Freeze Drying Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

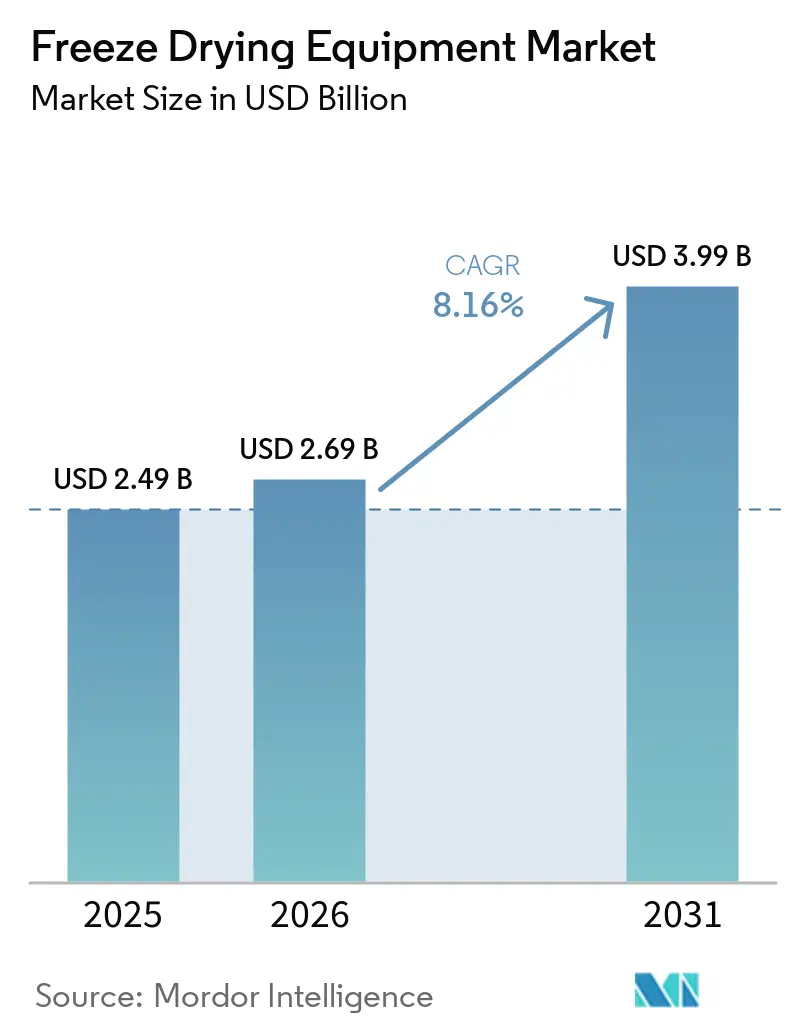

| Market Size (2026) | USD 2.69 Billion |

| Market Size (2031) | USD 3.99 Billion |

| Growth Rate (2026 - 2031) | 8.16% CAGR |

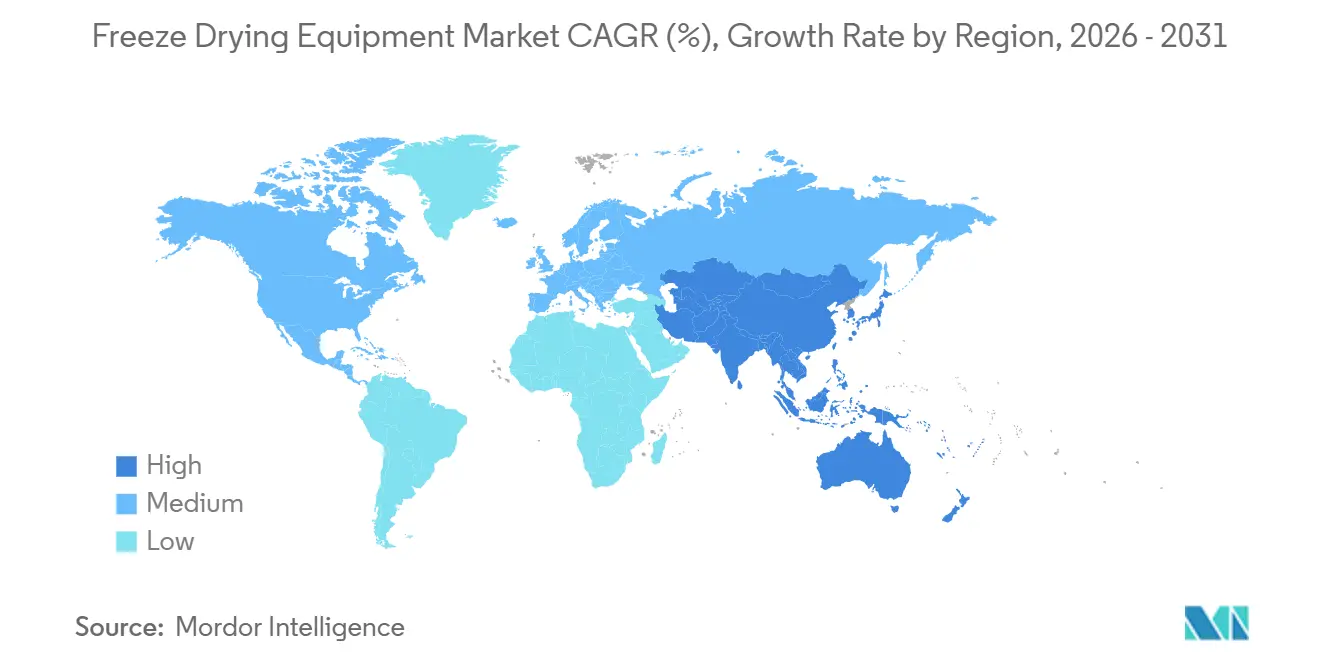

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Freeze Drying Equipment Market Analysis by Mordor Intelligence

The Freeze Drying Equipment Market size was valued at USD 2.49 billion in 2025 and is estimated to grow from USD 2.69 billion in 2026 to reach USD 3.99 billion by 2031, at a CAGR of 8.16% during the forecast period (2026-2031).

Pharmaceutical manufacturing is witnessing a shift in product mix, with biologics now accounting for a significant share of drug development. These products require preservation methods to protect heat-sensitive formulations. The growing focus on complex injectable therapies, including monoclonal antibodies, cell therapies, and advanced vaccine formats, is driving demand for lyophilization capacity across regulated manufacturing networks. The freeze drying equipment market is also influenced by stricter sterility standards, rapid automation adoption, and energy-efficient retrofits that reduce utility consumption without disrupting validated production.

Key Report Takeaways

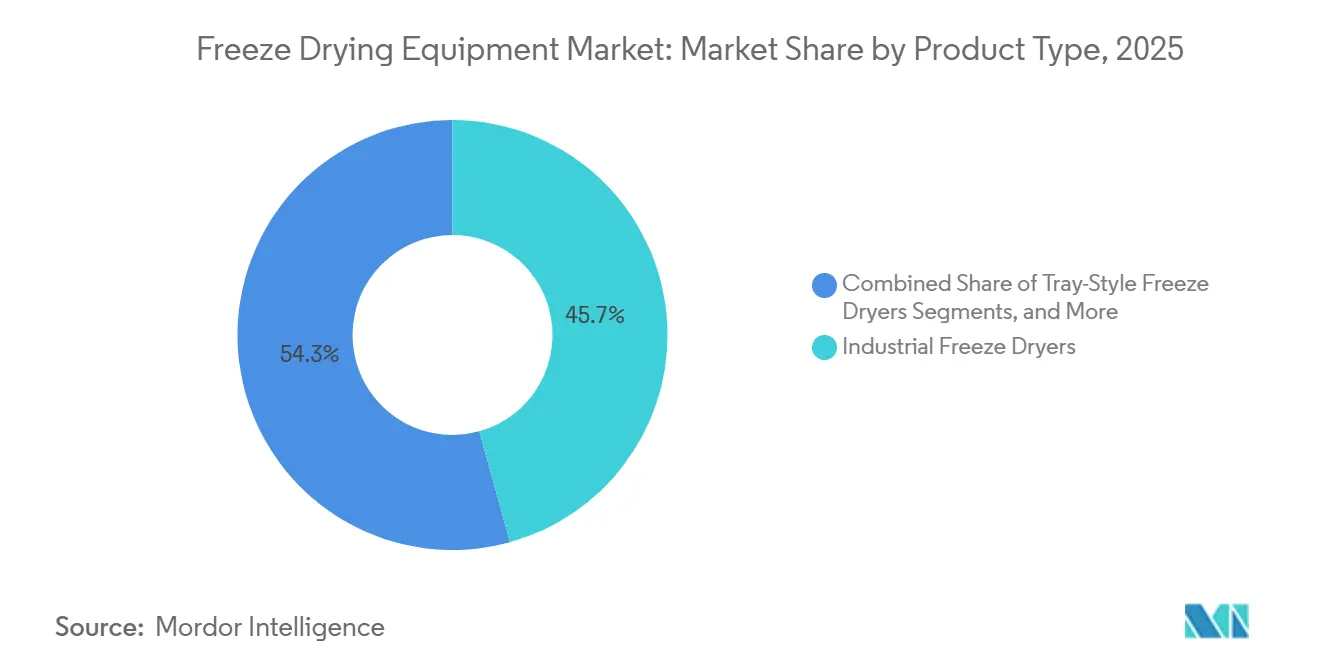

- By product type, industrial freeze dryers held 45.67% of the freeze drying equipment market share in 2025, while tray-style freeze dryers are forecasted to grow at a 10.10% CAGR through 2031.

- By scale of operation, industrial-scale systems accounted for 48.34% share of the freeze drying equipment market size in 2025, while laboratory-scale equipment is projected to expand at a 9.56% CAGR through 2031.

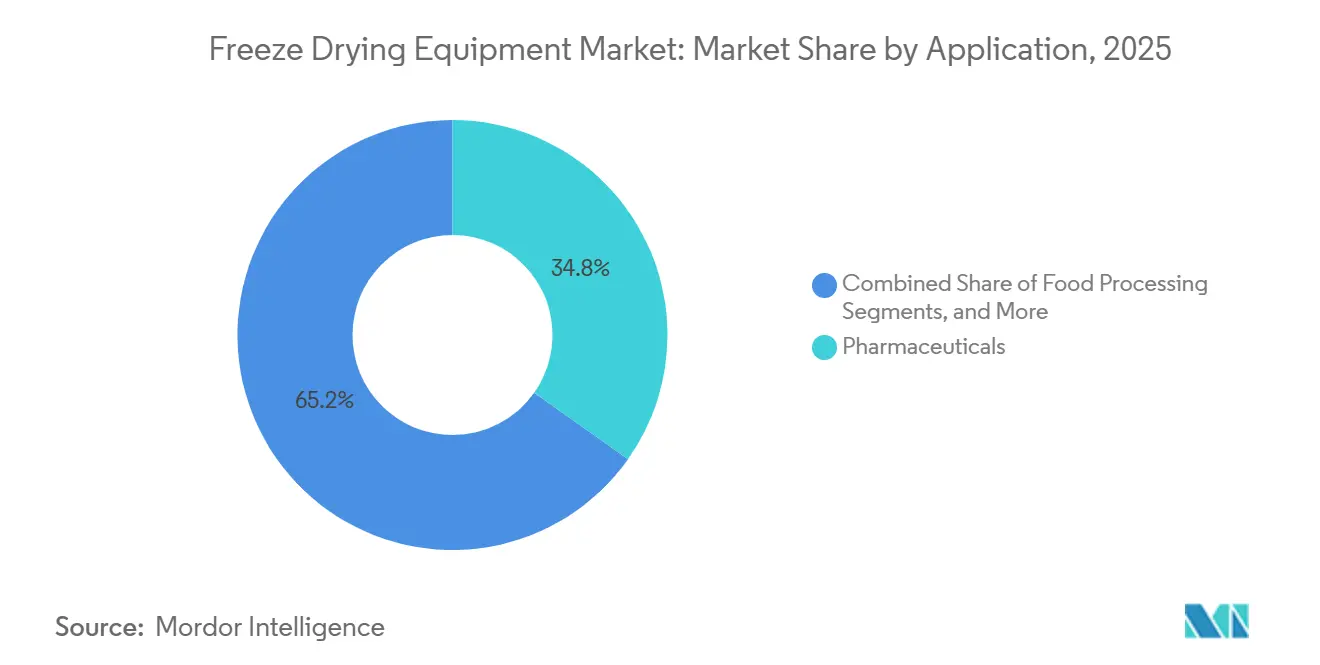

- By application, pharmaceuticals captured 34.77% share of the freeze drying equipment market size in 2025, while food processing is projected to grow at a 10.55% CAGR through 2031.

- By geography, North America held 39.25% of the global market in 2025, while Asia-Pacific is projected to record the highest regional CAGR of 11.20% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Freeze Drying Equipment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising biologics, vaccines, and injectable manufacturing | +2.5% | Global, concentrated in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Expanding freeze-dried food demand across premium and functional segments | +1.4% | Global, strongest in North America, Europe, and Asia-Pacific urban centers | Medium term (2-4 years) |

| Energy-efficient and low-carbon freeze drying retrofits | +0.6% | Europe core, with spillover to North America and Asia-Pacific | Long term (≥ 4 years) |

| Automation, IoT, and PAT adoption in lyophilization systems | +0.8% | North America and Europe, with early-stage adoption in Asia-Pacific | Medium term (2-4 years) |

| Cold-chain fragility and cargo disruption risk | +0.5% | Global, with stronger impact in Middle East and Africa and Latin America | Short term (≤ 2 years) |

| Sterility assurance pressure from annex 1 and aseptic manufacturing norms | +0.7% | Europe and North America, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Biologics, Vaccines, and Injectable Manufacturing

Pharmaceutical manufacturers are increasingly prioritizing spending on equipment for biologics, vaccines, and injectable therapies. These products, sensitive to heat, moisture, and storage conditions, underscore the importance of lyophilization in ensuring stability during sterile manufacturing. Consequently, as the output of injectables rises, so does the demand for pharmaceutical-grade systems in the freeze-drying equipment market. This is particularly true for facilities handling regulated products and export programs. Manufacturers face heightened pressure to ensure validated cycle reproducibility, contamination control, and support for intricate fill-finish workflows, all while maintaining product quality.

Sterility Assurance Pressure from Annex 1 and Aseptic Manufacturing

The updated European Union GMP Annex 1 has catalyzed a compliance-driven overhaul of older lyophilization systems. Effective August 2024, the binding lyophilization section heightened operational demands on manually loaded systems lacking advanced contamination controls, as highlighted by JUBILANT HOLLISTERSTIER.[1]AAPS Open, “Recent Trends in Pharmaceutical Freeze-Drying and Control Strategies Observed in Human Drug Applications and Manufacturing Inspections,” AAPS Open, link.springer.com The framework advocates for isolators, restricted access barrier systems, and robust contamination control strategies, nudging buyers towards modern platforms over mere maintenance of legacy systems. Health Canada's alignment with Annex 1 amplifies this regulatory pressure, extending its reach beyond the EU and into another significant pharmaceutical market.

Automation, IoT, and PAT Adoption in Lyophilization Systems

Automation and digital monitoring are becoming critical in lyophilization due to its complexity. AAPS Open's review of 162 FDA submissions from 2020 to 2023 revealed that PAT tools were used in only 4.17% of NDAs and 0.85% of ANDAs at the commercial stage, indicating significant room for improvement.[2]IMA Group, “IMA Life to Present AI, Soft PAT, and Digital Twin Innovations at Two Key Events in April 2026,” IMA Group, imagroup.com Additionally, over 37% of ANDAs relied on trial-and-error cycle development, prolonging development time and increasing transfer risks. In April 2026, IMA Life introduced AI, soft PAT, and digital twin tools to enhance freeze-drying cycle control. Quartic AI reported a 15% reduction in drying cycle time and a 23% decrease in energy consumption, driving interest in analytics-driven systems. These advancements are steering the freeze-drying equipment market towards automation-led specifications, especially for producers seeking enhanced throughput and batch control.

Expanding Freeze-Dried Food Demand Across Premium and Functional Segments

Freeze-dried products, once limited to emergency supplies, are now gaining mainstream acceptance. Consumers associate these products with premium quality, nutrient retention, and convenient storage, attracting mainstream manufacturers. This shift is driving demand for food-grade batch systems with high throughput and hygienic design. GEA addressed this trend with the RAY Plus series launched in October 2024, featuring reduced energy consumption and enhanced hygiene. The launch also reflects a move towards versatile systems capable of handling various cabinet sizes and production profiles. Nutraceutical and functional food producers are further fueling demand as their product claims increasingly rely on process-controlled drying systems.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High upfront capital cost versus conventional drying technologies | -1.2% | Global, most acute in Asia-Pacific and Middle East and Africa where CMOs face capital constraints | Medium term (2-4 years) |

| Long cycle times constraining throughput and installation flexibility | -0.6% | Global, more pronounced for multi-product pharmaceutical sites | Medium term (2-4 years) |

| Energy intensity and utility load requirements | -0.5% | Europe and North America, where carbon pricing and utility costs are higher | Long term (≥ 4 years) |

| Skilled operator and validation burden for complex multiproduct operations | -0.4% | Global, with stronger effect in lower-cost markets expanding into regulated biologics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Cost Versus Conventional Drying

Capital costs remain a significant barrier for first-time buyers, particularly contract manufacturers comparing lyophilization with lower-cost drying technologies. Production-scale pharmaceutical systems involve high acquisition expenses, which increase further with the addition of CIP and SIP infrastructure, clean utilities, containment features, and barrier technologies. These costs extend payback periods and make them sensitive to financing conditions, customer visibility, and plant utilization assumptions. Smaller CDMOs in India and Southeast Asia prefer modular or scaled-down installations when entering the freeze-drying equipment market, avoiding large integrated lines. This creates distinct demand tiers between high-capex pharmaceutical installations and cautious buyers still gaining experience in freeze-drying operations.

Energy Intensity and Utility Load Requirements

Energy consumption remains a structural challenge in freeze-drying, as primary drying under vacuum requires continuous condenser operation and precise shelf temperature control over cycles often exceeding 24 hours. This high operating cost can weaken the business case in applications with lower product value or high electricity prices. A validated protocol reduced primary drying time by 26% through model-based cycle design, significantly improving cost efficiency and environmental performance. GEA reported a 21.1% reduction in electricity use over a 46.55-hour production cycle with its retrofittable LYOVAC ECO mode, validated under DIN EN ISO 14021:2021-10. Energy performance is becoming a critical procurement factor in the freeze-drying equipment market, particularly in Europe and North America, where it is now prioritized over secondary engineering preferences.[3]GEA Group, “Launches New Freeze Dryer Series for Food Application,” GEA Group, presseportal.de

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Industrial Systems Lead, Tray-Style Gains Momentum on Versatility

In 2025, industrial freeze dryers captured 45.67% of the market, emphasizing their critical role in large-scale pharmaceutical and food operations that demand high throughput and consistent cycles. These systems are ideal for fixed product portfolios, aseptic lines, and facilities requiring Annex 1 compliance, driving demand for isolator-integrated setups. Tray-style freeze dryers, projected to grow at a 10.10% CAGR through 2031, are gaining popularity in multi-product sites and contract manufacturing environments due to their flexibility.

Rotary freeze dryers are preferred for bulk powder applications, utilizing continuous tumbling to improve morphology and accelerate drying compared to shelf-based methods. General-purpose systems are increasingly adopted in nutraceutical and specialty chemical processing, attracting first-time users who do not require fully validated pharmaceutical configurations. In May 2026, IMA Life launched the F57 EVO COMPACT freeze dryer, targeting manufacturers seeking production-grade performance in a compact design. GEA expanded the premium segment in February 2026 with its ALUS automatic loading and unloading systems, designed to minimize manual intervention and enhance contamination control in Annex 1-sensitive environments. These advancements indicate a market shift toward integrated solutions that combine loading, drying, and unloading.

By Scale of Operation: Industrial Dominance Masks Faster Laboratory Growth

In 2025, industrial-scale operations accounted for 48.34% of the market, driven by pharmaceutical plants and large food processing contracts that spread equipment costs over extended production cycles. This segment faces significant regulatory scrutiny, as pharmaceutical users must document sterilization, aseptic handling, and process consistency under strict cGMP standards. While industrial systems dominate revenue, buyers increasingly demand better automation, reduced energy consumption, and faster batch turnarounds. Laboratory-scale equipment is projected to grow at a 9.56% CAGR through 2031, supported by rising biopharmaceutical research investments and early-stage formulation capabilities in biotechnology firms. Compact and programmable systems remain vital for clinical material preparation, formulation screening, and product stability work in private and academic laboratories.

Pilot-scale systems bridge laboratory development and commercial transfer, supporting process validation as biologics and specialty injectables move toward market supply. Scale-up risks persist, as cycle behaviors can vary significantly between small development batches and larger production runs. Digital modeling, process simulation, and transfer tools are increasingly adopted to streamline transitions between lab, pilot, and commercial stages, reducing redevelopment efforts.

By Application: Pharma Leads, Food Processing Closes the Gap

Pharmaceuticals held a 34.77% market share in 2025, driven by the reliance on lyophilization for biologics, vaccines, and parenteral formulations. Regulatory-driven replacement demand further supports this segment, as compliance mandates prompt upgrades or removals of older installations in sterile manufacturing sites. CDMOs play a key role in procurement, benefiting from the expansion of outsourced fill-finish and lyophilized injectable programs across regulated and emerging markets. Biotechnology's role within pharmaceuticals is growing as protein and nucleotide-based therapies advance to clinical and commercial stages. Surgical and specialty medical applications, such as freeze-dried plasma and tissue-related products, remain smaller in volume but are attractive due to their reliance on room-temperature stability and preservation performance.

Food processing is forecast to grow at a 10.55% CAGR through 2031, making it the fastest-growing application in the freeze drying equipment market. This growth is driven by increased adoption among food manufacturers for premium fruits, functional ingredients, and ready-to-eat meal components. Nutraceutical producers are also expanding their use of freeze-drying for probiotics, botanical extracts, and sensitive proteins where heat exposure can compromise quality. Other applications, including diagnostics, industrial enzymes, and selected chemical compounds, provide a steady demand base, diversifying the market beyond its pharmaceutical core.

Geography Analysis

In 2025, North America accounted for 39.25% of the global freeze-drying equipment market, driven by a strong pharmaceutical manufacturing base, an extensive CDMO network, and stringent regulatory oversight. The U.S. remains the primary demand center, with sterile manufacturing sites expanding capacity and replacing older systems with automated, compliant alternatives. Biologics development further sustains demand for validated pharmaceutical lyophilizers among innovators and contract producers. In January 2026, IMA Life partnered with Sharp Sterile Manufacturing on a USD 28 million expansion in Lee, Massachusetts, featuring a fully automated isolated filling line and a high-performance lyophilizer to double site filling capacity. In Canada, Annex 1-aligned guidance is driving replacement demand by raising expectations for contamination control and aseptic processing.

Europe combines regulatory-driven replacement demand with a strong OEM manufacturing base, maintaining its importance in the freeze-drying equipment market. Germany leads the region with large pharmaceutical manufacturing operations and key equipment suppliers. In February 2026, GEA opened its pharmaceutical freeze-drying technology center in Elsdorf, investing over EUR 80 million (approximately USD 85 million) to expand R&D, production, and service capabilities. In March 2026, LYOCONTRACT and Syntegon initiated a EUR 50 million (approximately USD 53 million) expansion of a freeze-drying facility in Ilsenburg, Germany, with a new vial line expected by summer 2027.

Asia-Pacific is projected to grow at an 11.20% CAGR through 2031, making it the fastest-growing regional market. China is increasing procurement at biologics facilities by aligning with international regulatory standards and building export-ready capacity. India is gaining traction with CDMO expansions, sterile dosage growth, and supportive policies driving demand for pharmaceutical-grade installations. Japan and South Korea contribute through advanced pharmaceutical and food processing sectors, emphasizing precision systems and process control. The Middle East, Africa, and South America, while smaller in demand, are strategically important as local vaccine manufacturing and reduced cold-chain dependency boost interest in domestic lyophilization capabilities.

Competitive Landscape

The freeze drying equipment market is moderately concentrated, with GEA Group, IMA Group (via IMA Life), Thermo Fisher Scientific, SP Scientific LLC, and Syntegon Telstar holding strong positions in pharmaceutical-grade systems. Competition is driven by product reliability, aseptic integration, automation depth, service reach, and the ability to support customers through validation-heavy projects rather than equipment price alone. A major strategic development occurred in October 2024 when Syntegon acquired Telstar from Azbil, expanding its offerings to include fill-finish equipment, isolator systems, freeze-dryers, and loading/unloading systems.

IMA has responded by expanding its portfolio and enhancing its digital capabilities. In February 2026, the company acquired a majority stake in ProSys Sampling Systems to strengthen its aseptic and containment offerings for biopharmaceutical manufacturing. Additionally, IMA has emphasized advancements such as AI, soft PAT, digital twins, and cognitive manufacturing to support predictive process control and faster cycle development. GEA is differentiating itself by combining automation with validated sustainability claims, focusing on compliance and operational efficiency.

Chinese suppliers like Tofflon Science and Technology Group remain significant, anchoring domestic supply while expanding into export markets through improved technical capabilities and co-development partnerships. Smaller players such as Millrock Technology, Martin Christ, Cuddon Freeze Dry, and Kyowa Vacuum Engineering compete effectively by offering shorter lead times, specialized application knowledge, and accessible capital thresholds. Harvest Right targets a different segment with bench-top and smaller commercial systems, promoting awareness and entry-level adoption among artisan food and nutraceutical users.

Freeze Drying Equipment Industry Leaders

Azbil Corporation

GEA Group

IMA Group

SP Scientific LLC

Labconco Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: LYOCONTRACT and Syntegon initiated a EUR 50 million expansion of their freeze-drying facility in Ilsenburg, Germany. The project, featuring a new vial line for filling, isolating, and lyophilization, is expected to be completed by summer 2027, enhancing capacity for freeze-dried parenterals in the European CDMO market.

- February 2026: GEA opened its EUR 80 million pharmaceutical freeze-drying technology center in Elsdorf, Germany. The 45,500 m² CO2-neutral facility, powered by photovoltaic energy, integrates R&D, production, and services, strengthening lyophilizer manufacturing capabilities.

- February 2026: GEA launched the ALUS automatic loading and unloading systems for freeze dryers, aimed at reducing operator involvement, increasing productivity, and lowering operational costs. Over 350 ALUS® systems are in use globally.

- January 2026: IMA Life collaborated with Sharp Sterile Manufacturing to deliver a fully automated lyophilizer and isolated filling line for Sharp's USD 28 million facility expansion in Lee, Massachusetts, doubling the site's sterile filling capacity.

- November 2025: GEA's LYOVAC ECO mode was awarded the Add Better environmental label, validated by TÜV Rheinland under DIN EN ISO 14021:2021-10 standards. The feature achieves a 21.1% reduction in electricity consumption over a 46.55-hour production cycle and is retrofittable to existing liquid-condenser freeze dryers.

Global Freeze Drying Equipment Market Report Scope

As per the scope of the report, freeze-drying equipment (lyophilizers) dehydrates perishable materials by freezing them and then reducing the surrounding pressure, allowing the frozen water to sublimate directly into vapor. It preserves a product's structure, nutrients, and shelf life, and is widely used in food processing, pharmaceuticals, and laboratories.

The freeze drying equipment market is segmented by product type, scale of operation, application, and geography. By product type, the market includes tray-style freeze dryers, manifold freeze dryers, rotary freeze dryers, bench top freeze dryers, industrial freeze dryers, laboratory freeze dryers, and general-purpose freeze dryers. By scale of operation, the market is segmented into laboratory scale, pilot scale, and industrial scale. By application, the market is categorized into pharmaceuticals, biotechnology, food processing, surgical procedures, nutraceuticals, and other applications. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Tray-Style Freeze Dryers |

| Manifold Freeze Dryers |

| Rotary Freeze Dryers |

| Bench Top Freeze Dryers |

| Industrial Freeze Dryers |

| Laboratory Freeze Dryers |

| General Purpose Freeze Dryers |

| Laboratory Scale |

| Pilot Scale |

| Industrial Scale |

| Pharmaceuticals |

| Biotechnology |

| Food Processing |

| Surgical Procedures |

| Nutraceuticals |

| Other Applications in Freeze Drying Equipment |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Tray-Style Freeze Dryers | |

| Manifold Freeze Dryers | ||

| Rotary Freeze Dryers | ||

| Bench Top Freeze Dryers | ||

| Industrial Freeze Dryers | ||

| Laboratory Freeze Dryers | ||

| General Purpose Freeze Dryers | ||

| By Scale of Operation | Laboratory Scale | |

| Pilot Scale | ||

| Industrial Scale | ||

| By Application | Pharmaceuticals | |

| Biotechnology | ||

| Food Processing | ||

| Surgical Procedures | ||

| Nutraceuticals | ||

| Other Applications in Freeze Drying Equipment | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the freeze drying equipment market?

The freeze drying equipment market is valued at USD 2.69 billion in 2026 and is forecast to reach USD 3.99 billion by 2031, growing at a CAGR of 8.16% during 2026-2031.

Which region leads freeze drying equipment demand?

North America led with 39.25% of global demand in 2025 because of its strong pharmaceutical manufacturing base, mature CDMO network, and ongoing compliance-driven equipment replacement.

Which region is growing the fastest in freeze drying equipment?

Asia-Pacific is projected to expand at an 11.20% CAGR through 2031, supported by biologics capacity growth in China, CDMO expansion in India, and stronger sterile manufacturing investment across the region.

Which product category has the largest share in freeze drying systems?

Industrial freeze dryers held the largest share at 45.67% in 2025 because large pharmaceutical and food installations continue to prioritize throughput, reproducibility, and validated operating performance.

Which application is creating the strongest growth opportunity?

Pharmaceuticals remained the largest application at 34.77% in 2025, while food processing is the fastest-growing application with a 10.55% CAGR through 2031 as premium and functional freeze-dried foods gain wider acceptance.

What are buyers looking for when selecting new lyophilization equipment?

Buyers are increasingly prioritizing contamination control, automatic loading and unloading, PAT and digital tools, and energy-saving features such as validated retrofit options that reduce power use without disrupting existing production.

Page last updated on: