AI-powered Corporate Training Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.49 Billion |

| Market Size (2031) | USD 18.19 Billion |

| Growth Rate (2026 - 2031) | 19.43% CAGR |

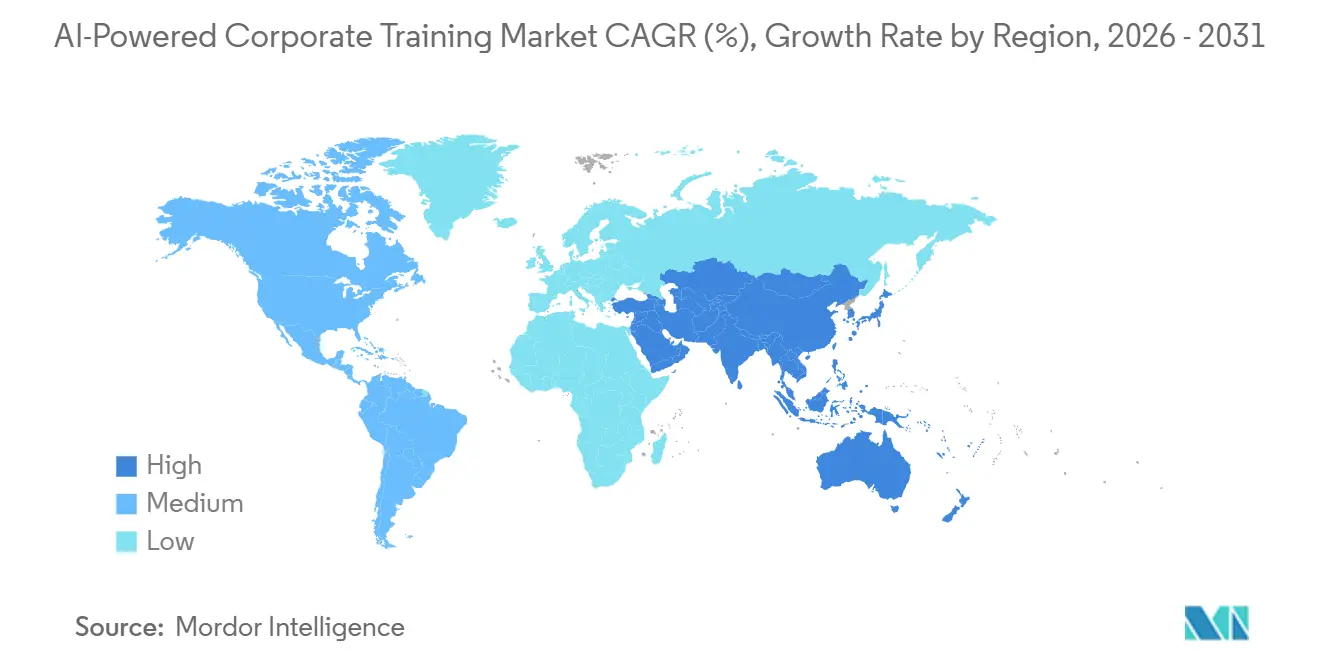

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-powered Corporate Training Market Analysis by Mordor Intelligence

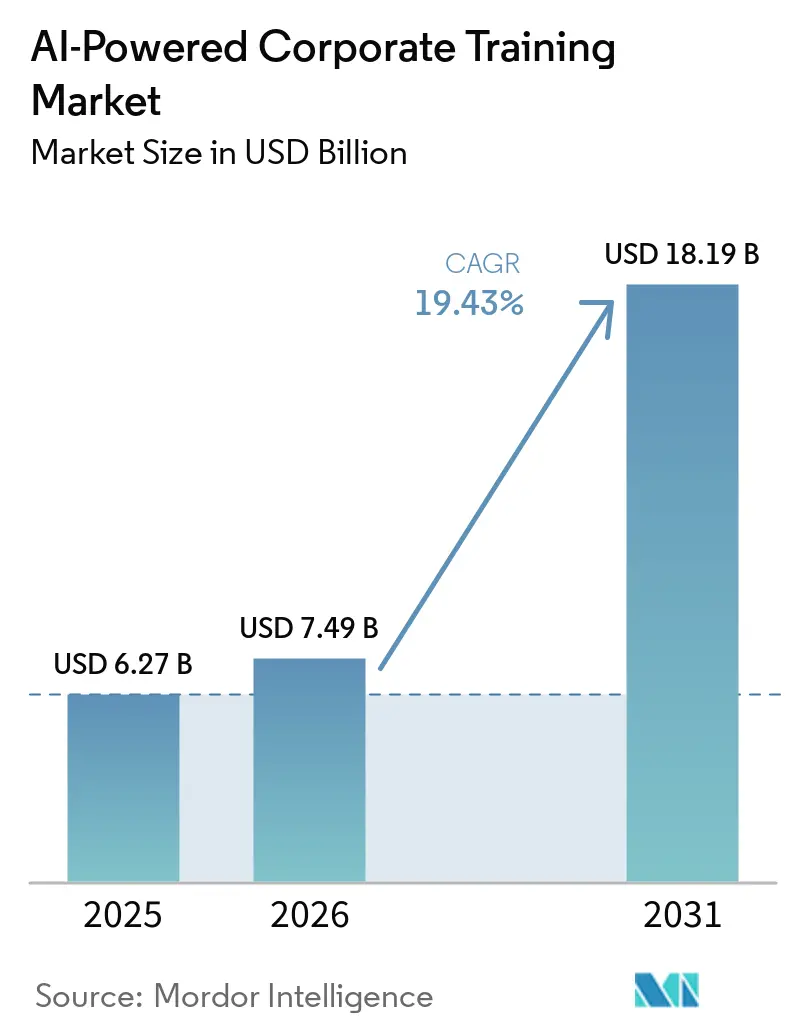

The AI-powered Corporate Training Market size is expected to grow from USD 6.27 billion in 2025 to USD 7.49 billion in 2026 and is forecast to reach USD 18.19 billion by 2031 at 19.43% CAGR over 2026-2031. Growth is being pushed by faster skill obsolescence, wider use of generative AI in daily work, and the steady shift of learning budgets from periodic programs to continuous reskilling systems. Enterprises are also moving AI-powered learning beyond the learning and development function and into HCM suites, ERP workflows, and collaboration tools, which is changing how vendors position their products and how buyers measure value. Competitive pressure is increasing as established suite vendors add LLM-driven coaching, adaptive learning, and skills intelligence into existing enterprise software stacks, while AI-native players try to differentiate through stronger personalization and workflow fit. The commercial model is also changing as verified skills, micro-credentials, and internal mobility links push buyers toward contracts tied more closely to workforce readiness outcomes than to seat counts alone. This creates room for vendors that can combine trusted enterprise data access, measurable skills validation, and low-friction deployment across large and distributed employee bases.

Key Report Takeaways

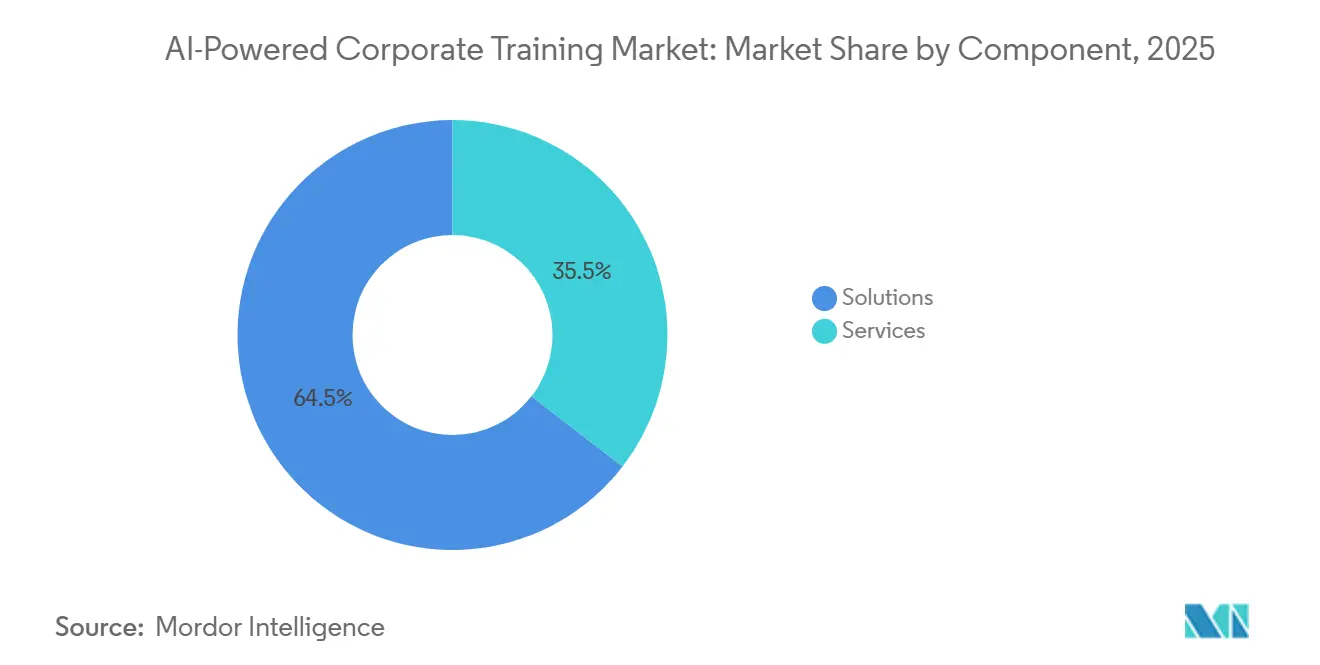

- By component, solutions held 64.52% of revenue in 2025 in the AI-powered Corporate Training Market, while services are projected to expand at a 20.27% CAGR through 2031.

- By deployment model, cloud accounted for 78.44% of revenue in 2025 and is projected to grow at a 21.42% CAGR through 2031.

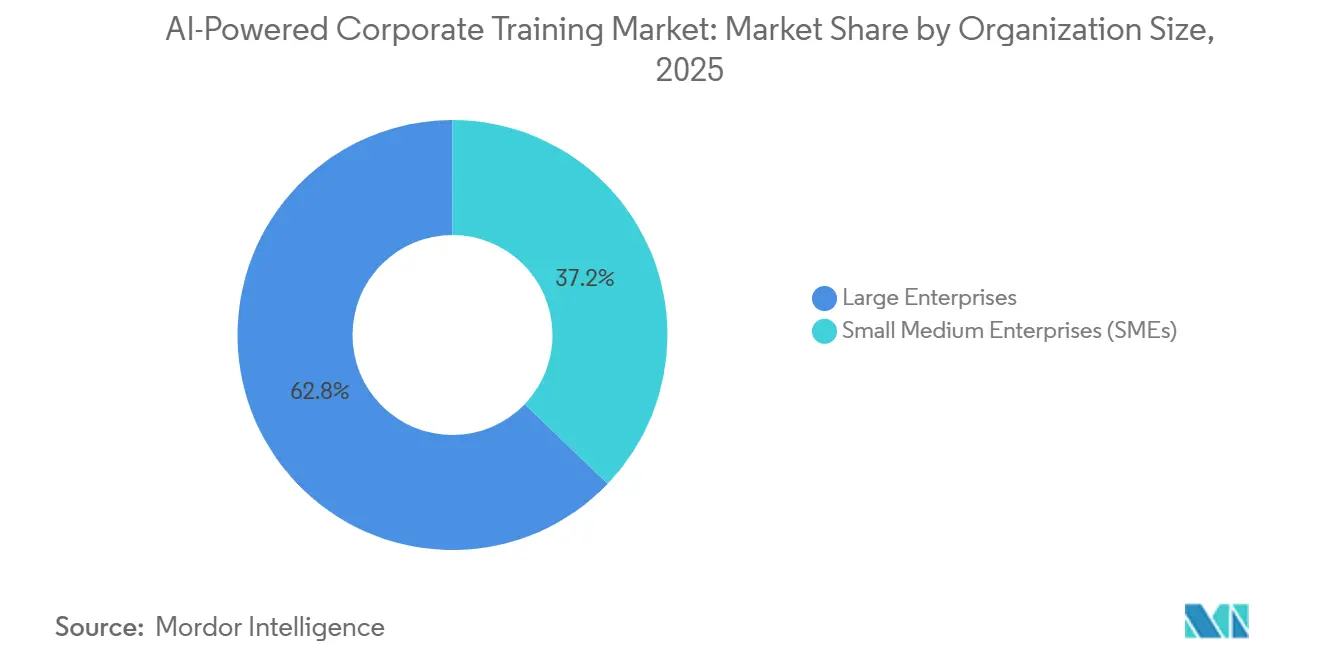

- By organization size, large enterprises represented 62.83% of revenue in 2025, while SMEs are expected to expand at a 21.93% CAGR through 2031.

- By end-user industry, IT and Telecom accounted for 24.92% of revenue in 2025, while healthcare and life sciences are projected to grow at a 23.51% CAGR through 2031.

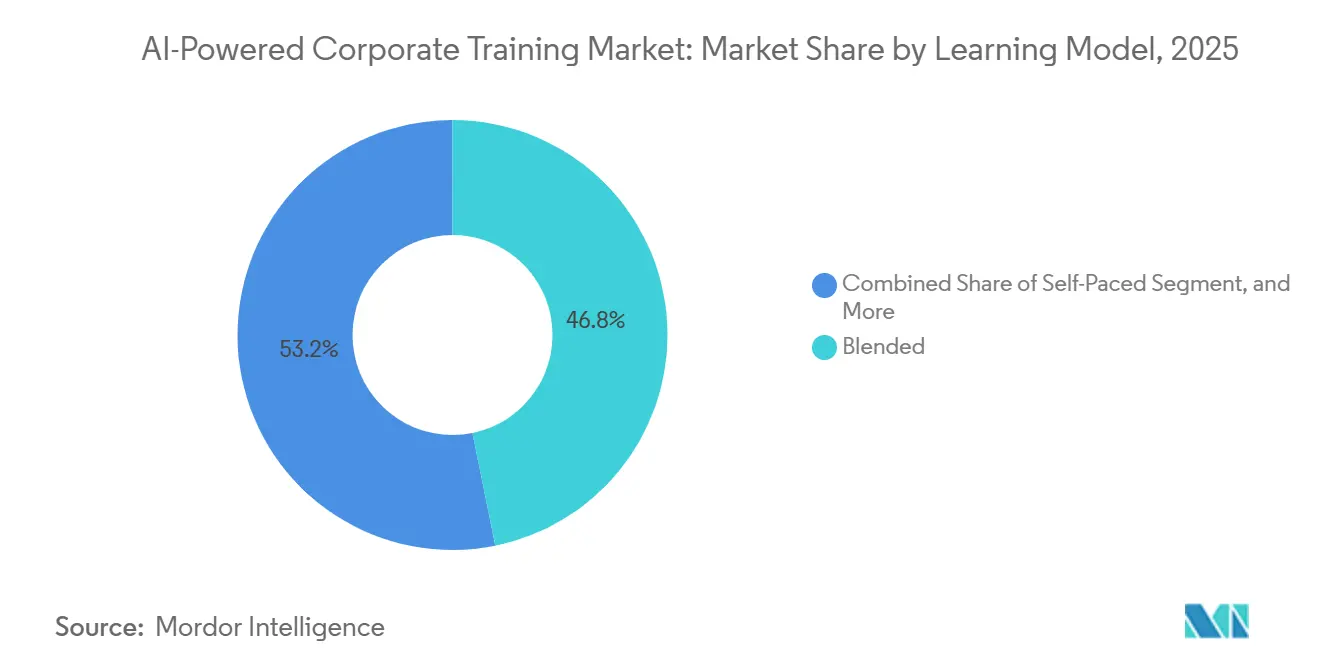

- By learning model, blended learning captured 46.81% of revenue in 2025, while AI-tutor-led learning is projected to grow at a 21.23% CAGR through 2031.

- By technology, machine learning accounted for 41.73% of revenue in 2025, while speech and voice recognition is projected to expand at a 24.71% CAGR through 2031.

- By geography, North America held 38.74% of the AI-powered Corporate Training Market share in 2025, while Asia-Pacific is projected to grow at a 20.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-powered Corporate Training Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid Skills Half-Life in Tech Roles | +4.5% | Global, with acute exposure in North America and Asia-Pacific | Short term (≤ 2 years) |

| Explosion of Remote and Hybrid Workforces | +3.8% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Rising Enterprise Spend on Personalized Learning Pathways | +3.2% | North America and Asia-Pacific core | Medium term (2-4 years) |

| Integration of LLM-Powered Coaching Bots With ERP-HCM Data | +2.8% | North America and EU, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Auto-Generated Micro-Credentials Linked to Internal Talent Marketplaces | +2.1% | North America and UK, emerging in Asia-Pacific | Medium term (2-4 years) |

| ESG-Driven Mandates For Continuous Reskilling Disclosures | +1.5% | EU-led, with early adoption in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Skills Half-Life Is Redefining The Training Procurement Cycle

The AI-powered Corporate Training Market is being shaped by the shrinking usable life of technical skills, especially in digital and data-heavy roles. The World Economic Forum reported that 39% of existing workforce skill sets will transform or become outdated by 2030, and 63% of employers identified skill gaps as the biggest barrier to business transformation.[1]World Economic Forum, “Future of Jobs Report 2025,” World Economic Forum, weforum.org This makes annual training refreshes less effective because role requirements are now shifting inside active business cycles rather than between them. The AI-powered Corporate Training Market is therefore moving toward always-on content updates, adaptive pathways, and frequent validation of role readiness instead of static catalogs. A 2026 study in Frontiers in Artificial Intelligence described reskilling fatigue as a real cognitive and motivational burden, which means platform design now matters as much as content breadth for sustained adoption. Vendors that can refresh learning in smaller steps and tie it to real work context are better placed to hold enterprise contracts as continuous reskilling becomes a normal operating expense.

Remote and Hybrid Workforce Proliferation Drives Infrastructure Investment

The AI-powered Corporate Training Market continues to benefit from the lasting shift to remote and hybrid work because training systems now need to serve employees across locations, time zones, and devices. Cloud deployment led with 78.44% share in 2025, which reflects the need for elastic compute, centralized content management, and live data connections across distributed organizations. A less visible effect of hybrid work is that asynchronous learning makes it harder for employers to compare actual skill levels across teams, which raises demand for stronger benchmarking and verifiable credentials. Skillsoft said AI-related Skill Benchmark completions on Percipio rose 994% year over year from December 2024 to December 2025, while AI content completions increased 261% and AI achievement badges rose 241%. Those usage patterns show that buyers are no longer satisfied with completion rates alone and are instead asking for evidence that training improves job readiness. The AI-powered Corporate Training Market is gaining from this shift because platforms that combine delivery, assessment, and workforce signal tracking are becoming more relevant than standalone content libraries.

Rising Enterprise Spend on Personalized Learning Pathways

The AI-powered Corporate Training Market is also being lifted by enterprise demand for learning pathways that reflect each employee’s role, skill gaps, and likely career movement. Skillsoft reported 146% year-over-year growth in usage of its CAISY conversational learning experience in 2025, with simulation launches growing 2.3 times faster than the overall learner base. That pattern supports the view that enterprises are spending more on guided practice and personalized reinforcement because generic course libraries do not reliably produce behavior change. Large enterprises, which held 62.83% of revenue in 2025, are leading this shift because they have the scale, skills, data, and internal mobility needed to justify deeper platform deployments. Cornerstone said in May 2026 that 46% of employees were using AI tools at work without formal employer training, while 65% were building AI skills independently outside work to remain competitive. As a result, the AI-powered Corporate Training Market is increasingly being evaluated on its ability to surface promotable talent, close verified skill gaps, and link learning outcomes to workforce decisions.

LLM-Powered Coaching Bots Integrating With ERP-HCM Data Pipelines

The AI-powered Corporate Training Market is entering a new phase as LLM-based coaching and learning assistants move closer to live workforce data inside enterprise systems. SAP launched its Workforce Upskilling Assistant in May 2026 and positioned it to deliver adaptive microlearning via Joule Agents, leveraging real-time HCM and business data.[2]SAP, “SAP Sapphire 2026 Workforce Upskilling Assistant Announcement,” SAP, sap.com Oracle extended this pattern in April 2026 with Fusion Agentic Applications for HR, where targeted development recommendations are delivered within Oracle Fusion Cloud HCM workflows. This changes the competitive standard because learning recommendations can now reflect role, project pipeline, performance history, and immediate workflow context, rather than only past course activity. Standalone systems that cannot connect to live ERP and HCM data are likely to face a harder sales process because their personalization depth is more limited. The AI-powered Corporate Training Market is, therefore, rewarding vendors that can move learning from scheduled enrollment into the natural flow of work without losing governance or auditability.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Up-Front Integration and Content-Conversion Costs | -3.2% | Global, most acute in SMEs and emerging markets | Short term (≤ 2 years) |

| Data-Privacy and Intellectual-Property Concerns | -2.8% | EU and North America, compliance factors from GDPR, EU AI Act | Short term (≤ 2 years) |

| Shadow-Learning Risk From Unsanctioned Gen-AI Tools | -2.1% | Global, particularly North America and EU | Medium term (2-4 years) |

| Algorithmic Bias Audits Delaying Procurement Cycles | -1.5% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Integration and Content-Conversion Costs Slow Adoption

The AI-powered Corporate Training Market still faces a meaningful adoption barrier in the cost and effort needed to convert legacy content and connect new systems to existing enterprise software. Much of the installed course base was designed for older learning formats, so adaptive delivery, AI-based feedback, and conversational practice often require full redesign rather than light editing. That burden is especially visible among SMEs, even though the segment is projected to grow at 21.93% through 2031, because upfront conversion and integration work can approach the cost of the software itself. Integration with Workday, SAP SuccessFactors, Oracle HCM, and identity tools adds another layer of implementation complexity around permissions, APIs, governance rules, and data mapping. SAP’s Learning Compliance Agent and Docebo’s MCP-based architecture both show that vendors are trying to reduce this friction with prebuilt connectors and embedded automation. Even so, the AI-powered Corporate Training Market still favors buyers that can absorb implementation effort, which keeps adoption more uneven than top-line demand might suggest.

Data-Privacy and Intellectual-Property Concerns Dampen Platform Confidence

The AI-powered Corporate Training Market is also constrained by privacy, governance, and intellectual-property risks because training systems increasingly interact with sensitive employee and enterprise data. GDPR requires organizations to ensure documented data-processing awareness for staff handling personal data, and the EU AI Act requires AI literacy measures while adding stricter obligations for high-risk employment uses from August 2026. These rules lengthen buying cycles because enterprises must review not only platform features but also data lineage, human oversight, audit trails, and recordkeeping. A 2025 State of Shadow AI report highlighted the scale of the challenge, showing that 91% of AI tools in enterprise environments operated outside IT control and that organizations averaged 269 unsanctioned AI applications per 1,000 employees. That shadow-learning pattern increases concern that proprietary content, employee performance information, or regulated data could move into tools outside approved workflows. The AI-powered Corporate Training Market, therefore, sees stronger demand for controlled deployment models, tighter permissions, and architectures that keep learning personalization compatible with compliance requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Anchor Revenue While Services Capture Complexity

Solutions held 64.52% of the AI-powered Corporate Training Market share in 2025, which confirms that the platform layer remains the core revenue engine for enterprise buyers. This segment covers AI-powered learning platforms, adaptive personalization engines, skills intelligence tools, content generation applications, assessment systems, conversational assistants, and immersive training environments. Buyers continue to spend most heavily on solutions because they want a single operating layer that can manage discovery, personalization, delivery, verification, and analytics across the learning cycle. The depth of this layer also explains why solutions continue to command a larger share, even as enterprise expectations become more outcome-focused. In the AI-powered Corporate Training Market, the solution stack has become the system of record for workforce learning signals rather than a simple catalog of digital courses.

Platform consolidation is reinforcing that position, as leading vendors are trying to unify fragmented learning functions within broader product architectures. Docebo launched AgentHub in April 2026 to connect skills intelligence, enterprise knowledge, and agentic AI within a single closed-loop environment, and it also introduced an MCP Server so Docebo could serve as a native knowledge source within LLMs such as Microsoft Copilot.[3]Docebo, “Docebo AgentHub And MCP Server Announcement,” Docebo, docebo.com At the same time, SAP said 62% of C-suite executives surveyed in April 2026 were dissatisfied with the way people data connected to business performance, which strengthens demand for analytics that link training to operating outcomes. Services remain smaller in share, but they are projected to grow at 20.27% through 2031, as enterprises need support with content conversion, model tuning, implementation, analytics, and performance-linked advisory services. The AI-powered Corporate Training Market is therefore seeing services gain importance not because software is losing relevance, but because large deployments are harder to operationalize without ongoing vendor involvement.

By Deployment Model: Cloud Dominates And Alternative Models Stay Relevant In Sensitive Environments

Cloud accounted for 78.44% of AI-powered Corporate Training Market size in 2025, which reflects the technical needs of adaptive learning, LLM inference, skills mapping, and continuous data synchronization. The segment is also projected to expand at 21.42% through 2031, which shows that market leadership at scale has not reduced its growth momentum. Cloud remains the preferred route because enterprises want faster updates, centralized administration, and easier integration with collaboration tools and HR platforms. It also supports the real-time feedback loops required for personalized learning journeys and measurable workforce readiness. In the AI-powered Corporate Training Market, cloud is now the default architecture for buyers that prioritize speed, scale, and broad employee access.

Recent product launches show why that advantage persists. Microsoft said its Learning Agent would integrate skill gap analysis and personalized learning plans into Microsoft 365 Copilot and Teams, a model that depends on the company’s cloud environment and embedded productivity stack. On-premise deployments still matter in defense, nuclear, and classified government settings because data sovereignty and security rules can make cloud SaaS impractical. Hybrid demand is also holding up in banking, financial services, insurance, and healthcare because these users often want cloud-side AI functionality while keeping sensitive records under tighter internal control. National data residency expectations in markets such as India, Germany, and China are sustaining that balance, which means the AI-powered Corporate Training Market is unlikely to become fully cloud-only even as cloud keeps widening its lead.

By Organization Size: Large Enterprises Lead While SMEs Open A New Volume Layer

Large enterprises held 62.83% of revenue in 2025, which shows that scale, procurement maturity, and integration capacity remain decisive in enterprise learning transformation. These organizations are better placed to fund software rollouts, connect learning platforms to existing HCM systems, and establish governance around AI use, data access, and skills taxonomies. They also have stronger incentives to invest because skill gaps across large workforces create measurable business risk in hiring, internal mobility, and project delivery. The AI-powered Corporate Training Market has therefore expanded first through large global customers that can absorb complexity and demand deep configuration. That pattern is reinforced by the fact that many leading vendors already sell into the same organizations through adjacent enterprise software relationships.

Cornerstone’s May 2026 launch of Workforce AI illustrates that scale bias clearly because the platform drew on data from 140 million users across 7,000 organizations in 186 countries. SMEs, however, are projected to grow faster at 21.93% through 2031 as vendors lower entry barriers through modular pricing, faster deployment, and lighter administration. The logic is straightforward because smaller employers also face AI skill gaps, but they cannot support long implementation cycles or large consulting engagements. In response, providers have widened rapid-deployment features, preconfigured integrations, and AI-assisted authoring to reduce the workload on lean HR and learning teams. The AI-powered Corporate Training Market is likely to gain a second growth layer from SMEs, but that expansion will depend on how successfully vendors reduce integration burden without sacrificing control or proof of outcomes.

By End-User Industry: IT And Telecom Sets The Revenue Base While Healthcare And Life Sciences Gain Speed

IT and Telecom held 24.92% of end-user revenue in 2025, which makes it the largest vertical in the AI-powered Corporate Training Market. This leadership is tied to the sector’s high technical skill intensity, stronger digital procurement processes, and early exposure to AI-driven role redesign. Tech employers were among the first to see that AI tools could automate parts of existing jobs while also creating new capability requirements across software, cloud, data, cybersecurity, and customer operations. That combination gave them both the urgency and the implementation capacity to invest sooner than other industries. In the AI-powered corporate training industry, IT and Telecom still acts as the baseline customer group against which product depth, workflow fit, and credentialing value are often tested.

Pluralsight’s AI Academy, launched in March 2026, was built directly around enterprise cohorts of 500 to 100,000 participants and structured learning levels that match this vertical’s demand for scalable, role-based skilling.[4]Pluralsight, “AI Academy Launch,” Pluralsight, pluralsight.com Healthcare and life sciences is projected to grow fastest at 23.51% through 2031 as hospital systems, pharmaceutical companies, and device manufacturers prepare workforces for AI use under tighter governance expectations. The FDA’s 2025 draft guidance and the EMA principles effective from 2026 both increased the practical need for staff training around validation, transparency, and auditability in AI-related processes. CVS Health said in 2026 that it launched an AI Learning Academy and was rolling out tailored AI training across the organization, which reflects how healthcare employers are treating AI capability as an operating requirement instead of a limited experiment. The AI-powered Corporate Training Market is also seeing differentiated demand from BFSI, manufacturing, and retail, but healthcare stands out because capability building and compliance preparation are moving together.

By Learning Model: Blended Learning Stays In Front While AI-Tutor-Led Formats Build Momentum

Blended learning accounted for 46.81% of revenue in 2025, indicating that most enterprises still want human facilitation alongside AI-generated content and adaptive delivery. This model remains attractive because it preserves instructor oversight, supports live discussion, and fits regulated environments where observed assessment and sign-off still matter. It also helps organizations manage change because learners and managers can adopt AI tools gradually without abandoning familiar delivery methods. In the AI-powered Corporate Training Market, blended learning remains the most practical bridge between legacy training processes and more dynamic skill development models. Self-paced formats play an important role in global workforces, while instructor-led programs remain relevant where compliance sensitivity is high and direct observation carries legal or operational value.

The fastest growth is coming from AI-tutor-led learning, which is projected to advance at 21.23% through 2031 as organizations become more comfortable with simulated practice and conversational coaching. Skillsoft said CAISY simulation experience launches rose 341% in 2025 and grew 2.3 times faster than the overall learner base, indicating that users are engaging with guided conversation rather than just watching or reading content. Degreed added evolved custom rubrics for AI-driven role-play sessions at LENS 2026, so companies could align practice sessions with their organizational priorities and measure performance more consistently. That matters because open-ended dialogue generates richer learning signals than click-through completion data, but it also requires stronger analytics and governance. The AI-powered Corporate Training Market is therefore moving toward models in which AI handles more of the coaching between human touchpoints, while enterprise buyers still expect clear evidence that these interactions improve workplace performance.

By Technology: Machine Learning Provides The Base While Voice-Led Interaction Gains Speed

Machine learning held 41.73% of technology revenue in 2025, which keeps it at the center of the AI-powered Corporate Training Market. Its role is foundational because recommendation engines, adaptive pathways, skill inference, learner analytics, and content prioritization all depend on machine learning models. Natural language processing adds another major layer by enabling chatbot interactions, content understanding, automated tagging, and taxonomy management at enterprise scale. Computer vision remains important in immersive training use cases, especially where procedural tasks, safety workflows, or environment simulation matter. In the AI-powered corporate training industry, machine learning still underpins most commercially deployed features, even when those features are presented to buyers through conversational or multimodal interfaces.

Speech and voice recognition is the fastest-growing technology segment, with a 24.71% CAGR through 2031, and that signals a broader shift in how learning is triggered and consumed. SAP’s Workforce Upskilling Assistant and Microsoft’s Learning Agent both support conversational interactions inside workflow environments such as SAP Work Zone, Teams, and Microsoft 365, which moves training closer to daily task execution. That design pattern matters because voice and conversational data can reveal levels of confidence, comprehension, and practical reasoning that static course completion data often misses. It also points to a future in which training is activated by context rather than by scheduled enrollment, especially for knowledge work that now unfolds across collaboration platforms. The AI-powered Corporate Training Market is therefore starting to reward technology stacks that can capture richer interaction signals and turn them into timely learning interventions without adding friction to the employee workflow.

Geography Analysis

North America held 38.74% of the AI-powered Corporate Training Market share in 2025, which kept it as the largest regional revenue base. The United States accounted for the bulk of that position because it combines dense technology employment, mature enterprise software procurement, and a strong concentration of platform vendors and enterprise buyers. Canada and Mexico added momentum through growing technology ecosystems and nearshoring-linked upskilling needs, but the regional center of gravity remained in the United States. Another advantage is the depth of integration between learning systems and broader enterprise platforms, which makes it easier to personalize training using workforce data already housed in HCM and ERP environments. The AI-powered Corporate Training Market in North America also benefits from the fact that many global vendors build and test new AI learning features in this region before scaling them elsewhere.

Asia-Pacific is projected to grow at 20.58% through 2031, making it the fastest-growing regional segment in the AI-powered Corporate Training Market size. Growth is being supported by broad enterprise AI adoption, large workforce bases, and increasing pressure to close technical skill gaps across China, India, Japan, South Korea, and ASEAN markets. India stands out because enterprises are moving ahead with AI-human workforce models and treating AI capability building as a strategic requirement rather than a delayed program. Europe remains a significant market led by Germany, the United Kingdom, and France, where compliance requirements are shaping training demand as much as direct return-on-investment logic. The EU AI Act made AI literacy a formal requirement from February 2025 and expanded enforcement obligations from August 2026, which has created a more structured procurement case for documented corporate AI training. Germany’s estimated annual cost of unfilled vacancies reached EUR 339 billion (USD 383 billion), in findings cited by Coursera, which underlines the macroeconomic cost of underinvestment in skills development.

South America is still a smaller regional base, but Brazil and Argentina are emerging as practical growth pockets because technology-sector expansion and multinational presence are pushing formal AI training adoption. Cloud-native and multilingual deployments are most relevant there because enterprises often need to serve geographically spread and language-diverse workforces with limited implementation friction. The Middle East and Africa is more uneven, with Gulf Cooperation Council countries such as Saudi Arabia and the United Arab Emirates investing in AI workforce capability as part of national digitalization agendas. South Africa remains the most developed corporate training market on the African continent, while broader sub-Saharan adoption is still at an earlier stage.

Competitive Landscape

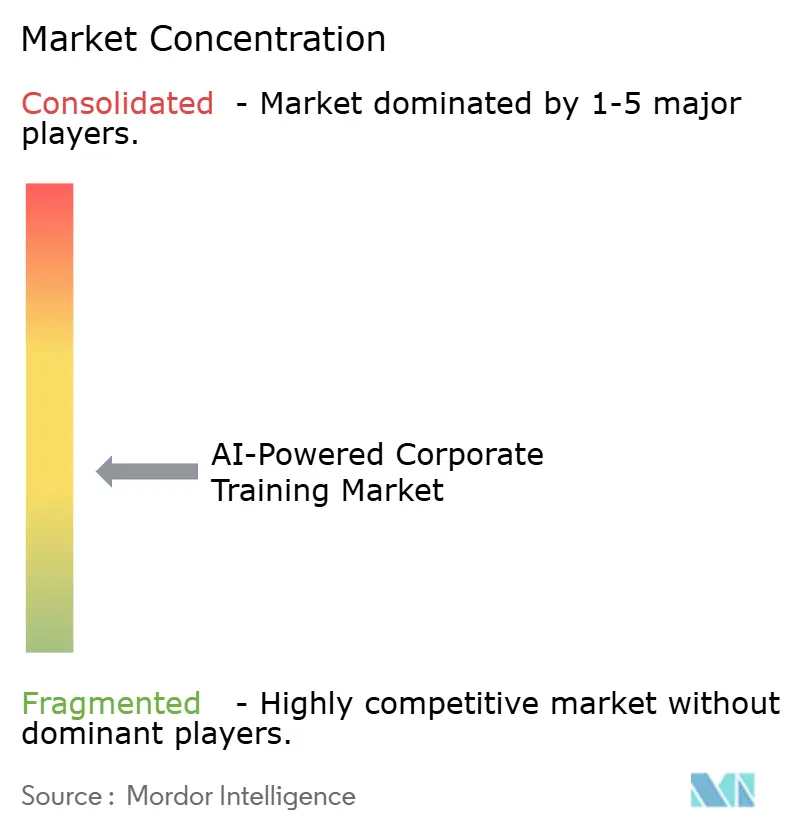

The AI-powered Corporate Training Market is moderately fragmented, but it is consolidating around scale, proprietary workforce data, and integration depth. Large platform companies such as Microsoft, Google, SAP, Oracle, and IBM are embedding learning and skills capabilities into software suites that enterprises already use for productivity, HR, and operations. That changes buyer behavior because standalone learning vendors must now prove not only content quality but also stronger workflow integration and measurable business value. The AI-powered Corporate Training Market is also separating into two broad groups, which are suite vendors extending existing enterprise footprints and AI-native players building around adaptive coaching, skills intelligence, and agentic interaction models. This combination keeps competition intense because both groups are trying to own the same budget line through different products and distribution advantages.

Cornerstone’s May 2026 release of Workforce AI showed how incumbents are using proprietary data assets as a moat, drawing on a large skills taxonomy and workforce profile base while extending distribution through Salesforce, Slack, and the AWS Marketplace.[5]Cornerstone OnDemand, “Cornerstone Workforce AI Launch And Salesforce Partnership Extension,” Cornerstone OnDemand, cornerstoneondemand.com SAP strengthened its position through the Workforce Upskilling Assistant and the H1 2026 Learning Compliance Agent, which together moved adaptive learning and compliance management deeper into existing enterprise workflows. Docebo took a different route by launching AgentHub and an MCP Server so enterprise knowledge and learner status could be surfaced natively inside LLM environments, which directly addresses interoperability as a buying criterion. These moves matter because they shift competition away from simple course delivery and toward embedded intelligence, data connectivity, and the ability to operate inside the tools employees already use every day.

Challengers are still able to reshape the field when they bring AI-native architectures and credible deployment proof. Cognizant launched Skillspring in April 2026 after first deploying it across hundreds of thousands of internal employees, which gave the product immediate scale credibility before external commercialization. Pluralsight also sharpened its enterprise pitch by structuring AI Academy around three progressive learning levels and large cohorts, which helps buyers that want clearer alignment between curriculum design and measurable workforce outcomes. White-space opportunities remain strongest in regulated sectors such as healthcare and financial services, where explainability, human oversight, bias auditing, and compliance recordkeeping are harder to solve through general-purpose learning platforms. The AI-powered Corporate Training Market is therefore likely to remain competitive and moderately fragmented in the near term, even as deeper enterprise integration gradually lifts switching costs and favors larger ecosystems.

AI-powered Corporate Training Industry Leaders

Microsoft Corporation

Coursera, Inc.

Skillsoft Corporation

Cornerstone OnDemand, Inc.

Udacity, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Cornerstone OnDemand launched Cornerstone Workforce AI, an intelligence platform for workforce readiness built on the Cornerstone People Graph with over 55,000 skills taxonomy entries and data from 140 million users across 7,000 organizations in 186 countries. The launch was accompanied by an extended partnership with Salesforce integrating Cornerstone Workforce AI across Agentforce, Slack, and the AWS Marketplace, strengthening Cornerstone's position at the intersection of skills intelligence and enterprise workflow execution.

- May 2026: SAP announced autonomous HCM innovations at SAP Sapphire in Orlando, including the Workforce Upskilling Assistant, orchestrated through multiple Joule Agents, which delivers personalized, AI-driven adaptive micro-learning and reinforcement directly within collaboration tools, mobile, desktop, and SAP SuccessFactors, enabling leaders to identify critical skill gaps from live business data and accelerate upskilling in fast-moving areas including AI.

- May 2026: Pluralsight launched Cloud Ready, an enterprise cloud upskilling program combining skill assessments, guided learning paths, certification preparation, hands-on labs, and cloud and AI sandboxes, targeting organizations undergoing cloud migration, AI infrastructure scaling, and cloud cost optimization.

- April 2026: Cognizant unveiled Cognizant Skillspring, a multimodal, AI-native conversational learning platform leveraging AI agent-driven tutoring and content creation deployed across hundreds of thousands of internal employees and made available to enterprise clients, framing AI upskilling as a core business infrastructure investment given the platform's finding that AI is capable of handling USD 4.5 trillion in U.S. work tasks.

Global AI-powered Corporate Training Market Report Scope

AI-Powered Corporate Training refers to the application of artificial intelligence technologies to develop, implement, and optimize employee learning and development programs. These platforms utilize machine learning, natural language processing, and predictive analytics to customize training content, automate administrative processes, and deliver real-time insights into workforce competencies.

The AI-powered Corporate Training Market Report is Segmented by Component (Solutions, and Services), Deployment Model (Cloud, On-Premise, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (IT and Telecom, BFSI, Manufacturing, Healthcare and Life Sciences, Retail and eCommerce, and Other End-User Industries), Learning Model (Self-Paced, Instructor-Led, and Blended), Technology (Machine Learning, NLP, Speech and Voice Recognition, Computer Vision, and Other Emerging AI Technology), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions | AI-powered Learning Platforms |

| Adaptive Learning and Personalization Engines | |

| AI Skills Intelligence Platforms | |

| AI Content Generation Tools | |

| AI Assessment and Learning Analytics | |

| Conversational AI Learning Assistants | |

| Immersive AI Training Platforms | |

| Services |

| Cloud |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small Medium Enterprises (SMEs) |

| IT and Telecom |

| BFSI |

| Manufacturing |

| Healthcare and Life Sciences |

| Retail and eCommerce |

| Other End-User Industries |

| Self-Paced |

| Instructor-Led |

| Blended |

| Machine Learning |

| Natural Language Processing |

| Speech and Voice Recognition |

| Computer Vision |

| Other Emerging AI Technology |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Solutions | AI-powered Learning Platforms | |

| Adaptive Learning and Personalization Engines | |||

| AI Skills Intelligence Platforms | |||

| AI Content Generation Tools | |||

| AI Assessment and Learning Analytics | |||

| Conversational AI Learning Assistants | |||

| Immersive AI Training Platforms | |||

| Services | |||

| By Deployment Model | Cloud | ||

| On-Premise | |||

| Hybrid | |||

| By Organization Size | Large Enterprises | ||

| Small Medium Enterprises (SMEs) | |||

| By End-User Industry | IT and Telecom | ||

| BFSI | |||

| Manufacturing | |||

| Healthcare and Life Sciences | |||

| Retail and eCommerce | |||

| Other End-User Industries | |||

| By Learning Model | Self-Paced | ||

| Instructor-Led | |||

| Blended | |||

| By Technology | Machine Learning | ||

| Natural Language Processing | |||

| Speech and Voice Recognition | |||

| Computer Vision | |||

| Other Emerging AI Technology | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of AI-powered corporate training?

The AI-powered Corporate Training Market was valued at USD 6.27 billion in 2025, stood at USD 7.49 billion in 2026, and is forecast to reach USD 18.19 billion by 2031 at a 19.43% CAGR.

Which region leads global revenue and which one is growing the fastest?

North America led with 38.74% share in 2025, while Asia-Pacific is projected to record the fastest growth at a 20.58% CAGR through 2031.

Which component generates the most revenue?

Solutions led the market with a 64.52% share in 2025 because buyers continue to spend most on core platforms, adaptive tools, skills intelligence, and analytics layers.

Why are enterprises adopting AI-based learning platforms faster now?

Faster skill obsolescence, wider use of generative AI in daily work, and the need for continuous verified reskilling are making always-on training systems more necessary than periodic course refreshes.

Which end-user vertical is expanding the fastest?

Healthcare and life sciences is projected to grow at a 23.51% CAGR through 2031 as employers prepare staff for AI use under stronger regulatory and operational expectations.

What technology trend is changing how training is delivered?

Speech and voice recognition is projected to grow at a 24.71% CAGR through 2031, pointing to learning experiences that are increasingly triggered by workflow context and conversational interfaces.

Page last updated on: