Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

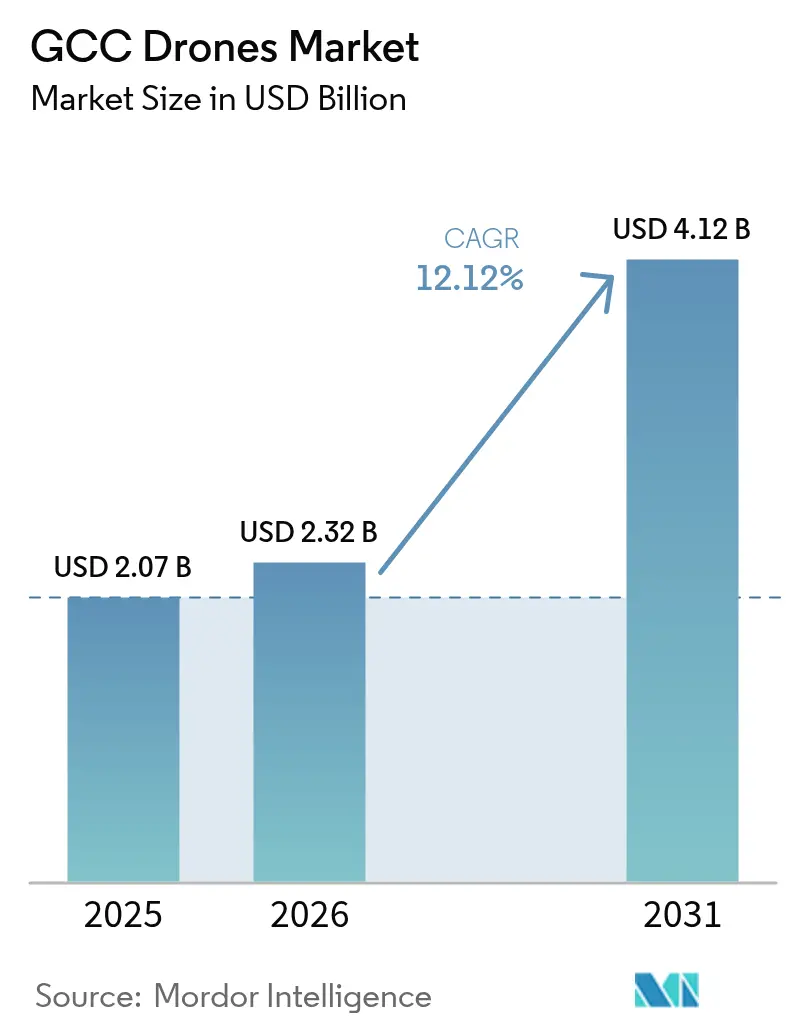

| Base Year Market Size (2025) | USD 2.07 Billion |

| Market Size (2026) | USD 2.32 Billion |

| Market Size (2031) | USD 4.12 Billion |

| Growth Rate (2026 - 2031) | 12.12% CAGR |

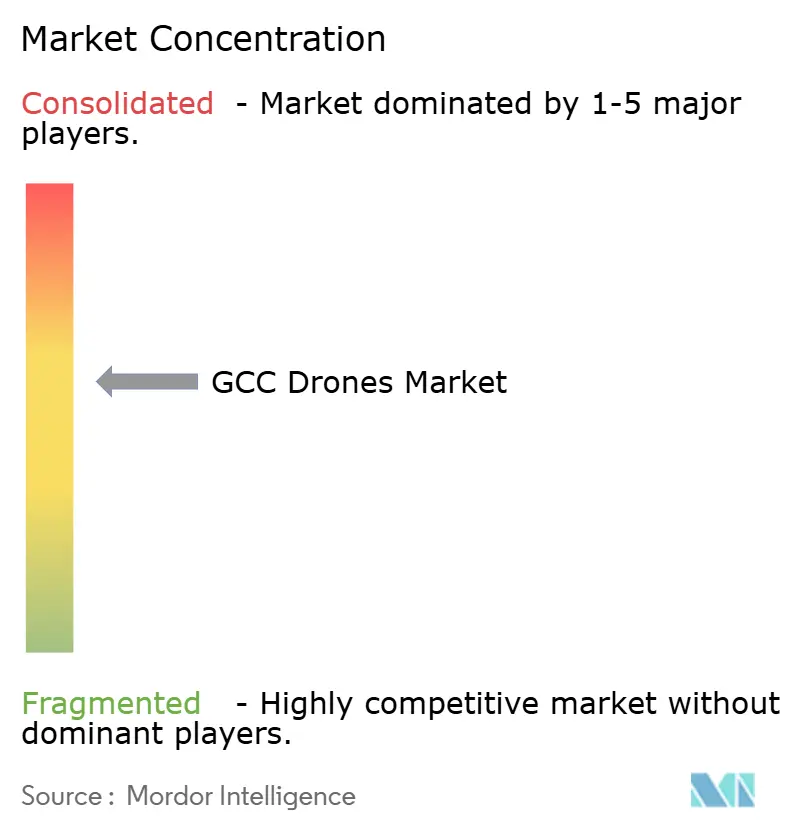

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Drones Market Analysis by Mordor Intelligence

The GCC drone market size is expected to grow from USD 2.07 billion in 2025 to USD 2.32 billion in 2026 and is forecast to reach USD 4.12 billion by 2031 at 12.12% CAGR over 2026-2031. A widening pipeline of giga-infrastructure projects, progressive aviation rules, and the energy sector’s pivot toward autonomous inspection anchor near-term growth. Sovereign wealth funds continue to channel capital into domestic drone manufacturing and AI algorithms, cutting dependence on imported systems while aligning with national Vision 2030 roadmaps. Saudi Arabia and the UAE dominate early adoption thanks to clear regulatory corridors and budget allocations for smart-city and oil-field surveillance. Qatar accelerates on defense-related procurements that spill over into commercial services. Competitive intensity rises as local assemblers partner with international OEMs to satisfy localization mandates. However, fragmented airspace approvals and a shortage of certified pilots temper the GCC drone market’s full potential.

Key Report Takeaways

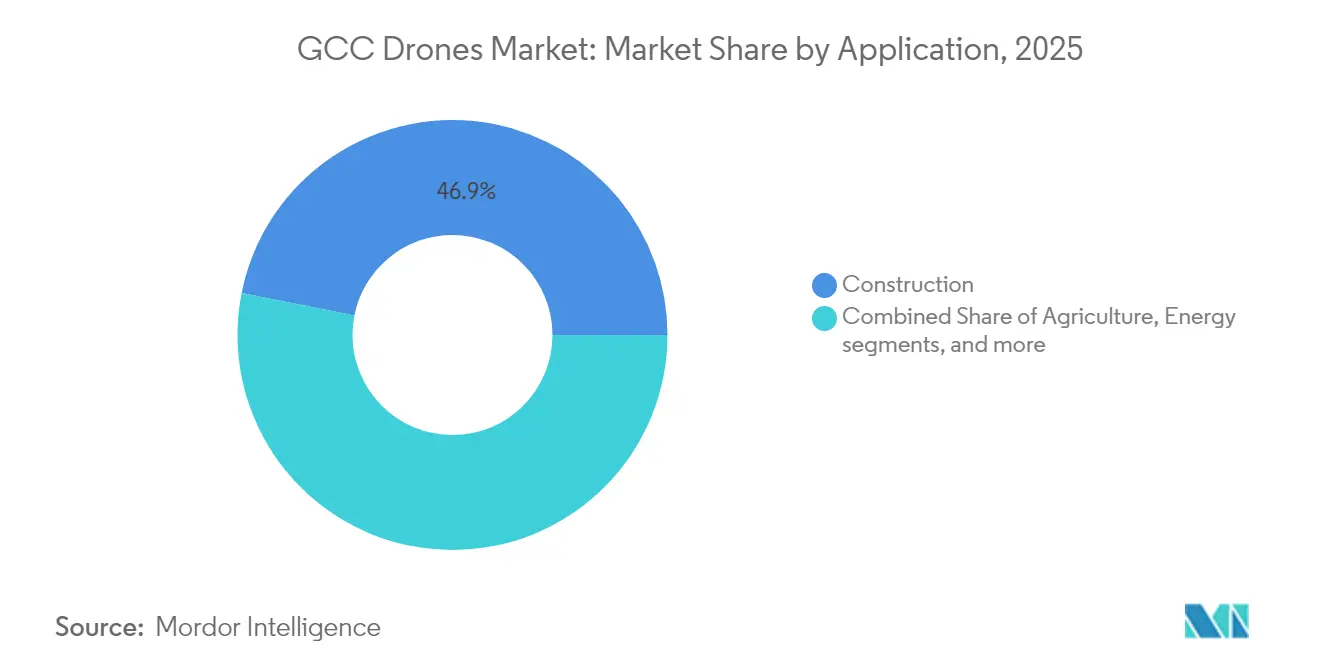

- By application, construction captured 46.88% of the GCC drone market share in 2025, while entertainment is forecasted to expand at a 13.12% CAGR to 2031.

- By type, rotary-wing drones led with 48.62% revenue share in 2025; hybrid/VTOL platforms are projected to grow at a 14.05% CAGR through 2031.

- By weight class, small platforms (2 to 25 kg) accounted for 47.75% of the GCC drone market size in 2025, and medium platforms (25 to 150 kg) are poised for a 13.02% CAGR over 2026-2031.

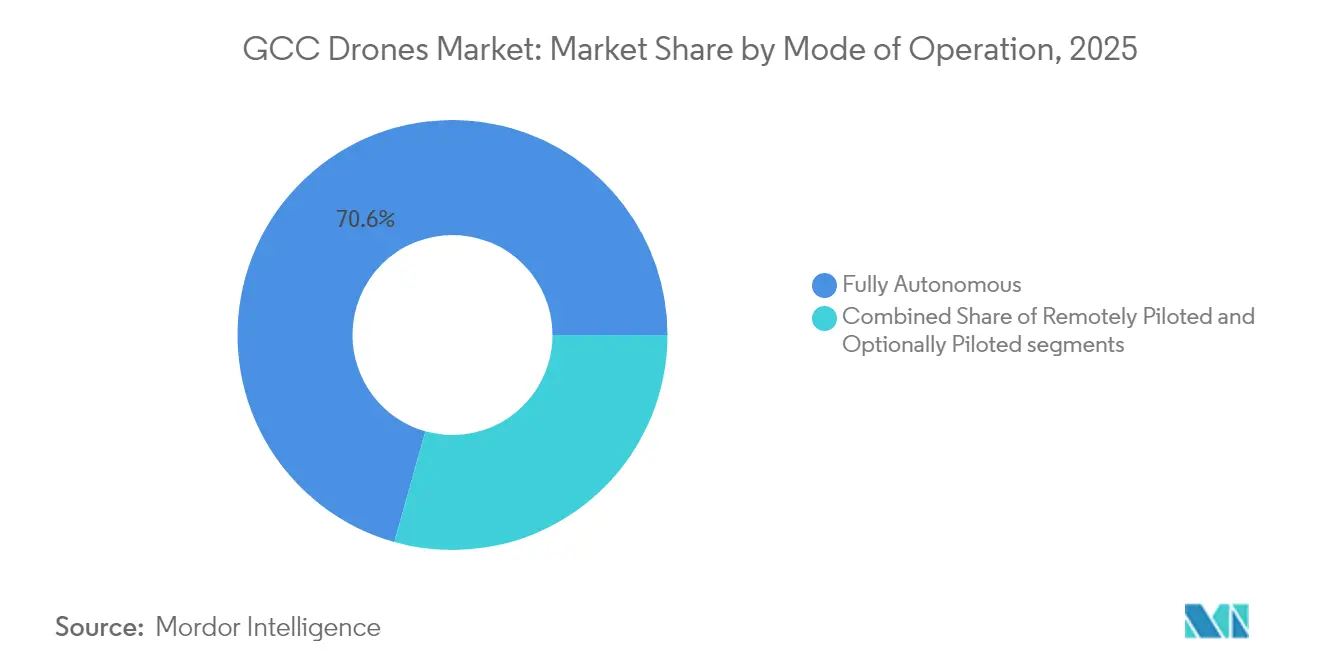

- By mode of operation, fully autonomous systems held 70.64% of the GCC drone market share in 2025 and continue at a 12.94% CAGR to 2031.

- By end-user, commercial and consumer segments commanded 58.45% of 2025 revenue, while government and civil demand registered the fastest 10.86% CAGR through 2031.

- By geography, Saudi Arabia led with a 34.12% share in 2025, and Qatar posts the highest 13.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Drones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming giga-project construction pipeline (e.g., NEOM, Expo City Dubai) | +1.7% | Saudi Arabia, UAE core, spill-over to Qatar | Medium term (2-4 years) |

| Expanding oil and gas/utilities asset-inspection demand | +1.4% | All GCC, concentrated in Saudi Arabia and UAE | Long term (≥4 years) |

| Progressive civil-aviation rules and dedicated drone corridors | +1.1% | UAE leading, Saudi Arabia following, Qatar accelerating | Short term (≤2 years) |

| E-commerce-led last-mile delivery pilots (Dubai Sky-Dome, SAL-KSA) | +0.9% | UAE and Saudi Arabia urban centers | Medium term (2-4 years) |

| Digital-twin mandates for smart-city projects | +0.7% | UAE, Saudi Arabia smart-city zones | Medium term (2-4 years) |

| Date-palm precision-farming and autonomous harvesting pilots | +0.6% | Saudi Arabia, UAE agricultural regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Giga-project construction pipeline

USD 1.3 trillion worth of active developments, such as NEOM and Expo City Dubai, demand continuous aerial surveillance for earthworks, concrete curing checks, and worker-safety compliance. AI-enabled drones with LiDAR and thermal imaging reduce rework costs and shorten progress-report cycles from days to hours. Tender documents now list drone flight-hour minima alongside cranes and cement mixers, embedding autonomous platforms into baseline project budgets. Real-time visual logs also help contractors verify adherence to mandatory demolition waste recycling, supporting ESG disclosures. The scale of these sites forces project owners to adopt fleet-management software that automates mission planning across multiple subcontractors, further anchoring demand in the GCC drone market.

Oil and gas asset inspection

Helicopter sorties for flare-stack checks cost USD 7,000 per hour, prompting ADNOC Gas to switch to robotics and drone fleets that lift inspection coverage by 99.6% while cutting costs by 93%.[1]Jennifer Pallanich, “ADNOC adds Gecko Robotics for AI inspections,” Journal of Petroleum Technology, jpt.spe.org Terra Drone’s expanded deal with Saudi Aramco illustrates a services model where machine-learning analytics predict corrosion hot spots on thousands of kilometers of pipeline. Offshore operators now deploy hybrid VTOL craft that land on FPSO helipads, lowering weather-delay downtime. Regulatory pressure to eliminate methane leaks adds continuous-monitoring missions that favor fully autonomous drones with gas-spectrometry payloads. The heightened frequency of preventive inspections propels recurring-revenue contracts, reinforcing the GCC drone market’s service backbone.

Progressive civil-aviation rules

The UAE’s Federal Decree-Law No. 26 of 2022 streamlines licensing and authorizes nationwide drone-service corridors via a single digital portal.[2]Staff writer, “UAE Federal Decree-Law No. 26 of 2022 on unmanned aircraft,” UAE Government, u.ae Dubai sealed design approval for its first vertiport, clearing the way for scheduled eVTOL services by 2026. Bahrain issues flight permission decisions within 7 days, injecting predictability for inspection firms. These frameworks enable beyond-visual-line-of-sight (BVLOS) operations and cross-border logistics trials, accelerating commercial scale-up across the GCC drone market.

E-commerce last-mile delivery pilots

Abu Dhabi’s 40-station medical-supply drone grid operates 24/7, demonstrating desert-climate resilience and a 30-minute urban delivery standard. Riyadh logistics firm SAL completed 2,000 parcel flights on predefined corridors, validating consumer acceptance.[3]Staff writer, “Abu Dhabi launches 24/7 medical drone network,” Department of Health-Abu Dhabi, doh.gov.ae NEOM’s USD 175 million alliance with Volocopter will field three eVTOL aircraft families across four dedicated airports by 2026. These pilots build airframe, battery-swap, and air-traffic-integration know-how transferable to large-scale retail delivery, bolstering the GCC drone market’s logistics segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented and evolving air-space approval procedures | -0.7% | All GCC, particularly cross-border operations | Short term (≤2 years) |

| Shortage of certified commercial drone pilots and service firms | -0.6% | Regional, acute in Kuwait and Oman | Medium term (2-4 years) |

| Harsh desert climate degrading batteries and sensors | -0.5% | All GCC, especially inland desert regions | Long term (≥4 years) |

| RF/GPS jamming near strategic sites hampers BVLOS ops | -0.4% | Border regions and strategic facilities across GCC | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Fragmented air-space procedures

Operators must win separate clearances from six aviation authorities, raising compliance costs and delaying multi-country expansion. Cross-border pipeline surveys routinely stall at land-boundary airspace hand-offs, forcing hybrid workflows that mix drones and trucks. Lack of mutual recognition also hampers package-delivery networks that aim to span the eastern coast from Muscat to KSA’s Eastern Province. Harmonization talks remain informal, meaning service providers must reserve legal and operations teams in each market, shaving margin from the GCC drone market’s early movers.

Pilot shortage

Advanced platforms still require certified operators for mission overrides, but regional training pipelines graduate fewer than 800 commercial pilots annually, far below demand curves. Kuwait and Oman import foreign crews at premium rates, inflating project budgets. Continuous software updates oblige recurrent training that smaller service firms struggle to finance. Without scaled academies, the pilot gap curbs addressable flight-hour capacity and caps revenue growth even as hardware prices fall.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Construction commands today, entertainment accelerates in the forecast period

Construction projects accounted for 46.88% of 2025 revenue. Site owners rely on drones to verify structural steel alignment, monitor worker heat stress, and capture photogrammetry for digital twin models, embedding aerial sorties into daily progress workflows. The segment’s entrenched use drives consistent demand across the GCC drone market.

Entertainment applications post a 13.12% CAGR through 2031 as sport mega-events require immersive camera angles and synchronized light shows. Abu Dhabi’s A2RL drone championship proved AI-piloted racers can exceed 150 km/h inside closed circuits, opening the door for large-venue entertainment packages. Stadium operators integrate drones for crowd management analytics and on-site merchandise delivery. These experiential services diversify revenue, deepening the GCC drone market’s consumer engagement footprint.

By Type: Rotary-wing dominance meets hybrid disruption

Rotary-wing craft held 48.62% of 2025 sales due to their vertical-takeoff agility, which is crucial for urban sites and offshore rigs. Quick-swap battery trays keep turnaround times under 5 minutes, making the configuration a staple across inspection and videography fleets.

Hybrid VTOL systems, however, clock a 14.05% CAGR. Longer ranges and 10-kg payload ceilings suit pipeline patrols and parcel delivery across sprawling suburbs. NEOM-Volocopter trials of VoloDrone cargo variants underscore the shift toward platform flexibility that merges helicopter hover with fixed-wing cruise efficiency. Hybrids broaden the GCC drone market’s mission spectrum as airworthiness rules converge.

By Weight Class: Small platforms lead, medium segment surges

Small drones (2 to 25 kg) comprise 47.75% of the 2025 turnover because regulations in Saudi Arabia and the UAE grant lighter craft expedited permits. Their compact frames carry RGB and thermal sensors for façade scans and crop-health imaging.

Medium platforms (25 to 150 kg) expand fastest at 13.02% CAGR as lift capacity accommodates LiDAR, methane sniffers, and 20-kg cargo pods. Riyadh-based ADMC’s USD 600 million order for 102 Sabrewing Rhaegal-B heavy-lift drones exemplifies demand for heftier airframes to ferry oil-field spares across desert zones. This shift enlarges the GCC drone market size for payload-intensive missions.

By Mode of Operation: Autonomy reshapes workflows

Fully autonomous flights represented 70.64% of 2025 spend and sustain a 12.94% CAGR to 2031. Saudi Arabia’s USD 100 billion AI program and purchase of 18,000 Nvidia GB300 GPUs facilitate on-device inference that replaces ground-station control loops. Reliability in 50°C heat and dust storms improves through real-time obstacle avoidance.

Remotely piloted models remain critical for sensitive zones such as airports, but optional human-in-the-loop modes gradually fade as regulators gain confidence in autonomy. This transition consolidates the GCC drone market around software IP and trust-certification services.

By End-User: Commercial share masks dual-use reality

Commercial and consumer operators held 58.45% of 2025 revenue. Construction firms, energy majors, and media studios anchor orders, while hobby flying grows within regulated parks. Government and civil agencies record the quickest 10.86% CAGR on the back of border security, emergency-response, and smart-city surveillance budgets.

Defense procurement often seeds dual-use spillovers. Qatar’s USD 2 billion MQ-9B and counter-UAS buy created a maintenance ecosystem serving private-sector fleets. Such overlaps blur categorical lines, expanding the GCC drone industry into integrated security-economic platforms.

Geography Analysis

Saudi Arabia’s slice of the GCC drone market combines giga-project surveillance and energy-asset inspections. The Kingdom’s NEOM build-out spans 26,500 km², requiring 24/7 LiDAR mapping to keep pace with desert-terrain reshaping. SAMI Aerospace’s Bayraktar line increases domestic UAV production from 3% to 15%, positioning Riyadh to export systems across MENA. Terra Drone’s contract expansion with Aramco demonstrates cost-saving proof at the world’s largest oil producer. The Kingdom’s AI workforce target of 20,000 specialists by 2030 underpins long-term autonomy advances. These initiatives consolidate Saudi Arabia’s leadership within the GCC drone market.

The UAE leverages efficient regulations and indigenous R&D. Federal Decree-Law No. 26 of 2022 slashed permit lead times to 48 hours. Dubai’s vertiport approval marks a first for commercial air-taxi hubs. Abu Dhabi’s 40-station medical-delivery network halves emergency-medicine transit times and cuts CO₂ emissions by 50%. Edge Group’s Jeniah program showcases 1,050 km/h indigenous jet-drone capability. Together, these milestones keep the UAE central to pilot projects that scale across the GCC drone market.

Qatar registers the fastest growth trajectory. A USD 3 billion order for MQ-9B drones plus Raytheon FS-LIDS counter-UAS systems positions Doha as a defense technology hub. The Civil Aviation Authority’s draft UAS code invites foreign operators for sandbox trials, accelerating commercial services incubation. Cooperative projects with Qatar Energy explore methane-leak monitoring over 800 km of pipelines, creating energy-sector use cases transferable across GCC peers. This convergence fuels Qatar’s outsized CAGR in the GCC drone market.

Competitive Landscape

Competition is moderate and tightening as localization rules reward players who can transfer IP and assemble hardware in-country. DJI maintains volume leadership in the small-drone tier through channel partners that localize firmware for Arabic interfaces. Terra Drone leverages inspection analytics to secure multi-year framework agreements with Aramco and ADNOC. General Atomics negotiates bulk sales with Saudi Arabia while offering industrial surveillance variants to diversify beyond defense.

Regional firms gain ground. FalconViz supplies LiDAR mapping packages tailored to desert topography for NEOM contractors. Edge Group’s Jeniah underscores the UAE’s capacity to design and flight-test high-performance systems at home, prompting international rivals to consider joint lines for market access. SAMI Aerospace’s Bayraktar joint venture provides a model: foreign OEM technology paired with domestic workforce and supply-chain commitments.

Strategic moves in 2024-2025 include USD 600 million in cargo-UAS purchases by ADMC, which creates the Gulf’s largest heavy-lift fleet; Terra Drone’s Saudi inspection expansion; and Volocopter’s four-airport blueprint inside NEOM. Supply-chain depth, regulatory advocacy, and AI-software prowess are decisive weapons in the emerging GCC drone market.

GCC Drones Industry Leaders

SZ DJI Technology Co., Ltd.

Parrot Drones SAS

Primoco UAV SE

FalconViz

Yuneec (ATL Drone)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Terra Drone expanded its inspection contract with Saudi Aramco to cover 35 offshore facilities.

- January 2025: Matternet, a drone delivery company hailing from California, has made a notable stride in its worldwide expansion. The company revealed it has secured the green light from Saudi Arabia’s General Authority of Civil Aviation (GACA) to deploy its M2 drone delivery system.

- June 2024: AgEagle Aerial Systems Inc. clinched a purchase order to supply 20 eBee VISION full-stack systems with control systems, batteries, backpacks, and select spares to a prominent distributor in the United Arab Emirates (UAE). This system contract is projected to be valued at around USD 2 million.

- March 2024: Edge Group completed the first flight of the Jeniah jet-powered drone at 1,050 km/h.

GCC Drones Market Report Scope

A drone is a technological device that operates without a human pilot onboard. It is equipped with remote control systems or autonomous programming, allowing it to navigate the air rapidly. Drones have diverse applications in civilian and military domains, such as photography, surveillance, agriculture, and recreational activities. These versatile devices feature cameras or sensors that capture high-quality images or data, making them practical tools in various industries.

The GCC drone market is segmented by application and geography. By application, the market is divided into construction, agriculture, energy, entertainment, law enforcement, and other applications. The other applications segment includes the deployment of drones for operations such as firefighting and aerial mapping. The report also offers the market size and forecasts for the drone market in six countries in the region. The report offers the market size and forecasts in value (USD) for all the above segments.

By Application

| Construction |

| Agriculture |

| Energy |

| Entertainment |

| Law-Enforcement |

| Other Applications |

By Type

| Fixed-Wing Drones |

| Rotary-Wing Drones |

| Hybrid/VTOL Drones |

By Weight Class

| Nano/Micro (Less than 2 kg) |

| Small (2 to 25 kg) |

| Medium (25 to 150 kg) |

| Large (Greater than 150 kg) |

By Mode of Operation

| Remotely Piloted |

| Optionally Piloted |

| Fully Autonomous |

By End-User

| Commercial and Consumer/Hobbyist |

| Government and Civil |

By Country

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Bahrain |

| Oman |

| By Application | Construction |

| Agriculture | |

| Energy | |

| Entertainment | |

| Law-Enforcement | |

| Other Applications | |

| By Type | Fixed-Wing Drones |

| Rotary-Wing Drones | |

| Hybrid/VTOL Drones | |

| By Weight Class | Nano/Micro (Less than 2 kg) |

| Small (2 to 25 kg) | |

| Medium (25 to 150 kg) | |

| Large (Greater than 150 kg) | |

| By Mode of Operation | Remotely Piloted |

| Optionally Piloted | |

| Fully Autonomous | |

| By End-User | Commercial and Consumer/Hobbyist |

| Government and Civil | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Bahrain | |

| Oman |

Key Questions Answered in the Report

What is the current size of the GCC drone market?

The market stands at USD 2.32 billion in 2026 and is forecasted to reach USD 4.12 billion by 2031, advancing at a 12.12% CAGR.

Which application segment leads revenue?

Construction holds the top position with 46.88% market share in 2025 due to giga-project surveillance needs.

Which drone type is growing fastest in the GCC?

Hybrid/VTOL platforms post the highest 14.05% CAGR because they combine hover capability with extended range.

Why is Saudi Arabia the largest geographic market?

Vision 2030 mega-projects, expanding oil-field inspections, and domestic manufacturing lines place Saudi Arabia at 34.12% share.

What major restraint could slow market growth?

Fragmented air-space approval procedures across the six GCC states currently shave 0.7 percentage points from forecast CAGR.

How autonomous are GCC drone operations today?

Fully autonomous flights already account for 70.64% of spending, supported by sizable national investments in AI hardware and talent.

Page last updated on: