Fusion Splicer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 774.23 Million |

| Market Size (2031) | USD 993.12 Million |

| Growth Rate (2026 - 2031) | 5.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fusion Splicer Market Analysis by Mordor Intelligence

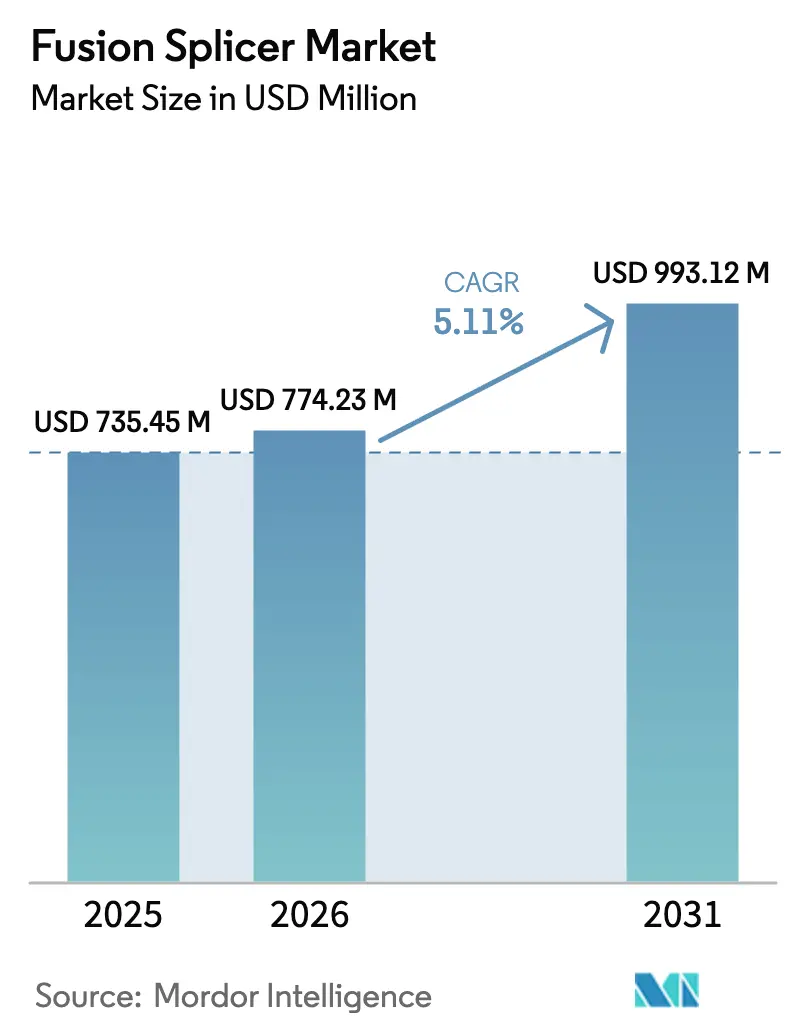

The Fusion Splicer Market size is expected to grow from USD 735.45 million in 2025 to USD 774.23 million in 2026 and is forecast to reach USD 993.12 million by 2031 at 5.11% CAGR over 2026-2031.

Demand is expanding as fiber backhaul for 5G densification, hyperscale data centers, and publicly funded rural broadband programs converge, creating sustained equipment requirements. Contractors are replacing mechanical splicing with automated fusion systems that lower insertion loss and improve long-run network reliability, while telecom operators, cloud providers, and system integrators allocate fresh capital to ribbon splicers that accelerate crew productivity. Competitive dynamics continue to shift as lower-priced Chinese entrants force incumbents to differentiate through AI-enabled alignment algorithms and cloud-linked splice diagnostics. Volatility in electrode raw materials and an aging, undersized technician workforce remain structural concerns for the fusion splicer market.

Key Report Takeaways

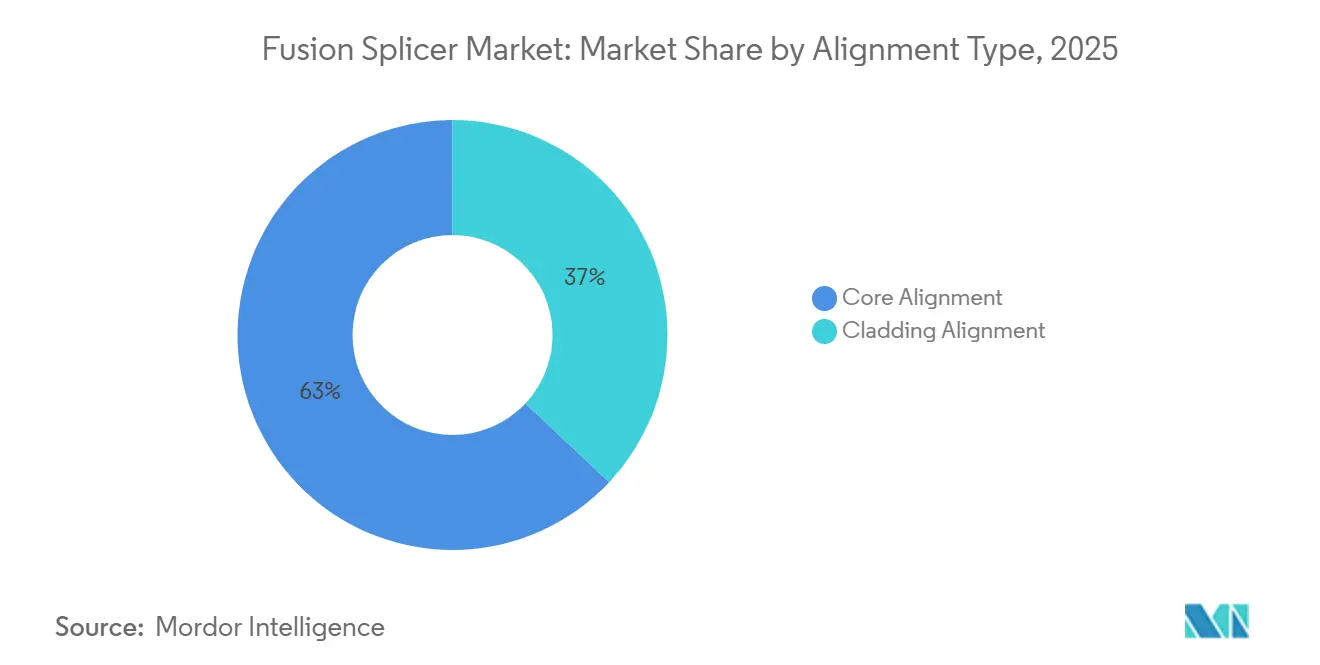

- By alignment type, core alignment held 63% fusion splicer market share in 2025, whereas cladding alignment is projected to record a 5.87% CAGR through 2031.

- By product type, single-fiber units led the fusion splicer market with 58% of the market share in 2025, while ribbon splicers are set to expand at a 6.12% CAGR.

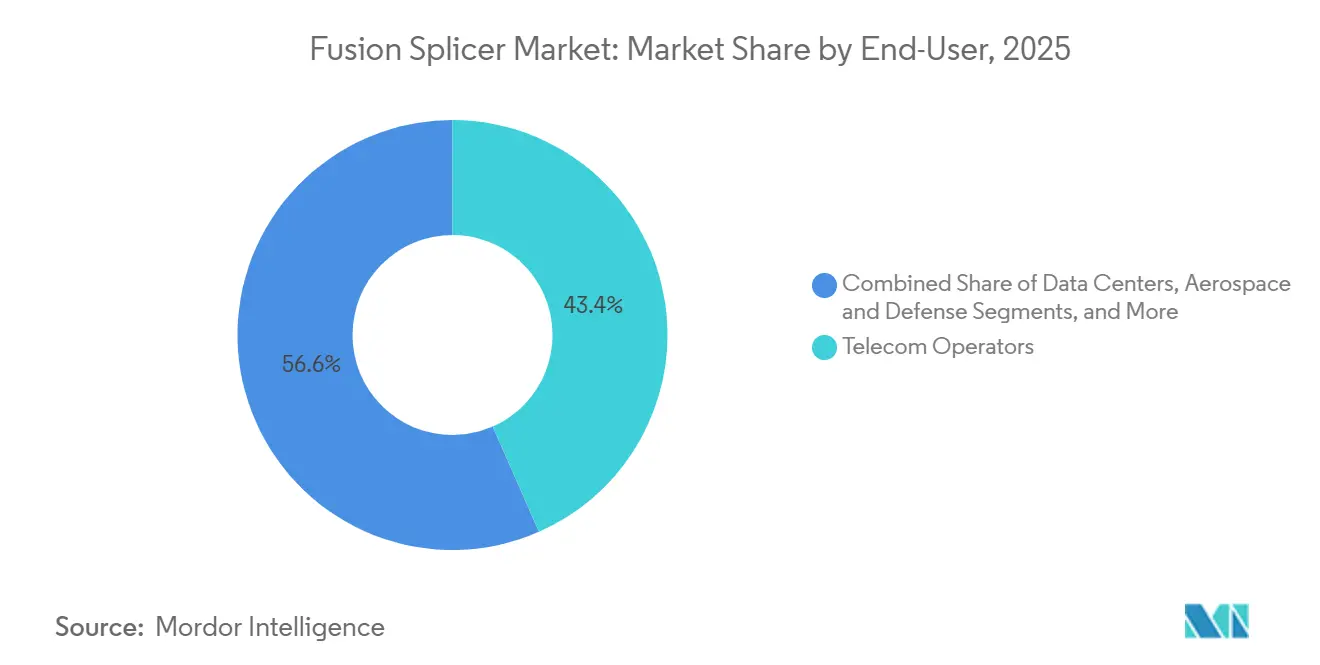

- By end user, telecom operators accounted for 43.4% of 2025 revenue, yet data centers are advancing at a 5.98% CAGR through 2031.

- By application, telecommunications accounted for 56.4% of demand in 2025, and premises networks are expected to rise at a 6.32% CAGR.

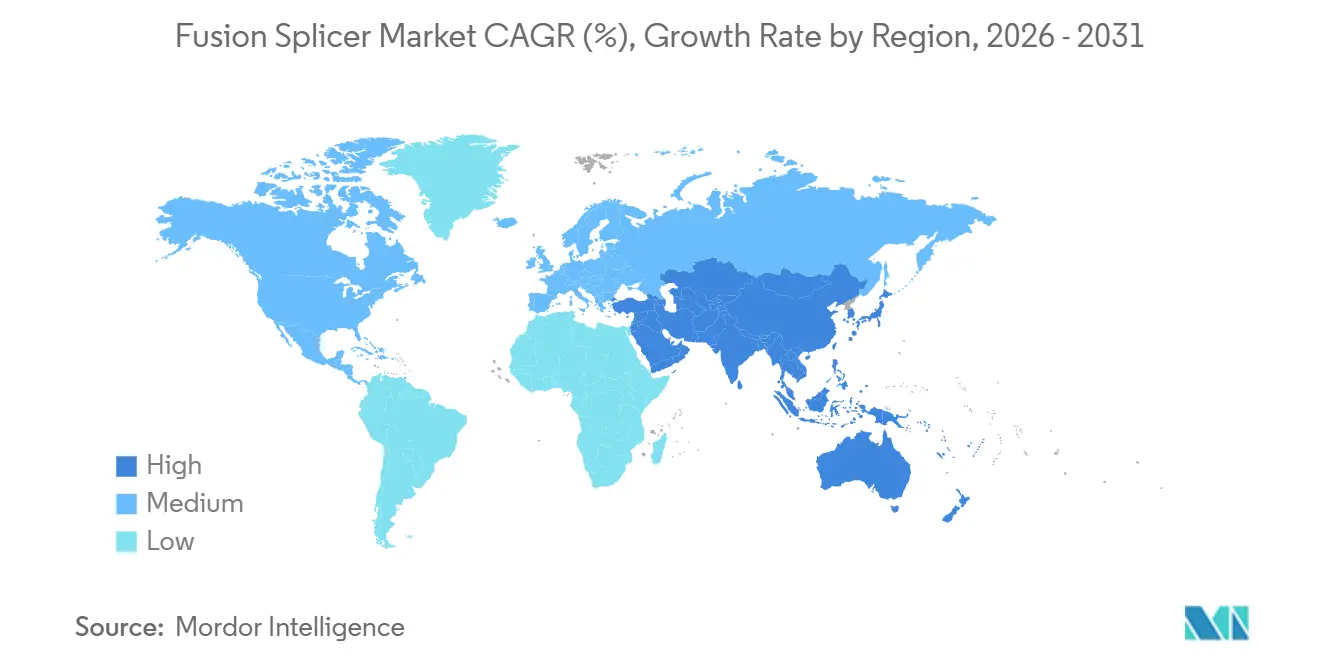

- By geography, Asia-Pacific captured 42.1% of 2025 revenue, and is expected to rise at a 6.78% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fusion Splicer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating 5G Backhaul Fiber Deployment | +1.2% | Global, strong in Asia-Pacific and North America | Medium term (2-4 years) |

| Rising Rural Broadband Funds | +0.9% | North America, India, Southeast Asia | Medium term (2-4 years) |

| Surge in Hyperscale Data Center Construction | +1.4% | North America, Europe, Asia-Pacific core markets | Short term (≤ 2 years) |

| Transition From Mechanical to Automated Fusion Splicing | +0.7% | Global, strong in Asia-Pacific and North America | Long term (≥ 4 years) |

| Adoption of AI-Enabled Self-Aligning Splicers | +0.6% | North America, Europe, Japan | Medium term (2-4 years) |

| Growing Use of Specialty Fibers | +0.3% | North America, Europe, select Asia-Pacific research hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Hyperscale Data Center Construction

Hyperscale operators are adding server capacity at a pace that eclipses traditional enterprise build cycles. Each data hall requires tens of thousands of low-loss fiber terminations, and 400 G to 800 G optical transceivers demand parallel fiber ribbons that magnify splice counts. In 2024 hyperscale capacity grew 18%, underpinned by 120 new facilities that collectively stretched global splice demand. Contractors now specify 12- and 24-fiber ribbon units that cut per-splice time to under 90 seconds, improving labor productivity and ensuring consistent optical performance across high-fiber-count interconnects.

Accelerating 5G Backhaul Fiber Deployment

Mobile operators continue to densify mid-band and millimeter-wave cells, with each small-cell node requiring several dedicated fibers. China plans to install fiber to more than 3 million 5G base stations by 2024, a build that will multiply splice points well beyond legacy macro architectures.[1]China Mobile, “Annual Report 2024,” chinamobileltd.com Portable, battery-driven splicers that withstand aerial and underground conditions are in high demand as field crews race to meet rollout deadlines.

Rising Rural Broadband Funds

Government subsidy programs such as the USD 42.5 billion BEAD initiative in the United States, BharatNet in India, and national rollouts across Southeast Asia mandate fiber-to-the-premises as the default technology. These policies translate directly into new orders for fusion splicers, often in challenging terrain where ribbon models enhance crew efficiency. Contractors that historically focused on wireless or coaxial deployments are ramping up splicer fleets to capture funded projects.[2]U.S. Department of Commerce NTIA, “BEAD Program,” broadbandusa.ntia.doc.gov

Transition From Mechanical to Automated Fusion Splicing

Insertion-loss budgets are tightening as operators push longer reach and higher bandwidth. Fusion splicing typically holds losses below 0.05 dB, well inside IEC 61300-3-4 thresholds. Automated units now use real-time image analytics to self-adjust arc energy and electrode gap, driving uniform results with less technician intervention. The shift lowers consumable costs and accelerates deployment compared to mechanical methods that rely on index-matching gel.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Equipment Costs for Contractors | -0.5% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Shortage of Certified Fiber-Splicing Technicians | -0.8% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Price Pressure From Low-Cost Chinese Entrants | -0.4% | Global, intense in Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Volatility in Rare-Earth Electrode Materials | -0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified Fiber-Splicing Technicians

The United States alone faces a projected deficit of 700,000 qualified fiber technicians through 2029, a gap that prolongs project timelines and inflates labor rates.[3]Fiber Broadband Association, “Workforce Report 2024,” fiberbroadband.org Europe reports similar hiring delays, with vacancies for installers remaining open twice as long as general construction trades. Although AI-enabled units reduce the learning curve, complex ribbon or specialty fiber tasks still require experienced personnel, limiting deployment velocity in rural and remote builds.

High Up-Front Equipment Costs for Contractors

Advanced core-alignment splicers list between USD 15,000 and USD 25,000, capital outlays that deter small regional contractors from bidding on large projects. In emerging markets the barrier is more acute, impeding fusion splicer market penetration despite strong underlying fiber demand. Leasing models and vendor financing are emerging, yet ownership costs remain a hurdle until unit prices decline or project margins expand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Alignment Type: Core Dominance With Specialty Pivot

Core-alignment systems delivered 63% of fusion splicer market revenue in 2025, underscoring their role in long-haul and metro backbones where ultralow loss is mandatory. Precise imaging aligns fiber cores within sub-micron tolerances, holding attenuation to 0.02-0.05 dB. The fusion splicer market size for core-alignment units is projected to stay ahead as telecom operators refresh existing fleets for AI-assisted versions.

Cladding-alignment demand is nevertheless climbing, expanding at a 5.87% CAGR as quantum sensing and aerospace programs rely on non-standard fiber geometries that preclude core-based alignment. Lower equipment prices, typically 15-20% below core units, help contractors address specialty projects without straining budgets. Manufacturers are now introducing hybrid platforms that toggle between modes, ensuring one chassis covers both mainstream and niche requirements.

By Product Type: Ribbon Splicers Gain As Data Centers Scale

Single-fiber models retained 58% of 2025 revenue owing to their versatility across access and enterprise links. Yet ribbon splicers are on a faster 6.12% trajectory because a single 12-fiber splice replaces a dozen sequential terminations, cutting labor time by up to 85%. The fusion splicer market share for ribbon equipment is poised to widen further as 400 G and 800 G transceivers proliferate across hyperscale sites.

Specialty-fiber units occupy a small volume yet command premium pricing, capturing 18% of vendor revenue on just 8% of shipments. Photonic crystal and polarization-maintaining fibers used in defense, quantum, and laser systems drive this niche, and vendors differentiate through programmable arc profiles and extended warranties that align with mission-critical reliability standards.

By End-User: Data Centers Outpace Telecom Growth

Telecom carriers generated 43.4% of fusion splicer market demand in 2025, anchored by 5G backhaul and fiber-to-the-home initiatives. The fusion splicer market size related to telecom will continue to expand, yet its growth rate trails that of hyperscale computing.

Data centers display a 5.98% CAGR through 2031 as cloud operators roll out multi-availability-zone regions and deploy edge facilities for AI inference workloads. Contractors servicing these builds now average more than three splicers per crew, versus barely two units just two years earlier, reflecting the intensity of ribbon work in dense rack environments.

By Application: Premises Growth Reflects Hybrid Work

Telecommunications networks still dominate equipment shipments, holding 56.4% of 2025 use cases. The fusion splicer market size for telecom remains anchored by long-haul capacity upgrades, yet enterprise premises networks are outpacing it, fueled by hybrid work and private 5G adoption.

Premises applications will grow at a 6.32% CAGR, encompassing campus backbones, colocation cross-connects, and cable operators migrating from coax to fiber-deep. Each corporate site typically needs multiple splice points for dual-path redundancy, driving demand for compact units that balance mobility with automated alignment.

Geography Analysis

the Asia-Pacific accounted for 42.1% of 2025 revenue. China’s operators added 65 million new fiber-to-the-home lines in 2024, while India’s BharatNet targets village-level connectivity by 2026. Japan, South Korea, and Singapore focus on 10-gigabit passive optical network upgrades that require low-loss re-splicing at distribution hubs. Emerging Southeast Asian economies such as Indonesia and Vietnam are scaling mobile backhaul, favoring ruggedized portable units for aerial and underground cable runs.

North America is the largest regional market, coupling rural buildouts with relentless data-center additions. BEAD funding ensures multi-year equipment orders from contractors expanding fiber to unserved communities, and hyperscale operators keep ribbon splicer demand elevated around Ashburn, Phoenix, and Columbus clusters. Canada’s Universal Broadband Fund mirrors this pattern, especially in provinces with harsh winters that require durable field hardware.

Europe presents a patchwork. Scandinavia approaches universal fiber penetration, shifting vendor focus to replacement cycles and ribbon upgrades in data centers. Southern and Eastern European markets lag, but EU Digital Decade targets gigabit coverage for all households by 2030, translating into accelerated purchases as national programs unlock grants. The Middle East and Africa trail in absolute volume yet post one of the steepest growth slopes, propelled by smart-city mega-projects in the Gulf and 5G backhaul across select African metros where operators migrate traffic from congested microwave links to fiber.

Competitive Landscape

Global supply is moderately concentrated: Fujikura, Sumitomo Electric, and Furukawa Electric control roughly 55-60% of revenue by pairing optical fiber expertise with broad service footprints. Chinese challengers such as INNO Instrument and Signal Fire disrupt on price and marketing, offering core-alignment models at 30-40% discounts that resonate in budget-sensitive regions. Korean firms Ilsintech and UCL Swift compete on mid-tier pricing and respectable performance metrics, winning share among buyers seeking a balance between cost and reliability.

Software and data increasingly differentiate offers. Leading vendors embed cloud dashboards that capture splice imagery, electrode-wear indicators, and technician performance statistics, turning each device into a service node within a wider ecosystem. Patent activity underscores this shift; Fujikura’s 2024 filing covers machine-learning algorithms that predict electrode fatigue days before failure, enabling scheduled maintenance that minimizes field interruptions. Ribbon splicer innovation continues, with roadmaps calling for sub-60-second, 24-fiber cycles aimed squarely at hyperscale sites.

Barriers to entry persist around optical-component quality control, ISO 9001 certification, and long-term supply agreements with tier-1 carriers. Nonetheless, integrators remain open to multi-vendor fleets when price gaps widen, maintaining competitive tension that puts pressure on incumbents' margins.

Fusion Splicer Industry Leaders

Fujikura Ltd.

Sumitomo Electric Industries, Ltd.

Furukawa Electric Co., Ltd.

INNO Instrument Inc.

Darkhorsechina (Beijing) Telecom Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Fujikura rolled out an AI-enhanced platform that auto-detects fiber type and optimizes arc parameters, cutting setup time by 60%. The unit lists at USD 22,000.

- November 2025: Sumitomo Electric landed a USD 15 million order for 2,000 ribbon splicers supporting a European FTTP build across Germany and France.

- October 2025: INNO Instrument increased South Korean production capacity by 40% to supply AI-ready models for the North American market.

- September 2025: Corning introduced a specialty splicer for quantum communication, priced at USD 45,000 and tuned for sub-micron alignment.

Global Fusion Splicer Market Report Scope

Fusion splicing is the technique of welding or fusing two fibers together by an electric arc. Fusion splicing is the most widely used method of splicing, as it achieves the lowest insertion loss and practically no back reflection. Fusion splicing gives the most stable joint between two fibers. Fusion splicing is performed by an automated machine called a fusion splicer.

The Fusion Splicer Market Report is Segmented by Alignment Type (Core Alignment, Cladding Alignment), Product Type (Single-Fiber, Ribbon-Fiber, Specialty-Fiber), End-User (Telecom Operators, Data Centers, Contractors and System Integrators, Aerospace and Defense), Application (Telecommunications, Cable TV, Premises and Enterprise, Research and Specialty), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

| Core Alignment |

| Cladding Alignment |

| Single-Fiber Fusion Splicer |

| Ribbon-Fiber Fusion Splicer |

| Specialty-Fiber Fusion Splicer |

| Telecom Operators |

| Data Centers |

| Contractors and System Integrators |

| Aerospace and Defense |

| Telecommunications |

| Cable TV |

| Premises and Enterprise |

| Research and Specialty Applications |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Gulf Cooperation Council |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Alignment Type | Core Alignment | |

| Cladding Alignment | ||

| By Product Type | Single-Fiber Fusion Splicer | |

| Ribbon-Fiber Fusion Splicer | ||

| Specialty-Fiber Fusion Splicer | ||

| By End-User | Telecom Operators | |

| Data Centers | ||

| Contractors and System Integrators | ||

| Aerospace and Defense | ||

| By Application | Telecommunications | |

| Cable TV | ||

| Premises and Enterprise | ||

| Research and Specialty Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Gulf Cooperation Council | |

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the fusion splicer market in 2031?

The market is forecast to reach USD 993.12 million by 2031 based on a 5.11% CAGR.

Which segment is growing fastest within the fusion splicer space?

Ribbon splicers are expanding at a 6.12% CAGR as hyperscale data centers adopt parallel fiber architectures.

Why are AI-enabled fusion splicers gaining traction now?

AI models automate fiber identification and arc optimization, cutting setup time and lowering the skill threshold amid a technician shortage.

How does 5G roll-out influence fusion splicer demand?

Dense small-cell backhaul requires substantially more splice points than legacy macro networks, increasing orders for portable, ruggedized units.

Which region currently leads global fusion splicer revenue?

Asia-Pacific currently leads global fusion splicer revenue, captured 42.1% of 2025 revenue, propelled by China's FTTH scale and India's BharatNet program.

What factor most constrains near-term deployment velocity?

A shortage of certified fiber-splicing technicians, particularly in North America and Europe, prolongs project timelines and raises labor costs.

Page last updated on: