France Engineering Plastics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

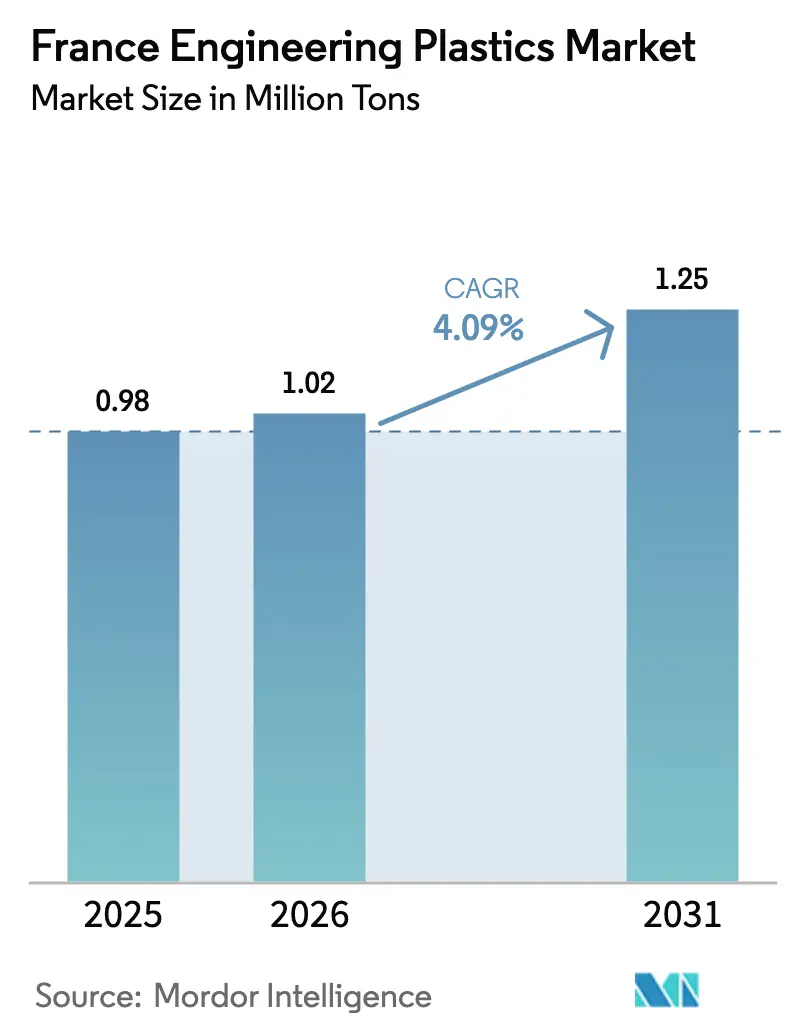

| Base Year Market Size (2025) | 0.98 Million tons |

| Market Volume (2026) | 1.02 Million tons |

| Market Volume (2031) | 1.25 Million tons |

| Growth Rate (2026 - 2031) | 4.09% CAGR |

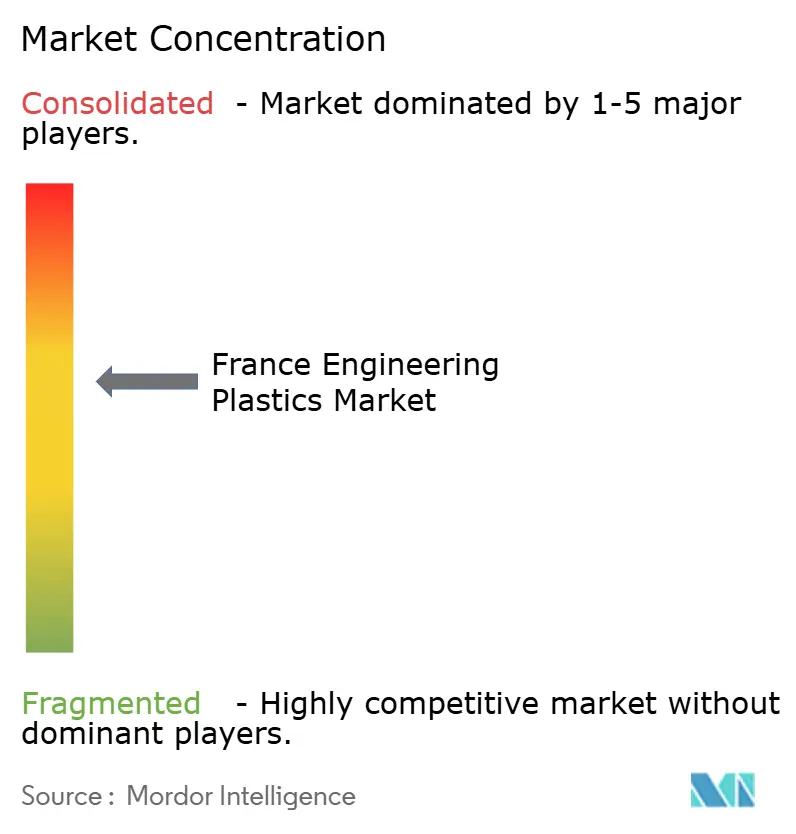

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Engineering Plastics Market Analysis by Mordor Intelligence

The France Engineering Plastics Market size is expected to grow from 0.98 Million tons in 2025 to 1.02 Million tons in 2026 and is forecast to reach 1.25 Million tons by 2031 at 4.09% CAGR over 2026-2031. The market is buoyed by the electrification of passenger vehicles, circular economy regulations under France’s AGEC law, and the rapid adoption of high-performance filaments in industrial 3D printing. The scale-up of super-critical CO₂ purification technologies enhances the quality of recycled resins, while EV-driven lightweighting prompts OEMs to replace metals with advanced polymers in structural parts. Regulations restricting PFAS are spurring product reformulation in fluoropolymers, yet capacity additions in polyamide precursors and bio-based acrylics are offsetting potential shortfalls. Robust aerospace and luxury goods manufacturing enables suppliers to command premium pricing, thereby sustaining investments in closed-loop solutions. These converging trends solidify France’s role as a European hub for sustainable materials innovation, maintaining the French engineering plastics market on a steady growth trajectory.

Key Report Takeaways

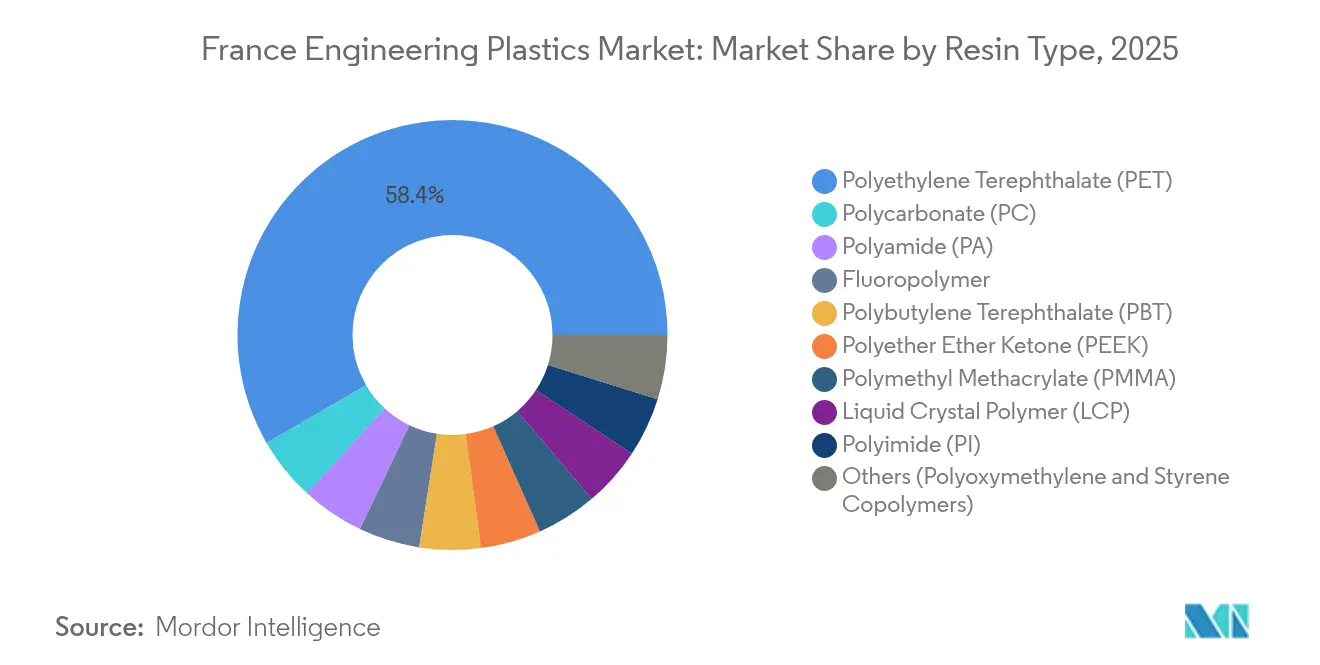

- By resin type, Polyethylene Terephthalate (PET) led with a 58.37% share of France's engineering plastics market in 2025, while fluoropolymers registered the fastest growth at a 6.22% CAGR through 2031.

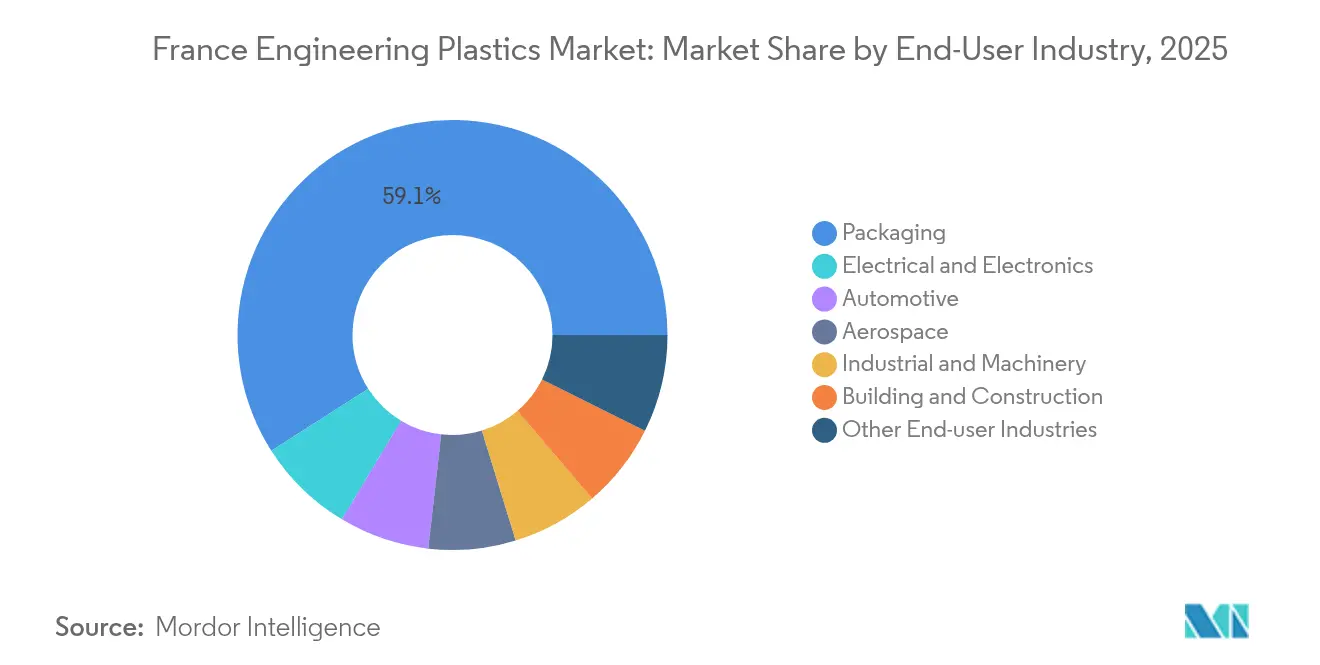

- By end-user industry, packaging accounted for a 59.05% share of the French engineering plastics market size in 2025; the electrical and electronics sector is advancing at a 7.01% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Engineering Plastics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in EV‐driven lightweighting for French OEM platforms | +2.10% | France | Medium term (2-4 years) |

| Circular-economy mandates under the AGEC law accelerating demand for recyclable engineering resins | +1.80% | France | Long term (≥4 years) |

| Rapid uptake of industrial 3D-printing filaments (PEEK, PA CF) by French service bureaus | +1.10% | France | Short term (≤2 years) |

| Scale-up of super-critical CO₂ purification lines raising availability of high-quality recyclate | +0.90% | France | Medium term (2-4 years) |

| Miniaturisation of high-voltage E/E components requiring high-CTI, high-heat polymers | +1.00% | France | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

EV-Driven Lightweighting Accelerates Advanced Polymer Adoption

Demand for lighter vehicles is surging as French automakers chase stricter fleet-emission targets. Stellantis and Renault now specify high-strength polyamide, polycarbonate, and fluoropolymer grades in battery enclosures, front-end carriers, and high-voltage connectors[1]BASF SE, “BASF ramps up HMD capacity in France,” basf.com. BASF’s new 260,000 tpa hexamethylenediamine complex in Chalampé secures the local supply of PA 6.6 intermediates, shortening lead times for Tier-1 molders. Covestro’s high-CTI polycarbonate allows miniaturized busbars that cut copper weight without compromising safety. These developments shift procurement budgets toward engineering plastics with superior creep, dielectric, and flame-retardant performance. As a result, the French engineering plastics market gains momentum in the automotive sector, reinforcing domestic polymer demand even as metal producers face order erosion.

AGEC Law Mandates Reshape Polymer Specification Priorities

The Anti-Waste and Circular Economy (AGEC) law compels manufacturers to choose materials designed for high-value recycling. Brand owners must now meet recycled-content thresholds in both rigid and flexible packaging, prompting converters to shift toward mass-balance-certified polyamides, polyesters, and polyoxymethylene. Arkema holds ISCC PLUS certification across multiple French sites, enabling customers to claim recycled or bio-attributed content in finished parts. Syensqo’s ECHO polysulfones with 33-98% recycled feedstock address high-temperature applications once reserved for virgin grades. EPR fees reward designs that simplify end-of-life sorting, steering R&D toward mono-material formats. Compliance pressures cascade down the supply chain, raising entry barriers for importers lacking traceable low-carbon feedstocks and strengthening domestic suppliers with circular-ready portfolios.

Industrial 3D-Printing Filaments Drive High-Performance Polymer Demand

French service bureaus have expanded industrial additive-manufacturing capacity by double digits since 2024, prioritizing PEEK, carbon-fiber-reinforced PA, and PEKK filaments for aerospace and medical prototyping[2]Arkema, “Arkema and Hexcel complete first thermoplastic composite aircraft panel,” arkema.com . Arkema’s partnership with Hexcel resulted in the first thermoplastic composite aircraft panel qualified for flight, validating the large-format printing of high-performance polymers. DEMGY Group operates multi-laser SLS systems that process carbon-fiber-PA in near-net-shape functional parts, slashing lead times for OEMs in Toulouse and Bordeaux. These applications require certified resins with tight melt-flow windows, favoring domestic producers that can provide technical support and localized inventories. The pull-through effect enhances the overall French engineering plastics market by creating new demand niches beyond conventional molding.

Super-Critical CO₂ Purification Enhances Recyclate Quality

De Dietrich and IPC have commissioned pilot lines that utilize super-critical CO₂ to remove legacy additives and odors from shredded polyamide and polycarbonate waste, enabling the production of grades with near-virgin mechanical properties. This technology reduces thermal history damage, enabling the inclusion of 40-60% recyclate in automotive and electrical and electronic (E&E) parts without tensile loss. French chemical clusters receive public funding to scale up such plants, aligning with EU targets on the uptake of recycled content. Premium recyclate feeds divert tonnage away from incineration, moving the France engineering plastics market closer to closed-loop goals and reducing carbon-adjustment costs for exporters.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Feed-stock price volatility linked to Brent & naphtha spreads | -0.90% | Global, with acute impact on European petrochemical complexes | Short term (≤ 2 years) |

| EU PFAS clamp-down impacting fluoropolymer value chains | -0.60% | EU-wide, with concentrated impact on specialty chemical hubs | Medium term (2-4 years) |

| Capacity rationalisation at Tier-1 auto suppliers dampening near-term resin procurement | -0.50% | EU automotive corridors, with spillover to France supplier networks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Feedstock Price Volatility Constrains Margin Expansion

Brent-linked naphtha costs bounced within a USD 15 per-barrel band in 2024-2025, squeezing crackers with limited feedstock flexibility. LyondellBasell’s strategic review of the Berre complex highlights competitiveness risks associated with standalone assets. LANXESS reported lower selling prices despite volumes recovering, illustrating how rapid cost swings can unsettle contract negotiations. French compounders, many of which import intermediates, face working capital spikes when benzene and caprolactam prices fluctuate abruptly. Smaller processors hedge through shorter contracts, but that raises procurement overhead, limiting their ability to fund R&D in advanced formulations.

EU PFAS Regulations Disrupt Fluoropolymer Applications

Law No. 2025-188 restricts PFAS usage in France from January 2025, with broader EU bans under consideration. Avient responded by introducing PTFE-free lubricated compounds across the PA, PC, and POM families; however, qualifying alternatives in critical valves and cabling remains slow. Battery manufacturers postpone specifications while exemptions are clarified, freezing purchase orders for some fluoropolymer grades. Aerospace OEMs require multi-year validation of PFAS-free seals, stretching development cycles. These uncertainties dampen near-term growth in fluoropolymer demand and weigh on overall France engineering plastics market volumes until compliant chemistries scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: PET Dominance Contrasts Fluoropolymer Acceleration

Polyethylene terephthalate held 58.37% of France Engineering Plastics market share in 2025, anchored by food-grade bottle demand and mature recycling streams. The France engineering plastics market size for PET equated to roughly 0.57 million tons. Mandatory deposit-return schemes increased rPET availability, encouraging converters to use high-viscosity grades in trays and thermoforms. Fluoropolymer volumes remain small, yet they grow at a 6.22% CAGR as PVDF coatings and seals become increasingly critical to lithium-ion batteries and chemical process equipment. Arkema’s Tavaux expansion of suspension-grade Solef PVDF under long-term contracts with battery cell makers illustrates this momentum.

Polyamide stands out for balanced growth. BASF’s full control of the Alsachimie joint venture secures an adipic acid supply, supporting local PA 6.6 production in engineering compounds for engine mounts and rocker covers. Polycarbonate gains share in EV connectors using Covestro’s flame-retardant grades certified to UL 94 V-0. PEEK and PEKK niches expand into aerospace 3D printing. Styrene copolymers face regulatory headwinds due to the postponed styrenic packaging ban; however, converters gain a five-year window to redesign in-mold labeling and foamed trays.

By End-User Industry: Packaging Leadership Yields to Electronics Growth

Packaging accounted for 59.05% of the France engineering plastics market size in 2025, equating to 0.58 million tons. The segment thrives on PET bottle demand and rPET mandates set by AGEC, but margins tighten as FMCG brand owners push lightweight formats. Electrical and electronics is the fastest-growing use case, pacing at a 7.01% CAGR thanks to EV charging hardware, photovoltaic junction boxes, and miniaturized consumer devices. High-CTI polycarbonate and glass-reinforced PA dominate these applications.

The automotive industry absorbs roughly 14% of engineering plastic consumption. Lightweighting imperatives and e-powertrain redesigns help maintain resilient demand despite cyclical fluctuations in vehicle output. Aerospace clusters in Toulouse and Bordeaux sustain a steady uptake of high-performance PEKK and PPS, while the building and construction sector benefits from thermal-break profiles in energy-efficient retrofits. Industrial machinery experiences incremental demand from automation equipment and precision gears molded from POM-ECO formulations, which offer reduced carbon footprints.

Geography Analysis

France serves as the linchpin for Western Europe's engineering plastics value chains. The Seine-Nord logistics corridor links feedstock imports arriving at Le Havre with polymer converters in Île-de-France, ensuring quick transit to EU customers. Auvergne-Rhône-Alpes hosts BASF’s Chalampé polyamide precursors and Arkema’s bio-based acrylics in Carling, positioning the region as the largest production zone. Nouvelle-Aquitaine integrates aerospace composites, leveraging suppliers clustered near Toulouse and Bordeaux.

Regional policy coherence accelerates innovation. The AGEC law enforces consistent EPR fees across departments, incentivizing the use of recyclables nationwide. Polymeris, the national competitiveness cluster, aggregates 590 members and EUR 894 million in funded projects that span recycling, additive manufacturing, and lightweight structures. Its accelerator programs help SMEs access pilot compounding lines, thereby shortening the commercialization loop for novel blends.

Port infrastructure underpins global reach. Marseille-Fos handles petrochemical imports from the Middle East, while Atlantic ports, including Nantes and La Rochelle, ship compounded pellets to North America. These gateways shield French converters from continental trucking bottlenecks. Combined, the logistical and regulatory environment supports a robust France engineering plastics market, enabling domestic suppliers to serve both intra-EU demand and premium export niches.

Competitive Landscape

The France Engineering Plastics Market is moderately concentrated. Arkema leads through vertical integration in fluoropolymers and bio-based materials, while BASF leverages scale in polyamide feedstocks. Syensqo captures high-value battery-grade PVDF contracts, and LANXESS pivots to specialty intermediates after divesting urethanes. Innovation pipelines spotlight composites and recycling. Arkema and Hexcel validated thermoplastic composite fuselage panels, promising 30% faster cycle times versus thermosets. De Dietrich’s super-critical CO₂ purification pilots open a new revenue stream in high-purity recyclate, tempting compounders to source local reclaimed feedstock.

France Engineering Plastics Industry Leaders

Arkema

Domo Chemicals

Solvay

Celanese Corporation

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: BASF took over DOMO Chemicals' 49% stake in the Alsachimie joint venture. This move positions BASF as the sole owner of a production facility in Chalampé, France, specializing in key polyamide (PA) 6.6 precursors. These precursors encompass KA-oil, adipic acid, and hexamethylenediamine adipate.

- May 2025: Syensqo signed multi-year contracts to supply its battery-grade Solef Polyvinylidene Fluoride (PVDF) to automotive OEMs and battery manufacturers. Deliveries will come from Syensqo's advanced plant in Tavaux, France, leveraging its suspension PVDF technology.

France Engineering Plastics Market Report Scope

Aerospace, Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging are covered as segments by End User Industry. Fluoropolymer, Liquid Crystal Polymer (LCP), Polyamide (PA), Polybutylene Terephthalate (PBT), Polycarbonate (PC), Polyether Ether Ketone (PEEK), Polyethylene Terephthalate (PET), Polyimide (PI), Polymethyl Methacrylate (PMMA), Polyoxymethylene (POM), Styrene Copolymers (ABS and SAN) are covered as segments by Resin Type.| Fluoropolymer | Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) | |

| Polytetrafluoroethylene (PTFE) | |

| Polyvinylfluoride (PVF) | |

| Polyvinylidene Fluoride (PVDF) | |

| Other Sub Resin Types | |

| Liquid Crystal Polymer (LCP) | |

| Polyamide (PA) | Aramid |

| Polyamide (PA) 6 | |

| Polyamide (PA) 66 | |

| Polyphthalamide | |

| Polybutylene Terephthalate (PBT) | |

| Polycarbonate (PC) | |

| Polyether Ether Ketone (PEEK) | |

| Polyethylene Terephthalate (PET) | |

| Polyimide (PI) | |

| Polymethyl Methacrylate (PMMA) | |

| Polyoxymethylene (POM) | |

| Styrene Copolymers (ABS, SAN) |

| Aerospace |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-user Industries |

| By Resin Type | Fluoropolymer | Ethylenetetrafluoroethylene (ETFE) |

| Fluorinated Ethylene-propylene (FEP) | ||

| Polytetrafluoroethylene (PTFE) | ||

| Polyvinylfluoride (PVF) | ||

| Polyvinylidene Fluoride (PVDF) | ||

| Other Sub Resin Types | ||

| Liquid Crystal Polymer (LCP) | ||

| Polyamide (PA) | Aramid | |

| Polyamide (PA) 6 | ||

| Polyamide (PA) 66 | ||

| Polyphthalamide | ||

| Polybutylene Terephthalate (PBT) | ||

| Polycarbonate (PC) | ||

| Polyether Ether Ketone (PEEK) | ||

| Polyethylene Terephthalate (PET) | ||

| Polyimide (PI) | ||

| Polymethyl Methacrylate (PMMA) | ||

| Polyoxymethylene (POM) | ||

| Styrene Copolymers (ABS, SAN) | ||

| By End-User Industry | Aerospace | |

| Automotive | ||

| Building and Construction | ||

| Electrical and Electronics | ||

| Industrial and Machinery | ||

| Packaging | ||

| Other End-user Industries | ||

Market Definition

- End-user Industry - Packaging, Electrical & Electronics, Automotive, Building & Construction, and Others are the end-user industries considered under the engineering plastics market.

- Resin - Under the scope of the study, consumption of virgin resins like Fluoropolymer, Polycarbonate, Polyethylene Terephthalate, Polybutylene Terephthalate, Polyoxymethylene, Polymethyl Methacrylate, Styrene Copolymers, Liquid Crystal Polymer, Polyether Ether Ketone, Polyimide, and Polyamide in the primary forms are considered. Recycling has been provided separately under its individual chapter.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms