GCC ITSM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

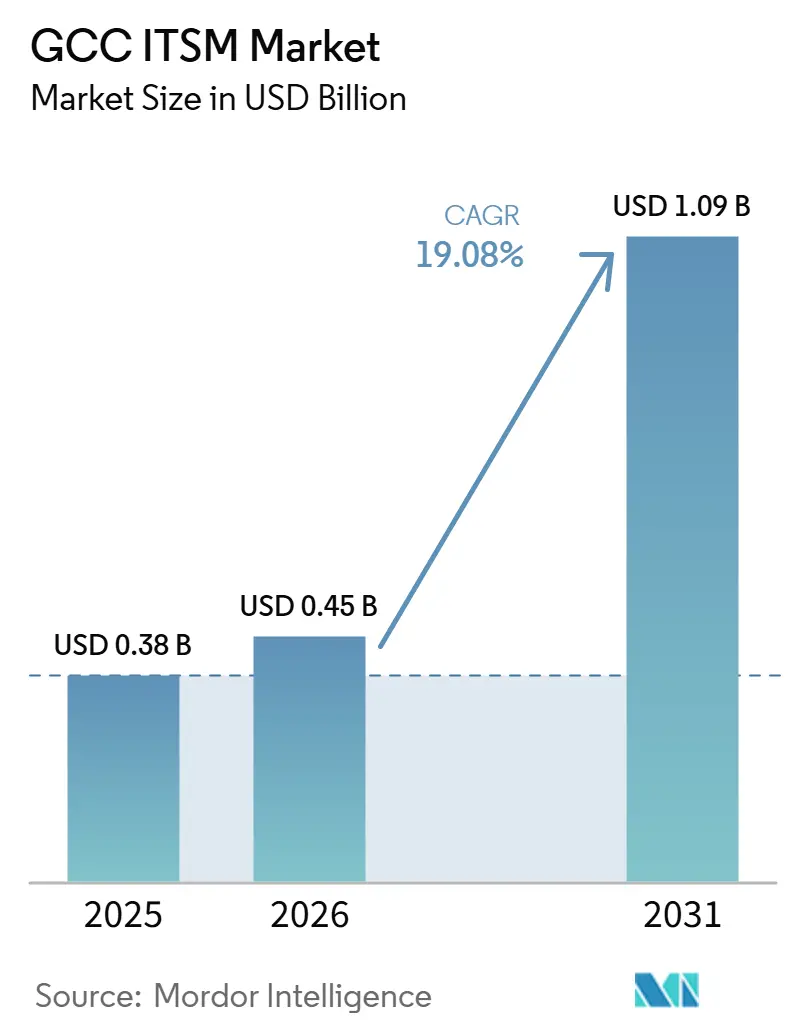

| Base Year Market Size (2025) | USD 0.38 Billion |

| Market Size (2026) | USD 0.45 Billion |

| Market Size (2031) | USD 1.09 Billion |

| Growth Rate (2026 - 2031) | 19.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC ITSM Market Analysis by Mordor Intelligence

The GCC ITSM Market size was valued at USD 0.38 billion in 2025 and is estimated to grow from USD 0.45 billion in 2026 to reach USD 1.09 billion by 2031, at a CAGR of 19.08% during the forecast period (2026-2031).

The GCC ITSM market is expanding because digital government programs, broader cloud adoption, and AI-led service automation are pushing organizations to formalize service operations across larger and more connected IT estates. Demand is also being shaped by a localization race, since vendors with in-country infrastructure, stronger Arabic-language support, and clearer compliance positioning are better placed to win regulated public and enterprise accounts. The market is also moving beyond large institutions, as modular pricing and lower deployment complexity are opening room for smaller enterprises that were previously outside the usual buyer base. At the same time, the GCC ITSM market still faces slower execution in some projects because legacy migrations remain difficult and experienced ITSM talent is limited across the region. Even with those limits, the operating case for structured service management remains strong because public agencies and enterprises are managing more digital services, more cloud workloads, and more workflow automation than before.

Key Report Takeaways

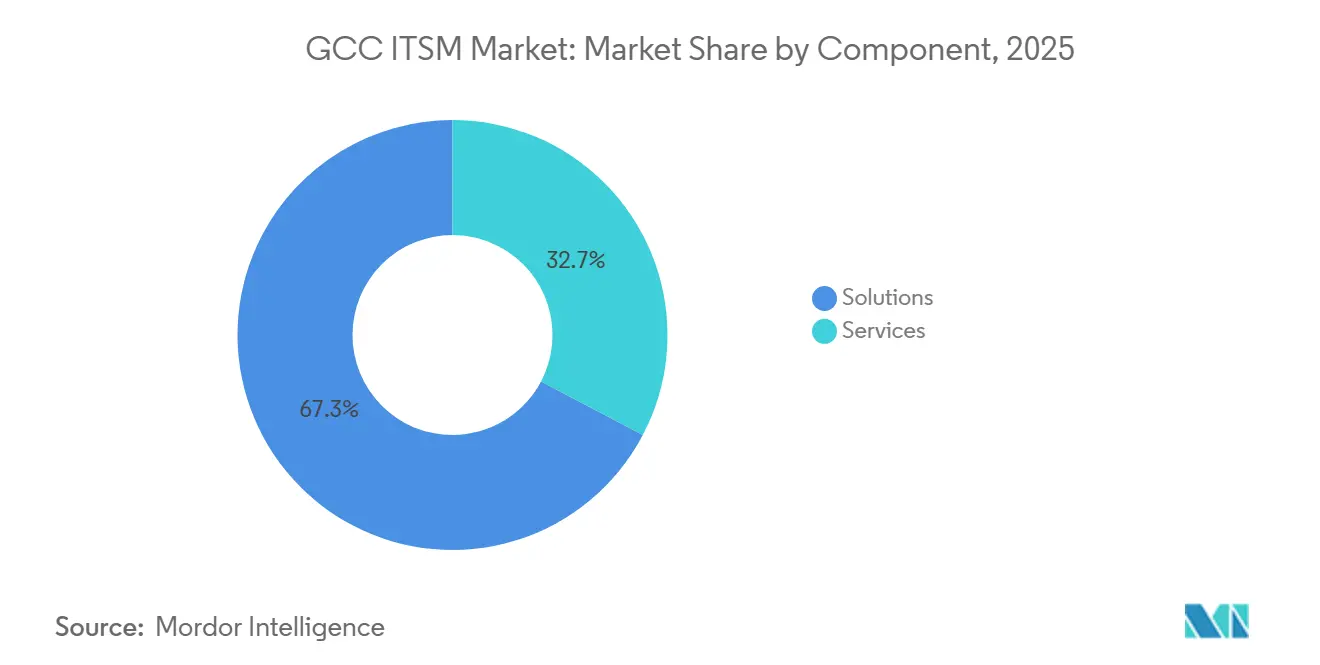

- By component, solutions held 67.30% share in 2025, while services are projected to expand at a 17.23% CAGR through 2031.

- By deployment, cloud held 72.10% of the GCC ITSM market share in 2025 and is projected to expand at an 18.37% CAGR through 2031.

- By application, service desk and incident management accounted for 30.70% share in 2025, while knowledge management is projected to grow at a 17.78% CAGR through 2031.

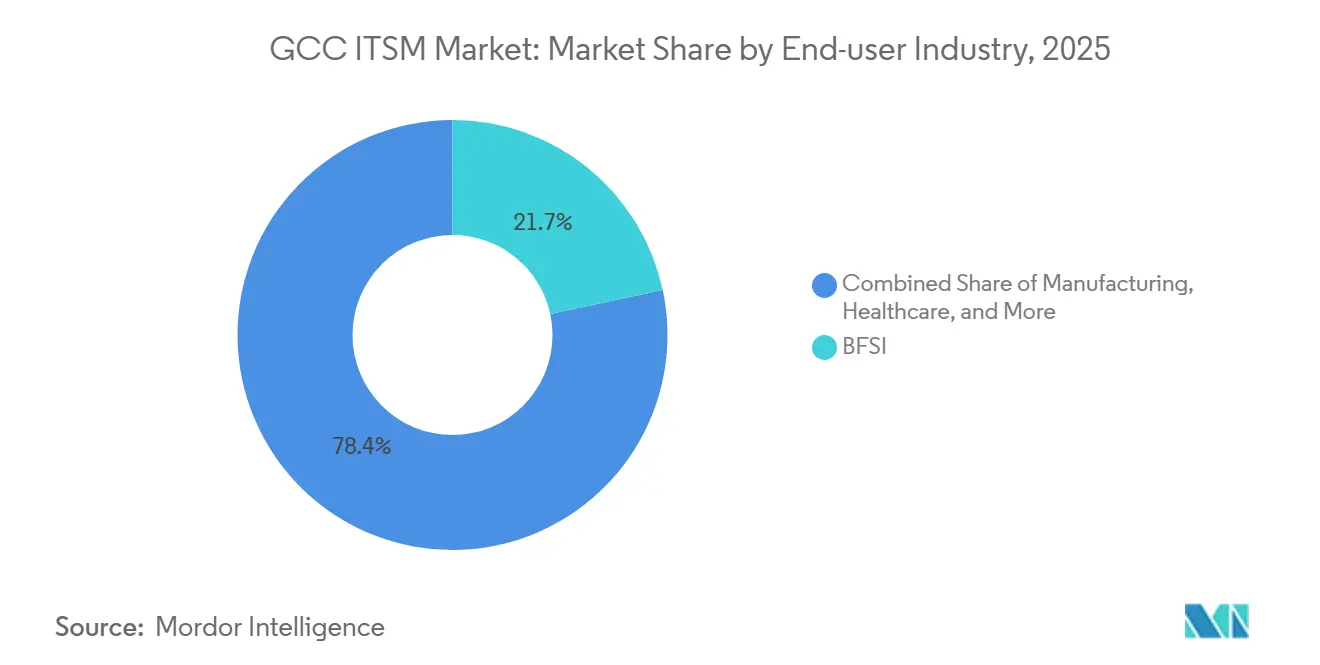

- By end-user industry, BFSI held 21.65% share in 2025, while healthcare is projected to expand at an 18.40% CAGR through 2031.

- By enterprise size, large enterprises held 64.20% share in 2025, while SMEs are projected to grow at a 17.80% CAGR through 2031.

- By country, Saudi Arabia held 46.40% share of the GCC ITSM market size in 2025, while the UAE is projected to expand at a 17.60% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC ITSM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-First Government And Enterprise Modernization | +4.2% | Global, with core gains in Saudi Arabia, UAE, and broader GCC | Short term (≤ 2 years) |

| AI-Enabled Service Automation And Ticket Deflection | +3.8% | Global, with GCC and Asia-Pacific leading public-sector adoption | Short term (≤ 2 years) |

| Multi-Cloud And Hybrid IT Complexity | +2.7% | North America and EU leading, strong spill-over to GCC | Medium term (2-4 years) |

| Low-Code Self-Service Workflow Expansion | +2.1% | Global, with early gains in UAE and Saudi Arabia enterprise segment | Long term (≥ 4 years) |

| FinOps And GreenOps Visibility Inside ITSM Workflows | +1.8% | Europe leading, expanding to GCC under ESG and sustainability mandates | Long term (≥ 4 years) |

| Edge, 5G, And Smart-Operations Support Demand | +1.5% | Asia-Pacific core, spill-over to GCC and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Government And Enterprise Modernization

Cloud-led modernization is a major growth engine for the GCC ITSM market because public institutions and large enterprises are standardizing service delivery across more digital systems. Saudi Arabia’s digital government policy framework is pushing agencies toward more structured governance, stronger operating controls, and clearer service accountability across public entities. The UAE also moved to tighten oversight of digital services in June 2026 when it established a federal AI and Data Authority to govern data quality, AI standards, and broader digital transformation compliance. These shifts matter because once services, data, and approvals are consolidated, incident, request, and change processes also need to be handled through consistent service management frameworks. That makes ITSM adoption less optional in many public-facing environments and more closely tied to policy execution and operating discipline.

AI-Enabled Service Automation And Ticket Deflection

AI is changing the GCC ITSM market from a system of record into a system of action, especially in environments with high service volume and repeated support requests. The UAE government launched its first set of AI agents in May 2026 across tax audits, procurement, customer service, and IT technical support, which shows that service automation is already moving into live government workflows[1]The National Staff, “UAE Launches First Batch of AI Agents to Aid Tax Audits and Customer Service,” The National, thenationalnews.com. Freshworks also introduced AI Agent Studio in Freshservice in 2026, giving IT and operations teams a no-code way to build service agents and automate resolution paths. As AI tools become part of daily support operations, buyers are placing more weight on autonomous workflow capability, knowledge reuse, and built-in governance than they did in earlier replacement cycles. This favors vendors that can combine automation speed with policy control in government, banking, healthcare, and other regulated settings.

Multi-Cloud And Hybrid IT Complexity

The GCC ITSM market is also benefiting from the fact that most large organizations are not moving into a single, simple cloud environment. Instead, they are adding new digital services while keeping sensitive systems, compliance data, or older workloads in separate environments that need to be managed together. ServiceNow’s plan to launch data centers in Saudi Arabia in 2026 shows how strongly buyers now value local hosting and closer alignment with sovereign infrastructure needs. OpenText’s October 2025 agreement with Core42 in the UAE also points to a broader push around sovereign cloud, AI infrastructure, and scalable digital services in the public sector. As estates become more mixed, enterprises need platform-neutral service governance that can connect incidents, assets, approvals, and change records across environments that do not sit under one stack or one operator. That is keeping ITSM relevant as a control layer rather than just a help desk tool.

Low-Code Self-Service Workflow Expansion

Low-code workflow design is widening the addressable base of the GCC ITSM market because it lowers the dependence on scarce specialist teams for every service change. Freshworks’ 2026 rollout of AI Agent Studio supports this shift by letting service owners configure automated workflows and agents through a no-code interface. This matters in the Gulf because many organizations are scaling digital services faster than they can hire experienced ITSM architects and workflow developers. A 2025 academic study on Saudi government entities found that workforce training and leadership commitment were primary enablers of ITSM maturity, which supports the case for tools that reduce the skills threshold for effective use. Low-code models also make it easier for HR, facilities, procurement, and other business functions to adopt service workflows without waiting on long development cycles from central IT teams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Migration Friction And Customization Lock-In | -2.8% | Global, most pronounced in Saudi Arabia and UAE large enterprise segment | Short term (≤ 2 years) |

| Shortage Of ITSM Architects And ITOM Skills | -2.2% | Global, with acute shortages across GCC technology hubs | Medium term (2-4 years) |

| Data Residency, AI Governance, And Compliance Constraints | -1.5% | GCC core, concentrated in Saudi Arabia, UAE, and Qatar | Medium term (2-4 years) |

| Tool Sprawl And Integration Overhead Across Point Solutions | -1.2% | Global, elevated risk in large GCC enterprise environments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Migration Friction And Customization Lock-In

Legacy migration remains a real brake on the GCC ITSM market because older service environments often contain years of local custom work that cannot be moved cleanly into newer platforms. The issue is not only software replacement, but also the need to preserve service history, approval logic, audit trails, and configuration records during transition. Saudi Arabia’s digital government policy direction places clear weight on governance, service continuity, and stronger public-sector operating standards, which raises the cost of getting migration wrong. The same pressure is visible in the UAE, where the new federal AI and Data Authority adds another layer of digital service oversight that organizations must accommodate as they modernize systems. This means even willing buyers can face longer project cycles when they move from older ticketing tools and heavily tailored workflows into more standardized cloud platforms.

Shortage Of ITSM Architects And ITOM Skills

The shortage of experienced ITSM architects and IT operations specialists is slowing the pace at which the GCC ITSM market can convert demand into live deployments. Organizations may be able to buy licenses quickly, but they still need experienced staff to design service models, govern automations, and connect monitoring data to operational workflows. The 2025 Saudi-focused academic work on ITSM maturity highlighted the value of training and leadership support, which shows that capability building is still central to successful rollout. The UAE Cabinet’s 2026 plan to train 80,000 employees in agentic AI also reflects how large the skills transition has become across public sector operations. AI features may reduce manual effort over time, but they do not remove the need for people who can set governance rules, escalation paths, service ownership models, and cross-platform controls.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Lead While Services Deepen Around Optimization Needs

Solutions held 67.30% share of the GCC ITSM market in 2025, which shows that software platform spending is still ahead of services spending in the current cycle. This reflects a market where many organizations first secured core platforms and only later moved into broader optimization, integration, and enterprise-wide workflow design. The GCC ITSM market has therefore been shaped by license-led adoption in its earlier phase, especially where public and large enterprise buyers moved quickly on platform selection. Services are projected to grow at a 17.23% CAGR from 2026 to 2031 as those early deployments mature, and buyers look for more value from automation, analytics, and cross-functional workflow expansion.

This second phase supports a wider role for implementation, integration, change management, and ongoing support partners. BMC said in February 2025 that it planned to expand its Saudi commitment and scale its certified regional partner headcount from 300 to more than 600 by 2030, which points to the growing need for delivery capacity around enterprise accounts[2]BMC, “BMC Expands Commitment to Saudi Arabia with New Regional HQ and Innovation Center,” Saudi News 247, saudinews247.com. At the same time, embedded AI is starting to reduce some of the manual work that once lifted services demand, especially for routine setup and service design tasks. Freshworks’ 2026 AI Agent Studio launch reinforces that shift by giving teams a faster way to automate workflows without heavy custom development.

By Deployment: Cloud Sets The Pace While Hybrid Stays Structurally Relevant

Cloud accounted for 72.10% of the GCC ITSM market size in 2025 and is also the fastest-growing deployment model with an 18.37% CAGR through 2031. This mix of leading share and leading growth shows that the market is still in an active transition phase rather than a settled one. The GCC ITSM market is gaining from buyer preference for faster deployment, lower infrastructure burden, and easier access to AI and workflow updates in cloud environments. Even so, on-premise and hybrid models remain relevant in sectors where data handling rules, internal control practices, or service continuity needs are stricter.

That is why hybrid is shaping up as a lasting operating model rather than just a step between legacy systems and full cloud. ServiceNow’s decision to launch Saudi data centers in 2026 addresses one side of this issue by improving local hosting, data residency comfort, and regional service delivery[3]ServiceNow, “US-Based ServiceNow to Launch Data Centers in Saudi Arabia in 2026,” Arab News, arabnews.com. OpenText’s agreement with Core42 in the UAE shows the same direction, as sovereign cloud and AI infrastructure are becoming central to public-sector digital programs. As a result, enterprises are likely to keep a mixed architecture where sensitive records remain tightly controlled while service automation and broader workflow orchestration continue to move into the cloud.

By Application: Service Desks Anchor Current Spend While Knowledge Management Gains Ground

Service desk and incident management held 30.70% share in 2025, which kept it as the largest application layer in the GCC ITSM market. This position makes sense because incident intake, ticket routing, and user support are usually the first areas organizations standardize when they begin formal IT service management. These functions also produce visible service metrics, which help budget owners justify investment. Knowledge management is projected to grow at a 17.78% CAGR through 2031 as organizations place more value on reusable answers, faster resolution, and more consistent service outcomes.

The role of knowledge is also changing because AI tools perform better when service teams have structured, current, and accessible information to work from. The 2025 Saudi government study found a direct relationship between stronger ITSM maturity and better service outcomes, including higher service uptime, which supports the case for better knowledge capture and process discipline. This is especially relevant in a bilingual operating environment where Arabic-language documentation and local workflow context matter for adoption. The GCC ITSM industry is also seeing service request management extend beyond core IT into HR, procurement, and facilities use cases, which increases the value of application breadth even when incident management remains the entry point.

By End-User Industry: BFSI Holds Scale While Healthcare Posts The Fastest Growth

BFSI held 21.65% share in 2025, which made it the largest end-user segment by revenue in the GCC ITSM market. Banks and financial institutions tend to adopt structured service management earlier because uptime, auditability, risk control, and service continuity are tightly linked to daily operations. Healthcare, however, is projected to grow at an 18.40% CAGR through 2031, which makes it the fastest-moving end-user group in the forecast period. That acceleration reflects the spread of electronic health records, telemedicine networks, and hospital information systems that require more disciplined service support and change control than older manual environments.

The gap between BFSI leadership and healthcare growth shows how sector maturity differs across the region. Highly governed sectors adopted formal ITSM earlier, while sectors that expanded digital infrastructure more recently are now moving through a faster catch-up phase. The GCC ITSM market size is also being supported by government and public sector demand, as public entities continue to standardize citizen-facing and internal service operations. At the same time, manufacturing and telecom are gaining importance as digital production systems, network infrastructure, and connected operations create more assets, more incidents, and more change activity to manage through one service framework.

By Enterprise Size: Large Enterprises Lead Revenue While SMEs Expand The Buyer Base

Large enterprises held 64.20% share of the GCC ITSM market in 2025, which reflects the resource intensity of full-platform deployments across complex IT estates. These buyers usually have the budgets, internal teams, and governance requirements needed to support broad rollouts across infrastructure, business services, and service automation programs. SMEs are projected to grow at a 17.80% CAGR from 2026 to 2031 as subscription-led delivery, modular packaging, and lower onboarding barriers improve affordability. This is widening the commercial reach of the GCC ITSM market beyond national champions, major banks, and large public organizations.

Growth among smaller buyers is not only a pricing story. Freshworks’ 2026 product launch supports this shift because no-code AI tools lower the operating threshold for companies that cannot fund large specialist teams. The UAE’s 2026 plan to train 80,000 employees in agentic AI also suggests that user expectations for faster and more intuitive service experiences will keep rising across organizations of different sizes. In practice, the most contested tier is the mid-market, where enterprise vendors are simplifying entry offers while lower-cost platforms add stronger workflow and governance features.

Geography Analysis

Saudi Arabia held 46.40% of the GCC ITSM market share in 2025, which made it the largest country market in the region. The country’s lead reflects the scale of its public digital programs, large enterprise base, and stronger policy push around structured digital government operations. Saudi Arabia’s digital government policy framework has formalized expectations around service quality, governance, and digital operating discipline across public entities. A 2025 academic study tied stronger ITSM maturity in Saudi government entities to better service uptime and better citizen outcomes, which supports the case for continued investment in formal service management capability. The country also remains central to vendor localization strategy, since platforms that can support Saudi hosting, compliance needs, and Arabic-first operating environments are better positioned to win large public and regulated accounts.

The UAE is projected to grow at a 17.60% CAGR through 2031, which makes it the fastest-growing geography in the GCC ITSM market. The April 2026 federal plan to convert 50% of government operations to agentic AI within 2 years shows how deeply service workflows are being redesigned[4]The National Staff, “UAE Targets Agentic AI to Power Half of Government Operations,” The National, thenationalnews.com. That shift became more concrete in May 2026 when the government launched its first 4 AI agents across tax audits, procurement, customer service, and IT technical support. The June 2026 creation of the federal AI and Data Authority, along with the approved training of 80,000 employees in agentic AI, points to a broad operating transition that places workflow governance and service control at the center of execution. Abu Dhabi’s AED 13 billion Digital Strategy 2025-2027, USD 3.5 billion, reinforces that direction by targeting full automation of government services over the strategy period.

Qatar, Kuwait, Oman, and Bahrain together account for the remaining share of the GCC ITSM market and each is progressing from a different base. Bahrain ranked within the top 40 globally in the UN E-Government Survey 2024, which supports its position as a steady digital government market within the Gulf[5]United Nations Department of Economic and Social Affairs, “UN E-Government Survey 2024,” United Nations, un.org. Kuwait is drawing more delivery ecosystem attention, and Deloitte’s 2026 expansion of its ServiceNow alliance into Kuwait shows that advisory, implementation, and managed services capacity is broadening around local demand. Oman and Qatar are also moving through digital government and enterprise modernization programs that will require stronger service governance as new systems scale. The smaller GCC markets should also benefit from localization investments already made for Saudi Arabia and the UAE, because in-region infrastructure, Arabic-language support, and partner capacity can be extended with lower incremental effort across the rest of the bloc.

Competitive Landscape

The GCC ITSM market remains moderately fragmented, with a clear leadership layer but no single vendor that closes the field to meaningful challengers. Competition is strongest among global platforms that can combine enterprise workflow depth with regional delivery, compliance positioning, and a more credible localization story. ServiceNow continues to hold a leading strategic position in the GCC ITSM market because it has invested early in regional scale and broader platform breadth. In February 2025, Arab News reported that ServiceNow planned to launch Saudi data centers in 2026, which strengthened its position in a market where local hosting and regulated sector trust matter. This raises the entry bar for vendors that still depend on offshore delivery or a thinner regional operating base.

BMC is also strengthening its regional footprint. In February 2025, BMC established a regional headquarters and innovation center in Riyadh and said it planned to raise its Saudi investment from USD 60 million to USD 150 million by 2030 while expanding its certified partner base. These moves show that competition in the GCC ITSM market is now shaped as much by local ecosystem depth as by product functionality. Vendors that can support implementation, training, language needs, and compliance discussions on the ground are better placed to retain pricing power.

Another competitive shift is coming from AI-led simplification and partner ecosystem expansion. Freshworks’ 2026 AI Agent Studio launch shows how mid-market and upper-mid-market vendors are using no-code automation to shorten time to value and challenge heavier deployment models. In September 2025, NextEra, backed by LTIMindtree and Aramco Digital, partnered with ServiceNow to accelerate digital transformation in the Middle East, which signaled deeper partner activation around leading platforms. The competitive picture therefore remains active rather than settled, with ServiceNow, BMC, Freshworks, ManageEngine, Ivanti, and Zendesk all relevant across different buyer tiers, use cases, and deployment preferences.

GCC ITSM Industry Leaders

ServiceNow, Inc.

BMC Software, Inc.

IBM Corporation

Atlassian Corporation

Ivanti, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: The UAE federal government established a new Artificial Intelligence and Data Authority, consolidating three previously separate regulatory entities under a unified mandate to govern federal data quality, AI standards, and digital transformation compliance. The authority's formation directly affects ITSM procurement frameworks for federal entities seeking compliant AI-powered service management platforms.

- June 2026: Deloitte expanded its ServiceNow strategic alliance into Kuwait, offering advisory, implementation, and managed services across IT, employee, customer, and industry workflows. The expansion covers government, financial services, energy, and national infrastructure sectors in line with Kuwait's national digital modernization agenda.

- May 2026: Freshworks unveiled AI Agent Studio in Freshservice, enabling IT and operations teams to build AI-powered service agents without coding through a no-code visual interface. The product also introduced an MCP Gateway bridging Freshservice with external AI tooling ecosystems.

- October 2025: OpenText signed a strategic Memorandum of Understanding with Core42, a G42 company specializing in sovereign cloud and AI infrastructure, to accelerate AI, cloud, and automation initiatives across the UAE public sector. The collaboration targets sovereign, scalable digital solutions for UAE government services aligned with the country's national technology leadership strategy.

GCC ITSM Market Report Scope

IT Service Management (ITSM) is the set of repeatable practices, processes, and enabling technologies used by organizations to plan, provision, operate, secure, and optimize IT‑delivered services for internal and external customers. It covers the full service lifecycle service strategy, design, transition, operation, and continual improvement, and includes core domains such as incident, problem, change, configuration, request, asset, and knowledge management, plus service-catalog and SLA governance.

The Gulf Cooperation Council (GCC) ITSM Market Report is Segmented by Component (Solutions and Services), Deployment (Cloud, On-premise, and Hybrid), Application (Service Desk and Incident Management, Asset and Configuration Management, Change and Release Management, Service Request Management, Knowledge Management, and Other Applications), End-user Industry (BFSI, Manufacturing, Government and Public Sector, IT and Telecommunications, Retail and E-commerce, Healthcare, Travel and Hospitality, and Other End-user Industries), Enterprise Size (Large Enterprises and Small and Mid-size Enterprises (SME)), and Country (Saudi Arabia, United Arab Emirates, Qatar, Kuwait, Oman, and Bahrain). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Services |

| Cloud |

| On-premise |

| Hybrid |

| Service Desk and Incident Management |

| Asset and Configuration Management |

| Change and Release Management |

| Service Request Management |

| Knowledge Management |

| Other Applications |

| BFSI |

| Manufacturing |

| Government and Public Sector |

| IT and Telecommunications |

| Retail and E-commerce |

| Healthcare |

| Travel and Hospitality |

| Other End-user Industries |

| Large Enterprises |

| Small and Mid-size Enterprises (SME) |

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| By Component | Solutions |

| Services | |

| By Deployment | Cloud |

| On-premise | |

| Hybrid | |

| By Application | Service Desk and Incident Management |

| Asset and Configuration Management | |

| Change and Release Management | |

| Service Request Management | |

| Knowledge Management | |

| Other Applications | |

| By End-user Industry | BFSI |

| Manufacturing | |

| Government and Public Sector | |

| IT and Telecommunications | |

| Retail and E-commerce | |

| Healthcare | |

| Travel and Hospitality | |

| Other End-user Industries | |

| By Enterprise Size | Large Enterprises |

| Small and Mid-size Enterprises (SME) | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain |

Key Questions Answered in the Report

What is the current size of the GCC ITSM market?

The GCC ITSM market is valued at USD 0.45 billion in 2026 and is projected to reach USD 1.09 billion by 2031 at a CAGR of 19.08%.

Which deployment model is leading GCC IT service management adoption?

Cloud is the leading model, with 72.10% share in 2025, and it is also the fastest-growing deployment type with an 18.37% CAGR through 2031.

Which sectors are driving demand across the Gulf?

BFSI led by revenue share at 21.65% in 2025, while healthcare is the fastest-growing sector with an 18.40% CAGR as digital care systems expand.

Why is Saudi Arabia the largest country market in the region?

Saudi Arabia held 46.40% share in 2025 because of its scale, public digital modernization agenda, and stronger policy push around formal digital service governance.

Why is the UAE growing faster than other GCC countries?

The UAE is projected to grow at a 17.60% CAGR through 2031 because federal AI adoption, workforce training, and tighter digital governance are accelerating workflow modernization.

What is shaping vendor competition in GCC ITSM platforms?

Competition is being shaped by localization, in-country hosting, partner depth, and AI workflow capability, with ServiceNow, BMC, Freshworks, ManageEngine, Ivanti, and Zendesk remaining relevant across buyer tiers.

Page last updated on: