Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

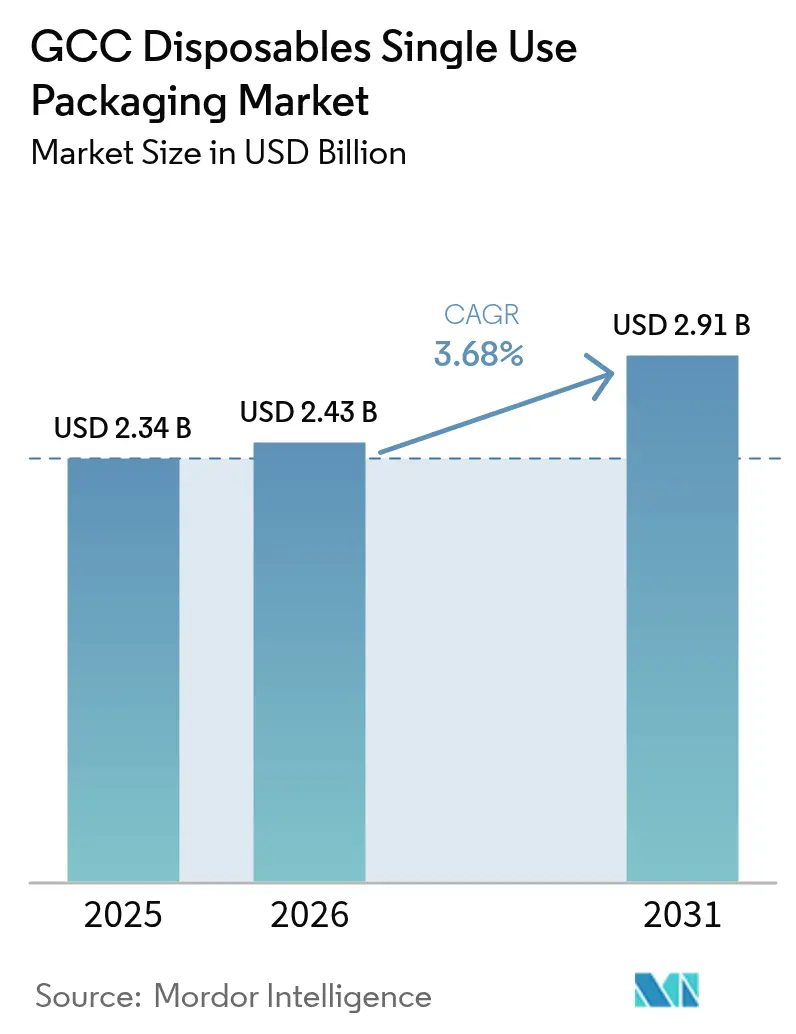

| Base Year Market Size (2025) | USD 2.34 Billion |

| Market Size (2026) | USD 2.43 Billion |

| Market Size (2031) | USD 2.91 Billion |

| Growth Rate (2026 - 2031) | 3.68% CAGR |

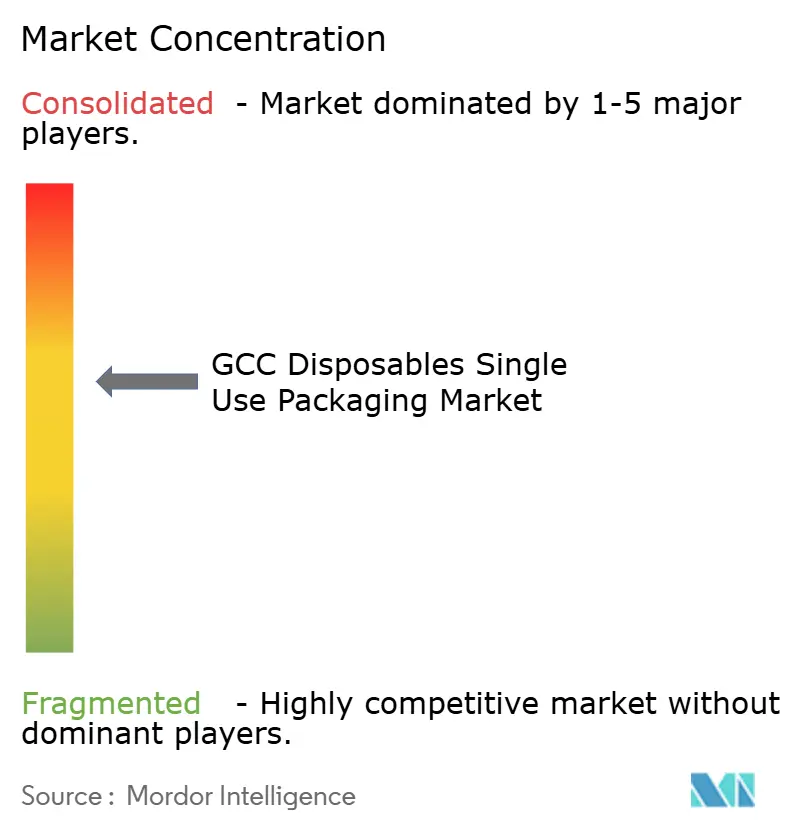

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Disposables Single Use Packaging Market Analysis by Mordor Intelligence

GCC disposables single use packaging market size in 2026 is estimated at USD 2.43 billion, growing from 2025 value of USD 2.34 billion with 2031 projections showing USD 2.91 billion, growing at 3.68% CAGR over 2026-2031. This steady growth is anchored by tourism-led food service expansion, rapid e-commerce penetration, and regulatory mandates that accelerate the pivot toward compostable and recyclable formats. Government hospitality projects generate large-volume demand, while coffee culture has strengthened the cups and lids segment. Simultaneously, extended producer responsibility fees and single-use plastic bans are tilting procurement toward bagasse, molded fiber, and hybrid solutions. Supply chains are re-aligning around regional PLA production, and logistics investments at Jebel Ali and Jeddah Logistics Park are reducing lead times for imported substrates.[1]U.S. Embassy, “Logistics,” uae-embassy.org Price sensitivity still favors traditional polymers, yet brand owners increasingly pay premiums for certified eco-friendly alternatives to mitigate future compliance risk.

Key Report Takeaways

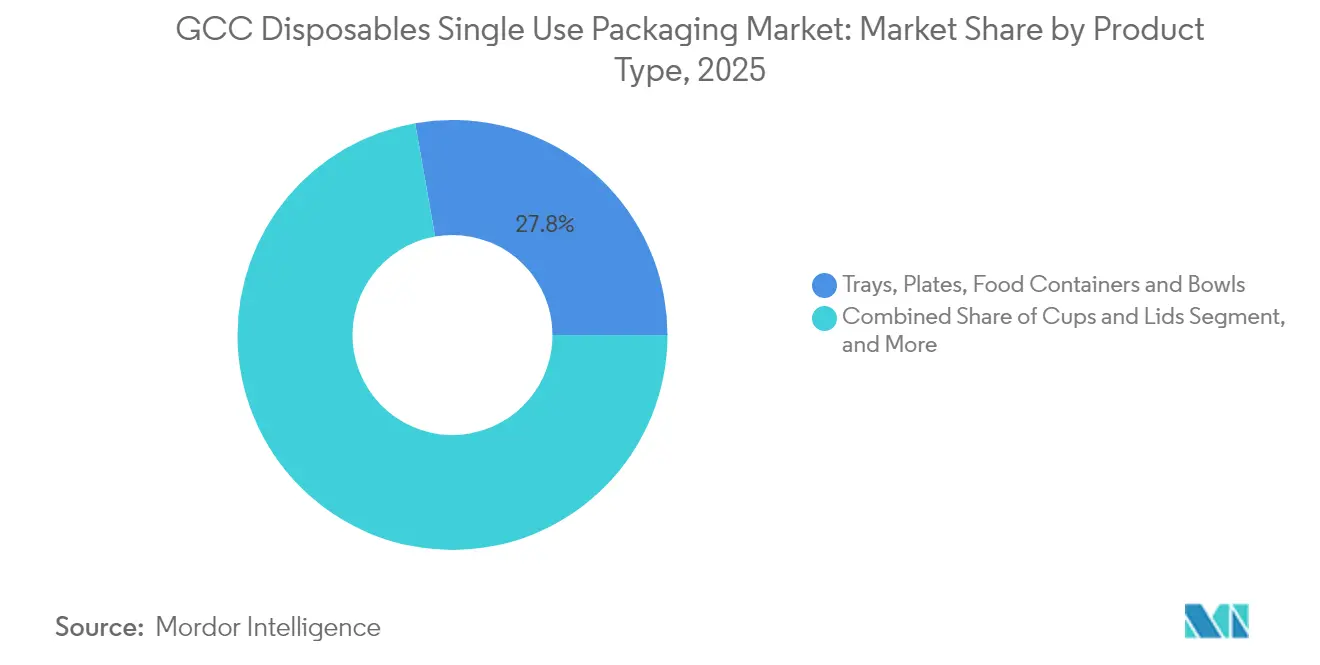

- By product type, trays, plates, food containers, and bowls captured 27.78% of the GCC disposables single-use packaging market share in 2025.

- By end-user application, the GCC disposables single-use packaging market size for the coffee and snack outlets segment is projected to grow at a 5.53% CAGR between 2026-2031.

- By packaging format, flexible solutions captured 41.25% of the GCC disposables single-use packaging market share in 2025.

- By material type, the GCC disposables single-use packaging market size for the bagasse and plant-based fibers segment is projected to grow at a 6.55% CAGR between 2026-2031.

- By country, Saudi Arabia captured 28.74% of the GCC disposables single-use packaging market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Disposables Single Use Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory-driven bans on single-use plastics (UAE 2026 ban) | +1.2% | UAE primary, spillover to Saudi Arabia and Qatar | Medium term (2-4 years) |

| Explosive growth of online food delivery apps across GCC | +0.8% | Regional, strongest in Saudi Arabia and UAE urban centers | Short term (≤ 2 years) |

| Rapid expansion of QSR and café chains backed by Vision 2030 tourism push | +0.7% | Saudi Arabia and UAE core, expansion to Qatar and Kuwait | Long term (≥ 4 years) |

| Rising demand for hygienic packaging in healthcare, Hajj and mass-event catering | +0.5% | Saudi Arabia primary (Hajj), regional healthcare expansion | Medium term (2-4 years) |

| Surge in sustainable materials capacity (bagasse, molded fibre) in UAE and KSA | +0.4% | UAE and Saudi Arabia manufacturing hubs | Long term (≥ 4 years) |

| Logistics re-export hub advantage (Jebel Ali, King Abdullah Port) boosting packaging throughput | +0.3% | UAE and Saudi Arabia trade corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory-driven bans on single-use plastics

The UAE ban effective 2026 mandates food service operators to transition to recyclable or compostable substrates that meet Al Sa'fat criteria. Manufacturers are accelerating material reformulation programs, with regional PLA capacity reducing reliance on Asian imports.[2]Dubai Municipality, “Al Sa'fat Certification Framework,” dm.gov.ae Multinational QSR chains are standardizing GCC-wide specifications to streamline sourcing, which is expected to amplify demand for molded fiber trays and water-based barrier coatings. Saudi Arabia’s Waste Management Law is adding fee pressure on non-recyclable formats, reinforcing the competitive edge of compliant alternatives. Early adopters with credible environmental certifications are already commanding price premiums of 8-10% over legacy plastic SKUs.

Explosive growth of online food delivery apps

Food aggregators now account for a double-digit share of restaurant revenue, and their packaging specifications privilege leak-proof, thermal-retentive containers that survive desert heat profiles. Demand has surged for multi-compartment clamshells, dual-layer paper bowls, and tamper-evident lids that preserve freshness during 30-minute average transit windows. Each delivered meal generates more discrete packs than dine-in service, multiplying unit volumes sold per transaction. Platform contracts increasingly bundle service-level penalties tied to packaging failure rates, prompting converters to adopt higher-gauge laminates and QC automation. Innovations such as time-temperature labels are entering pilot trials to bolster consumer confidence in delivered food safety.

Rapid expansion of QSR and café chains

Vision 2030 hospitality investments foresee 320,000 new hotel rooms and a proliferation of global food brands across mega-projects in Riyadh, Jeddah, and the Red Sea corridor. Alshaya Group alone targets 3,000 Starbucks outlets by 2028, underpinning robust demand for insulated paper cups and molded fiber cup carriers. Café chains prize aesthetic differentiation, catalyzing orders for custom-printed lids and textured sleeves. In malls and transit hubs, fast casual formats are blending dine-in and takeaway, increasing the share of disposable serviceware per customer. Suppliers that align print quality, supply reliability, and sustainability credentials are capturing high-margin long-term agreements.

Rising demand for hygienic packaging in healthcare, Hajj and mass-event catering

Annual Hajj catering for over 2 million pilgrims requires sterile, stackable meal boxes that withstand high ambient temperatures without leaching chemicals. Healthcare reforms and new medical cities have raised baseline specifications for antimicrobial coatings and double-sealed pouches. Institutional buyers are awarding contracts to vendors with ISO 22000 and HACCP certification, lifting barriers to entry for smaller converters. Mass-event organizers favor portion-controlled packs that ease rapid distribution, encouraging innovation in corrugated dispenser sleeves and pre-attached cutlery kits. These specialized SKUs carry premium margins that offset the added cost of medical-grade resins and coatings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating compliance cost from EPR pilots and eco-fees | -0.6% | Regional, strongest impact in UAE and Saudi Arabia | Medium term (2-4 years) |

| Limited commercial composting and recycling infrastructure in GCC | -0.4% | Regional, particularly acute in smaller GCC states | Long term (≥ 4 years) |

| Petro-feedstock price volatility squeezing resin margins | -0.3% | Regional, affecting plastic packaging manufacturers | Short term (≤ 2 years) |

| Consumer perception shift toward reusables in premium dining | -0.2% | UAE and Qatar premium segments, spillover to Saudi Arabia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating compliance cost from EPR pilots and eco-fees

EPR registration, audit, and fee payments projected at USD 200-400 per tonne for plastic packaging are squeezing manufacturer margins. Larger groups amortize these costs across diversified portfolios, but SMEs with single-line operations face price undercutting risks. When non-recyclable items incur higher multipliers, buyers renegotiate supply contracts quarterly to hedge fee volatility, creating forecasting challenges for converters. Some suppliers are shifting toward toll manufacturing models in free-trade zones to mitigate mainland fee exposure, yet the administrative burden remains. Over the medium term, the fee differentials are expected to accelerate the exit of commodity plastics in favor of substrate mixes with lower fee classes.

Limited commercial composting and recycling infrastructure

Recycling capacity processes only 10% of regional packaging waste, and industrial composting is nascent outside select UAE and Saudi pilot sites.[3]Dubai Municipality, “Waste Processing Statistics,” dm.gov.ae Without downstream infrastructure, the environmental advantage of compostable packs is muted, undermining customer ROI. Import dependence on recycled PET and r-HDPE exacerbates supply volatility, while land-blocking for new MRFs competes with high-value real estate development. Smaller GCC states lack the waste streams to justify large-scale facilities, prompting cross-border waste transfers that inflate logistics costs. Until infrastructure investment catches up, the circularity narrative will remain aspirational, restraining near-term conversion to higher-cost biodegradable substrates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Beverage-led growth reshapes portfolio

Trays, plates, food containers, and bowls retained leadership in the GCC disposables single-use packaging market with 27.78% share in 2025, fueled by institutional catering contracts linked to mega-events and expansive hotel pipelines. The segment benefits from volume contracts that stabilize baseline plant utilization across converters. Simultaneously, cups and lids exhibit a 5.55% CAGR due to burgeoning café chains and premium ready-to-drink beverage launches. GCC disposables single-use packaging market size for cups is forecast to add more than 650 million additional units annually by 2031. Suppliers are responding with double-wall cups and ripple-textured sleeves that reduce heat transfer, while fiber-based lids are entering commercial production to replace polystyrene tops.

Across smaller SKUs, straws, stirrers, and cutlery confront outright bans or fee surcharges in the UAE, spurring a pivot toward bamboo and coated wood. Clamshell designs tailored for online delivery platforms now incorporate ventilated lids to release steam, preventing soggy fried foods. Rigid box formats for gourmet desserts employ PET windows laminated to kraft board for premium shelf appeal. The product mix evolution underscores a dual mandate of performance and sustainability, forcing manufacturers to balance stock-keeping complexity with economies of scale.

By End-user Application: Convenience channels surge

Quick service restaurants held the largest slice of the GCC disposables single-use packaging market size at 32.11% in 2025, supported by franchised burger, fried chicken, and pizza operators rolling out across secondary cities. Nonetheless, coffee and snack outlets are poised for the fastest 5.53% CAGR, driven by Millennials and Gen Z who frequent grab-and-go formats. The GCC disposables single-use packaging market share captured by cafés is expanding as chains demand bespoke cup graphics and seasonal, limited-edition sleeves.

Full-service restaurants, though slower growing, are upgrading to molded fiber table-ready bowls for takeout orders that preserve plating aesthetics. Retail prepared-food counters in hypermarkets now seek re-heatable trays compatible with in-store rotisseries. Institutional segments, notably hospitals and universities, specify color-coded lids to segregate dietary requirements, pushing customization depth. Overall, end-user heterogeneity compels converters to operate flexible print lines capable of short runs without cost penalties.

By Material Type: Bio-based acceleration tempered by cost

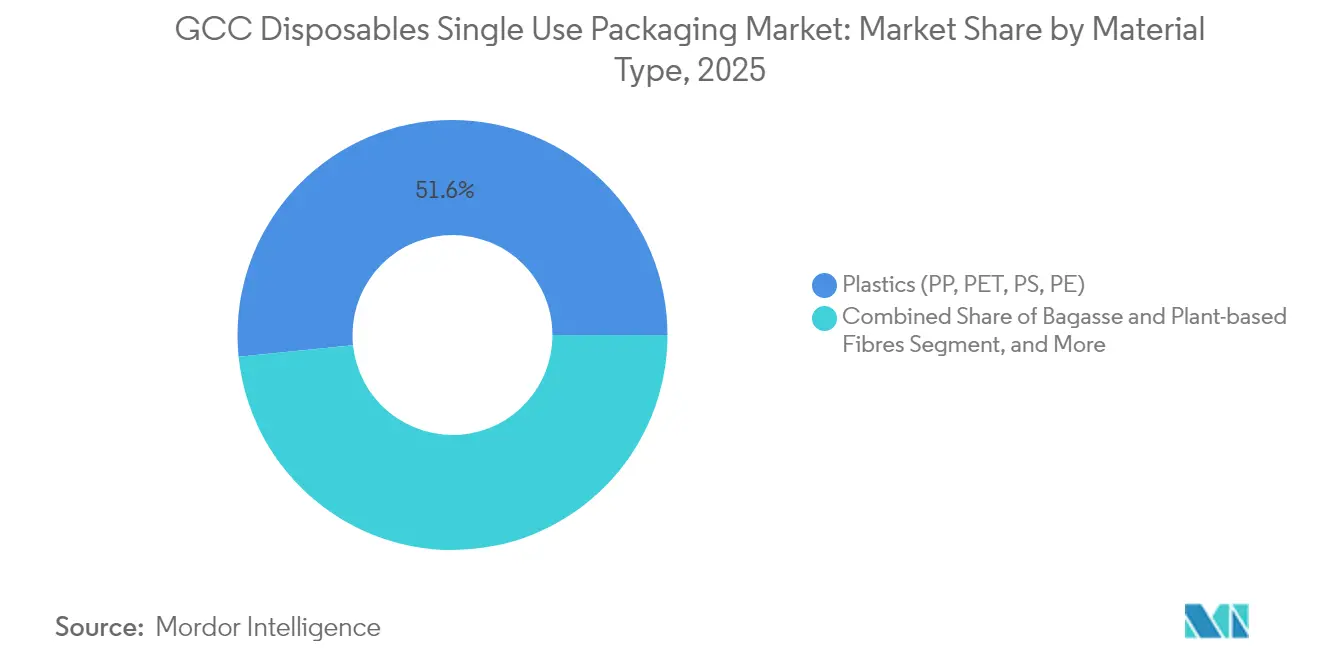

Plastics remained dominant at 51.62% GCC disposables single-use packaging market share in 2025, leveraging unmatched barrier properties and attractive unit economics. Yet the GCC disposables single-use packaging market size for bagasse and plant-based fibers is set to climb at a 6.55% CAGR through 2031 as regional PLA capacity comes online. Bagasse pulp, sourced from Saudi sugar refineries, underpins thermoformed clamshells that withstand microwave reheating. Paperboard cup stock laminated with water-based coatings has emerged as a recyclable alternative to PE-lined cups that hinder fiber recovery.

Wood and bamboo dominate cutlery conversions where mechanical strength offsets marginally higher costs. Aluminum foil trays persist in airline and mass-event catering where thermal shock resistance is critical. Hybrid structures, such as kraft paper with EVOH nano-barriers, aim to bridge plastic-like performance with 90% fiber content to qualify for lower EPR fees. In the medium term, material selection will hinge on a three-factor calculus: fee exposure, performance risk, and consumer perception.

By Packaging Format: Hybrid rises as a compliance facilitator

Flexible packs controlled a 41.25% share in 2025, prized for cube optimization and low logistics weight. However, hybrid formats that marry paper substrates with ultra-thin polymer coatings are projected to post a 5.74% CAGR, creating a sweet spot where converters meet recyclability thresholds without sacrificing moisture barriers. GCC disposables single-use packaging market size captured by hybrid pouches is forecast to double by 2031 as retailers pilot kerbside-recyclable prepared-meal bags.

Rigid polypropylene bowls remain entrenched in high-temperature applications, yet mono-material PET trays with heat-resistant crystallized bases are displacing multi-layer laminates. Active and intelligent packaging, while niche, is winning airline and hospital tenders that favor time-temperature indicators to minimize spoilage. As EPR fees tighten, format decisions increasingly revolve around fee tier classification and downstream sorting compatibility.

Geography Analysis

Saudi Arabia accounted for 28.74% of the GCC disposables single-use packaging market in 2025, propelled by a large domestic consumption base and Vision 2030 tourism megaprojects that demand high-volume serviceware. The kingdom’s plan to welcome 100 million annual visitors by 2030 is fostering sustained orders across hotel, entertainment, and quick service chains. Food delivery growth in Riyadh and Jeddah has pushed suppliers to design heat-retentive clamshells and leak-proof soup cups suitable for motorcycle couriers. The USD 240 million Jeddah Logistics Park, slated for completion in 2026, will improve cold-chain throughput for temperature-sensitive packaging substrates.

The United Arab Emirates is projected to log the fastest 4.36% CAGR, underpinned by a 2026 single-use plastic ban that is accelerating demand for certified compostable SKUs. Dubai Municipality’s Al Sa'fat framework is already influencing procurement, with importers favoring goods that carry cradle-to-cradle documentation. The world’s largest PLA plant in Abu Dhabi positions the country as a regional hub for bio-polymer supply, cutting lead times versus Asian imports. Jebel Ali Port’s connectivity supports re-export trade, enabling converters to balance domestic and overseas order books rapidly. Qatar, buoyed by post-World-Cup hospitality assets, is adopting premium packaging aesthetics in gourmet stadium eateries. Kuwait’s mature retail sector is trialing smart labels that monitor cold-case temperature excursions. Oman’s Duqm port expansion is catalyzing logistics corridors that benefit small-batch specialty packaging producers. Bahrain, despite a smaller footprint, serves as an innovation sandbox where beverage brands test fiber-based cup linings before scaling to neighboring markets. Collectively, these countries contribute incremental demand that favors agile converters capable of tailoring SKU assortments to varied regulatory and consumer preferences.

Competitive Landscape

The GCC disposables single use packaging market exhibits moderate fragmentation with more than 200 active converters, yet competitive intensity is sharpening as sustainability credentials become table stakes. Hotpack Packaging leverages region-wide distribution and price leadership to defend share in commodity PET lids, while Huhtamaki deploys its global R&D muscle to introduce lightweight fiber trays with grease-resistant coatings. Amcor’s merger with Berry Global in March 2025 created a USD 24 billion packaging giant that is cross-licensing bio-barrier patents across its GCC plants to outflank niche players.

Sabert Corporation’s Pulp Ultra launch in September 2025 demonstrated performance parity between thermoformed fiber and PP containers, unlocking new airline and premium catering accounts. Local mid-tier firms are investing in digital flexo presses to deliver short-run branded sleeves for café chains seeking seasonal designs. Strategic partnerships with waste-management firms are emerging as converters seek closed-loop collection streams to secure r-PET and r-HDPE inputs at predictable prices. Over the next five years, consolidation is likely among sub-scale PE thermoformers unable to finance EPR compliance and food-contact migration testing.

GCC Disposables Single Use Packaging Industry Leaders

Jebel Pack LLC

Detpak - Detmold Group

Falcon Pack

Precision Plastic Products Co. (LLC)

Freshpack LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Sabert Corporation appointed its first Chief Sustainability Officer and unveiled Pulp Ultra fiber containers targeting food service clients.

- August 2025: Dubai Municipality issued updated Al Sa'fat guidelines, clarifying compostability verification protocols for disposable serviceware.

- July 2025: Alshaya Group reported progress toward 3,000 Starbucks outlets by 2028, reinforcing demand for custom paper cups

- June 2025: DP World and Saudi Ports Authority broke ground on the USD 240 million Jeddah Logistics Park to bolster refrigerated packaging distribution.

GCC Disposables Single Use Packaging Market Report Scope

The study tracks the demand for disposable packaging options in terms of sales offered by various vendors operating in the GCC region. The impact of COVID-19 has also been considered for current market estimation and future growth projections. The study on GCC disposable packaging Market tracks demands for Trays, Plates, Food Containers, and Bowls, Boxes and Carton, Bottles, Cups and Lids on the high level while it tracks the market size in terms of revenue for the respective end-user industry verticals in the respective countries from the listed product types.

The GCC disposables (single-use) packaging market is segmented by product type (trays, plates, food containers, & bowls, boxes & cartons, bottles, cups & lids, clamshells, bags & wraps), end-user applications (quick service restaurants, full-service restaurants, coffee and snack outlets, retail establishments, institutional and hospitality), and by Country (United Arab Emirates, Saudi Arabia, Rest of GCC). The report offers market forecasts and size in value (USD) for all the above segments.

By Product Type

| Trays, Plates, Food Containers and Bowls |

| Boxes and Cartons |

| Bottles |

| Cups and Lids |

| Clamshell |

| Bags and Wraps |

| Cutlery, Stirrers, Straws |

By End-user Application

| Quick Service Restaurants |

| Full-Service Restaurants |

| Coffee and Snack Outlets |

| Retail Establishments |

| Institutional and Hospitality |

| Other End-User Applications |

By Material Type

| Plastics (PP, PET, PS, PE) |

| Paper and Paperboard |

| Bagasse and Plant-Based Fibres |

| Wood and Bamboo |

| Aluminium Foil |

By Packaging Format

| Rigid |

| Flexible |

| Hybrid (Paper-Plastic, Laminate) |

| Active and Intelligent |

By Country

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Product Type | Trays, Plates, Food Containers and Bowls |

| Boxes and Cartons | |

| Bottles | |

| Cups and Lids | |

| Clamshell | |

| Bags and Wraps | |

| Cutlery, Stirrers, Straws | |

| By End-user Application | Quick Service Restaurants |

| Full-Service Restaurants | |

| Coffee and Snack Outlets | |

| Retail Establishments | |

| Institutional and Hospitality | |

| Other End-User Applications | |

| By Material Type | Plastics (PP, PET, PS, PE) |

| Paper and Paperboard | |

| Bagasse and Plant-Based Fibres | |

| Wood and Bamboo | |

| Aluminium Foil | |

| By Packaging Format | Rigid |

| Flexible | |

| Hybrid (Paper-Plastic, Laminate) | |

| Active and Intelligent | |

| By Country | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

What is the current value of the GCC disposables single use packaging market?

The sector was valued at USD 2.43 billion in 2026.

How fast is the market expected to grow through 2031?

It is forecast to register a 3.68% CAGR, reaching USD 2.91 billion.

Which product segment is growing the fastest?

Cups and lids, supported by booming café chains, are advancing at a 5.55% CAGR.

What material is gaining share the quickest?

Bagasse and plant-based fibers are expanding at a 6.55% CAGR as regulations favor compostable options.

Which GCC country is projected to record the highest growth?

The United Arab Emirates is expected to post the fastest 4.36% CAGR, driven by its 2026 plastic ban and logistics advantages.

How are EPR fees affecting manufacturers?

Fees ranging from USD 200-400 per tonne for plastic packs are compressing margins and accelerating the shift to lower-fee recyclable or compostable materials.

Page last updated on: