Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

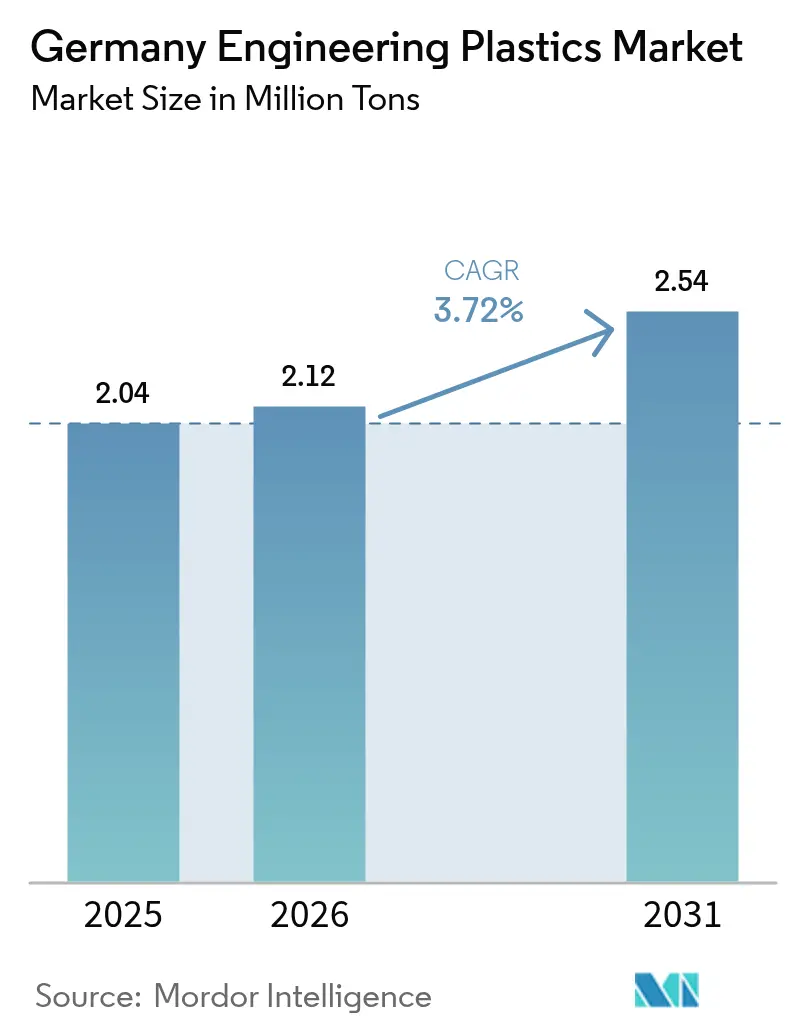

| Base Year Market Size (2025) | 2.04 Million tons |

| Market Volume (2026) | 2.12 Million tons |

| Market Volume (2031) | 2.54 Million tons |

| Growth Rate (2026 - 2031) | 3.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Engineering Plastics Market Analysis by Mordor Intelligence

The Germany Engineering Plastics Market size was valued at 2.04 million tons in 2025 and estimated to grow from 2.12 million tons in 2026 to reach 2.54 million tons by 2031, at a CAGR of 3.72% during the forecast period (2026-2031). Rising hydrogen infrastructure projects, electric vehicle lightweighting, and energy-efficient building retrofits are the principal forces that keep demand growth steady, even as the market matures. Polymer innovators are aligning their formulations with the EU Battery Regulation and Germany’s Gebäudeenergiegesetz, prompting the rapid commercial rollout of flame-retardant polyphthalamide, mass-balance polyamide, and recycled-content polycarbonate. Supply competition remains balanced: incumbents deploy vertical integration to stabilize feedstock costs while challengers pitch bio-based and circular-content grades that fetch price premiums. Feedstock volatility, linked to EU energy swings and automaker cost-down programs, has tempered price realizations but has not derailed volume expansion. Germany’s dense manufacturing clusters and its 10 GW hydrogen roadmap further underpin multi-sector polymer demand, supporting moderate yet durable market growth through 2030.

Key Report Takeaways

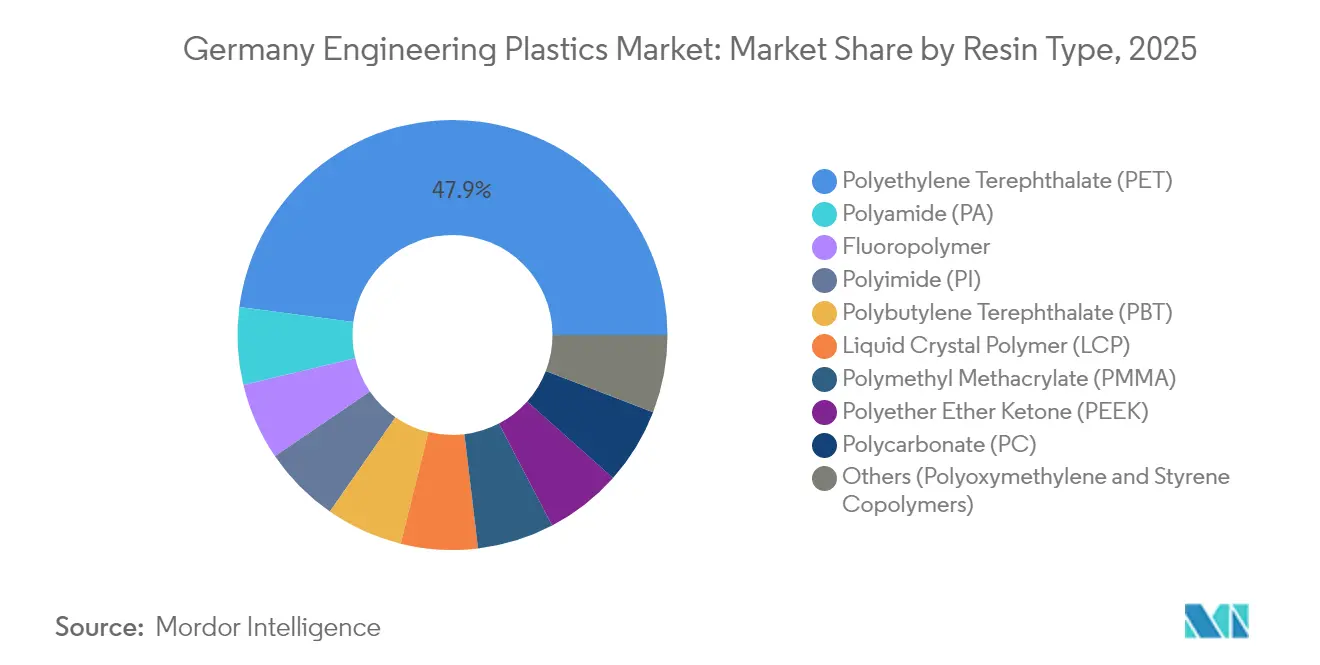

- By resin type, polyethylene terephthalate captured 47.92% of the Germany Engineering Plastics market share in 2025. Styrene copolymers are projected to advance at a 4.01% CAGR through 2031.

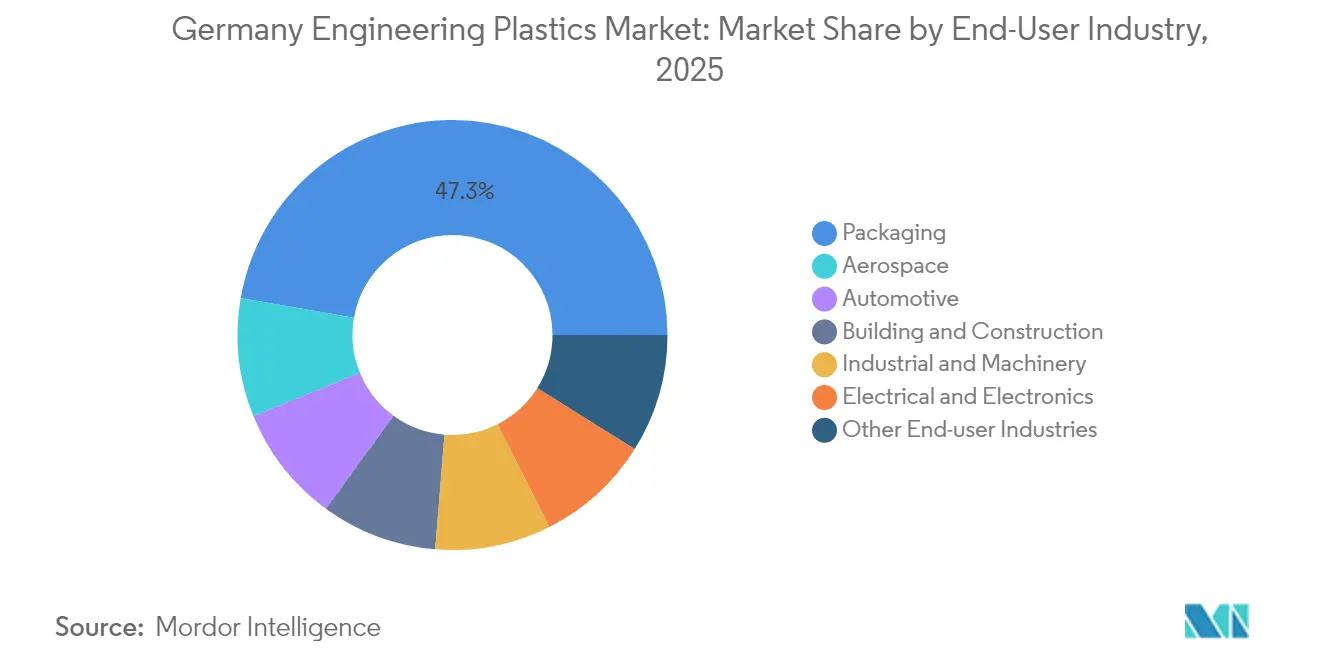

- By end-user industry, packaging commanded 47.25% of the Germany engineering plastics market size in 2025. Aerospace applications are set to rise at a 5.23% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Engineering Plastics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging EV-related lightweighting demand | +1.2% | Germany and EU automotive corridors | Medium term (2-4 years) |

| Energy-efficient building retrofits push high-performance plastics | +0.8% | Germany residential and commercial stock | Long term (≥ 4 years) |

| OEM substitution of metal components in machinery | +0.6% | German export-oriented machinery hubs | Medium term (2-4 years) |

| Germany’s hydrogen-economy scaling | +0.4% | Industrial hydrogen corridors | Long term (≥ 4 years) |

| EU Battery Regulation triggers specialty polymer housings | +0.3% | EU, led by German gigafactories | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging EV-related Lightweighting Demand

Battery-electric vehicle platforms require polymer housings and high-voltage components that trim curb weight without compromising safety. Major suppliers, such as BASF, Trinseo, and Envalior, have launched flame-retardant polyphthalamide and thermoplastic battery enclosures tailored to German OEM specifications. Automakers validate new materials within three- to five-year model cycles, anchoring a medium-term demand uplift that spills over into EU satellite plants[1]BASF SE, “Flame Retardant Polyphthalamide for EV Components,” basf.com.

Energy-efficient Building Retrofits Push High-Performance Plastics

Germany's Gebäudeenergiegesetz (GEG) building energy regulations are creating sustained demand for high-performance insulation materials and specialized polymer components that enable energy-efficient retrofits across residential and commercial sectors. The regulation's pipe insulation requirements specifically drive consumption of advanced polymer foams and specialized engineering plastics that maintain thermal performance under varying temperature conditions. This regulatory push aligns with Germany's broader decarbonization strategy, which necessitates material solutions that combine thermal efficiency with long-term durability in the building sector. Since retrofit projects span decades, polymer suppliers enjoy a steady long-run market where lifetime energy savings justify premium pricing.

OEM Substitution of Metal Components in Machinery

Germany's machinery and equipment sector is systematically replacing metal components with engineering plastics to achieve weight reduction and design flexibility advantages. This substitution trend accelerates as manufacturers pursue cost optimization while maintaining performance standards, particularly in applications where corrosion resistance and electrical insulation properties provide functional advantages beyond weight savings. The medium-term impact timeline aligns with machinery development cycles, where component redesign and validation processes require 2-4 years from material selection to market introduction. Export orientation creates multiplier effects, as successful German machinery applications influence global material standards and create reference cases for international polymer adoption.

Germany’s Hydrogen-Economy Scaling

The German Federal Government's National Hydrogen Strategy aims to achieve 10 GW of electrolysis capacity by 2030, generating specialized demand for PTFE, PEEK, and other high-performance polymers in pipeline seals, tank liners, and electrolysis system components[2]Bundesregierung, “National Hydrogen Strategy,” bundesregierung.de. This infrastructure scaling requires materials that maintain integrity under high-pressure hydrogen environments while resisting permeation and chemical degradation over extended service life. Germany's position as Europe's largest chemical producer offers strategic advantages in hydrogen adoption, as its existing industrial infrastructure can be adapted more readily than in greenfield development, thereby creating sustained demand for specialized polymer solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automakers' cost-down pressure amid BEV margin squeeze | -0.70% | Germany automotive sector, with EU supply chain effects | Short term (≤ 2 years) |

| Feedstock volatility due to EU energy-price swings | -0.50% | Germany and broader EU chemical industry | Medium term (2-4 years) |

| Recycling-quota gaps for high-temperature polymers | -0.40% | EU-wide, with concentrated impact on German specialty polymer producers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Automakers’ Cost-Down Pressure Amid BEV Margin Squeeze

German automotive OEMs are intensifying cost reduction initiatives as battery electric vehicle margins remain under pressure from battery costs and competitive pricing dynamics, directly impacting engineering plastics procurement strategies. This cost pressure manifests in aggressive supplier negotiations and material substitution evaluations, where premium engineering plastics are being replaced by lower-cost alternatives that meet minimum performance specifications. This restraint particularly affects high-performance polymer segments where technical differentiation commands premium pricing, forcing suppliers to demonstrate clear value propositions that justify cost premiums in increasingly price-sensitive applications.

Feedstock Volatility Due to EU Energy-Price Swings

European energy price volatility continues to impact chemical feedstock costs, creating margin pressure for engineering plastics producers who face unpredictable raw material pricing while operating under fixed customer contracts. German producer price data, showing a 1.2% year-over-year decline in basic chemicals in April 2025, masks the underlying volatility that complicates procurement planning and inventory management. The EU's energy transition policies create additional uncertainty as renewable energy deployment and grid stability investments influence industrial electricity pricing, affecting energy-intensive polymer production processes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: PET Dominance Meets Styrenic Innovation

PET held 47.92% of Germany engineering plastics market share in 2025, reflecting entrenched packaging demand and closed-loop recycling streams. Styrene copolymers, although smaller in base, are forecast to grow 4.01% CAGR to 2031 and capture incremental applications in electronics housings and interior trims. The Germany engineering plastics market size for styrenic grades is poised to expand as INEOS Styrolution introduces mass-balance ABS with up to 100% recycled content, easing OEM compliance burdens.

Second-tier resins reveal diverging stories. Polycarbonate capacity tightened after the 2025 divestment of a 160 kt unit, lifting utilization rates for remaining producers. Fluoropolymers, though niche in volume, garner premium prices in hydrogen seals and battery binders, reinforcing the value skew of the Germany engineering plastics market. Polyamide segments benefit from e-mobility yet face pricing tension from metal-replacement cost targets. Overall, sustainability certification now carries as much weight as mechanical performance in resin selection decisions.

By End-User Industry: Packaging Leadership Challenged by Aerospace Growth

Packaging contributed 47.25% to the Germany engineering plastics market size in 2025, underpinned by beverage and personal-care bottles. Aerospace demand, however, is projected to register the fastest 5.23% CAGR through 2031 as OEMs in Hamburg and Bavaria convert metal brackets and ducts to high-temperature polymers, shaving kilograms from each airframe.

The automotive industry retains its strategic importance but navigates mixed signals. Electrification drives the demand for high-voltage polymer components, yet cost-down pressures limit the use of non-critical polymer grades. Building and construction volumes grow steadily due to retrofit insulation mandates, while the electrical and electronics segments capitalize on Germany’s automation boom, driving demand for connector and sensor housing. The Germany engineering plastics market share mix is thus tilting from commodity applications toward specialized, higher-margin uses that reward certified recycled and bio-based content.

Geography Analysis

Germany is both the largest EU producer of polymers and a magnet for downstream consumption. North Rhine-Westphalia hosts chemical parks that supply feedstocks to Bavarian and Baden-Württemberg automotive giants, fostering a resilient intranational supply chain. Hamburg’s aerospace cluster and Lower Saxony’s battery cell plants diversify regional demand, ensuring that no single end-use industry dominates capacity utilization.

Cross-border trade amplifies local developments. Machinery built in Bavaria incorporates domestically sourced engineering plastics that accompany exported equipment worth EUR 66.8 billion in 2023. Germany engineering plastics market participants thus influence material standards worldwide by embedding advanced polymers into exported machinery and vehicles.

Circular-economy policy further shapes geography. New recycling hubs in Bavaria and Saxony-Anhalt convert post-consumer durables into feedstock, reducing reliance on virgin imports and creating closed loops within national borders. Hydrogen corridors planned along the Rhine and in coastal industrial zones add localized spikes in fluoropolymer consumption, reinforcing regional specialization. Collectively, these dynamics sustain balanced growth across Germany’s federal states, insulating the Germany engineering plastics market from isolated sector downturns.

Competitive Landscape

The Germany Engineering Plastics market is moderately concentrated. Acquisitions, such as ADNOC’s bid for Covestro and Deepak Chem Tech’s purchase of Trinseo’s Stade assets, signal a rising strategic value for German polymer expertise. Challengers exploit circular-content differentiation. INEOS Styrolution markets ABS grades with 100% mechanical recyclate, while Avient debuts recycled-content PC blends for electronics enclosures. Success hinges on meeting OEM performance criteria and securing ISCC Plus certification.

Germany Engineering Plastics Industry Leaders

Celanese Corporation

Covestro AG

BASF

LANXESS

Evonik Industries AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Avient Corporation announced the addition of new grades to its portfolio of recycled-content polycarbonate (PC) and PC blends, developed to meet the growing demand for materials that support sustainability in the electrical and electronics (E&E) industry in the Europe, Middle East, and Africa (EMEA) regions.

- October 2024: Envalior announced the launch of Pocan X-MB series of new polybutylene terephthalate (PBT) compounds based on bio-circular 1,4-butanediol (BDO). The sustainable content of the thermoplastics is certified and classified in accordance with the ISCC PLUS (International Sustainability and Carbon Certification) standard.

Germany Engineering Plastics Market Report Scope

Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging are covered as segments by End User Industry. Fluoropolymer, Liquid Crystal Polymer (LCP), Polyamide (PA), Polybutylene Terephthalate (PBT), Polycarbonate (PC), Polyether Ether Ketone (PEEK), Polyethylene Terephthalate (PET), Polyimide (PI), Polymethyl Methacrylate (PMMA), Polyoxymethylene (POM), Styrene Copolymers (ABS and SAN) are covered as segments by Resin Type.By Resin Type

| Fluoropolymer | Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) | |

| Polytetrafluoroethylene (PTFE) | |

| Polyvinylfluoride (PVF) | |

| Polyvinylidene Fluoride (PVDF) | |

| Other Sub Resin Types | |

| Liquid Crystal Polymer (LCP) | |

| Polyamide (PA) | Aramid |

| Polyamide (PA) 6 | |

| Polyamide (PA) 66 | |

| Polyphthalamide | |

| Polybutylene Terephthalate (PBT) | |

| Polycarbonate (PC) | |

| Polyether Ether Ketone (PEEK) | |

| Polyethylene Terephthalate (PET) | |

| Polyimide (PI) | |

| Polymethyl Methacrylate (PMMA) | |

| Polyoxymethylene (POM) | |

| Styrene Copolymers (ABS, SAN) |

By End-User Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-user Industries |

| By Resin Type | Fluoropolymer | Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) | ||

| Polytetrafluoroethylene (PTFE) | ||

| Polyvinylfluoride (PVF) | ||

| Polyvinylidene Fluoride (PVDF) | ||

| Other Sub Resin Types | ||

| Liquid Crystal Polymer (LCP) | ||

| Polyamide (PA) | Aramid | |

| Polyamide (PA) 6 | ||

| Polyamide (PA) 66 | ||

| Polyphthalamide | ||

| Polybutylene Terephthalate (PBT) | ||

| Polycarbonate (PC) | ||

| Polyether Ether Ketone (PEEK) | ||

| Polyethylene Terephthalate (PET) | ||

| Polyimide (PI) | ||

| Polymethyl Methacrylate (PMMA) | ||

| Polyoxymethylene (POM) | ||

| Styrene Copolymers (ABS, SAN) | ||

| By End-User Industry | Aerospace | |

| Automotive | ||

| Building and Construction | ||

| Electrical and Electronics | ||

| Industrial and Machinery | ||

| Packaging | ||

| Other End-user Industries | ||

Market Definition

- End-user Industry - Packaging, Electrical & Electronics, Automotive, Building & Construction, and Others are the end-user industries considered under the engineering plastics market.

- Resin - Under the scope of the study, consumption of virgin resins like Fluoropolymer, Polycarbonate, Polyethylene Terephthalate, Polybutylene Terephthalate, Polyoxymethylene, Polymethyl Methacrylate, Styrene Copolymers, Liquid Crystal Polymer, Polyether Ether Ketone, Polyimide, and Polyamide in the primary forms are considered. Recycling has been provided separately under its individual chapter.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms