GCC Corporate Training Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

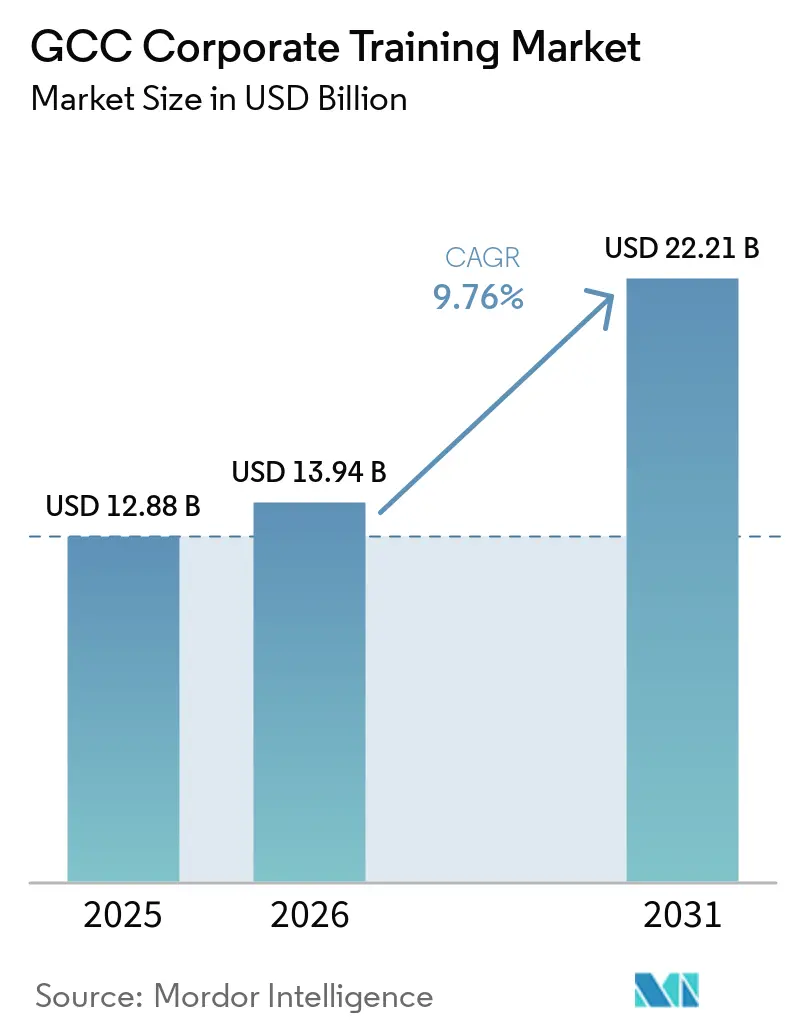

| Base Year Market Size (2025) | USD 12.88 Billion |

| Market Size (2026) | USD 13.94 Billion |

| Market Size (2031) | USD 22.21 Billion |

| Growth Rate (2026 - 2031) | 9.76% CAGR |

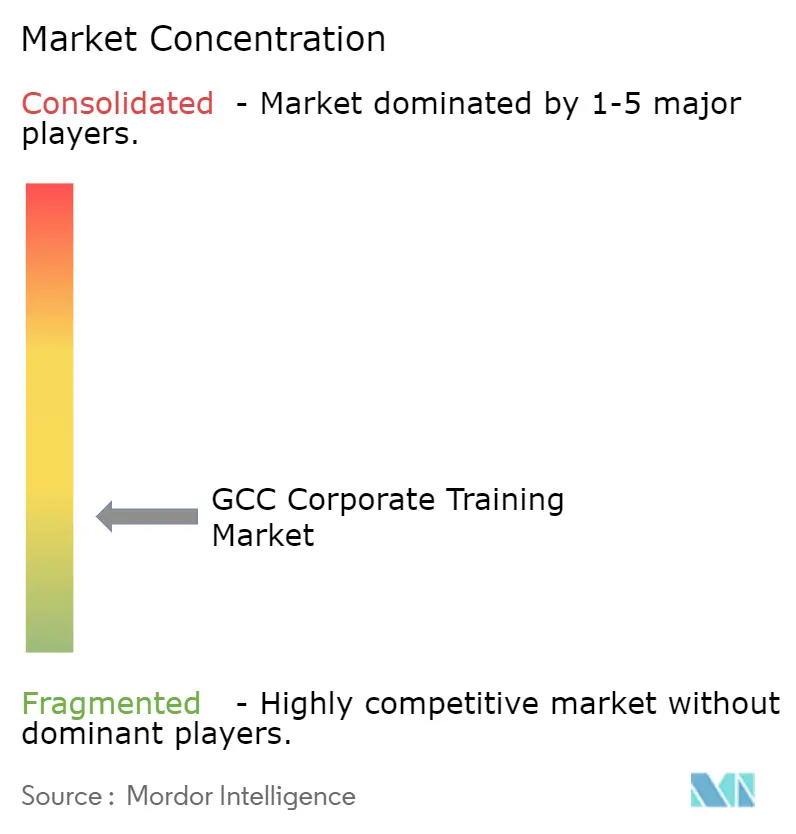

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Corporate Training Market Analysis by Mordor Intelligence

The GCC corporate training market size is expected to increase from USD 12.88 billion in 2025 to USD 13.94 billion in 2026 and reach USD 22.21 billion by 2031, growing at a CAGR of 9.76% over 2026-2031. The GCC corporate training market is being shaped by national development plans that tie workforce capability to private-sector growth, digital adoption, and public-sector reform. This has kept training budgets closer to strategic spending than optional spending, especially in Saudi Arabia and the United Arab Emirates. The GCC corporate training market is also benefiting from stronger demand for AI, cybersecurity, cloud, and management skills as employers face faster technology rollouts and tighter localization goals. Online learning, blended delivery, and live virtual formats are widening reach across multinational workforces, while the shortage of strong Arabic-language content is creating room for localized providers. Competition remains moderate to high because global platforms still have scale, but regional specialists are winning business where bilingual delivery, cultural fit, and compliance alignment matter most.

Key Report Takeaways

- By geography, Saudi Arabia held a 45.12% share of the GCC corporate training market in 2025, while the United Arab Emirates is projected to expand at an 11.12% CAGR through 2031.

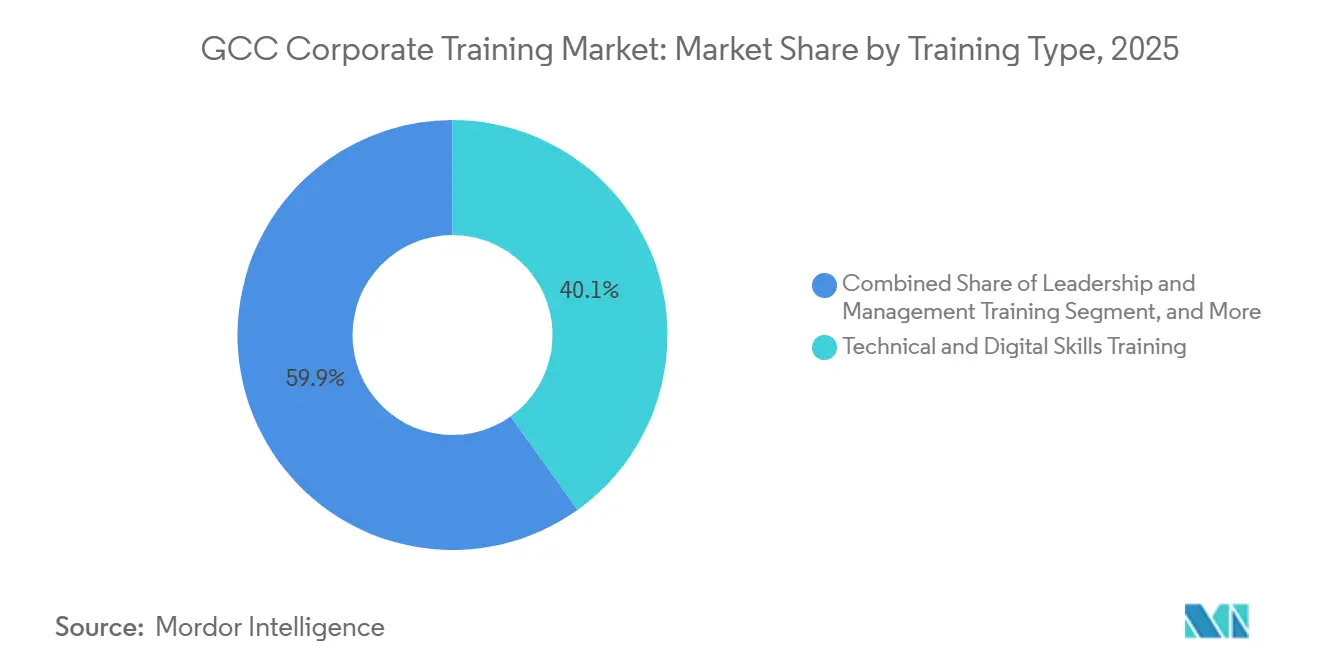

- By training type, technical and digital skills training accounted for 40.12% of revenue in 2025, while leadership and management training is forecast to grow at a 12.27% CAGR through 2031.

- By delivery mode, online self-paced learning commanded a 55.23% share in 2025, while virtual instructor-led training is projected to rise at a 12.64% CAGR through 2031.

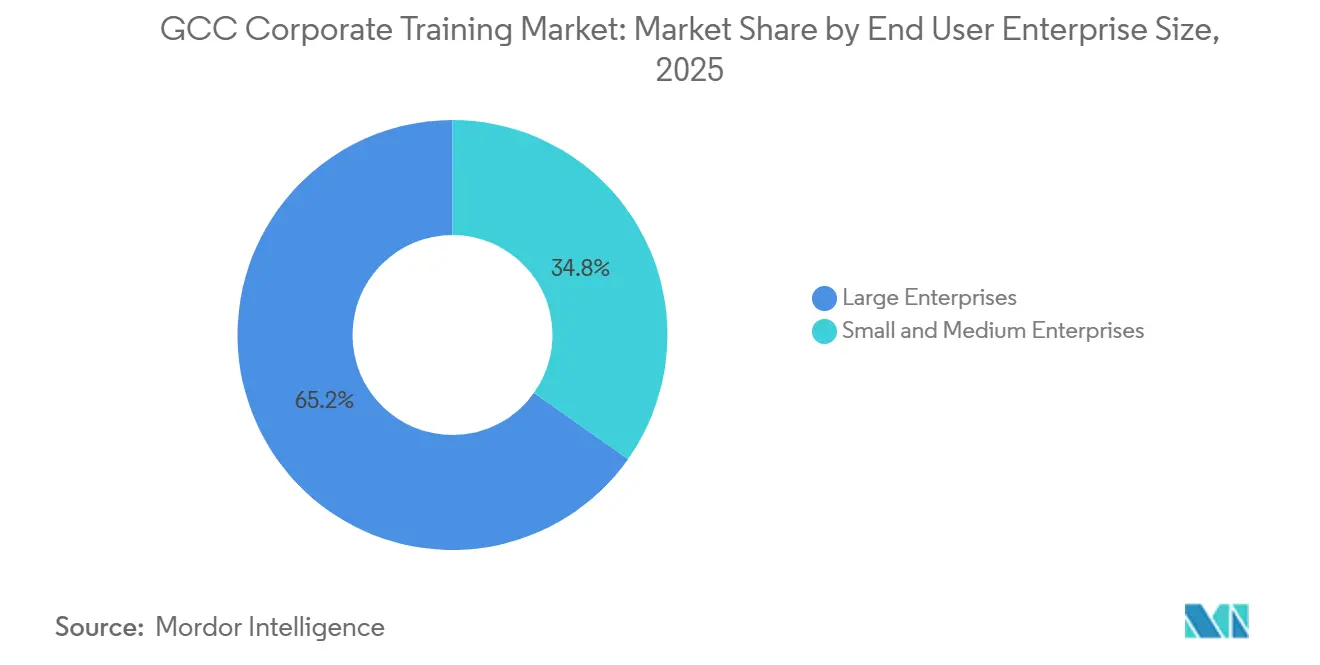

- By enterprise size, large enterprises accounted for 65.19% of spending in 2025, while small and medium enterprises are expected to grow at a 13.11% CAGR through 2031.

- By end-user industry, BFSI held a 35.23% share in 2025, while IT and telecom are forecast to expand at an 11.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC Corporate Training Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economic Diversification And Human Capital Agendas | +3.2% | GCC-wide, core in Saudi Arabia and UAE | Long term (= 4 years) |

| Enterprise Digital Transformation And AI Upskilling | +2.8% | GCC-wide, led by UAE and Saudi Arabia | Medium term (2-4 years) |

| Shift Toward Online, Blended, And Virtual Instructor-Led Learning | +1.8% | GCC-wide | Medium term (2-4 years) |

| Rising Leadership And Soft Skills Priorities | +1.2% | GCC-wide, strongest in Saudi Arabia and UAE | Medium term (2-4 years) |

| Localization Quota Enforcement Raising Capability Spend | +0.9% | Saudi Arabia, UAE, Qatar, Kuwait, Oman, Bahrain | Short term (= 2 years) |

| Bilingual Arabic-English Workforce Enablement Demand | +0.4% | GCC-wide, most acute in Saudi Arabia, UAE, Qatar | Short term (= 2 years) |

| Source: Mordor Intelligence | |||

Economic Diversification And Human Capital Agendas

National human capital plans remain the strongest structural support for the GCC corporate training market because training demand is tied to economic policy rather than short budget cycles. Saudi Vision 2030 reported that non-oil activities contributed 55% of GDP in 2025, which keeps workforce development linked to the country's economic rebalancing effort.[1]Vision 2030, “Saudi Vision 2030 - 2025 Annual Report,” Vision 2030, vision2030.gov.sa The same 2025 annual report stated that the Public Investment Fund had USD 925 billion in assets under management, indicating sustained funding capacity across state-linked employers and portfolio companies. Saudi Arabia's 2024 Vision 2030 annual report also noted a transformation strategy for the Institute of Public Administration focused on leadership capacity and digital transformation, indicating that public-sector training budgets are becoming more embedded in reform programs. HRDF's Doroob platform further shows that public support is now built into the delivery infrastructure and policy direction, reducing dependence on one-off training purchases. This gives the GCC corporate training market a firmer foundation, as hiring, productivity, and capability development are treated as interconnected policy outcomes.

Enterprise Digital Transformation And AI Upskilling

Enterprise digital transformation is shifting training decisions closer to business and technology leaders across the GCC corporate training market because AI, data, and automation now affect core operations. In October 2025, it was reported that skills transition inefficiencies cost Saudi Arabia SAR 62 billion (USD 16.3 billion) annually in lost earnings, which moves reskilling into a business performance discussion rather than a narrow HR discussion.[2]Pearson plc, “Lost in Transition: Gaps in Career Paths Costing Saudi Arabia SAR 62 Billion Annually,” Pearson plc, plc.pearson.com Digital Dubai launched the AI Workforce Transformation Program in April 2026 to train 50,000 government employees across five competency tiers, underscoring how deeply AI capability-building has entered public-sector operations. In Saudi Arabia, the Ministry of Communications and Information Technology funded senior private-sector leaders to attend Microsoft's Global AI Leadership Program in February 2026, elevating executive AI learning to the national capability-planning level. Coursera and Naseej entered a strategic partnership in June 2025 to expand access to AI, data science, cybersecurity, and business content across government, campus, and business channels in MENA. Together, these moves show that providers with applied AI, cloud, data, and automation content are becoming more central to the GCC corporate training market.

Shift Toward Online, Blended, And Virtual Instructor-Led Learning

Delivery is moving toward online, blended, and live virtual formats because employers in the GCC corporate training market need scalable learning for teams spread across sites, cities, and countries. Saudi Arabia's Doroob platform shows how self-paced e-learning has become a formal part of workforce development rather than a side channel.[3]Skillsoft Corporation, “Skillsoft Leads the Shift to Skills Management for Workforce Readiness,” Skillsoft Corporation, investor.skillsoft.com Skillsoft's February 2026 Percipio release combined learning content, skills mapping, and workforce-readiness measurement into one platform, reflecting stronger employer demand for more structured digital learning systems. Coursera and Naseej widened digital training access across government, campus, and business channels in 2025, which supports greater use of platform-based learning across the region. MBZUAI The Academy's executive AI program combines direct expert access and site visits with structured learning, reflecting how premium offerings blend digital scale with high-touch engagement. As a result, the GCC corporate training market is favoring providers that can support self-paced modules, live virtual sessions, and focused in-person touchpoints within one learning model.

Rising Leadership And Soft Skills Priorities

Leadership development is gaining weight in the GCC corporate training market because many employers need stronger people management capability at the same time that organizations are moving through digital and operating change. Saudi Arabia's Financial Academy offers the New Leaders Program in partnership with the Center for Creative Leadership, demonstrating that formal leadership pathways are being built within regulated sectors. FranklinCovey Middle East supports more than 1,500 client engagements annually and offers more than 25 localized solutions across leadership, trust, and execution, which shows steady demand for practical manager development. Nesma and Partners' NHTI and Kent signed a February 2026 agreement that includes leadership training alongside engineering and commissioning programs in Saudi Arabia. MBZUAI The Academy also offers an executive AI program, indicating that senior leaders are being targeted with structured capability-building rather than short awareness sessions. This is widening spending beyond technical courses because employers now need manager readiness, communication, and decision-making to support large change programs in the GCC corporate training market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget Scrutiny And Difficulty Proving Learning ROI | -1.4% | GCC-wide | Short term (≤ 2 years) |

| Low Learner Engagement In Digital-First Programs | -0.8% | GCC-wide | Medium term (2-4 years) |

| Shortage Of Arabic-English Facilitators And Localized Content | -0.6% | GCC-wide, most acute in Saudi Arabia and smaller GCC states | Medium term (2-4 years) |

| Data Residency And Explainable-AI Compliance Complexity | -0.3% | UAE (ADGM/DIFC), Saudi Arabia (NDMO) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget Scrutiny And Difficulty Proving Learning ROI

Budget scrutiny remains a real brake on the GCC corporate training market, as buyers increasingly demand proof that training improves workforce readiness and business performance. In February 2026, it was noted that fewer than 1 in 4 organizations have a consolidated view of workforce skills, which makes it harder for employers to link training budgets to measurable capability outcomes. Saudi analysis framed the cost of weak skills transition in earnings terms, which raises the bar for providers seeking to defend training spend with hard business value. FranklinCovey Middle East's work on retention and agility also reflects how employers are tying people programs more closely to performance and turnover outcomes.[4]FranklinCovey Middle East, “From High Turnover to High Agility,” FranklinCovey Middle East, franklincoveyme.com In this setting, procurement cycles lengthen when vendors cannot demonstrate pre-program baselines, post-program progress, and clear manager follow-through. Providers that combine content with skills measurement, assessments, and reporting are therefore better placed to protect budgets in the GCC corporate training market.

Low Learner Engagement In Digital-First Programs

Low learner engagement in digital-first programs continues to limit the full upside of the GCC corporate training market, even as access to online learning improves. Large-scale systems such as Doroob show that digital reach is expanding, but outcomes still depend on language fit, support quality, and course design. Coursera and Naseej built delivery across business, campus, and government channels, which suggests institutions still need guided adoption rather than simple content access. Skillsoft's latest platform added personalization and skills management, which points to the market's response to weak completion and uneven follow-through in standard digital libraries. MBZUAI's executive format still relies on direct expert interaction, which shows that many employers continue to value structured engagement over pure on-demand consumption. Providers that improve Arabic-English flow, tutor support, and learning design are therefore more likely to sustain participation across the GCC corporate training market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Training Type: Technical Skills Lead, Leadership Spending Accelerates

Technical and digital skills training held 40.12% of the GCC corporate training market share in 2025, while leadership and management training is projected to grow at a 12.27% CAGR through 2031. This lead reflects strong employer demand for role-based certification and proficiency with digital tools across oil and gas, banking, and public-sector functions. In February 2026, Saudi Arabia's Ministry of Communications and Information Technology funded senior private-sector leaders to attend Microsoft's Global AI Leadership Program, which showed that technical AI learning had moved into national capability planning. Saudi Arabia also ranked first in the Global Cybersecurity Index for the second consecutive year in 2025, which supports continuing demand for cybersecurity certifications and framework-linked learning.

Leadership and management training is expanding because employers need more supervisors and middle managers who can lead mixed teams while absorbing fast process change. The Financial Academy in Saudi Arabia runs the New Leaders Program with the Center for Creative Leadership, which formalizes leadership development in a regulated end market. The GCC corporate training industry is therefore broadening beyond basic technical instruction into manager readiness, communication, decision-making, and change support. Compliance, risk, and ESG training also remain active where employers face evolving disclosure, governance, and operating standards. Industry-specific functional training continues to matter in healthcare, construction, and energy because technical standards, safety rules, and digital systems are constantly evolving.

By Delivery Mode: Self-Paced Scales As VILT Deepens Engagement

Online self-paced learning accounted for 55.23% of the GCC corporate training market in 2025, while virtual instructor-led training is forecast to grow at a 12.64% CAGR through 2031. This split shows that scale and flexibility matter, but employers still want live interaction for discussion, guided practice, and immediate feedback. Saudi Arabia's Doroob platform illustrates how self-paced digital delivery has become part of formal workforce development infrastructure. Skillsoft's February 2026 Percipio release also showed how enterprise buyers are leaning toward platforms that combine content, skills data, and readiness measurement.

VILT is growing because it lowers travel costs while keeping instructor presence for teams spread across multiple locations. Coursera and Naseej expanded digital access across government, campus, and business channels in 2025, which supports wider acceptance of remotely delivered learning. Classroom delivery still holds value for leadership work, negotiation practice, and high-stakes simulations where direct group dynamics matter most. Blended models are becoming more practical in the GCC corporate training market because they combine lower-cost digital preparation with focused live sessions. MBZUAI The Academy's executive AI program adds site visits and direct expert engagement, demonstrating that premium formats still rely on in-person elements as a differentiator.

By End User Enterprise Size: Large Enterprises Anchor Spend, SMEs Accelerate Fastest

Large enterprises accounted for 65.19% share of the GCC corporate training market size in 2025, while small and medium enterprises are set to expand at a 13.11% CAGR through 2031. Their lead came from higher training budgets, formal learning teams, and stricter compliance and certification needs. State-linked entities, sovereign wealth fund portfolio companies, and large conglomerates also provide providers with more stable, multi-year demand in the GCC corporate training market. FranklinCovey Middle East's client base includes Saudi Aramco, SABIC, ADNOC, and Jumeirah, demonstrating how deeply established providers can embed themselves in large-enterprise accounts.

Small and medium enterprises are growing faster because public support, modular pricing, and digital delivery are lowering the entry barrier for structured training. Saudi Arabia's Doroob program provides a scalable route for smaller employers to access standardized digital learning without building their own systems. In January 2026, Alkhaleej Training and Education signed a cooperation agreement with the Social Development Bank in Saudi Arabia, expanding its reach in workforce development and financially supporting learning programs. Bahrain's EMIC AI program also shows how fully funded enrollment can widen access for smaller firms and early-career professionals. The GCC corporate training industry is therefore expanding from large anchor accounts toward a broader SME buyer base seeking practical, lower-risk training purchases.

By End-User Industry: BFSI Leads, IT And Telecom Edges Forward On Velocity

BFSI held 35.23% of the GCC corporate training market share in 2025, while IT and telecom are projected to advance at an 11.89% CAGR through 2031. BFSI leads because compliance cycles, fintech programs, and role-specific certification needs create repeat training demand that firms cannot easily defer. Saudi Arabia's Financial Academy offers structured programs, such as the New Leaders Program, that support ongoing capability development in financial services. The segment also benefits from the fact that governance, risk, and compliance learning must keep pace with evolving operating frameworks and the adoption of digital tools.

IT and telecom are moving fastest because 5G rollout, cloud migration, and AI deployment all require steady technical reskilling. Government-led AI programs in Dubai and Saudi Arabia are reinforcing this pattern by increasing the supply and visibility of applied digital learning pathways. Healthcare and life sciences are also active because coverage expansion, specialized care investment, and digital administration create training needs across clinical and nonclinical roles. Construction, engineering, energy, and utilities remain important because project pipelines, safety requirements, and operational digitization continue to drive skill requirements. Retail, ecommerce, transportation, and logistics still drive meaningful demand, especially as customer experience, digital sales, and supply chain systems are upgraded.

Geography Analysis

Saudi Arabia's 45.12% share in 2025 made it the anchor of the GCC corporate training market. Non-oil activities contributed 55% of GDP in 2025, and the Public Investment Fund reached USD 925 billion in assets under management, supporting a large, policy-linked base for workforce capability spending. The 2024 Vision 2030 annual report also highlighted a transformation strategy for the Institute of Public Administration that focused on leadership capacity and digital transformation, which supports more institutionalized public-sector training demand. In October 2025, skills transition inefficiencies were estimated to cost Saudi nationals SAR 62 billion (USD 16.3 billion) annually, which helps explain why employers are treating reskilling as a business issue. Public programs and enterprise partnerships such as MCIT's AI leadership support, the Financial Academy's leadership pathway, and Nesma's training agreement with Kent reinforce Saudi Arabia's central role in the GCC corporate training market.

The United Arab Emirates is the fastest-growing geography in the GCC corporate training market with an 11.12% CAGR through 2031. Digital Dubai launched AI+ in April 2026 to train 50,000 government employees, underscoring the scale of the country's state-backed digital capability-building. MBZUAI The Academy adds an executive AI route with direct expert access and site visits, broadening the market from general digital literacy to senior decision-maker capability building. These factors keep the UAE important to the GCC corporate training market because employer demand is being reinforced by public-sector AI adoption, premium executive learning, and faster private-sector skills expectations.

Qatar, Kuwait, Oman, and Bahrain accounted for the remaining share of the GCC corporate training market, with demand shaped by sector hiring plans, localization efforts, and digital capability gaps. Bahrain's Tamkeen-backed EMIC AI program demonstrates how public co-funding supports targeted workforce capability-building in smaller GCC markets. Oman and Kuwait are developing more gradually, and demand is strongest where private employers face capability gaps in technical, regulated, and supervisory roles. Across these markets, the GCC corporate training market remains closely tied to public policy, bilingual delivery needs, and employer demand for practical digital skills.

Competitive Landscape

The GCC corporate training market remains moderately fragmented, with global platforms and regional specialists competing across enterprise accounts. FranklinCovey Middle East supports more than 1,500 client engagements annually and offers more than 25 localized solutions, underscoring the importance of relationship depth and localization in this region. Skillsoft's February 2026 Percipio release combined learning, skills mapping, and workforce-readiness measurement, reflecting the pressure to prove outcomes as well as deliver content. Coursera and Naseej expanded access to AI, data science, cybersecurity, and business content across government, campus, and business channels in 2025, which strengthens the position of scalable digital platforms in the GCC corporate training market. This means providers are increasingly judged on content breadth, localization, and their ability to align with national skilling agendas.

Recent strategic moves show that competition is shifting toward AI capability, applied enterprise delivery, and deeper local reach in the GCC corporate training market. Nesma and Partners' NHTI and Kent signed an agreement in February 2026 to build industry-driven technical, vocational, and leadership training in Saudi Arabia. EnterOne Corporation and NIL Data Communications Middle East announced a February 2026 cooperation agreement to deliver technology training, professional services, and AI consulting across the region. Alkhaleej Training and Education signed a January 2026 cooperation agreement with the Social Development Bank in Saudi Arabia, which extended its reach in workforce development and financial services training.

Regional specialists continue to benefit when they can offer Arabic-English delivery, local case material, and alignment with compliance requirements, which remain core buying needs in the GCC corporate training market. Global providers still retain an advantage in platform scale, certification pathways, and cross-border content libraries. The market still has room for SME-focused programs, Arabic-first AI content, and assessment-linked compliance training, as those needs are expanding faster than standardized supply can keep pace. Competition is therefore likely to remain active rather than narrow to a small group of providers, keeping the GCC corporate training market open to both scaled global brands and agile local firms.

GCC Corporate Training Industry Leaders

Franklin Covey Co.

Dale Carnegie & Associates Global, Inc.

Skillsoft Corporation

Udemy, Inc.

Coursera, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Digital Dubai launched AI+ to upskill 50,000 government employees across five AI competency tiers, marking one of the region’s largest public-sector AI programs.

- February 2026: Nesma and Partners’ NHTI and Kent signed an MoU to deliver technical and vocational training in Saudi Arabia, aligned with Vision 2030.

- February 2026: Skillsoft released the next-gen Percipio® Platform, integrating learning, skills mapping, and workforce readiness measurement.

- January 2026: Alkhaleej Training and Education partnered with the Social Development Bank to expand corporate training in financial services and social workforce development.

GCC Corporate Training Market Report Scope

The GCC Corporate Training Market comprises platforms, programs, and services designed to enhance workforce capabilities across the Gulf Cooperation Council countries. It includes training in technical, digital, leadership, compliance, and industry-specific skills, delivered through online, blended, and immersive modes. The market serves enterprises of all sizes across diverse industries, supporting organizational transformation, regulatory alignment, and workforce competitiveness in the region.

The GCC Corporate Training Market is segmented by Training Type (Technical Skills Training, Digital Transformation, AI and Data Training, Cybersecurity Training, Leadership and Management Training, Soft Skills and Behavioral Training, Sales and Commercial Excellence Training, Compliance, Risk and ESG Training, Diversity, Equity & Inclusion Training, and Industry-specific Functional Training), Delivery Mode (Online Self-paced Learning, Virtual Instructor-led Training, Classroom Instructor-led Training, Blended Learning, Mobile Learning and Microlearning, AI-powered Adaptive Learning, and AR/VR Immersive Training), Enterprise Size (Large Enterprises and Small and Medium Enterprises), Industry (IT and Telecom, Industrial Manufacturing, Healthcare and Life Sciences, Retail and Ecommerce, Energy and Utilities, Transportation and Logistics, BFSI, Construction and Engineering, Government, Defense, and Public Sector), and Geography (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, and Bahrain).

| Technical Skills Training |

| Digital Transformation, AI and Data Training |

| Cybersecurity Training |

| Leadership and Management Training |

| Soft Skills and Behavioral Training |

| Sales and Commercial Excellence Training |

| Compliance, Risk and ESG Training |

| Diversity, Equity and Inclusion (DEI) Training |

| Industry-specific Functional Training |

| Online Self-paced Learning |

| Virtual Instructor-led Training (VILT) |

| Classroom Instructor-led Training |

| Blended Learning |

| Mobile Learning and Microlearning |

| AI-powered Adaptive Learning |

| AR/VR Immersive Training |

| Large Enterprises |

| Small and Medium Enterprises |

| IT and Telecom |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Retail and Ecommerce |

| Energy and Utilities |

| Transportation and Logistics |

| BFSI |

| Construction and Engineering |

| Government, Defense, and Public Sector |

| Other End-user Industries |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Training Type | Technical Skills Training |

| Digital Transformation, AI and Data Training | |

| Cybersecurity Training | |

| Leadership and Management Training | |

| Soft Skills and Behavioral Training | |

| Sales and Commercial Excellence Training | |

| Compliance, Risk and ESG Training | |

| Diversity, Equity and Inclusion (DEI) Training | |

| Industry-specific Functional Training | |

| By Delivery Mode | Online Self-paced Learning |

| Virtual Instructor-led Training (VILT) | |

| Classroom Instructor-led Training | |

| Blended Learning | |

| Mobile Learning and Microlearning | |

| AI-powered Adaptive Learning | |

| AR/VR Immersive Training | |

| By End User Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By End-user Industry | IT and Telecom |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Retail and Ecommerce | |

| Energy and Utilities | |

| Transportation and Logistics | |

| BFSI | |

| Construction and Engineering | |

| Government, Defense, and Public Sector | |

| Other End-user Industries | |

| By Geography | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

What is the GCC corporate training market size in 2026?

The GCC corporate training market stands at USD 13.94 billion in 2026 and is projected to reach USD 22.21 billion by 2031 at a 9.76% CAGR.

Which GCC country leads corporate training demand?

Saudi Arabia led with a 45.12% share in 2025, supported by national development programs, public training infrastructure, and large enterprise demand.

Which training category is largest in the GCC?

Technical and digital skills training was the largest category with a 40.12% share in 2025, reflecting demand for AI, cybersecurity, and role-based digital capabilities.

Which delivery format is growing the fastest across GCC companies?

Virtual instructor-led training is the fastest-growing delivery format with a 12.64% CAGR through 2031, while online self-paced learning remained the largest in 2025.

Which business segment is expanding fastest in corporate learning across the GCC?

Small and medium enterprises are projected to grow at a 13.11% CAGR through 2031, helped by digital delivery, modular pricing, and public support programs.

Which end-user sector spends the most on corporate training in the GCC?

BFSI held the largest share at 35.23% in 2025 because regulatory compliance, certification cycles, and fintech transformation create recurring training demand.

Page last updated on: