Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

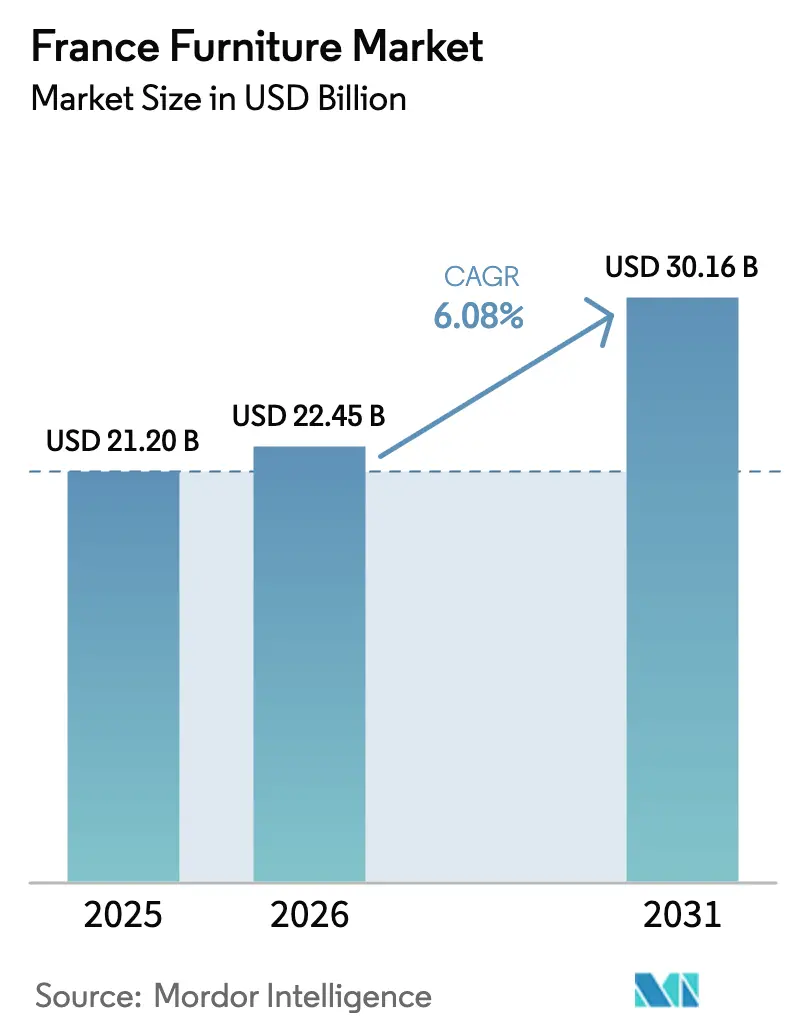

| Base Year Market Size (2025) | USD 21.20 Billion |

| Market Size (2026) | USD 22.45 Billion |

| Market Size (2031) | USD 30.16 Billion |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Furniture Market Analysis by Mordor Intelligence

The France Furniture Market size was valued at USD 21.20 billion in 2025 and is estimated to grow from USD 22.45 billion in 2026 to reach USD 30.16 billion by 2031, at a CAGR of 6.08% during the forecast period (2026-2031).

Product design and material selection now converge around circularity, with certified wood, recycled steel, and advanced polymers gaining presence in kitchen, bedroom, and office applications under reinforced EPR rules that change cost curves as well as brand positioning. The regulatory architecture tightens in parallel with France's AGEC law, renewed through 2029 for Ecomaison, which mandates that public purchasers acquire 20% second-hand office furniture and 15% incorporating recycled feedstock, percentages that escalate to 25% each by 2030. The net effect is a France furniture market that grows through disciplined omnichannel models, product transparency, and renovation-linked spending rather than pure cycle momentum, creating balanced opportunities for scale retailers and premium makers centered on provenance.

Key Report Takeaways

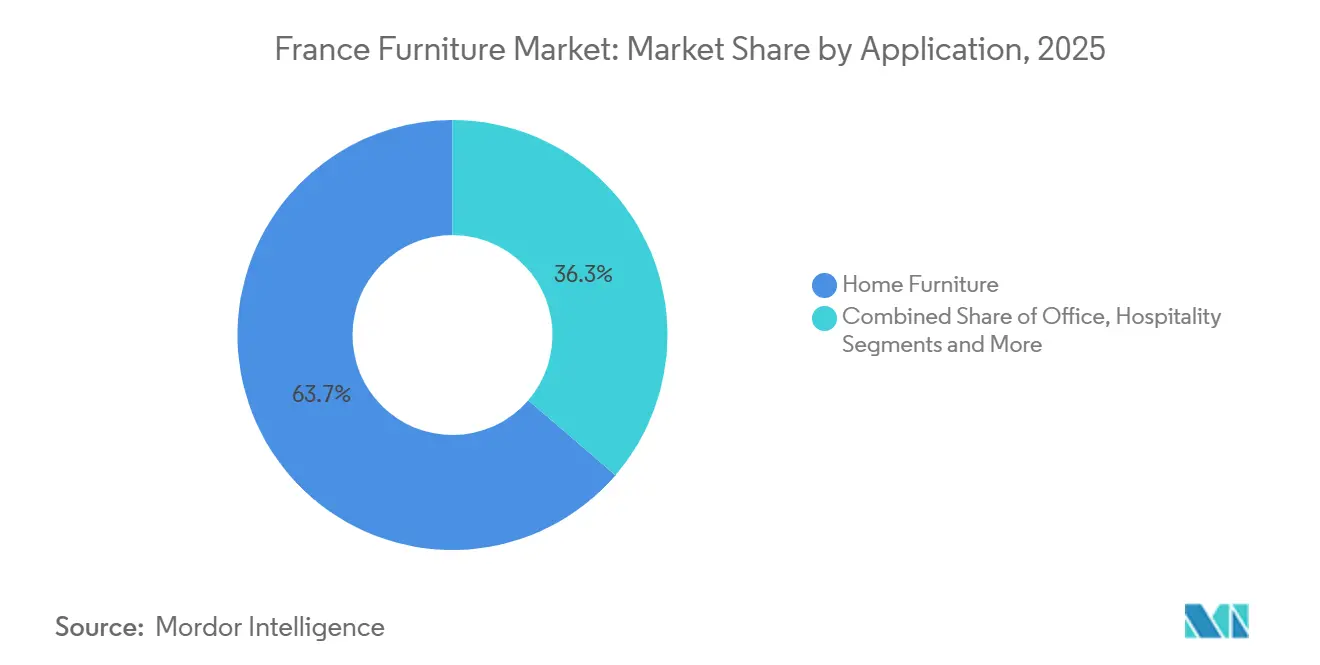

- By application, Home Furniture led with 63.7% of the total market size by application in 2025 and is forecast to expand at a 6.28% CAGR, reflecting resilient spending on sofas, beds, storage, and outdoor integrations that upgrade daily living environments.

- By material, Wood held a 56.8% market share in 2025, while Plastic & Polymer recorded the fastest growth at a 6.62% CAGR due to recycled composites and bio-based formulations aligned with EPR incentives.

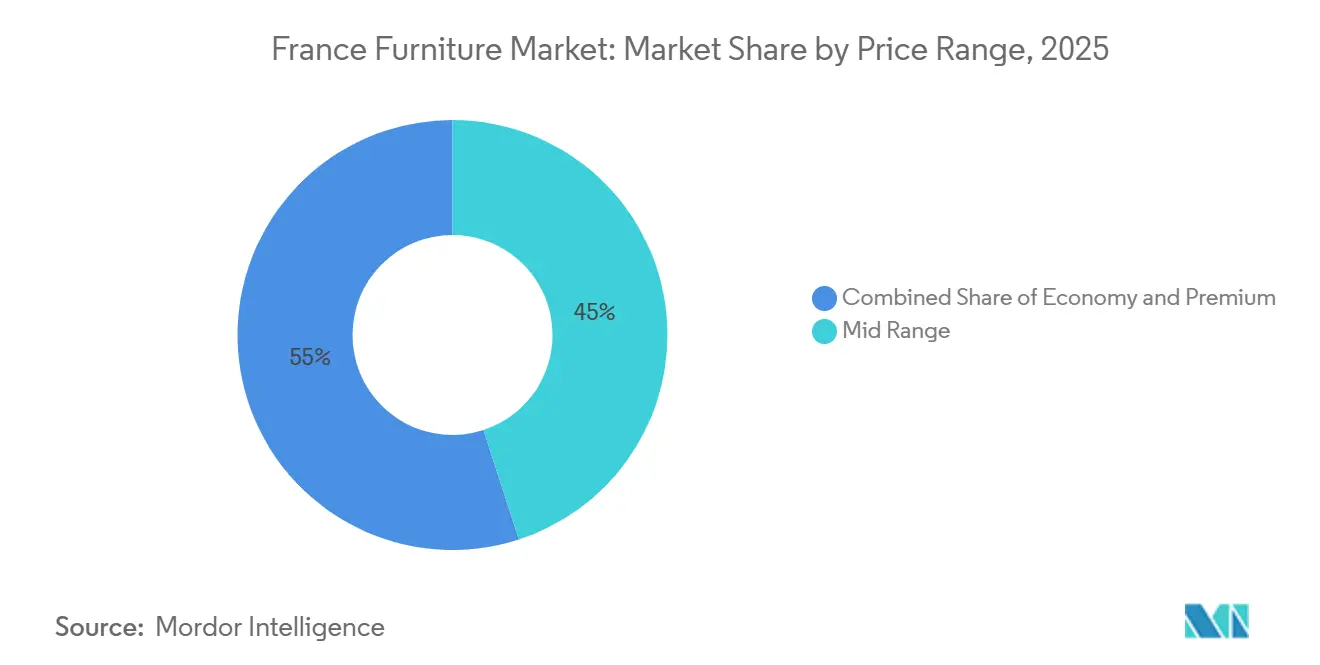

- By price range, the Mid-Range tier accounted for 45.0% in 2025, while Premium advanced at a 6.11% CAGR, supported by demand for Made in France and certified materials.

- By distribution channel, B2C/Retail commanded 70.0% of sales in 2025, while Online sub-channels posted the fastest trajectory at a 7.23% CAGR as AR tools and logistics upgrades convert digital discovery into fulfillment.

- By geography, Île-de-France captured 29.4% of market share in 2025 and posted the fastest growth at a 6.84% CAGR, reflecting premium residential projects and large-scale office retrofits anchored in La Défense.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward E-commerce & Omnichannel Retailing | +1.2% | Global, strongest in Île-de-France and urban cores, with spillover to secondary cities through dark-store logistics | Medium term (2-4 years) |

| Residential Remodeling Boom Amid Energy-Efficient Retrofits | +1.5% | National, with early gains in Île-de-France, Auvergne-Rhône-Alpes, Nouvelle-Aquitaine | Medium term (2-4 years) |

| Hybrid Work Model Fueling Home-Office Furniture Demand | +0.9% | Île-de-France, Auvergne-Rhône-Alpes, Provence-Alpes-Côte d'Azur | Short term (≤ 2 years) |

| Public Incentives for Bio-Based Manufacturing & Low-Carbon Materials | +0.7% | National, concentrated in regions with timber clusters, including Nouvelle-Aquitaine and Grand Est. | Long term (≥ 4 years) |

| AI-Powered Design/Configuration Platforms | +0.5% | Île-de-France and Auvergne-Rhône-Alpes, with early adopters in tech-forward retail | Medium term (2-4 years) |

| Reuse/Refurbishment Marketplaces Accelerating the Circular Economy | +0.8% | National, Île-de-France leads with urban collection infrastructure and ESS networks across all regions. | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward E-commerce & Omnichannel Retailing

Digital furniture revenue in France reached around USD 4.07 billion (EUR 3.5 billion) in 2025 and accounted for 24% of domestic sales, highlighting structural online traction that now integrates showrooms and logistics nodes for faster click-and-collect and home delivery flows. Retailers scale augmented reality and configuration tools to support modular planning, reduce prototyping time, and convert discovery into orders with fewer post-sale changes or returns [1]Source: imagine.io, “AI Accelerates Furniture Prototyping Timelines,” imagine.io, imagine.io . Omnichannel leaders rely on showrooms as conversion engines because many buyers still prefer tactile validation of upholstery, finishes, and ergonomics before finalizing higher-ticket items. Last-mile costs and reverse logistics remain material for bulky formats, so operators are piloting centralized returns and micro-fulfillment hubs to stabilize unit economics at scale. As compact store formats extend coverage into secondary cities and strengthen in-store support for online orders, the France furniture market broadens its reach and carries a consistent service model across regions.

Residential Remodeling Boom Amid Energy-Efficient Retrofits

RE2025 thermal rules are channeling budgets into energy upgrades that support sustained demand for fitted kitchens, bathroom cabinetry, and built-in storage during 2026. The shift toward renovation offsets weak new-build cycles and improves throughput for modular products that adapt to older apartments and complex room geometries in major cities. EPR eco-modulation grants fee bonuses for recycled content and certified wood, which reduces net cost for compliant producers and encourages broader adoption of circular materials at an industrial scale. The tactical opportunity emerges in pre-packaged retrofit bundles—suppliers bundling certified low-VOC cabinetry with installation labor and take-back logistics for obsolete units—that compress decision fatigue and align with circular-economy mandates requiring distributors with sales areas exceeding 200 m² to offer free one-for-one furniture removal[2]Source: Ecomaison, “Furniture 2025 Eco-modulated Rates,” Ecomaison, ecomaison.com .

Hybrid Work Model Fueling Home-Office Furniture Demand

Hybrid work patterns have stabilized and are driving corporate retrofits for flexible collaboration zones, lounge seating, and height-adjustable desks that balance onsite rotations with productivity needs. Households continue to upgrade ergonomic seating and compact desks for multi-purpose rooms as online channels facilitate assortment discovery and configuration support. Major metropolitan areas, including Paris and Lyon, sustain steady contract orders as office reconfiguration remains a multi-year program that staggers categories and budgets. Manufacturers are answering with integrated power, cable management, and modular lounge formats that fit smaller zones without compromising durability or comfort. These patterns increase replacement cycles in both office and home settings and support incremental value capture in the France furniture market as hybrid routines embed across sectors.

Public Incentives for Bio-Based Manufacturing & Low-Carbon Materials

France's position as the world's leading linen producer and Europe's foremost hemp cultivator underpins a strategic pivot toward bio-sourced composites, amplified by Ecomaison's eco-modulation framework that rewards manufacturers incorporating post-consumer recycled content with financial bonuses of USD 47 per tonne for wood exceeding 35% thresholds and USD 588 per tonne for textiles. The policy mix supports broader adoption of certified timber, recycled steel, and advanced polymers in kitchens, bedrooms, and contract settings, which narrows cost gaps with virgin inputs. EU work on Ecodesign for Sustainable Products is also advancing design-for-disassembly and product passport requirements, which further incentivize transparent materials and standardized fastening systems across product families. As these measures scale, the France furniture market consolidates an early lead in sustainable design choices and builds competitive moats around traceability and reparability claims.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Timber & Plywood Prices Tied to EUDR Traceability | -1.1% | National, acute in Nouvelle-Aquitaine after storm damage, with effects cascading to all wood-reliant segments | Short term (≤ 2 years) |

| Competition from Low-Cost Asian Imports | -0.9% | National, most pronounced in mass-market B2C channels and online pure-players | Short term (≤ 2 years) |

| Fragmented Domestic Production Capacity Limiting Scale Efficiencies | -0.6% | National, manufacturing is dispersed across more than 1,500 entities, which hinders capex pooling. | Long term (≥ 4 years) |

| Slow Building-Permit Cycle Dampening New-Build Furniture Sales | -0.8% | National, particularly Hauts-de-France, Île-de-France, and Provence-Alpes-Côte d’Azur where dense zoning adds complexity | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Timber & Plywood Prices Tied to EUDR Traceability

The European Deforestation Regulation becomes enforceable on December 30, 2025, for larger operators and on June 30, 2026, for smaller firms, and it requires plot-level geolocation to verify deforestation-free sourcing of at-risk commodities like timber and wood panels. Importers and manufacturers must build verification workflows and maintain digital records for multiple years, which adds operating cost for SMEs that lack in-house compliance or GIS systems. The transition period coincides with regional supply strain after 2024 storm damage in Nouvelle-Aquitaine, which increased sourcing pressure for plywood and spurred some substitution to non-wood materials in targeted categories. Certified wood supply reduces risk of penalties and offers shorter lead times than distant imports for many buyers restructuring their chains in the France furniture market. Compliance timing and raw-material recovery shape kitchen and office timelines in 2026 as procurement programs re-weight certified domestic inputs.

Competition from Low-Cost Asian Imports

Price pressure is elevated in B2C channels as low-cost imports expand in mass retail and online formats, and this dynamic compresses margins for mid-market assortments. Operators with cross-border models reduce landed costs and complicate enforcement for environmental and compliance rules in fragmented customs regimes. Domestic producers respond with shorter lead times, customization, and certification footprints aligned with EPR to differentiate from economy imports. The result is polarization in the France furniture market where value share concentrates in premium and bespoke labels, while volume shifts remain pronounced at entry price points. Industry bodies advocate tighter border harmonization to limit non-compliant inflows and to protect the integrity of sustainability standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Hybrid Rhythms Recalibrate Home-Versus-Office Mix

Home Furniture captured 63.7% of France furniture market share in 2025 and is advancing at 6.28% through 2031 as living rooms absorb work functions, small-format storage solves space limits, and outdoor settings extend use seasons for terraces and balconies. Buyers emphasize sofas, beds, and storage with stronger preferences for repairability and certified materials, and these choices align with EPR incentives that reward durable construction and recycled content. Functional crossovers between living and working zones sustain demand for height-adjustable desks and ergonomic seating that visually blend into home settings without appearing strictly professional. As households rely more on online tools for planning and configuration, showrooms play a complementary role for final confirmation on fabrics, finishes, and fit in tight spaces. In contract settings, office retrofits emphasize collaborative zones and soft seating to support hybrid routines and to compress individual desk ratios while preserving comfort and flexibility.

The broader application mix continues to evolve as hospitality upgrades outdoor seating and dining formats, education refreshes classrooms with mobile desks and stackable seating, and healthcare integrates materials that meet hygiene and durability standards without compromising comfort. Project cycles vary by funding and permitting status, so suppliers with modular product systems and reliable lead times capture more of the staggered procurement in 2026. Renovation incentives keep replacement cabinetry and storage on a steady footing, which supports volumes during uneven new-build trends across metropolitan regions. The France furniture market benefits when application lines blur, because residential buyers procure office items for home use and commercial programs adapt domestic comfort cues in lobbies and collaboration zones. This interplay supports steady growth in the application mix with a tilt toward multi-use products that fit both living and working needs.

By Material: Wood Dominates, Yet Polymer Innovation Accelerates

Wood held a 56.8% share in 2025 as buyers value tactile warmth, repairability, and the aesthetic range achieved through veneers and solid wood selections across kitchens, bedrooms, and living room storage. EUDR compliance pushes procurement toward certified sources and domestic mills that streamline traceability and reduce transit uncertainty during the early enforcement period. Metal remains a mainstay in contract seating and storage, where powder-coated steel and aluminum frames meet performance specifications and benefit from established recycling streams. Recycled and certified content earns fee reductions within the EPR framework, which lifts economic viability for alternative materials that previously carried a price premium without compliance benefits.

The France furniture market size associated with next-generation polymers is positioned to expand with a 6.62% CAGR as manufacturers use recycled plastics and bio-sourced inputs in seating, panels, and soft goods aligned with repairability and circularity targets. Glass, stone, and neo-composites hold niche shares and appear in premium and design-forward projects where aesthetics and durability offset higher mass and cost. As product passports and design-for-disassembly advances under the EU’s 2025–2030 plan, fasteners and substrates are getting standardized and labeled so materials can be identified and recovered at the end of life. Domestic buyers place a premium on reliable sourcing and lead-time control, which reinforces wood’s leadership while enabling faster adoption of recycled polymers that face fewer traceability frictions than importing mixed-wood inputs. The combined effect is a more balanced material mix with certified wood at the core and fast-growing polymer alternatives gaining share in segments where durability, weight, and logistics costs matter most.

By Price Range: Mid-Range Anchors, Premium Gains Via Provenance

Mid-Range accounted for 45.0% of sales in 2025, signaling that buyers seek durability and sensible pricing that extends replacement cycles while keeping total ownership costs predictable. This tier often includes standardized modular kitchens and living-room storage that combine accessible pricing with installation options and reliable after-sales support across national retail chains. Premium advanced at a 6.11% CAGR as buyers pay for Made in France provenance, certified materials, and exclusive collaborations that reinforce long-run brand equity. Willingness to pay more for local and certified content supports design-forward ranges with longer warranties and high service levels for delivery and installation across urban cores.

Segment polarization persists in 2026 as inflation fatigue and financing costs still influence the value tier, while wealth effects stabilize premium budgets in Île-de-France and coastal regions. The premium tier absorbs traceability and compliance costs more easily, which aligns with AGEC rules and emerging EU standards and creates a branding moat around sustainability practices. Mid-Range retailers respond with private-label pushes and modular assortments that protect margins while offering configurability seen in higher-priced lines. The France furniture market thus spreads across both stability from the core mid-tier and growth at the top, as provenance and lower-risk sourcing draw consistent demand. Over the forecast period, service models like trade-in and repair can support each price tier by extending product life and by smoothing spend across cycles.

By Distribution Channel: Online Sprints, Specialty Stores Adapt

B2C/Retail channels held 70.0% of 2025 distribution, and Online sub-channels are the fastest growth pocket at a 7.23% CAGR as AR-enabled planning and upgraded logistics remove friction across the order-to-delivery path. Online revenue around EUR 3.5 billion and a 24% share in 2025 underscores a deep shift in discovery and configuration stages that now move seamlessly between mobile, web, and store interactions. Specialty Furniture Stores adapt by merging digital configuration with in-store validation and by using showrooms as service centers that reduce returns and increase attachment rates for delivery and installation. DIY home centers and regional workshops retain roles at opposite ends of the spectrum, with DIY catering to self-install buyers and workshops executing bespoke commissions that emphasize local sourcing and repairability. The France furniture market favors models that standardize customer journeys and maintain consistent service expectations across dense urban cores and smaller cities now covered by compact store formats.

Returns and last-mile costs remain prominent in bulky categories, so large operators are piloting centralized returns and expanded click-and-collect to balance convenience with healthy unit economics. As in-store traffic normalizes, kitchen and bedding specialists retain a growth edge due to consultative selling and service-intensive installation models that customers value in higher-consideration purchases. Retailers are prioritizing product information, traceability, and after-sales support in digital channels to ensure service parity and to meet rising sustainability disclosure expectations. The France furniture market size associated with online channels is projected to expand alongside investments in regional fulfillment, AR workflows, and appointment-based store formats that reduce friction at every step. Combined digital and physical investments tie directly to coverage goals, including faster service into secondary cities with compact Plan & Order formats.

Geography Analysis

Île-de-France secured 29.4% of market share in 2025 and is the fastest-growing region at 6.84%, driven by premium residential projects, large office retrofits in La Défense, and dense last-mile logistics that support same-day service for a wider assortment. Retailers deploy compact store formats to extend reach and to support omnichannel journeys that start online and finish in-store with material checks and service scheduling. The region benefits from extensive take-back and collection networks that shorten reverse logistics cycles and improve cost positions for reuse and refurbishment streams. The France furniture market mirrors the region’s service intensity by emphasizing flexible delivery windows, installation options, and trade-in programs that align with policy requirements and customer expectations. With complex renovation and retrofit programs underway, procurement cycles continue to favor modular lines and certified materials across residential and commercial categories in 2026.

Provence-Alpes-Côte d’Azur stands out for hospitality-driven demand in Nice, Marseille, and Aix-en-Provence, where hotels and restaurants refresh outdoor seating and dining footprints for extended warm seasons in 2026. Affluent residential segments maintain a taste for premium upholstery and bedroom ranges with provenance and certified content, reinforcing stable growth at the top of the assortment. Auvergne-Rhône-Alpes combines design hubs around Lyon with pilot circular programs that model design-for-disassembly and material recovery, which inform national practice and EPR rules over time. Contract demand around Grenoble and Lyon contributes to steady orders for office seating and modular collaboration zones in 2026 as hybrid routines persist in regional service sectors. The France furniture market uses these regional advantages to expand premium exports and to showcase circular models that scale to other regions with support from EPR funds and industry partnerships.

Nouvelle-Aquitaine navigates a tighter timber supply after storm impacts in 2024, which reshaped plywood availability and pushed buyers toward certified local mills and non-wood substitutes in selected categories. Hauts-de-France, with complex urban zoning and heritage overlays in parts of the region, has longer permit cycles that stagger kitchen and bathroom installation timing and reinforce the role of renovation over new-build in 2026. Occitanie benefits from steady office demand around Toulouse, supporting collaboration seating and storage for expanding workplaces, while Brittany and coastal communes maintain robust outdoor furniture cycles across extended seasonal windows. The France furniture market share that accrues to Île-de-France reflects both purchasing power and the ecosystem of logistics, showrooms, and take-back nodes that support circularity at lower cost per unit. Regional dispersion of EPR-funded infrastructure will remain a lever in 2026 as planners seek to close gaps between dense cores and meso-regions for reverse logistics and reuse processing.

Regulatory Landscape

France furniture regulation is anchored in the Extended Producer Responsibility (EPR) scheme for furnishing elements (DEA) under the Environmental Code, reinforced by the AGEC circular-economy framework. Oversight sits with the Ministry for Ecological Transition, with implementation handled through approved PROs such as Ecomaison and Valobat. Under this system, eco-contributions fund collection, reuse, repair, and recycling, and the framework sets performance targets, including a 48% furniture-waste collection target for 2026 that increases to 51% in 2028.

Operational compliance has tightened through updated eco-fee mechanics and product obligations. An incentive-based bonus/malus eco-modulation applies from 1 January 2025, and new pricing scales for furniture eco-fees took effect from 1 January 2026, as published by PROs for declarations and item coding. On the product side, compliance includes general safety duties under the French Consumer Code and the EU General Product Safety Regulation (EU) 2023/988, applicable since 13 December 2024, alongside REACH chemical-substance requirements. Together, these rules push manufacturers and retailers to align design, materials, labeling, and documentation with both circularity and safety enforcement.

Value Chain Analysis

The France furniture value chain begins with raw materials (timber and wood panels, metals, foams, textiles, and polymers), then moves through processing, component manufacturing, assembly, and finishing across a fragmented base of domestic manufacturers and workshops, alongside import flows. Sector coordination and collective programs are supported by industry bodies such as CODIFAB, which manages the furniture and wood tax used to fund innovation and international development actions, and L’Ameublement francais. Compliance functions link many producers and importers to EPR operators like Ecomaison for eco-fee declarations and for funding take-back and recycling.

Downstream, distribution runs across B2C retail (specialty stores, home centers, and online) and B2B project channels serving offices, hospitality, education, and public procurement. For bulky goods, delivery, installation, and reverse logistics sit at the center of day-to-day operations. Under AGEC-linked requirements, product information and end-of-life handling increasingly show up in operational routines through mandatory TRIMAN-style sorting information and invoice disclosure of waste-management costs, while eco-modulation since 1 January 2025 ties product design choices (recyclability, durability, recycled content) to eco-fee economics. The circular loop is closed through collection networks and refurbishment or reuse pathways financed via EPR, bringing take-back, sorting, repair, and recycling partners into the functional value chain rather than treating them as ancillary services.

Competitive Landscape

France's furniture market oscillates between moderate consolidation, with top-five brands holding just over half of sales. Large groups leverage buying power and logistics to manage cost, while boutiques monetize provenance, repair, and bespoke work that attract buyers willing to pay for certified materials and local sourcing. IKEA’s investment plan of USD 1.4 billion (EUR 1.2 billion) from 2023 to 2026 expands compact formats and builds a river-connected distribution center in Limay to lower urban delivery friction and to extend 60-minute coverage targets across more of the population[3]. Omnichannel consistency remains a strategic theme as retailers unify digital planning, appointment-based showrooms, and installation in a single customer journey that reduces returns and increases attachment rates. Premium labels continue to pair design leadership with material transparency and repairability, turning compliance into a brand asset with lasting value among discerning buyers.

Heritage operator Roche Bobois advanced footprint and integration moves, including store openings and franchise consolidation in Asia, while reporting stable sales performance into mid-2025 after the 2024 contraction. Roche Bobois also reported 2024 full-year performance and continued investment in store upgrades and new formats, which anchor premium positioning through curated showrooms and stronger direct operations. Ligne Roset reinforced design-led credentials through collaborative initiatives and material innovation that signal the direction of premium seating and modular systems in 2026. As omnichannel tools spread, mass customization becomes accessible at mid-market price points, which supports differentiation through finishes, fabrics, and size options without lengthening lead times. The France furniture market prizes suppliers that can deliver predictable lead times and service parity across digital and store channels while maintaining verified sustainability claims.

Competitive pressure from low-cost imports is most visible in price-entry formats online, so French producers emphasize fast delivery windows, certified wood supply, and customization to hold share where provenance matters. Retailers are reinforcing compliance by aligning assortment choices with EPR incentives and by expanding trade-in and repair services that retain customers inside the brand ecosystem. IKEA’s logistics investments underscore how waterborne urban delivery can reduce congestion costs and support same-day windows in dense areas, raising service levels across compact store networks. Premium and design-forward groups protect value through curated assortments and showroom experiences that pair with transparent sourcing and after-sales commitments. In 2026, the France furniture market rewards firms that harmonize omnichannel systems, circularity, and traceability into one coherent proposition that is easy to shop and simple to service.

France Furniture Industry Leaders

Ligne Roset

BoConcept

Gautier Furniture

Roche Bobois SA

Natuzzi S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

EPR-driven eco-modulation and the 1 January 2026 eco-fee scales provide a commercialization pathway for eco-designed furniture that is modular, repairable, and easier to dismantle, since design choices translate into recurring fee outcomes for producers and importers operating in France. That regulatory pull supports opportunities in product lines with measurable circular attributes, such as recycled-content wood and textiles, reduced disruptors, and standardized fasteners, as well as in service bundles that combine sale, installation, and compliant take-back. The fit is strongest in renovation-linked categories like kitchens, storage, and fitted solutions that need to work within older housing geometries.

Retailers and manufacturers also have an execution opening in digital and project-facing capabilities that can improve conversion and reduce friction in higher-consideration categories. One tangible signal is BoConcepts five-year partnership with Dassault Systemes (announced June 2025) to roll out HomeByMe 3D planning and configuration tools, which frames interactive planning as operational infrastructure across stores and channels. At the premium and contract end, industrial modernization aimed at bespoke throughput is visible in C4 Manufactures (launched May 2026, grouping Maison Lelièvre, Faiencerie de Gien, and Duvivier Canapes) through investments in production equipment and ERP/CRM, offering a model for value capture through customization for interior designers and luxury hospitality projects.

Recent Industry Developments

- July 2026: Gautier expanded its retail footprint with the opening of a 370 square meter franchised store in Vannes, France. The new location increases local coverage for the legacy French manufacturer and supports nearer-to-customer service for ordering, delivery coordination, and after-sales activities.

- December 2025: The Poitiers Commercial Court approved Gautiers exit from receivership following a creditor vote and a financial rescue package involving investors, including Rudy Gobert. The court-backed outcome stabilizes operations and preserves industrial and distribution continuity in the French furniture supply base.

- June 2025: BoConcept entered a five-year partnership with Dassault Systemes to deploy HomeByMe 3D space planning and product configuration solutions across its stores. The rollout strengthens omnichannel selling by making room-planning and customization more scalable, while also improving data flow between customer configuration, ordering, and fulfillment.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the France furniture market covers the value of furniture products sold for residential and non-residential use within France, counted in current prices and consolidated at the market level.

Scope exclusions: We exclude home textiles, major appliances, and pure home decor items, and we also exclude installation-only services when no furniture product is supplied.

Segmentation Overview

- By Application

- Home Furniture

- Chairs

- Tables (side tables, coffee tables, dressing tables, etc.)

- Beds

- Wardrobes

- Sofas

- Dining Tables / Dining Sets

- Kitchen Cabinets

- Other Home Furniture (bathroom, outdoor, etc.)

- Office Furniture

- Office Chairs

- Tables

- Storage Cabinets

- Desks

- Sofas & Other Soft Seating

- Other Office Furniture

- Hospitality Furniture

- Educational Furniture

- Healthcare Furniture

- Other Applications (public places, retail malls, government offices, etc.)

- Home Furniture

- By Material

- Wood

- Metal

- Plastic & Polymer

- Other Materials

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- B2C / Retail

- Home Centers

- Specialty Furniture Stores

- Local Workshops (unorganized market)

- Online

- Other Distribution Channels

- B2B / Project

- B2C / Retail

- By Region

- lle-de-France

- Provence-Alpes-Cote d'Azur

- Auvergne-Rhone-Alpes

- Nouvelle-Aquitaine

- Hauts-de-France

- Rest of France (all other metropolitan & overseas regions)

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to anchor the market boundary and to build the first set of sizing inputs that can be cross-checked. We referred to public statistics and sector publications such as INSEE national accounts and furniture-related turnover series, Eurostat structural business statistics, UN Comtrade trade flows, French customs trade releases, and Banque de France macro indicators.

On top of these, we used company annual reports, filings, investor presentations, retailer announcements, and reputable business press to understand how pricing, imports, and demand moved year to year in France. For coverage consistency, some company financials and news-intelligence subscriptions and an import and export shipment-level database were consulted to confirm directional signals and map the value chain. The desk research sources listed here are illustrative, and many other public and paid sources were also reviewed to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work was then used to confirm what the numbers could not fully explain, especially how volumes, promotions, and product mix were shifting across French channels. We spoke with stakeholders across the supply chain, including manufacturers, importers, distributors, specialist retailers, and project-focused buyers to validate assumptions on unit movement, pricing behavior, and channel mix in France.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 18% | |

| Mid tier: 54% | Functional/Unit leaders: 35% | |

| Smaller Players: 19% | Managers: 47% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where production and trade statistics, together with retail turnover and household demand signals, are used to reconstruct the addressable furniture value sold inside France. Once that total is formed, it is corroborated with selective bottom-up approximations, such as sampled average selling price (ASP) checks by product group and channel, plus supplier and retailer revenue sanity checks, and then adjusted when gaps appear.

Key inputs that guided the model included furniture retail turnover direction, import and export values for furniture categories, housing and renovation activity proxies, CPI and furniture-related price inflation, and channel shift indicators linked to online penetration and store network changes in France. When a bottom-up check could not cover smaller sellers or informal trade cleanly, we used conservative uplift factors based on interview feedback and public registration patterns, followed by another round of reasonability checks.

For forecasting, scenario analysis was applied so demand could be flexed around housing cycle outlook, inflation normalization, and channel mix changes that affect ASP progression. Assumptions were reviewed with experts so the forward curve stayed realistic, especially in years where promotions, financing availability, and renovation sentiment can swing buying decisions.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, and the largest variances are investigated before the model is locked. We check for year-to-year jumps that are not supported by trade flows, retail turnover, or macro demand indicators, and then the input series and conversion steps are rechecked by another analyst.

When new public statistics revise prior periods, or when interviews indicate a material shift in pricing or channel mix, the assumptions are revisited and experts can be re-contacted to close the gap. Reports are refreshed annually, with interim updates for material events, and before delivery an analyst performs a fresh pass so clients receive the latest updated view.

Mordor Intelligence's France Furniture Market Size Measured Against Other Published Estimates

Published market numbers for France furniture do not always line up because authors often count different value layers and they do not always track the same demand signals. Differences also come from the year selected, the currency conversion timing, and whether online and project orders are treated as part of the same market pool.

Retail turnover indicators and import and export flows are the checks that keep Mordor Intelligence's estimate aligned to a total furniture market view, rather than a single channel view. A second gap driver is scope, since some estimates stay close to specialist retail activity, and others mix furniture with adjacent home categories, which changes the value base even before forecasting choices are applied.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 21.20 B (2025) | |

| Trade Journal A | USD 14.97 B (2024) | Uses sector turnover reporting in EUR and typically reflects retail market value, which can miss B2B project sales and parts of non-specialist channel activity, and it is also a different base year. |

| Industry Data Platform B | USD 21.73 B (2025) | Tracks specialized furniture retail turnover (NACE G4759) and can exclude furniture sold through general merchandise and direct channels, and the latest year can be extrapolated from partial-year turnover patterns. |

The spread in the table is mainly explained by what is being counted, not by a simple math difference. When the estimate is tied to retail-only turnover, the market looks smaller, and when total market demand and trade signals are considered together, the value base becomes broader and more comparable across years.

Key Questions Answered in the Report

What is the current size and growth outlook for the France furniture market?

The France furniture market size is USD 22.45 billion in 2026 and is projected to reach USD 30.16 billion by 2031 at a 6.08% CAGR, led by omnichannel gains and renovation-linked demand.

Which product application leads sales in France and why?

Home Furniture leads with 63.7% share in 2025 and grows at 6.28% as living spaces integrate work functions and outdoor and storage solutions gain traction for small-format homes.

What materials are gaining ground in France furniture production?

Wood remains dominant with a 56.8% share, and Plastic & Polymer is the fastest-growing material group at a 6.62% CAGR as recycled composites and bio-based inputs scale under EPR incentives.

Which channel is expanding fastest in France furniture distribution?

Online sub-channels are the fastest, posting a 7.23% CAGR within the B2C mix, as AR planning, compact store formats, and improved delivery expand addressable demand.

How do regulations affect sourcing and product design in France?

EUDR enforces plot-level geolocation for timber, and the EPR eco-modulation rewards recycled and certified inputs, pushing manufacturers toward traceable materials and design-for-disassembly.

Which region contributes the most to the France furniture market?

Île-de-France accounts for 29.4% of sales and is the fastest-growing region at 6.84% due to premium residential projects, large office retrofits, and tight logistics networks.

Page last updated on: