Farm Equipment Rental Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

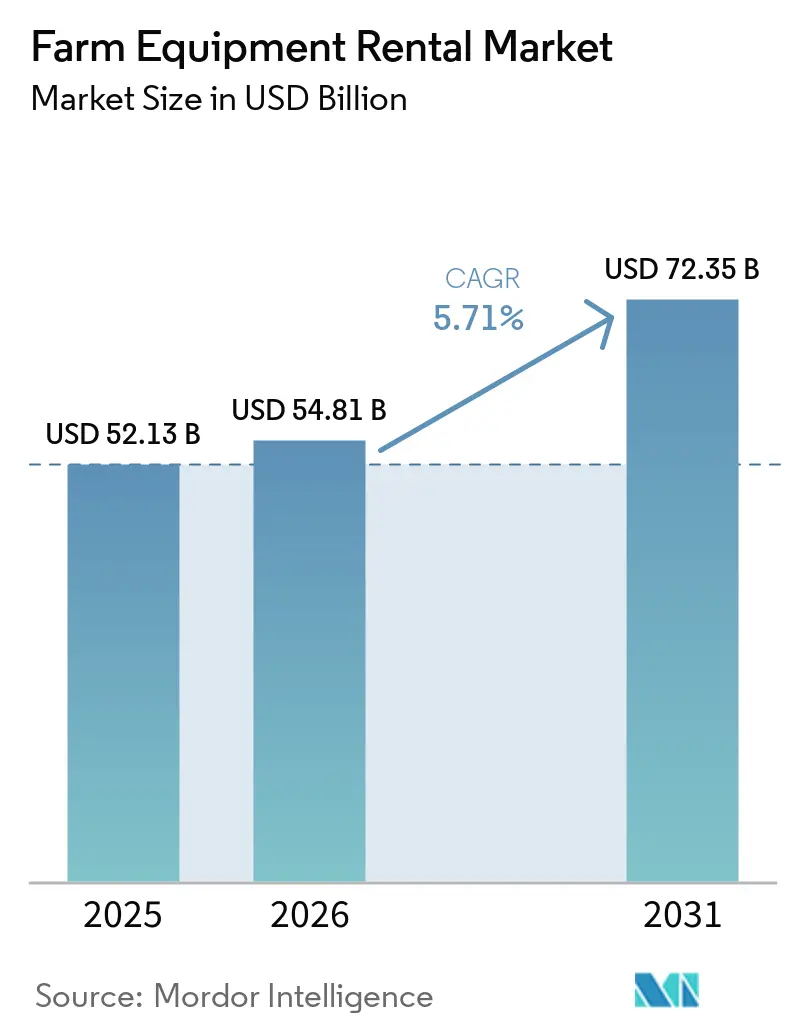

| Market Size (2026) | USD 54.81 Billion |

| Market Size (2031) | USD 72.35 Billion |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

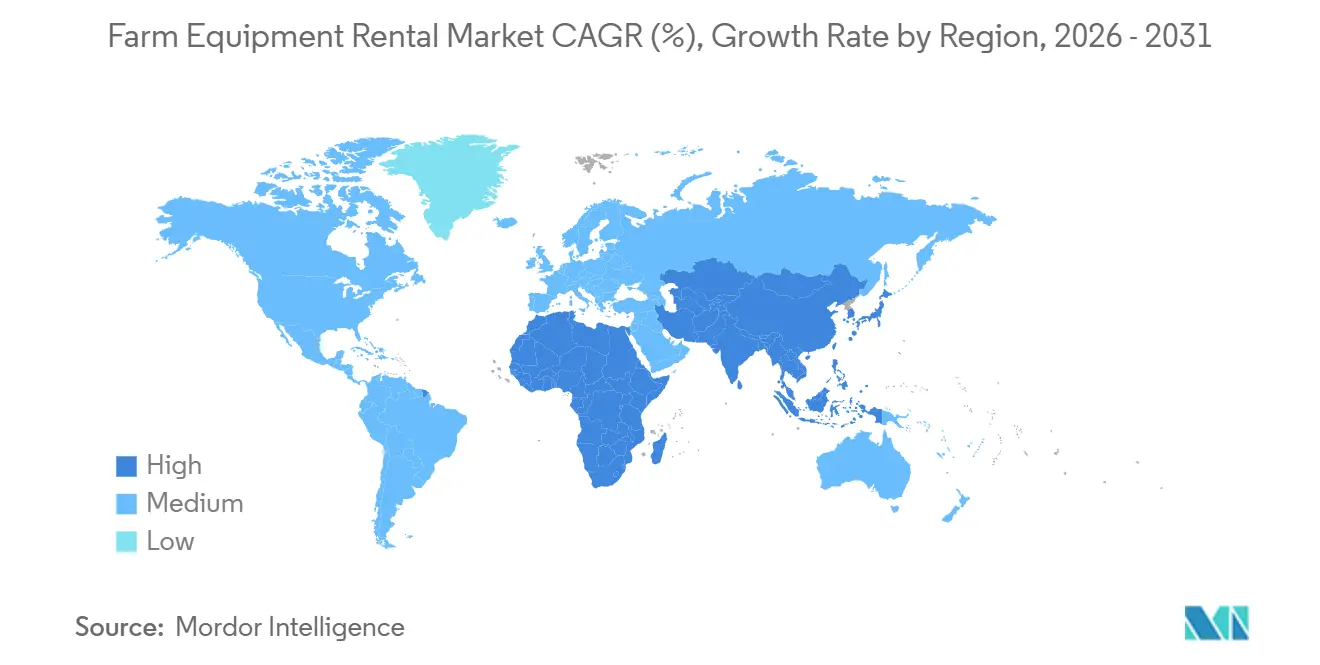

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Farm Equipment Rental Market Analysis by Mordor Intelligence

The farm equipment rental market size was valued at USD 52.13 billion in 2025 and estimated to grow from USD 54.81 billion in 2026 to reach USD 72.35 billion by 2031, at a CAGR of 5.71% during the forecast period (2026-2031). As precision machinery becomes more capital-intensive and commodity prices fluctuate, farmers are increasingly turning to pay-per-use models, easing their upfront cash burdens. Recognizing the potential, original equipment manufacturer finance arms are prioritizing rental portfolios as a key source of revenue. While Asia Pacific accounts for a significant share of revenue, Africa is poised for the quickest expansion, driven by donor-funded mechanization initiatives and the rise of mobile booking applications. Innovations like app-driven dynamic pricing, ESG-focused financing for electric fleets, and trials of autonomous equipment are transforming fleet dynamics. Meanwhile, labor shortages in OECD countries are spurring a heightened demand for driverless tractors.

Key Report Takeaways

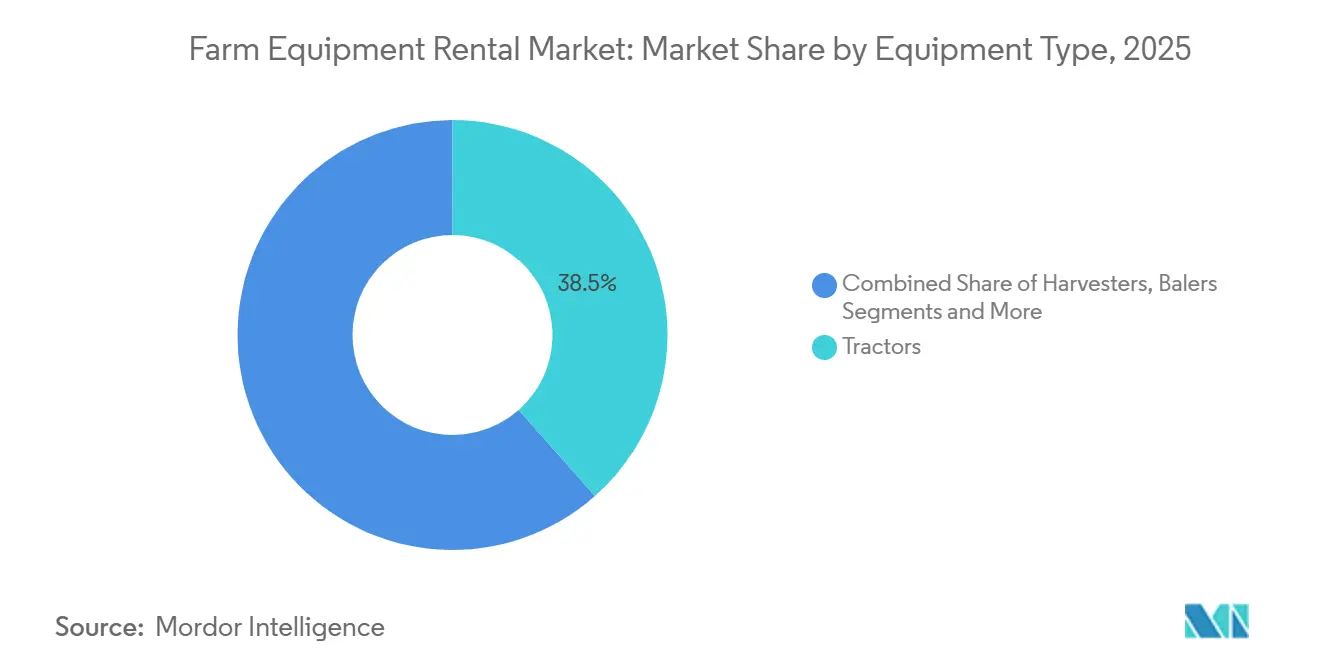

- By equipment type, tractors led with 38.47% of farm equipment rental market share in 2025, while harvesters are projected to compound at a 7.40% CAGR to 2031.

- By power output, the 71-130 HP segment accounted for 31.34% of the farm equipment rental market size in 2025; units with a power output greater than 250 HP are forecast to grow at an 8.50% CAGR through 2031.

- By drive type, four-wheel-drive machines captured 64.61% of the revenue in 2025; two-wheel-drive equipment is projected to show the highest CAGR of 7.80% from 2026 to 2031.

- By business model, offline dealers and co-op yards held an 89.43% share of the farm equipment rental market size in 2025, whereas online platforms are expected to rise at a 15.20% CAGR until 2031.

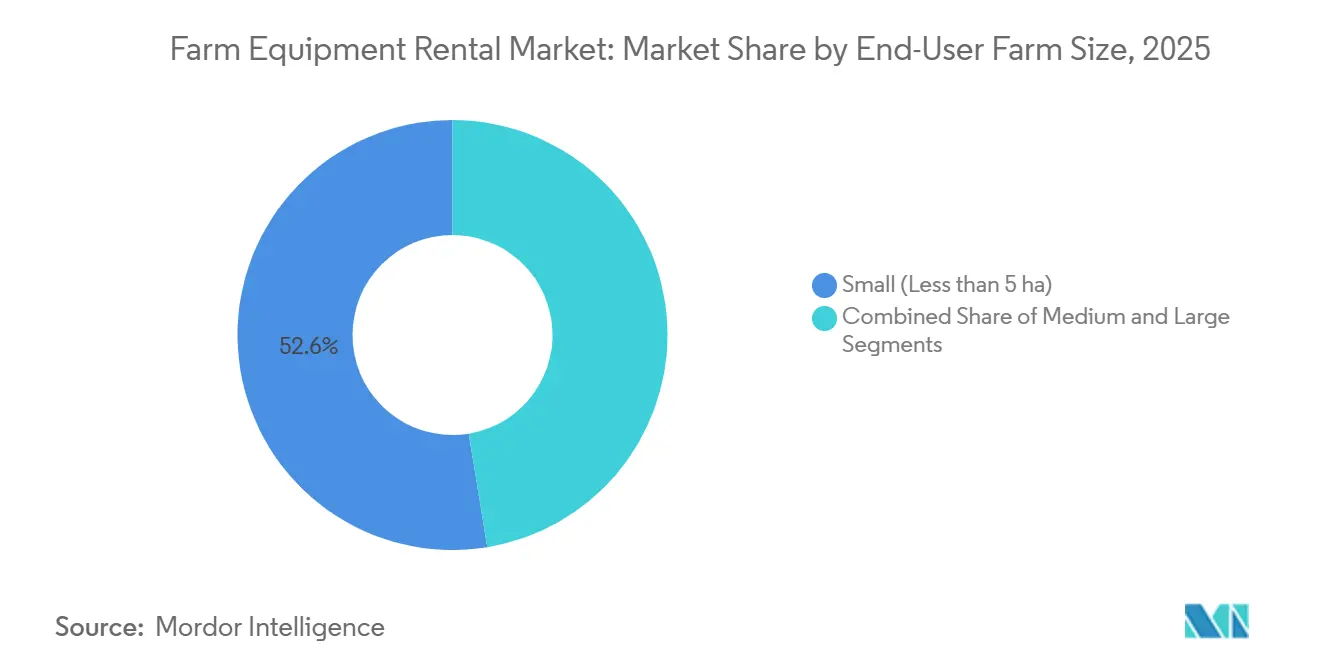

- By end-user farm size, small farms (less than 5 ha) represented 52.59% share in 2025, but large farms (greater than 20 ha) are expanding fastest in the Farm Equipment Rental Market at a 6.50% CAGR to 2031.

- By rental duration, seasonal contracts (3-9 months) made up 50.80% of 2025 revenue; annual agreements (greater than 9 months) are expected to grow at a 6.15% CAGR through 2031.

- By region, Asia Pacific contributed a dominant 44.25% share in 2025 in the Farm Equipment Rental Market, while Africa is poised for the fastest growth at 7.50% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Farm Equipment Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-Inflation of Smart Machinery | +1.2% | Asia Pacific; spillover to South America | Medium term (2–4 years) |

| Indian CHC-Linked Subsidies | +1.1% | India; pilots in Bangladesh and Nepal | Medium term (2–4 years) |

| Seasonal Workforce Deficit | +0.9% | North America and Europe | Short term (≤ 2 years) |

| App-Based Fleet Marketplaces | +0.8% | Western Europe | Medium term (2–4 years) |

| Peak-Harvest Demand Spikes | +0.7% | United States Midwest | Short term (≤ 2 years) |

| ESG-Linked Finance for Electrified Fleets | +0.5% | Europe and California lead | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost-Inflation of Smart Machinery Accelerating Pay-per-Use Adoption in Asia Pacific

Mid-range tractor list prices have increased significantly due to the use of precision components, which extend ownership payback periods for smaller farms. However, rental options provide a viable alternative [1]“2025 Component Cost Disclosure,”, CNH Industrial, cnhindustrial.com. For example, Deere’s See & Spray retrofit, while expensive to purchase, can be rented at a fraction of the cost. This approach allows smallholders in Asia to benefit from agronomic advancements without significant capital investment. Additionally, bookings for GPS planters on India's Tringo platform have risen, reflecting improved access to precision tools. Small farms with limited machine usage are increasingly finding rental options more economical than ownership, driving growth in the Farm Equipment Rental Market.

Indian CHC-Linked Subsidies Catalyzing Village-Level Rental Hubs

India has allocated significant funding to establish numerous Custom Hiring Centres, each of which benefits from an equipment subsidy [2]“Sub-Mission on Agricultural Mechanization Progress,”, Press Information Bureau, pib.gov.in. Strategically located in proximity to users, these centres have significantly reduced tractor transport times. This initiative has also increased annual tractor utilization. Trringo, in collaboration with the government’s Direct Benefit Transfer portal, has expedited reimbursement cycles, significantly reducing delays. Looking ahead, neighboring countries Bangladesh and Nepal are planning pilot rollouts, signaling an expansion in the agricultural equipment rental market.

Seasonal Workforce Deficit in OECD Nations Driving Autonomous Tractor Rentals

Farm labor in the Organisation for Economic Co-operation and Development (OECD) countries has contracted significantly. Concurrently, United States H-2A visa issuances have declined, resulting in a surge in wages in the Midwest [3]“Farm Labor and H-2A Statistics 2025,”, U.S. Department of Agriculture, usda.gov. Deere unveiled its cableless 8R tractor, enabling a single supervisor to manage multiple driverless units. This innovation has substantially reduced labor input per hectare in the Farm Equipment Rental Market. Priced at a premium, farmers are opting to rent these tractors, allowing them to experiment with autonomy while sidestepping the intricacies of software licensing. AGCO has observed a significant increase in the rental of its autonomous-ready tractors in Europe, accompanied by a notable rise in adoption over time.

App-Based Fleet Marketplaces Scaling Rapidly in Western Europe

Germany's FarmLease has significantly improved its asset utilization, surpassing dealer yards. By leveraging algorithms, FarmLease optimizes inventory matching, timing, and trucking routes, effectively minimizing idle time in the Farm Equipment Rental Market. Meanwhile, France's Growy harnesses telematics from OEM cloud portals, providing verified service histories and reducing disputes. With dynamic rate engines, Growy adjusts prices daily, capitalizing on peak periods and expanding its foothold in the agricultural equipment rental sector.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low Awareness Among Sub-Saharan Smallholders | -0.6% | Ethiopia, Tanzania, Uganda | Medium term (2–4 years) |

| High Logistics Cost in Fragmented Asia Pacific | -0.5% | South and Southeast Asia | Medium term (2–4 years) |

| Scarcity of <250 HP Units During United States Harvest | -0.4% | Midwest and Great Plains | Short term (≤ 2 years) |

| Equipment Misuse Liability on P2P Platforms | -0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low Awareness of Rental Economics Among Sub-Saharan Smallholders

Rental penetration in Africa remains low despite a positive growth outlook in the Farm Equipment Rental Market. This stagnation is primarily attributed to the fact that many smallholders in Ethiopia, Tanzania, and Uganda remain unaware of the benefits of rentals. Hello Tractor's need for multiple live demos for each first-time customer highlights these behavioral challenges. Furthermore, with limited access to mobile money in rural East Africa, many are compelled to resort to cash payments, increasing transaction friction. Additionally, trust issues surrounding equipment maintenance and payment disputes hinder repeat bookings, stunting the growth of the agricultural equipment rental market.

Scarcity of Less than 250 HP Units During North American Harvest Window

By mid-September, Iowa's inventory of mid-range combines was completely depleted. With high utilization rates, late renters were compelled to turn to larger Class 9 units, which came at a significant premium per hour. Original Equipment Manufacturers (OEMs) are focusing on high-horsepower production to secure better profit margins, resulting in a shortage at rental yards in the Farm Equipment Rental Market. Acquiring additional mid-range machines would lead to an idle off-season period, subsequently pushing the Return on Investment (ROI) below acceptable thresholds. Surge pricing, which occurs during periods of high demand compared to off-peak rates, poses a risk of steering growers towards used purchases, thereby moderating the growth of the agricultural equipment rental market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Tractors Anchor Demand, Harvesters Surge

Tractors generated 38.47% of 2025 revenue, the most significant slice of the agricultural equipment rental market share, thanks to their year-round utility across tillage, planting, and hauling. Harvesters are growing at a 7.40% CAGR to 2031, as compressed harvest windows nudge growers toward temporary access to USD 600,000 combines. Bookings for sprayers on Trringo surged as the See & Spray technology became available for rent. Balers and sprayers accounted for a significant portion of the total volume. Specialty implements, which benefit from peer-to-peer aggregation, are experiencing heightened utilization, thereby boosting the agricultural equipment rental market for these niche tools.

Demand for autonomous-ready tractors is set to escalate, with Deere’s cableless 8R leading the charge. Operators now have the opportunity to test guidance software with no risk, paving the way for quicker adoption of tractors and surpassing earlier forecasts. As balers and precision sprayers continue to gain traction, their ability to offset rising input costs through variable-rate applications underscores the widespread significance of the agricultural equipment rental market.

By Power Output: Mid-Range Dominates, High-Capacity Accelerates

The 71–130 HP band accounted for 31.34% of the 2025 share, as mixed-crop farms favor fuel efficiency and versatility. Machines above 250 HP, however, are accelerating at 8.50% CAGR, propelling the agricultural equipment rental market size for high-capacity units, especially in large United States and Australian grain estates. Asian smallholders, benefiting from subsidy-aided village hubs, accounted for a significant share of the volume in sub-30 HP compact tractors.

High-horsepower rentals, despite lower annual utilization, command premium hourly rates. This trend is underscored by Deere Financial's notable lease exposure to tractors in the higher horsepower category. Furthermore, the scarcity of mid-range combines during United States harvests highlights a misalignment in fleet mix. Rental operators are urged to address this through data-driven procurement, emphasizing the evolving dynamics of the agricultural equipment rental market.

By Drive Type: Four-Wheel Drive Dominance, Two-Wheel Gains

Four-wheel-drive units comprised 64.61% of 2025 deployments due to superior traction for precision planting in the Farm Equipment Rental Market. Two-wheel-drive machines are expanding at a 7.80% CAGR, buoyed by cost sensitivity in South Asia and lower maintenance overhead. CNH reported that two-wheel-drive operators demonstrated higher availability compared to four-wheel-drive units, leading to improved operational efficiency and increased opportunities for revenue generation. This higher availability allows for more consistent usage, making two-wheel-drive units a more reliable option in various applications.

Electrification is expected to influence a shift in preference toward two-wheel drives. This trend is driven by the advantages of lighter drivetrains, which enhance battery efficiency and overall performance in compact tractors. These technological advancements are likely to expand the agricultural equipment rental industry’s portfolio, offering a wider range of solutions to meet diverse customer needs and increasing the industry’s overall flexibility and market appeal.

By Business Model: Offline Stronghold Faces Digital Disruption

Dealer and co-operative yards held 89.43% of 2025 transactions, underscoring the relationship-driven nature of farm purchasing. Yet, app-based platforms are surging at a 15.20% CAGR by unlocking 72% utilization through algorithmic dispatch. While digital platforms excel in short-term commodity rentals, traditional offline yards focus on intricate assets needing service support. This dynamic maintains a balanced dual-channel system in the agricultural equipment rental market.

Peer-to-peer platforms like Kwipped have significantly enhanced the utilization of specialty equipment. However, the rise in damage claims highlights the importance of verification technologies, such as blockchain usage logs, which are now patented by Deere, in ensuring accountability and reliability.

By End-User Farm Size: Smallholder Concentration Defies Expectations

Holdings under 5 ha produced 52.59% of the 2025 demand, driven by India’s CHC subsidy, which funds 40% of the equipment costs. Medium farms, typically ranging in size from 5 to 20 hectares, contribute significantly to the market volume. These farms often rely on rental services for specialized tools that are used only occasionally.

Large estates exceeding 20 ha generated a significant portion of the revenue, yet they are growing at a 6.50% CAGR as they hedge against obsolescence risk by renting autonomous and precision-ready machinery. These estates are increasingly adopting rental services for advanced machinery, such as autonomous and precision-ready equipment, to mitigate the risks associated with technological obsolescence. Smallholders, due to their overwhelming numbers, continue to serve as the foundation of the agricultural equipment rental market.

By Rental Duration: Seasonal Contracts Lead, Annual Agreements Climb

Seasonal contracts covering 3–9 months delivered 50.80% of 2025 revenue, mirroring crop-cycle demand peaks. Annual agreements (exceeding 9 months) are expanding at a 6.15% CAGR because European mixed-crop operators are increasingly focusing on adopting year-round autonomous fleets to significantly reduce machinery costs per hectare. Harvest compressions in the United States have influenced the demand for short-term contracts, which are typically less than three months in duration. The agricultural equipment rental market is primarily driven by dual-peak economics, where the highest value is achieved during either very short or very long rental periods.

Geography Analysis

Asia Pacific contributed 44.25% of 2025 revenue for the agricultural equipment rental market. India's CHC scheme and China's efforts in consolidating farm plots have strengthened Trringo's network, enabling it to achieve significant asset utilization across numerous villages while serving a large farmer base. Additionally, Japan's aging farmer population and South Korea's subsidy program for machinery-sharing cooperatives continue to support the region's agricultural dominance.

Africa is experiencing a 7.50% CAGR, although awareness hurdles are limiting penetration to under 8%. Hello Tractor’s SMS marketplace spans 12 nations, yet it still spends heavily on in-person demos. Donor-funded mechanization drives volume, but low mobile-money reach slows digital scaling, tempering agricultural equipment rental market uptake.

North America and Europe collectively account for a significant portion of the revenue in the agricultural equipment rental industry. Deere's lease receivables emphasize the company's focus on generating income through usage-based models. FarmLease and Growy have successfully consolidated inventory from multiple dealers, optimizing utilization rates through the implementation of dynamic pricing strategies. In Latin America, the agricultural equipment rental market is gradually developing, with soybean estates increasingly turning to rentals as a strategy to manage currency fluctuations. Electrification initiatives in the European Union are currently restricted to peri-urban areas due to the need for grid infrastructure upgrades, which is influencing the regional growth patterns within the sector.

Competitive Landscape

Deere, CNH Industrial, AGCO, Kubota, and Titan Machinery, the top suppliers, collectively hold a significant share of the global agricultural equipment rental market, indicating moderate fragmentation. CNH's equipment receivables have shown growth, reflecting a shift toward rentals driven by the equipment's lifecycle. Digital aggregators, such as Trringo, Farmease, FarmLease, and Growy, utilize algorithmic dispatch to optimize utilization rates, positioning data as a critical competitive advantage. Telematics-enabled predictive maintenance is another key differentiator; for example, Growy's integration with OEM cloud portals has significantly reduced disputes.

Electrified fleets remain an area of untapped potential, with Kubota's EK1 rollout currently focused on peri-urban areas in Europe where grid infrastructure is more developed. The scarcity of mid-range combines during harvest seasons in North America remains a persistent challenge. Platforms capable of accurately forecasting demand surges and dynamically managing inventory are expected to gain a competitive edge. Deere's blockchain patent for usage verification points to a future where unchangeable data enhances renter trust and strengthens residual values, further solidifying its leadership in the agricultural equipment rental market.

Farm Equipment Rental Industry Leaders

-

Deere & Company

-

CNH Industrial N.V

-

AGCO Corporation

-

Kubota Corporation

-

Titan Machinery Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: JFarm Services is a Chennai-based platform enabling farmers to rent tractors and equipment via app or call, enhancing access to mechanization across 16 Indian states.

- April 2025: CASE launched new compact loaders and upgraded machines tailored for rental businesses—offering intuitive operation, easy maintenance, and versatility to boost utilization, customer satisfaction, and fleet profitability.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the farm equipment rental market as the gross revenue booked when farmers, cooperatives, or ag-service outfits rent brand-new field machines such as tractors, combine harvesters, seeders, sprayers, balers, tillage, and other implements for periods that may run from a few hours to a full crop cycle. Payments can follow time, acreage, or output contracts, and we keep this boundary unchanged at every forecast refresh.

Short-term landscaping tool hire, construction machinery, and any lease of pre-owned agricultural equipment sit outside the scope.

Segmentation Overview

-

By Equipment Type

- Tractors

- Harvesters

- Balers

- Sprayers

- Seeders & Planters

- Tillage & Soil-Cultivation Equipment

- Other Implements

-

By Power Output (HP)

- Less than 30 HP

- 31-70 HP

- 71-130 HP

- 131-250 HP

- More than 250 HP

-

By Drive Type

- Two-Wheel Drive

- Four-Wheel Drive

-

By Business Model

- Offline Dealer & Co-op Yards

- Online / App-Based Platforms

-

By End-User Farm Size

- Small (Less than 5 ha)

- Medium (5-20 ha)

- Large (More than 20 ha)

-

By Rental Duration

- Short-Term (Less than 3 m)

- Seasonal (3-9 m)

- Annual / Long-Term (More than 9 m)

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia Pacific

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Egypt

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed rental-yard managers, app founders, cooperative heads, and regional ag-credit officers across Asia Pacific, North America, Europe, and Africa. Their inputs validated utilization peaks, service price ladders, and downtime patterns that public statistics leave vague.

Desk Research

The analyst team started with open datasets from FAO mechanization ratios, USDA and Eurostat machinery price files, UN Comtrade HS-8432/8433 trade flows, and OECD farm-income curves. We then layered insights from Agrievolution, India's FICCI custom-hiring dashboard, and ministry portals that track subsidy releases and rainfall shocks. Annual reports, press briefs, and fleet-age notes sharpened tariff benchmarks, while paid feeds from D&B Hoovers and Dow Jones Factiva anchored firm-level splits. The sources named are illustrative; many additional publications helped us confirm trends and close data gaps.

A second sweep mapped smartphone booking uptake, seasonality, and repair-cost ratios, giving our desk estimates real-world texture before they entered the model.

Market-Sizing & Forecasting

One top-down plus bottom-up loop powers the model. We rebuild demand from cultivated area multiplied by mechanization penetration and rental intensity, then reconcile totals with supplier roll-ups of active fleets and sampled tariffs. Six driver variables, horsepower mix, mobile booking share, subsidy timing, farm cash-flow swings, rainfall deviation, and machinery inflation, feed a multivariate regression that projects value through 2030. Regional analogs bridge sparse datapoints before senior sign-off.

Data Validation & Update Cycle

Outputs pass variance scans against shipment tallies and listed lessor revenues, followed by a peer review. We refresh numbers each year and issue interim updates whenever policy or weather events materially shift demand.

Why Mordor's Farm Equipment Rental Baseline Commands Credibility

Published estimates often diverge because firms adopt differing scopes, base years, and refresh cadences while rental income swings with crop margins.

Key gap drivers include whether used equipment is counted, how tariff inflation is layered, and if informal farmer-to-farmer sharing is modeled before currency conversion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 54.8 B (2025) | Mordor Intelligence | - |

| USD 56.0 B (2024) | Global Consultancy A | Counts used-equipment leases, single mid-year FX rate |

| USD 66.4 B (2025) | Regional Consultancy B | Assumes uniform tariff growth, no utilization check |

| USD 53.7 B (2024) | Trade Journal C | Omits online-platform revenue, limited geography |

These comparisons confirm that our disciplined scoping, driver-level modeling, and yearly refresh give decision-makers a balanced, transparent baseline they can trust.

Key Questions Answered in the Report

What is the current global value of the agricultural equipment rental market?

It stood at USD 54.81 billion in 2026 and is projected to hit USD 72.35 billion by 2031.

Which region leads revenue contribution?

Asia Pacific held 44.25% of 2025 revenue, driven by India’s Custom Hiring Centre program and rising app-based platforms.

Which equipment category commands the greatest rental demand?

Tractors rank first with 38.47% of 2025 revenue due to their year-round versatility.

How fast are app-based rental platforms growing?

Digital marketplaces are expanding at 15.20% CAGR, achieving 72% fleet utilization by matching inventory and timing algorithmically.

Page last updated on: