Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

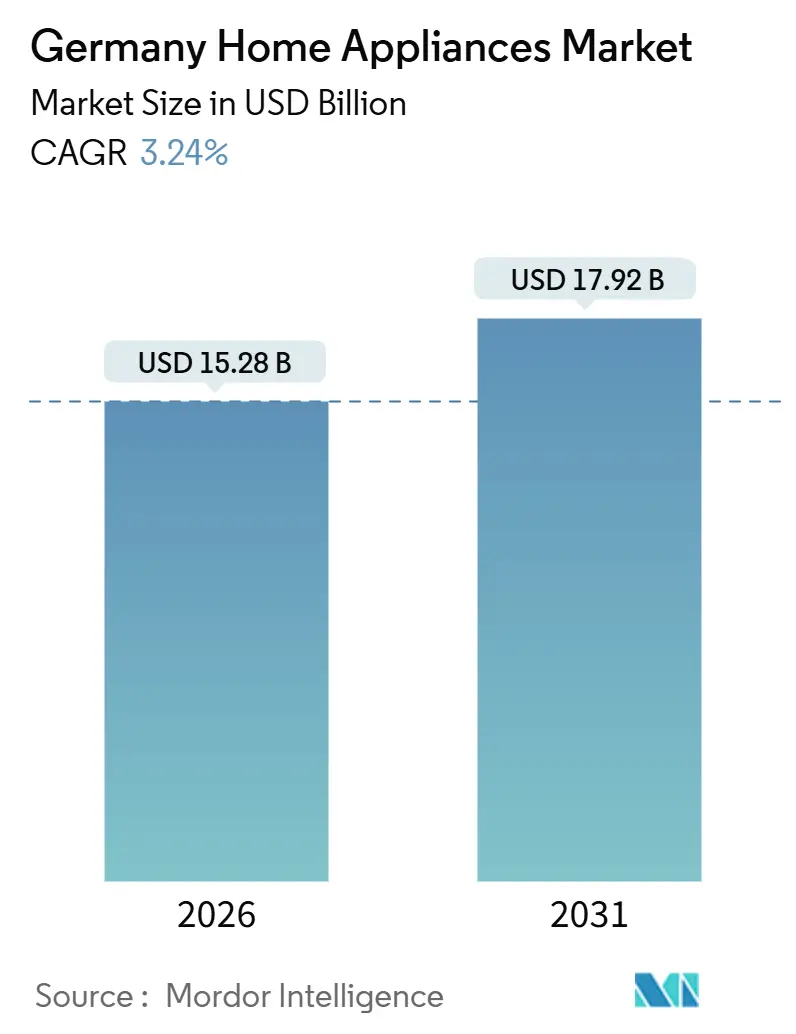

| Market Size (2026) | USD 15.28 Billion |

| Market Size (2031) | USD 17.92 Billion |

| Growth Rate (2026 - 2031) | 3.24% CAGR |

| Market Concentration | Medium |

Major Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Home Appliances Market Analysis by Mordor Intelligence

Germany home appliances market size is estimated at USD 15.28 billion in 2026, and is expected to reach USD 17.92 billion by 2031, at a CAGR of 3.24% during the forecast period (2026-2031). Growth reflects a policy-driven replacement cycle as energy-efficiency mandates reframe buying criteria and shorten upgrade timelines beyond technical failure rates. The Building Energy Act that came into effect in 2024 requires new heating systems to derive 65% of energy from renewables, which accelerates the adoption of heat pumps and adjacent efficient appliances[1]Source: Federal Ministry for Economic Affairs and Climate Action, “Building Energy Act,” BMWK, bmwk.de. The EU’s Ecodesign for Sustainable Products Regulation, in force since 2024, adds digital product passports and repairability scores to product listings, which elevates durability and serviceability alongside energy labels in consumer decisions. Omnichannel retail capabilities, next-day delivery, and click-and-collect models strengthen online conversion while preserving in-store evaluation that remains important for major appliances. The strategic focus is shifting from pure hardware benchmarks toward software features such as AI diagnostics and interoperability built on Matter, which reshape differentiation and post-sale service models[2]Source: Connectivity Standards Alliance, “Matter,” CSA-IoT, csa-iot.org.

Key Report Takeaways

- By product, major home appliances led with a 72.31% of the Germany home appliances market size in 2025, while Small Home Appliances recorded the fastest growth at a 4.93% CAGR through 2031.

- By distribution channel, multi-brand stores held 47.62% of the Germany home appliances market share in 2025, while online channels are projected to expand at a 5.85% CAGR to 2031.

- By geography, North Rhine-Westphalia accounted for 24.00% of the Germany home appliances market share in 2025, while Bavaria is forecast to grow at a 4.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Germany Home Appliances Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Smart, Connected Appliances | +0.9% | National, with early gains in Baden-Württemberg, Bavaria | Medium term (2-4 years) |

| EU and German Energy-Efficiency Regulations Driving Replacements | +1.2% | EU-wide, concentrated in North Rhine-Westphalia, Hesse | Short term (≤ 2 years) |

| Post-Pandemic Home-Upgrade Spending | +0.6% | National, spill-over to suburban Lower Saxony | Short term (≤ 2 years) |

| E-Commerce and Omnichannel Expansion | +0.8% | National, with platform density in Berlin, Hamburg, Munich | Medium term (2-4 years) |

| Federal BEG Subsidies Boosting Demand for Heat-Pump Dryers | +0.7% | National, higher uptake in Baden-Württemberg, Bavaria | Long term (≥ 4 years) |

| Subscription or Appliance-as-a-Service Models Widening Access | +0.5% | APAC core influence, spill-over to German urban cohorts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Smart, Connected Appliances

Adoption of connected appliances in Germany continues to climb as the broader smart home footprint expands and device ecosystems converge on the Matter standard. The Germany home appliances market is seeing manufacturers embed interoperable connectivity so users can coordinate brands within a single app environment and avoid proprietary gateways that constrain device choice. Smart meter deployment crossed the one million mark by September 2024, which provides real-time energy dashboards that nudge usage toward off-peak tariffs and incentivize smart-ready appliances with programmable cycles. Building code updates require smart-ready wiring in new construction, and that reduces the friction of installing connected appliances during renovations. Subsidy frameworks from KfW and BAFA reinforce this trend by funding energy management and encouraging integrated upgrades that tie appliances into home energy systems. The cumulative effect is a steady shift from basic connectivity toward AI diagnostics and automation features that drive higher average selling prices and lock-in service relationships over the product lifetime.

EU and German Energy-Efficiency Regulations Driving Replacements

The EU’s revised Energy Efficiency Directive sets higher savings obligations through 2030, which pushes member states to accelerate energy reductions and encourages households to replace functioning but inefficient appliances with A-class models[3]Source: European Commission, “Energy Efficiency Directive 2023/1791,” EUR-Lex, eur-lex.europa.eu. The Ecodesign for Sustainable Products Regulation extends sustainability criteria to durability, repairability, software updates, and digital product passports, which online marketplaces can rank and display at the point of sale. Labels and standby limits for laundry categories tighten across 2025 and 2027, and this technical pressure leads brands to redesign components that reduce idle consumption. KfW and BAFA funding covers a significant portion of A-class equipment costs within defined caps, which steers upgrades toward higher tiers when households qualify for grants. Regions with higher electricity prices and dense urban profiles show faster replacement behavior, reinforcing the distribution of demand concentration across leading states. As retailers clear pre-regulatory inventory, short-term discounting can further catalyze churn and pull forward purchases ahead of rule inflection points.

E-Commerce and Omnichannel Expansion

Online sales of consumer electronics and appliances in Germany grew in 2024, supported by platform scale, reliable logistics, and user-friendly app experiences that lift conversion rates for complex purchases. Click-and-collect has become a preferred path for many households since it lets buyers secure stock online then inspect units before finalizing the transaction. Marketplace competition has pushed faster delivery windows, value-added installation services, and better returns handling that reduce the perceived risk of buying large appliances online. Brick-and-mortar leaders counter with retail media to supplement margins and with experiential showrooms that emphasize tactile evaluation for high-ticket items. Mobile-first shopping continues to expand as app ecosystems combine product registration, warranty workflows, and subscription management in a single interface. Over time, algorithms that surface repairability, energy usage, and digital passport data will reshape product discovery in channels where search relevance dictates share of attention.

Federal BEG Subsidies Boosting Demand for Heat-Pump Dryers

Germany’s BEG program, administered by KfW with coordination from BAFA, has funded large volumes of building efficiency projects and has made whole-home retrofit stacks more attainable. The Germany home appliances market benefits when households bundle heat pump projects with complementary appliance upgrades, including heat-pump dryers that qualify for program bonuses tied to efficiency and refrigerants. The incentive architecture allows combinations of base grants and targeted adders, which encourages proactive replacement to unlock total subsidy value rather than waiting for failure events. Higher uptake in regions with larger shares of single-family homes reflects easier coordination for project approvals and metering requirements. Subsidized systems must be paired with smart metering for measurement and verification, which also accelerates the digitalization of the installed base. Manufacturers are starting to incorporate control algorithms that can qualify for future scheme criteria and support grid flexibility services.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Near-Saturation of Core Major-Appliance Ownership | -0.8% | National, pronounced in urban centers | Long term (≥ 4 years) |

| Inflation-Led Consumer Price Sensitivity | -1.1% | National, acute in lower-income eastern states | Short term (≤ 2 years) |

| High Upfront Cost of Premium Smart Appliances | -0.6% | National, dampening rural uptake | Medium term (2-4 years) |

| EU Right-to-Repair Rules Extending Replacement Cycles | -0.7% | EU-wide, impact in North Rhine-Westphalia, Hesse | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Near-Saturation of Core Major-Appliance Ownership

Penetration of refrigerators and washing machines in German households is near universal, which limits first-purchase headroom and shifts growth toward replacements and upgrades. Metropolitan areas have a high share of single-person households that favor compact formats, but unit volume expansion is constrained when new household formation slows. With replacement cycles stretching a decade or more for some categories, the German home appliances market must rely on energy-label re-ratings and subsidies to pull forward upgrades. Historic upgrade waves have matured, and the next surge is expected later in the decade as installed fleets reach the end of life. In this context, additive differentiation depends on software features and premium tiers that deliver tangible utility savings or convenience. Price competition intensifies when consumers prioritize core functionality and energy use over brand identity, which erodes pricing power for incumbents in saturated categories.

Inflation-Led Consumer Price Sensitivity

Headline inflation in Germany eased in 2025, yet consumers remain cautious, and discounting behavior in large-ticket durables remains high. Even as appliance deflation appears in some months, a larger share of buyers anchor on promotions and lower entry price points, especially in regions with lower median incomes. Online marketplaces amplify price comparisons, which can compress average selling prices and shift volumes toward value brands. Willingness to pay green premiums recedes when energy cost savings are not immediate or transparent, which requires suppliers to monetize efficiency through clearer lifetime cost messages. Embedded financing and buy-now-pay-later options can ease upfront pressure, but conversion varies by payment preference and credit access. The net effect is a consumer mix that is more bifurcated between entry and premium segments, leaving mid-tier SKUs under pressure.

Segment Analysis

By Product: Major Appliances Anchor Revenue, Air Fryers Lead Growth Sprint

In the Germany home appliances market, major home appliances led by product category, capturing 72.31% of the total market size in 2025, while small home appliances are projected to record the fastest growth, expanding at a 4.93% CAGR through 2031. With major home appliances, refrigerators led the market share in 2025, and within this category, the German home appliances market share reflects near-universal ownership and 10-year replacement cycles that link churn to evolving energy labels. Smart interoperability has gained importance as brands like Bosch deploy Matter-compatible models so consumers can integrate mixed-brand ecosystems without dedicated hubs. Air fryers are the fastest-growing small appliance segment in the small home appliances market as health-focused users reduce cooking fats and urban households embrace multifunction solutions that fit compact kitchens. Freezers cede share to flexible refrigeration formats, and ovens gain from embedded steam and air-fry modes that support better cooking results without additional countertop devices. Laundry care remains stable, though washer-dryer combos gain traction among single-person households that need space efficiency in smaller dwellings.

Dishwasher growth is supported by newer cycles that deliver faster full loads with reduced water usage, showing how incremental performance upgrades can move buyers who prioritize convenience. Air conditioning penetration continues to climb as summers warm and comfort expectations rise, which widens the Germany home appliances market for seasonal cooling devices across multifamily housing. Vacuum cleaners are split between traditional and robotic formats as households weigh the trade-off between deep cleaning and daily maintenance, while premium cordless models signal a lifestyle positioning in higher-income segments. Small appliances, including coffee makers and blenders, contribute to steady growth as wellness and convenience trends spur kitchen upgrades that favor automation. Across product lines, repairability indices and digital product passports elevate design for service and modularity, which starts to influence rankings on e-retail platforms and long-term resale value. Together, these shifts point to a portfolio balance where the German home appliances market combines reliable major appliance revenue with faster-growing small appliance segments that capture lifestyle and wellness preferences.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Multi-Brand Stores Retain Edge, Online Closes Gap Fast

Multi-brand stores captured 47.62% of 2025 sales, providing the tactile evaluation many buyers expect before committing to high-value appliances, which keeps this route central in the Germany home appliances market. Retailers invest in retail media to support price matching and protect margins on core categories, while showrooms deepen engagement through live kitchens and integrated suite demonstrations. Exclusive brand outlets hold share in urban cores by offering premium installations and fast service turnaround, leveraging higher-margin SKUs to sustain curated brand experiences. Online channels are advancing at a 5.85% CAGR through 2031 as faster delivery, installation add-ons, and stronger returns handling reduce friction for large appliance purchases. Click-and-collect covers a significant portion of online baskets since it combines inventory certainty with in-person inspection at pickup, which blends the best of both channels for consumers.

Mobile commerce now drives most digital transactions, and proprietary brand apps integrate ownership journeys, including warranty management and predictive service alerts that can upsell extended support. Micro-fulfillment hubs in populous states shorten last-mile windows and often pair delivery with white-glove installation, which builds trust and reduces post-purchase friction. Over the forecast period, search relevance on e-retail platforms will respond to energy labels, repairability indices, and digital passport data, which raises the bar for product content quality and compliance. Privacy and security compliance frameworks such as GDPR and ISO baselines remain table stakes as retailers standardize robust data handling for connected product ecosystems. Omnichannel now acts as the default posture for the Germany home appliances market, and brands that integrate consistent pricing, inventory visibility, and frictionless service across touchpoints gain structural advantage. As the Germany home appliances industry matures under these dynamics, channel partners that deliver predictable fulfillment and service speed will capture a larger share of repeat purchases.

Geography Analysis

North Rhine-Westphalia held a 24.00% market share in 2025, and this concentration highlights how urban density and logistics hubs support higher purchase volumes and faster service coverage within the Germany home appliances market. The region’s economic base supports consistent employment, which steadies demand and underpins premium kitchen upgrades in ongoing renovations. Bavaria is forecast to grow at a 4.46% CAGR through 2031 as tech-forward households adopt smart appliances earlier and integrate them with home energy systems. Smart device density in southern states also fosters cross-category automation where appliances coordinate with solar and storage for off-peak usage. Hesse contributes a notable share as financial sector employment drives shorter replacement cycles and higher penetration of connected SKUs among digital-native consumers. Berlin’s rental profile favors subscription adoption where flexible access trumps upfront ownership for mobile urban renters.

Baden-Württemberg mirrors Bavaria’s engineering-driven brand preferences and a willingness to pay for German-made quality in premium refrigeration and laundry categories. Lower Saxony skews toward value segments that respond to aggressive promotions and reliable entry models, which keeps mass-market brands well represented. State-level logistics assets in Frankfurt and Cologne enable fast cross-border fulfillment, which cements leadership for distribution and aftermarket coverage. Over the forecast, federal climate targets and the 65% renewable requirement in building systems will keep incentives flowing toward retrofit-ready states with high single-family home shares. The Germany home appliances market size will see higher retrofit linkage in southern regions as BEG program rules and smart meter integration streamline verification and energy reporting. These regional patterns reinforce a dual-speed map in which urban logistics and rural retrofit demand both contribute to sustained growth.

Competitive Landscape

Competitive intensity is rising as software-centric features displace traditional hardware-only benchmarks, and this is reshaping the Germany home appliances market. BSH Hausgeräte reported EUR 15.3 billion in 2024 revenue and allocated EUR 800 million to R&D, which is 5.2% of revenue, to embed AI diagnostics across key lines and accelerate software functionality[4]Source: BSH Group, “Company News and Reports,” BSH, bsh-group.com.

Bosch’s first Matter-compatible refrigerator presentation at CES 2025 signaled an explicit move to break down proprietary gateway lock-in and simplify mixed-brand installs. Miele responded by extending a 25-year motor guarantee in October 2025 on selected machines, which positions longevity and total cost of ownership as alternatives to near-term IoT upsells. Midea’s acquisition of Teka Group, parent of Küppersbusch, reflects a strategy to leverage heritage German brands to penetrate premium built-in channels where architect specifications carry weight.

White-space opportunities cluster in subscription access models, predictive maintenance that preempts failures, and decarbonization retrofits tied to BEG subsidy criteria. Dyson’s time-saving cordless proposition supports premium pricing across floor care, while Grover’s rental options target liquidity-constrained urban consumers who prefer flexibility over ownership. Interoperability based on Matter is a unifying platform effect as BSH, Samsung, and LG certify products for cross-brand control and a consistent experience through mainstream smart home hubs. EU-mandated digital product passports will expand into appliance categories, which increases transparency on material provenance and repairability and aligns with broader circularity goals. Over time, ISO 50001 and related energy management frameworks will influence factories and suppliers as manufacturers decarbonize production and target lower embodied carbon in appliances.

Germany Home Appliances Industry Leaders

BSH Hausgeräte GmbH

Miele & Cie. KG

Whirlpool Corporation

Electrolux AB

LG Electronics

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: BSH opened a new manufacturing facility in Cairo, following its 2024 refrigeration factory launch in Monterrey, and outlined its dual-hemisphere diversification strategy.

- April 2025: Midea Group acquired Teka Group, parent of Küppersbusch, gaining access to premium built-in channels shaped by architect specifications.

- January 2025: LG Electronics partnered with Microsoft to embed generative AI agents into home appliances for natural-language control and predictive maintenance forecasting.

- December 2024: Samsung Electronics expanded AI Home screens across Bespoke refrigerators, washers, dryers, and wall ovens and integrated natural-language control with SmartThings.

Germany Home Appliances Market Report Scope

A complete background analysis of the Germany Home Appliances Industry, which includes an assessment of the industry associations, overall economy, emerging market trends by segments, significant changes in the market dynamics, and market overview is covered in the report. The market is segmented by Major Appliances (Refrigerators, Freezers, Dishwashing Machines, Washing Machines, and Cookers & Ovens), Small Appliances (Vacuum Cleaners, Small Kitchen Appliances, Hair Clippers, Irons, Toasters, Grills & Roasters, and Hair Dryers), Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, E-Commerce and Others). The report offers market size and forecasts for Germany Home Appliances Market in value (USD Million) for all the above segments.

By Product

| Major Home Appliances | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Ovens (Incl. Combi & Microwave) | |

| Air Conditioners | |

| Other Major Home Appliances (range hoods, cooktops, etc.) | |

| Small Home Appliances | Coffee Makers |

| Food Processors | |

| Grills and Roasters | |

| Electric Kettles | |

| Juicers and Blenders | |

| Air Fryers | |

| Vacuum Cleaners | |

| Toasters | |

| Other Small Home Appliances (waffle makers, tea makers, rice cookers, etc.) |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Region

| North Rhine-Westphalia |

| Bavaria |

| Baden-Württemberg |

| Lower Saxony |

| Hesse |

| Rest of Germany |

| By Product | Major Home Appliances | Refrigerators |

| Freezers | ||

| Washing Machines | ||

| Dishwashers | ||

| Ovens (Incl. Combi & Microwave) | ||

| Air Conditioners | ||

| Other Major Home Appliances (range hoods, cooktops, etc.) | ||

| Small Home Appliances | Coffee Makers | |

| Food Processors | ||

| Grills and Roasters | ||

| Electric Kettles | ||

| Juicers and Blenders | ||

| Air Fryers | ||

| Vacuum Cleaners | ||

| Toasters | ||

| Other Small Home Appliances (waffle makers, tea makers, rice cookers, etc.) | ||

| By Distribution Channel | Multi-Brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Region | North Rhine-Westphalia | |

| Bavaria | ||

| Baden-Württemberg | ||

| Lower Saxony | ||

| Hesse | ||

| Rest of Germany | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the Germany home appliances market size and growth outlook to 2031?

The Germany home appliances market size stands at USD 15.28 billion in 2026 and is projected to reach USD 17.92 billion by 2031 at a CAGR of 3.24%.

Which product categories lead revenue and which are growing fastest in Germany?

Major Home Appliances led with a 72.31% revenue share in 2025, while Small Home Appliances recorded the fastest growth at a 4.93% CAGR through 2031.

How do regulations like ESPR and the Building Energy Act influence appliance purchases in Germany?How do regulations like ESPR and the Building Energy Act influence appliance purchases in Germany?

ESPR elevates repairability and digital product passports in online rankings, and the Building Energy Act’s 65% renewable requirement steers households toward efficient upgrades, which accelerates replacements beyond failure-driven cycles.

Which sales channels are gaining share in the Germany home appliances market?

Multi-brand stores hold the largest share, but online channels are the fastest growing at an 5.85% CAGR to 2031, reinforced by click-and-collect and fast delivery.

What are the main risks to appliance demand in Germany over the next two years?

Price sensitivity remains elevated, and Right-to-Repair rules may extend replacement cycles, both of which can delay upgrades unless balanced by subsidies and clear lifetime cost savings.