Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 210 Billion |

| Market Size (2026) | USD 221.66 Billion |

| Market Size (2031) | USD 290.37 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

France Energy Bar Market Analysis by Mordor Intelligence

France energy bar market size in 2026 is estimated at USD 221.66 million, growing from 2025 value of USD 210 million with 2031 projections showing USD 290.37 million, growing at 5.55% CAGR over 2026-2031. This growth is largely driven by regulatory pressures, notably the Nutri-Score labeling system, which encourages healthier product formulations, the increasing acceptance of plant proteins as a sustainable and nutritious option, and a surge in digital retail, which offers convenience and wider accessibility. In response, manufacturers are ramping up reformulation efforts, aiming for A or B ratings under the Nutri-Score system, as these ratings now influence over half of consumer purchase decisions. While plant-based bars dominate in volume due to their appeal among health-conscious and environmentally aware consumers, there's a notable uptick in animal-based recipes. This growth is particularly evident among endurance athletes who prioritize products with a complete amino-acid profile to support their performance and recovery. High-margin avenues are expanding for both established multinationals and nimble newcomers, driven by strategies such as travel-retail positioning to capture on-the-go consumers, endorsements from sports federations to build credibility, and a push towards subscription-based e-commerce, which ensures consistent consumer engagement and loyalty.

Key Report Takeaways

- By product type, the conventional tier retained 77.62% revenue share in 2025; the organic tier is projected to expand at a 6.32% CAGR, the fastest within the market.

- By protein source, plant-based bars captured 57.99% of France's energy bar market share in 2025, while animal-based bars are forecast to grow at a 5.89% CAGR through 2031.

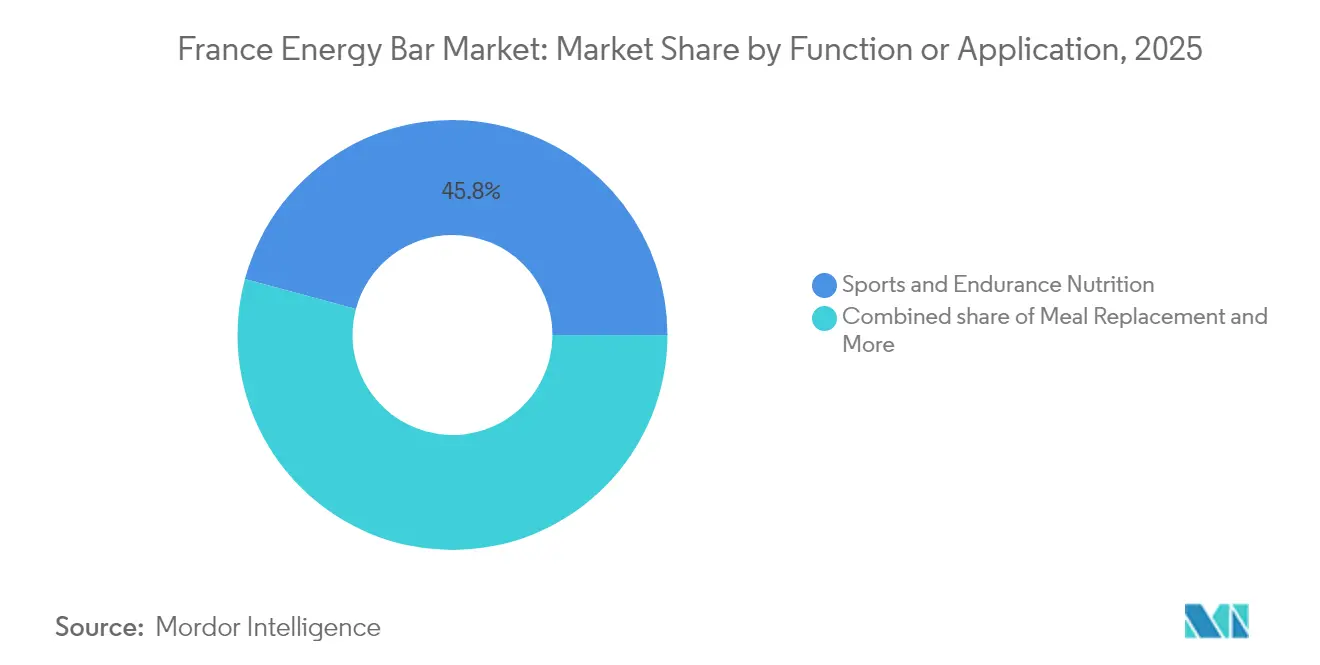

- By function, sports and endurance nutrition led with 45.81% of the France energy bar market size in 2025, whereas meal-replacement formats are advancing at a 6.93% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets commanded 56.53% of the France energy bar market size in 2025; online sales are set to post the highest 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Energy Bar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of Vegan and Flexitarian Diets Boosting Plant-Protein Bar Innovation | +2.2% | National, with higher adoption in urban centers (Paris, Lyon, Marseille) | Medium term (~ 3-4 years) |

| Growing Tourism and Travel Retail Footprint in Airports/Rail Hubs Increasing Impulse Purchases | +1.5% | Concentrated in major transportation hubs and tourist destinations (CDG, Orly, Gare du Nord) | Short term (≤ 2 years) |

| Sports Federation Partnerships Fueling Demand in Athletic and Amateur Fitness Circles | +1.2% | National, with stronger impact in regions hosting major sporting events | Medium term (~ 3-4 years) |

| Accelerated Adoption of On-the-Go Breakfast Solutions Among Working-Age French Population | +0.9% | Urban centers with high concentration of office workers (Île-de-France, Rhône-Alpes) | Medium term (~ 3-4 years) |

| Influence of Digital Marketing Strategies | +0.8% | National, with higher penetration in digitally-savvy demographics | Short term (≤ 2 years) |

| Government-Led Nutrition Labelling (Nutri-Score) Steering Consumers Toward Better-for-You Snacks | +0.7% | National | Long term (≥ 5 years) |

| Source: Mordor Intelligence | |||

Rise of Vegan and Flexitarian Diets Boosting Plant-Protein Bar Innovation

Flexitarian eating patterns are reshaping the French energy bar market. While plant-based protein bars are set to retain their leading position, the animal-based segment is witnessing quicker growth. This trend underscores a nuanced segmentation in the plant protein arena, with manufacturers crafting tailored formulations to meet distinct consumer demands, moving away from one-size-fits-all plant-based products. Initiatives such as France's National Nutrition and Health Program (PNNS) emphasize the importance of sustainable and plant-based diets, aligning with the growing consumer preference for environmentally friendly products [1]Source: French National Nutrition and Health Program, www.sante.gouv.fr. The French Ministry of Agriculture has also reported an increase in funding for plant-based food innovation, further encouraging manufacturers to invest in research and development for advanced formulations. These government-backed efforts, combined with rising consumer awareness, are expected to sustain the dominance of plant-based protein bars in the market while fostering innovation and competition within the segment.

Growing Tourism and Travel Retail Footprint in Airports/Rail Hubs Increasing Impulse Purchases

Energy bars are strategically positioned in French transportation hubs, carving out a lucrative growth channel largely insulated from the typical pressures of retail pricing. This segment of travel retail holds particular weight, especially with France being the globe's top tourist destination. Paris's Charles de Gaulle and Orly airports stand out as pivotal distribution points. The French economy ministry heralded 2024 as a banner year for tourism, buoyed by a surge in international arrivals. Data from 2024 reveals that France welcomed over 100 million international visitors [2]Source: Republique Francaise, "2024, a record year for international tourism in France", www.campusfrance.org. By placing energy bars as convenient grab-and-go options in these bustling locales, there's an opportunity for premium pricing, with travelers often shelling out 15-20% more than standard retail prices. Additionally, the high foot traffic in transportation hubs ensures consistent visibility and accessibility for energy bar brands, making these locations a strategic choice for market penetration and brand reinforcement. PowerBar's enduring collaboration with the Tour de France underscores the potential for brands to harness France's tourism strengths. This partnership highlights how aligning with iconic events can amplify brand awareness and drive consumer engagement, leveraging the synergy between sports, tourism, and retail.

Sports Federation Partnerships Fueling Demand in Athletic and Amateur Fitness Circles

According to the Baromètre National des Pratiques Sportives 2023 report, 26% of French people engaged in physical activity at least four times a week or more in 2023, while 14% participated in physical activity three or four times a week, reflecting a growing interest in sports and fitness activities [3]Source: Institut National de la Jeunesse et de l'Éducation Populaire,"Baromètre national des pratiques sportives 2023", www.injep.fr. The UEFA expert group statement on nutrition in elite football highlights the importance of proper nutrition timing and composition for performance and recovery, creating scientific validation for specialized energy bar formulations. These collaborations aim to promote healthier lifestyles and provide nutritional support for athletes and fitness-conscious individuals. Furthermore, government initiatives, such as the "National Sports Nutrition Program," emphasize the importance of energy-dense snacks like energy bars for sustained performance. The French government has also allocated funding to promote sports participation and nutrition awareness, which is expected to further boost the adoption of energy bars. This growing focus on fitness and nutrition, coupled with increasing consumer awareness, is anticipated to drive the demand for energy bars in both professional athletic and amateur fitness circles.

Accelerated Adoption of On-the-Go Breakfast Solutions Among Working-Age French Population

With increasingly hectic schedules, French consumers, particularly those in the workforce, are seeking convenient and nutritious breakfast options that align with their fast-paced routines. Energy bars, known for their portability and balanced nutritional content, have emerged as a preferred choice. World Bank data reveals that in 2024, France's labor participation rate for those aged 15 to 64 held steady at approximately 73.79% [4]Source: World Bank, "Labor Force- total, France", www.databank.worldbank.org. This trend is further supported by the growing awareness of health and wellness, prompting individuals to opt for quick yet wholesome alternatives to traditional breakfast meals. Additionally, the increasing prevalence of dual-income households in France has further fueled the demand for ready-to-eat breakfast solutions. Moreover, the rising participation in fitness and sports activities among the working-age population has amplified the need for energy-boosting snacks, further propelling the popularity of energy bars. Manufacturers are responding to this demand by introducing innovative flavors, organic ingredients, and functional benefits, such as high protein content or added vitamins, to cater to the evolving preferences of French consumers. These factors collectively underscore the pivotal role of on-the-go breakfast solutions in shaping the growth trajectory of the France energy bar market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Raw Material Prices Disrupting Cost Structure | -1.3% | National, with greater impact on premium segments | Short term (≤ 2 years) |

| Allergen Concerns Hindering the Market Growth | -1.1% | National, particularly affecting traditional energy bar segments | Medium term (~ 3-4 years) |

| Sugar-content Scrutiny by Santé Publique France Dampening Indulgent Bar Sales | -0.9% | National | Medium term (~ 3-4 years) |

| Competition from Meal Replacement Drinks and Alternative Snack Bars Hindering Growth | -0.7% | Urban centers, particularly among younger demographics (25-40 age group) | Medium term (~ 3-4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw Material Prices Disrupting Cost Structure

In the France Energy Bar Market, volatile raw material prices pose a significant restraint, disrupting the cost structure for manufacturers. These price variations directly impact production costs, making it challenging for manufacturers to maintain consistent pricing strategies. Additionally, the increasing demand for organic and premium-quality ingredients further exacerbates cost pressures, as these materials often come at a higher price point. This dynamic creates a challenging environment for market players, requiring them to adopt efficient procurement strategies and explore alternative ingredient sources to mitigate the impact of price volatility. Furthermore, the global economic environment, including inflationary pressures and currency fluctuations, adds another layer of complexity to raw material procurement. Manufacturers must also contend with the rising costs of transportation and logistics, which further inflate the overall production expenses. As a result, companies operating in the France Energy Bar Market are increasingly focusing on building resilient supply chains, negotiating long-term contracts with suppliers, and investing in research and development to identify cost-effective ingredient alternatives.

Sugar-content Scrutiny by Santé Publique France Dampening Indulgent Bar Sales

As regulatory scrutiny and consumer awareness sharpen on sugar content, the energy bar market is witnessing a significant split. This shift is largely driven by the updated Nutri-Score system's algorithm, which places a stronger emphasis on sugar content, fostering greater transparency in nutritional labeling. The algorithm update has compelled manufacturers to reformulate their products to achieve better ratings, aligning with evolving consumer preferences for healthier options. Research highlights that the Nutri-Score system effectively counters misleading "reduced sugar" claims by providing a more holistic nutritional assessment. This transparency empowers consumers to make informed purchasing decisions, favoring products with lower sugar content and better overall nutritional profiles. The impact of these changes is particularly pronounced in the indulgent segment of the energy bar market. Products that were traditionally marketed based on taste rather than nutritional benefits are now under increased scrutiny. As consumers prioritize health-conscious choices, these indulgent energy bars face the risk of losing market share to low-sugar alternatives. This trend underscores the growing importance of balancing taste with nutritional value to remain competitive in the evolving market landscape.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Organic Segment Captures Premium Positioning

In 2025, the conventional segment dominates the France energy bar market with a substantial 77.62% market share. This dominance is attributed to its well-established distribution networks and affordability, which cater to a broad consumer base. Conventional energy bars are widely available across various retail channels, making them a convenient choice for consumers. Their competitive pricing further strengthens their position, appealing to cost-conscious buyers. However, while the conventional segment maintains its stronghold, it faces growing competition from the organic segment, which is steadily gaining traction among health-conscious consumers. The conventional segment's ability to sustain its market share will depend on its adaptability to evolving consumer preferences and its capacity to innovate within its product offerings.

On the other hand, the organic segment is emerging as a key growth driver in the France energy bar market, with an impressive CAGR of 6.32% projected through 2031. This robust growth reflects a structural shift in consumer preferences toward premium and health-oriented products. The organic segment aligns closely with broader French food trends, where consumers increasingly prioritize clean labels, transparent sourcing, and sustainable production practices. Organic energy bars cater to these demands, offering products free from artificial additives and made with high-quality, natural ingredients. As awareness of health and wellness continues to rise, the organic segment is expected to capture a larger share of the market, challenging the conventional segment's dominance. This trend underscores the growing importance of innovation and differentiation in meeting the evolving needs of French consumers.

By Protein Source: Plant-Based Dominates, Animal-Based Accelerates

In 2025, plant-based protein sources held a commanding 57.99% share of the French energy bar market. This dominance comes even as the animal-based segment is projected to outpace it, growing at a rate of 5.89% CAGR through 2031. This seeming paradox underscores the maturation of the plant-based segment, which is now advancing through refined formulations rather than just expanding its market share. The plant-based segment's lead is bolstered by its resonance with flexitarian diets and a preference for clean labels. Consumers increasingly favor plant-based options due to their perceived health benefits, environmental sustainability, and ethical considerations. Notably, pea protein has emerged as a key ingredient, prized for its complete amino acid profile and allergen-free nature, making it a versatile choice for manufacturers aiming to meet diverse dietary needs.

Meanwhile, the swift ascent of the animal-based segment can be attributed to its robust foothold in the performance nutrition subsector. Here, whey protein's superior leucine content and absorption profile offer distinct advantages to dedicated athletes, supporting muscle recovery and growth. Furthermore, innovations in dairy protein processing are enhancing taste and texture, effectively overcoming past consumer acceptance hurdles. These advancements are making animal-based energy bars more appealing to a broader audience, including those who prioritize performance and functionality. Highlighting the momentum in plant protein innovation, the EU-backed PROTEIN2FOOD project is working to adapt crops like quinoa and amaranth to European climates, broadening ingredient choices for energy bar producers. Such initiatives underscore the plant-based segment's ongoing evolution, ensuring its sustained relevance even in the face of the animal-based segment's brisker growth.

Function/Application: Performance Nutrition Maintains Leadership

In 2025, the sports and endurance nutrition segment commanded a 45.81% share of the France energy bar market, underscoring its longstanding ties to athletic performance. This segment has been a cornerstone of the market, driven by the increasing adoption of energy bars among professional athletes and fitness enthusiasts seeking convenient and effective nutritional solutions. Meanwhile, the meal replacement segment, boasting a 6.93% CAGR projected through 2031, signals a broadening functional appeal as consumers increasingly turn to energy bars as a substitute for traditional meals. This growth is fueled by the rising demand for on-the-go nutrition, particularly among busy urban populations in France. The sports nutrition segment solidifies its leading stance, bolstered by its close ties to athletic communities and robust scientific backing. A case in point is the UEFA expert group's statement on elite football nutrition, highlighting the critical nature of nutrition timing and composition. This scientific validation has significantly influenced consumer trust and adoption of energy bars tailored for sports and endurance activities.

Furthermore, this segment reaps rewards from collaborations with sports federations, crafting a robust endorsement network that resonates from elite athletes down to amateur fitness buffs. These partnerships not only enhance brand visibility but also reinforce the credibility of energy bars as an essential component of athletic performance and recovery. Additionally, the France energy bar market benefits from a growing focus on product innovation, with manufacturers introducing energy bars enriched with functional ingredients such as protein, vitamins, and minerals. This trend aligns with the increasing consumer preference for clean-label and health-focused products. The market also sees a surge in demand for plant-based energy bars, driven by the rising popularity of vegan and vegetarian diets in France. These developments are expected to further propel the growth of the sports and endurance nutrition segment, as well as the overall energy bar market in the country.

Distribution Channel: Supermarkets/Hypermarkets Leads, Online Retail Gain Momentum

In 2025, supermarkets and hypermarkets held a commanding 56.53% market share in the France energy bar market, leveraging their unmatched physical distribution advantages. These retail formats have been instrumental in ensuring widespread availability of energy bars across urban and rural areas, catering to diverse consumer needs. Their ability to stock a wide variety of energy bar brands and flavors has further strengthened their position in the market. Meanwhile, online channels are on track to expand at a robust 7.12% CAGR through 2031, signaling a significant shift in consumer purchasing behaviors. The convenience of online shopping, coupled with the increasing penetration of e-commerce platforms in France, has made it easier for consumers to access a broader range of energy bars, including niche and premium options.

Additionally, the growing trend of health-conscious consumers seeking detailed product information has driven the popularity of online channels, where such information is readily available. Traditional retail formats have thrived, thanks to their knack for seizing impulse buys and their broad geographic reach. Supermarkets and hypermarkets often capitalize on strategic product placements, such as near checkout counters, to encourage impulse purchases of energy bars. However, this dominance is increasingly challenged by both specialized outlets and digital platforms. Specialized health and wellness stores, for instance, are gaining traction by offering curated selections of energy bars that cater to specific dietary preferences, such as vegan, gluten-free, or high-protein options. Similarly, digital platforms are eroding the market share of traditional formats by providing competitive pricing, subscription models, and personalized recommendations, which appeal to the evolving preferences of French consumers.

Geography Analysis

The French energy bar market demonstrates notable regional differences in consumption patterns, with urban centers such as Paris, Lyon, and Marseille leading the way in adopting innovative products. These cities are characterized by a consumer base that values convenience, health-conscious choices, and is more open to trying new nutritional solutions. In contrast, rural areas exhibit a preference for traditional snacking habits, reflecting a slower pace of lifestyle, limited exposure to modern dietary trends, and a stronger inclination toward familiar products. This divergence highlights the need for manufacturers to understand and cater to the unique preferences of each region to effectively penetrate the market and maximize their reach.

Urban areas, particularly Paris and its surrounding Île-de-France region, dominate the market due to several key factors. Higher disposable incomes in these regions enable consumers to spend more on premium and convenient nutrition options like energy bars. Additionally, urban lifestyles, marked by busy schedules, long working hours, and a growing focus on health and wellness, drive demand for on-the-go nutritional products. Paris, as the largest consumption hub, benefits from its high concentration of office workers who seek quick and healthy snacking alternatives during their workdays. The city's dynamic retail environment, with a mix of supermarkets, convenience stores, and specialty health food outlets, further supports the growth of energy bar consumption.

However, this geographic diversity presents significant challenges for manufacturers aiming to achieve national coverage. The stark contrast between urban and rural consumption patterns necessitates tailored retail strategies to address the specific needs of each market segment. For instance, urban markets may require a focus on modern retail channels, e-commerce platforms, and innovative marketing campaigns to attract tech-savvy and health-conscious consumers. On the other hand, rural markets might benefit from traditional distribution networks, partnerships with local retailers, and localized product offerings that align with regional tastes and preferences. Successfully navigating these challenges is crucial for manufacturers to establish a strong foothold in the French energy bar market and ensure sustainable growth across diverse regions.

Regulatory Landscape

Energy bars sold in France are treated as conventional foods under the EU Food Information to Consumers framework (Regulation (EU) No 1169/2011), which requires clear French-language labeling, ingredient lists, allergen disclosure, and nutrition declarations. Marketing messages also face constraints from EU rules on nutrition and health claims (Regulation (EC) No 1924/2006). In France, DGCCRF is the key enforcement authority, with market controls focused on labeling accuracy and unauthorized claims, which is particularly relevant for performance, energy, and meal-replacement positioning.

Nutritional front-of-pack signaling has tightened through Nutri-Score, with Santé publique France documenting the updated algorithm that entered into force on 16 March 2025 and drives reformulation toward lower sugar and improved nutrient profiles. Decree No 2026-312 dated 24 April 2026 transposed EU Directive 2024/1438 into French law, adding transparency requirements for breakfast-related food products effective 14 June 2026. This can affect energy bars positioned for on-the-go breakfast through additional composition or origin-related disclosure expectations.

Value Chain Analysis

The France energy bar value chain begins with agricultural and commodity inputs (oats and cereals, nuts, dried fruits, cocoa, sweeteners) and protein systems (notably pea and whey). These inputs are then processed through formulation and manufacturing steps such as mixing, baking or cold extrusion, and coating, followed by primary packaging and secondary packing for retail display. Brand owners operate via a combination of in-house production and contract manufacturing, with partners such as Bariatrix Europe (Guilherand-Granges) and service providers like Yourbarfactory supporting formulation, prototyping, and packaging for private label and emerging brands. Local players such as Baouw (Annecy) and Hard Bar (Chamonix) illustrate how upstream sourcing choices (organic, vegan) and community-led branding feed into market availability.

Downstream, supermarkets and hypermarkets remain the dominant route to shelf, while online retail and subscription models expand direct access and data-driven assortment. At retail interfaces, regulatory and commercial oversight shapes the chain: DGCCRF controls focus on labeling and claims compliance, and food-chain policy has increased transparency pressure through Law No 2025-337 (14 April 2025), which introduced new reporting requirements around gross margins for food retailers and frameworks for price coefficients. On the operational side, manufacturers manage equipment and ingredient risk, including longer lead times for specialized cold-extrusion equipment and the need for resilient procurement on key proteins and inclusions.

Competitive Landscape

France's energy bar market, with a moderate concentration, presents a competitive and dynamic landscape. Multinational food giants compete alongside specialized nutrition brands and emerging local players, creating a fragmented market that caters to a wide range of consumers. These consumers include casual snackers seeking convenience and athletes looking for performance-enhancing nutrition, each with unique preferences and purchasing motivations. A distinct strategic divide characterizes the market, where mass-market players prioritize volume-driven approaches, while specialized brands focus on carving out a premium niche. This divide is further highlighted by acquisition activities, such as Mondelēz International's acquisition of Clif Bar, which underscores the ongoing consolidation efforts in the market.

Opportunities abound in combining nutritional benefits with indulgent flavors, particularly for products targeting the expanding meal replacement segment. This trend reflects the growing consumer demand for convenient yet nutritious options that align with their busy lifestyles. Retail dynamics play a crucial role in shaping the competitive environment. For instance, Carrefour's push for private-label products introduces both challenges and opportunities for branded manufacturers. While private labels may intensify competition, they also encourage innovation among established brands to differentiate their offerings. Meanwhile, new entrants are capitalizing on direct-to-consumer strategies, bypassing traditional retail channels to reach consumers more effectively and build brand loyalty.

Established brands are increasingly leveraging technology to strengthen their connection with consumers. They are offering personalized nutrition insights and subscription-based models to cater to individual needs and preferences. Additionally, the Nutri-Score system is emerging as a significant factor in the market, leveling the playing field for smaller brands. This system allows brands with superior nutritional profiles to stand out, even when competing against larger players with substantial marketing budgets. By empowering consumers to make informed choices, the Nutri-Score system is driving competition and encouraging innovation, ultimately benefiting the overall market landscape.

France Energy Bar Industry Leaders

-

PepsiCo, Inc.

-

General Mills Inc.

-

Mars Inc.

-

WK Kellogg Co.

-

Mondelez International

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory change provides the near-term anchor, with the Nutri-Score algorithm update on 16 March 2025, DGCCRF enforcement of EU nutrition and health-claim rules under Regulation (EC) No 1924/2006, and Decree No 2026-312 (24 April 2026) setting transparency requirements for breakfast-related products effective 14 June 2026.

Commercial opportunities cluster around (i) premium organic and clean-label bars that combine Agriculture Biologique (AB) cues with Nutri-Score performance, (ii) sports and endurance formats supported by federation or community partnerships, and (iii) e-commerce subscriptions that reduce dependence on crowded supermarket shelves. Product momentum is visible through continued high-protein innovation, including Nutripure launching a 17 g protein bar in April 2026 and RXBAR expanding its high-protein line in 2026, which points to active competition around ingredient simplicity and protein density. On the supply side, ingredient and traceability capabilities are becoming more central, supported by moves such as Nexira acquiring Moroccan carob specialist Keragum in July 2026 to strengthen control over natural texturizers and label-friendly formulations used across functional snacks.

Recent Industry Developments

- July 2026: Joyfuel launched the Crunchy Nuts Protein Bar in France in flavors such as Salted Caramel Peanut and Hazelnut Chocolate, positioning the line around nut-forward textures and double-digit protein per bar. The launch increases pressure on incumbents in the high-protein segment to defend shelf space and online visibility with differentiated textures and clean-label ingredient stories.

- April 2026: Nutripure released its Protéinée Barre in France, formulated with 17 g of protein from pasteurized egg white. This addition provides a high-protein option for gym users and endurance consumers who compare macros across brands.

- April 2025: Clif Bar introduced its Caffeinated Collection energy bars in France, with around 65 mg of organic caffeine per bar in flavors including Vanilla Almond and Caramel Chocolate Chip. The line expands energy on the go options for performance and on-the-go use cases.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers packaged energy bars sold in France that are marketed for energy, sports performance, endurance, or functional snacking, and that are bought through retail and online channels.

Scope exclusions (not counted): gels and chews, traditional confectionery bars, and ready-to-drink nutrition beverages are excluded from the market totals.

Segmentation Overview

-

By Type

- Organic

- Conventional

-

By Protein Source

- Plant-Based

- Animal-Based

-

By Function/Application

- Sports and Endurance Nutrition

- Meal Replacement

- Weight Management and Lifestyle Energy

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retailers

- Other Distribution Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure of the market and to align definitions across products sold in France. We referenced public sources such as French customs and trade statistics, national nutrition and health publications, relevant EU food labeling guidance, peer-reviewed food science journals, and category reporting from retail associations and open press releases.

These inputs helped us form assumptions on channel mix, pricing direction, and how claims like energy and sports positioning show up on-pack in France. We also reviewed company filings, investor presentations, and reputable news coverage to confirm launches, portfolio changes, and distribution pushes. Where needed, paid subscriptions focused on company financials and intelligence, patent databases, and shipment-level import-export visibility were used to cross-check directional movements. This desk list is illustrative, and many other public sources were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test what we built from public information and to close gaps around channel execution, pricing behavior, and consumer purchase triggers. We spoke with stakeholders across branded suppliers, contract manufacturing and ingredient specialists, distributors, and retail-side category teams, and we covered demand signals across France with extra checks on online-first sellers and modern retail buyers.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 13% | |

| Mid tier: 56% | Functional/Unit leaders: 31% | |

| Smaller Players: 14% | Managers: 56% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where category consumption in France is reconstructed using retail channel splits, observed price bands, and how energy bars are positioned versus nearby snack-bar formats. The totals are then checked using selective bottom-up approximations, including sampled price per bar times estimated volumes by channel, plus supplier and distributor sense checks to adjust for under-reported parts of the market.

Key inputs used in the model include the share of sales flowing through supermarkets and hypermarkets versus convenience and online retail, average selling price movement by pack format, the mix shift between plant-based and animal-based protein positioning, the share of products marketed for sports and endurance versus meal replacement, and the pace of new product activity that meets French label expectations (including Nutri-Score sensitivity). For forecasting, scenario analysis is used around pricing and channel mix, and the year-by-year path is guided by expert expectations on promo intensity, ingredient cost pass-through, and online penetration. Where bottom-up visibility is thinner, we apply conservative fill factors that are later re-checked with interview feedback before finalizing the series.

Data Validation & Update Cycle

Outputs are validated through multiple checks that look for unrealistic jumps in price, channel mix, or implied per-capita consumption. We also compare results against independent signals like retail shelf expansion, frequency of new launches, and trade and ingredient indicators, and then investigate any large variance before sign-off.

A second analyst review is completed to confirm that assumptions match the written scope and that calculations tie back to the same unit basis and currency timing. The report is refreshed annually, and interim updates are made when material events occur, such as regulation changes, large portfolio shifts, or sharp pricing swings. Before delivery, a final review pass is done so clients receive the most current view available.

Mordor Intelligence's France Energy Bar Market Sizing Compared With Other Published Estimates

Published market sizes for France energy bars can look different even when they use similar words, because the boundaries around what counts as an energy bar are not always the same. Differences also come from how firms treat channel coverage, pricing inputs, and the year chosen for currency timing.

Retail channel signals and on-pack claim screening are the main checks that keep Mordor Intelligence's estimate aligned to packaged bars sold in France that are explicitly marketed for energy or performance, instead of being widened to all snack bars with similar ingredients. Some published numbers also lean on shorter forecast windows, or they apply broad growth rates without validating shifts between online and store-based sales, which can move the total up or down.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 210.00 M (2025) | |

| Industry Research Desk A | USD 16.68 M (2024) | Uses a narrower value base and likely different category boundary, which can exclude sports-positioned functional bars sold through broader retail sets, and it anchors sizing to a different base year that affects pricing and currency timing. |

| Trade-led Forecast Note B | USD 21.82 M (2030) | Reports a later-year point estimate and can mix forecast uplift with the current market size, which makes comparisons hard unless the same year, scope of channels, and included bar formats are held constant. |

The spread is mainly explained by year alignment and what is counted as an energy bar in the first place, followed by how pricing and channel coverage are treated. By tying the model to observable channel movement and repeatable scope rules, the final value stays traceable and can be re-checked when new product formats or claims become common in France.

Key Questions Answered in the Report

What is the current size of the France energy bar market?

The market is valued at USD 221.66 million in 2026 and is forecast to reach USD 290.37 million by 2031.

Which protein source leads sales?

Plant-based formulations hold 57.99% of France energy bar market share, thanks to flexitarian and vegan adoption.

Which channel will grow fastest through 2031?

Online direct-to-consumer and subscription models are projected to post a 7.12% CAGR, surpassing brick-and-mortar growth.

Why are animal-based bars still gaining momentum?

Whey and collagen deliver complete amino-acid profiles valued by endurance athletes, driving a 5.89% CAGR despite lower baseline volume

Page last updated on: