Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 181.34 Billion |

| Market Size (2026) | USD 184.59 Billion |

| Market Size (2031) | USD 201.76 Billion |

| Growth Rate (2026 - 2031) | 1.79% CAGR |

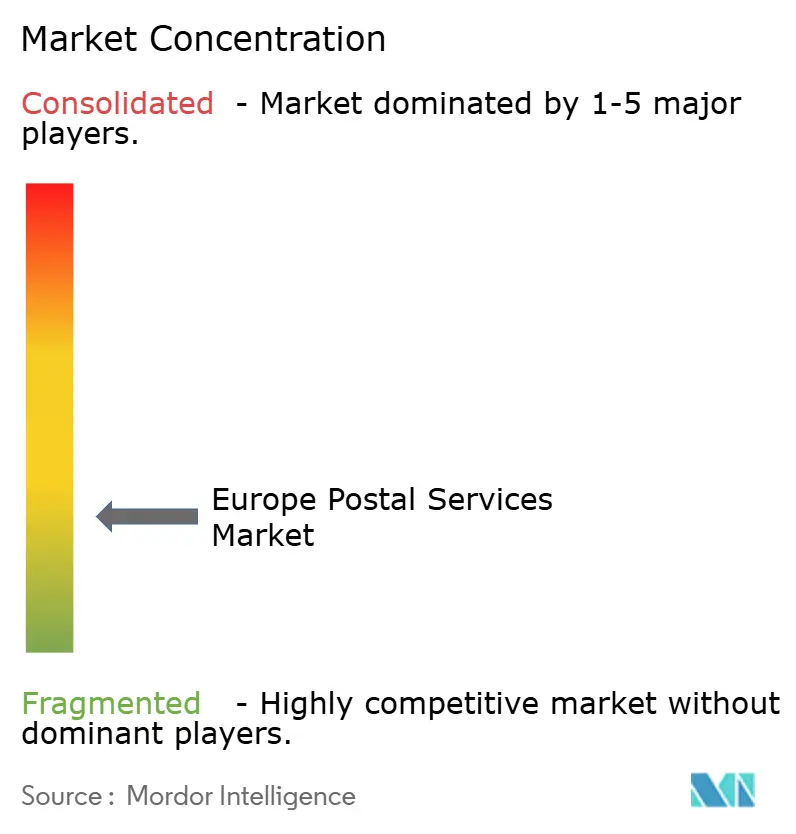

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Postal Services Market Analysis by Mordor Intelligence

Europe Postal Services Market size in 2026 is estimated at USD 184.59 billion, growing from 2025 value of USD 181.34 billion with 2031 projections showing USD 201.76 billion, growing at 1.79% CAGR over 2026-2031.

Underpinning this expansion is the decisive shift toward parcels, revenue and continue to offset the gradual drop in traditional letters. Express postal services, backed by rising demand for same-day and next-day delivery, are on course for the strongest advance at a 7.1 % CAGR, far outpacing the overall market. Germany retains its leadership position with 24 % share on the strength of a dense logistics backbone, while Spain stands out as the fastest-growing national market, tracking 6.1 % annual expansion as e-commerce partnerships deepen. Operators are responding to tighter competition and digital substitution by accelerating automation, broadening service portfolios, and adapting to new regulatory frameworks such as Germany’s revised Postal Act, which seeks to balance universal service with financial sustainability.

Key Report Takeaways

- By service type, Standard Postal Service held 52.35% of the Europe Postal Services market share in 2025, whereas Express Postal Service is forecast to grow at a 6.96 % CAGR through 2031.

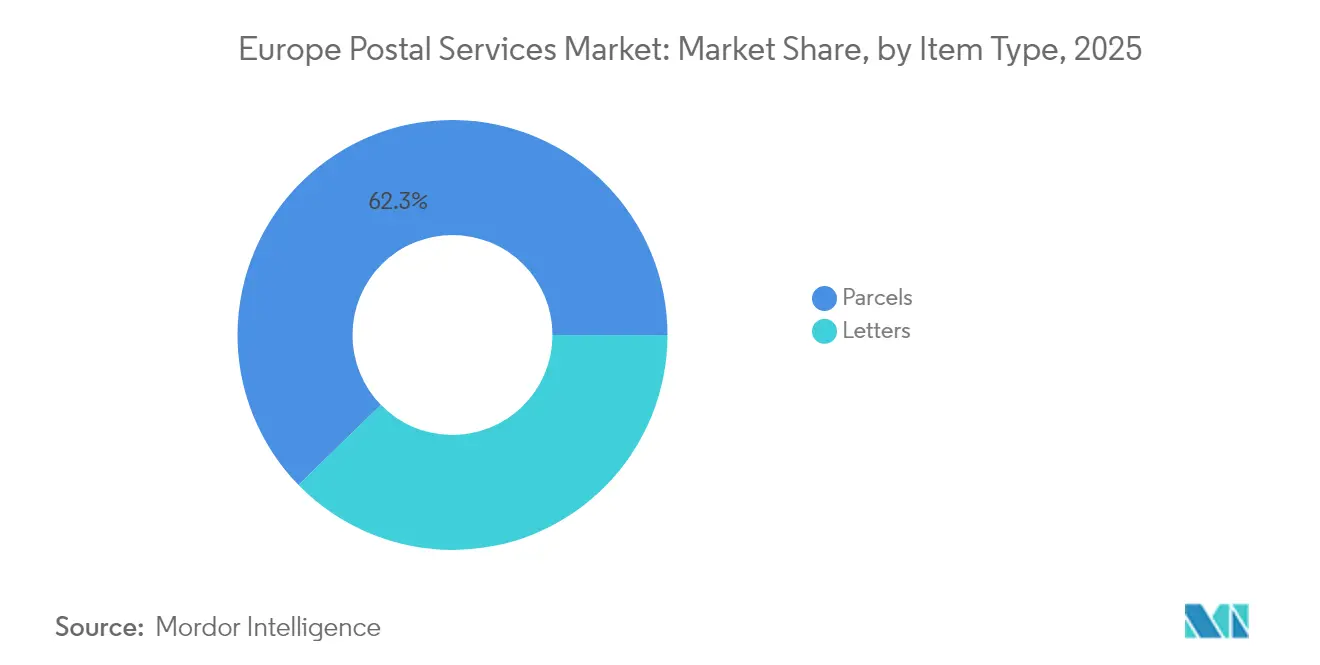

- By item type, Parcels commanded 62.30% of the Europe Postal Services market share in 2025 and are expected to expand at a 6.18% CAGR to 2031.

- By destination, Domestic shipments accounted for 76.45% of the Europe Postal Services market share in 2025, while International shipments are set to register a 6.07% CAGR over 2026-2031.

- By geography, Germany led with a 23.70% of the Europe Postal Services market share in 2025, while Spain is projected to post the fastest growth at a 5.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Postal Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Boom | +1.8% | Germany, UK, France, Spain | Short term (≤ 2 yrs) |

| EU Carbon Regulations | +0.6% | EU-wide | Medium term (3-4 yrs) |

| Cross-Border Single Market Initiatives | +0.5% | Border regions | Medium term (3-4 yrs) |

| Ageing Population | +0.2% | Germany, Italy | Long term (≥ 5 yrs) |

| Same-Day Delivery Expectations | +1.2% | Urban Europe | Short term (≤ 2 yrs) |

| Logistics Automation | +0.7% | Western Europe | Medium term (3-4 yrs) |

| Source: Mordor Intelligence | |||

E-commerce Boom Driving Parcel Volumes in Germany & the UK

Parcel volumes in Germany rose 9 % year-on-year during Q2 2024 even as consumer spending moderated. The United Kingdom echoes this pattern, with e-commerce holding 26 % of retail in 2024 and set to reach 31 % by 2028. This demand imbalance between parcels and letters is producing asymmetric network utilisation that nudges operators to repurpose letter routes for parcel pickups. A fresh inference is that suburban depots originally designed for mail sorting are quietly morphing into parcel micro-fulfilment hubs, unlocking hidden asset productivity.

EU Carbon Regulations Accelerating Fleet Electrification Investments

Stricter emission caps have accelerated electric-vehicle roll-outs, with UPS deploying more than 100 new EVs in Paris and planning 600 across Europe by end-2024 [1]Carter Chase, “New UPS Electric Vehicles Hit The Streets Of Europe,” UPS, about.ups.com. Bpost doubled its electric van fleet, while PostNL logged 82 % emission-free delivery kilometres in 2023. The underlying inference is that early movers can price carbon-neutral delivery at a modest premium, creating a two-tier service catalogue that hedges against regulatory costs.

Cross-Border Single Market Initiatives Simplifying Customs for SMEs

The Centralised Clearance for Import (CCI) system went live on 1 July 2024, allowing declarations in one EU state and physical presentation in another [2]Directorate-General for Taxation and Customs Union, “Centralised Clearance For Import (CCI) Goes Live,” European Commission, taxation-customs.ec.europa.eu. Together with IPC INTERCONNECT™, these changes compress clearance times and lower paperwork for exporters. One emerging inference is that mid-sized postal operators can now bundle customs brokerage with logistics, generating ancillary revenue streams that did not exist under legacy rules.

Ageing Population Sustaining Letter-Mail Demand for Government Correspondence

Citizens aged 65 + already make up 21.3 % of the EU demographic base. Pension and healthcare agencies still rely on paper notices, so postal operators are seeing a slower erosion of letters in regions with older populations. The fresh takeaway is that demographic pockets create natural hedges against digital substitution, enabling operators to cross-subsidise rural deliveries with stable government mail contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining Letter Volumes | –1.1% | Nordics | Short term (≤ 2 yrs) |

| High Labor Costs & Unionization | –0.7% | Western Europe | Medium term (3-4 yrs) |

| Urban Congestion | –0.5% | Major cities | Medium term (3-4 yrs) |

| Digital Substitutes | –0.9% | EU-wide | Short term (≤ 2 yrs) |

| Source: Mordor Intelligence | |||

Declining Traditional Letter Volumes in Nordic Region

PostNord notes that 76 % of Nordic consumers now purchase cross-border online, diverting attention from domestic mail services. Letter declines accelerate cost-to-serve, forcing operators to trim headcount; Posti’s recent layoffs confirm this restructuring path. The inference is that the Nordic region may pioneer hybrid public-private funding models to keep universal service afloat.

High Labor Costs & Unionization in Western Europe

A one-day strike in Germany during March 2025 illustrates wage tension in heavily unionised markets. Operators respond by accelerating robotics and route optimisation. An immediate inference is that labor volatility indirectly drives technology adoption curves upward, shortening the payback horizon for automation projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Service Type: Express Services Outpace Standard Offerings

Express services hold a Europe Postal Services market size that is forecast to expand at 6.96 % CAGR from 2026-2031, significantly faster than standard services, which still command 52.35 % market share in 2025. The widening spread highlights how premium time-definite products monetise consumer willingness to pay for speed. A current inference is that network design is pivoting toward later collection cut-offs and earlier morning delivery waves, squeezing utilisation out of existing fleets.

Standard services, although lower growth, remain indispensable for regulatory service obligations and nationwide coverage. Germany’s revised Postal Act extends permissible delivery time to three business days for 95 % of letters starting 2025, freeing operators to batch deliveries. This regulatory slack implies that standard services will increasingly serve as the cost-optimised backbone, while express layers generate surplus cash.

Item Type: Parcels Dominate Future Growth Landscape

Parcels represent 62.30% Europe Postal Services market share in 2025 and are projected to post 6.18 % CAGR through 2031. DHL’s 9 % year-on-year parcel growth in Germany validates continued outperformance. The inference here is that sustained parcel growth presses operators to standardise packaging and labelling requirements, shaving micro-delays in sortation.

Letters continue a structural downtrend with a 6 % decline logged in Q2 2024. Yet critical government communication and legal correspondence keep this segment relevant. A fresh inference is that digital identity services embedded within registered letters could reposition the category as a trust-anchored channel rather than a volume play.

Destination: International Shipments Accelerate

International services are forecast to grow at 6.07 % CAGR versus domestic’s larger but slower 76.45 % share base. The CCI clearance model materially trims cross-border friction. The emergent inference is that SMEs now perceive postal operators as integrated trade facilitators, not merely carriers, boosting loyalty in a previously price-sensitive cohort.

Domestic networks remain crucial for last-mile density, with 94 % of online sellers in Spain offering out-of-home options through parcel lockers. InPost’s November 2024 expansion into eight EU markets demonstrates convergence of domestic locker infrastructure with international flows. The fresh implication is that the boundary between domestic and international sortation nodes will blur as consolidated facilities handle both streams seamlessly.

Geography Analysis

Germany retains 23.70 % Europe Postal Services market share in 2025, supported by robust logistics infrastructure and central geography. Although e-commerce volumes dipped in value terms during early 2024, parcel counts still climbed, reinforcing the principle that unit volume growth can offset softer ticket sizes. The new Postal Act’s requirement for 12,000 outlets also hints that bricks-and-mortar access remains politically non-negotiable, anchoring service ubiquity even as digital substitutes proliferate. A key inference is that Germany’s slower letter speed mandate may let operators redeploy labor from evening sortation to early-morning parcel waves, raising asset turns without raising headcount.

Spain posts the region’s fastest forecast CAGR at 5.97 %. Government digital-transformation strategy and a resilient consumer economy feed this trajectory. Correos aims to lift logistics revenue share from 25 % to 40 % by 2024, signalling a decisive parcel pivot. Temu’s partnership with Correos in March 2025 to secure full national coverage illustrates how platform alliances rapidly amplify parcel volume. One inference is that Spain could leapfrog into parcel-first workflow designs, sidestepping legacy letter optimisation stages many peers still manage.

The United Kingdom, France, and Italy each hold meaningful slices of the Europe Postal Services market size. British policy debate on trimming Saturday letter deliveries mirrors continental precedents, signalling a gradual convergence of universal service scopes. Meanwhile, a London-Glasgow parcel train operating at 100 mph exemplifies how rail decarbonisation can carve new express corridors. The inference is that carbon-efficient rail freight could emerge as an alternative to intra-national airlift, offering express reliability with lower emissions.

Competitive Landscape

Deutsche Post DHL Group leads Europe Postal Services industry revenue at EUR 81.76 billion in 2023, with Europe contributing EUR 45.35 billion and an estimated 40 % German parcel market share [3]Agnes Putri, “PowerPoint Presentation,” DHL Group, group.dhl.com. La Poste Groupe, Royal Mail, and Poste Italiane follow, each pursuing diversification into banking or digital trust services. A salient inference is that postal incumbents increasingly treat data security as a service in its own right, evident in Swiss Post’s purchase of cybersecurity firm Open Systems.

White-space opportunities abound in sustainability-themed delivery; 66 % of consumers are willing to pay more for eco-friendly shipping. PostNL’s 82 % emission-free mileage showcases first-mover leverage, while DPD Portugal’s EUR 30 million hub signals scale bets on e-commerce. The inference here is that carbon reporting transparency becomes a differentiator as corporate shippers embed Scope 3 emissions into procurement scorecards.

Emerging disruptors such as InPost exploit parcel locker density and asset-light cross-border models. Acquiring Mondial Relay for EUR 513 million and full control of Menzies Distribution extends its reach into France, Benelux, and the UK. An inference is that locker ecosystems could disintermediate home delivery in dense urban zones, freeing capacity for rural last-mile routes where lockers are less viable.

Europe Postal Services Industry Leaders

Deutsche Post DHL

La Poste

Royal Mail

PostNL

FedEx/TNT Express

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: InPost acquired Mondial Relay for EUR 513 million, creating the largest e-commerce delivery platform in Europe, broadening its footprint in France, the Benelux region and the Iberian Peninsula, and targeting a medium-term EBITDA uplift of EUR 100-150 million.

- September 2024: Swiss Post agreed to acquire cybersecurity specialist Open Systems, a move that will strengthen its secure digital-communication offerings for public authorities and private companies.

- September 2024: DHL Group unveiled its Strategy 2030, targeting 50 % revenue growth by 2030 and prioritizing investment in high-growth areas such as Life Sciences, New Energy and E-commerce.

- June 2024: La Poste Groupe, through GeoPost, expanded its cross-border Out-of-Home delivery network to 28 European countries, further enhancing international parcel coverage.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the European postal services market as all revenue earned from the clearing, sorting, routing, and final-mile delivery of letters, packets, and parcels handled by licensed universal service operators or private carriers across EU-27, the United Kingdom, and EFTA nations. Services counted span standard mail, express mail, parcel lockers, and ancillary tracking or customs brokerage sold under a postal tariff.

Scope Exclusion. We do not include in-house corporate courier fleets, standalone third-party logistics contracts, or financial products such as postal banking.

Segmentation Overview

- By Service Type

- Express Postal Service

- Standard Postal Service

- By Item Type

- Letters

- Parcels

- By Destination

- Domestic

- International

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Nordics (Sweden, Denmark, Norway, Finland)

- Rest of Europe (incl. Eastern Europe & Balkans)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed senior planners at national posts, parcel locker vendors, and bulk mailers across five leading economies, then surveyed small e-retailers in Poland and Spain. These conversations validated service pricing ladders, the real cost of universal service obligations, and appetite for greener last-mile fleets.

Desk Research

We began with Eurostat postal datasets, Universal Postal Union annual statistics, and country regulator filings such as Ofcom and BNetzA, which clarify volume shifts and tariff ceilings. Trade association briefings from PostEurop, e-commerce penetration data from the EU Digital Economy and Society Index, and import-export shipment records drawn from Volza shaped baseline traffic flows. Company 10-Ks, investor decks, and press releases supplied recent parcel mix and automation milestones. D&B Hoovers and Dow Jones Factiva provided cross-checks on operator revenue. The sources cited above are illustrative; many additional references fed our evidence pool.

Market-Sizing & Forecasting

A top-down reconstruction combines 2024 letter and parcel volume from regulators with weighted average postage and parcel tariffs to yield 2024 market value. Results are corroborated through selective bottom-up checks, sampled operator revenue roll-ups and average selling price times volume in Germany, France, and the Nordics, before adjustments. Key variables in the model include letter-mail decline rate, parcel volume per capita, domestic versus cross-border share, e-commerce retail penetration, average postage tariff index, and electric-van total cost of ownership. Forecasts to 2030 rely on multivariate regression where e-commerce growth, GDP per capita, and tariff trajectories explain over 85 percent of variance, supported by scenario vetting with interviewees. Data gaps in smaller markets are bridged by applying proxy parcel intensity ratios from demographically similar states.

Data Validation & Update Cycle

Outputs pass a three-step analyst review that flags anomalies against independent indicators such as fuel price trends or airport cargo throughput. We refresh every twelve months, with interim updates triggered by material tariff changes or mergers. A final sense-check is performed before report delivery, ensuring clients receive the latest view.

Why Mordor's Europe Postal Services Baseline Commands Reliability

Published estimates often differ because firms pick contrasting service scopes, exchange rates, and refresh cadences.

Key gap drivers include varying inclusion of universal-service subsidy revenue, different parcel weight cut-offs, currency conversion timing, and whether forecast models capture the sharp 6 percent annual letter decline that our interviews confirmed.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 181.34 B (2025) | Mordor Intelligence | - |

| USD 58.20 B (2023) | Regional Consultancy A | Narrow scope limited to five Western economies and excludes express parcels |

| USD 98.50 B (2024) | Global Consultancy B | Uses average parcel tariff that omits fuel surcharges and relies on 2022 e-commerce ratios |

| USD 165 B (2023) | Trade Journal C | Converts local currencies at fixed 2021 rates and assumes flat letter volume |

These comparisons show that our disciplined variable selection, annual refresh, and two-layer validation give decision-makers a balanced, transparent baseline they can trace and replicate with confidence.

Key Questions Answered in the Report

What is the current Europe Postal Services market size?

The market is valued at USD 184.59 billion in 2026.

How fast is the Europe Postal Services industry expected to grow?

It is projected to grow at a 1.79 % CAGR between 2026 and 2031.

Which segment is growing the quickest?

Express postal services, with an expected 6.96 % CAGR through 2031, are expanding the fastest.

Why are parcels dominating Europe Postal Services market share?

Structural e-commerce growth and consumer demand for fast deliveries push parcel volumes, already representing 62.30 % of market revenues.

How are postal operators addressing carbon regulations?

Companies are electrifying fleets, investing in emission-free delivery infrastructure, and offering carbon-neutral shipping options to meet EU targets.

What role do cross-border initiatives play in market growth?

Systems like Centralised Clearance for Import simplify customs, lowering barriers for SMEs and accelerating international parcel traffic across the region.

Page last updated on: