Freeze Drying Equipment and Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

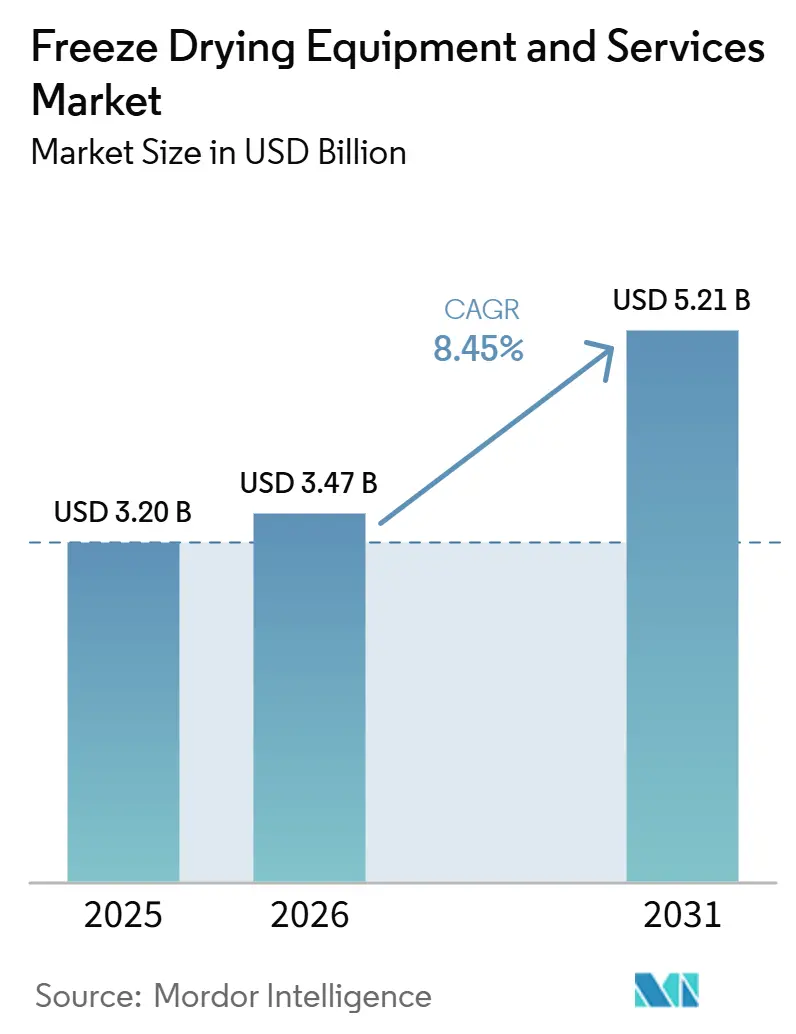

| Market Size (2026) | USD 3.47 Billion |

| Market Size (2031) | USD 5.21 Billion |

| Growth Rate (2026 - 2031) | 8.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Freeze Drying Equipment and Services Market Analysis by Mordor Intelligence

The Freeze Drying Equipment And Services Market size is expected to grow from USD 3.20 billion in 2025 to USD 3.47 billion in 2026 and is forecast to reach USD 5.21 billion by 2031 at 8.45% CAGR over 2026-2031.

The freeze drying equipment and services market continues to derive its core demand from biologics and sterile injectables, where lyophilization helps maintain product stability and extend storage life. The market driven by biologics capacity expansion, contract development and manufacturing organization (CDMO) activity, and manufacturing upgrades across China and India. Pharmaceutical use remains the largest application area, while food processing is gaining traction as premium food and nutraceutical brands use freeze drying to preserve texture, nutrients, and shelf life.

Key Report Takeaways

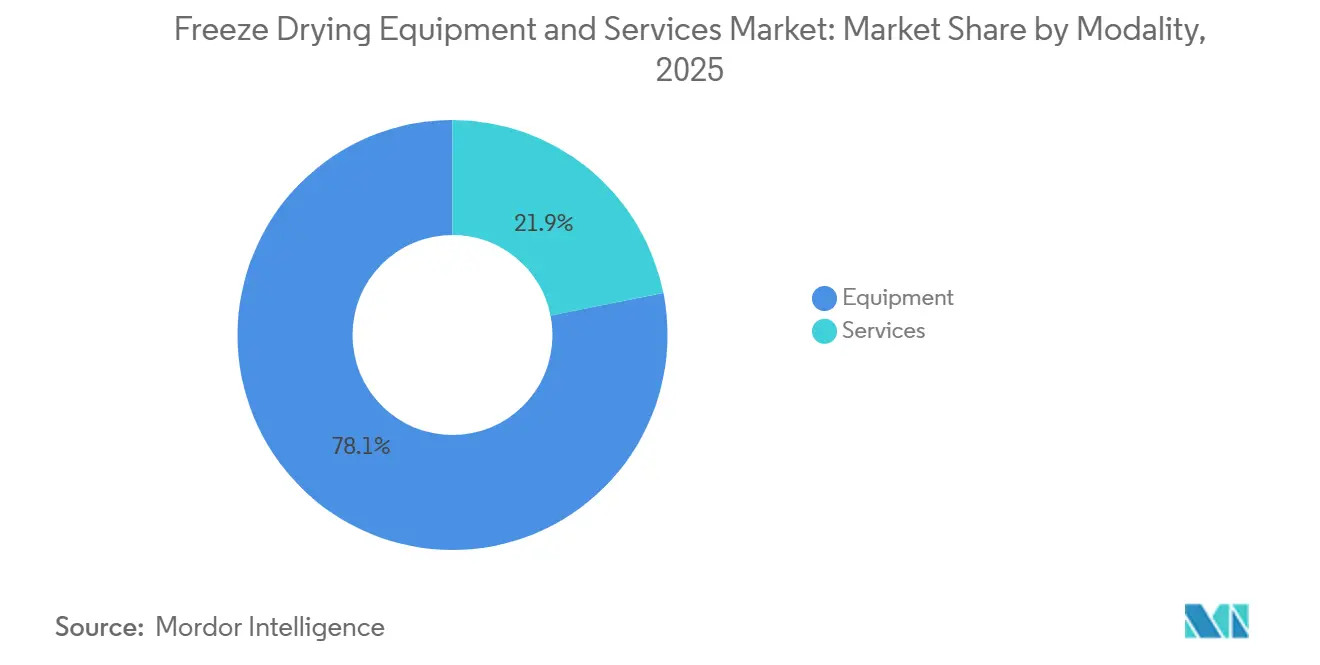

- By modality, equipment held 78.12% of the freeze drying equipment and services market share in 2025, while services are projected to expand at a 9.53% CAGR through 2031.

- By scale of operation, industrial-scale systems accounted for 48.45% of the freeze drying equipment and services market size in 2025, while laboratory-scale systems are forecast to grow at a 10.67% CAGR through 2031.

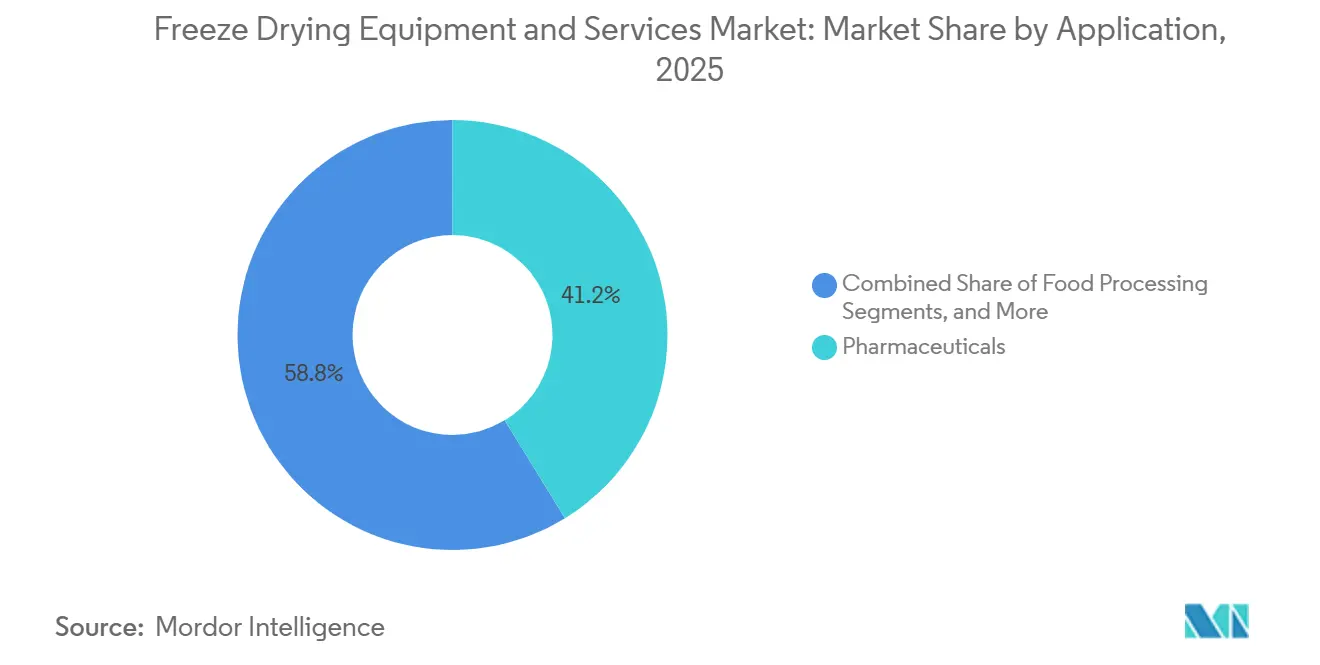

- By application, pharmaceuticals captured 41.24% of the freeze drying equipment and services market size in 2025, while food processing is expected to advance at a 9.35% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies held 38.67% share in 2025, while CDMOs are projected to grow at an 11.67% CAGR through 2031.

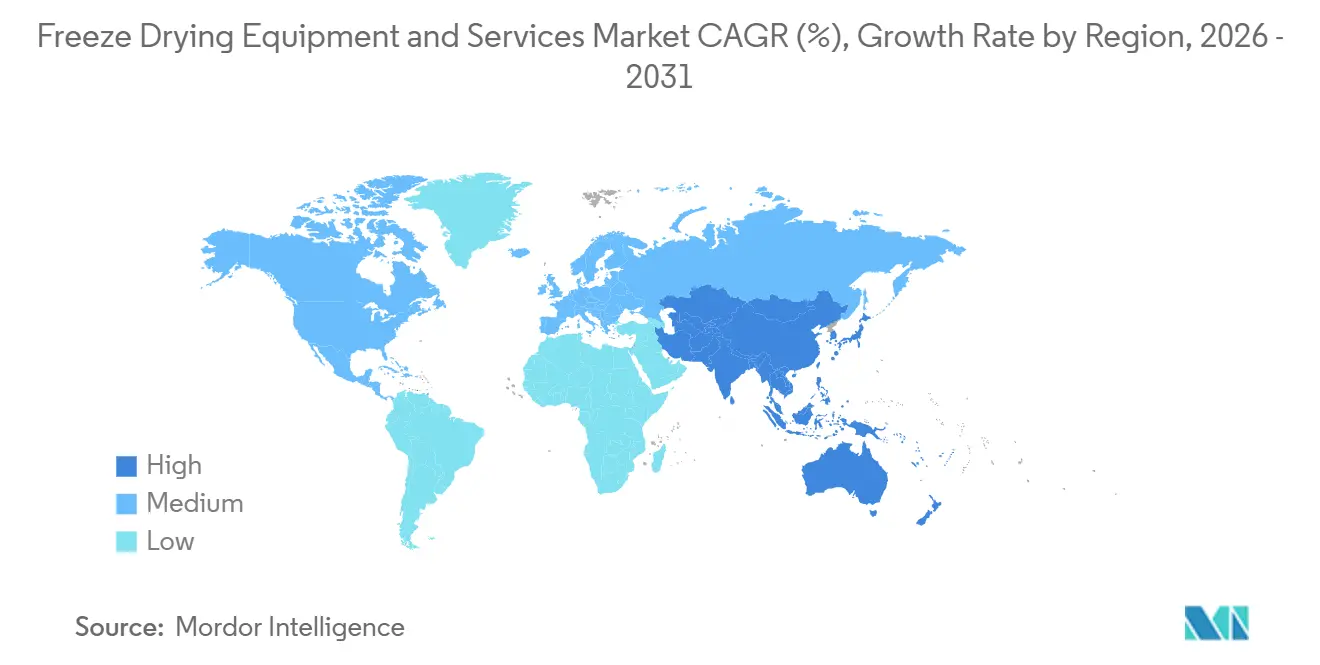

- By geography, North America led with 42.56% share in 2025, while Asia-Pacific is expected to record the highest regional CAGR of 12.56% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Freeze Drying Equipment and Services Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising biologics, vaccines, and injectable manufacturing | +2.5% | Global, highest intensity in North America and Europe | Long term (≥ 4 years) |

| Expansion of freeze-dried food and nutraceutical formulations | +1.8% | Global, fastest uptake in APAC and North America | Medium term (2-4 years) |

| Automation, IOT, and process analytical technology adoption | +1.4% | North America and Europe core, early adoption in APAC | Long term (≥ 4 years) |

| Annex 1 driven sterility and contamination control upgrades | +1.2% | Europe primarily, with spillover to the UK, Canada, and export-regulated markets | Short term (≤ 2 years) |

| Energy-efficient and low-carbon retrofit demand | +0.7% | Europe and North America | Medium term (2-4 years) |

| Cold chain fragility and product stability requirements | +0.6% | Global, with emphasis on the Middle East, Africa, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Biologics, Vaccines, and Injectable Manufacturing

The freeze drying equipment and services market is recording stronger demand from biologics, as lyophilization is shifting from a supporting process step to a core production requirement. Monoclonal antibodies, antibody-drug conjugate therapies, and messenger RNA-based vaccines often require freeze drying when liquid formats do not provide sufficient ambient-temperature stability. Lyophilization of messenger RNA lipid nanoparticles is becoming a critical formulation route for next-generation therapeutics, with growing use of Quality by Design and Process Analytical Technology in regulatory work. Buyers are increasingly specifying Process Analytical Technology integration at the purchase stage because retrofitting a unit later is difficult in a Good Manufacturing Practice setting. As a result, contract development and manufacturing organizations competing for large-molecule programs are favoring open-architecture systems that support third-party Process Analytical Technology tools and broader process control requirements.

Expansion of Freeze-Dried Food and Nutraceutical Formulations

The freeze drying equipment and services market is benefiting from wider adoption in premium food and nutraceutical products. Freeze-dried food has moved beyond military and survival applications and is now part of mainstream premium retail demand. In nutraceuticals, probiotics, botanical extracts, and sensitive proteins often require freeze drying because heat-based methods can damage the active compounds that define product value. Clean-label snacking and functional nutrition trends are expanding the installation base for food-grade lyophilizers beyond traditional fruit and vegetable processing. This segment follows a different buying pattern than pharmaceutical demand, as cleanroom requirements are lower, while price pressure and throughput requirements are higher.

Automation, IoT, and Process Analytical Technology Adoption

Automation is reshaping plant-level operations in the freeze drying equipment and services market. New systems increasingly include advanced supervisory control and data acquisition platforms, automated loading and unloading, and real-time Process Analytical Technology tools such as tunable diode laser absorption spectroscopy and wireless temperature sensors. These additions improve cycle visibility and help reduce conservative operating margins that often extend production time. Process control gaps remain a key focus area in freeze drying inspections, prompting manufacturers to strengthen instrumentation and data capture. Digital twin environments are also gaining relevance because they reduce physical scale-up iterations and help companies shorten development timelines.

Annex 1 Driven Sterility and Contamination Control Upgrades

Regulatory enforcement is creating a direct upgrade cycle in the freeze drying equipment and services market. European Union Good Manufacturing Practice Annex 1 reached full implementation after the last deferred lyophilizer sterilization provision, and 2026 marks the year of full enforcement for affected facilities.[1]Critical Reviews in Biotechnology, “Lyophilization of Biologics: Innovations, Challenges, and Future Directions in Stabilizing Next-Generation Therapeutics,” doi.org The rule requires documented contamination control strategies across the site, with freeze dryer loading and unloading remaining key inspection focus areas because these steps are highly sensitive in aseptic operations. West Pharmaceutical Services noted that manufacturers are redesigning isolator configurations so vial filling and freeze drying operate as one integrated aseptic environment rather than separate operations. This shift is increasing demand for automated loading systems and isolator-integrated freeze dryers, even where existing units remain operational.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High upfront capital cost versus conventional drying | -1.5% | Global, most pronounced in emerging markets | Long term (≥ 4 years) |

| Long cycle times and throughput constraints | -0.9% | Global, particularly for high-volume commercial facilities | Medium term (2-4 years) |

| Energy intensity and utility load requirements | -0.7% | Europe and North America, where energy costs are high | Medium term (2-4 years) |

| Skilled operator and validation burden | -0.5% | Global, acute in APAC and the Middle East and Africa emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Cost Versus Conventional Drying

High capital costs remain a key barrier to expansion in the freeze drying equipment and services market. A large pharmaceutical-grade production freeze dryer can cost USD 1 million to more than USD 5 million before installation, qualification, and validation costs. This cost is significantly higher than that of spray dryers or fluidized bed systems with similar throughput requirements. For generic injectable manufacturers and emerging-market contract development and manufacturing organizations (CDMOs), this cost profile extends return periods and can delay investment decisions by several years. Higher financing costs from 2022 through 2025 are expected to make procurement more difficult for smaller operators, especially where price-sensitive end products limit the scope for premium processing choices.

Skilled Operator and Validation Burden

The freeze drying equipment and services market also faces structural constraints from validation complexity and workforce scarcity. Manufacturers must develop, scale up, validate, and document each lyophilization cycle for a specific product, and this process can take 12 to 24 months within a regulated submission pathway. The required skill base combines vacuum engineering, thermodynamics, formulation science, and Good Manufacturing Practice (GMP) documentation, and this expertise is not widely available across all regions. Digital platforms and Process Analytical Technology (PAT) tools can reduce part of this burden, but documentation and compliance requirements will continue to create a long-term challenge for the freeze drying equipment and services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: Equipment Dominance Shapes Capital Allocation, Services Accelerate

Equipment is expected to hold 78.12% of the freeze drying equipment and services market in 2025, reflecting the capital-intensive nature of lyophilization build-outs. Tray-style systems remain the preferred configuration across pharmaceutical and food applications because they support batch uniformity and automated loading. Manifold and rotary systems continue to serve laboratory and nutraceutical applications, where flexibility is more important than maximum throughput.

Replacement demand is also supporting equipment purchases, as older units in Europe face refrigerant-related compliance pressure. Retrofit costs of up to EUR 80,000 (USD 91,498.80) for older units have encouraged some operators to choose full replacement over partial upgrades. Services are projected to grow faster, at a CAGR of 9.53% through 2031, driven by long-term requirements for validation, calibration, maintenance, training, and outsourced lyophilization support.

By Scale of Operation: Industrial Scale Anchors Revenue While Laboratory Systems Lead Growth

Industrial-scale systems are expected to account for 48.45% of the freeze drying equipment and services market size in 2025, as commercial pharmaceutical and food facilities require large batch capacity and consistent throughput. Major biopharma companies, contract development and manufacturing organizations (CDMOs), and food processors typically purchase these systems to improve shelf utilization and turnaround time. Pilot-scale units remain important because they connect development work with commercial manufacturing.

Large-scale demand remains visible through supplier investments. GEA is expected to inaugurate its EUR 80 million (USD 91.50 million) pharmaceutical technology center in Elsdorf, Germany, in February 2026, combining research, production, and digital workflows in a 40,000+m² CO2-neutral site. Laboratory-scale freeze dryers are projected to grow at a CAGR of 10.67% through 2031, supported by contract research organizations (CROs), academic institutes, and pharmaceutical research and development (R&D) teams working on formulation and scale-up.

By Application: Pharmaceuticals Lead as Food Processing Closes the Gap

Pharmaceuticals are expected to account for 41.24% of the freeze drying equipment and services market in 2025, supported by stringent specification and compliance requirements. Demand is driven by monoclonal antibodies, antibody-drug conjugate (ADC) therapies, gene therapy vectors, and vaccines that require lyophilization due to aqueous instability or storage limitations. Biotechnology applications further support demand through cell therapy processing and research-driven vaccine work.

Quality by design (QbD) frameworks and artificial intelligence-assisted cycle development are helping pharmaceutical teams shorten formulation-to-filing timelines and manage more freeze drying programs. Food processing is projected to grow faster, at a CAGR of 9.35% through 2031, as demand increases for premium fruit snacks, ready meals, and functional ingredients. Nutraceutical products, including probiotics, botanical extracts, and sensitive proteins, add further demand because freeze drying protects bioactivity better than heat-based alternatives.

By End User: CDMO Surge Redefines the Lyophilization Procurement Model

Pharmaceutical and biotechnology companies are expected to hold 38.67% of the freeze drying equipment and services market in 2025, as integrated manufacturers continue to operate a large share of proprietary lyophilization capacity. These companies are replacing or upgrading systems with built-in process analytical technology (PAT) functions and automated loading to meet regulatory expectations. Food processing companies form the next major end-user group, while academic and research institutes continue to support laboratory equipment demand.

CDMOs are projected to grow the fastest, at a CAGR of 11.67% through 2031, as pharmaceutical manufacturing outsourcing expands across development and commercial supply. Thermo Fisher Scientific is expected to invest USD 1 billion across its global 60-site CDMO network in 2026 to expand capacity and digital capabilities for complex biologics and advanced delivery formats. PCI Pharma Services is expected to commission a good manufacturing practice (GMP)-ready isolator vial and lyophilization line in Bedford, New Hampshire, in April 2026, with twin 40m² freeze dryers, automatic loading and unloading, and capacity of up to 300,000 vials per batch at 400 units per minute.

Geography Analysis

North America is expected to hold 42.56% of the freeze drying equipment and services market in 2025, making it the largest regional contributor. The region benefits from the scale of the US biopharmaceutical manufacturing base and strong demand for lyophilized injectables. FDA oversight of process validation and freeze drying control continues to support demand for advanced equipment, process analytical technology (PAT) integration, and revalidation services. PCI Pharma Services’ planned commissioning in April 2026 of a twin 40 m² lyophilizer line in Bedford, New Hampshire, with an annual capacity of 33 million vials, highlights sustained regional investment.

Europe remains the second-largest regional market in the freeze drying equipment and services market and has the deepest concentration of pharmaceutical-grade equipment suppliers. The region includes major companies such as GEA Group, Syntegon, Martin Christ, IMA S.p.A., OPTIMA, and ZIRBUS. Germany serves as both a manufacturing hub and a major end-user center, supported by GEA’s EUR 80 million (USD 91.50 million) Elsdorf facility, scheduled to open in February 2026. Compliance with European Union Good Manufacturing Practice (EU GMP) Annex 1 is driving investment in sterilization validation and automated loading systems across European facilities.

Asia-Pacific is the fastest-growing region in the freeze drying equipment and services market, with a projected CAGR of 12.56% through 2031. China is recording strong local demand as biosimilar, antibody-drug conjugate (ADC), and messenger ribonucleic acid (mRNA) manufacturing scale up. Domestic manufacturers are strengthening their position in standard pharmaceutical systems, while imported brands continue to lead the higher-end biopharmaceutical tier. India is benefiting from export-focused contract development and manufacturing organization (CDMO) expansion, sterile dosage growth, and continued manufacturing modernization, while the Middle East, Africa, and South America remain smaller but are seeing opportunities from local vaccine manufacturing and lower cold-chain dependence in Brazil, South Africa, Saudi Arabia, and the UAE.

Competitive Landscape

The freeze drying equipment and services market remains moderately consolidated in the high-end pharmaceutical tier, where a limited group of suppliers competes on technology depth, validation expertise, and service reach. GEA Group, Syntegon, IMA S.p.A., Martin Christ, OPTIMA, SP Industries, and ZIRBUS remain prominent in this segment of the market. These companies maintain their position through proprietary system design, regulatory credibility, and support across qualification, installation, and long-term maintenance. This creates a clear distinction between high-specification pharmaceutical projects and demand from standard food applications or lower-tier pharmaceutical customers.

Syntegon’s October 2024 acquisition of Azbil Telstar is a key strategic move in the freeze drying equipment and services market, as it expanded the company’s ability to deliver integrated vial filling, isolator, and freeze drying lines from a single source. This integrated approach has gained importance as Annex 1 increases demand for unified aseptic line design and lowers tolerance for multi-vendor complexity. GEA’s EUR 80 million (USD 91.50 million) investment in Elsdorf is another major strategic move, as it combines research, manufacturing, and service capabilities in one facility and improves execution speed for global customers. IMA S.p.A. continues to benefit from its loading automation capabilities, which support contamination control and workflow efficiency at pharmaceutical sites.

Mid-tier and emerging players are adopting different strategies to compete in the freeze drying equipment and services market. Shanghai Tofflon is strengthening its position in China and other emerging markets with a price-competitive offering that appeals to Contract Development and Manufacturing Organizations (CDMOs) and generic manufacturers focused on cost per batch. Labconco, Millrock Technology, and BUCHI remain important in laboratory and pilot-scale segments, where precision, flexibility, and research workflow matter more than large production volume. Smaller consumer-oriented brands, such as Harvest Right, operate in a different part of the market and are not directly tied to pharmaceutical procurement cycles, while stricter requirements for data integrity, sterility, and validation continue to raise the minimum specification level across all tiers.

Freeze Drying Equipment and Services Industry Leaders

GEA Group Aktiengesellschaft

IMA S.p.A.

SP Industries, Inc.

Christ Freeze Dryers GmbH

Cuddon Freeze Dry

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: PCI Pharma Services commissioned a GMP-ready bespoke isolator vial and lyophilization line at its Bedford, New Hampshire campus, supported by over USD 1 billion in global investment commitments.

- March 2026: LYOCONTRACT and Syntegon broke ground on a EUR 50 million (USD 54 million) expansion at LYOCONTRACT’s Ilsenburg, Germany facility, adding filling and lyophilization capacity.

- February 2026: GEA Group inaugurated its EUR 80 million (USD 91.50 million) pharmaceutical technology center for freeze-drying systems in Elsdorf, Germany, integrating R&D, production, and services.

- February 2026: Axplora announced a EUR 30 million (USD 35 million) multi-year program at its Le Mans, France CDMO site to add commercial lyophilization capacity for ADC manufacturing.

- January 2026: Martin Christ Gefriertrocknungsanlagen GmbH delivered its 30,000th freeze dryer, an Epsilon 2-10D LyoLift system, to Coriolis Pharma Research GmbH.

Global Freeze Drying Equipment and Services Market Report Scope

As per the scope of the report, freeze drying is a dehydration process where a product is frozen, then subjected to a vacuum to remove ice via sublimation (transitioning directly from a solid to a gas). This preserves cellular structure, flavor, and nutrients without heat degradation, yielding long-lasting, shelf-stable goods.

The freeze drying equipment and services market is segmented by modality, scale of operation, application, end user, and geography. By modality, the market includes equipment and services. The equipment segment includes tray-style freeze dryers, manifold freeze dryers, rotary freeze dryers, benchtop freeze dryers, industrial freeze dryers, laboratory freeze dryers, and others. The services segment includes installation and commissioning, validation and qualification, maintenance and repair, calibration and upgrades, contract freeze drying services, and training and technical support. By scale of operation, the market is segmented into laboratory scale, pilot scale, and industrial scale. By application, the market is categorized into pharmaceuticals, biotechnology, food processing, surgical procedures, nutraceuticals, and others. By end user, the market is segmented into pharmaceutical and biotechnology companies, food processing companies, academic and research institutes, contract development and manufacturing organizations, hospitals and surgical centers, and others. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Equipment | Tray Style Freeze Dryers |

| Manifold Freeze Dryers | |

| Rotary Freeze Dryers | |

| Bench Top Freeze Dryers | |

| Industrial Freeze Dryers | |

| Laboratory Freeze Dryers | |

| Others | |

| Services | Installation and Commissioning |

| Validation and Qualification | |

| Maintenance and Repair | |

| Calibration and Upgrades | |

| Contract Freeze Drying Services | |

| Training and Technical Support |

| Laboratory Scale |

| Pilot Scale |

| Industrial Scale |

| Pharmaceuticals |

| Biotechnology |

| Food Processing |

| Surgical Procedures |

| Nutraceuticals |

| Others |

| Pharmaceutical and Biotechnology Companies |

| Food Processing Companies |

| Academic and Research Institutes |

| Contract Development and Manufacturing Organizations |

| Hospitals and Surgical Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Modality | Equipment | Tray Style Freeze Dryers |

| Manifold Freeze Dryers | ||

| Rotary Freeze Dryers | ||

| Bench Top Freeze Dryers | ||

| Industrial Freeze Dryers | ||

| Laboratory Freeze Dryers | ||

| Others | ||

| Services | Installation and Commissioning | |

| Validation and Qualification | ||

| Maintenance and Repair | ||

| Calibration and Upgrades | ||

| Contract Freeze Drying Services | ||

| Training and Technical Support | ||

| By Scale of Operation | Laboratory Scale | |

| Pilot Scale | ||

| Industrial Scale | ||

| By Application | Pharmaceuticals | |

| Biotechnology | ||

| Food Processing | ||

| Surgical Procedures | ||

| Nutraceuticals | ||

| Others | ||

| By End User | Pharmaceutical and Biotechnology Companies | |

| Food Processing Companies | ||

| Academic and Research Institutes | ||

| Contract Development and Manufacturing Organizations | ||

| Hospitals and Surgical Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the freeze drying equipment and services space?

The freeze drying equipment and services market stands at USD 3.47 billion in 2026 and is projected to reach USD 5.21 billion by 2031 at an 8.45% CAGR.

Which product category leads revenue today?

Equipment leads with a 78.12% share in 2025 because lyophilization capacity expansion is still driven mainly by capital equipment purchases.

Which end-user group is growing the fastest?

CDMOs are expected to grow the fastest at an 11.67% CAGR through 2031 as outsourcing in biologics and sterile manufacturing expands.

Why are laboratory freeze dryers gaining attention?

Laboratory-scale systems are projected to grow at a 10.67% CAGR because mRNA-LNPs and other complex biologics require extensive bench-scale cycle development before commercial scale-up.

Which region offers the strongest near-term growth potential?

Asia-Pacific is forecast to grow the fastest at a 12.56% CAGR through 2031, supported by biologics capacity expansion, CDMO scale-up, and manufacturing modernization.

What is the biggest barrier to wider adoption?

High upfront capital cost remains the main barrier, since pharmaceutical-grade production freeze dryers can cost from USD 1 million to more than USD 5 million before installation and validation.

Page last updated on: