GCC Paper Bags Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

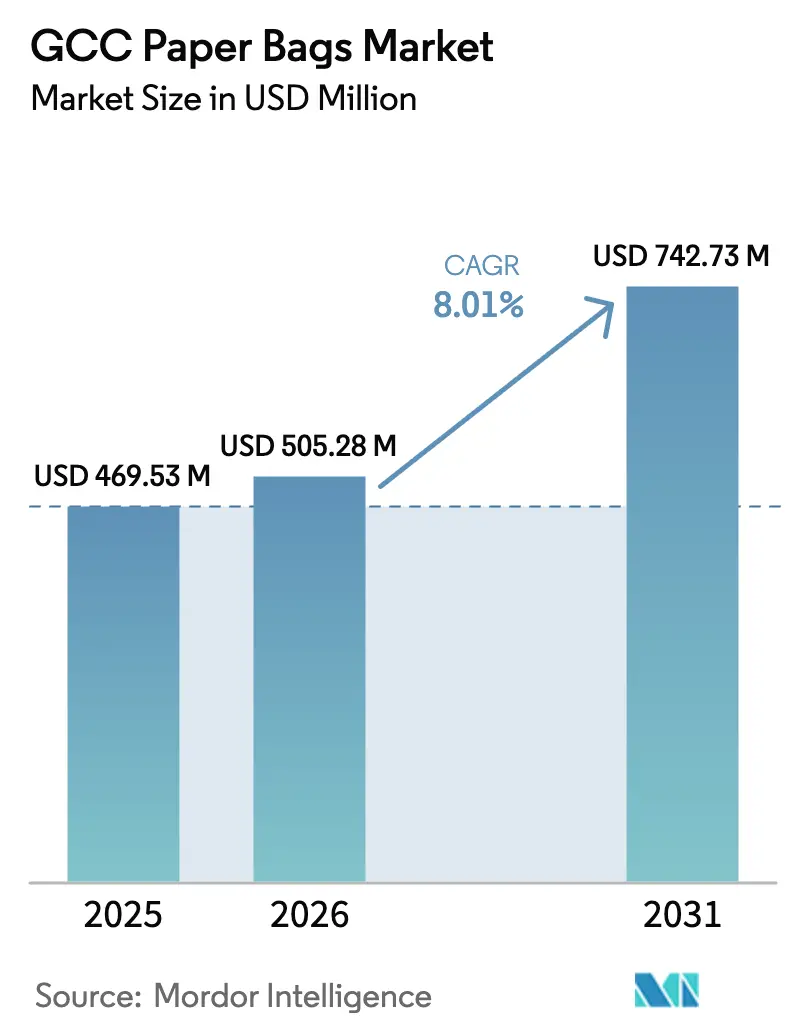

| Base Year Market Size (2025) | USD 469.53 Million |

| Market Size (2026) | USD 505.28 Million |

| Market Size (2031) | USD 742.73 Million |

| Growth Rate (2026 - 2031) | 8.01% CAGR |

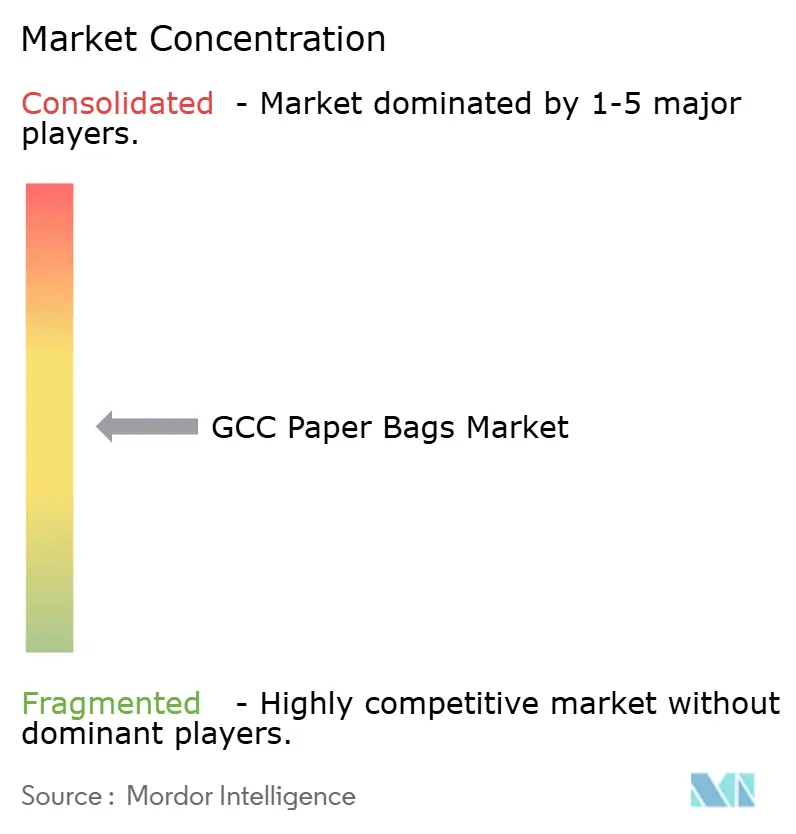

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Paper Bags Market Analysis by Mordor Intelligence

The GCC paper bags market size was valued at USD 469.53 million in 2025 and is estimated to grow from USD 505.28 million in 2026 to reach USD 742.73 million by 2031, at a CAGR of 8.01% during the forecast period (2026-2031). Rising regulatory pressure on single-use plastics, together with retailers’ and food-service operators’ search for easily recyclable packaging, is redirecting bulk purchasing budgets toward kraft paper. Accelerated capacity additions at regional mills are shortening lead times for converters, while integrated e-commerce platforms insist on parcel formats that withstand the humid Gulf climate without compromising brand aesthetics. Brand owners also favor paper substrates that help them meet forthcoming Extended Producer Responsibility targets, pushing converters to differentiate through barrier coatings, multi-ply designs, and ISO-certified quality controls. Capital inflows triggered by Saudi Vision 2030 incentives and the United Arab Emirates’ fast-tracked plastic phase-out timeline compress the investment window, forcing converters to upgrade machinery, secure long-term pulp contracts, and strengthen backward integration. Together, these shifts signal that the GCC paper bags market will remain on a robust growth path, supported by consistent demand from construction, retail, e-commerce, and food-delivery channels.

Key Report Takeaways

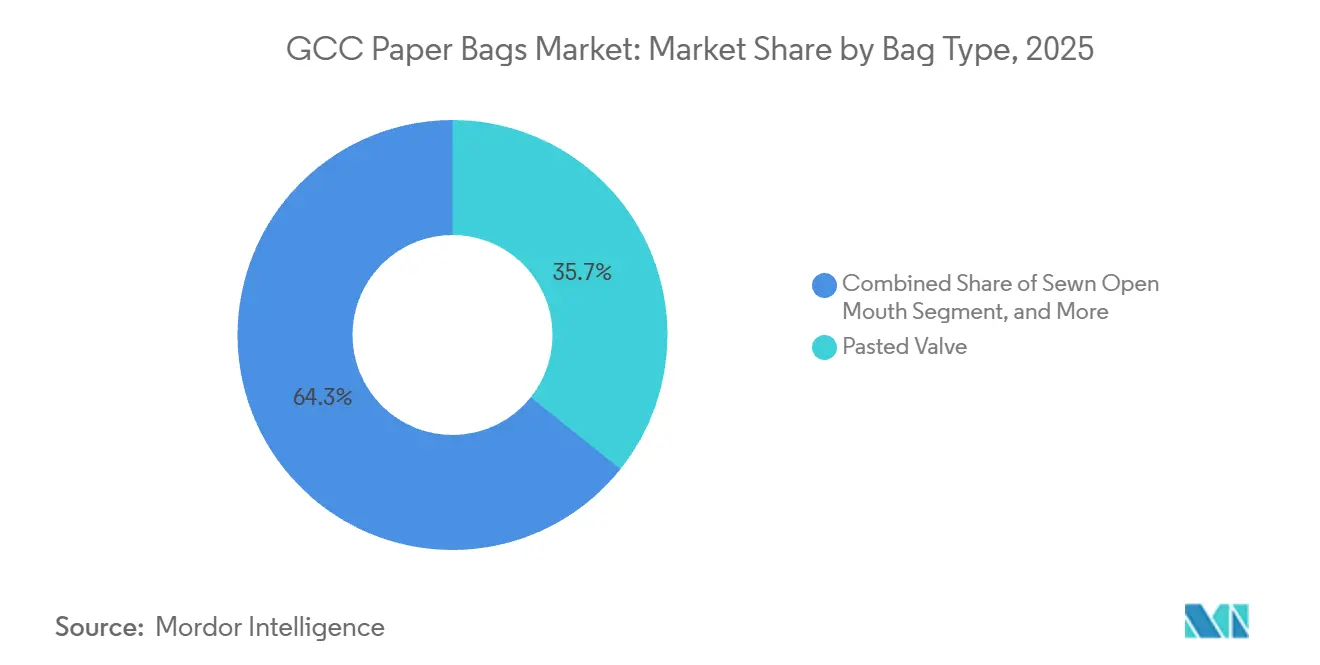

- By bag type, pasted valve bags led with 35.72% of GCC paper bags market share in 2025, while sewn open-mouth bags are projected to expand at a 9.31% CAGR through 2031.

- By material type, brown kraft accounted for 46.79% market share in 2025, whereas coated kraft is forecast to register a 9.57% CAGR to 2031.

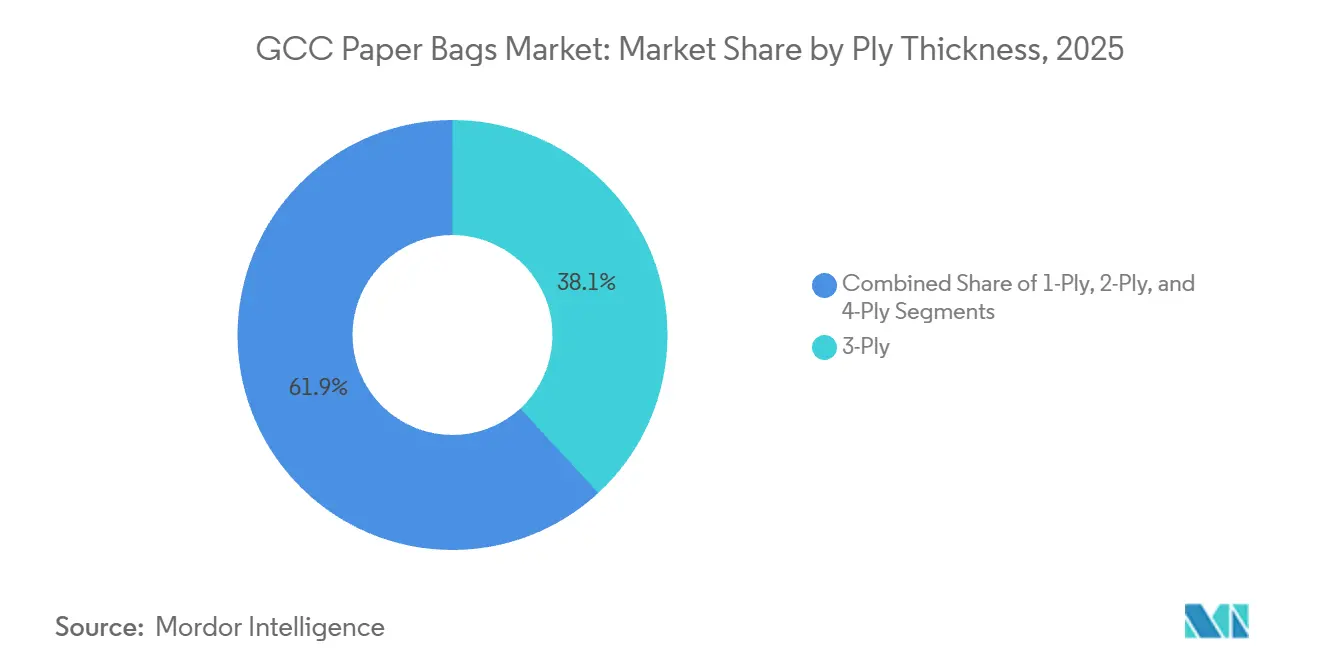

- By ply thickness, the 3-ply segment captured 38.14% of the GCC paper bags market size in 2025, and 4-ply bags are advancing at a 9.22% CAGR during the same period.

- By end user, retail accounted for 32.62% of GCC paper bags market share in 2025, while e-commerce is expected to post the fastest 9.84% CAGR through 2031.

- By geography, Saudi Arabia controlled 42.76% of the GCC paper bags market share in 2025, but the United Arab Emirates is projected to log a 10.08% CAGR, the highest in the region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Paper Bags Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainable-Packaging Regulations Spur Paper Adoption | +2.1% | UAE, Saudi Arabia, Oman | Short term (≤ 2 years) |

| E-Commerce Parcel Growth Fuels Protective Paper Mailers | +1.8% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Vision 2030 Manufacturing Diversification Incentives | +1.4% | Saudi Arabia, spillover to the GCC | Long term (≥ 4 years) |

| Food-Delivery Boom Boosts Takeaway Paper Bags | +1.2% | UAE, Saudi Arabia, Kuwait | Medium term (2-4 years) |

| Date-Palm Fibre-Based Kraft Pulp Pilot Projects | +0.7% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Regional Recycled-Containerboard Capacity Expansions | +0.9% | GCC-wide, led by the UAE and Saudi Arabia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sustainable-Packaging Regulations Spur Paper Adoption

The United Arab Emirates enforced a federal ban on single-use plastic bags in January 2024, compelling retailers and food-service chains to shift procurement to paper carriers. Dubai’s Resolution 124 of 2023 added local penalties that further accelerated conversion timelines. Oman tightened the regional regime through Decision 8/2024, which blocks imports of single-use plastic bags from September 2024.[1]Oman Ministry of Commerce, “Decision 8/2024 on Single-Use Plastic Ban,” moci.gov.om Because implementation windows were short, converters with existing multi-wall capacity captured sudden order spikes while plastic-film specialists lost shelf space.

E-Commerce Parcel Growth Fuels Protective Paper Mailers

Parcel volumes handled by regional fulfillment centers are rising double-digit annually as smartphone adoption, digital payments, and last-mile footprint expand. Online platforms are piloting fully recyclable padded mailers that combine kraft outer layers with cushioning inserts, replacing traditional plastic bubble envelopes. Retrofit programs for automatic mailer-loading equipment are progressing, and several logistics providers are testing humidity-controlled depots to protect paper parcels. Brand owners view curbside recyclability as a marketing edge, increasing willingness to pay a premium for advanced barrier coatings. The result is a virtuous cycle in which higher-value mailer formats elevate both revenue and margin per unit for converters engaged in the GCC paper bags market.

Vision 2030 Manufacturing Diversification Incentives

Saudi Arabia’s Public Investment Fund committed SAR 1.8 billion (USD 480 million) to Middle East Paper Company’s PM5 recycled-containerboard machine, anchoring upstream fiber supply within the Kingdom.[2]Middle East Paper Company, “PM5 Project Announcement,” mepco.com.saThe project supports Vision 2030 goals to localize industrial inputs and trim import exposure.As new tonnage ramps, converters expect shorter lead times and lower freight costs for kraft linerboard moving into the wider Gulf.

Food-Delivery Boom Boosts Takeaway Paper Bags

Cloud kitchens and aggregator platforms are multiplying order frequency, demanding grease-resistant, brandable bags that survive 30-minute rides in 40 °C coastal heat. Quick-service restaurants are standardizing on coated kraft grades that block oil stains yet remain fully recyclable. Fold-over handles and reinforced bottoms are now specified to avoid accidental spillage during motorcycle delivery. As platform algorithms reward outlets with higher packaging quality scores, restaurants treat premium paper bags as part of customer-experience budgets rather than expendable costs. The near-term result is a sales surge for converters offering moisture-barrier coatings certified for direct food contact.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Wood-Pulp Prices and Import Dependence | -1.4% | GCC-wide, with acute exposure in UAE and Qatar | Short term (≤ 2 years) |

| Competition from Reusable PP and Cotton Tote Bags | -0.9% | UAE and Saudi Arabia premium retail channels | Medium term (2-4 years) |

| Weak GCC Paper-Recycling Logistics Network | -0.5% | GCC-wide, most acute in Oman and Qatar | Medium term (2-4 years) |

| Gulf Humidity Challenges Bag Integrity in Wet Uses | -0.3% | UAE, Qatar, coastal Saudi Arabia, Oman | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Wood-Pulp Prices and Import Dependence

Regional converters still import the bulk of virgin fiber, tying their cost base to global commodity cycles. Recent mill closures in North America tightened supply, pushing spot kraft prices to multi-year highs just as converters quoted fixed-price tenders for supermarket chains. Freight surcharges from Asia added further pressure, and not all customers accept quarterly price escalators. Smaller converters with limited inventory buffers face working-capital strain, occasionally resorting to short-weighting or delayed deliveries that erode buyer trust. Unless upstream pulp self-sufficiency accelerates, margin volatility will continue to cap near-term profitability in the GCC paper bags market.

Competition from Reusable PP and Cotton Tote Bags

Abu Dhabi’s awareness campaign helped slash single-use plastic bag consumption by 95% since 2022 and spurred a 2 000% increase in reusable bag adoption.[3]Abu Dhabi Government, “Sustainability Initiatives,” abudhabi.aeA 2024 knowledge, attitude, practice survey found 47.1% of UAE consumers would switch to reusable bags if incentives were offered. Major supermarket chains such as Lulu and Carrefour now promote branded polypropylene totes at checkout and award extra loyalty points to customers who bring them back on subsequent visits. Retail buyers note that monthly paper-bag orders for premium outlets fell by 12% after tote-bag promotions launched in mid-2025, signaling a measurable channel shift toward durable carriers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bag Type: Performance-Driven Shift Toward Multi-Function Formats

Pasted valve formats, holding 35.72% of GCC paper bags market share in 2025, stayed dominant because cement producers require dust-tight seals compatible with rotary packers. Construction mega-projects such as NEOM and The Red Sea Project consume millions of 50-kilogram units monthly, anchoring baseline volumes. Downstream, the sewn open mouth segment is forecast to post a 9.31% CAGR, propelled by animal-feed and grain processors that value tamper-evident stitching for traceability audits. Flat bottom variants, which stand upright on retail shelves, are carving out niche demand from premium coffee roasters and specialty pet food. Pinched bottom open mouth bags serve dry commodities like flour and sugar, offering a compromise between cost and burst strength. The proliferation of bag-type SKUs encourages converters to invest in modular lines that switch quickly among sealing options, improving asset utilization.

Second-generation equipment imported from Europe allows one plant to alternate between pasted valve and pinch-bottom designs within a single shift, smoothing order peaks. Digital die-cutting combined with inline flexographic presses accelerates custom branding for mid-volume jobs, a feature appreciated by e-commerce sellers launching limited-edition merchandise. In parallel, quality inspectors deploy machine-vision cameras to verify glue application and stitch density, reducing rejection rates. These productivity gains help cushion raw-material price shocks. Market awareness campaigns by packaging institutes also underline the dust-emission benefits of valve bags, persuading regulators to include minimum performance thresholds in new cement-logistics guidelines. All told, evolutionary improvements in bag-type engineering underpin diversified revenue streams for participants in the GCC paper bags market.

By Material Type: Cost Leadership Meets Functional Innovation

Brown kraft retained 46.79% market share in 2025 as its unbleached fibers offer the lowest delivered-cost profile and adequate printability for mass retail. Nevertheless, coated kraft is projected to clock a 9.57% CAGR up to 2031, thanks to proprietary barrier layers that repel grease, moisture, and even oxygen. Quick-service restaurants now specify water-based dispersion coatings, avoiding polyethylene laminations that complicate recycling. Bleached kraft, bright and smooth, remains the substrate of choice for cosmetics gift packs and luxury apparel, but price premiums constrain adoption in grocery carry-outs. Recycled brown kraft sourced from new containerboard machines offsets virgin fiber exposure, soothing ESG scrutiny from corporate buyers.

Converters fine-tune basis weights between 70 g m⁻² and 120 g m⁻² to balance stiffness with foldability in high-speed form-fill-seal systems. Extrusion coaters recently installed in Jeddah can apply dual-layer barriers in one pass, shaving energy consumption by double-digit percentages. Meanwhile, pilot trials for date-palm fiber pulping show early promise, although variability in lignin content complicates bleaching sequences. Intellectual-property filings on bio-based resins further suggest that functional performance and circularity are no longer mutually exclusive. These material-type breakthroughs keep the GCC paper bags market in the spotlight for brand owners chasing both legislative compliance and differentiated shelf presence.

By Ply Thickness: Structural Integrity Drives Premium Upsell

Three-ply constructions captured 38.14% of GCC paper bags market size in 2025, providing the sweet spot between cost and tensile strength for general retail. Four-ply bags, however, are forecast to advance at a 9.22% CAGR as industrial fillers migrate toward higher burst thresholds to mitigate losses from automated palletizers. Two-ply variants still populate the apparel and pharmacy segments where loads are light, but the one-ply category is increasingly relegated to promotional giveaways. Petrochemical players now mandate four-ply multi-wall sacks for polymer granules after field testing showed 18% fewer split seams than three-ply alternatives.

Investment in multi-head slitters and precision pasting units helped regional converters maintain tight ply-weight tolerances, crucial for preventing sheet-curl and lay-flat issues on filling lines. Adhesive suppliers introduced starch blends with faster set-times, boosting line throughput by 10-15% without sacrificing delamination resistance. Parallel R and D explores integrating micro-perforations that allow trapped air to escape during valve-bag filling, further reducing line stoppages. Customers that once balked at the price delta now recognize lifecycle savings from reduced product spillage and fewer downtime incidents. Premiumization by ply thickness thus deepens margin pools across the GCC paper bags market.

By End User: Channel Realignment Favors Digital and Delivery Models

Traditional retail still delivered 32.62% of market share in 2025 as supermarket checkout lanes shifted swiftly from plastic to paper. Volume multipliers include loyalty-card promotions that reward patrons for choosing paper over plastic. The e-commerce cohort is poised for the strongest 9.84% CAGR to 2031 as fashion, electronics, and online grocery scale beyond early-adopter phases. Agricultural and feed operators prefer sewn open mouth and four-ply sacks that guard against humidity in outdoor depots. Food-service brands, facing intense aggregator ratings scrutiny, pay extra for coated Kraft with anti-skid exteriors that reduce delivery bag slippage on scooter racks.

Meanwhile, cosmetics and personal-care boutiques emphasize unboxing theatrics, selecting bleached kraft with ribbon handles to convey premium positioning. Pharmaceutical and specialty-chemical makers rely on pasted open-mouth bags certified under Good Manufacturing Practice, ensuring zero fiber shedding. Each vertical issues distinct technical datasheets, pressuring converters to maintain broad SKU catalogs and rapid artwork changeovers. As omnichannel retail matures, cross-channel brand consistency in material appearance becomes a new purchasing criterion, adding complexity and opportunity to the GCC paper bags market.

Geography Analysis

Saudi Arabia controlled 42.76% of market share in 2025, reflecting unmatched scale in cement, petrochemical, and food-service sectors. Public Investment Fund backing for a new 450,000 t y⁻¹ recycled-containerboard line guarantees domestic kraft liner supply, reducing foreign-exchange leakage and bolstering converter margins. Mega-infrastructure programs funnel predictable order books for pasted valve sacks, while retail chains roll out voluntary plastic-reduction pledges ahead of formal legislation. Rising quick-service restaurant footprints in Riyadh and Jeddah reinforce coated-kraft uptake, and Vision 2030 certifications encourage private investors to fund high-efficiency bag-making lines. Collectively, these developments ensure Saudi Arabia remains the volume anchor for the GCC paper bags market.

The United Arab Emirates is forecast to deliver a rapid 10.08% CAGR through 2031, the highest regional clip. Federal and emirate decrees banning single-use plastic pushed every major retailer into emergency sourcing rounds, sparking a wave of long-term procurement contracts for paper alternatives. E-commerce parcel counts in Dubai soared alongside last-mile hubs installed for Expo 2020 legacy logistics, driving mailer adoption. Abu Dhabi records a 95% plastic-bag usage reduction, yet paper demand persists because home-delivery and tourism channels still require disposable carriers. Converters with ISO-certified plants near Jebel Ali Free Zone benefit from duty-free upstream pulp imports, underscoring the regulatory-driven dynamics fueling the GCC paper bags market.

Qatar, Oman, Kuwait, and Bahrain form a secondary growth cluster, lifted by synchronized sustainability agendas but constrained by smaller populations. Oman’s ban on plastic-bag imports effective September 2024 opened an immediate supply gap that paper makers quickly filled, though local converting capacity remains limited. Qatar leverages liquefied natural gas revenues to modernize retail and hospitality venues, translating into upgraded packaging specifications. Kuwait and Bahrain follow suit, aligning standards with regional peers to streamline cross-border trade. Given these trends, converters operating dual hubs in Saudi Arabia and the United Arab Emirates can serve peripheral Gulf states via consolidated distribution centers, ensuring that geography-based demand fragmentation does not erode economies of scale for the GCC paper bags market.

Competitive Landscape

The GCC paper bags market is moderately fragmented. Global packaging majors such as Mondi, Smurfit Westrock, and International Paper compete head-to-head with regional specialists such as Hotpack, Gulf East Paper, and Middle East Paper Company. Multinationals leverage vertical integration, owning pulp, paper, and converting assets that safeguard raw-material flow and stabilize unit economics. For instance, Mondi’s EUR 1.2 billion (USD 1.36 billion) expansion in Czechia added 210,000 t y⁻¹ of kraft capacity, enabling one-stop sourcing for Gulf importers. Smurfit Westrock’s 2024 mega-merger pooled 63 mills and more than 500 converting plants, promising standardized ESG audits that appeal to multinational brand owners.

Regional champions counter by embedding localized service, faster turnaround, and Arabic-language artwork capabilities. Hotpack’s AED 350 million (USD 95 million) plant in Malaysia hedges pulp supply risk and creates a cost-competitive export base, while its planned SAR 1 billion (USD 267 million) Saudi unit shortens delivery cycles to inland projects. Middle East Paper Company’s recycled-containerboard line secures feedstock for captive bag plants, compressing lead times and insulating against pulp volatility. Smaller converters differentiate through digital printing for limited runs and boutique designs targeting cosmetics shops.

Asian pulp surpluses threaten to unleash a wave of discounted containerboard into the Gulf, pressuring converters without backward integration. Consequently, several mid-tier players court private-equity funding to acquire minority stakes in pulp mills or negotiate long-term supply agreements. Technology adoption accelerates as machine-vision quality control, real-time moisture monitoring, and automated palletizers migrate from European benchmarks into Gulf plants. Compliance certificates under ISO-9001 and ISO-14001 are now table stakes for government and multinational tenders, erecting formal entry barriers. Overall, rivalry centers on cost leadership versus functional specialization, positioning the GCC paper bags market firmly in the moderate-fragmentation zone.

GCC Paper Bags Industry Leaders

Huhtamaki Flexibles UAE

Hotpack Packaging Industries LLC

Gulf East Paper & Plastic Industries LLC

Al Zaini Converting Industries

Falcon Pack Industries LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Mondi commissioned a 210,000 t y⁻¹ kraft paper machine at Štětí, reinforcing its integrated kraft and bag operations and widening product options for Gulf importers.

- January 2025: International Paper finalized its USD 9.9 billion acquisition of DS Smith, creating a larger corrugated-packaging and paper-bag platform able to serve multinational customers across Europe, the Middle East, and the Gulf.

- December 2024: Hotpack announced an AED 350 million (USD 95 million) investment in a Malaysian manufacturing facility to diversify supply chain risk and serve Southeast Asian demand.

- November 2024: Huhtamaki Flexibles UAE merged three local sites into two, trimming overheads and upgrading machinery for higher throughput.

GCC Paper Bags Market Report Scope

The study covers the paper bag market, tracked by consumption and sales of paper bags offered by various vendors.

The GCC Paper Bags Market Report is Segmented by Bag Type (Flat Bottom, Pasted Valve, Pinched Bottom Open Mouth, Pasted Open Mouth, and Sewn Open Mouth), Material Type (Brown Kraft, Bleached or White Kraft, Coated Kraft, and Recycled Brown Kraft), Ply Thickness (1-Ply, 2-Ply, 3-Ply, and 4-Ply), End User (Retail, Agriculture and Animal Feed, Food Service, Cosmetics and Personal Care, E-Commerce, and Other End Users), and Country (Saudi Arabia, Oman, United Arab Emirates, Qatar, and Rest of GCC). The Market Forecasts are Provided in Terms of Value (USD).

| Flat Bottom |

| Pasted Valve |

| Pinched Bottom Open Mouth |

| Pasted Open Mouth |

| Sewn Open Mouth |

| Brown Kraft |

| Bleached/White Kraft |

| Coated Kraft |

| Recycled Brown Kraft |

| 1-Ply |

| 2-Ply |

| 3-Ply |

| 4-Ply |

| Retail |

| Agriculture and Animal Feed |

| Food Service |

| Cosmetics and Personal Care |

| E-Commerce |

| Other End Users |

| Saudi Arabia |

| Oman |

| United Arab Emirates |

| Qatar |

| Rest of GCC |

| By Bag Type | Flat Bottom |

| Pasted Valve | |

| Pinched Bottom Open Mouth | |

| Pasted Open Mouth | |

| Sewn Open Mouth | |

| By Material Type | Brown Kraft |

| Bleached/White Kraft | |

| Coated Kraft | |

| Recycled Brown Kraft | |

| By Ply Thickness | 1-Ply |

| 2-Ply | |

| 3-Ply | |

| 4-Ply | |

| By End User | Retail |

| Agriculture and Animal Feed | |

| Food Service | |

| Cosmetics and Personal Care | |

| E-Commerce | |

| Other End Users | |

| By Country | Saudi Arabia |

| Oman | |

| United Arab Emirates | |

| Qatar | |

| Rest of GCC |

Key Questions Answered in the Report

How large is the GCC paper bags market in 2026?

The GCC paper bags market size is estimated at USD 505.28 million in 2026.

What growth rate is forecast for GCC paper bags through 2031?

The market is projected to advance at an 8.01% CAGR between 2026 and 2031.

Which bag type currently commands the greatest share?

Pasted valve designs led with 35.72% of 2025 shipments, anchored by cement logistics.

Why is coated kraft demand rising quickly?

Quick-service restaurants and parcel shippers need grease- and moisture-resistant barriers that coated kraft provides, fueling a forecast 9.57% CAGR.

Which country will expand the fastest?

The United Arab Emirates is set to grow at a 10.08% CAGR through 2031, propelled by stringent plastic bans and booming e-commerce.

What is the principal restraint facing converters?

Volatile imported wood-pulp prices compress margins for firms lacking backward integration.

Page last updated on: