Gaming Console Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

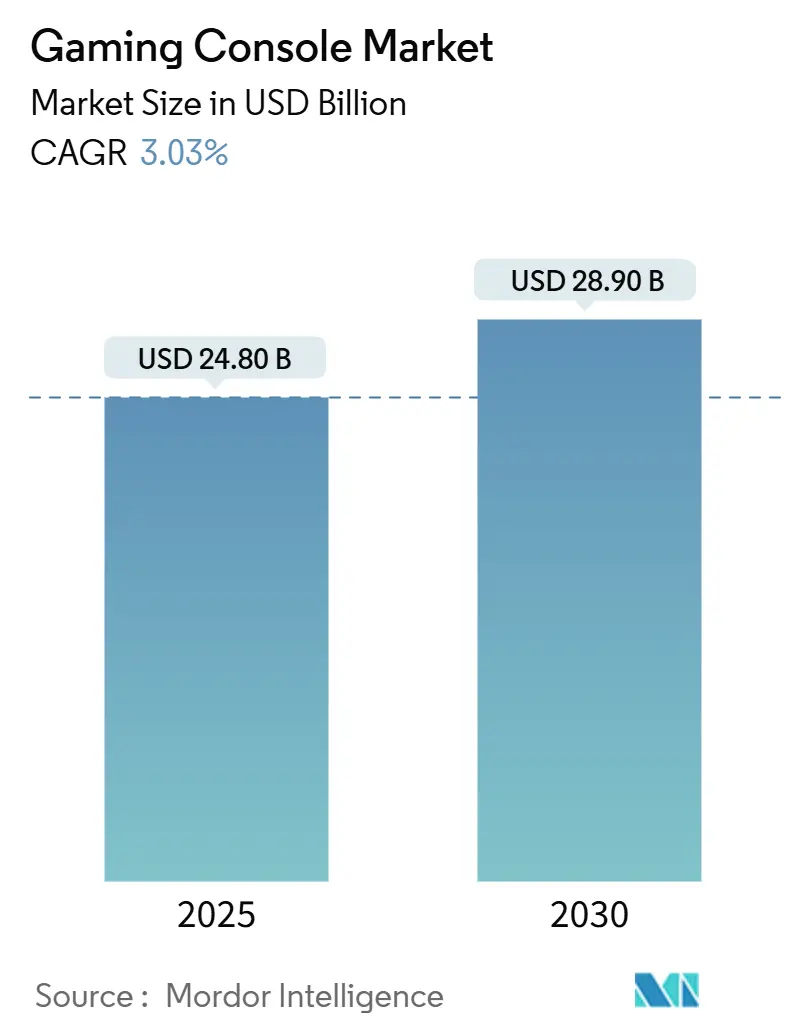

| Market Size (2025) | USD 24.80 Billion |

| Market Size (2030) | USD 28.90 Billion |

| Growth Rate (2025 - 2030) | 3.03% CAGR |

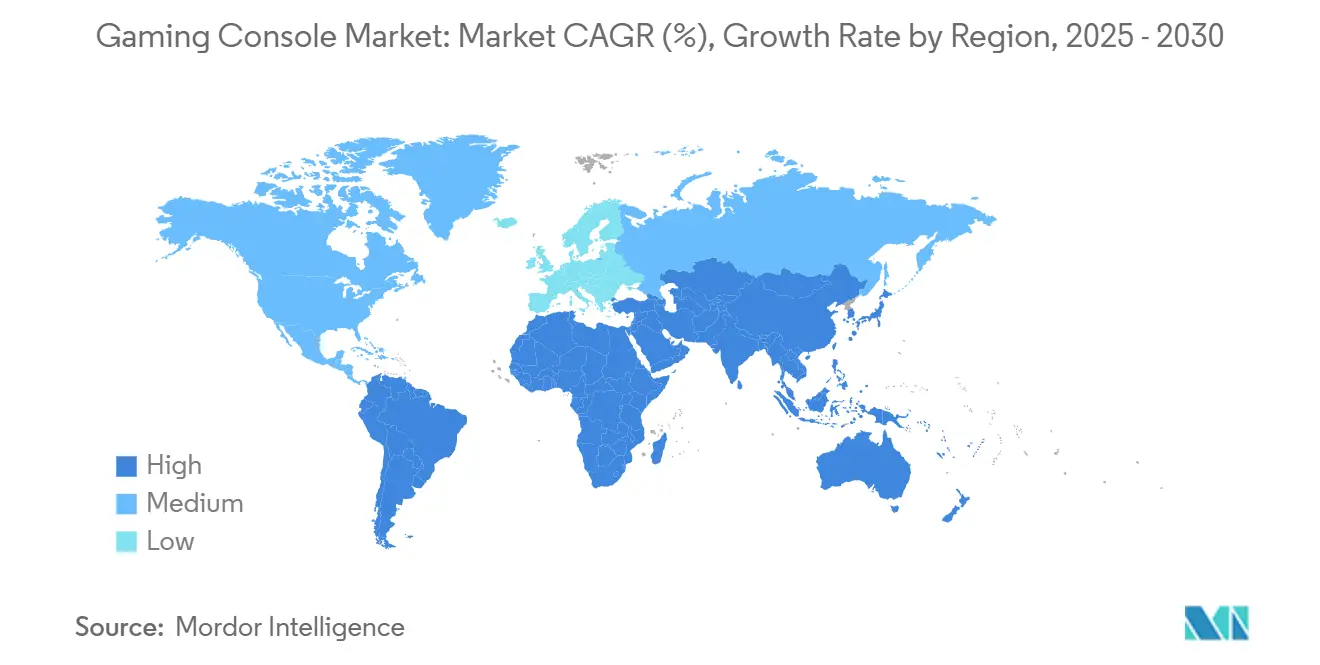

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gaming Console Market Analysis by Mordor Intelligence

The gaming console market size is estimated at USD 24.8 billion in 2025 and is forecast to climb to USD 28.85 billion by 2030, progressing at a 3.03% CAGR between 2025 and 2030. Demand stems from hardware refresh cycles triggered by visually intense AAA titles, the rapid spread of 8K UHD televisions in Asia, and lower bill-of-materials costs for hybrid devices using cloud-agnostic silicon. While established regions approach saturation, emerging economies in the Middle East, Africa, and Latin America present fresh revenue streams as broadband access widens and esports ecosystems mature. Competitive dynamics underscore Sony’s continued dominance, Microsoft’s pivot toward a services-first model, and Nintendo’s focus on portable–hybrid innovation, even as smaller entrants leverage ARM-based architectures to address untapped niches. Supply-chain volatility around 5 nm wafers and rising substitution risk from cloud-only sticks temper growth yet also spur strategic partnerships that diversify sourcing and drive investments in regional assembly.

Key Report Takeaways

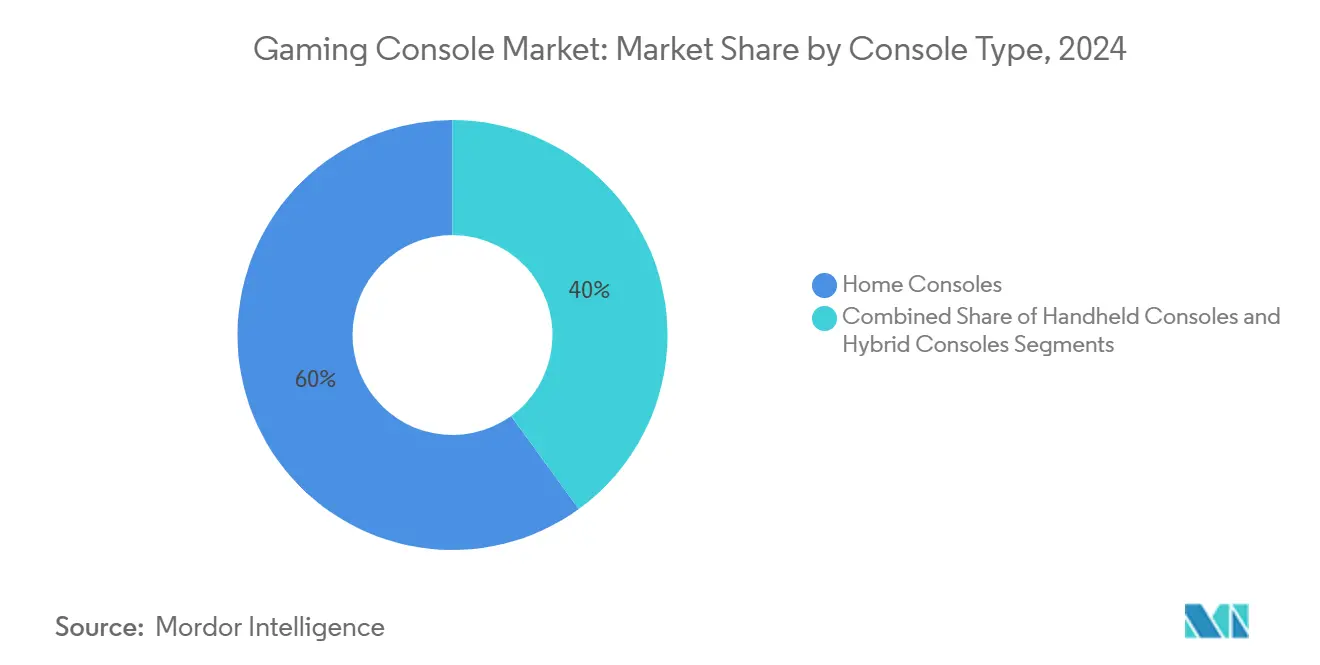

- By console type, home consoles led with 60% of gaming console market share in 2024, whereas hybrid models are projected to post the fastest 5.9% CAGR through 2030.

- By technology, 4 K-ready systems captured 64% revenue share in 2024; 8 K-ready devices are forecast to expand at a 9.4% CAGR to 2030.

- By processor architecture, x86 designs held 72% share of the gaming console market size in 2024, while ARM-based systems recorded the highest projected 7% CAGR for 2025-2030.

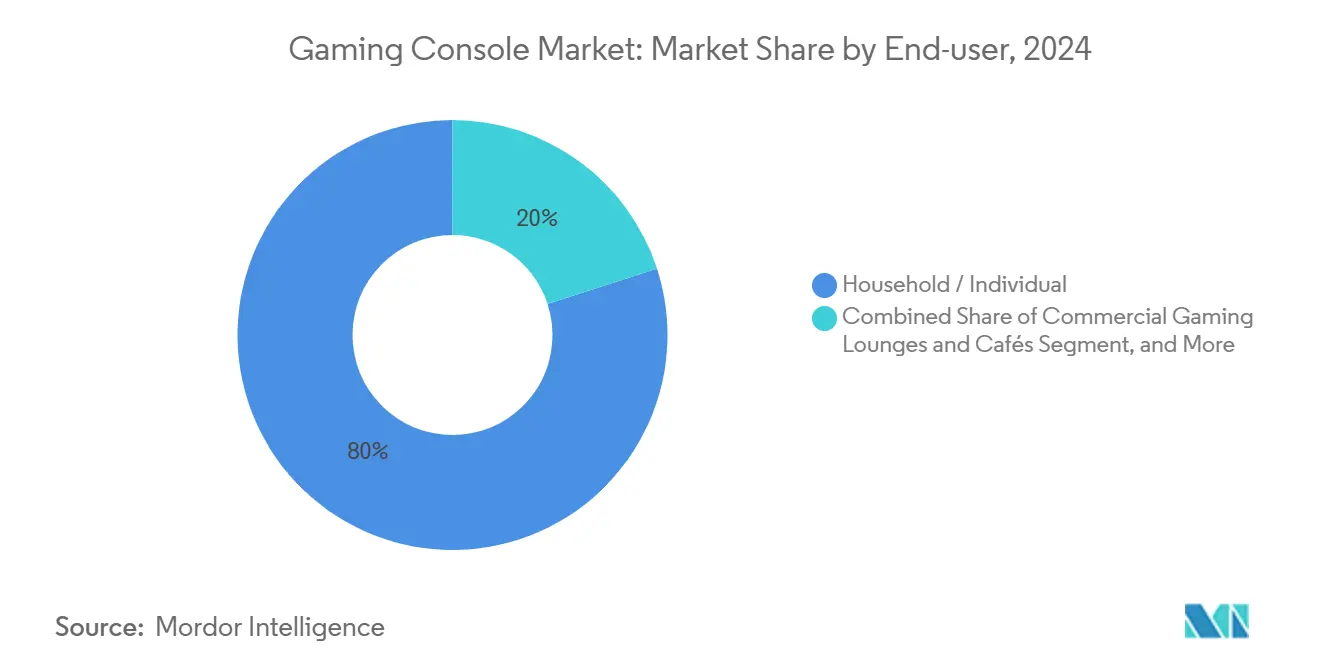

- By end-user, household/individual buyers accounted for an 88% share in 2024; institutional customers are advancing at a 7.3% CAGR.

- By distribution channel, offline stores retained 48% of sales in 2024, yet online channels are rising fastest at a 6.5% CAGR.

- By geography, Asia-Pacific commanded 37% of 2024 revenue; the Middle East & Africa region is the quickest-growing at a 4.8% CAGR.

Global Gaming Console Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AAA-grade photorealistic titles | +1.2% | Global (North America, Europe, developed APAC) | Medium term (2–4 years) |

| 8K UHD TV adoption in Asia | +0.9% | Japan, South Korea, China | Medium term (2–4 years) |

| Cloud-agnostic silicon for hybrids | +0.6% | Global | Medium term (2–4 years) |

| Esports franchise licensing | +0.5% | Middle East, Africa, SE Asia, Latin America | Long term (≥ 4 years) |

| Government subsidies on locally-assembled consoles | +0.4% | Brazil, India, with potential expansion to other emerging markets | Medium term (3-4 years) |

Source: Mordor Intelligence

Launch of AAA-Grade, Photorealistic Titles Driving Hardware Refresh Cycles

Blockbuster releases such as Grand Theft Auto 6, slated for 2025, are expected to convert a significant portion of lingering PS4 users to new-generation systems. Sony’s November 2024 launch of PS5 Pro, equipped with a 45% faster renderer and advanced ray-tracing, exemplifies the tight feedback loop linking software ambition with hardware capability. Historical performance underlines the effect: Hogwarts Legacy pushed PS5 sales up 30% month on month in early 2023, while Helldivers II and Final Fantasy VII Rebirth each added double-digit bumps during 2024 releases. Publishers and platform holders now coordinate launch calendars more closely, ensuring marquee titles arrive alongside or shortly after mid-cycle console upgrades that monetize pent-up demand.

Proliferation of 8K UHD TVs in Asia Accelerating Premium-Console Demand

Rising disposable income and aggressive television pricing have lifted 8K screen penetration across Japan and South Korea, compelling consumers to seek consoles that match display capabilities. Sony’s PS5 Pro supports 8K at 60 FPS through PlayStation Spectral Super Resolution, turning the device into an aspirational companion for premium home-theater setups [1] Luke Henderson, “PS5 Pro 8K support revealed,” TechRadar, techradar.com. The phenomenon extends to China, where domestic TV manufacturers bundle consoles in cross-promotions, reinforcing a virtuous upgrade cycle between display and gaming hardware. Early-adopter enthusiasm in Asia remains a bellwether for global high-end trends and informs production planning for the 2026-2027 console refresh window.

Cloud-Agnostic Silicon Designs Lowering BOM Costs for Hybrid Consoles

Samsung-fabricated Tegra T239 chips in Nintendo’s forthcoming Switch 2 highlight a shift toward standardized, cloud-friendly silicon that handles both local rendering and low-latency streaming workloads [2]Igor Choi, “NVIDIA Tegra T239 to power Switch successor,” Korea Herald, koreaherald.com. Harmonized designs slash bill-of-materials by up to 15%, allowing firms to reinvest savings into battery life and thermal headroom rather than raw silicon area. Combined local-and-cloud versatility attracts developers who can target broader device classes with minimal optimization overhead, accelerating software libraries and bolstering the hybrid segment’s credibility versus pure home consoles.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-gaming-only sticks | -0.8 | North America, Western Europe | Medium term (2–4 years) |

| Supply-chain volatility for 5 nm wafers | -0.7 | Global | Short term (≤ 2 years) |

Source: Mordor Intelligence

Regional league licences create strong local fan identities that, in turn, motivate hardware purchases required for competitive play. Console vendors have begun underwriting prize pools and training facilities, a move that accelerates adoption by embedding hardware standards into the esports rulebook. A logical outcome is that rising console usage in the Middle East and Africa mirrors earlier PC-gaming waves in Southeast Asia, albeit compressed into a shorter timeframe thanks to social-media amplification. Fiscal multipliers appear particularly high where telecom operators bundle low-latency connectivity with console-focused esports subscriptions.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-gaming-only sticks | -0.8% | North America, Western Europe | Medium term (2–4 years) |

| Supply-chain volatility for 5 nm wafers | -0.7% | Global | Short term (≤ 2 years) |

| Rising mobile gaming stickiness among Gen-Z in Europe | -0.5% | Europe, with spillover to North America | Long term (≥5 years) |

Source: Mordor Intelligence

Intensifying Substitution Threat from Cloud-Gaming-Only Sticks in North America

Nvidia-powered streaming dongles and Microsoft’s own “Xbox Everywhere” initiative offer console-class experiences at a fraction of hardware cost, eroding entry-level demand. Broadband penetration above 80% in the United States underpins this shift, as latency margins drop to levels tolerable for mainstream titles. Platform exclusivity becomes less decisive when the same subscription unlocks high-fidelity play on TVs, laptops, and tablets, forcing console makers to double down on differentiated IP or bundled content to justify upfront device purchases.

Supply-Chain Volatility of Advanced 5 nm GPU Wafers

Hurricane Helene curtailed high-purity quartz output in North Carolina, while SK hynix confirmed its entire 2025 HBM allocation is sold out. Limited substrate supply at TSMC for cutting-edge nodes further bottlenecks console GPU production, threatening launch timelines and constraining promotional bundles. Manufacturers have responded by staggering regional rollouts, prioritizing markets with favorable attach rates, and diversifying back-end assembly lines to hedge geopolitical and climate risks.

Segment Analysis

By Console Type: Hybrid Models Redefine Gaming Boundaries

Home systems preserved a 60% hold on 2024 revenue, underpinned by entrenched ecosystems and abundant 4K living-room displays. Yet hybrid devices form the fastest-moving cohort, advancing at a 5.9% CAGR to 2030. The upcoming Switch 2 promises backward compatibility plus an 8-inch screen, positioning it to accelerate hybrid uptake across Japan and family-oriented Western markets. Valve’s Steam Deck validated premium handheld viability with 4 million units shipped, nudging Microsoft to prototype its own handheld “Keenan” for 2025. Micro-consoles in the “Others” bucket face intensified pressure from both hybrids and subscription sticks, narrowing their niche to retro enthusiasts and entry-level customers.

Consumer migration toward versatility hints at a structural pivot: households increasingly expect one device to bridge docked 4K play and portable sessions. Should hybrids secure incremental gains beyond their projected pace, the gaming console market size could tilt more decisively away from stationary hardware in the next cycle.

Note: Segment shares of all individual segments available upon report purchase

By Technology: 8K-Ready Consoles Capture Premium Market

4 K-capable machines led 2024 revenue with a 64% share, supported by networked households sporting UHD screens. The next wave favors 8 K-ready systems, forecast to surge at a 9.4% CAGR. Sony’s PS5 Pro already primes the channel, while AI-assisted upscalers such as Project Amethyst hint at strong value retention even if native 8K rendering remains content-limited. Asia’s tech-savvy consumers set the adoption tempo: every percentage-point uptick in 8K TV ownership feeds premium console intent. Over time, AI-driven supersampling could allow mid-tier models to emulate flagship visuals, reshaping price ladders and smoothing transition risks for budget-conscious buyers.

By Processor Architecture: ARM Gains Ground in Mobile-First Markets

X86 continues to dominate with 72% of 2024 shipments, reflecting its compute prowess for cinematic experiences. ARM, however, is slated to gain fastest at a 7% CAGR as battery-efficient designs unlock thinner portable chassis and cooler thermals. Nintendo’s ARM-based Switch 2 serves as the vanguard, but Qualcomm and Samsung see opportunity in white-label solutions for boutique makers. Custom SoC hybrids blur lines: Microsoft’s roadmap incorporates PC-like architectures while retaining proprietary accelerators for secure loading and AI post-processing. The interplay between energy efficiency and graphics throughput will dictate architecture choices for late-decade devices.

By End-User: Institutional Segment Grows Through Esports Expansion

Individual households generated 88% of 2024 revenue, yet esports clubs, schools, and gaming cafés provide a 7.3% CAGR upside. League organizers supply standardized console kits, ensuring parity across tournaments, while educational programs adopt consoles to teach teamwork and design. The gaming console market size for institutions remains modest but strategic: bulk procurement stabilizes quarterly shipments and presents recurring refresh cycles tied to competitive seasons.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Online Growth Reshapes Retail Landscape

Brick-and-mortar outlets claimed 48% of 2024 sales, buoyed by instant pickup and bundled trade-in programs. Online marketplaces grow faster, riding a 6.5% CAGR as free shipping, stock notifications, and digital-only promotions sway purchasing. Nintendo’s “game-key cards” illustrate a hybrid pathway that keeps foot traffic flowing while nudging users toward fully downloadable ecosystems. For hardware, manufacturers experiment with direct-to-consumer portals offering limited-edition colorways or loyalty discounts that bypass intermediary mark-ups.

Geography Analysis

Asia-Pacific led the gaming console market with a 37% share in 2024, sustained by robust gaming cultures and early adoption of 8K displays in Japan and South Korea. Localized content, exemplified by Arabic-language titles in Gulf markets, reveals the importance of cultural adaptation as regional publishers secure licensing deals. North America remains pivotal; the United States alone generated USD 4.9 billion in gaming revenue in March 2024, confirming high spending power and premium attach rates. Europe, meanwhile, balances console growth with a mobile-centric Gen-Z cohort that challenges traditional upgrade cycles.

Latin America gains momentum, paced by Brazil’s May 2024 legal framework that reduces taxes on locally assembled consoles and encourages inward investment. The Middle East & Africa shows the steepest trajectory, logging a 4.8% CAGR to 2030 from a smaller base; Sony’s stake in Carry1st supports distribution and payments infrastructure across sub-Saharan markets. Nigeria’s anticipated 8.6% CAGR in video games and esports testifies to untapped potential where mobile penetration rises faster than fixed-line broadband. Supply-chain strategies now emphasize regional assembly, with Sony producing physical PS5 discs in Brazil to shorten lead times and dodge import tariffs [3]Dean Takahashi, “Brazil passes landmark games law,” GamesBeat, venturebeat.com.

Competitive Landscape

The industry remains oligopolistic, with Sony, Microsoft, and Nintendo accounting for most global unit sales. Sony’s PS5 outsold Xbox by roughly 5:1 in late 2024, leveraging exclusives such as Spider-Man 2 and robust first-party studios. Microsoft counters by broadening Xbox Game Pass to 34 million subscribers and green-lighting select exclusives for rival platforms to monetize dormant IP. Nintendo’s family-friendly franchises and hybrid hardware carve a differentiated niche; 139 million lifetime Switch sales underscore enduring appeal.

Second-tier challengers exploit white-space segments. Valve’s Steam Deck has shipped 4 million units, validating the premium handheld PC form factor. Asus and MSI enter the ring with ARM-based or x86 portable PCs to capture enthusiasts seeking open ecosystems. Strategic moves center on AI partnerships: Sony and AMD’s Project Amethyst aims to embed machine learning accelerators for real-time upscaling and physics, while Microsoft explores cloud-native chiplets that offload compute to Azure. Supply chain jitters push all majors to multisource memory and package substrates, although securing advanced 5 nm capacity remains a zero-sum contest.

Gaming Console Industry Leaders

-

Sony Corporation

-

Microsoft Corporation

-

Nintendo Co. Ltd.

-

Sega Sammy Holdings Inc.

-

Valve Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Nintendo formally unveiled Switch 2, featuring an 8-inch display, magnetic Joy-Cons, and backward compatibility, with launch penciled in for June 2025.

- January 2025: Sony partnered with Carry1st to extend PlayStation distribution and localized content across Africa.

- December 2024: Sony and AMD initiated Project Amethyst to integrate AI-driven graphic enhancements into future PlayStation consoles.

- November 2024: Sony rolled out PlayStation 5 Pro at USD 699.99, adding 67% more GPU compute units and PlayStation Spectral Super Resolution upscaling.

Global Gaming Console Market Report Scope

A gaming console is mainly a specialized electronic device designed for playing video games. It connects to a display, such as a television or a monitor, and uses controllers for user input. Consoles often feature powerful hardware, exclusive games, and multimedia capabilities, offering an immersive entertainment experience.

Gaming Consoles Market Report is segmented by sales channel (online, offline), console type (handheld, home consoles, hybrid), geography (North America [United States, Canada], Europe [Germany, United Kingdom, France, and Rest of Europe], Asia-Pacific [China, Japan, India, and Rest of Asia-Pacific], Latin America [Brazil, Argentina, Rest of Latin America], Middle East and Africa [United Arab Emirates, Saudi Arabia, South Africa, Egypt, Rest of Middle East and Africa]). The market sizes and forecasts are provided in value terms (USD) for all the above segments.

| By Console Type | Home Consoles | ||

| Handheld Consoles | |||

| Hybrid Consoles | |||

| Others (Micro-consoles / TV Boxes) | |||

| By Technology | HD (>1080 p) Consoles | ||

| 4K-capable Consoles | |||

| 8K-ready Consoles | |||

| By Processor Architecture | x86-based Consoles | ||

| ARM-based Consoles | |||

| Custom SoC-based Consoles | |||

| By End-user | Household / Individual | ||

| Commercial Gaming Lounges and Cafes | |||

| Institutional (Esports Clubs, Schools) | |||

| By Distribution Channel | Online Retailers and Marketplaces | ||

| Offline | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

| Home Consoles |

| Handheld Consoles |

| Hybrid Consoles |

| Others (Micro-consoles / TV Boxes) |

| HD (>1080 p) Consoles |

| 4K-capable Consoles |

| 8K-ready Consoles |

| x86-based Consoles |

| ARM-based Consoles |

| Custom SoC-based Consoles |

| Household / Individual |

| Commercial Gaming Lounges and Cafes |

| Institutional (Esports Clubs, Schools) |

| Online Retailers and Marketplaces |

| Offline |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the current value of the gaming console market?

The market is valued at USD 24.24 billion in 2024 and is expected to reach USD 28.85 billion by 2030.

Which region holds the largest gaming console market share?

Asia-Pacific leads with a 37% share in 2024, propelled by strong gaming cultures and early adoption of premium displays.

Which console segment is growing fastest?

Hybrid consoles, blending portable and docked play, are forecast to expand at a 5.9% CAGR between 2025 and 2030.

How are cloud-gaming sticks affecting console demand?

In North America and Western Europe, inexpensive streaming devices substitute entry-level consoles, trimming the forecast CAGR by an estimated 0.8 percentage points.

What role do government incentives play in the market?

Subsidies for locally assembled hardware in Brazil and India lower retail prices and stimulate regional manufacturing, adding roughly 0.4 percentage points to projected CAGR.

Which processor architecture is gaining momentum?

ARM-based designs are set to grow at a 7% CAGR, driven by energy-efficient chips in next-generation hybrid devices and handheld PCs.

Page last updated on: June 22, 2025