Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

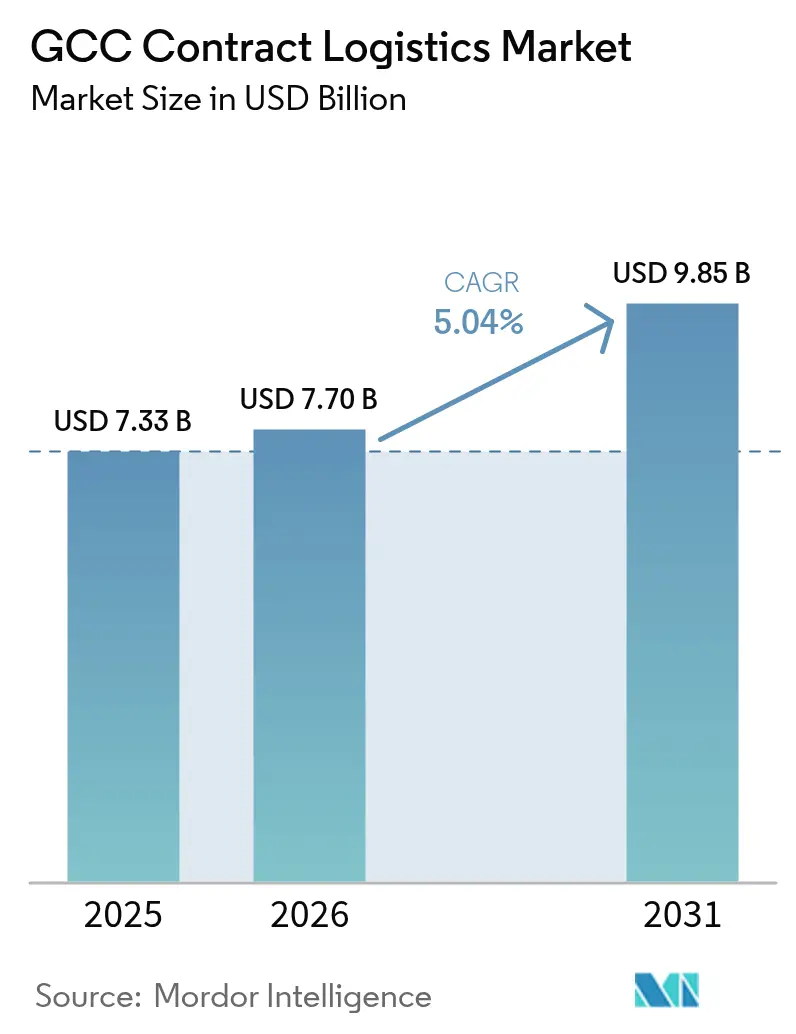

| Base Year Market Size (2025) | USD 7.33 Billion |

| Market Size (2026) | USD 7.7 Billion |

| Market Size (2031) | USD 9.85 Billion |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

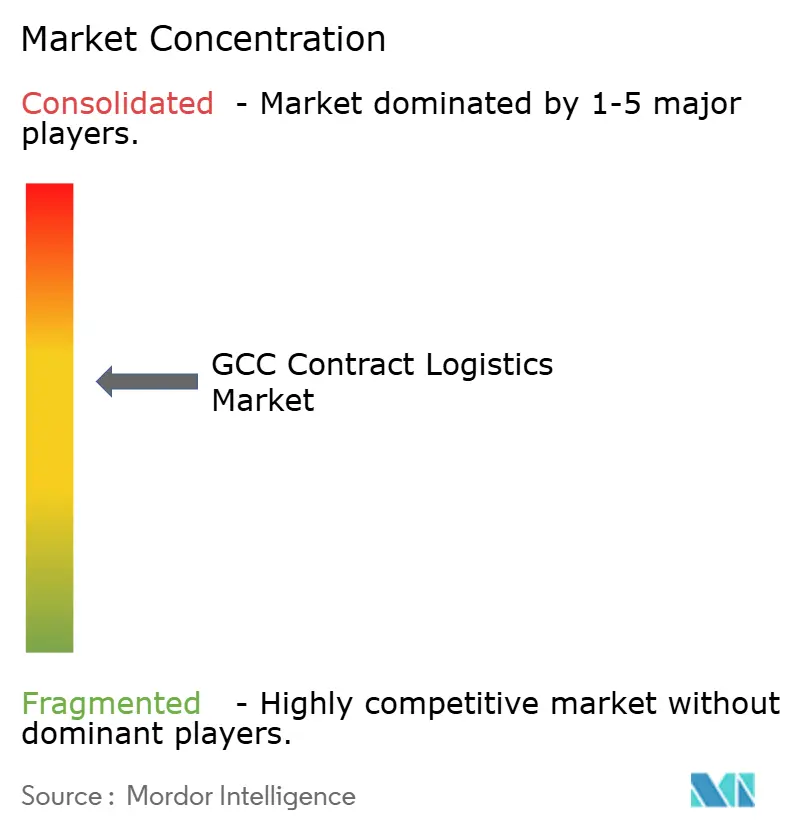

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Contract Logistics Market Analysis by Mordor Intelligence

The GCC Contract Logistics Market size is expected to grow from USD 7.33 billion in 2025 to USD 7.7 billion in 2026 and is forecast to reach USD 9.85 billion by 2031 at 5.04% CAGR over 2026-2031. Regional governments are channeling record infrastructure spending into free trade zones, multimodal corridors, and digital trade platforms, positioning contract logistics as a cornerstone of diversified economic growth. Accelerating e-commerce, large-scale industrial projects under Saudi Vision 2030, and rising healthcare shipment volumes are amplifying demand for sophisticated fulfillment, cold-chain, and value-added services. Competitive intensity is increasing as global integrated logistics players add robotics and data-driven solutions while regional specialists leverage local knowledge to secure long-term partnerships. Despite strong momentum, cabotage rules and a chronic shortage of Grade-A warehouses continue to inflate operating costs and curb network optimization.

Key Report Takeaways

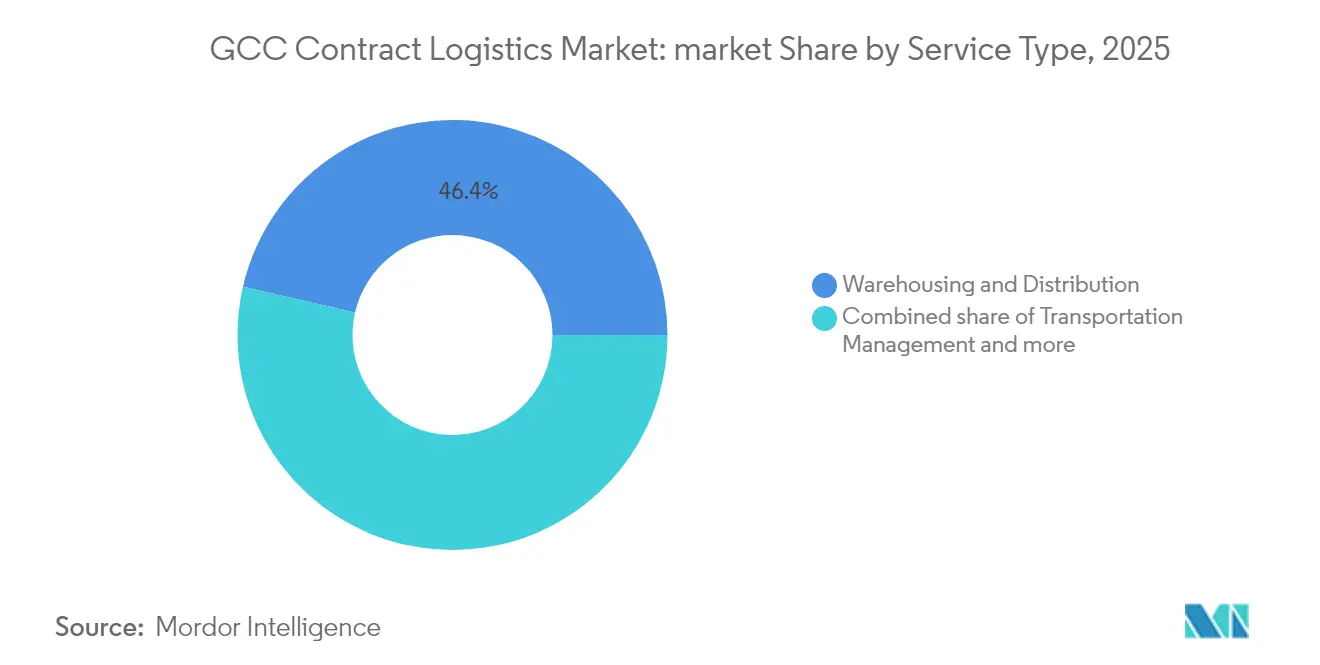

- By service, Warehousing and Distribution led with 46.40% of the GCC Contract Logistics market share in 2025. The GCC Contract Logistics market for Value-Added Services is forecast to grow at a 7.35% CAGR between 2026-2031.

- By end-user industry, Consumer Goods and Retail held 31.50% of the GCC Contract Logistics market size in 2025. The GCC Contract Logistics market for Healthcare and Pharmaceuticals is expanding at a 8.65% CAGR between 2026-2031.

- By contract duration, Long-term agreements (≥ 1 year) accounted for 67.30% of the GCC Contract Logistics market share in 2025. The GCC Contract Logistics market for Short-term contracts is projected to grow at a 6.55% CAGR between 2026-2031.

- By geography, Saudi Arabia commanded 52.60% of the GCC Contract Logistics market size in 2025. The GCC Contract Logistics market for the UAE is set for the fastest CAGR of 5.95% between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Contract Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid e-commerce fulfillment growth | +1.2% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Vision 2030 industrial diversification logistics needs | +1.5% | Saudi Arabia, spillover GCC | Long term (≥ 4 years) |

| Free trade zones expanding warehousing demand | +0.8% | UAE, Saudi Arabia, Oman | Medium term (2-4 years) |

| Government cold-chain investment | +0.6% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Gulf Railway multimodal connectivity | +0.7% | All GCC countries | Long term (≥ 4 years) |

| In-Country Value mandates favoring local 3PLs | +0.5% | Saudi Arabia, UAE, Oman | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid e-commerce fulfillment growth in KSA and UAE

Online orders in the MENA region climbed 30% in 2024, with the UAE’s average order value moving from USD 30 to USD 35.6. Around 42% of e-commerce firms still list last-mile efficiency as the chief obstacle. Contract logistics providers are building regional fulfillment centers, adding parcel sortation automation, and integrating cross-border routing tools to cut delivery windows while controlling cost.

Vision 2030 industrial diversification projects require integrated logistics

Saudi Arabia approved USD 50 billion of projects under Vision 2030 in 2024 and earmarked funding for 59 national logistics centers. NIDLP allocates a further USD 36 billion for logistics infrastructure, plus USD 28 billion for industrial zones. These capital programs demand turnkey contract logistics capable of synchronized inbound, storage, and outbound flows. Operators embedded at project sites report rising localization targets, with 68% of companies prioritizing supply-chain localization for resilience.

Expansion of free trade zones enhances warehousing demand

Jafza’s Phase 2 logistics park brings an extra 360,000 sq ft of space via an AED 90 million (USD 24.51 million) investment to help lift UAE logistics revenue to AED 200 billion (USD 54.46 billion) by 2032. Umm Al Quwain FTZ adds 350,000 sq ft of warehouses and 65,000 sq ft of commercial area, boosting inventory positioning flexibility. Multinational firms cite these hubs’ simplified customs and value-added zones as decisive factors in regional network design.

Government-led cold-chain investment boosting temperature-controlled logistics

Temperature-controlled shipments grew more than 30% in 2023, the highest on record, driven by pharmaceutical and food security priorities. Technology layers such as AI-enabled condition monitoring are improving product integrity.[1]International Air Transport Association Research Division, “Temperature-Controlled Air Freight Trends 2024,” IATA Publications, iata.org Logistics players are deploying dedicated GDP-compliant facilities; Aramex highlights quality assurance and compliance as competitive requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cabotage restrictions | −0.8% | All GCC countries | Medium term (2-4 years) |

| Shortage of Grade-A warehousing | −0.6% | Saudi Arabia, UAE | Short term (≤ 2 years) |

| Fragmented customs procedures | −0.4% | All GCC countries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cabotage restrictions are hindering cross-border network optimization

Regional rules barring foreign tractors from domestic moves raise cross-border costs 18-23% and add 36 hours to multi-border transits[2]Gulf Cooperation Council Secretariat General, “Cabotage Regulations and Harmonization Roadmap,” GCC Transport Committee, gcc-sg.org. Temperature-sensitive cargo suffers most. Providers adopt hub-and-spoke models, yet still face double handling at borders. Regulatory harmonization lags physical links such as the Gulf Railway, muting potential productivity gains.

Shortage of Grade-A warehousing is increasing operating costs

Supply of modern space remains tight, lifting rents and forcing retrofits. In Saudi Arabia, logistics assets under management total 3.5 million sq ft, yet expansion to USD 2 billion of assets is planned by 2025 to narrow the gap. Dubai Logistics City and other pipeline projects will ease constraints, but near-term shortages elevate service costs and erode margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Warehousing holds scale, value-added services accelerate

Warehousing and distribution captured 46.40% of GCC Contract Logistics market share in 2025 on the back of the region’s role as a crossroads between Asia, Europe, and Africa. GCC Ongoing investments include Saudi Arabia’s USD 2.66 billion program to build 18 logistics zones by 2030. Robotics and high-bay automation are raising throughput and labor productivity, enabling faster cycle times that retailers and manufacturers demand. Yet limited Grade-A capacity still inflates costs for temperature-controlled storage, keeping barriers high for new entrants and supporting premium pricing.

Value-added services are projected to expand at 7.35% CAGR through 2031 as 3PLs bundle kitting, light assembly, and customization into comprehensive solutions. High-tech adoption drives this growth: DHL is deploying 1,000 additional Boston Dynamics robots after investing EUR 1 billion (USD 1.16 billion) in automation. Swisslog is promoting AutoStore robots that align with Saudi Vision 2030’s innovation push. As clients pivot from transactional storage to integrated value chains, providers that integrate IT visibility, co-packing, and compliance support gain share.

By End-User Industry: Retail leads, healthcare builds momentum

Consumer goods and retail, including e-commerce, represented 31.50% of the GCC Contract Logistics market in 2025, owing to rising digital adoption and omnichannel retail models. Platforms in Saudi Arabia and the UAE registered the highest GMV in the region, amplifying demand for rapid fulfillment and flexible returns. Retailers pursue distributed inventory and predictive replenishment, driving 3PL collaboration in network design, last-mile optimization, and reverse logistics.

Healthcare and pharmaceuticals is the fastest climber with a 8.65% forecast CAGR. GCC Contract Logistics market size for this vertical is expected to double by 2030 as Saudi Arabia allocates more than USD 65 billion to hospital infrastructure and targets 65% private sector participation. Strict temperature and traceability standards favor providers that invest in GDP-certified facilities, IoT-based monitoring, and regulatory expertise. Partnerships with global pharma firms and vaccine distributors are reinforcing cold-chain specialization across the region.

By Contract Duration: Long-term commitments dominate, flexibility gains favor

Long-term contracts of at least 1 year accounted for 67.30% of the GCC Contract Logistics market in 2025, reflecting the capital-intensive nature of dedicated warehouses, fleet investments, and IT integration. Multi-year deals enable cost predictability and justify automation expenditures for both shippers and 3PLs. Gulf Warehousing Company focuses on such partnerships to underpin expansion plans.

Short-term agreements under 12 months are, however, growing at 6.55% CAGR as volatility, rapid product launches, and technology disruptions compel companies to retain flexibility. GCC Contract Logistics market size for short-term engagements remains smaller yet increasingly important for projects in renewables, events, and humanitarian relief. Firms adopt modular warehousing and pay-as-you-go transport to balance risk, while digital freight platforms help match capacity in real time.

Geography Analysis

Saudi Arabia held 52.60% of the GCC Contract Logistics market in 2025, powered by Vision 2030’s goal of a global logistics hub backed by over SR1 trillion (USD 267 billion) in planned spending. The Kingdom has already invested SR200 billion (USD 53.31 billion) toward infrastructure upgrades, including 59 logistics centers spanning 100 million sq m. Logistics market investments exceeding USD 106.6 billion are improving port capacity, corridor roads, and bonded zones. National e-commerce and industrial strategies continue to elevate contract logistics demand for technology-enabled warehousing and domestic distribution.

The UAE is projected to record a 5.95% CAGR, the fastest within the GCC Contract Logistics market, leveraging world-class sea ports, air hubs, and digital trade initiatives. Jafza’s ongoing expansion and Dubai Logistics City’s integrated freight campus support the country’s ambition to grow logistics revenue to AED 200 billion (USD 54.46 billion) by 2032. Advanced Trade and Logistics Platform rollouts reduce documentation steps and provide single-window visibility, attracting multinationals to set up regional distribution centers.

Qatar, Kuwait, Bahrain, and Oman collectively diversify the GCC Contract Logistics market. Oman’s Port of Duqm expansion, backed by new investment, anchors an Indian Ocean gateway strategy. Kuwait is streamlining customs while Bahrain promotes a five-hour clearance pledge to lure just-in-time inventory flows. The Gulf Railway will eventually bind these markets into a contiguous multimodal corridor, promising cost efficiencies once regulatory harmonization catches up.

Regulatory Landscape

Contract logistics operations across GCC member states operate under the GCC Customs Union framework anchored by the Common Customs Law for GCC States (2002), which supports the Common Customs Tariff and core customs processes. Operational convergence has also been reinforced through the Unified Guide for Customs Procedures at First Points of Entry (2025), which standardizes documentation and clearance steps at the first port of entry and shapes how 3PLs design bonded warehousing, inventory visibility, and cross-border distribution flows.

On the transport side, the Unified Law of International Land Transport between GCC States (approved at the 43rd GCC Supreme Council session in December 2022) provides a region-wide legal base for cross-border road operations, while country regulators set licensing and compliance requirements. In Saudi Arabia, the Transport General Authority (TGA) governs licensing for operators and logistics facilities, including via the Logisti platform, increasing the role of digital compliance in onboarding sites and fleets. In the UAE, Ministerial Decision No. 74 of 2026 introduced a prohibition on unjustified price increases for domestic land transport, port operational services, and related land-based logistics services during emergency circumstances, which adds a cost-stability lever that can influence contract pricing and service-level commitments.

Value Chain Analysis

The GCC contract logistics value chain starts with inbound flows at sea and air gateways, then moves through port or terminal handling and customs clearance into bonded and non-bonded warehousing, multi-user fulfillment, and in-country distribution. The midstream layer is shaped by free zone and industrial cluster warehousing (including cold-chain and GDP-compliant space for healthcare shipments), along with value-added services such as kitting, packaging, labeling, and light assembly that turn storage into shipper-specific workflows. Control towers, WMS/TMS platforms, and compliance systems connect these steps, while last-mile and reverse logistics close the loop for consumer, retail, and after-sales programs.

Recent investments and partnerships show how infrastructure owners and shippers are tightening port-to-inland links and expanding routing options. Gulftainer is accelerating its Khor Fakkan port investment program, expanding capacity from 3.5 million to 5 million TEUs, and Saudi Ports Authority (Mawani) announced a USD 170 million expansion at Jeddah Islamic Port with DP World and Red Sea Gateway Terminal, both of which affect throughput and warehouse siting decisions around key gateways. On the shipper side, Borouge signing logistics partnerships with Gulftainer and Etihad Rail highlights growing rail-enabled export and inland distribution needs tied to large industrial producers, while Maersk and Saudi Post (SPL) partnering around the Maersk Integrated Logistics Park in Jeddah reflects tighter integration between fulfillment, linehaul, and final delivery capabilities for e-commerce-led volumes.

Competitive Landscape

The GCC Contract Logistics industry is moderately concentrated. Global integrators such as DHL Supply Chain, CEVA Logistics, and Kuehne + Nagel compete against regional champions Aramex, Gulf Warehousing Company, and Almajdouie Logistics. Automation investments are redefining the playing field; DHL’s commitment of EUR 1 billion (USD 1.16 billion) and its pact with Boston Dynamics to add 1,000 robots expanding productivity and safety. CEVA deploys cloud-based control towers that feed AI route engines, while Kuehne + Nagel scales pharma-grade sites in Dubai South.

Regional firms counter with localized compliance expertise and integrated land-bridge services. GWC logged QAR 1.582 billion (USD 434.25 million) revenue in 2024 and now scales e-commerce, freight forwarding, and contract logistics across Qatar and neighboring states. Almajdouie invests in bonded trucking networks that align with In-Country Value mandates, securing petrochemical contracts.

Strategic acquisitions accelerate capability building. Recent transactions target cold-chain, reverse logistics, and e-commerce tech, signaling consolidation as a route to market breadth and digital depth. Sustainability emerges as a competitive axis: GWC pledges a 3% reduction in Scope 1 and 6% in Scope 2 emissions, installing solar rooftops and LED retrofits. Clients increasingly weigh ESG metrics in tender evaluations, reinforcing the need for green operations alongside speed and cost.

GCC Contract Logistics Industry Leaders

DHL Supply Chain (Deutsche Post DHL Group)

Aramex PJSC

CEVA Logistics

Kuehne + Nagel International AG

DSV Solutions

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is most visible where capacity, compliance, and multimodal connectivity intersect, particularly multi-user e-commerce fulfillment (including returns), pharma-grade cold-chain operations, and port-to-inland corridors that reduce dwell time and double handling. Concrete build-outs already underway reinforce these opportunity areas, including CEVA Logistics inaugurating a 23,000 sq m e-commerce-oriented facility in Dubai South with 30,000 units/day capability, and MEDLOG opening an integrated logistics park at King Abdulaziz Port in Dammam spanning over 100,000 sq m with capacity exceeding 300,000 TEUs. These additions support demand for integrated warehousing, inventory orchestration, and contract-based distribution across Saudi Arabia and the UAE, where long-term agreements dominate and shippers increasingly request bundled value-added services.

A second opportunity track is the shift from standalone nodes to interconnected trade and industrial logistics networks anchored by ports, inland dry ports, and rail links. AD Ports Group establishing a consolidated multimodal inland logistics network and Gulftainer unveiling the Al Dhaid Multi-Modal Trade Corridor, a 150-hectare facility designed with 1.5 million TEUs annual capacity, expand the addressable scope for 3PLs able to operate end-to-end solutions across sea, road, and rail interfaces. The operating environment also creates room for differentiated offerings around compliance-led service design, such as customs procedure standardization at first points of entry and digital licensing workflows, and cost-stability service models where emergency-related controls on transport and port service pricing influence contract structures and SLA risk allocation.

Recent Industry Developments

- May 2026: Aramex announced a multi-year strategic partnership with Amazon in the UAE aimed at scaling logistics capabilities and reliability. The tie-up supports higher-throughput fulfillment and delivery operations around large e-commerce volumes, raising the bar for service levels and technology integration among competing 3PLs.

- December 2025: DHL Supply Chain announced an investment of EUR 120 million to build a 55,000 sq m multi-user warehouse in Dubai South, with groundbreaking scheduled for Q1 2026. The project expands Grade-A multi-user capacity in a key free zone logistics cluster and strengthens DHLs ability to serve multi-vertical customers with standardized, scalable operations.

- October 2024: CEVA Logistics and Almajdouie Logistics finalized their joint venture, CEVA Almajdouie Logistics, to deliver integrated logistics solutions in Saudi Arabia. The JV structure deepens local operating coverage and supports contract logistics bids that require in-country capabilities aligned with large industrial and retail programs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market tracks the revenue earned in GCC countries when a third party runs contracted logistics work for a customer, covering warehousing, in-country transport execution, inventory visibility, and order fulfillment as part of a managed agreement.

Scope exclusions: Cross-border freight forwarding billed outside the GCC, stand-alone last-mile parcel revenues, and pure warehouse space rentals are excluded.

Segmentation Overview

- By Service

- Transportation Management

- Road

- Air

- Sea

- Rail

- Warehousing and Distribution

- Cold Chain/Temperature-Controlled

- Non-Cold Chain/Non-Temperature-Controlled

- Value-Added Services (Kitting, Packaging, Assembly, etc.)

- Transportation Management

- By End-User Industry

- Manufacturing and Automotive

- Consumer Goods and Retail (incl. E-commerce)

- High-Tech and Electronics

- Healthcare and Pharmaceuticals

- Oil, Gas and Chemicals

- Other End Users

- By Contract Duration

- Short-Term (Less Than 1 Year)

- Long-Term (Greater than or equal to 1 Year)

- By Country

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Oman

- Bahrain

Data Sources, Market Sizing, and Validation

Desk Research

We start with desk research to set the demand pool and keep the GCC boundaries consistent across countries. We use public source types such as GCC national statistics portals, central bank releases, customs and trade statistics, and ports and civil aviation authority traffic updates, to anchor freight activity and warehouse throughput signals.

To translate activity into an outsourced contract logistics value, we also review operator websites, annual reports, investor presentations, and regional business press for contract wins, capacity additions, and service footprints. Where needed, we reference paid subscriptions for company financials and intelligence, shipment-level import export checks, and patent databases to confirm automation adoption and changes in service capability. These examples are illustrative and not exhaustive, and other public references were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Next, we validate assumptions through expert calls and structured surveys with logistics providers, facility operators, freight buyers, and sector specialists across Saudi Arabia, the UAE, Qatar, Kuwait, Oman, and Bahrain. Respondent input is used to confirm outsourcing penetration, the common contract constructs in the region, and how pricing moves with fuel, labor, and warehouse utilization, so the model reflects current operating reality.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 14% | |

| Mid tier: 57% | Functional/Unit leaders: 33% | |

| Smaller Players: 14% | Managers: 53% |

Market-Sizing & Forecasting

Sizing is built using top-down and bottom-up logic, where country-level logistics activity and sector demand signals are reconstructed into an addressable outsourced contract logistics pool, then filtered through service intensity assumptions. In practice, we map indicators such as non-oil trade flows, retail and e-commerce order growth signals, industrial output trends, port and airport cargo throughput, and warehousing capacity additions, and then relate them to contract logistics spending patterns described by interviewees.

The totals are then stress-tested with selective bottom-up checks, such as rolling up a sampled set of provider revenues, triangulating warehouse square footage with utilization and typical rate ranges, and validating transport management volumes through channel conversations. Where company disclosures are limited, gaps are handled using peer-group proxies and country-mix logic, followed by an adjustment pass so outliers do not distort the GCC total.

For forecasting, scenario analysis is applied around macro and sector drivers that matter in the region, including infrastructure build-outs, manufacturing and pharma investment, and changes in customer outsourcing preference. Assumptions for price progression and utilization are aligned to the consensus from primary discussions so the forward view remains realistic year by year.

Data Validation & Update Cycle

Outputs are validated by comparing implied spend per ton and spend per square foot against independent signals from trade, cargo, and capacity datasets, and then checking that country shares remain directionally consistent with known investment patterns. If a variance looks too high, we revisit the driver assumptions, re-check currency conversion timing, and re-contact selected respondents for clarification before sign-off.

A second analyst review is completed for logic consistency, followed by a final pre-release pass to capture material events such as major contract awards, policy changes, or sharp freight cost shifts. The report is refreshed annually, with interim updates triggered when a significant market-moving development is confirmed.

Mordor Intelligence's Gcc Contract Logistics Market Size Measured Against Other Published Estimates

Published numbers for GCC contract logistics can differ even when the titles look similar, because the service scope, billing location, and included contract types are not always matched. Differences also come from how each publisher treats outsourcing penetration and how quickly pricing assumptions are refreshed in a market that is sensitive to fuel and labor movements.

Stand-alone last-mile parcel income sits outside Mordor Intelligence's scope, which is why some broader logistics estimates can land higher even if their growth rate looks similar. Another common gap is that some figures fold in cross-border forwarding billed outside the region, or treat pure storage rentals as contract logistics, even though those revenues do not behave like managed service contracts.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.33 B (2025) | |

| Global Consultancy A | USD 12.50 B (2024) | Uses a broader definition that appears to include additional supply chain management and adjacent logistics revenues, with limited clarity on exclusions like parcel last-mile and storage rentals, which can raise the total. |

| Industry Publisher B | USD 6.90 B (2023) | Starts from an earlier base year and applies a higher long-range growth path, and it does not state explicit exclusions, which makes it harder to separate managed contract logistics from adjacent services when aligning years. |

Looking across the table, the spread is mainly explained by what gets counted as contracted managed service revenue versus adjacent logistics income, and by differences in base year and refresh cadence. The steps are kept transparent by tying totals back to observable activity signals and then re-checking them with provider-side and facility-side inputs, which helps keep assumptions realistic for client use.

Key Questions Answered in the Report

What is the current size of the GCC Contract Logistics market and how fast is it growing?

The market stands at USD 7.7 billion in 2026 and is forecast to reach USD 9.85 billion by 2031, reflecting a 5.04% CAGR.

Which country holds the largest share in the GCC Contract Logistics market?

Saudi Arabia leads with 52.60% of the market in 2025, supported by Vision 2030 investments that aim to establish 59 logistics centers.

Which service segment dominates the market today?

Warehousing and distribution accounts for 46.40% of revenue in 2025, driven by extensive investments in logistics zones across Saudi Arabia and the UAE.

What end-user industry is expanding the fastest?

Healthcare and pharmaceuticals shows the quickest pace, advancing at a 8.65% CAGR during 2026-2031 due to rising cold-chain needs and healthcare spending.

What are the primary challenges limiting market efficiency?

Cabotage restrictions, Grade-A warehouse shortages, and varying customs procedures add cost, extend lead times, and restrict cross-border network optimization.

How concentrated is the competitive landscape?

The top five logistics providers together control roughly 55% of market revenues, indicating moderate concentration with both global and regional players holding influence.

Page last updated on: