Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

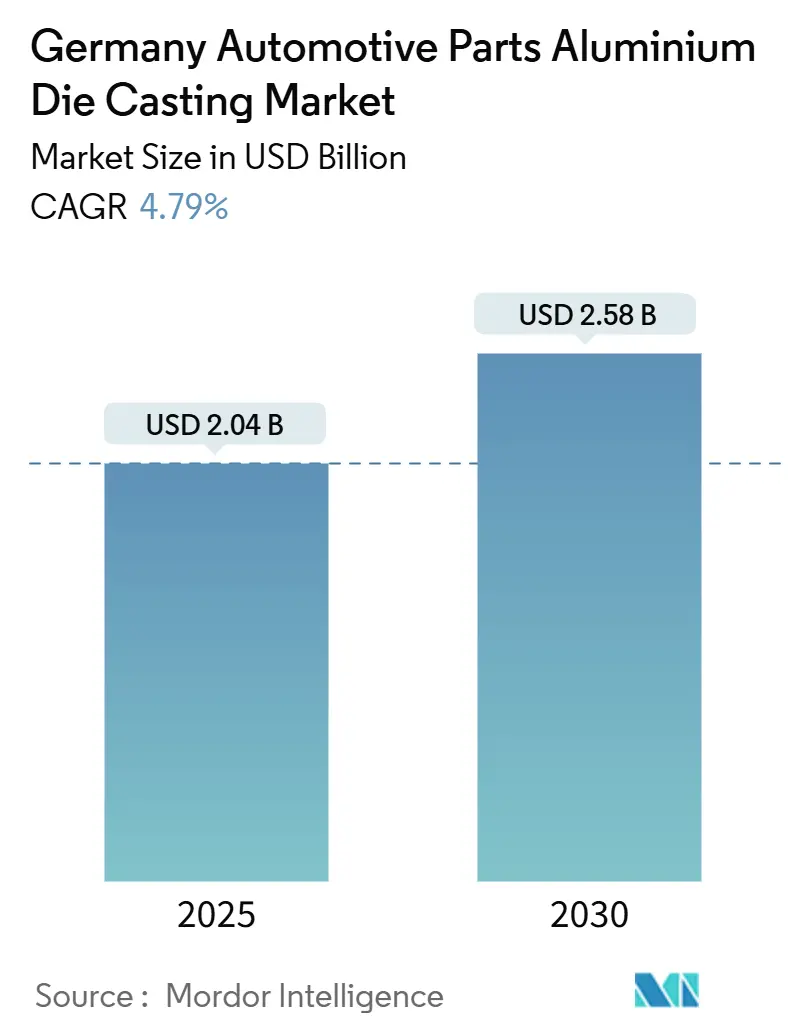

| Market Size (2025) | USD 2.04 Billion |

| Market Size (2030) | USD 2.58 Billion |

| Growth Rate (2025 - 2030) | 4.79% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Automotive Parts Aluminium Die Casting Market Analysis by Mordor Intelligence

The German automotive parts aluminum die casting market size reached USD 2.04 billion in 2025 and is projected to climb to USD 2.58 billion by 2030, translating into a 4.79% CAGR across the forecast horizon. This steady topline disguises a fundamental product mix pivot from engine blocks to electrification-centric castings, with battery housings, integrated thermal systems, and significant structural elements charting the fastest volume gains. Broad electrification roadmaps pursued by Volkswagen, BMW, and Mercedes-Benz stimulate continuous tooling upgrades, while megacasting investments compress multi-part assemblies into single die-cast structures, trimming vehicle weight and spot-weld counts. At the same time, pressure from the EU Carbon Border Adjustment Mechanism and OEM circular-economy mandates accelerates the shift toward secondary aluminum and renewable-powered melting, forcing foundries to master alloy housekeeping, real-time process controls, and energy-efficient furnace technology.

Key Report Takeaways

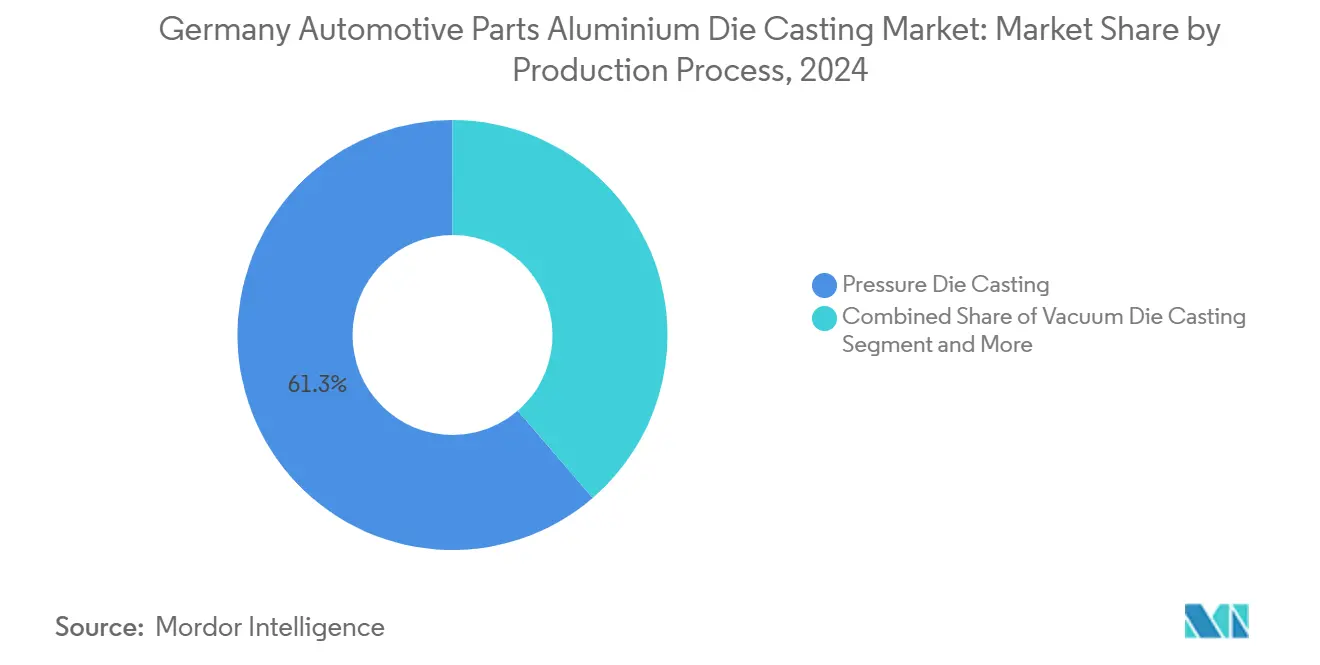

- By production process, pressure die casting led with 61.25% of Germany's automotive parts aluminum die casting market share in 2024, while vacuum die casting is on track to expand at a 5.45% CAGR to 2030.

- By application, engine parts captured 39.16% of Germany's automotive parts aluminum die casting market share in 2024; e-mobility battery housings and thermal systems are projected to advance at a 6.94% CAGR through 2030.

- By vehicle type, passenger cars accounted for 76.24% of Germany's automotive parts aluminum die casting market size in 2024, whereas light commercial vehicles are expected to record the strongest 5.82% CAGR through 2030.

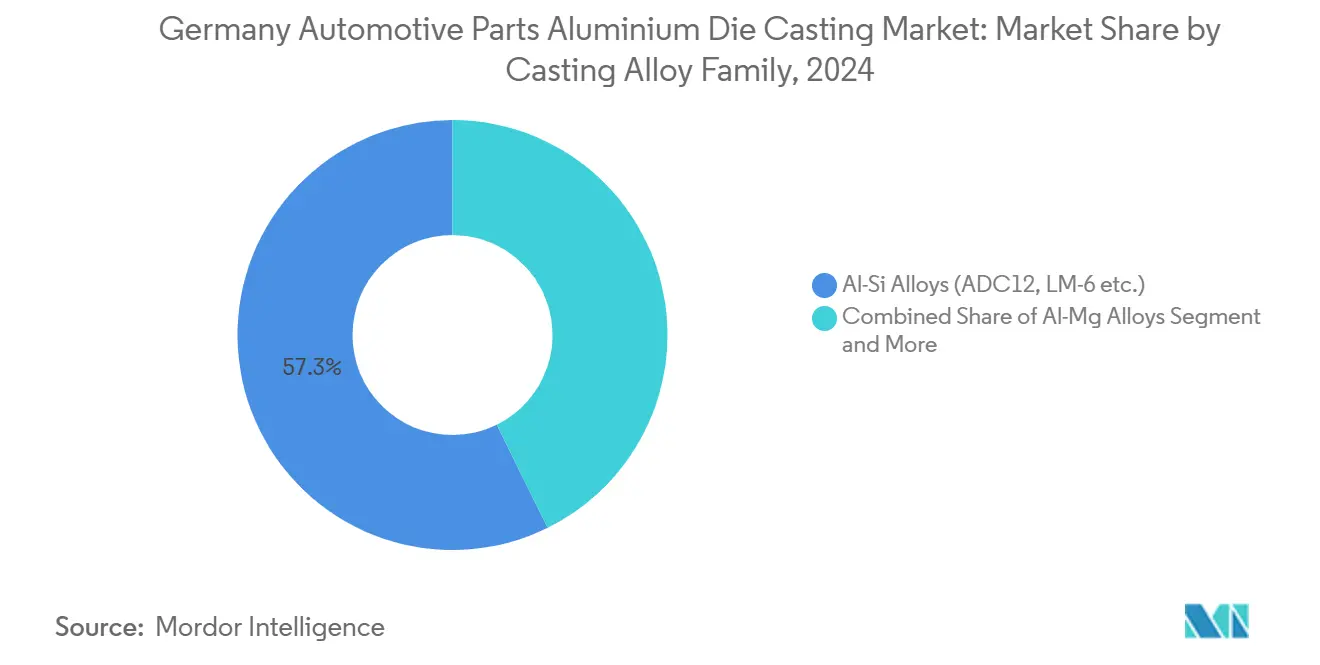

- By casting alloy family, Al-Si grades accounted for 57.25% of Germany's automotive parts aluminum die casting market size in 2024, while Al-Mg alloys are forecasted to grow at a 6.21% CAGR through 2030.

- By end-user, OEM/Tier-1 suppliers commanded 73.08% of Germany's automotive parts aluminum die casting market size in 2024 and are projected to post a 5.19% CAGR during 2025-2030.

Germany Automotive Parts Aluminium Die Casting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-Led Giga and Megacasting | +1.2% | Germany's core, spill-over to the EU | Medium term (2-4 years) |

| Surge in Integrated Battery Housing | +1.1% | Germany's automotive hubs | Medium term (2-4 years) |

| Stricter EU Fleet Emission Rules | +0.8% | EU-wide, Germany focus | Short term (≤ 2 years) |

| OEM Circular Economy Mandates | +0.6% | Germany | Long term (≥ 4 years) |

| AI Driven HPDC Process Control | +0.4% | Germany's foundry clusters | Medium term (2-4 years) |

| Incentives for Foundry Decarbonization | +0.3% | Germany's federal and state levels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EV-led Giga and Mega-Casting Adoption

Investments in giga- and megacasting lines dramatically reconfigure vehicle underbodies, battery frames, and crash-load structures. Handtmann’s Biberach plant operates Europe’s first series megacasting unit capable of injecting 128 kg per cycle, knocking out significant welded parts with weight savings [1]“Europe’s First Series Megacasting Line,” EUROGUSS, euroguss.de. At its Kassel facility, Volkswagen is replacing multiple sheet-metal pieces with a single rear module, showcasing Germany's readiness to adopt advanced structural casting techniques. Meanwhile, Mercedes-Benz is testing its Bionicast rear structure, utilizing a one-piece design that integrates various components. This approach streamlines production processes and emphasizes the economic advantages of simplified tooling, faster takt times, and improved logistics. Foundries scale 4,000-ton presses, tailor vacuum valves for porosity control, and integrate AI sensors for real-time shot analytics, cementing Germany's automotive parts aluminum die casting market leadership in structural EV castings.

Surge in Integrated Battery-Housing Programs

Handtmann secured a EUR 630 million (~USD 680 million) order for high-voltage battery enclosures, a single contract that nearly replaces multi-year engine-block volumes. BMW’s Landshut expansion boosts capacity for Neue Klasse housings, achieving dual roles of structural support and heat dissipation in a single casting. Suppliers engineer multi-cavity molds with embedded cooling circuits and crush-proof ribbing, broadening the addressable value of the German automotive parts aluminum die casting market per EV.

Stricter EU Fleet-Emission Rules Beyond Euro 7

Euro 7 extends compliance beyond exhaust to life-cycle carbon metrics, intensifying aluminum substitution for stamped steel. BMW’s Landshut shop adopted injector casting technology that lowers melt temperature, curbing energy use and enabling thinner walls for next-generation e-drive housings [2]“Landshut Foundry Expands for Neue Klasse EVs,” BMW Group Press, bmwgroup.com. Foundries that leverage renewable power and closed-loop scrap streams enable OEMs to log verifiable CO₂ reductions within scope-3 audits, thereby strengthening demand for premium, low-carbon die-cast parts produced domestically.

OEM Circular-Economy Mandates (≥40% Recycled Al by 2040)

Volkswagen and Mercedes aim to achieve significant recycled content by 2040, prompting alloy chemists to counter iron-rich scrap with manganese additions to suppress β-Al₅FeSi brittleness, while targeting low sludge factors. Rapid solidification in high-pressure die casting effectively addresses micro-segregation. This advancement enables significant end-of-life scrap recovery in high-strength AlSi10MnMg, along with notable reductions in CO₂ emissions. Commercially, these results underpin long-term scrap procurement contracts, insulating foundries against CBAM surcharges on imported primary metal.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Aluminum Premiums and CBAM | -0.9% | Germany's import-dependent regions | Short term (≤ 2 years) |

| Labor Shortage In German Foundries | -0.7% | Germany's foundry clusters | Long term (≥ 4 years) |

| High Scrap-Rate Risk | -0.5% | Germany's megacasting facilities | Medium term (2-4 years) |

| Competition from Extrusion-Welded Structures | -0.4% | Germany's automotive hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Aluminum Premiums and CBAM Surcharge Risk

Raw-metal volatility plus CBAM’s phased-in carbon tariffs could lift landed ingot costs for non-EU supply, squeezing EBITDA for import-reliant shops [3]“CBAM Impact on Foundries,” Bundesverband Deutsche Gießerei-Industrie, bdguss.de. Foundries hedge on multi-year scrap contracts and pivot to domestic recyclers, yet higher melt-loss variability forces tighter furnace controls and additional melt-treatment costs that challenge smaller operators.

Skilled-Labor Shortage in German Foundries

Since 2019, metalworking payrolls have dropped significantly, resulting in unfilled positions for robotics programmers, tool-room technologists, and metallurgists. Highlighting the gap between new machinery and achieving peak production, BMW has taken considerable time to retrain its employees for AI-equipped HPDC cells. Sector bodies press for incentives to promote vocational training, and fast-tracking skilled immigration to sustain market competitiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Process: Vacuum Die Casting Gains Momentum Despite Pressure Die Casting Dominance

Pressure die casting retained 61.25% of Germany's automotive parts aluminum die casting market share in 2024, reflecting entrenched machine parks and proven cost-per-shot economics. Yet, vacuum die casting is advancing at a 5.45% CAGR through 2030, driven by battery-housing and body-in-white programs that require porosity levels below 0.2% and post-heat-treat tensile targets exceeding 240 MPa. Foundries retrofit shot sleeves with vacuum valves, add inline degassers, and deploy seal-plate designs to capture incremental contracts from OEM crash-zone engineers.

Gravity, semi-solid, and squeeze processes serve niche under-hood brackets and suspension knuckles, but their collective volume trails high-pressure technologies by a factor of ten. Moving toward 2030, megacasting’s 6,000-ton presses will primarily rely on de-gassed molten pools, meaning hybrid HPDC-vacuum setups will capture most incremental orders and solidify Germany's automotive parts aluminum die casting market leadership in critical safety castings.

By Application Type: E-Mobility Components Surge While Engine Parts Decline

Engine parts represented 39.16% of Germany's automotive parts aluminum die casting market size in 2024; however, volumes plateaued as ICE model launches tapered post-2025. E-mobility battery housings and thermal plates are expected to record a 6.94% CAGR through 2030, outpacing growth in legacy powertrain castings. Structural body castings for floor assemblies now benefit from OEM megacasting platforms, lifting the average aluminum content per vehicle.

Transmission cases shrink in prominence yet pivot toward e-axle designs, requiring integrated cooling galleries, which preserves selective demand for thin-wall die casting expertise. With the growing shift toward electric vehicles, parts designed for electrification are poised to outpace engines, becoming the primary revenue driver for Germany's automotive parts aluminum die-casting market.

By Vehicle Type: Light Commercial Vehicles Drive Growth Despite Passenger-Car Dominance

Passenger cars delivered 76.24% of the German automotive parts aluminum die casting market size in 2024, anchored by VW’s modular platforms and BMW’s high-volume exports. However, last-mile delivery electrification is expected to lift light commercial-vehicle demand at a 5.82% CAGR through 2030, supported by urban access regulations and e-commerce network build-outs. Battery-box dimensions in vans run 30-40% larger than in hatchbacks, amplifying die-casting tonnage per unit.

Two-wheeler electrification in densely populated German cities drives small-lot orders for swingarms and motor housings. In contrast, heavy commercial vehicles rely on highly specialized low-volume castings for e-bus chassis cross-members. Foundries with flexible cell configurations and quick-change tooling are well-positioned to capture a share as the model mix widens across various payload categories.

By Casting Alloy Family: Al-Mg Alloys Gain Ground Against Al-Si Dominance

Al-Si chemistries, such as ADC12 and LM-6, commanded a 57.25% share of Germany's automotive parts aluminum die casting market in 2024, prized for their fluidity and long tool life. Yet Al-Mg families will post a 6.21% CAGR as OEM circular-economy mandates favor copper-free, high-recycle blends. Mg additions enhance the strength-to-density ratio, allowing for thinner EV battery-tray walls without compromising deformation energy.

German metallurgists utilize online spectrometers and automated grain-refiner dosing systems to mitigate scrap variability, ensuring that Germany's automotive parts aluminum die casting industry alloys meet weldability and corrosion resistance benchmarks. Growth in the Al-Cu and hybrid alloy segments remains niche, focusing on e-motor shells that require enhanced thermal conductivity for insulation-class F winding temperatures.

By End-User: OEM and Tier-1 Suppliers Maintain Dominance Over Aftermarket

OEMs/Tier-1s held 73.08% of Germany's automotive parts aluminum die casting market size in 2024, and their 5.19% CAGR underscores deepening vertical integration. Automakers pre-book megacasting slots via multi-year offtake agreements, effectively locking out spot aftermarket buyers.

Higher component consolidation reduces serviceable item counts, limiting traditional replacement demand and prompting aftermarket players to focus on specialized retrofit cooling plates and performance-tuning cast parts. Tier-1s embed casting cells in modular e-drive assembly lines, shortening supply chains and safeguarding intellectual property for proprietary stator designs.

Geography Analysis

Germany controlled a significant share of European automotive aluminum die-casting output in 2024, leveraging dense supplier clusters in Baden-Württemberg, Bavaria, and North Rhine-Westphalia. Within these regions, short logistics corridors between die casters and OEM stamping or assembly plants support just-in-sequence delivery models.

Early CBAM reporting, since 2023, positions domestic foundries as low-carbon sourcing partners for pan-European vehicle programs, enabling price premiums over higher-emission imports. France and Italy host sizable vehicle assembly but rely on German casting imports for giga-casting expertise and equipment know-how. Eastern European plants offer labor-cost relief yet trail in vacuum casting adoption and AI-driven process monitoring, ceding complex EV programs to German incumbents.

Suppliers such as Handtmann deploy satellite facilities to complement their domestic megacasting hubs, striking a balance between cost and proximity. Trade-policy uncertainty and logistical emissions-tracking favor regionally integrated value chains, reinforcing the market's gravity at the continent’s center.

Competitive Landscape

Germany’s market exhibits moderate concentration. Handtmann leads structural giga-casting; Nemak specializes in e-drive housings; Rheinmetall excels in vacuum die-cast battery plates; and Alutech Holding expanded its reach by acquiring AE Group’s 1,300-employee site in 2024. Strategic differentiation hinges on AI process controls, porosity-free large-part capability, and verified low-carbon metal sourcing.

VW and BMW push preferred-supplier frameworks that reward decarbonization roadmaps, prompting smaller shops to consolidate or focus on niche contract manufacturing. Equipment vendors like Bühler supply 6,000-ton presses with integrated shot analytics, raising capex thresholds and erecting entry barriers.

R&D alliances among foundries, universities, and alloy producers speed the qualification of high-scrap Al-Mg grades, embedding Germany's automotive parts aluminum die casting market know-how that distant competitors struggle to replicate.

Germany Automotive Parts Aluminium Die Casting Industry Leaders

Nemak, S.A.B. de C.V.

Rheinmetall AG (KS HUAYU AluTech GmbH)

Handtmann Group

Ryobi Limited

KSM Casting Group GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Volkswagen announced the adoption of giga-casting for its forthcoming ID-series entry-level EVs during IAA Mobility 2025 in Munich.

- April 2025: Handtmann announced a second megacasting cell at its Biberach site following a successful 2024 ramp-up.

- February 2024: Alutech Holding GmbH & Co. KG acquired 100% of AE Group AG, expanding high-pressure die-casting capacity in Thuringia.

- January 2024: LMG Manufacturing GmbH opened a new HPDC hall in Hoym/Seeland to supply BMW with aluminum parts for electromobility.

Germany Automotive Parts Aluminium Die Casting Market Report Scope

The German Automotive Parts Aluminum Die Casting Market segments its offerings by Production Process (including Pressure Die Casting and Vacuum Die Casting), Application Type (such as Engine Parts and Body and Structural Parts), Vehicle Type (covering Passenger Cars and Two-Wheelers), Casting Alloy Family (featuring Al-Si Alloys and Al-Mg Alloys), and End-User (OEM / Tier-1 suppliers, and independent aftermarket).

Market forecasts are presented in terms of value (USD).

By Production Process

| Pressure Die Casting |

| Vacuum Die Casting |

| Squeeze Die Casting |

| Gravity Die Casting |

| Semi-solid / Rheo Casting |

By Application Type

| Engine Parts |

| Body and Structural Parts |

| Transmission and Driveline Parts |

| E-mobility Battery Housings and Thermal Systems |

| Other Applications (HVAC, Steering, Braking) |

By Vehicle Type

| Passenger Cars |

| Two-Wheelers |

| Three-Wheelers |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles and Buses |

By Casting Alloy Family

| Al-Si Alloys (ADC12, LM-6 etc.) |

| Al-Mg Alloys |

| Al-Cu and Others |

By End-User

| Original Equipment Manufacturer (OEM) / Tier-1 Suppliers |

| Independent Aftermarket |

| By Production Process | Pressure Die Casting |

| Vacuum Die Casting | |

| Squeeze Die Casting | |

| Gravity Die Casting | |

| Semi-solid / Rheo Casting | |

| By Application Type | Engine Parts |

| Body and Structural Parts | |

| Transmission and Driveline Parts | |

| E-mobility Battery Housings and Thermal Systems | |

| Other Applications (HVAC, Steering, Braking) | |

| By Vehicle Type | Passenger Cars |

| Two-Wheelers | |

| Three-Wheelers | |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles and Buses | |

| By Casting Alloy Family | Al-Si Alloys (ADC12, LM-6 etc.) |

| Al-Mg Alloys | |

| Al-Cu and Others | |

| By End-User | Original Equipment Manufacturer (OEM) / Tier-1 Suppliers |

| Independent Aftermarket |

Key Questions Answered in the Report

Which processes dominate aluminum die casting volumes in Germany?

Pressure die casting remains the workhorse, holding 61.25% share in 2024, but vacuum die casting is growing fastest at 5.45% CAGR on rising structural-part quality requirements.

Which segment grows fastest within the casting application mix?

Battery housings and integrated thermal systems rise at 6.94% CAGR through 2030 as EV penetration reshapes the component portfolio.

What is the outlook for light commercial-vehicle castings?

Electrification of delivery vans drives a 5.82% CAGR, with larger battery trays boosting aluminum tonnage per unit and offering high-value contracts to flexible die casters.

How are German die casters coping with EU carbon regulations?

Foundries localize scrap sourcing, invest in renewable energy furnaces, and adopt AI-driven process controls to meet CBAM and OEM recycled-content mandates while protecting margins.

Page last updated on: