed surgical-planning software. The Germany Diagnostic Imaging Equipment market therefore splits along care-setting lines. Hospitals concentrate on high-acuity cases that demand advanced CT and MRI, whereas outpatient hubs seek versatile, lower-footprint units that maximize patient flow at lower cost.

Geography Analysis

Germany hosts 1,874 hospitals with 476,924 beds and a 71.2% occupancy rate, ensuring a broad installed base for vendors. Nordrhein-Westfalen leads with 328 hospitals and 112,610 beds, making it the single largest regional buyer of replacement scanners. Bavaria and Baden-Württemberg follow, supported by proximity to med-tech clusters that include Siemens Healthineers’ manufacturing hubs in Erlangen and Kemnath.

Federal policy channels KHZG funds toward rural eastern states to correct historic under-investment, catalyzing teleradiology installation grants that open new addressable demand for the Germany Diagnostic Imaging Equipment market. Rural sites often select mobile CT or compact MRI systems because space and staffing are constrained, while urban teaching hospitals deploy high-field MRI and photon-counting CT for research and tertiary care.

Cross-border care further shapes geography. Clinics in Bavaria treat Austrian patients for advanced imaging, and North Sea coastal regions serve Danish referrals, which smooths utilization peaks and influences procurement volumes. Government insistence on universal access means state health ministries co-finance mobile breast-screening buses that circulate through sparsely populated districts, reinforcing equitable distribution of imaging resources nationwide.

Competitive Landscape

The Germany Diagnostic Imaging Equipment market exhibits moderate concentration. Siemens Healthineers anchors domestic supply with EUR 60 million production expansion in Kemnath and a EUR 350 million high-energy photonics center in Forchheim, granting speed-to-market advantage for photon-counting CT and next-generation MRI.[2]Source: Siemens Healthineers, “Siemens Healthineers invests €60 million in Kemnath production location,” siemens-healthineers.com Philips secures EU MDR certificates across its imaging portfolio and scales cloud-based enterprise imaging to Europe, positioning itself to capitalize on hospitals’ digitization budgets.[3]Source: Medical Device Network, “Philips secures EU MDR certificate for imaging solution,” medicaldevice-network.com

GE Healthcare pursues theranostics differentiation and collaborates with German university centers to broaden PET tracer research, while Canon Medical focuses on AI-driven workflow tools that minimize technologist workload. Domestic mid-size firms such as Drägerwerk and Carl Zeiss Meditec supply specialized imaging peripherals and integrated operating-room solutions that complement large-vendor scanners.

Private-equity deal flow remains brisk. Duke Street acquired Agito Medical from Philips to target refurbished-equipment demand, and imaging-center platforms merge to scale procurement power. Vendors therefore tailor offerings for both premium university hospitals and cost-sensitive outpatient chains, sustaining balanced sales channels.

Germany Diagnostic Imaging Equipment Industry Leaders

Koninklijke Philips NV

Siemens Healthineers AG

FUJIFILM Holdings Corporation

Hologic Inc.

GE HealthCare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Deutsche Forschungsgemeinschaft invites proposals for multimodal Magnetic Particle Imaging instrumentation under a new Major Instrumentation Initiative.

- June 2024: Fraunhofer IBMT unveils a 256-channel ultrasound system capable of precise deep-brain stimulation for neurological disorders.

- June 2023: Exo partners with Sana Kliniken AG to deploy AI-powered hand-held ultrasound across 44 hospitals and affiliated facilities.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Germany diagnostic imaging equipment market as all new, factory-built scanners and related hardware, MRI, CT, ultrasound, X-ray (digital and analog), nuclear imaging, fluoroscopy/C-arms, and mammography, supplied to end users inside German borders for human clinical diagnosis. Accessories, maintenance contracts, software-only PACS/RIS, and imaging services are not counted.

Scope Exclusion: Refurbished systems and veterinary imaging devices remain outside the market boundary.

Segmentation Overview

- By Modality

- MRI

- Computed Tomography (CT)

- Ultrasound

- X-Ray (Digital & Analog)

- Nuclear Imaging (PET / SPECT)

- Mammography

- Fluoroscopy & C-arms

- By Portability

- Fixed Systems

- Mobile and Hand-held Systems

- By Application

- Cardiology

- Oncology

- Neurology

- Orthopaedics

- Obstetrics & Gynaecology

- Gastro-Urology

- Other Applications

- By End-User

- Hospitals

- Diagnostic Imaging Centres

- Ambulatory Surgery Centres

- Speciality Clinics & Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed radiology department heads, procurement leads at public and private hospitals, modality distributors, and health-insurance technology advisers across Bavaria, North-Rhine Westphalia, and Saxony. The conversations validated installed-base age, budget triggers under the Hospital Future Act, and practical ASP corridors, filling gaps left by desk work and grounding forecast drivers in day-to-day reality.

Desk Research

We began with publicly available fundamentals that anchor demand patterns: Destatis hospital equipment inventories, DRG modality utilization audits, Eurostat procedure volumes, and Federal Insurance (GKV) reimbursement tariffs. Trade data from German Customs clarified import traction for high-field MRI magnets, while COCIR shipment dashboards traced Europe-wide replacement cycles. Company 10-Ks, investor decks, and clinical trial registries supplied average selling price (ASP) cues. Paid lenses from D&B Hoovers and Dow Jones Factiva helped us verify revenue splits and flag outlier growth claims. These sources are illustrative; many additional databases and journals were reviewed to cross-check numbers and narrative consistency.

Market-Sizing & Forecasting

A top-down model starts from modality-level procedure counts and equipment penetration, reconstructing national demand by tying scanner life cycles to replacement propensity and new site roll-outs. Select bottom-up cross-checks, sampled supplier revenue roll-ups and ASP × unit estimates, adjust totals where reporting lags appear. Key variables include annual CT and MRI scans per 1,000 inhabitants, average scanner service life, KHZG grant disbursements, over-65 population growth, and oncology incidence rates. Multivariate regression links these drivers to historical market value, after which an ARIMA overlay projects five-year trajectories and scenario bands. Gaps in granular unit data are bridged with distributor channel checks and weighted interpolation from completed tenders.

Data Validation & Update Cycle

Outputs pass variance checks against OECD capital-equipment indicators; then a senior analyst reviews anomalies before sign-off. Reports refresh yearly, with mid-cycle updates triggered by material events such as reimbursement policy shifts or large procurement tenders. Clients receive a final pre-delivery sweep to ensure data freshness.

Why Mordor's Germany Diagnostic Imaging Baseline Commands Reliability

Published estimates often diverge because firms select differing device baskets, price bases, and refresh windows.

Key gap drivers lie in scope width, as some studies fold in AI software or imaging services, currency translation timing, and whether replacement-only or replacement plus incremental installs are counted. Mordor presents the base year as 2025 equipment revenue inside Germany, whereas others may report 2024 numbers or bundle service contracts, leading to sizable deltas.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.75 B (2025) | Mordor Intelligence | - |

| USD 1.97 B (2024) | Global Consultancy A | Excludes high-end ultrasound and mobile X-ray; uses hospital procurement lists only |

| USD 2.83 B (2025) | Global Consultancy B | Bundles refurbished units and applies regional average ASPs rather than Germany-specific prices |

| USD 8.00 B (2024) | Regional Consultancy C | Adds imaging services revenue and includes veterinary scanners |

The comparison shows that once scope and price assumptions align with actual German purchasing patterns, Mordor's disciplined, annually refreshed approach delivers a balanced, transparent baseline that decision-makers can retrace and reproduce with confidence.

Key Questions Answered in the Report

How is Germany’s shift toward value-based care influencing the feature set that hospitals demand in new imaging systems?

Providers increasingly look for scanners that embed real-time analytics and structured reporting tools because these capabilities link diagnostic performance to outcome-based reimbursement metrics.

What makes interoperability a critical purchasing criterion for German radiology departments today?

With electronic patient records now mandatory, facilities favor equipment that uses open standards such as DICOMweb and HL7 FHIR to ensure hassle-free data exchange across multi-vendor networks.

In what way are workforce shortages accelerating adoption of remote-operation technologies in imaging suites?

Platforms that enable off-site technologists to set protocols or monitor exams are gaining traction, helping hospitals keep scanners running during night shifts and in underserved regions.

Why are theranostics capabilities becoming a talking point in Germany’s nuclear-medicine segment?

Interest in personalized oncology treatments is driving demand for hybrid PET/SPECT systems that support both diagnostic imaging and targeted radionuclide therapy planning.

How do Germany’s cancer-screening program updates affect modality replacement cycles?

Expanded guidelines for breast and lung screening push facilities to upgrade to digital detectors and AI-assisted triage tools, shortening acceptable equipment lifespans.

What role does the new telematics infrastructure flat-rate reimbursement play in teleradiology investments?

Guaranteed digital-service payments give rural hospitals budget certainty, encouraging them to procure cloud-ready CT and MRI scanners that integrate smoothly with hub-and-spoke reading models.

Page last updated on: