Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

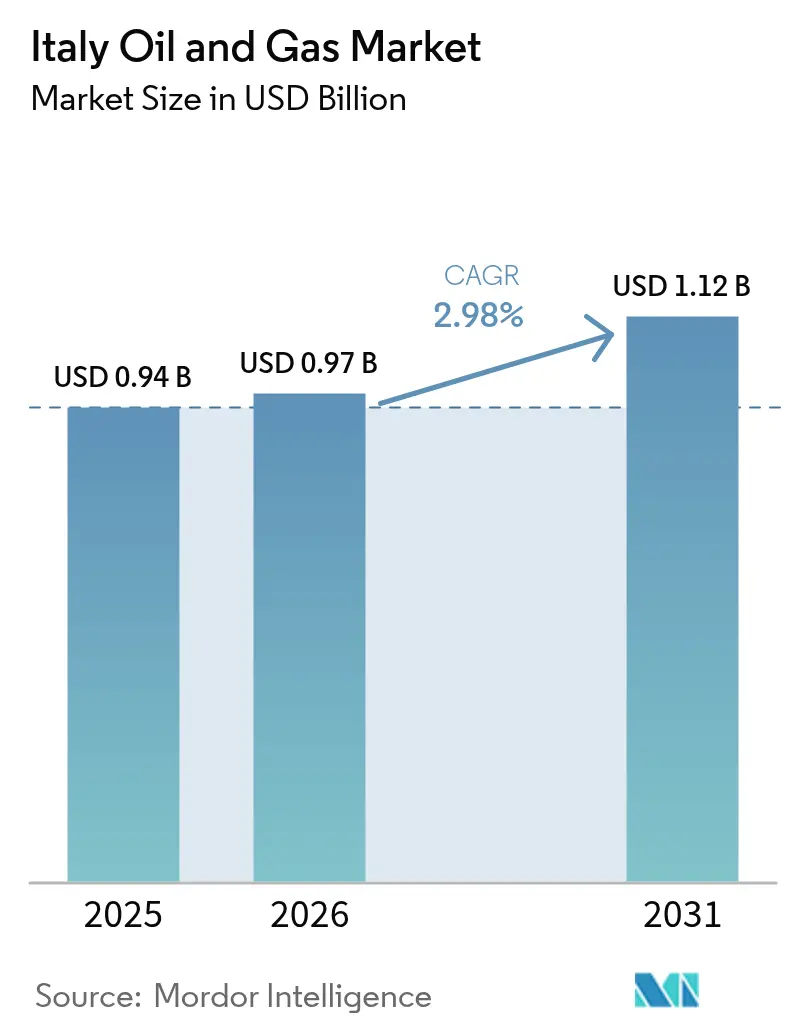

| Base Year Market Size (2025) | USD 0.94 Billion |

| Market Size (2026) | USD 0.97 Billion |

| Market Size (2031) | USD 1.12 Billion |

| Growth Rate (2026 - 2031) | 2.98% CAGR |

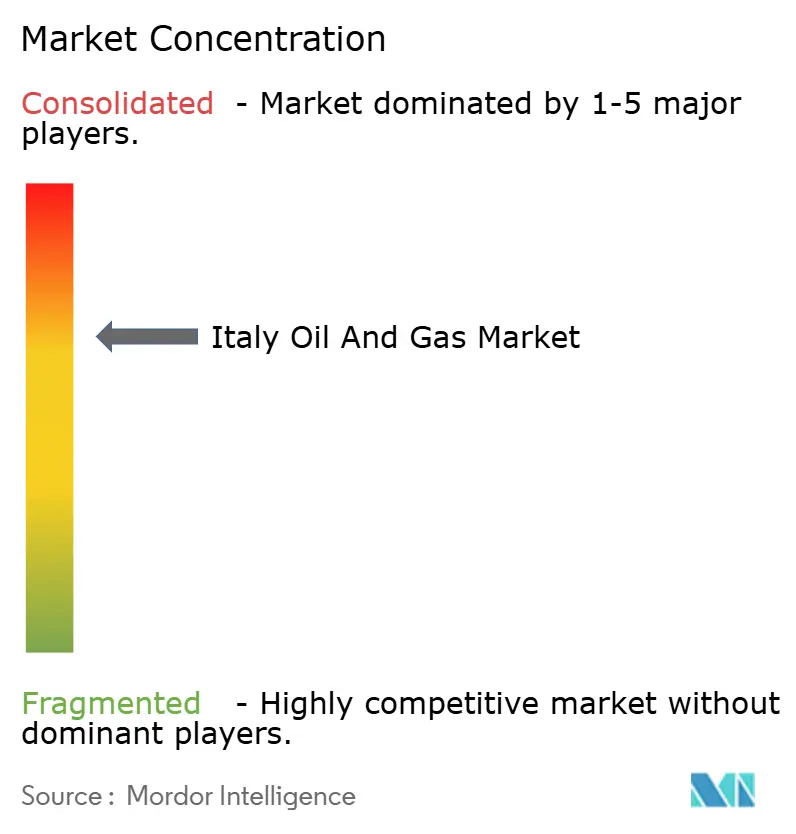

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Oil And Gas Market Analysis by Mordor Intelligence

The Italy Oil And Gas Market size was valued at USD 0.94 billion in 2025 and estimated to grow from USD 0.97 billion in 2026 to reach USD 1.12 billion by 2031, at a CAGR of 2.98% during the forecast period (2026-2031).

Infrastructure-led resilience underpins this trajectory as the country accelerates its LNG import capacity, converts refineries to bio-processing facilities, and prepares hydrogen-compatible pipelines. Upstream activity remains dominated by mature Adriatic platforms that demand intensive maintenance, while midstream operators invest in hydrogen-ready assets to diversify revenue streams. Offshore CO₂-storage pilots and expanding small-scale LNG bunkering provide new commercial opportunities that partially offset declines in domestic production. Policy clarity around the September 2024 offshore exploration ban reshapes capital allocation; yet, integrated majors continue to leverage existing assets for blue-hydrogen, CCS, and biofuel ventures, ensuring the Italian oil and gas market remains relevant during the wider energy transition.

Key Report Takeaways

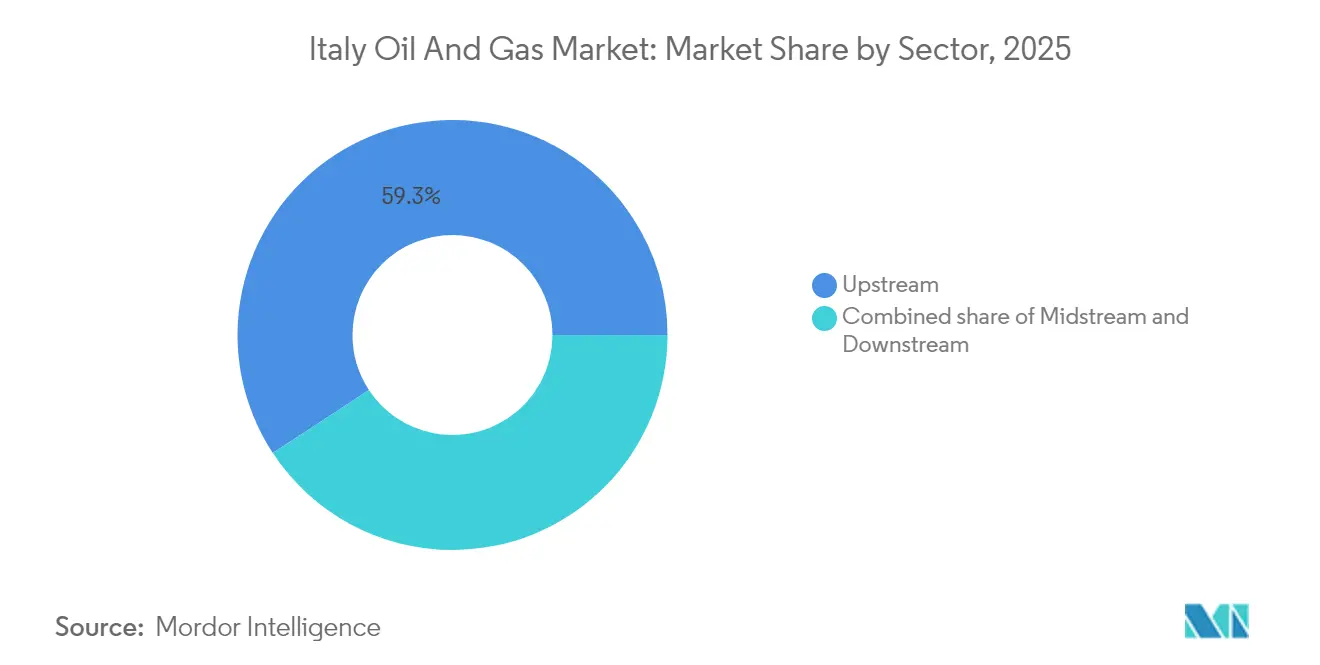

- By sector, upstream operations held 59.25% of Italy's oil and gas market share in 2025, whereas the midstream segment is projected to record the fastest growth, with a 4.27% CAGR through 2031.

- By location, offshore assets commanded an 85.60% share of Italy's oil and gas market size in 2025, and this segment is also expected to remain the fastest-growing at a 3.45% CAGR through 2031.

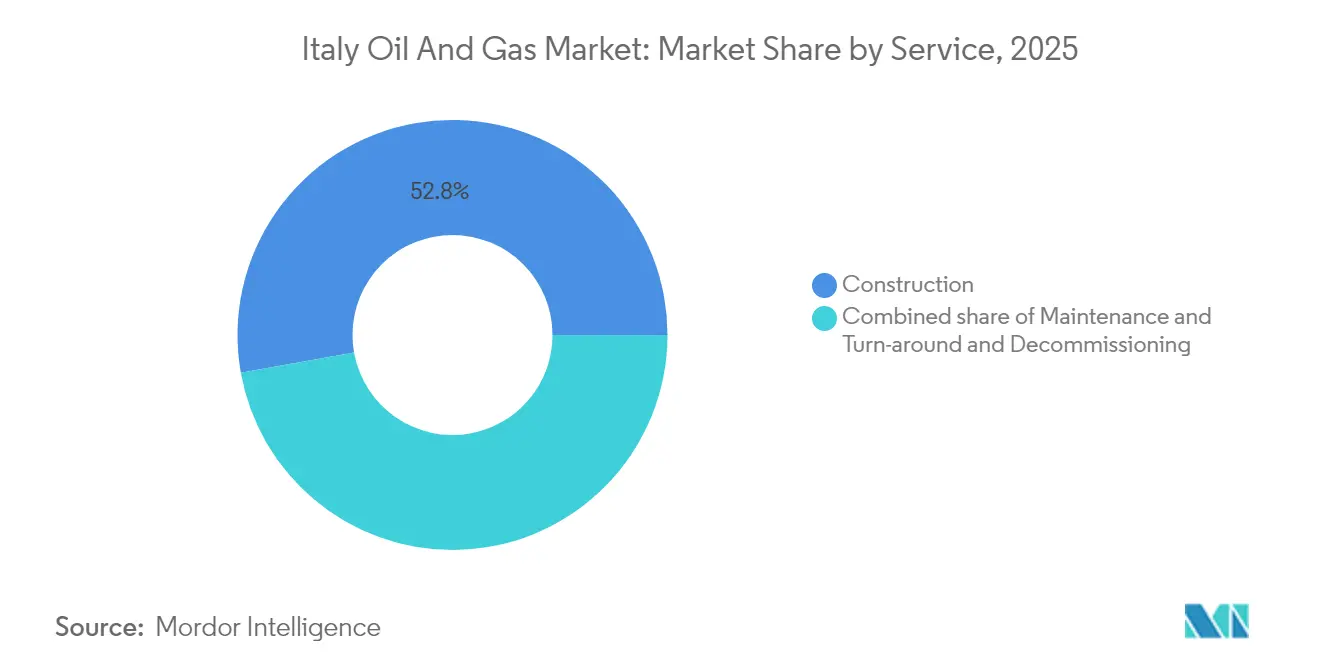

- By service, construction services led with a 52.80% share of the Italian oil and gas market size in 2025, but decommissioning services are advancing at a 6.03% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Oil And Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diversification push after Russian-gas supply crisis | +0.9% | Global, with concentrated effects in Northern Italy industrial hubs | Short term (≤ 2 years) |

| Surging natural-gas demand for power generation | +0.8% | National, with peak demand in Po Valley and Southern Italy | Medium term (2-4 years) |

| LNG import expansion (Piombino & Ravenna FSRUs) | +0.6% | Adriatic coast and Tyrrhenian Sea regions, spill-over to Central Europe | Medium term (2-4 years) |

| Refinery upgrades & bio-refinery conversions | +0.5% | Sicily, Sardinia, and mainland coastal refineries | Long term (≥ 4 years) |

| Offshore CO₂-storage hubs enabling blue-hydrogen clusters | +0.4% | Adriatic Sea offshore fields, Northern Italy industrial clusters | Long term (≥ 4 years) |

| Growth in small-scale LNG bunkering for Adriatic shipping | +0.3% | Adriatic ports (Venice, Trieste, Bari), with expansion to Mediterranean routes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Diversification Push After Russian-Gas Supply Crisis

Russia supplied 40% of Italy's gas in 2021, but this share fell to under 5% by 2024, as emergency legislation enabled the rapid approval of LNG terminal projects and alternative pipeline deals with Algeria and Azerbaijan.[1]Snam, “Annual Report 2024,” snam.it The EUR 4 billion national security package funded two FSRUs, which together add 10 billion m³ of annual capacity, thereby strengthening supply flexibility. Algerian pipeline flows rose to 32% of 2024 imports, while new U.S. and Qatari LNG cargoes reached Piombino and Ravenna, anchoring Italy's role as a Central European gas gateway. Storage fill rates above 90% ahead of winter 2025 underscore improved resiliency, and midstream contractors benefit from accelerated compression-station and metering upgrades. The structural reshaping of supply chains solidifies Italy's position as the Mediterranean conduit for diversified gas flows, extending well beyond the immediate crisis horizon.

Surging Natural-Gas Demand for Power Generation

Gas-fired plants accounted for 48% of national electricity in 2024, up from 43% in 2019, as coal closures and renewable energy intermittency necessitated the need for fast-ramping capacity. Efficiency gains in combined-cycle turbines lowered marginal costs, making gas the preferred balancing fuel, especially during winter peaks when industrial heating coincides with subdued solar output. Data-center investments in Apulia and Campania drive additional baseload requirements, and developers are increasingly signing long-term gas supply contracts to hedge against price volatility. These dynamics establish a medium-term demand floor that supports further growth in Italy's oil and gas market, despite long-term decarbonization targets.

LNG Import Expansion (Piombino & Ravenna FSRUs)

The Piombino FSRU received its first LNG cargo in April 2025, delivering 5 billion m³ of annual regasification capacity. Meanwhile, Ravenna’s BW Singapore unit is expected to bring an equivalent volume online by early 2026. Both vessels are moored near existing pipeline corridors, enabling swift gas dispatch to industrial demand centers in the north and offering re-export optionality toward Austria and Germany. Integrated small-scale loading arms at the terminals create new revenue from truck and bunkering services, further diversifying income streams. The EUR 1.2 billion combined investment triggers demand for cryogenic equipment, mooring systems, and class certifications, firmly anchoring midstream momentum within the Italy oil and gas market.

Refinery Upgrades & Bio-Refinery Conversions

Eni has invested EUR 2 billion to convert its Livorno, Venice, and Gela sites, increasing annual biofuel output by 1.2 million tons by 2027.[2]Eni, “Eni Confirms the Conversion of the Livorno Refinery,” eni.com The Livorno conversion, authorized in September 2024, integrates Honeywell UOP Ecofining™ technology to process 500,000 tons of waste oils into renewable diesel and sustainable aviation fuel. These projects comply with EU Renewable Energy Directive mandates and yield premium margins over conventional refining. EPC firms secure multi-year contracts for hydrogen units, catalyst change-outs, and digital control upgrades, sustaining downstream services through the transition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating renewable-energy competitiveness | -0.6% | National, with strongest impact in Southern Italy and Sicily solar/wind zones | Medium term (2-4 years) |

| Mature domestic reserves & declining production | -0.5% | Adriatic Sea offshore fields, Po Valley onshore fields | Short term (≤ 2 years) |

| Strict offshore drilling moratoria & seismic rules | -0.4% | Italian territorial waters, particularly protected marine areas | Long term (≥ 4 years) |

| Slow permitting for midstream expansions | -0.3% | National, with regulatory bottlenecks in Rome and regional authorities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Renewable-Energy Competitiveness

Solar and wind capacity reached 60 GW in 2024, supplying 35% of generation and achieving EUR 40/MWh levelized costs in Sicily. Grid-scale battery deployments begin to smooth hourly volatility, trimming gas peaker dispatch during midday solar peaks. The National Recovery and Resilience Plan allocates EUR 15 billion for additional renewable energy sources through 2026, signaling an intensification of competition for gas in the power mix. Yet seasonal variability and the absence of long-duration storage maintain a reserve role for flexible gas plants, mitigating immediate displacement risks for the Italy oil and gas market.

Mature Domestic Reserves and Declining Production

Adriatic output fell 15% between 2019 and 2024 as aging fields such as Clara and Annamaria neared depletion limits despite infill drilling. Artificial-lift and water-injection costs now erode margins on shallow-water wells, prompting operators to schedule 12 platform removals by 2028. While this dynamic trims upstream growth, it simultaneously unlocks decommissioning demand and repurposing opportunities for CO₂ storage. The decline in net national production, however, pushes dependency onto pipeline and LNG imports, influencing midstream tariff structures and storage strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Midstream Infrastructure Drives Growth

Midstream activities are projected to account for a 4.27% CAGR to 2031, a faster pace than any other sector within the Italian oil and gas market. Snam's EUR 8.1 billion capital plan includes 1,200 kilometers of hydrogen-ready pipelines and 4 billion cubic meters of new storage, expanding Italy's oil and gas market size for midstream services alongside tariff-backed earnings. Cross-border interconnections such as the Adriatic Line enhance north-south flexibility, reinforce transit revenue, and create optionality for future hydrogen blends. Upstream remains the largest revenue source but faces plateauing production volumes, prompting service providers to shift toward maintenance and brownfield enhancement projects that generate predictable, albeit slower, revenue streams.

A robust downstream conversion trend also manifests. Bio-refineries supply premium fuels that fetch higher margins than traditional products, moderating the impact of tightening European fuel-spec standards. The sector therefore evolves from volume-driven processing to margin-driven specialty fuels, a shift that keeps Italy oil and gas market players engaged across the full value chain while meeting EU taxonomy criteria for sustainable operations.

By Location: Offshore Dominance Faces Transition Pressures

Offshore assets represent 85.60% of 2025 revenue and remain central to Italy's oil and gas market share despite a 3.45% CAGR cap through 2031. The shallow-water Adriatic environment supports cost-efficient tie-backs and life-extension programs, yet stricter seismic norms and the September 2024 exploration ban curtail frontier drilling. Operators redirect capital toward asset integrity, digital twins for predictive maintenance, and eventual conversion of depleted fields into CO₂ sinks, maintaining revenue continuity while satisfying environmental mandates.

Onshore opportunities center on the Po Valley, where brownfield wells transition into geothermal or storage functions. Although the onshore contribution to Italy's oil and gas market size is modest, lower permitting hurdles and shorter cycle times offer niche earnings for specialized service firms. The combination of offshore maturity and onshore adaptability creates a balanced, albeit cautious, outlook for locations.

By Service: Decommissioning Accelerates as Construction Leads

Construction services accounted for 52.80% of Italy's oil and gas market size in 2025, thanks to LNG terminal build-outs, pipeline loops, and refinery retrofits. The surge, however, eases after 2025 as major assets reach mechanical completion, leading to a shift in growth momentum toward decommissioning services, which post a 6.03% CAGR through 2031. Italy's 47 offshore platforms have an average service life of 35 years, making the removal of structures, plugging of wells, and site remediation critical compliance tasks. Premium day-rates for heavy-lift vessels and specialized cutting equipment support margin expansion for experienced contractors.

Routine maintenance remains a stable revenue pillar. Aging platforms require enhanced fire and gas detection, cathodic protection, and emissions monitoring that align with EU methane regulations. These ongoing needs ensure a diversified workload, even as greenfield activity moderates, underpinning service segment resilience in the Italian oil and gas market.

Geography Analysis

Northern Italy consumes 45% of the nation's gas, primarily anchored by the Po Valley's industrial corridor, which relies on both Algerian imports via TransMed and Azerbaijani flows through the Trans Adriatic Pipeline. Elevated winter demand squeezes regional capacity, triggering incremental compression projects and strategic storage drawdowns that stabilize grid pressure. Central European shippers increasingly nominate Italian exit points, converting the country into a fee-generating transit hub.

Southern regions exhibit contrasting dynamics. Sicily hosts two major refineries undergoing biofuel conversion, while abundant solar and wind output intermittently reduces local gas offtake. Seasonal swings create market volatility that pipeline operators mitigate through line-pack management and flexible tariffs. Additionally, the coastal Sicilian ports position the island as a future LNG break-bulk center for North African gas streams, extending Italy's influence in the oil and gas market into the wider Mediterranean.

The Adriatic coastline concentrates upstream production, LNG reception, and nascent CCS initiatives. Ravenna exemplifies vertical integration: offshore wells feed existing gas plants, new FSRU capacity injects fresh supply, and depleted reservoirs transition into CO₂ stores. This geographic stacking optimizes logistics and workforce allocation, although it heightens environmental scrutiny and necessitates rigorous stakeholder engagement to ensure project timelines are secured.

Competitive Landscape

Italy’s oil and gas sector is moderately concentrated, with Eni leading an integrated portfolio spanning legacy reservoirs to renewable fuels. The company leverages proprietary enhanced-oil-recovery chemistries and digital optimization suites to prolong field life, while redirecting spare cash toward bio-refinery projects that meet EU directives. Snam dominates regulated midstream assets—operating 38,000 kilometers of pipelines, 16.9 billion cubic meters of storage, and three regasification sites—granting it tariff-backed revenue that funds hydrogen-ready retrofits.[3]Snam, “1H 2024 Results Presentation,” snam.it

International companies, such as TotalEnergies and Shell, compete in downstream retail and petrochemicals, leveraging their global trading books to secure feedstock flexibility. Smaller independent producers struggle with capital intensity and compliance costs, prompting consolidation exemplified by Vitol’s EUR 550 million acquisition of Saras’ refinery stake in 2024. Technology adoption acts as a differentiator; digital twins, predictive analytics, and low-carbon process upgrades lower operating costs and carbon footprints, reshaping competitive rankings within the Italy oil and gas market

Italy Oil And Gas Industry Leaders

Eni SpA

Snam SpA

Saras SpA

Sonatrach Raffineria Italiana (Augusta)

API Group (Ancona refinery & retail)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Energean, a London-based oil and gas player, has resumed production at its Italian field located off the coast of Abruzzo.

- September 2024: Italy enacted a ban on new offshore exploration permits, affecting 12 pending Adriatic applications.

- July 2024: Eni and EIB ink EUR 500 million deal to transform Italy's Livorno refinery into a biorefinery.

- January 2024: Snam, an Italian gas company, announced plans to invest USD 12.51 billion in gas and liquefied natural gas (LNG) infrastructure in Italy by 2027. Compared to the 2022-26 plan, the company's investment increased by 15%.

Italy Oil And Gas Market Report Scope

The oil and gas market refers to the industry involved in the exploration, production, refining, transportation, and distribution of oil and natural gas resources. It encompasses various activities and sectors related to the extraction and utilization of hydrocarbon reserves.

The Italian oil and gas market is segmented by sector into upstream, midstream, and downstream. For each segment, market sizing and forecasts were made based on production (thousand barrels per day).

By Sector

| Upstream |

| Midstream |

| Downstream |

By Location

| Onshore |

| Offshore |

By Service

| Construction |

| Maintenance and Turn-around |

| Decommissioning |

| By Sector | Upstream |

| Midstream | |

| Downstream | |

| By Location | Onshore |

| Offshore | |

| By Service | Construction |

| Maintenance and Turn-around | |

| Decommissioning |

Key Questions Answered in the Report

What is the current value and projected growth rate of Italy’s oil and gas sector?

It is valued at USD 0.97 billion in 2026 and is projected to reach USD 1.12 billion by 2031, advancing at a 2.98% CAGR.

Which segment is expanding the fastest?

Midstream operations—driven by hydrogen-ready pipelines and new LNG terminals—are forecast to grow at a 4.27% CAGR through 2031.

How much LNG regasification capacity do the Piombino and Ravenna FSRUs add?

Together they supply an extra 10 billion m³ of annual capacity, enough to cover about 16% of national gas demand.

Why do offshore assets dominate national production?

Mature Adriatic platforms still account for 85.60% of oil and gas revenue because of decades of legacy infrastructure and shallow-water accessibility.

What role do bio-refineries play in the energy transition?

Eni’s conversions at Livorno, Venice and Gela will add 1.2 million tons of renewable fuel output by 2027, improving margins while meeting EU decarbonization mandates.

How concentrated is corporate control of the sector?

A combined share slightly above 60% for the top five players yields a moderate concentration score of 6 on a 1-to-10 scale.

Page last updated on: