Corporate Training In Retail Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

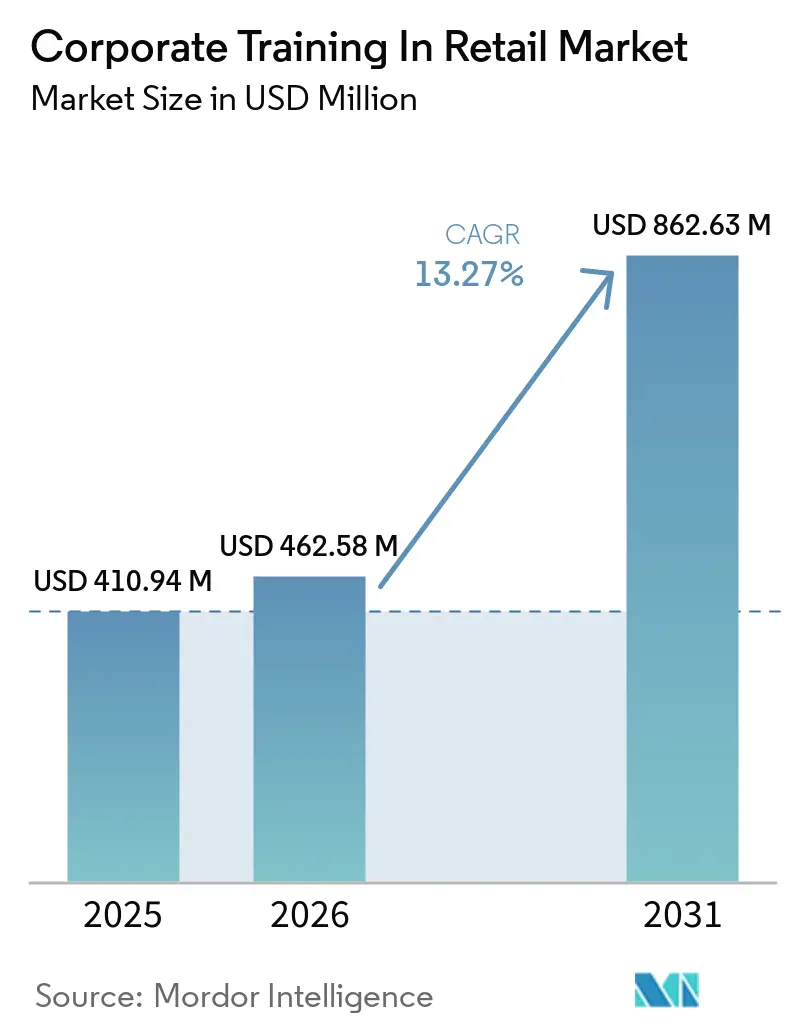

| Market Size (2026) | USD 462.58 Million |

| Market Size (2031) | USD 862.63 Million |

| Growth Rate (2026 - 2031) | 13.27% CAGR |

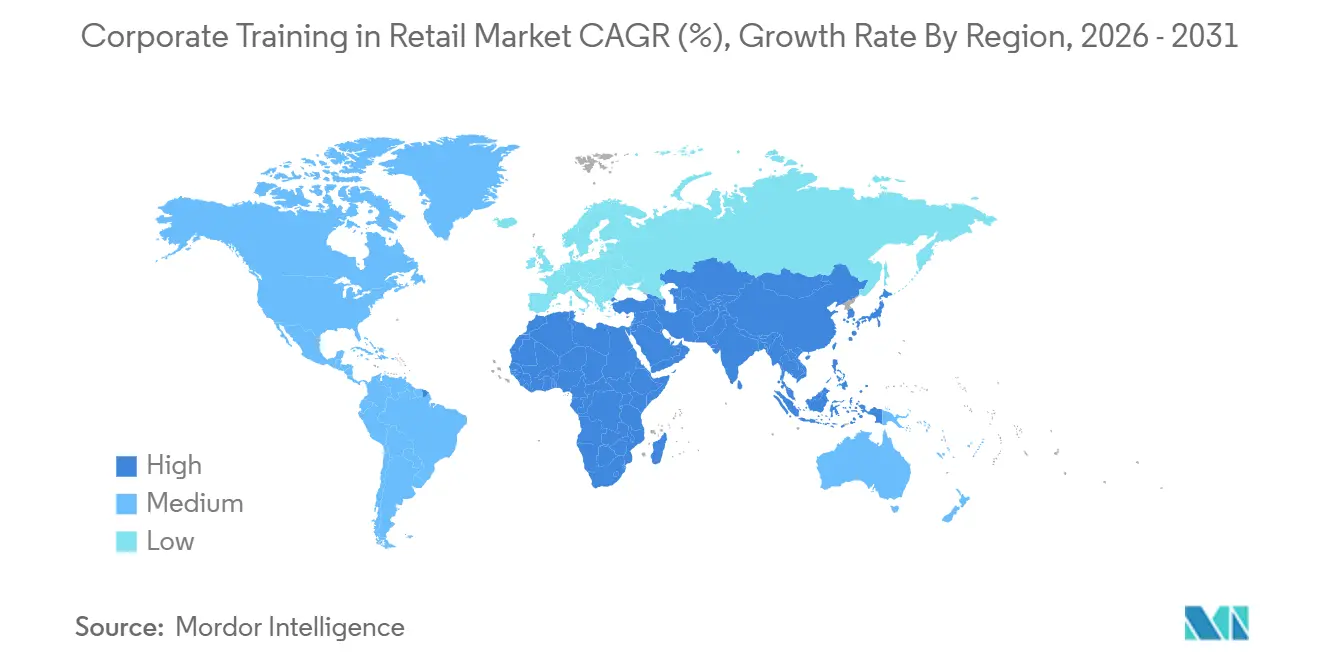

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

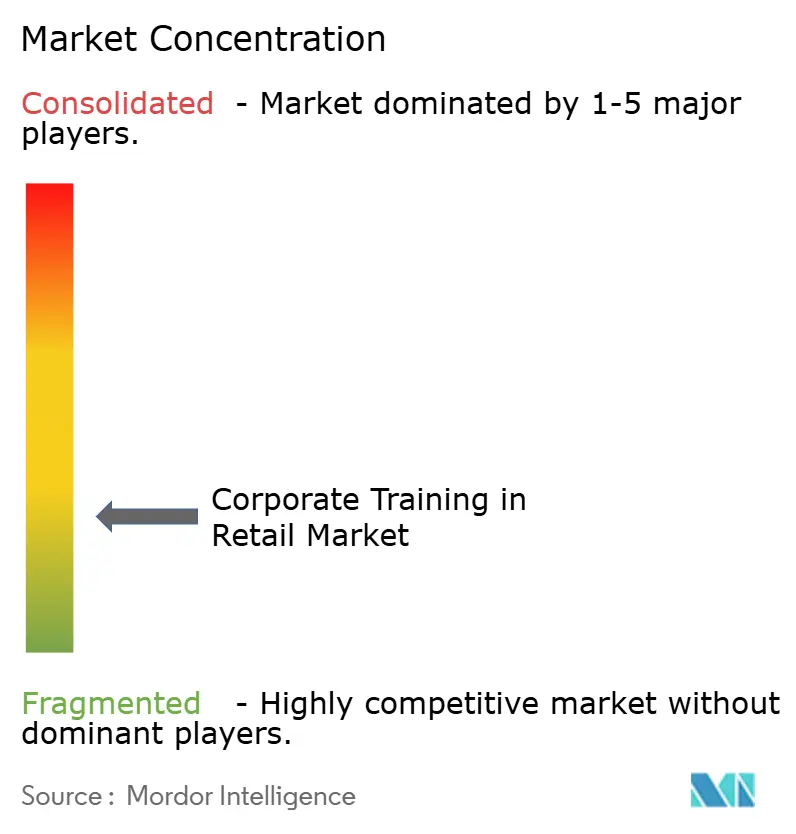

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Corporate Training In Retail Market Analysis by Mordor Intelligence

The corporate training market in the retail sector is projected to be USD 410.94 million in 2025, USD 462.58 million in 2026, and reach USD 862.63 million by 2031, growing at a CAGR of 13.27% from 2026 to 2031. Growth is being shaped by rising demand for structured workforce development as retailers manage persistent frontline attrition and repeated hiring cycles across grocery, apparel, and specialty formats. Spending is also moving away from compliance-only training toward learning systems linked to store performance, customer engagement, and operating discipline. This shift is widening executive support because training is being evaluated less as overhead and more as an operating tool in a tight-margin setting. Retailers are also building stronger learning programs because omnichannel selling requires associates to advise customers across store, pickup, fulfillment, and digital touchpoints. The opportunity remains strongest where providers can connect training activities to clear business outcomes, simplify deployment across large store networks, and support rapid content updates to support changing retail workflows.

Key Report Takeaways

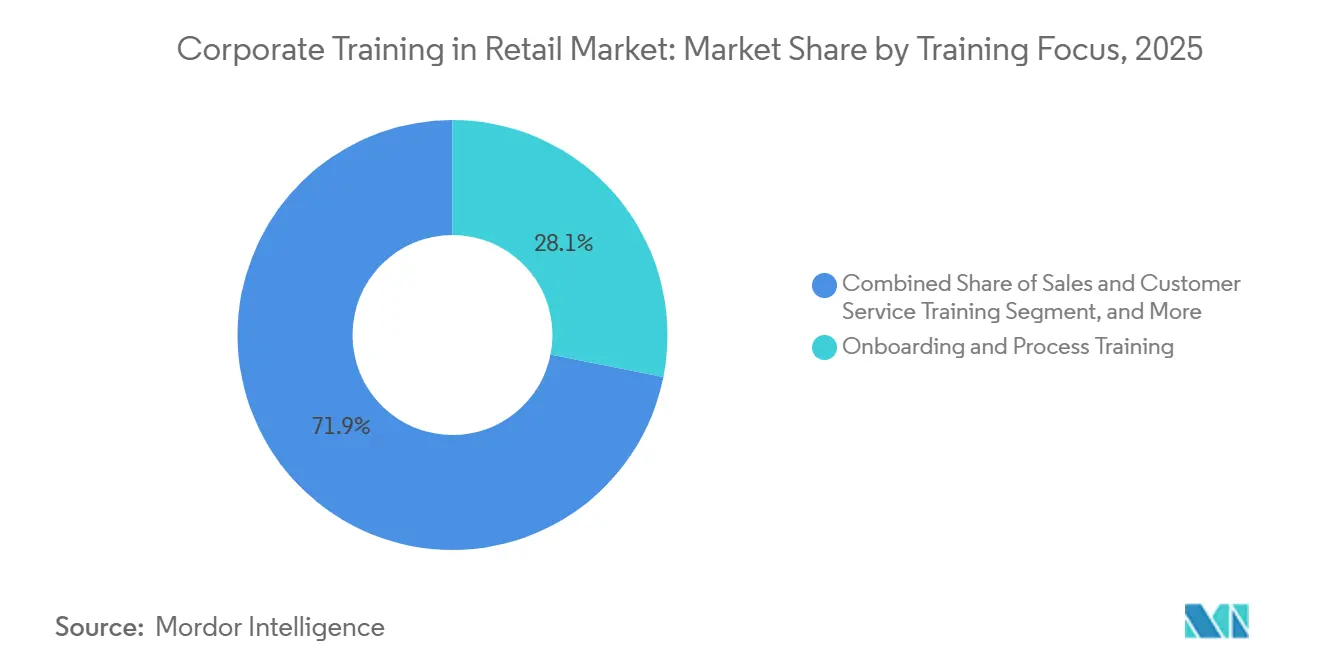

- By training focus, Onboarding and Process Training held 28.12% of the retail corporate training market in 2025, while Sales and Customer Service Training is forecast to expand at a 13.31% CAGR from 2026 to 2031.

- By delivery mode, Online Self-paced Learning accounted for 40.13% of the market in 2025, while Blended Learning is advancing at a 13.42% CAGR through 2031.

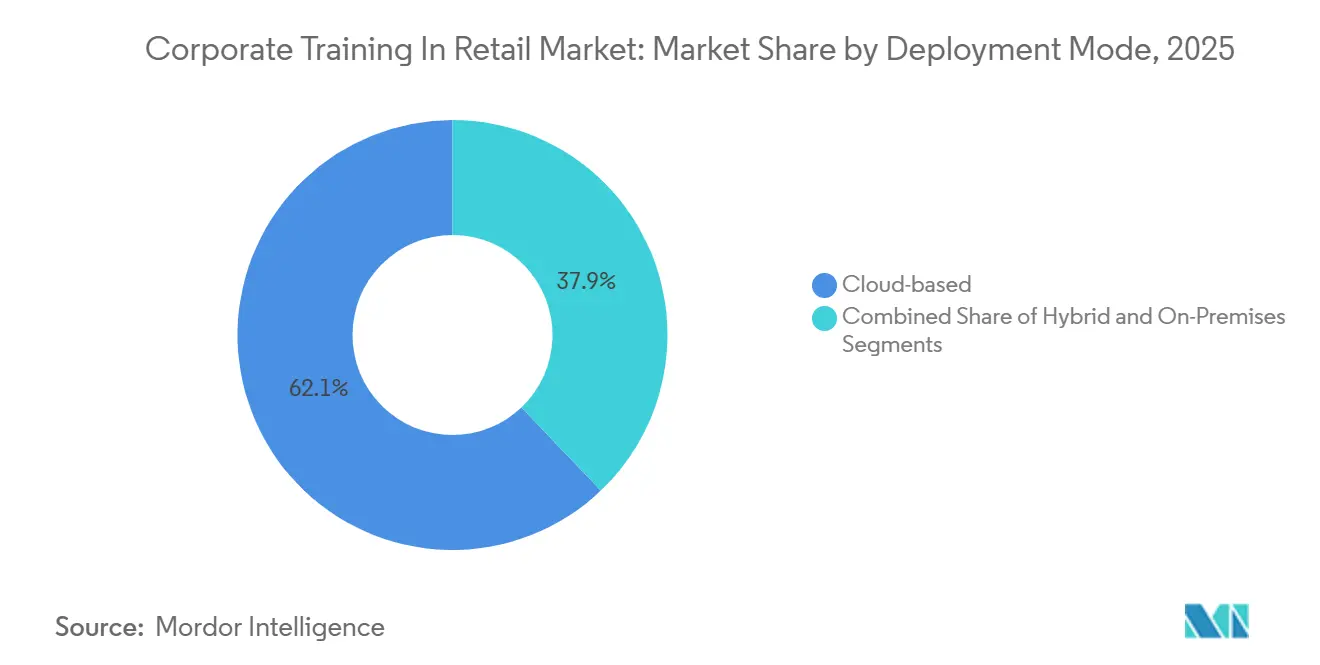

- By deployment mode, Cloud-based deployment captured 62.12% of the market in 2025, and the corporate training market size for cloud-based deployment in the retail market is projected to expand at a 14.67% CAGR from 2026 to 2031.

- By enterprise size, Large Enterprises represented 58.32% of spending in 2025, while SMEs are expected to record the highest CAGR at 14.83% through 2031.

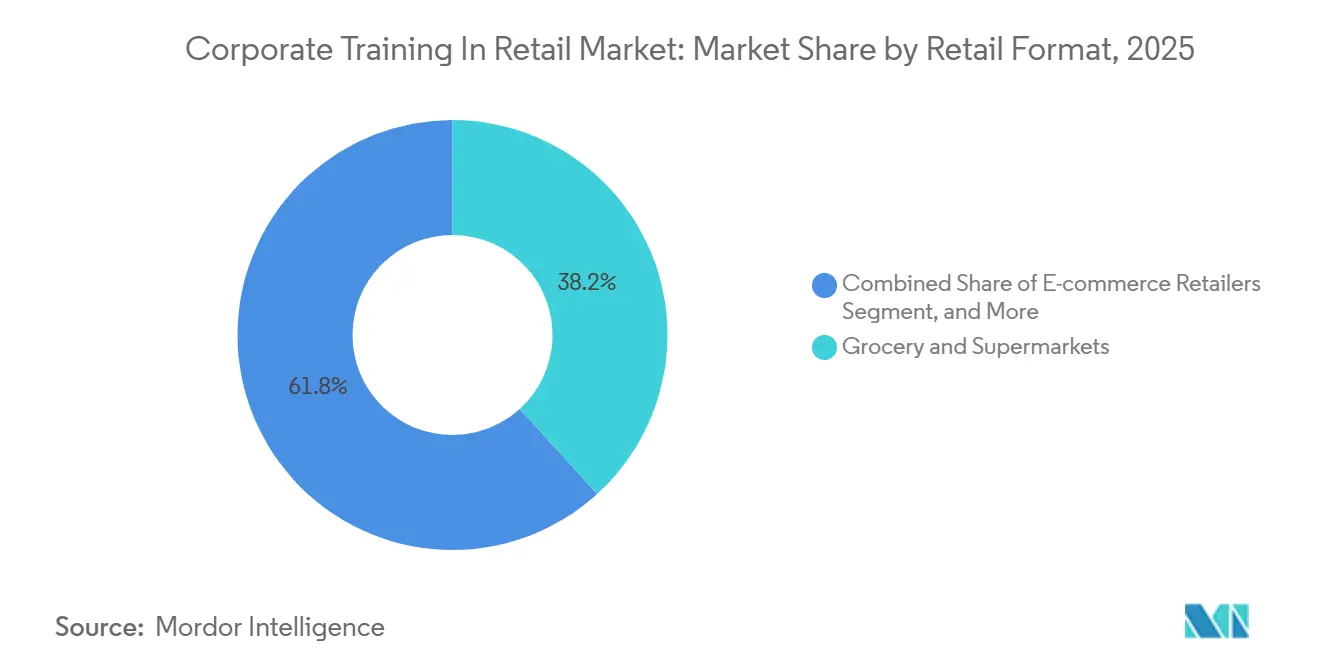

- By retail format, Grocery and Supermarkets held 38.24% of the market in 2025, while E-commerce Retailers are forecast to grow at a 15.29% CAGR through 2031.

- By geography, North America held 36.12% of the retail corporate training market share in 2025, while Asia-Pacific is projected to grow at a 16.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Corporate Training In Retail Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Frontline Turnover and Seasonal Hiring Intensity | +3.2% | Global, with acute pressure in North America and Asia-Pacific | Short term (= 2 years) |

| Omnichannel Retail Expansion Requires Standardized Cross-Channel Training | +2.8% | Global, anchored in North America, Europe, and Asia-Pacific core | Medium term (2-4 years) |

| Rising Compliance Burdens Across Safety, Privacy, and Responsible Selling | +2.1% | North America and EU, with spill-over to APAC and Middle East | Medium term (2-4 years) |

| Mobile-First Microlearning Adoption for Deskless Retail Workforces | +1.9% | Global, highest adoption in emerging APAC and Africa markets | Short term (= 2 years) |

| AI-Enabled Content Localization for Multi-Brand and Multi-Country Store Networks | +1.5% | Global, with early adoption in North America and Western Europe | Medium term (2-4 years) |

| Retail Media and Assisted Selling Models Increase Advisory-Sales Training Demand | +1.3% | North America and Europe, with spill-over to Asia-Pacific | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

High Frontline Turnover and Seasonal Hiring Intensity

In corporate training for the retail market, persistent attrition remains the strongest near-term demand trigger, as retailers must keep reopening onboarding pipelines across formats and seasons. Annual frontline turnover across retail averaged 60% in 2025, and full-time and part-time sales associate turnover in convenience stores exceeded 100%, indicating how often store networks need fresh training cycles.[1]National Association of Convenience Stores, “State of the Industry Talent Insights Dashboard,” NACS, convenience.org This churn raises the value of onboarding systems that can be rolled out quickly and repeatedly without putting pressure on store managers to rebuild instruction from scratch. Seasonal hiring makes the issue more urgent because temporary workers must become productive in short windows while stores still maintain floor coverage and service quality. The corporate training in the retail market is therefore seeing stronger demand for role-based learning that can be delivered quickly, refreshed often, and reused across high-volume hiring waves. Providers that support rapid deployment, short lesson formats, and consistent rollout across many locations are better placed to capture spending tied to turnover pressure.

Omnichannel Retail Expansion Requires Standardized Cross-Channel Training

In corporate training for the retail market, omnichannel expansion is increasing demand for standardized training because store associates now move across advisory selling, pickup support, fulfillment, and digital service tasks. A January 2026 survey found that only 15% of retail leaders believed they were using their omnichannel systems to their full potential, indicating a significant execution gap that training vendors can address.[2]AI Innovation and Omnichannel Are Critical to Retail Success in 2026,” Kyndryl, kyndryl.com That gap is not only technical; frontline staff now need to handle product guidance, order processing, and customer service across connected retail journeys. The Skills4Retail program across 9 European member states is reinforcing digital and sustainability upskilling in retail and wholesale, thereby raising workforce standards across cross-country operating environments. The corporate training in the retail market benefits from this shift because retailers prefer unified learning architectures that can push the same lesson logic across stores, support teams, and digital operations. As retailers seek consistency across touchpoints, training providers with centralized content management and strong role mapping are gaining relevance.

Rising Compliance Burdens Across Safety, Privacy, and Responsible Selling

In corporate training in the retail market, compliance needs are broadening because retailers now face overlapping requirements across worker safety, privacy, responsible selling, and sustainability-related claims. These demands are turning training from a periodic event into an ongoing operating requirement that must be documented and refreshed across locations and roles. Publicly backed retail upskilling frameworks in Europe are adding structure to this shift by linking competence development to formal workforce-readiness expectations.[3]Skills4Retail: Transforming Europe’s Retail Through Education,” Skills4Retail, skills4retail.eu The corporate training in the retail market is moving toward cloud-based delivery, automated re-enrollment, and audit-ready completion tracking, because these features are easier to manage than classroom-heavy compliance programs. Responsible selling also widens the curriculum burden for retailers that operate across categories with age checks, brand claims, or sensitive customer information. As a result, vendors that combine compliance tracking with role-based content are in a stronger position than providers focused only on generic content libraries.

Mobile-First Microlearning Adoption for Deskless Retail Workforces

In corporate training for the retail market, mobile-first microlearning is expanding because most retail workers spend their shifts on the floor, at the point of sale, or in stock movement rather than at desks. Conventional learning systems designed for seated employees have struggled in this setting, with reported completion rates below 5% in traditional retail LMS environments, compared with 95% or higher in mobile-first microlearning formats. This difference matters because short lessons can fit into shift starts, break windows, and manager huddles without disrupting staffing plans. The corporate training in the retail market is also seeing better alignment between microlearning and frontline realities because quick sessions are easier to repeat when products, promotions, or process rules change. That makes mobile delivery useful not only for onboarding but also for reinforcement, product updates, and daily execution routines. Providers that can deliver content in 3-5 minute units, support phone-based access, and keep interfaces simple are well aligned with how retail work is actually organized.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget Pressure and Hard-to-Prove Store-Level Training ROI | -2.1% | Global, most acute among SMEs in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Integration Complexity Across POS, HRIS, Scheduling, and Communication Systems | -1.6% | Global, intensified in multi-country enterprise retail networks | Medium term (2-4 years) |

| Thin Store Staffing Limits Protected Learning Time | -1.2% | Global, most severe in convenience, grocery, and fast-fashion formats | Short term (= 2 years) |

| Franchise and Concession Governance Weakens Training Standardization | -0.8% | Global, particularly in North America, South America, and Middle East franchise systems | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

Budget Pressure and Hard-to-Prove Store-Level Training ROI

In corporate training in the retail market, budget pressure remains a real brake because many operators still struggle to connect learning activities with specific store results within a short financial cycle. Retail procurement teams often want proof within one quarter, while behavior change, knowledge retention, and sales effects usually take longer to appear. This issue is more severe for SMEs because smaller chains rarely have the analytics setup needed to separate the impact of training from pricing moves, footfall changes, or promotional effects. Schoox launched its Learning Impact Suite to address this problem by linking skills, business goals, and KPI tracking more directly, which shows how strongly vendors see outcome measurement as a buying obstacle. Corporate training in the retail market will continue to face uneven spending, where learning benefits are hard to quantify at the store level, especially among smaller and mid-market operators. Providers that can show cleaner ROI pathways are more likely to defend budgets when retail margins tighten.

Integration Complexity Across POS, HRIS, Scheduling, and Communication Systems

In corporate training for the retail market, integration complexity slows adoption because training rarely exists in isolation within retail technology environments. Retailers need completion data to move into scheduling systems, role data to flow from HR systems, and content triggers to connect with communication tools and daily operating systems. Reports show that 33% of retail leaders saw mission-critical infrastructure reaching end-of-service as a limit on digital innovation, and that problem extends directly to LMS integration timelines and cost. This makes deployment harder in large multi-banner networks where owned stores, franchise units, and concession formats run on different technology stacks. The corporate training in the retail market, therefore, faces slower conversions when legacy systems lack clean API layers or when governance rules differ across vendors and countries. Vendors that offer open architecture, prebuilt connectors, and simpler data mapping can reduce this friction and win enterprise contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Training Focus: Onboarding Anchors Spending as Advisory Selling Gains Ground

In corporate training in the retail market, Onboarding and Process Training accounted for 28.12% in 2025, making it the largest training focus, as retailers had to repeatedly train new hires across frontline roles. This segment remained central even when budgets tightened because basic process readiness, task discipline, and policy understanding could not be delayed without affecting store operations. Product Knowledge Training stayed important as product catalogs expanded and update cycles shortened across many retail categories. Compliance and Safety Training also played a meaningful role, as retailers needed recurring training on worker safety, privacy, and responsible selling practices. The corporate training in the retail market, therefore, continued to direct a large portion of spend toward programs that quickly and consistently bring new hires to operational readiness.

The corporate training in the retail market also showed a clear shift toward revenue-oriented learning, with Sales and Customer Service Training growing at a 13.31% CAGR from 2026 to 2031. This pattern reflects the growing value of associates who can advise rather than only process transactions in store, pickup, and assisted selling environments. Reports indicated that associates trained as trusted advisors outperformed their transactional counterparts by 25% on units-per-transaction metrics in enterprise retail settings, further supporting the stronger business case for this sub-segment. Leadership and Store Operations Training remained relevant for retailers building management depth, but spending in that area was less recurring than frontline-focused instruction. Across the corporate training in the retail industry, the strongest momentum now lies in training that improves both employee readiness and customer-facing performance without separating the two.[4]AI Sales Training for Enterprise Retail Teams,” Retorio, retorio.com

By Delivery Mode: Self-Paced Scale Meets Blended Depth

segment in 2025, which reflected its fit with uneven shift patterns and variable store schedules. Associates could access modules during breaks, at shift starts, or between customer tasks, giving self-paced learning a clear advantage over fixed-session formats. Virtual Instructor-led Training and Classroom Instructor-led Training remained useful for manager training and group-based instruction that benefited from live discussion. Even so, their relative weight was lower because frontline teams needed formats that worked without pulling many employees off the floor simultaneously. The corporate training market in the retail sector for self-paced delivery remained strong because accessibility, repeatability, and lower scheduling friction mattered more than formal session structure in most store environments.

Corporate training in the retail market is also moving toward richer combinations of formats, with Blended Learning projected to grow at a 13.42% CAGR through 2031. Retailers are finding that digital reinforcement and coached practice work better together when the goal is behavior change on the sales floor. AI-powered adaptive learning and AR or VR training kept premium positions because they can shorten time to competence, improve product understanding, and make task practice more realistic. Mobile learning and microlearning also remained especially relevant in markets where smartphone access was stronger than desktop access across store networks. In corporate training in the retail industry, delivery is no longer defined by a single channel, as buyers increasingly want scalable digital access supported by coaching and real-world reinforcement.

By Deployment Mode: Cloud-Based Architectures Define the Competitive Standard

In corporate training in the retail market, Cloud-based deployment captured 62.12% in 2025 and was the fastest-growing deployment mode, with a 14.67% CAGR from 2026 to 2031. This leading position reflected the needs of multi-site operators seeking centralized content control, faster updates, and real-time visibility across store networks. The corporate training in the retail market for cloud-based deployment is expanding because retailers cannot maintain version consistency efficiently across hundreds of locations with heavy on-premises systems. Cloud platforms also make it easier to track participation, update lessons, and support role-specific delivery without high local IT effort. The corporate training in the retail market has therefore made SaaS architecture the practical standard for broad retail rollout rather than an optional feature.

On-premises deployment persisted in data-sensitive markets and among operators that needed tighter control over where information was stored. Hybrid models also remained relevant because they allowed retailers to balance centralized learning management with localized data-handling requirements. Corporate training in the retail market is likely to remain hybrid, with scale, compliance, and regional infrastructure needs all requiring simultaneous management. Platform updates in 2026 introduced capabilities such as Learning Everywhere You Work and deeper AI-linked functionality, which reflected how cloud vendors are expanding beyond simple hosting into embedded workflow support. As deployment decisions become more tied to integration, analytics, and AI compatibility, cloud-native vendors are strengthening their position against traditional, isolated LMS installations.

By Enterprise Size: Large Enterprise Dominance Faces an SME Counter-Wave

In the corporate training in the retail market, Large Enterprises accounted for 58.32% of spending in 2025 because they had the budgets, internal teams, and scale needed to build structured learning programs across wide store portfolios. These operators were more likely to run proprietary academies, buy enterprise-grade systems, and commission custom content suited to their brands and workflows. Their buying behavior also favored platforms that could standardize training across regions, banners, and business units while maintaining strong reporting discipline. The corporate training in the retail market remained anchored by these larger buyers because their workforce volume made even modest improvements in readiness or retention financially meaningful. Large operators also had more room to centralize fragmented learning initiatives into unified systems that served onboarding, leadership, and operational needs together.

Corporate training in the retail market is nevertheless seeing faster change on the SME side, with SMEs projected to grow at a 14.83% CAGR through 2031. SaaS pricing, subscription access, and AI-assisted content creation are reducing the internal design burden that previously limited structured training for smaller chains. This shift is making formal training more accessible to operators who previously relied on ad hoc manager coaching or static documents. Launches in 2026 highlighted how large retailers are centralizing development and career pathways, but they also underscored the broader direction of the category toward more organized, platform-led learning systems. In corporate training in the retail industry, the combination of enterprise-scale at the top and lower entry barriers for smaller chains is widening the addressable customer base.

By Retail Format: Grocery Leads, but E-commerce Retailers Accelerate Fastest

In corporate training in the retail market, Grocery and Supermarkets accounted for 38.24% of spending by retail format in 2025 because the format combines large workforces, broad assortments, food-handling rules, and steady refresh needs. High employee counts make training scale especially valuable in grocery stores, while food safety and process discipline keep recurring instruction essential. Department Stores and Specialty Retail also maintained consistent demand because associates often needed product and service guidance beyond simple onboarding. Fashion, Apparel, and Electronics Retail faced added pressure from fast product turnover, campaign changes, and short training windows for new ranges. The corporate training in the retail market share stayed high in grocery because the format’s operational complexity created repeated reasons to train at scale rather than rely on one-time instruction.

The corporate training in the retail market is also being reshaped by the rapid rise of E-commerce Retailers, which are expected to grow at a 15.29% CAGR through 2031. These businesses need distinct training for fulfillment associates, live-commerce teams, customer experience staff, and newer digital support roles that traditional store curricula did not address. That creates demand for training designs that blend process precision with service quality and cross-functional coordination. South American retail ecosystems are also becoming more active in structured skills development, with regional platforms launched in 2025 reflecting stronger attention to professional retail capability building. Across the corporate training in the retail industry, format-specific needs are becoming more visible, pushing providers to tailor content by operating model rather than treating retail as a single, uniform category.

Geography Analysis

In the corporate training market for the retail industry, North America accounted for 36.12% of revenue in 2025, making it the largest regional contributor. The region benefited from established eLearning adoption, a high concentration of large-format retailers, and strong demand for repeatable frontline training across multi-site networks. Corporate training in the retail market also remained well supported in the United States because large retailers treat workforce development as part of operating execution rather than a narrow HR function. Industry-backed training initiatives continued to widen the talent pipeline, including programs launched in February 2026 to support 3,000 participants across 30 partner organizations. Canada and Mexico added to regional growth through tighter labor conditions, rising organized retail activity, and broader demand for structured onboarding and compliance-related instruction.

In the corporate training market for the retail industry, Asia-Pacific is the fastest-growing region, with a 16.41% CAGR from 2026 to 2031. Growth is being supported by organized retail expansion, rising adoption of smartphone-led learning, and a wide need for frontline capability building across modern trade formats. The region also shows strong potential, as training demand is no longer limited to stores and now extends to fulfillment, customer support, and digitally assisted selling roles. Markets such as India, China, Southeast Asia, and Australia are drawing provider attention because they combine retail scale, workforce growth, and uneven training maturity across formats. The corporate training in the retail market, therefore, has strong headroom in Asia-Pacific, where rapid retail expansion still outpaces the formal training systems available to many frontline teams.

In the corporate training in the retail market, Europe held a significant share in 2025, with Germany, the United Kingdom, and France as the largest markets in the region. Initiatives are strengthening digital, green, and resilience skill development through multi-partner structures across member states, which supports broader corporate training adoption in retail and wholesale. Structured leadership development access also expanded in 2025 through partnerships with learning providers, showing how industry associations are shaping formal learning pathways for retail professionals. South America remained smaller but active, with more visible professional development activity around organized retail capability building. The Middle East and Africa led earlier in adoption, but demand foundations are strengthening, with modern retail expansion and workforce formalization gaining pace.

Competitive Landscape

In corporate training for the retail market, competition is moderate to high because no single provider dominates across retail formats, geographies, or training needs. The field is shaped by three broad groups: retail-specialist platforms built for frontline workforces, general enterprise LMS vendors with retail overlays, and custom content firms that design brand-specific programs. This mix keeps the market fragmented, while also making differentiation more dependent on use-case fit than on scale alone. AI capability depth, integration breadth, and the ability to show measurable operational value are becoming the main points of contrast between vendors. The market is therefore moving away from simple content library competition and toward platform models that can support workflow delivery, analytics, and faster content production.

Docebo has been one of the clearest examples of platform expansion through AI and capability layering. The company’s 2026 announcements around AgentHub, Skills Intelligence, Enterprise Knowledge, and MCP-linked functionality showed a strategy focused on embedding learning more deeply into enterprise work environments. Docebo also stated that the 365Talents acquisition was expected to contribute nearly USD 9 million to 2026 revenue, signaling that skills intelligence is becoming commercially important in vendor roadmaps. YOOBIC followed a similar path in April 2026 by launching V15 with an AI-powered Store Manager Copilot, an AI Search Assistant, AI-driven learning creation tools, and automated performance reporting, reinforcing the push toward manager-facing execution support rather than stand-alone training delivery. The market is rewarding vendors that can connect learning, communication, and execution into one operating layer for store teams.

Specialist providers are also defending their position by focusing more sharply on their vertical rather than matching every enterprise platform feature. Schoox strengthened that message through its Learning Impact Suite and then added market visibility by winning the 2026 Lighthouse Tech Awards for practical AI and frontline-focused solutions. That matters because mid-market and franchise-heavy retailers often need stronger frontline alignment and simpler KPI mapping instead of large, generalized platform stacks. The corporate training in the retail market still contains white-space opportunities in franchise governance, multilingual localization, and pricing models tied to outcome delivery. As those gaps remain open, smaller retail-focused vendors can continue gaining ground even as larger platforms expand their AI and integration scope.

Corporate Training In Retail Industry Leaders

Axonify Inc.

Docebo S.p.A.

YOOBIC Inc.

Epignosis LLC

360LEARNING SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Kroger launched Pearl Street Academy, a centralized training and career development platform for associates.

- April 2026: YOOBIC released V15 with AI-powered Store Manager Copilot, AI Search, learning creation tools, and automated dashboards.

- April 2026: Docebo unveiled AgentHub, Skills Intelligence, and Enterprise Knowledge; reported Q1 revenue of USD 65.4 Million (+14.3% YoY) and raised 2026 guidance.

- February 2026: NRF Foundation and PepsiCo Foundation launched a USD 1 Million retail training initiative for 3,000 participants.

Global Corporate Training In Retail Market Report Scope

The Corporate Training in Retail Market refers to technology-enabled platforms, services, and methodologies designed to deliver, manage, and track workforce learning programs across retail enterprises. These solutions cover areas such as onboarding, product knowledge, sales and customer service, compliance, safety, and leadership training, and are deployed via cloud, on-premises, or hybrid models. Delivered through self-paced, instructor-led, blended, mobile, AI-powered, and immersive AR/VR formats, corporate retail training helps large and small enterprises enhance employee skills, improve customer engagement, ensure compliance, and optimize store operations across diverse retail formats worldwide.

The Corporate Training in Retail Market Report is segmented by Training Focus (Onboarding and Process Training, Product Knowledge Training, Sales and Customer Service Training, Compliance and Safety Training, and Leadership and Store Operations Training), Delivery Mode (Online Self-paced Learning, Virtual Instructor-led Training (VILT), Classroom Instructor-led Training, Blended Learning, Mobile Learning and Microlearning, AI-powered Adaptive Learning, and AR/VR Immersive Training), Deployment Mode (Cloud-based, On-premises, and Hybrid), Enterprise Size (Large Enterprises and Small and Medium-sized Enterprises), Retail Format (Grocery and Supermarkets, Fashion and Apparel, Electronics Retail, Department Stores, Specialty Retail, Convenience Stores, and E-commerce Retailers), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Onboarding and Process Training |

| Product Knowledge Training |

| Sales and Customer Service Training |

| Compliance and Safety Training |

| Leadership and Store Operations Training |

| Online Self-paced Learning |

| Virtual Instructor-led Training (VILT) |

| Classroom Instructor-led Training |

| Blended Learning |

| Mobile Learning and Microlearning |

| AI-powered Adaptive Learning |

| AR/VR Immersive Training |

| Cloud-based |

| On-premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Grocery and Supermarkets |

| Fashion and Apparel |

| Electronics Retail |

| Department Stores |

| Specialty Retail |

| Convenience Stores |

| E-commerce Retailers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Training Focus | Onboarding and Process Training | |

| Product Knowledge Training | ||

| Sales and Customer Service Training | ||

| Compliance and Safety Training | ||

| Leadership and Store Operations Training | ||

| By Delivery Mode | Online Self-paced Learning | |

| Virtual Instructor-led Training (VILT) | ||

| Classroom Instructor-led Training | ||

| Blended Learning | ||

| Mobile Learning and Microlearning | ||

| AI-powered Adaptive Learning | ||

| AR/VR Immersive Training | ||

| By Deployment Mode | Cloud-based | |

| On-premises | ||

| Hybrid | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium-sized Enterprises | ||

| By Retail Format | Grocery and Supermarkets | |

| Fashion and Apparel | ||

| Electronics Retail | ||

| Department Stores | ||

| Specialty Retail | ||

| Convenience Stores | ||

| E-commerce Retailers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the size of the corporate training in retail market?

The corporate training in retail market stands at USD 462.58 million in 2026 and is expected to reach USD 862.63 million by 2031 at a 13.27% CAGR.

Which training focus leads spending in retail workforce learning?

Onboarding and Process Training led the category with a 28.12% share in 2025 because retailers continue to face high frontline attrition and frequent hiring cycles.

Which delivery model is growing fastest among retail training buyers?

Blended Learning is the fastest-growing delivery mode, with a 13.42% CAGR from 2026 to 2031, as retailers pair digital reinforcement with coached practice.

Why are cloud-based learning platforms gaining ground with retailers?

Cloud-based deployment held 62.12% in 2025 and is also the fastest-growing deployment mode at a 14.67% CAGR because retailers want centralized updates, analytics, and easier rollout across many locations.

Which region is expanding fastest in this space?

Asia-Pacific is the fastest-growing region, with a 16.41% CAGR from 2026 to 2031, supported by organized retail expansion and rising mobile-first learning adoption.

Why are SMEs becoming more important buyers?

SMEs are projected to grow at a 14.83% CAGR through 2031 because SaaS pricing and AI-assisted content creation are lowering the cost and complexity of launching formal training programs.

Page last updated on: