Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

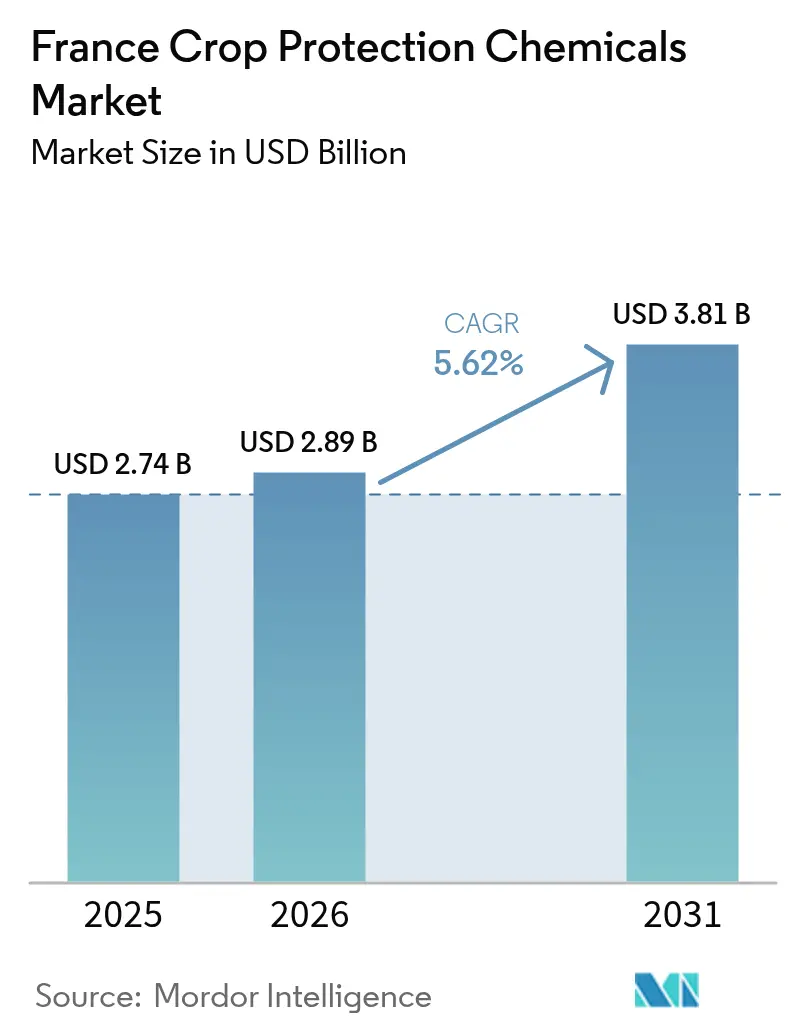

| Base Year Market Size (2025) | USD 2.74 Billion |

| Market Size (2026) | USD 2.89 Billion |

| Market Size (2031) | USD 3.81 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Crop Protection Chemicals Market Analysis by Mordor Intelligence

The France crop protection chemicals market size was valued at USD 2.74 billion in 2025 and estimated to grow from USD 2.89 billion in 2026 to reach USD 3.81 billion by 2031, at a CAGR of 5.62% during the forecast period (2026-2031). This forward trajectory mirrors France’s commitment to balancing environmental goals with high farm productivity across 27.8 million hectares of cropland.[1]Source: Ministry of Agriculture and Food Sovereignty, “Écophyto 2030 Strategy,” agriculture.gouv.fr Regulatory withdrawals of aging active ingredients accelerate demand for new molecules and biological alternatives rather than shrinking overall consumption, lending resilience to the France crop protection chemicals market. A steady pipeline of government grants, tax incentives, and research collaborations sustains innovation momentum, while climate variability pushes growers toward more intensive pest and disease management. Competitive advantage now rests on companies’ capacity to supply premium, regulation-ready technologies that dovetail with precision-application equipment and digital advisory tools.

Key Report Takeaways

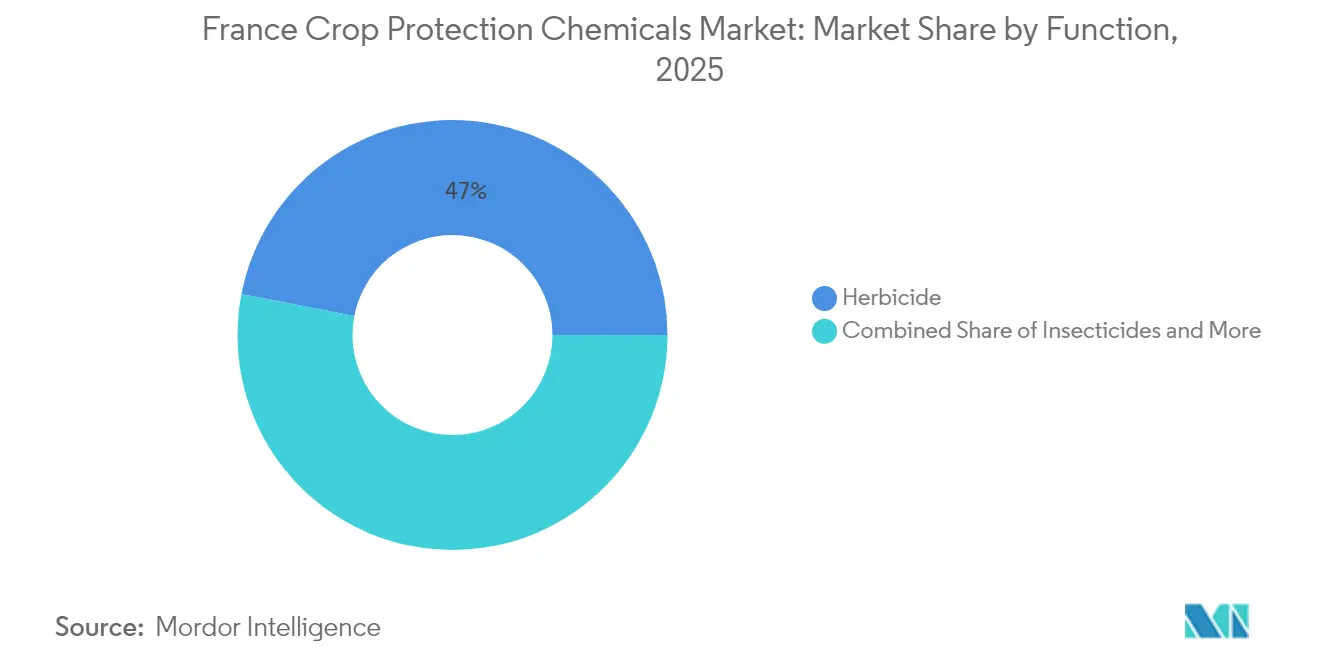

- By function, herbicides led with 46.95% revenue share in 2025, whereas insecticides recorded the fastest 6.17% CAGR through 2031.

- By application mode, foliar sprays commanded 45.35% of the France crop protection chemicals market share in 2025, while seed treatment is expanding at a 6.01% CAGR to 2031.

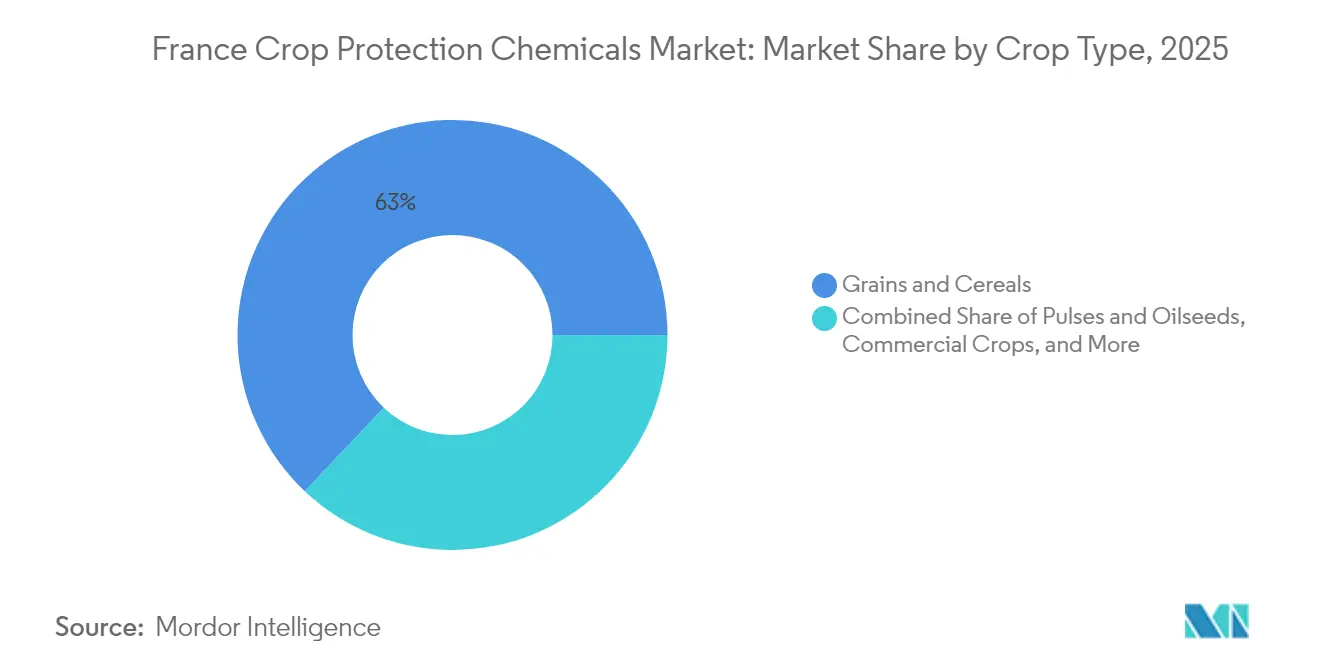

- By crop type, grains and cereals accounted for 62.95% of the France crop protection chemicals market size in 2025 and are set to advance at a 5.96% CAGR by 2031.

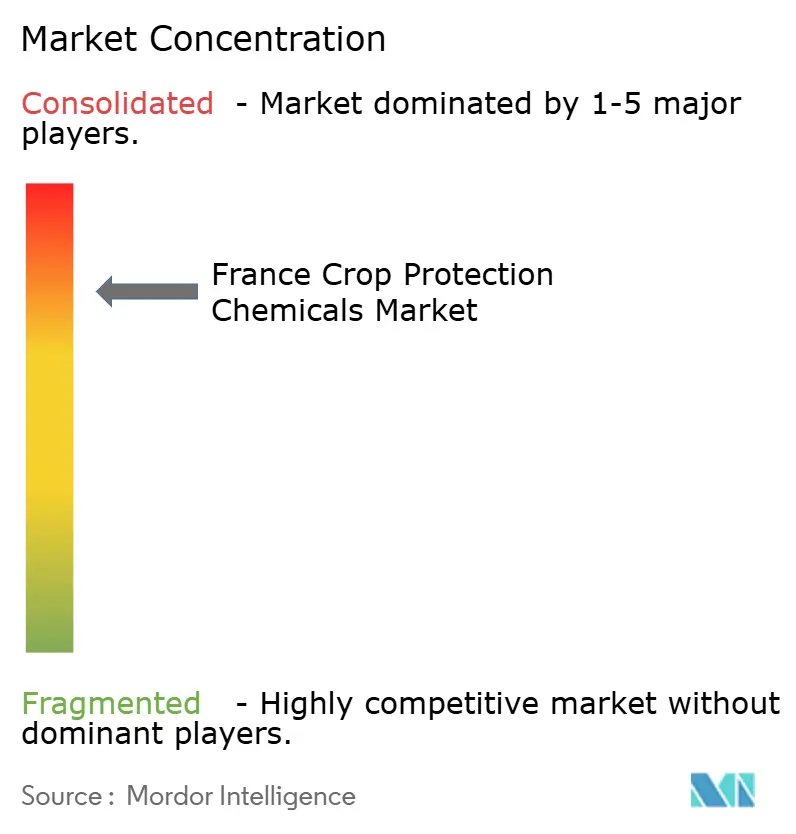

- By company concentration, the top five suppliers, Syngenta, Bayer, Nufarm, BASF, and Corteva, controlled about 69.15% of 2025 sales, reflecting a highly concentrated structure.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Crop Protection Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward sustainable agriculture and biocontrol adoption | +1.2% | National, strongest in Nouvelle-Aquitaine and Occitanie | Medium term (2-4 years) |

| High herbicide demand in large arable areas and glyphosate substitution | +1.8% | Northern regions such as Hauts-de-France and Grand Est | Short term (≤ 2 years) |

| Rising pest pressure driven by climate variability | +1.1% | National, acute in Mediterranean zones | Long term (≥ 4 years) |

| Precision-application and seed-treatment technology gains | +0.9% | Early uptake in Île-de-France and Normandy | Medium term (2-4 years) |

| Expansion of irrigated vineyards in Mediterranean regions | +0.4% | Provence-Alpes-Côte d’Azur and Languedoc-Roussillon | Long term (≥ 4 years) |

| Tax incentives for drift-reducing spray equipment | +0.3% | National, higher uptake in intensive farming districts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift Toward Sustainable Agriculture and Biocontrol Adoption

France’s Écophyto 2030 strategy, run by the Ministry of Agriculture and Food Sovereignty, mandates a 50% cut in synthetic pesticide use while safeguarding yields. The PARSADA (Plan d’Action Stratégique pour l’Anticipation du Retrait européen des Substances Actives1`) program allocates EUR 146 million (USD 161 million) for transition support, stimulating a rapid rise in biocontrol sales that reached 23,800 metric tons in 2023. The French National Agency for Food, Environmental and Occupational Health Safety (ANSES) has halved registration lead times for qualifying biologicals, benefiting firms such as Lallemand Plant Care and Koppert France. Producers gain pricing power because biological solutions carry value premiums over legacy chemistry, redirecting competition toward innovation rather than volume. As a result, the France crop protection chemicals market is becoming a laboratory for disruptive technologies that can later scale across Europe.

High Herbicide Demand in Large Arable Areas and Glyphosate Substitution

Cereal farms in the north cover 4.2 million hectares, keeping herbicides central to crop protection strategies. ANSES withdrew 36 glyphosate formulations in 2024, instantly opening a EUR 280 million (USD 308 million) substitution opportunity.[2]Source: ANSES, “Withdrawal of Plant Protection Products,” anses.fr Growers have shifted toward pre-emergence blends that require multiple passes, lifting expenditure even as sprayed volumes flatten. Suppliers holding diverse herbicide portfolios and precision application add-ons are well placed to capture this spend. The adjustment period is inflating short-term demand in the France crop protection chemicals market while growers refine new weed-control protocols.

Rising Pest Pressure Driven by Climate Variability

Warmer winters and erratic rainfall foster earlier insect emergence and longer disease windows. The European corn borer now threatens 1.8 million hectares of maize, and aphid flights occur 15-20% ahead of historical averages.[3]Source: INRAE, “Climate Change Impacts on French Agriculture,” inrae.fr Fungus-friendly microclimates expand across cereals and vineyards, pushing preventive spraying. Consequently, insecticides are projected to log the fastest segment growth to 2030. Providers that marry biological controls with selective chemistry are securing early-mover advantages by addressing environmental compliance and efficacy in tandem.

Precision-Application and Seed-Treatment Technology Gains

Global Positioning System (GPS) variable-rate systems are active on 35% of large French farms, nearly doubling penetration since 2022. A 40% tax credit on drift-reducing sprayers accelerates adoption. Parallel progress in seed-treatment coatings concentrates multiple actives and biological enhancers onto a single kernel, aligning with policymakers’ preference for targeted delivery. Corteva and Syngenta have poured capital into French seed-treatment lines capable of supplying such multi-stacked solutions. Farmers willingly pay a premium when precise targeting reduces overall load and field passes, reinforcing value growth for the France crop protection chemicals market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent ANSES withdrawals of key active ingredients | -1.4% | National, heavier in conventional cereal regions | Short term (≤ 2 years) |

| Surge in organic or zero-pesticide initiatives | -0.8% | National, focused in peri-urban belts | Medium term (2-4 years) |

| Input-cost volatility curbing application rates | -0.6% | National, severe for price-sensitive crops | Short term (≤ 2 years) |

| Local residential buffer-zone charters limiting spraying windows | -0.3% | Dense peri-urban clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent ANSES Withdrawals of Key Active Ingredients

ANSES bans continue, with metam-sodium struck off in 2024 and new constraints on flufenacet enacted in March 2025. Withdrawals cut supply of broad-spectrum low-cost solutions. Farmers scramble for costlier substitutes, shrinking their margin cushions, and distributors juggle short-dated inventories. Uncertainty complicates season planning, causing missed spray windows and diminishing effectiveness, which dampens volume expansion in the France crop protection chemicals market.

Surge in Organic or Zero-Pesticide Initiatives

Organic acreage hit 2.78 million hectares in 2024, equal to 11.2 % of farmland. Municipal zero-pesticide programs add another 180,000 hectares subject to chemical bans. Conversion subsidies of EUR 350 per hectare (USD 385) make organic shifts financially attractive for peri-urban growers. While organic produce captures price premiums, the reduction in synthetic inputs lowers conventional market volumes, particularly around large cities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Herbicides Lead Market Transformation

Herbicides controlled 46.95% of 2025 sales, within the France crop protection chemicals market size. Cereal monocultures depend on herbicides for yield insurance, and glyphosate removal has not diminished that reliance. Instead, growers are layering pre-emergence mixes with mechanical weeding, pushing value per hectare higher. Insecticides are on track for a 6.17% CAGR due to climate-driven pest surges and neonicotinoid bans that demand more frequent but selective treatments. Fungicides contribute stable growth as wheat and vineyards fight intensified disease cycles. Niche segments such as molluscicides and nematicides cater to vegetables and potatoes and achieve above-average unit margins despite modest volume.

A wave of research focuses on mode-of-action innovation to satisfy ANSES toxicology thresholds. Companies able to pair novel active ingredients with digital prescriptions enjoy early adoption premiums. As precision spraying spreads, total liters applied may decline, but value resilience continues because products carry higher efficacy, resistance-management features, and regulatory compliance assurances. The France crop protection chemicals market share of herbicides remains dominant but its composition is shifting toward multi-site and biological blends.

By Application Mode: Foliar Dominance Faces Seed Treatment Challenge

Foliar sprays represented 45.35% of turnover in 2025, benefiting from versatile timing and existing equipment fleets. Even so, technology convergence is pushing the fastest 6.01% CAGR toward seed treatments, which deposit active ingredients directly on the seed surface and minimize field exposure. Syngenta’s and Corteva’s French coating plants demonstrate confidence in this delivery path. Chemigation, although still niche, gains relevance in drip-irrigated vineyards because it unites water and protection inputs. Soil fumigation and in-furrow treatments persist for high-value horticulture that tolerates premium inputs.

Precision agriculture is shrinking unintentional overlap and drift, lifting the cost-benefit ratio of advanced formulations. Growers who invested in GPS and optical sensors now tailor rates to stand counts or weed patches, reducing waste yet nurturing value per liter. Over time, the France crop protection chemicals market will likely see revenue gravity shift toward pre-programmed seed treatment packets, supported by data analytics that predict pest intensity.

By Crop Type: Grains and Cereals Drive Market Stability

Grains and cereals occupy 9.2 million hectares and draw 62.95% of 2025 demand within the France crop protection chemicals market. Wheat, maize, and barley top the list, explaining the outsized herbicide share. Climate volatility increases disease and insect pressure, prompting growers to layer more modes of action for resistance management, which underpins a 5.96% CAGR through 2031. Fruits and vegetables, concentrated along the Mediterranean coast, claim about one-fifth of sales yet command the highest value per hectare due to stringent residue limits. Commercial crops, such as sugar beet and rapeseed, contribute less, while turf and ornamentals remain specialty niches.

Food-safety regulations tighten maximum residue levels, pressing suppliers to refine degradation profiles and facilitate fast harvest-to-market intervals. As vineyards expand irrigation, fungicide sophistication will deepen. Hence diversification across crop types cushions the France crop protection chemicals market against regulatory swings in any single sector.

Geography Analysis

Northern grain belts, Hauts-de-France and Grand Est, anchor herbicide consumption, courtesy of dense wheat and barley rotations that necessitate multi-site weed management. Mediterranean departments present higher per-hectare spend because vegetables and vines require season-long fungicide and insecticide programs. The Loire Valley and Burgundy, with premium appellation wines, absorb advanced biocontrols to meet export tolerance thresholds. Brittany and Normandy livestock regions purchase forage-crop protection and grassland herbicides to secure feed quality under moist conditions.

Uniform ANSES governance and nationwide Écophyto 2030 objectives give suppliers a single regulatory playbook. Climatic gradients mean distinct timing and intensity patterns. Southern regions endure longer pest seasons and adopt chemigation and seed treatments earlier. Northern farms lean on drift-reducing boom technology to satisfy buffer-zone rules adjacent to villages. Organic density swings by county, from under 5% in some cereal plains to over 25% in peri-urban vegetable belts. Marketing strategies therefore weave national scale with regional tailoring, enabling firms to hold share across the France crop protection chemicals market. Government grants channeled through France 2030 and PARSADA funnel disproportionately into innovation clusters near Toulouse and Lyon, sustaining a domestic ecosystem of start-ups and research institutes. These hubs forge pilot trials that often become templates for European Union policy alignment, reinforcing France’s standing as an innovation nexus.

Competitive Landscape

Top-five companies, Syngenta, Bayer, Nufarm, BASF, and Corteva, captured an estimated 70% of 2024 revenue in the France crop protection chemicals market. Scale lets them digest compliance costs and sustain multi-crop portfolios. Syngenta leverages an expansive herbicide line and a strong distributor network to defend leadership. Bayer is channeling EUR 2 billion (USD 2.2 billion) globally into biological technologies, boosting its product flow through its Lyon facility. BASF’s acquisition of M2i Life Sciences in August 2024 widens its biocontrol options for vines and fruits.

Niche French players such as De Sangosse, Lallemand Plant Care, and Koppert France thrive on localized technical support and tight feedback loops with grower cooperatives. Their agility in biostimulants and beneficial insects secures premium positions even under moderate market concentration. Patent filings in biologicals reached 127 in 2024, indicating intensified R and D among incumbents and start-ups alike. Competitive success now prizes regulatory affairs capabilities, robust field-data packages, and alliances with digital farming platforms.

The Écophyto 2030 target forces every supplier to showcase stepwise reduction in environmental load. Consequently, pricing no longer aligns purely with kilograms applied but with efficacy-per-dose and compliance guarantees. Companies that integrate decision-support algorithms, on-farm sensors, and low-toxicity actives are fortifying customer lock-in and raising switching barriers.

France Crop Protection Chemicals Industry Leaders

BASF SE

Bayer AG

Corteva Agriscience

Nufarm Ltd

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: France’s environmental authority overruled a plan to reintroduce a banned neonicotinoid pesticide, citing risks to biodiversity and public health. This decision reflects France’s ongoing commitment to phasing out hazardous crop protection chemicals and tightening regulatory controls.

- July 2025: BASF initiated the construction of a fermentation plant in Ludwigshafen, Germany, for manufacturing chemical crop protection products, specifically fungicides and insecticides. The facility, though located in Germany, will serve European markets, including France, strengthening BASF's ability to meet the regional demand for crop protection solutions.

- January 2025: Sumitomo Chemical completed the acquisition of Philagro France, integrating its crop protection operations in the country. The acquisition expands its chemical pesticide portfolio and aligns with its objective to double sales in Europe by 2030.

France Crop Protection Chemicals Market Report Scope

Fungicide, Herbicide, Insecticide, Molluscicide, Nematicide are covered as segments by Function. Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type.Function

| Fungicide |

| Herbicide |

| Insecticide |

| Molluscicide |

| Nematicide |

Application Mode

| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

Crop Type

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

| Function | Fungicide |

| Herbicide | |

| Insecticide | |

| Molluscicide | |

| Nematicide | |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental |

Market Definition

- Function - Crop Protection Chemicals are apllied to control or prevent pests, including insects, fungi, weeds, nematodes, and mollusks, from damaging the crop and to protect the crop yield.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms