Floating Production Storage and Offloading (FPSO) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 9.03 Billion |

| Market Size (2031) | USD 13.43 Billion |

| Growth Rate (2026 - 2031) | 8.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | South America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Floating Production Storage and Offloading (FPSO) Market Analysis by Mordor Intelligence

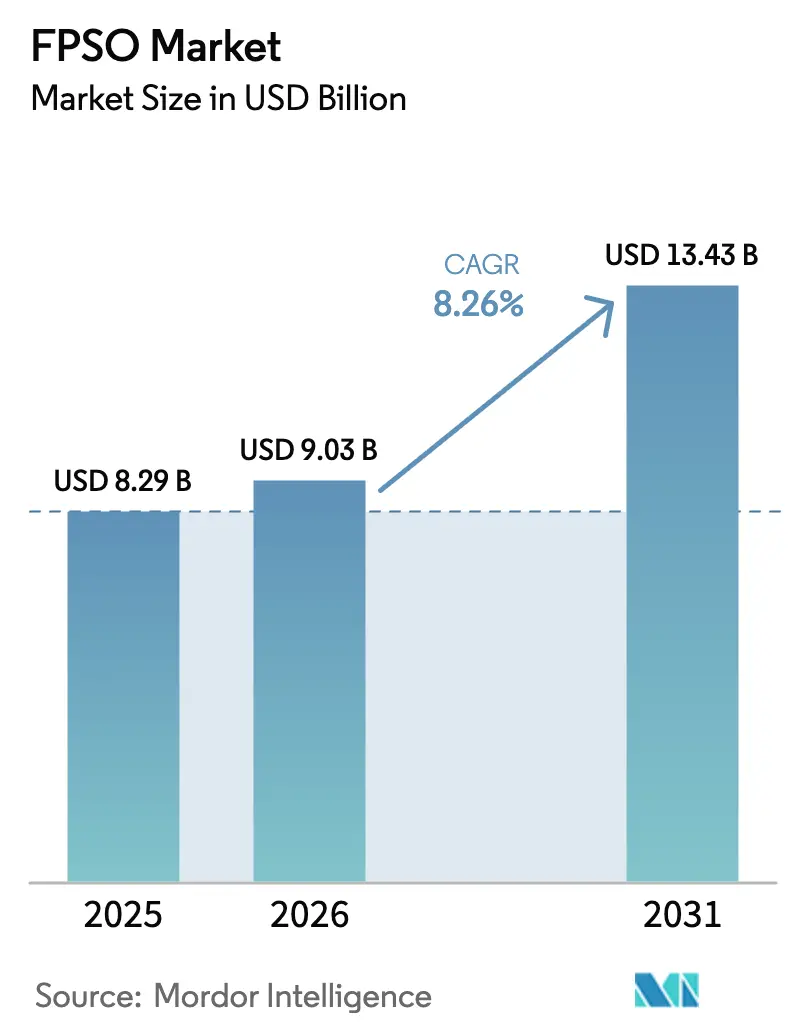

The Floating Production Storage and Offloading (FPSO) Market size was valued at USD 8.29 billion in 2025 and is estimated to grow from USD 9.03 billion in 2026 to reach USD 13.43 billion by 2031, at a CAGR of 8.26% during the forecast period (2026-2031).

Rising deep-water final investment decisions, the shift from onshore to offshore capital spending, and the spread of lease-and-operate procurement are expanding the Floating Production Storage and Offloading (FPSO) Market, while carbon-capture-ready topsides ensure compliance with Scope-1 emissions limits without sacrificing throughput.[1]SBM Offshore, “Annual Report 2024,” sbmoffshore.com South America delivered one-third of 2025 revenue as Brazil and Guyana sanctioned high-capacity units, and Asia-Pacific is pacing future growth on the back of Malaysia’s marginal-field program and Australia’s gas-condensate projects.[2]Petronas, “Press Release: FPSO Contracts for Marginal Fields,” petronas.com Converted tankers dominated 2025 demand, but orders for purpose-built newbuilds are climbing as operators confront ultra-deepwater loads above 2,000 tonnes.[3]TotalEnergies, “Engineering Standards 2024,” totalenergies.com The Floating Production Storage and Offloading (FPSO) Market is further buoyed by hybrid oil-and-gas units that monetize associated gas once flared under tighter methane rules.

Key Report Takeaways

- By type, converted tankers held 65.1% of the Floating Production Storage and Offloading (FPSO) Market share in 2025; purpose-built newbuilds are forecast to expand at a 9.7% CAGR to 2031.

- By hull type, single-hull units accounted for 58.9% of the Floating Production Storage and Offloading (FPSO) Market size in 2025, and double-hull designs are advancing at a 9.4% CAGR through 2031.

- By propulsion, self-propelled units commanded 67.5% of 2025 revenue and are projected to grow 8.6% annually to 2031.

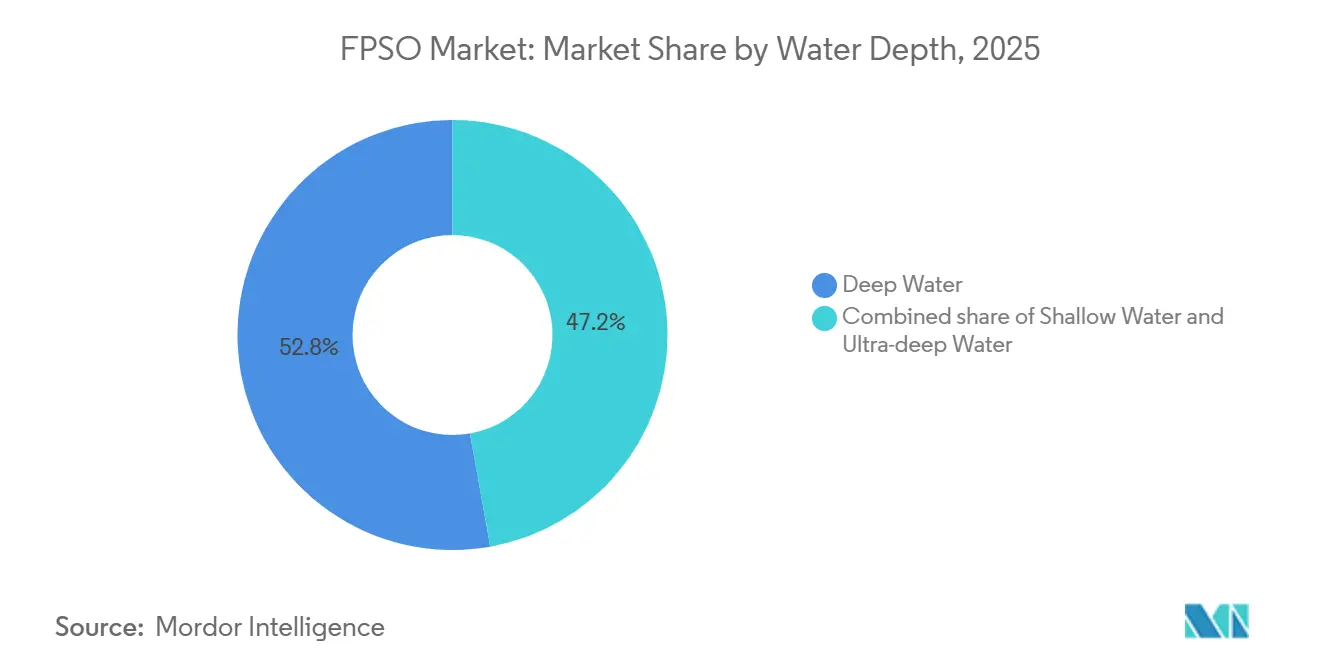

- By water depth, deep-water installations captured 52.8% of the 2025 value; ultra-deepwater projects led growth at a 9.3% CAGR.

- By storage capacity, FPSOs above 2 million barrels represented 40.4% of the 2025 value and are rising at an 8.5% CAGR.

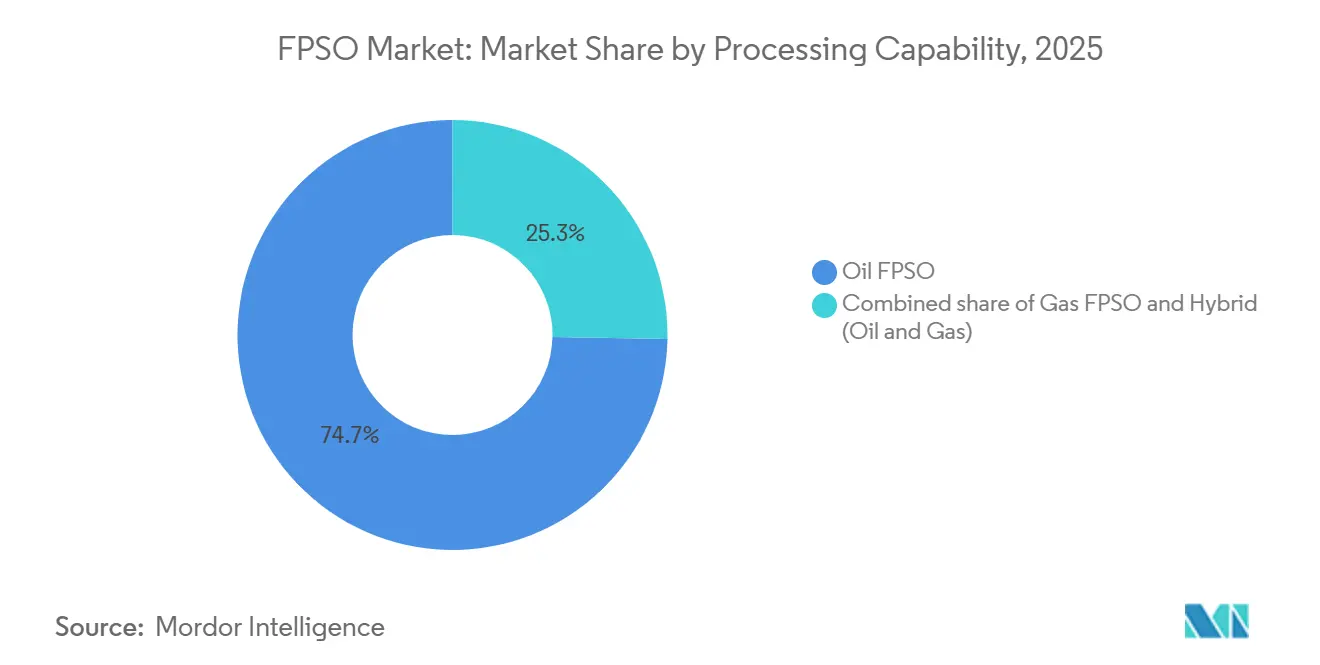

- By processing capability, oil-only units supplied 74.7% of 2025 throughput, while hybrid oil-and-gas FPSOs are expanding at a 10.2% CAGR to 2031.

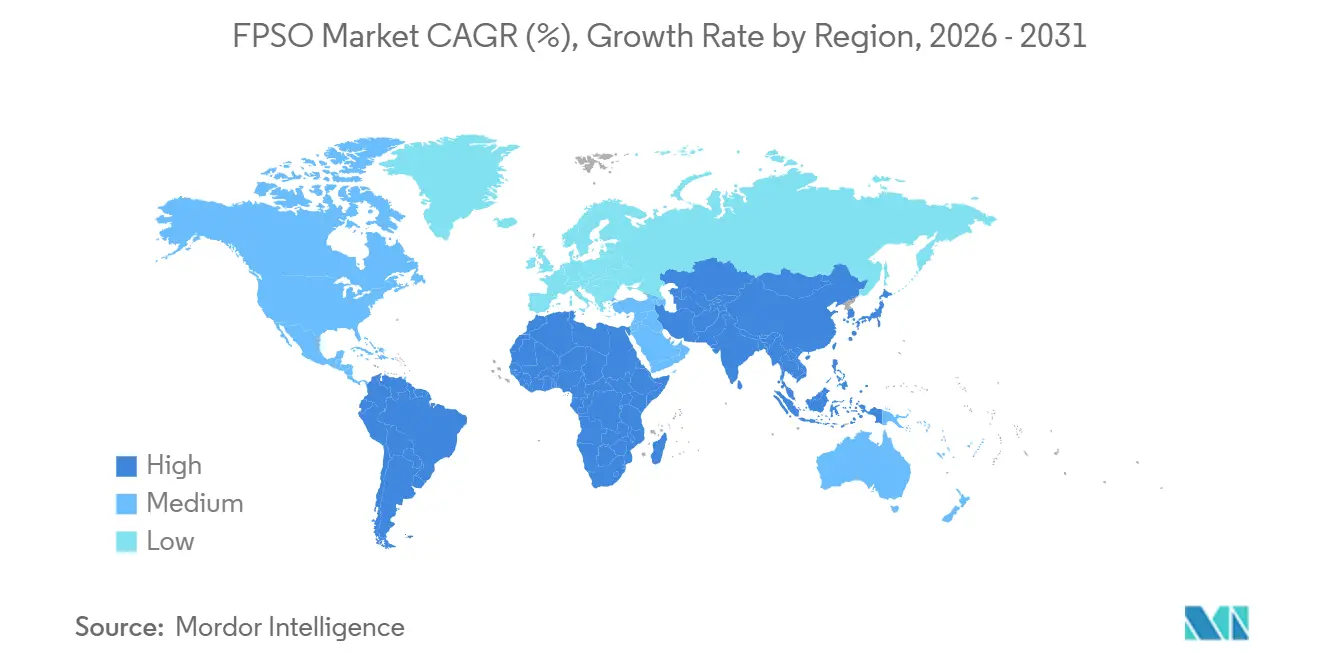

- By geography, South America led with 33.3% in 2025, while Asia-Pacific is set to advance at a 9.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Floating Production Storage and Offloading (FPSO) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic rebound in deep-water project FIDs | +1.8% | South America, West Africa | Medium term (2-4 years) |

| Depleting onshore reserves shifting CAPEX offshore | +1.5% | Middle East, North America, Asia-Pacific | Long term (≥ 4 years) |

| Turn-key lease models lowering operator CAPEX | +1.3% | South America, Asia-Pacific | Short term (≤ 2 years) |

| Redeployable midsize units unlocking marginal fields | +1.0% | Asia-Pacific, Middle East, West Africa | Medium term (2-4 years) |

| CCS-ready FPSO designs meeting Scope-1 targets | +1.2% | Europe, North America, Brazil | Long term (≥ 4 years) |

| Gas-focused FPSOs monetizing stranded gas | +1.4% | Middle East, Africa, Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Post-Pandemic Rebound in Deep-Water Project FIDs

Petrobras sanctioned four pre-salt FPSOs in 2025 valued at USD 18 billion, while ExxonMobil approved three 250,000 bpd units in Guyana’s Stabroek block - in stark contrast to the seven global awards during 2020-2021.[4]Petrobras, “Press Release: Petrobras Sanctions Four Pre-Salt FPSOs,” investidorpetrobras.com.br Pre-engineered hull programs trimmed decision cycles from 36 months to 24 months and improved early cash-flow visibility for contractors. Modular topsides preserve space to add carbon-capture units later, balancing current budgets with future regulatory compliance. With break-even costs near USD 35-40 per barrel, deep-water plays shield operator economics from price swings. The resulting backlog secures fabrication yards through 2028 and underpins confidence in the Floating Production Storage and Offloading (FPSO) Market.

Depleting Onshore Reserves Shifting CAPEX Offshore

Mature onshore reservoirs now decline 6-8% annually, steering capital toward offshore prospects where plateau profiles run 20 years. Saudi Aramco intends to devote 35% of upstream spending to offshore assets by 2028, up from 22% in 2023. Chevron’s Gulf of Mexico FPSOs already provide 18% of its total production, underscoring the permanence of this pivot. Petronas followed suit, awarding three FPSOs for marginal fields under 100 million barrels that cannot justify fixed platforms. The redirection sustains long-cycle demand in the Floating Production Storage and Offloading (FPSO) Market even as onshore shale efficiency improves.

Turn-Key Lease Models Lowering Operator CAPEX

Lease-and-operate contracts covered 72% of FPSO awards in 2024-2025, up from 58% in 2020-2021. Under these models, contractors finance construction and recover capital through 15-20-year day-rate streams, trimming operator upfront outlays by USD 1-1.5 billion per unit. Yinson’s Limbayong contract exemplifies the economics: a USD 1.2 billion build generates a USD 285,000 daily lease with an estimated 12% internal rate of return. The structure shifts operational risk to contractors, who must maintain ≥ 95% uptime or face penalties, promoting reliability and long-term service innovation in the Floating Production Storage and Offloading (FPSO) Market.

Redeployable Midsize Units Unlocking Marginal Fields

Converted Aframax and Suezmax tankers processing 30,000-80,000 bpd are reviving fields with 50-150 million-barrel reserves. BW Offshore’s Polvo FPSO, redeployed to the Maromba field after a USD 180 million refit, demonstrates a capital-light path to monetize assets that would otherwise remain stranded. Petronas has ordered three such units since 2024 to serve the Malay Basin, compressing payback periods to 8-10 years. Standardized topsides and quicker dry-dock cycles, now 18-24 months, make redeployment a strategic lever for the Floating Production Storage and Offloading (FPSO) Market where exploration risk is shifting toward smaller discoveries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX and long lead times | -1.1% | Asia-Pacific, Africa | Short term (≤ 2 years) |

| Oil-price volatility dampening FIDs | -1.4% | North America, Europe | Short term (≤ 2 years) |

| Dry-dock scarcity for life-extension conversions | -0.7% | Singapore, UAE, Brazil | Medium term (2-4 years) |

| Local-content mandates inflating costs | -0.9% | Brazil, Nigeria, Malaysia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX and Long Lead Times

Purpose-built units demand USD 1.5-3.5 billion and four-to-five-year execution windows, weighing on small operators’ balance sheets. Conversions reduce cost to USD 600 million-1.2 billion but still span 30-36 months, exposing projects to commodity swings and rising interest rates that lifted weighted-average capital costs from 7.5% to 9.2% in 2025. Steel-price volatility pushed contractors to adopt escalation clauses, adding complexity to budgeting. These dynamics moderate near-term growth, but leasing models partly offset the barrier.

Oil-Price Volatility Dampening FIDs

Brent fluctuations between USD 72-92 per barrel during 2024-2025 forced several operators to pause awards until price stability returns. Chevron deferred its Ballymore FPSO, and Shell suspended the Pierce redevelopment when Brent slipped below USD 75. Three-year hedges now cost 8-10% of notional value, eroding project margins and raising hurdles for speculative developments within the Floating Production Storage and Offloading (FPSO) Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Conversion Economics Favor Near-Term Awards

Converted tankers captured 65.1% of 2025 revenue within the Floating Production Storage and Offloading (FPSO) Market size thanks to 30-40% capex savings and 12-18-month lead-time advantages. Tightening VLCC supply as single-hull scrapping accelerates, restraining future conversions, yet redeployments of existing units keep near-term demand vibrant. Purpose-built hulls, expanding at a 9.7% CAGR, satisfy ultra-deepwater structural loads above 2,000 tonnes that conversions cannot economically meet. Petrobras’ Mero-5 demonstrates newbuild necessity, pairing a reinforced hull and 3.5 million-barrel storage to operate at 2,200 m water depth.

In the medium term, hybrid approaches such as SBM Offshore’s Fast4Ward, which fabricates standardized hulls in China before topside customization, aim to blend newbuild integrity with conversion speed, sustaining technological momentum in the Floating Production Storage and Offloading (FPSO) Market.

By Hull Type: Double-Hull Gains on Safety Mandates

Single-hull units still represent 58.9% of the installed fleet, but double-hull FPSOs are growing 9.4% annually under IMO and North Sea regulations that require enhanced spill protection. Shell’s Penguins redevelopment selected a double-hull despite a 12% premium, citing insurance savings and lower environmental liability. Retrofitting older single-hulls with double-bottom plating, as BW Offshore did on Polvo, offers a bridge solution until replacement becomes mandatory. Insurers now add 15-20% surcharges for single-hulls in sensitive areas, reinforcing a structural pivot in the Floating Production Storage and Offloading (FPSO) Market.

Double-hull void spaces also house ballast systems that cut weather downtime by roughly 10 days annually, an operational edge attractive to lease-and-operate contractors who depend on uptime-indexed day rates.

By Propulsion: Self-Propelled Dominates Repositioning Needs

Self-propelled FPSOs held 67.5% of 2025 revenue and are forecast to rise 8.6% annually, prized for autonomous disconnect and sail-away during hurricanes without tug support. Chevron’s Jack/St. Malo relocated ahead of Hurricane Beryl in 2024, averting a USD 400 million damage risk. Self-propelled designs command lease premiums but reduce downtime, an attractive trade-off in volatile weather belts. Towed FPSOs remain valid in benign seas, freeing topside space for processing modules and lowering build cost, yet they rely on third-party tugs at USD 150,000-250,000 per day for repositioning.

The divergence leaves the Floating Production Storage and Offloading (FPSO) Market balancing cost and resilience, with self-propulsion gradually becoming the default spec where extreme weather frequency is climbing.

By Water Depth: Ultra-Deepwater Technology Unlocks Reserves

Deep-water projects (1,500-3,000 m) captured 52.8% of the 2025 value, while ultra-deepwater units over 3,000 m water depth are expanding 9.3% annually. Polyester mooring lines, 40% lighter than chain, and titanium stress joints extend riser fatigue life to 25 years, unlocking high-pressure reservoirs in Brazil and the Gulf of Mexico. Installation bottlenecks exist: only 18 vessels worldwide lift 3,000-tonne turrets, adding 6-9 months to schedules. Disconnectable turrets, as on TotalEnergies’ Lapa North-East, cost an extra USD 120 million but are mandated for iceberg drift zones.

As reservoirs migrate deeper, the Floating Production Storage and Offloading (FPSO) Market size stands to benefit from premium specifications that raise unit economics and entry barriers.

By Storage Capacity: Mega-Projects Drive Large Tanks

FPSOs storing above 2 million barrels commanded 40.4% of 2025 revenue and are growing 8.5% as Brazil’s Búzios and Mero fields benchmark 7-10-day offloading cycles. Large tanks lower per-barrel shuttle costs by around 15-20% and improve uptime in rough seas. ExxonMobil’s Liza Unity, at 1.6 million barrels, showed 98.5% uptime in 2024, validating mid-range capacity. Below-1-million-barrel units remain viable for North Sea fields close to shore.

Advances such as heated coil systems keep crude above wax-precipitation temperature, supporting reliable offloading and reinforcing an efficiency trend that supports revenue growth in the Floating Production Storage and Offloading (FPSO) Market.

By Processing Capability: Hybrid Units Capture Gas Value

Oil-only platforms delivered 74.7% of 2025 throughput, but hybrid oil-and-gas FPSOs are climbing 10.2% annually as flare penalties escalate. BP’s Greater Tortue Ahmeyim, due in late 2025, integrates dual-train liquefaction to process 2.3 million t LNG per year and 40,000 bpd condensate. Gas modules add USD 400-600 million to capex yet yield > 15% IRRs when LNG prices exceed USD 8 per million BTU. Flare-gas compressors, like Petrobras’ P-77 retrofit, cut methane intensity by two-thirds, aligning operational economics with ESG goals and unlocking additional revenue streams in the Floating Production Storage and Offloading (FPSO) Market.

Geography Analysis

South America generated 33.3% of the 2025 Floating Production Storage and Offloading (FPSO) Market revenue, led by Brazil’s 18 active units producing 2.1 million bpd at break-even costs near USD 35-40 per barrel. Guyana added three FPSOs between 2024-2025 and targets 800,000 bpd by 2027, reshaping regional rankings. Local-content rules inflate budgets by 10-15% but cultivate a 45,000-person supply chain across Brazilian yards.

Asia-Pacific is the fastest-growing territory, rising 9.9% annually to 2031. Petronas awarded Lang Lebah, Limbayong, and Jerun, each with under 150 million-barrel reserves, serviced by redeployable units. Australia’s Barossa FPSO adds cyclone-proof disconnectable turrets, while India commissioned its first deep-water unit in Mumbai High, signaling diversification. China’s state-owned CNOOC maintains cost advantages through domestic yards, yet its units seldom compete abroad due to technology-transfer constraints.

The Middle East and Africa collectively delivered 22% of the 2025 value. ADNOC’s USD 2.8 billion sour-gas FPSO incorporates acid-gas injection to sequester 2.3 million t CO₂ annually, dovetailing with the UAE’s net-zero program. Nigeria’s Bonga South-West and Angola’s mid-life Agogo projects exemplify replacement demand in maturing basins. North America and Europe held 18% of revenue as Gulf of Mexico and Norwegian North Sea operators pivot toward carbon-capture-ready specifications under stringent environmental frameworks.

Competitive Landscape

Top contractors, SBM Offshore, MODEC, BW Offshore, Yinson, and Bumi Armada, controlled roughly 60% of the global order book worth USD 48 billion as of mid-2025, reflecting moderate concentration in the Floating Production Storage and Offloading (FPSO) Market. SBM’s Fast4Ward reduced engineering-to-sail-away time to 38 months, winning eight awards since 2022. MODEC’s internal turret technology halves disconnect time to six hours, critical in hurricane regions. Chinese yards, COOEC, COSCO, and Dalian, bid 15-20% below Western peers on conversions but face adoption hurdles where advanced turret or CCS modules are required.

Innovation centers on carbon-capture retrofits and digital-twin maintenance. Equinor estimates a USD 3-5 billion retrofit market as 2030 emissions deadlines approach. Seatrium leverages digital twins to cut unplanned downtime by 18% under performance-based leases. Lease-and-operate procurement now underpins 72% of awards, shifting competition from capex cost to operational excellence and financing capacity, an axis that favors contractors with strong balance sheets and established uptime records.

Floating Production Storage and Offloading (FPSO) Industry Leaders

SBM Offshore N.V.

Modec Inc.

BW Offshore Ltd.

Yinson Holdings Bhd.

Bumi Armada Bhd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: BW Energy has renamed its former FPSO Polvo to BW Maromba and is refurbishing it in China for deployment in Brazil's Maromba field. The refurbished FPSO, designed for oil processing and offloading, is a key component in plans to access over 120 million barrels of crude, enhancing production capacity and supporting development in the Campos Basin.

- September 2025: The BW Opal FPSO, a key component of Santos’ Barossa LNG offshore development in northern Australia, has commenced production operations with the receipt of first gas. The floating production, storage, and offloading vessel has a capacity to process up to 850 million standard cubic feet of gas per day and manages condensate as the project advances toward full commissioning and LNG exports.

- August 2025: Yinson Holdings' largest FPSO, the Agogo FPSO, began operations under a 15-year charter agreement with Azule Energy off the coast of Angola, with a contract value exceeding US$5 billion. The vessel achieved first oil ahead of schedule and incorporates emissions-reducing technologies, including carbon capture.

- February 2025: SBM Offshore entered into a study agreement with Petrobras to assess carbon capture modules for future Floating Production Storage and Offloading (FPSO) vessels. The study incorporates Mitsubishi Heavy Industries’ CO₂ capture technology and SBM’s Fast4ward® design. It aims to lower emissions from FPSO gas turbines and evaluate different configurations for deployment on Petrobras fields as part of the emissionZERO® initiative.

Global Floating Production Storage and Offloading (FPSO) Market Report Scope

FPSO stands for floating production, storage, and offloading. It is a type of offshore vessel used in the oil and gas industry for producing, processing, storing, and offloading hydrocarbons. FPSOs are typically deployed in offshore fields where it is not feasible or economically viable to build fixed production platforms.

The Floating Production Storage and Offloading (FPSO) Market is segmented by type, hull type, propulsion, water depth, storage capacity, processing capability, and geography. By type, the market is segmented into converted tankers, purpose-built newbuilds. By hull type, the market is divided into double-hull and single-hull. By propulsion, the market is segmented into self-propelled FPSO, towed FPSO. By water depth, the market is segmented into shallow water, deep water, and ultra-deep water. By storage capacity, the market is divided into below 1 Mn Bbl, 1 to 2 Mn Bbl, and above 2 Mn Bbl. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The report offers the market sizes and forecasts in revenue (USD) for all the above segments.

| Converted Tanker |

| Purpose-built (Newbuild) |

| Double Hull |

| Single Hull |

| Self-Propelled FPSO |

| Towed FPSO |

| Shallow Water |

| Deep Water |

| Ultra-deep Water |

| Below 1 Mn Bbl |

| 1 to 2 Mn Bbl |

| Above 2 Mn Bbl |

| Oil FPSO |

| Gas FPSO |

| Hybrid (Oil and Gas) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Spain | |

| France | |

| Italy | |

| Norway | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Singapore | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Egypt | |

| Algeria | |

| Rest of Middle East and Africa |

| By Type | Converted Tanker | |

| Purpose-built (Newbuild) | ||

| By Hull Type | Double Hull | |

| Single Hull | ||

| By Propulsion | Self-Propelled FPSO | |

| Towed FPSO | ||

| By Water Depth | Shallow Water | |

| Deep Water | ||

| Ultra-deep Water | ||

| By Storage Capacity | Below 1 Mn Bbl | |

| 1 to 2 Mn Bbl | ||

| Above 2 Mn Bbl | ||

| By Processing Capability | Oil FPSO | |

| Gas FPSO | ||

| Hybrid (Oil and Gas) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Spain | ||

| France | ||

| Italy | ||

| Norway | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Singapore | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Egypt | ||

| Algeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Floating Production Storage and Offloading (FPSO) Market in 2026?

The Floating Production Storage and Offloading (FPSO) Market size is projected to exceed USD 9.03 billion in 2026, tracking the 8.26% CAGR toward USD 13.43 billion by 2031.

Which region grows fastest for FPSO demand through 2031?

Asia-Pacific expands at a 9.9% CAGR, spurred by Malaysia's marginal fields and Australia's gas-condensate developments.

Why are lease-and-operate contracts popular for FPSOs?

They cut operator upfront costs by USD 1-1.5 billion per unit and shift reliability risk to contractors committed to over 95% uptime.

What drives the move toward double-hull FPSOs?

Environmental mandates and insurance surcharges on single-hull units make double-hull designs safer and more cost-effective over the life of the vessel.

How do hybrid oil-and-gas FPSOs create value?

By processing associated gas into LNG, hybrid units generate additional revenue streams and comply with stricter flaring penalties, often yielding > 15% IRRs.

Page last updated on: