Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

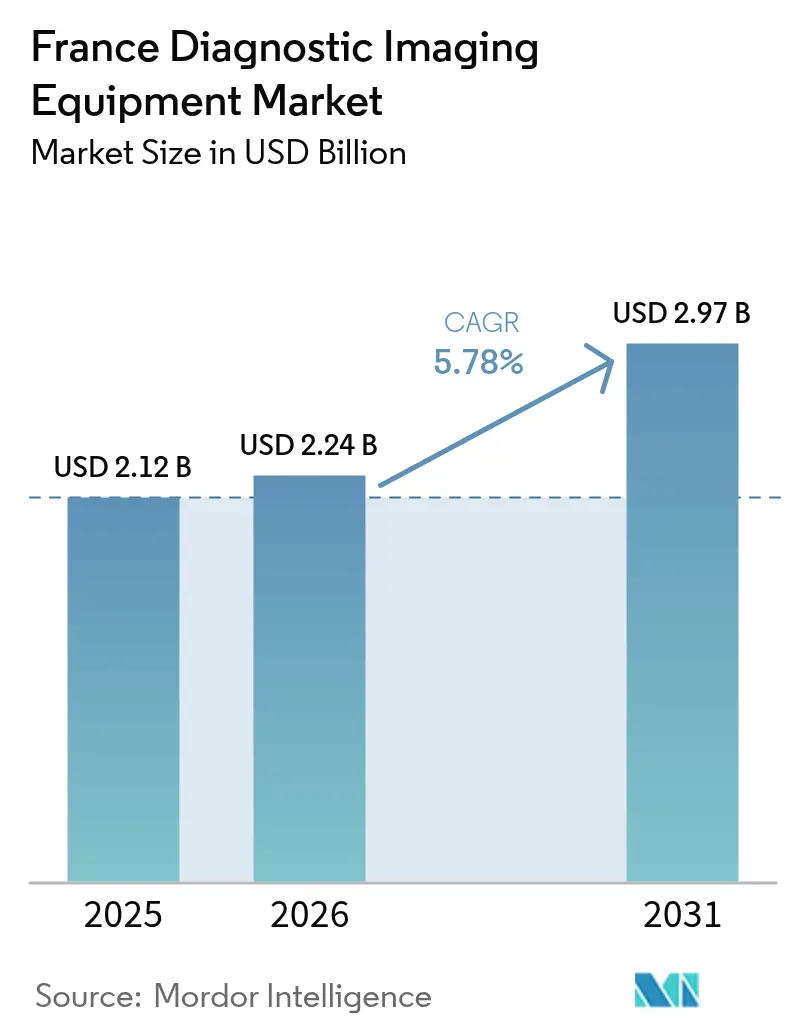

| Base Year Market Size (2025) | USD 2.12 Billion |

| Market Size (2026) | USD 2.24 Billion |

| Market Size (2031) | USD 2.97 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Diagnostic Imaging Equipment Market Analysis by Mordor Intelligence

The France diagnostic imaging equipment market size in 2026 is estimated at USD 2.24 billion, growing from 2025 value of USD 2.12 billion with 2031 projections showing USD 2.97 billion, growing at 5.78% CAGR over 2026-2031. This growth is bolstered by government funding, steady growth in healthcare spending, and increasing demand from an aging population. Capital allocation under the national EUR 7 billion health-innovation plan, including EUR 1.5 billion earmarked for artificial intelligence deployment, keeps equipment refresh cycles on track, even as public hospitals face budget deficits.[1]Source: Gouvernement français, “La France championne européenne en santé d’ici à 2030,” info.gouv.fr Structural shifts, such as the growth of outpatient care, the adoption of mobile imaging, and the integration of AI-assisted workflows, further strengthen demand signals across modalities, particularly MRI and connected ultrasound. Competitive intensity remains moderate; major multinationals leverage bundled service contracts, while domestic innovators target portable and AI-enabled niches to unlock rural and suburban opportunities

Key Report Takeaways

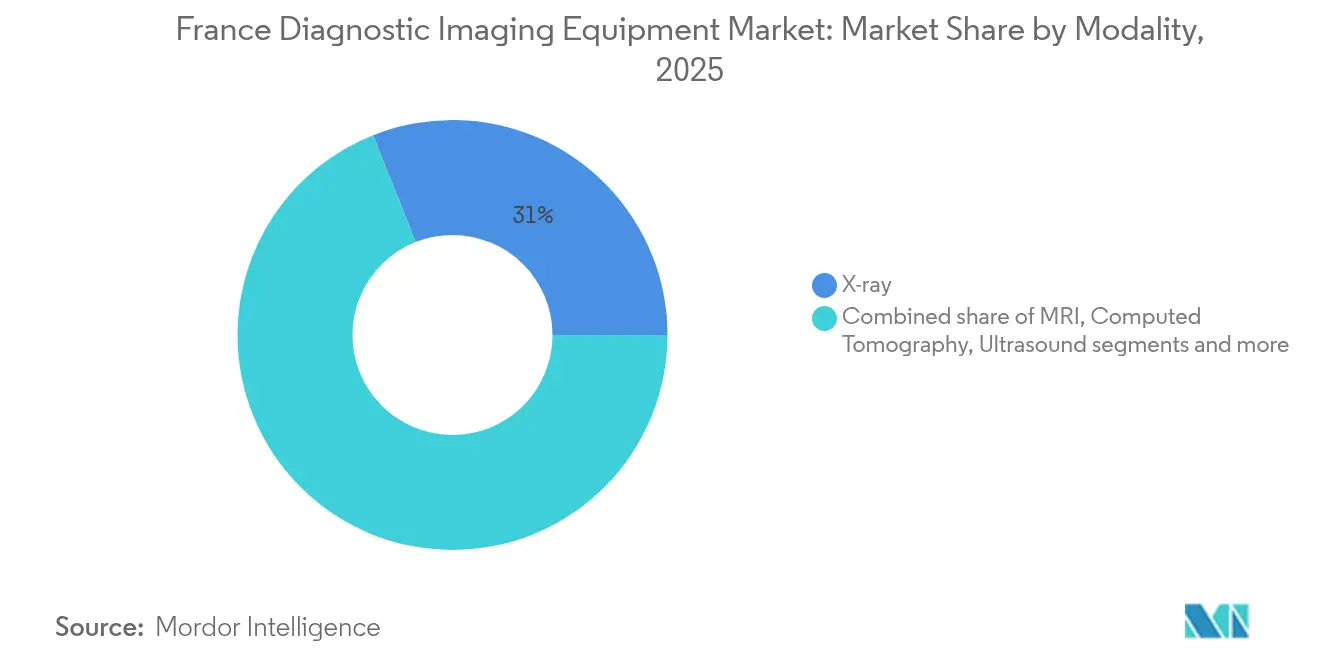

- By modality, X-ray systems led with 31.02% of France diagnostic imaging equipment market share in 2025; MRI is on course for a 6.73% CAGR through 2031.

- By portability, fixed systems accounted for 81.74% of the France diagnostic imaging equipment market size in 2025, whereas mobile/portable systems are forecast to expand at a 7.02% CAGR between 2026-2031.

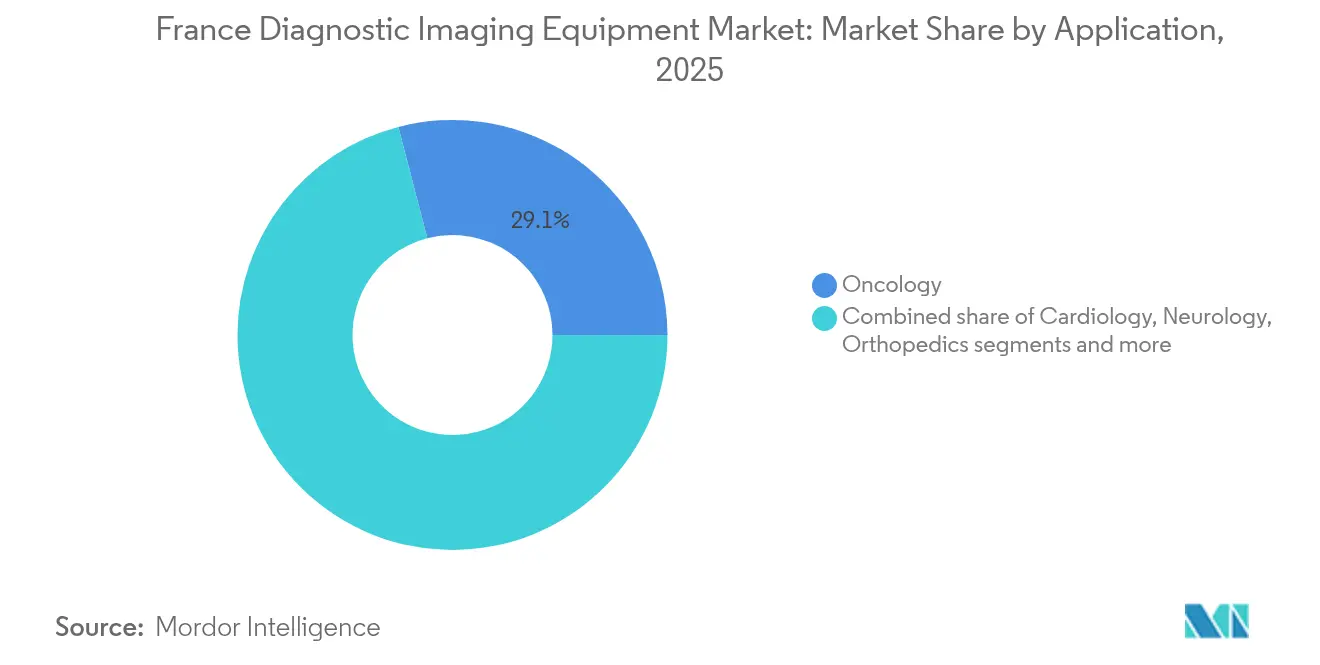

- By application, oncology captured 29.05% of France diagnostic imaging equipment market share in 2025; cardiology shows the highest projected CAGR at 7.18% through 2031.

- By end-user, hospitals held a 67.18% revenue share in 2025; diagnostic centers recorded the fastest growth, at a 6.63% CAGR, from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Diagnostic Imaging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases & aging population | +1.8% | National, higher in rural and southern regions | Long term (≥ 4 years) |

| Government investment to modernize hospital imaging capacity | +1.2% | National, prioritizing public hospital networks | Medium term (2-4 years) |

| Steady growth in national healthcare spending and equipment replacement programmes | +0.9% | National, focused on public sector facilities | Medium term (2-4 years) |

| Shift toward outpatient and ambulatory imaging centers boosts system installations outside hospitals | +0.7% | Urban and suburban areas | Short term (≤ 2 years) |

| Emphasis on early, value-based diagnosis increases utilization rates | +0.6% | National, early adoption in academic medical centers | Medium term (2-4 years) |

| Integration of digital health and cloud-based image management drives demand for connected modalities | +0.4% | National, led by Île-de-France and major metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases & Aging Population

Chronic disease prevalence continues to rise, pushing imaging volumes across France. Healthcare reimbursements for diabetes, cardiovascular conditions, and cancer reached EUR 167 billion in 2024, making imaging a frontline diagnostic tool. An older demographic intensifies complexity, demanding AI-assisted protocols to detect multiple pathologies in a single scan. Survival gaps tied to travel distance—up to 10% lower five-year cancer survival for patients located farther from referral centers—spotlight the clinical value of locally available scanners. Limited radiologist supply heightens reliance on intelligent image triage, while mobile units help bridge urban–rural access disparities. Collectively, these factors anchor long-term growth in the France diagnostic imaging equipment market.

Government Investment to Modernize Hospital Imaging Capacity

France’s EUR 7 billion health-innovation program identifies diagnostic imaging as a modernization priority. Funds channel toward large-scale equipment renewals, AI pilots, and specialized ventures such as Institut Curie’s EUR 37 million FLASH-radiotherapy platform. The push responds to bottlenecks: annual mechanical-thrombectomy procedures plateaued at 7,500 amid staffing and scanner shortages. Vendor–provider “value partnerships,” like Siemens Healthineers’ EUR 60 million, 12-year contract with University Hospital Nantes, illustrate a new procurement logic that bundles hardware, service, and lifecycle upgrades.[2]Source: Siemens Healthineers, “Value Partnership with University Hospital Nantes,” siemens-healthineers.com Such financing mechanisms accelerate deployments while containing upfront capital strain, underpinning the France diagnostic imaging equipment market expansion.

Steady Growth in National Healthcare Spending and Equipment Replacement Programmes

The 2025 Social-Security Financing Law lifts the national health-expenditure target to EUR 265.9 billion, a 3.4% uptick that safeguards hospital operating budgets. Yet equipment depreciation outpaces new purchases, leaving an investment gap estimated at EUR 5.6 billion. Replacement demand therefore skews toward cost-efficient, energy-saving scanners that promise lower total-ownership costs. Manufacturers respond with helium-free MRI, dose-optimized CT, and service-inclusive contracts, reinforcing steady procurement cycles and propelling the France diagnostic imaging equipment market.

Shift Toward Outpatient and Ambulatory Imaging Centers Boosts System Installations Outside Hospitals

Diagnostic imaging centers grow rapidly as patients seek faster appointments and hospitals redirect routine studies to decongest workloads. The segment’s 6.85% CAGR rests on investor-backed expansion, with private funds now owning 15-20% of imaging practices. Mobile X-ray and robotic ultrasound solutions deliver hospital-grade quality in community settings, validated by studies showing equivalent diagnostic accuracy and reduced time-to-treatment. These trends diversify equipment placements, expand procurement avenues, and stimulate software demand for remote reading, all supportive of the France diagnostic imaging equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ionizing-radiation safety concerns | −0.8% | National, stricter in densely populated areas | Long term (≥ 4 years) |

| High capital & maintenance cost of advanced systems | −1.1% | National, greater impact on smaller facilities | Medium term (2-4 years) |

| Lengthy CE-mark & reimbursement approval timelines | −0.6% | EU-wide, affects market entry timing | Short term (≤ 2 years) |

| Ongoing shortage of trained radiologists and technologists | −1.3% | National, acute in rural and underserved regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ionizing-Radiation Safety Concerns

The January 2025 creation of the Autorité de sûreté nucléaire et de radioprotection consolidates nuclear-safety oversight and intensifies inspection frequency for 60,000 radiation-emitting devices nationwide. Stricter dose-reference levels prompt facilities to favor low-dose CT, iterative-reconstruction software, or MRI alternatives. Vendors develop visual and acoustic dose-alert systems showcased at AP-HP’s APinnov 2025 event. While safety vigilance limits indiscriminate CT and X-ray growth, it also boosts demand for next-generation scanners with automated exposure control, mitigating, rather than halting, expansion of the France diagnostic imaging equipment market.

Ongoing Shortage of Trained Radiologists and Technologists

France faces persistent personnel deficits; AI modeling indicates automated assistance could cut reading workloads by up to 53%. Rural departments endure the heaviest constraints, fueling mobile-scanner deployments and tele-radiology networks. Nuclear-medicine expansion strains capacity further, as 60% of procedures are expected to involve therapeutic tracers within a decade, yet subspecialty training pipelines remain limited. This human-resource bottleneck tempers volume growth yet simultaneously accelerates AI integration, both a restraint and an innovation engine within the France diagnostic imaging equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: X-ray Leads While MRI Gains Momentum

X-ray systems dominated 2025 with 31.02% France diagnostic imaging equipment market share, underscoring their ubiquity in emergency, chest, and musculoskeletal evaluations. The segment’s growth moderates amid radiation-dose scrutiny, but upgrades to digital detectors sustain replacement demand. MRI, propelled by helium-free magnet technology that slashes annual operating costs, exhibits a robust 6.73% CAGR, the fastest in the landscape. The France diagnostic imaging equipment industry benefits from Philips BlueSeal and other zero-boil-off platforms that simplify siting and cut maintenance. CT maintains relevance for trauma and oncology staging, where AI-based image reconstruction reduces dose exposure. Ultrasound innovation—exemplified by Samsung’s acquisition of Sonio—adds deep-learning capabilities for obstetric diagnostics.

In nuclear imaging, theranostic pathways drive SPECT/CT and PET/CT replacements as oncology centers pair diagnostics with targeted radionuclide therapy. Mammography remains vital to national screening programs, though novel magnetic-marker navigation shows promise in lowering re-excision rates for breast-cancer surgery. Overall, modality diversification ensures steady equipment cycles, reinforcing the France diagnostic imaging equipment market’s value trajectory.

By Portability: Fixed Units Anchor Capacity, Mobile Systems Outpace Growth

Fixed scanners retained 81.74% of the 2025 France diagnostic imaging equipment market size, reflecting hospital dependence on high-throughput, full-featured rooms. Widespread picture-archiving integration, power requirements, and advanced technologist workflows continue to favor stationary installations for complex imaging. However, portable systems record 7.02% CAGR, tapping unmet rural and elderly-care needs. Studies verify equal diagnostic accuracy when chest radiographs are performed at bedside, cutting transfer time and potential complications. DMS Group’s Onyx mobile radiology platform exemplifies local manufacturer momentum, lifting company sales 9% to EUR 46.1 million in 2024.

COVID-19 reinforced clinical acceptance of point-of-care scanning, spurring permanent workflow changes. Battery life gains, AI on-device analytics, and 5G connectivity now allow real-time remote consultation, making mobility central to future procurement. These advances shape a two-tier market where fixed rooms handle high-complexity imaging and mobile units ensure proximity care, together enlarging the France diagnostic imaging equipment market.

By Application: Oncology Dominates, Cardiology Accelerates

Oncology retained 29.05% France diagnostic imaging equipment market share in 2025, supported by the National Cancer Institute’s early-detection campaigns and high PET-CT demand for staging. Cardiology charts a 7.18% CAGR as demographic aging lifts cardiovascular case loads; CT angiography and echocardiography gains drive purchases. Precision medicine widens imaging’s clinical scope: approval of 177Lu-PSMA therapy underscores the need for sophisticated nuclear-imaging protocols.

Neurology benefits from ultra-high-field MRI, which enhances cortical-microstructure visualization for neurodegenerative research. Orthopedics orders grow on sports injury screening and aging joint replacements, favoring low-dose 3D systems. Collectively, diversified specialty needs secure a stable pipeline of orders throughout the French diagnostic imaging equipment market.

By End-User: Hospitals Still Rule, Diagnostic Centers Rise

Hospitals accounted for 67.18% of revenue in 2025, operating the broadest modality mix under emergency and inpatient mandates. Budget constraints spur preference for multi-year service contracts that bundle upgrades and training. Diagnostic imaging centers, expanding at 6.63% CAGR, cater to outpatient demand for rapid slots and specialized expertise. Investor-backed networks leverage economies of scale and cloud reading to boost utilization, reshaping competitive dynamics within the France diagnostic imaging equipment market.

Research institutes, veterinary clinics, and mobile providers comprise the remaining share, though their collective volume is trending upward as novel applications—animal oncology imaging, field-based trauma assessment—gain traction. Private clinics posted EUR 362 million in net results for 2024, yet one-third remain loss-making, creating an incentive to adopt workflow-optimizing scanners that improve throughput.

Geography Analysis

Regional disparities define equipment distribution across France. Île-de-France, the nation’s wealth engine, paradoxically reports lower healthcare access indices than certain southern regions as population density exceeds facility capacity. Rural territories confront cardiology wait-times surpassing 42 days, doubling the urban benchmark, highlighting diagnostic inequality. Cancer-survival divergence—up to 10% lower five-year survival for patients distant from reference centers—further validates the need for localized scanners. Government strategies target balanced development. France 2030 funds subsidize equipment in underserved départements, while tele-radiology links extend specialist coverage across multi-site hospital groups. The Loire-Atlantique imaging network, comprising 13 public hospitals, shows regional pooling can maximize utilization. Mobile deployments plug remaining gaps, allowing bedside exams in community nursing homes or emergency triage at local clinics. Such initiatives ensure the France diagnostic imaging equipment market expands beyond metropolitan hubs, reinforcing national goals for equitable care.

Cloud-based enterprise imaging accelerates geographic coverage. Philips’ European launch of HealthSuite Imaging grants radiologists secure access to studies regardless of location, supporting workload sharing among facilities. AI-powered triage funnels complex cases to academic centers while rural technologists handle routine protocols, harmonizing quality standards. Over the forecast horizon, policy, technology, and investment converge to mitigate regional supply-demand mismatches, driving inclusive growth across the France diagnostic imaging equipment market.

Competitive Landscape

Global majors preserve brand recognition and service footprints, yet competitive contours shift toward partnership-driven models. Siemens Healthineers, Philips, and GE HealthCare collectively manage a majority of high-end modalities in tertiary centers; their contracts increasingly bundle uptime guarantees, staff training, and AI upgrades. Philips’ cloud-imaging expansion differentiates through enterprise-wide workflow integration, enabling multi-site reading and fostering customer stickiness. GE HealthCare pursues sustainability upgrades and dose-optimized CT to satisfy emerging regulatory standards GE.

Domestic innovators fill technology gaps. Guerbet SA applies contrast-media leadership to co-develop AI-supported protocols for low-dose liver imaging, enhancing local credibility. Start-ups such as Sonio, now a Samsung subsidiary, add fetal-anomaly detection software to ultrasound consoles, underscoring the strategic importance of AI assets.

Financial investors intensify consolidation among outpatient centers, injecting capital for multi-site expansion and advanced modality purchases. While this boosts equipment demand, it prompts debate over medical governance and cost control. Vendors attuned to this duality—offering flexible financing and regulatory-compliant AI stand to secure long-term market shares within the France diagnostic imaging equipment market.

France Diagnostic Imaging Equipment Industry Leaders

FUJIFILM Holdings Corporation

Koninklijke Philips N.V.

GE HealthCare

Siemens Healthineers AG

Canon Medical Systems Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The French government created the Autorité de sûreté nucléaire et de radioprotection (ASNR), merging IRSN and ASN to strengthen radioprotection oversight for imaging devices.

- November 2024: Paris Brain Institute installed a 7T MAGNETOM Terra.X MRI, funded by Richard Mille and the Paris Region, enhancing national neuro-imaging research capacity.

- September 2024: Sonio Detect received CE marking, allowing nationwide release of its AI ultrasound-image-quality software, now backed by Samsung’s acquisition.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the France diagnostic imaging equipment market as the yearly value of new, human-health devices that create two- or three-dimensional anatomical images through X-ray, ultrasound, computed tomography, magnetic resonance, nuclear imaging, fluoroscopy, and dedicated mammography systems.

Scope exclusion: revenues generated by imaging service provision, software-only visualization tools unbundled from hardware, and accessories such as contrast media are outside the market boundary.

Segmentation Overview

- By Modality

- MRI

- Computed Tomography

- Ultrasound

- X-Ray

- Nuclear Imaging

- Fluoroscopy

- Mammography

- By Portability

- Fixed Systems

- Mobile / Portable Systems

- By Application

- Cardiology

- Oncology

- Neurology

- Orthopedics

- Gastroenterology

- Gynecology

- Other Applications

- By End-User

- Hospitals

- Diagnostic Centers

- Other End-Users

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed radiologists, biomedical engineers, modality product managers, and procurement heads across public-sector hospitals, large private clinic chains, and independent imaging centers spanning Ile-de-France, Auvergne-Rhone-Alpes, and Nouvelle-Aquitaine. Insights on typical device lifetimes, average selling prices, and modality substitution trends helped us validate assumptions surfaced during desk work.

Desk Research

Public datasets from Sante Publique France, INSEE health-expenditure files, and the Ministry of Solidarity and Health reveal annual procedure volumes, hospital investment grants, and equipment replacement cycles. Trade body releases, such as those of the European Coordination Committee of the Radiological, Electromedical and Healthcare IT Industry, complement customs shipment records visible on Volza and patent activity screened through Questel. Company 10-Ks, investor decks, and reputable medical journals round out our desktop evidence base. The sources listed are illustrative only; several other open publications and proprietary feeds were consulted for cross-checks and clarifications.

Market-Sizing & Forecasting

A top-down construct converts procedure counts and modality mix into installed-base needs, followed by roll-forward replacement and expansion factors. Sampled bottom-up checks, supplier shipment tallies, and channel margin views anchor the totals before adjustments. Key variables include CT scans per thousand inhabitants, radiologist density, average replacement age, private-sector cap-ex ratios, reimbursement tariff shifts, and the Health Innovation Plan's grant disbursal timeline. Forecasts draw on a multivariate regression that links device demand to chronic disease prevalence and public capital budgets, with scenario overlays from our expert panel when policy or macro indicators deviate. Gap areas in bottom-up evidence, such as privately negotiated ASPs, are bridged with mid-point ranges validated by at least two respondent confirmations.

Data Validation & Update Cycle

Outputs undergo variance checks against historical growth corridors, modality benchmarks, and external sentiment signals. Two-level analyst reviews precede release. The report is refreshed once every twelve months, with interim revisions triggered by funding announcements, major product launches, or regulatory shifts.

Why Mordor's France Diagnostic Imaging Baseline Commands Reliability

Published values often diverge because firms select different equipment mixes, convert currencies on varied dates, or project from limited site audits.

Our disciplined scoping, yearly refresh cadence, and dual-path modeling minimize those pitfalls.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.12 B (2025) | Mordor Intelligence | - |

| USD 1.73 B (2025) | Regional Consultancy A | excludes mobile X-ray and fluoroscopy, applies conservative ASP deflators |

| USD 1.26 B (2024) | Trade Journal B | reports only digital modalities and omits public-sector retrofit tenders |

| USD 2.50 B (2025) | Global Consultancy C | blends equipment and service revenue, assumes faster replacement every five years |

The comparison shows that methodology choices on scope breadth, price inflators, and refresh rates explain most gaps. By anchoring values to verified installation needs and openly documenting each assumption, Mordor Intelligence delivers a balanced, decision-ready baseline that clients can trace and reproduce with confidence.

Key Questions Answered in the Report

Which imaging modality is most widely used across French hospitals today?

Digital X-ray remains the workhorse in emergency and primary-care settings due to its speed, versatility, and relatively low radiation dose.

What is the biggest technology trend shaping new equipment purchases?

Hospitals and outpatient centers now prioritize scanners with built-in AI for automated triage, dose optimization, and workflow orchestration to counteract staff shortages.

How are government policies influencing vendor strategies in France?

Value-based procurement rules tied to the national health-innovation plan push manufacturers toward long-term service packages that bundle hardware, training, and software upgrades.

Why is mobile imaging attracting growing investor interest?

Portable MRI, CT, and X-ray units allow providers to reach rural communities and long-term-care facilities without building new departments, improving access while keeping capital outlays manageable.

What are providers doing to address radiation-safety concerns?

Facilities are adopting low-dose protocols, iterative-reconstruction software, and visual dose-alert systems to comply with stricter oversight from the new radioprotection authority.

How is financial consolidation affecting independent imaging practices?

Private-equity ownership is introducing stronger capital backing for technology refreshes but also heightens scrutiny over clinical governance and physician autonomy.

Page last updated on: