Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

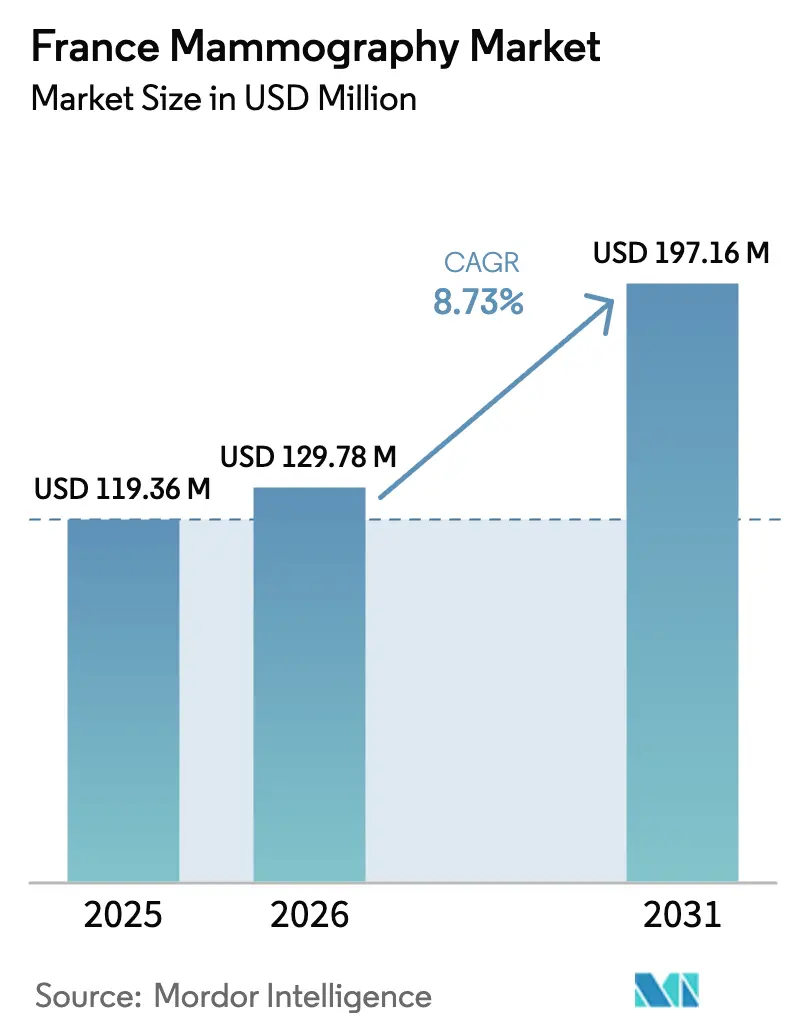

| Base Year Market Size (2025) | USD 119.36 Million |

| Market Size (2026) | USD 129.78 Million |

| Market Size (2031) | USD 197.16 Million |

| Growth Rate (2026 - 2031) | 8.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Mammography Market Analysis by Mordor Intelligence

The France Mammography Market size is expected to grow from USD 119.36 million in 2025 to USD 129.78 million in 2026 and is forecast to reach USD 197.16 million by 2031 at 8.73% CAGR over 2026-2031. This expansion reflects the combined effect of a nationwide screening program that now covers 2.5 million women biennially, an aging population that pushes breast-cancer incidence above 61 000 new cases per year, and steady replacement of analog equipment by 2-D and 3-D digital systems. Uptake also benefits from the January 2024 transfer of invitation management to Assurance Maladie, a move designed to add 1 million extra examinations each year by 2025. On the supply side, the France Mammography Market gains momentum from the Haute Autorité de Santé’s endorsement of tomosynthesis for organized screening and the Agence nationale de sécurité du médicament’s stricter quality-control rules that compel facilities to modernize equipment. Vendor competition now focuses on workflow automation, embedded AI and value-based service contracts that mitigate capital-budget barriers. Simultaneously, radiologist shortages in rural departments, lingering patient anxiety over radiation exposure and the high cost of advanced systems create selective headwinds that modulate—but do not derail—the market’s upward trajectory.

Key Report Takeaways

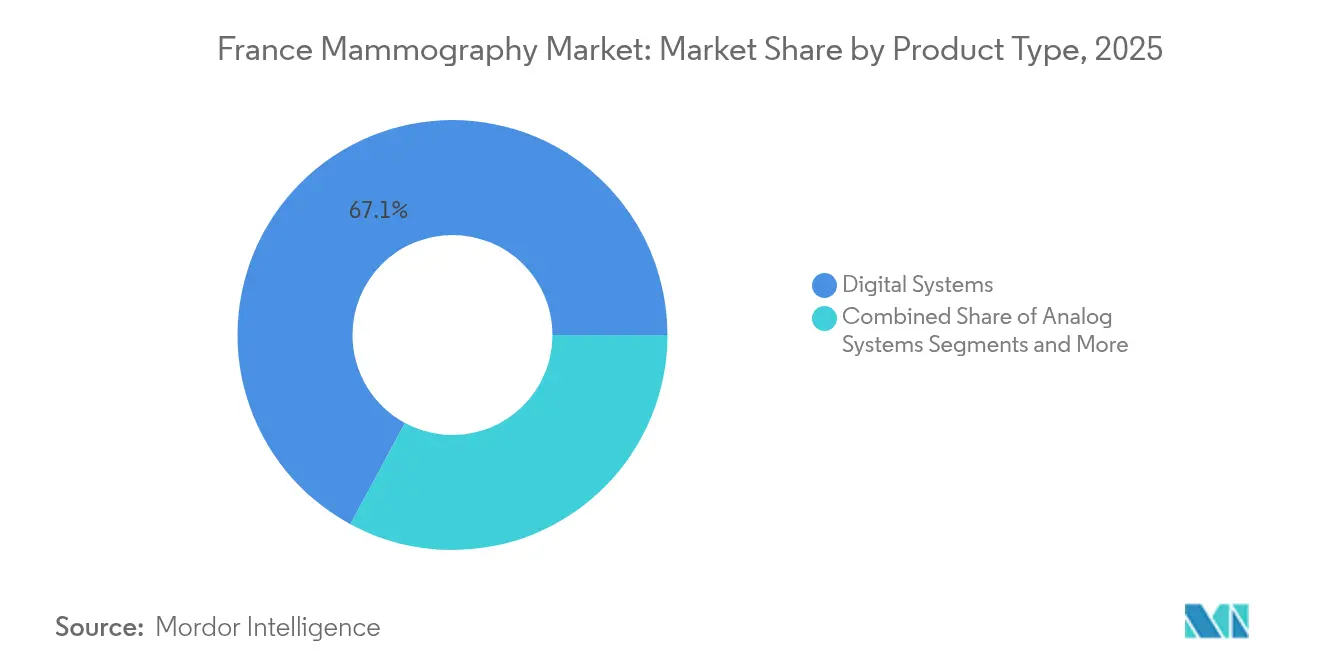

- By product type, Digital Systems captured 67.12% of the France Mammography market share in 2025 while Breast Tomosynthesis is projected to expand at a 9.03% CAGR through 2031.

- By end user, Hospitals held 53.42% of the France Mammography market size in 2025, whereas Diagnostic Centers are advancing at a 9.11% CAGR to 2031.

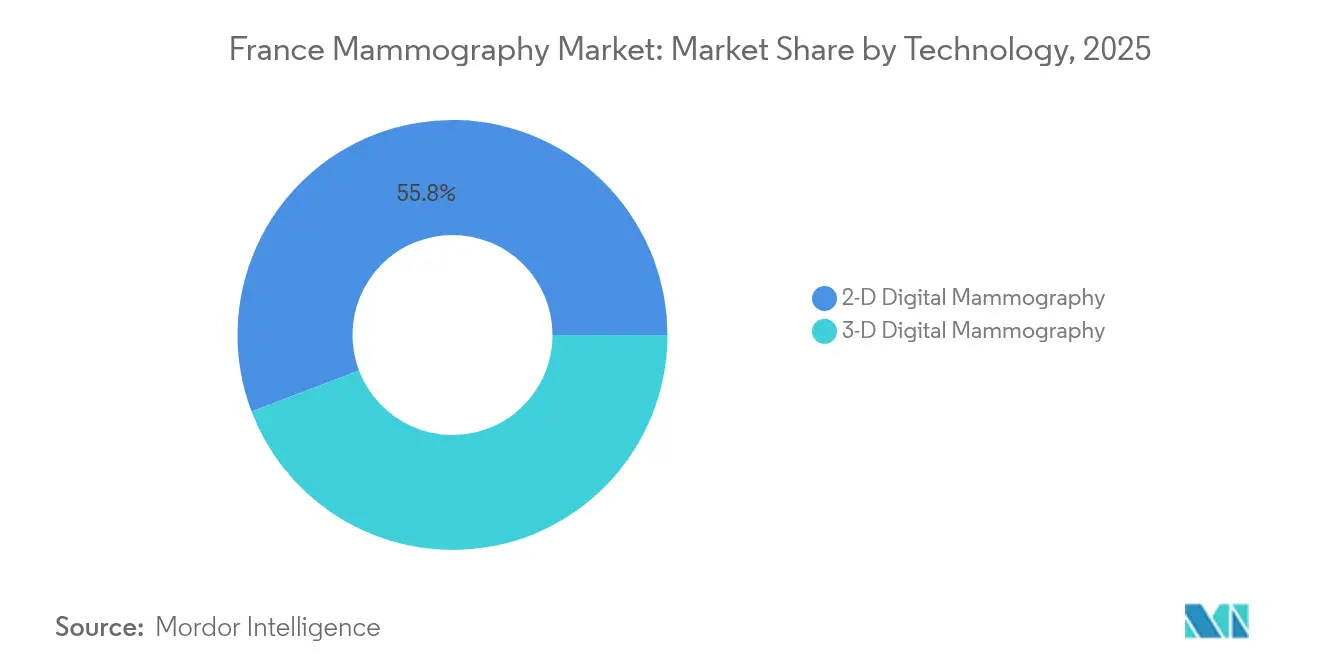

- By technology, 2-D Digital accounted for 55.78% of the France Mammography market size in 2025; 3-D Digital is set to grow at a 9.42% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Mammography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising breast-cancer incidence | +2.1% | National; highest in aging regions | Long term (≥ 4 years) |

| Shift from 2-D to 3-D tomosynthesis | +1.8% | University hospitals lead, cascading to regional centers | Medium term (2-4 years) |

| National screening expansion & reimbursement | +1.5% | All departments; priority to rural territories | Short term (≤ 2 years) |

| AI-enabled CAD adoption | +1.2% | Large urban hospitals and diagnostic hubs | Medium term (2-4 years) |

| Rising Public-Private Awareness Campaigns | +1.0% | National, with higher impact in low-participation regions | Short term (≤ 2 years) |

| Deployment of mobile units | +0.8% | Rural and overseas territories | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Incidence of Breast Cancer in France

More than 61 000 women received a breast-cancer diagnosis in 2024, keeping the disease France’s most common female malignancy [1]ARS Centre-Val-de-Loire, “Les femmes concernées par le dépistage…,” centre-val-de-loire.ars.sante.fr. Eight out of ten cases arise after age 50, perfectly aligning with the target age bracket of the organized screening program. Policymakers are now evaluating an age-threshold reduction as nearly 5 000 women under 40 receive a diagnosis each year, signaling potential expansion in screening volumes. Regional disparities are stark, with participation ranging from 35% in Corsica to 57% in Centre-Val-de-Loire. These participation gaps translate into equipment-density imbalances that vendors can exploit by focusing sales efforts on low-uptake departments. The Institut National du Cancer reported 38 000 cancers detected via screening in 2023, underscoring how capacity additions directly influence early-detection outcomes. Rising incidence therefore sustains a baseline demand curve for the France Mammography Market that is immune to macroeconomic volatility.

Technological Shift Toward 3-D Breast Tomosynthesis

In March 2023 the Haute Autorité de Santé validated tomosynthesis for organized screening after clinical evidence demonstrated superior lesion detection without exceeding acceptable radiation limits. Large centers, such as Hôpital d’Instruction des Armées Bégin, quickly installed new-generation 3-D units in 2024. Yet national rollout faces bottlenecks—mainly limited PACS bandwidth and the need for radiologist re-training. Vendors that bundle 3-D hardware with robust archiving and AI-triage software capture a competitive edge. Over 2025-2027, procurement frameworks managed by regional health agencies are expected to prioritize tomosynthesis-ready systems, accelerating replacement cycles. As a result, the France Mammography Market anticipates double-digit annual installations of 3-D units through the medium term.

Expansion of National Screening & Reimbursement Programs

Assurance Maladie’s takeover of invitation logistics in 2024 standardized messaging and data-capture processes, aiming to lift participation from 47% toward the European 70% benchmark. Full reimbursement of both the examination and second reading removes financial friction for patients and facilities. The D2LM platform now automates double reading nationwide, cutting administrative overhead by 25% and improving diagnostic concordance. Mobile screening projects like Mammobile in Normandy complement this push by physically reaching underserved areas. Collectively these initiatives expand procedure volumes and stabilize cash flows for equipment operators, giving lenders more confidence to finance new purchases.

AI-Enabled CAD Tools Boosting Diagnostic Throughput

AI vendors have proven in French multicenter trials that algorithmic triage reduces radiologist workload by roughly one-third while preserving sensitivity. Commercial adoption is rising: VIDI Group partnered with Lunit to deploy AI across 400 sites in 2024, a deal covering nearly one-quarter of France’s private radiology footprint. The Institut Curie’s ongoing collaboration with Galen and the Therapixel–Onsite Women’s Health alliance show that local and international actors alike view France as a fertile test bed for AI deployment. Regulatory hurdles remain—ANSM requires rigorous clinical validation—but once cleared, AI provides a scalable answer to workforce shortages, especially in the high-volume diagnostic-center segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of advanced systems | -1.8% | Smaller clinics and rural hospitals | Medium term (2-4 years) |

| Radiation-exposure concerns & anxiety | -1.3% | Educated urban populations | Long term (≥ 4 years) |

| Radiologist shortages in rural areas | -1.1% | Rural departments and overseas territories | Long term (≥ 4 years) |

| Legacy analog infrastructure | -0.9% | Older public hospitals | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Systems

Acquiring a tomosynthesis platform plus PACS integration can exceed EUR 450 000 (USD 490 000) for a mid-size public hospital, a price tag that strains budgets set under the national Objective de Dépenses d’Assurance Maladie framework. Smaller diagnostic centers often postpone upgrades or lease antiquated units, creating a technology gap. To mitigate sticker shock, Siemens Healthineers signed a 12-year, EUR 55 million value partnership with University Hospital Nantes that spreads costs across service years and guarantees technology refreshes. Such models are gaining traction, yet financing hurdles still slow overall adoption, dragging the France Mammography Market CAGR by an estimated 1.8 percentage points.

Risk of Radiation Exposure & Patient Anxiety

Surveys indicate 68.3% of women report mild to high anxiety ahead of mammography appointments. Fear of ionizing radiation amplifies this unease, despite doses falling well within safety thresholds set by the Autorité de sûreté nucléaire. Incidents of pediatric overexposure from unrelated mobile radiology units in 2024 received wide media coverage, reinforcing public skepticism. Manufacturers now tout low-dose innovations, such as Fujifilm’s AMULET SOPHINITY platform, which claims a 30% dose reduction while maintaining image quality. Education campaigns run by regional cancer agencies help neutralize misconceptions, yet lingering anxiety still deters some eligible women, marginally depressing equipment utilization rates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Systems Anchor the Transition

Digital Systems generated 67.12% of 2025 revenue, cementing their role as the backbone of organized screening because ANSM quality-control rules effectively disqualify analog units from program participation. Hospitals typically renew digital hardware every 7-8 years, so a sizable installed base is now entering a replacement cycle that will buoy the France Mammography Market through 2031. Breast Tomosynthesis, though currently smaller, is growing at a 9.03% CAGR as facilities pivot toward 3-D imaging for its higher cancer-detection yield. Analog Systems command single-digit revenue shares and face imminent retirement, while Other Product Types—such as contrast-enhanced mammography—remain niche but could gain relevance for high-risk populations.

Procurement behavior illustrates two tiers: university hospitals purchase fully loaded tomosynthesis suites with integrated AI, whereas community clinics favor entry-level digital machines with upgrade paths. GE Healthcare’s Senographe Pristina and Hologic’s 3Dimensions exemplify vendor strategies that pair ergonomic design with workflow-friendly features like zero-click positioning. Fujifilm and IMS Giotto differentiate on dose-sparing technology, appealing to facilities eager to address patient-radiation concerns. These competitive nuances will shape market-share shifts within the Digital and Tomosynthesis subsegments over the forecast horizon.

By End User: Diagnostic Centers Accelerate While Hospitals Retain Scale

Hospitals controlled 53.42% of 2025 spending, driven by their integration into the national referral network and their access to public-sector capital budgets. Yet Diagnostic Centers are expanding faster at a 9.11% CAGR because they offer shorter wait times, extended hours and high equipment utilization that drives favorable economics in a fee-for-service landscape. Their growth also reflects rising outpatient care preferences among French consumers and the health ministry’s push to decongest hospitals. Specialty Clinics occupy a middle ground, focusing on high-risk or follow-up imaging that requires subspecialist expertise; they maintain stable but comparatively modest growth.

Mobile units, though representing less than 2% of the France Mammography market size, wield outsized strategic importance by servicing rural and overseas territories where fixed infrastructure is sparse. Projects like Mammobile, funded through regional health-agency grants, demonstrate public-private collaboration models that vendors can replicate across departments with participation rates below 40%. Overall, competition for new installations will intensify within the diagnostic-center channel, prompting manufacturers to craft leasing and pay-per-exam packages that accommodate facility cash-flow constraints.

By Technology: 3-D Digital Gains Momentum Over 2-D Mainstay

2-D Digital Mammography retained a 55.78% France Mammography market share in 2025, reflecting its entrenched status as the default screening modality and its cost-advantage over tomosynthesis. However, 3-D Digital Mammography is projected to outpace every other subsegment with a 9.42% CAGR through 2031, as clinical studies and regulatory endorsement validate its superior diagnostic yield in dense-breast populations. Facilities undergoing hardware refresh cycles increasingly opt for 3-D-capable systems even if immediate tomosynthesis use is deferred, effectively future-proofing their investments.

Workflow considerations influence purchasing decisions; tomosynthesis generates larger image sets, thus requiring higher-capacity servers and faster network links. Vendors that bundle storage, AI-powered triage and cloud-reading services ease this burden. Radiologist-training programs, often co-sponsored by manufacturers, further accelerate technology adoption by shortening learning curves. Consequently, the France Mammography Market is on the cusp of a technology-mix shift where 3-D installations will represent the majority of new units by 2028.

Geography Analysis

Regional uniformity in reimbursement policy masks pronounced geographic disparities in screening access and equipment density. Metropolitan regions such as Île-de-France, Auvergne-Rhône-Alpes and Provence-Alpes-Côte d’Azur concentrate tertiary hospitals and private diagnostic hubs, capturing more than half of annual mammography volumes. These areas are also the earliest adopters of AI-assisted and 3-D systems, helped by stronger capital budgets and robust radiologist pools. By contrast, rural departments in Grand Est, Bourgogne-Franche-Comté and parts of Nouvelle-Aquitaine experience radiologist vacancy rates exceeding 25% and average travel times to screening centers above 40 minutes. Mobile units funded through regional grants have proven effective stopgaps, yet fixed-site deployment lags because facilities struggle to recruit personnel and finance maintenance contracts.

Overseas departments—including Réunion and Martinique—face logistics costs that inflate equipment pricing by 12-18% relative to mainland quotes, while maintenance delays can stretch beyond 30 days because spare parts transit through Paris. The health ministry’s 2024 cancer-strategy circular earmarked EUR 16.7 million for equipment upgrades in these territories, signaling an avenue for vendors willing to provide localized service footprints. Meanwhile, participation-rate volatility continues: Corsica’s 35% remains the lowest in the republic, yet recent outreach campaigns lifted Hérault from 38% in 2022 to 46% in 2024, illustrating that targeted interventions can move the needle. Overall, geographic imbalances create a mosaic of high-growth pockets within an otherwise nationally orchestrated market landscape.

Competitive Landscape

The supplier ecosystem combines three multinational heavyweights—GE Healthcare, Siemens Healthineers and Hologic—alongside mid-size European specialists such as Fujifilm, IMS Giotto, Planmed and Metaltronica. Top-three combined share approached 48% in 2024, while the top-six surpassed 72%, yielding a moderately concentrated structure that rewards product differentiation over price wars. French procurement rules favor multi-year service contracts, prompting vendors to bundle hardware, software, training and uptime guarantees. Siemens Healthineers’ EUR 55 million, 12-year value partnership with University Hospital Nantes exemplifies the shift from transactional sales to capacity-as-a-service models [3]Siemens Healthineers, “Value Partnership with University Hospital Nantes,” siemens-healthineers.com .

Innovation pipelines spotlight AI integration and dose-reduction. GE Healthcare’s Senographe Pristina Via introduced zero-click positioning that trims exam times by 18%, an attractive feature for throughput-driven diagnostic centers. Hologic collaborates with Bayer to commercialize contrast-enhanced mammography that may complement tomosynthesis for high-risk patients. Meanwhile, local AI firms such as Therapixel leverage domestic clinical-data access to refine algorithms attuned to French population characteristics, forging partnerships with both public hospitals and private imaging chains.

Barriers to entry remain formidable: ANSM clinical-data requirements, ISO-13485 compliance and the need for nationwide service coverage deter smaller foreign entrants. Nonetheless, specialized providers find niches—Metaltronica targets budget-sensitive buyers with modular digital systems, and iCAD focuses on software that improves quality control. With replacement cycles accelerating, incumbents that deliver seamless AI workflows, competitive financing and credible low-dose performance are positioned to solidify or expand share within the France Mammography Market.

France Mammography Industry Leaders

Fujifilm Holdings Corporation

Siemens AG

Planmed OY

Hologic Inc.

GE Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Lunit and VIDI Group signed a strategic alliance to deploy the Lunit INSIGHT MMG AI suite across more than 400 radiology sites and 1 200 physicians, covering nearly one-quarter of France’s private imaging market.

- November 2024: GE Healthcare unveiled the Senographe Pristina Via, emphasizing zero-click workflow and predictive maintenance features that promise 99% uptime.

- October 2024: Siemens Healthineers entered a 12-year, EUR 55 million value partnership with University Hospital Nantes encompassing tomosynthesis hardware, AI analytics and staff training.

- October 2024: Toutenkamion Group launched the next-generation Mammobile, a self-contained mobile screening clinic designed to operate in rural departments with limited power infrastructure.

France Mammography Market Report Scope

As per the scope of the report, mammography refers to a standard diagnostic and screening technique that is used to screen breast tissues to check the presence of a malignant tumor. The process involves the usage of low-energy X-rays for the early detection of breast cancer. France Mammography Market is Segmented by Product Type (Digital Systems, Analog Systems, Breast Tomosynthesis, and Other Product Types), End Users (Hospitals, Specialty Clinics, and Diagnostic Centers). The report offers the value (in USD million) for the above segments.

By Product Type

| Digital Systems |

| Analog Systems |

| Breast Tomosynthesis |

| Other Product Types |

By End User

| Hospitals |

| Specialty Clinics |

| Diagnostic Centers |

By Technology

| 2-D Digital Mammography |

| 3-D Digital Mammography |

| By Product Type | Digital Systems |

| Analog Systems | |

| Breast Tomosynthesis | |

| Other Product Types | |

| By End User | Hospitals |

| Specialty Clinics | |

| Diagnostic Centers | |

| By Technology | 2-D Digital Mammography |

| 3-D Digital Mammography |

Key Questions Answered in the Report

How big is the France Mammography Market?

The France Mammography Market size is expected to reach USD 129.78 million in 2026 and grow at a CAGR of 8.73% to reach USD 197.16 million by 2031.

Which product category holds the biggest share?

Digital Systems command 67.12% of 2025 revenue.

Who are the key players in France Mammography Market?

Fujifilm Holdings Corporation, Siemens AG, Planmed OY, Hologic Inc. and GE Healthcare are the major companies operating in the France Mammography Market.

Why is 3-D tomosynthesis adoption accelerating?

Regulatory endorsement and superior cancer-detection rates are driving hospitals to upgrade.

Page last updated on: