Oil And Gas Accumulator Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 658.55 Million |

| Market Size (2031) | USD 826.09 Million |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

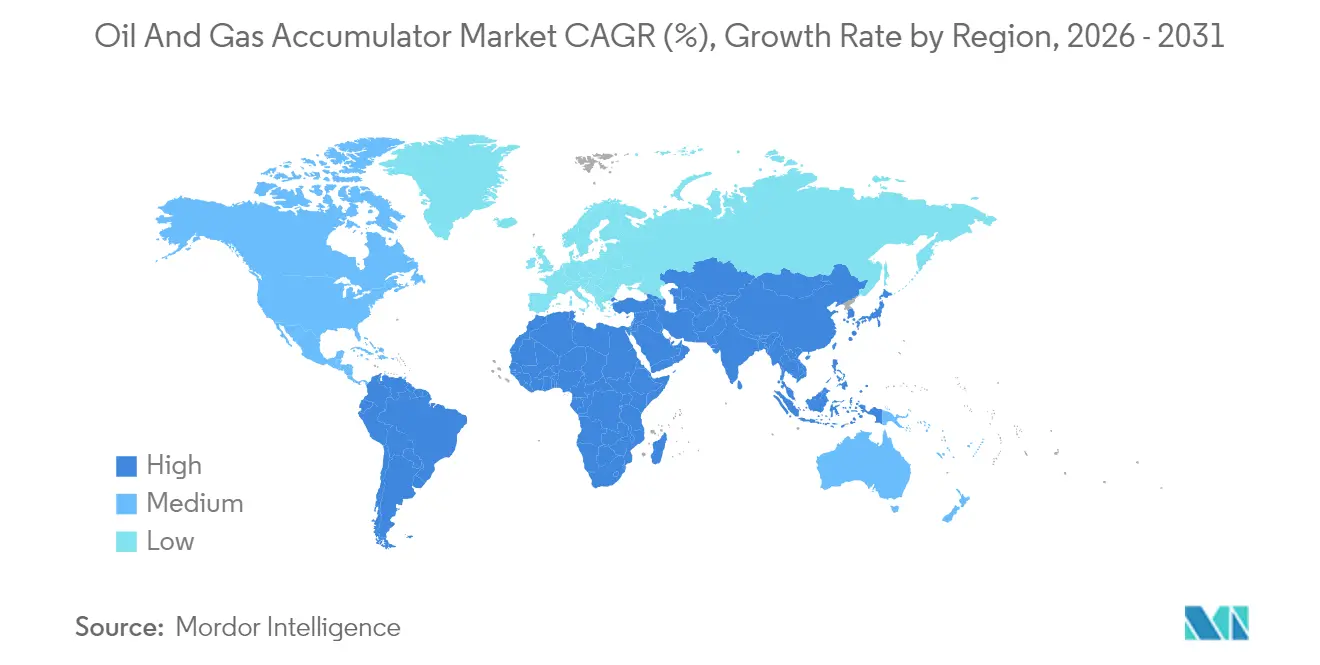

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

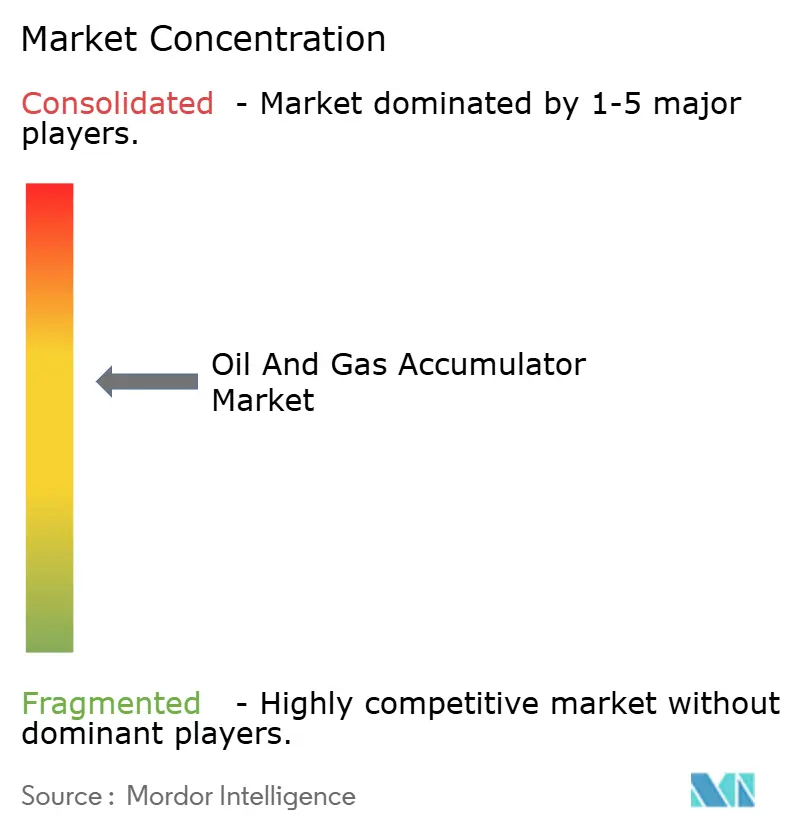

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oil And Gas Accumulator Market Analysis by Mordor Intelligence

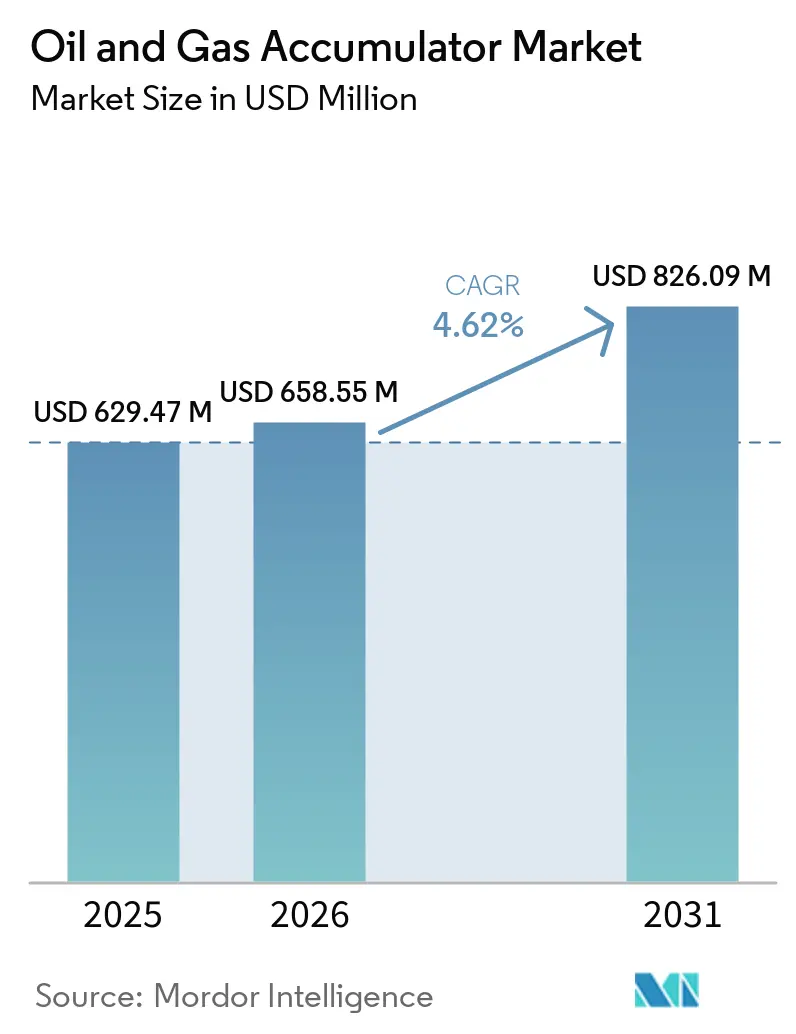

The Oil And Gas Accumulator Market size is expected to grow from USD 629.47 million in 2025 to USD 658.55 million in 2026 and is forecast to reach USD 826.09 million by 2031 at 4.62% CAGR over 2026-2031.

Growth reflects operators’ focus on safety compliance and operational efficiency rather than large-scale capacity additions. Mandatory API 16D requirements for blowout preventer (BOP) systems underpin steady demand for redundant hydraulic energy storage, particularly in subsea installations[1]Bureau of Safety and Environmental Enforcement, “Oil and Gas Operations – Requirements for Subsea Blowout Preventers,” bsee.gov. Parallel electrification efforts in well control have not displaced accumulators; instead, hybrid electro-hydraulic designs retain them as fail-safe power sources. North America leads current adoption, thanks to shale recompletions and a revival in the Gulf of Mexico, while the Middle East & Africa are the fastest-growing regions as sovereign producers scale up sour-gas and deepwater programs. As technology advances toward 20,000 psi projects, such as Chevron’s Anchor field, sales of higher-specification units continue to be boosted.

Key Report Takeaways

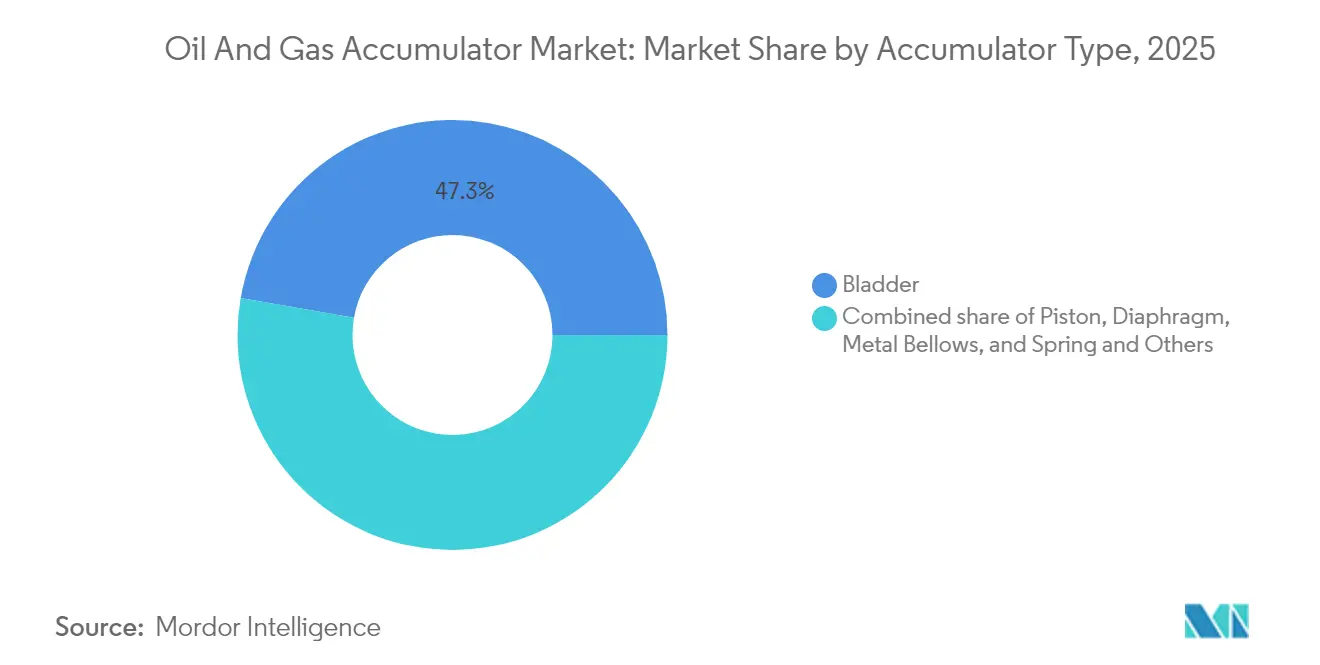

- By accumulator type, bladder designs led with 47.25% revenue share in 2025; metal bellows systems are forecast to expand at a 5.72% CAGR through 2031.

- By pressure rating, systems below 3,000 psi captured 54.45% of the oil & gas accumulator market share in 2025, while units rated above 5,000 psi are poised to grow at 6.27% CAGR to 2031.

- By capacity, accumulators under 10 gallons accounted for 51.05% share of the oil & gas accumulator market size in 2025, whereas units above 50 gallons are projected to advance at 5.88% CAGR over the forecast period.

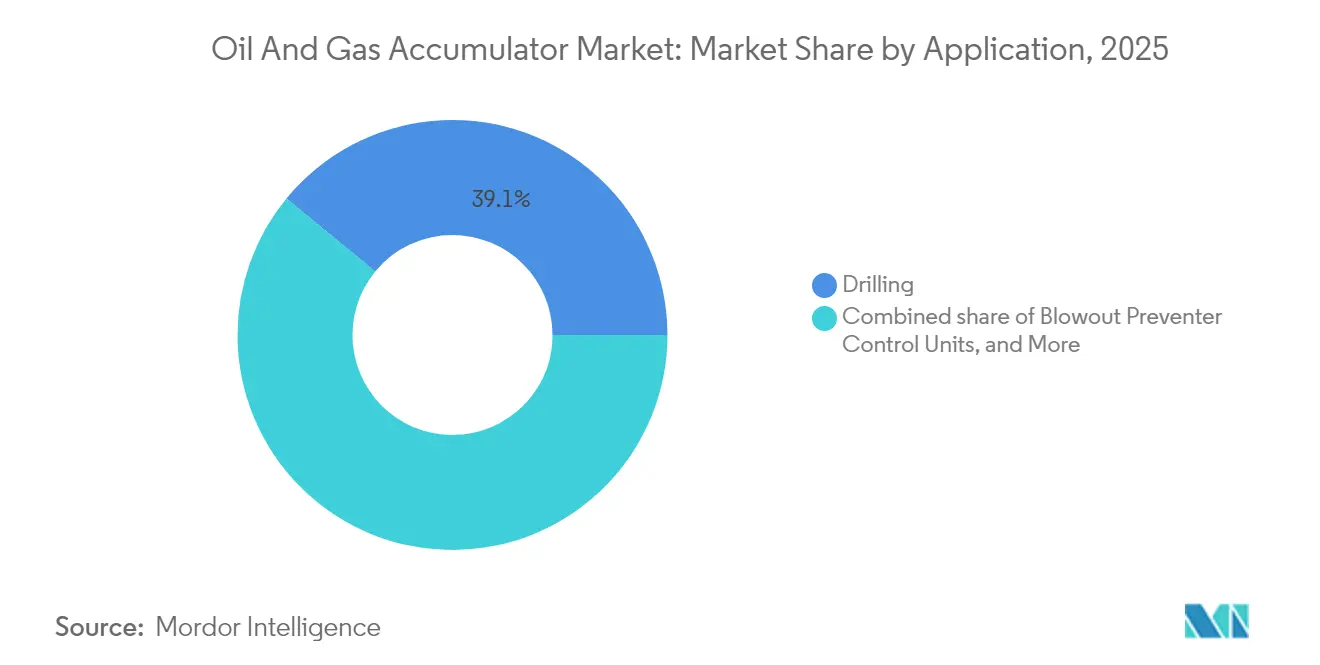

- By application, drilling operations dominated with a 39.05% revenue share in 2025; BOP control units are expected to record the highest CAGR of 6.45% from 2025 to 2031.

- By location of deployment, onshore is projected to account for 70.3% of the oil and gas accumulator market share in 2025, while offshore is expected to grow at a CAGR of 7.2% through 2031.

- By geography, North America commanded 37.15% revenue share in 2025, while the Middle East & Africa region is estimated to expand at 6.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oil And Gas Accumulator Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-cycle in global offshore rig count | +1.2% | Gulf of Mexico, North Sea, West Africa | Medium term (2-4 years) |

| Stringent BOP safety mandates (API 16D) | +0.9% | US OCS, North Sea | Long term (≥ 4 years) |

| Surging shale well recompletions | +0.8% | Permian, Eagle Ford, Bakken | Short term (≤ 2 years) |

| CAPEX rebound in MENA sour-gas projects | +0.7% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Retrofit programmes for low-emission electro-hydraulic units | +0.5% | Norway, Gulf of Mexico | Long term (≥ 4 years) |

| Digital twins enabling predictive accumulator maintenance | +0.4% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Up-cycle in Global Offshore Rig Count

Offshore rig utilisation rebounded to 82% in 2024 with 639 active units, stimulating replacement and upgrade cycles for accumulator banks that power high-spec managed-pressure drilling systems[2]Drilling Contractor, “Global Offshore Rig Utilization Trends 2024,” drillingcontractor.org. Fleet investment now favours upgrading existing rigs over newbuilds, extending service lifetimes, and raising demand for advanced hydraulic storage capable of faster BOP actuation. Deepwater projects, forecasted to grow at 8% annually from 2025 to 2028, will continue to push the oil & gas accumulator market toward higher pressure and temperature thresholds. Floating rig awards in Latin America and West Africa, scheduled for 2025-2026, further enlarge the addressable opportunity for premium accumulator packages.

Stringent BOP Safety Mandates (API 16D)

API 16D sets minimum accumulator volume, pre-charge, and response time criteria for critical BOP functions, compelling operators to adopt high-capacity units with redundant banks. Regulatory audits now emphasize the readiness of remote-operated vehicle intervention and third-party recertification, prompting specification upgrades that favor metal bellows and piston designs rated for 20,000 psi service. Ongoing compliance cycles generate repeat revenue for OEM service divisions that supply inspection, testing, and recharge programs.

Surging Shale Well Recompletions

North American producers are increasingly favouring refracturing existing wells to unlock bypassed resources, a strategy that has doubled the average number of completions per location to above three in 2024[3]U.S. Energy Information Administration, “Drilling Productivity Report June 2024,” eia.gov. Each refrac stage prolongs high-pressure pumping periods, accelerating accumulator wear and shortening maintenance intervals. Electric frac spreads, such as Halliburton’s ZEUS, cut fuel burn by 30% yet still rely on hydraulic accumulators for emergency shutdown, preserving a sizable onshore aftermarket.

CAPEX Rebound in MENA Sour-Gas Projects

Saudi Aramco’s USD 25 billion Jafurah phase-two awards and ADNOC’s rig procurement drive have resulted in sizable orders for accumulators built from hydrogen-sulfide-resistant alloys. The pipeline expansion of 4,000 km and 17 compression trains through 2028 requires large-volume units to dampen pressure transients during start-up and emergency blowdown. Although short-term rig cancellations have moderated drilling growth, long-cycle gas infrastructure maintains strong demand visibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil-price volatility curbing drilling budgets | -1.1% | North American shale | Short term (≤ 2 years) |

| High recertification & ASME code compliance costs | -0.8% | North Sea, US OCS | Medium term (2-4 years) |

| Shift toward all-electric subsea BOPs | -0.6% | North Sea, Gulf of Mexico | Long term (≥ 4 years) |

| ESG pressure on hydraulic-fluid spill risk | -0.4% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Oil-Price Volatility Curbing Drilling Budgets

Erratic commodity prices encourage operators to stretch equipment life, delaying accumulator renewals and favouring service-life extension kits over full replacements. While activity remains steady, discretionary spend on premium hydraulic upgrades contracts during price dips, tightening near-term revenue growth for suppliers.

High Recertification & ASME Code Compliance Costs

Periodic inspection, testing, and documentation required under ASME Section VIII add substantial cost to offshore accumulator ownership. Smaller contractors sometimes defer compliance or opt for lower-spec onshore units, shrinking margins for high-end OEMs. Nonetheless, stringent audits in the North Sea and US OCS ensure a baseline service market even during spending downturns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Accumulator Type: Metal Bellows Systems Gain Momentum

The oil & gas accumulator market size for bladder designs remained the largest in 2025, capturing a 47.25% share due to the strength of a mature supply chain and ease of maintenance. However, metal bellows units are set to record the fastest 5.72% CAGR, thanks to their superior fatigue resistance at 20,000 psi deployments, such as Chevron’s Anchor field.

Metal bellows construction also tolerates sour-gas environments without elastomer degradation, positioning the segment for long-term growth in deep-HPHT projects. Piston and diaphragm types retain roles in niche circuits where precise volume control or fluid separation is crucial, while spring accumulators serve legacy rigs with compact space envelopes. The oil & gas accumulator industry increasingly favours modular platforms that allow operators to swap internal elements rather than replacing complete vessels, a cost-saving trend benefiting flexible OEMs.

By Pressure Rating: High-Pressure Designs Accelerate

Systems rated below 3,000 psi held a 54.45% share in 2025, primarily due to the widespread adoption of onshore drilling. Above 5,000 psi models are expected to log a 6.27% CAGR as deepwater and ultra-deepwater wells proliferate across the US Gulf and Brazil.

Higher ratings demand forged alloy shells, stricter welding procedures, and advanced NDT, driving unit prices upward but reducing total vessel count through increased capacity. At the same time, intermediate units with pressures of 3,001-5,000 psi serve proliferating shallow-water redevelopment projects, where operators upgrade aging platforms rather than sanction greenfield builds. The oil & gas accumulator market continues to pivot toward high-pressure variants that can be standardised across multiple rig classes to simplify logistics.

By Capacity: Large Vessels Attract Investment

Accumulators under 10 gallons accounted for 51.05% of 2025 sales, aligning with conventional BOP control skids on most land rigs. Above 50 gallons, however, revenue is expected to grow at a 5.88% CAGR, as multi-well pads and simultaneous operations require longer reserve periods between recharge cycles.

Larger vessels enable operators to downsize pump horsepower, lowering topside installation weight and enhancing energy efficiency. Yet, logistical challenges—such as transport weight, nitrogen pre-charge, and certification—encourage OEMs to offer field-assembled modular designs that fit through tight moonpools or facility doorways.

By Location of Deployment: Offshore Demand Outpaces Onshore

Onshore drilling still represents 69.85% of demand thanks to North American shale activity, but offshore deployments will climb at a 6.95% CAGR to 2031 as Latin American and African deepwater campaigns ramp up. Subsea trees and BOP stacks require accumulators capable of unattended service intervals of five years or longer. This offshore specification premium explains why the oil & gas accumulator market commands higher average selling prices in marine projects compared with land rigs. Remote monitoring and ROV-friendly interfaces further differentiate supplier offerings.

By Application: BOP Control Units Lead Growth

Drilling operations dominated revenue in 2025, with a 39.05% share; however, BOP control units are expected to outstrip other segments, growing at a 6.45% CAGR to 2031. Regulators increasingly demand independent secondary energy sources so that each critical ram can close within specified time limits after primary power loss. Accumulators, therefore, migrate from generic hydraulic storage to integral safety devices complete with self-diagnostics, temperature compensation, and redundancy, reinforcing their centrality to well-control integrity.

Geography Analysis

North America retained a 37.15% revenue lead in 2025 owing to sustained shale recompletion and a cautious offshore revival. The region’s emphasis on capital efficiency and adoption of electric fracturing fleets keeps demand steady for compact, digitally monitored accumulators that integrate with real-time cloud analytics. Upstream developers in Argentina and Brazil are adding incremental growth through subsea tree awards, which require 20,000 psi solutions.

The Middle East & Africa oil & gas accumulator market size is expected to register the highest CAGR of 6.08% through 2031. Massive sour-gas projects such as Jafurah, with compression trains and thousands of kilometres of pipeline, need large-volume vessels rated for H₂S service. ADNOC’s rig expansion and subsea prospects off Namibia and Angola reinforce the trajectory despite temporary jack-up cancellations. Regional content mandates also motivate OEMs to localise assembly and service hubs, reducing lead times and creating new joint-venture structures.

Europe and the Asia-Pacific exhibit stable replacement-driven demand. European North Sea operators retrofit ageing rigs to meet new environmental regulations, adding sensors and leak-proof bellows to existing skids. Asia-Pacific’s upstream capex, led by China and Indonesia, tops USD 300 billion in 2025 and underpins fresh orders for medium-pressure units suited to brownfield life-extension projects. Meanwhile, the growing number of carbon-storage pilots across the North Sea introduces novel accumulator roles in CO₂ injection systems, opening a complementary market for corrosion-resistant designs.

Competitive Landscape

The oil & gas accumulator market is moderately fragmented, with legacy hydraulic experts and newer electro-hydraulic integrators pursuing system-level contracts. HYDAC International, Parker-Hannifin, and Eaton leverage broad product portfolios and global service centres to bid on turnkey packages. Parker-Hannifin’s record USD 19.9 billion in fiscal 2024 sales and recent divestiture of its composites division highlight a sharpened focus on core hydraulics.

Baker Hughes, SLB, and TechnipFMC integrate accumulators within digital BOP and subsea production architectures, blurring traditional component boundaries. AI-enabled monitoring suites offered by these firms promise an 80% reduction in maintenance costs, an attractive proposition for operators under ESG scrutiny.

Emerging specialists such as Nippon Accumulator and Technetics Group secure high-pressure bellows niches, particularly for 20,000 psi-rated trees. Bosch Rexroth’s EUR 160 million Mexican plant signals localisation moves aimed at shortening supply chains and hedging tariff risks. Consolidation pressure remains: operators are increasingly issuing frame agreements that bundle accumulators with pumps, valves, and digital support, favouring manufacturers able to guarantee end-to-end performance across a rig fleet.

Oil And Gas Accumulator Industry Leaders

HYDAC International GmbH

Parker-Hannifin Corp.

Eaton Corporation plc

Freudenberg (Tobul)

Bosch Rexroth AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Baker Hughes won a multi-year, integrated coiled-tubing drilling contract at Dubai’s Margham gas storage project, expanding the deployment of its CoilTrak system.

- January 2025: Baker Hughes secured orders for six gas compression trains and six propane compressors for Aramco’s Jafurah expansion.

- October 2024: Baker Hughes booked its largest Integrated Compressor Line order—10 units—for Dubai’s Margham storage facility.

- July 2024: BP approved the USD 5 billion Kaskida 20,000 psi Gulf of Mexico project targeting first oil in 2029.

Global Oil And Gas Accumulator Market Report Scope

The oil and gas accumulator report include:

| Bladder |

| Piston |

| Diaphragm |

| Metal Bellows |

| Spring and Others |

| Below 3,000 psi |

| 3,001 to 5,000 psi |

| Above 5,000 psi |

| Below 10 gal |

| 10 to 50 gal |

| Above 50 gal |

| Onshore |

| Offshore |

| Drilling |

| Well Workover and Intervention |

| Blowout Preventer Control Units |

| Hydraulic Fracturing Units |

| Other Upstream Operations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| Norway | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Accumulator Type | Bladder | |

| Piston | ||

| Diaphragm | ||

| Metal Bellows | ||

| Spring and Others | ||

| By Pressure Rating | Below 3,000 psi | |

| 3,001 to 5,000 psi | ||

| Above 5,000 psi | ||

| By Capacity | Below 10 gal | |

| 10 to 50 gal | ||

| Above 50 gal | ||

| By Location of Deployment | Onshore | |

| Offshore | ||

| By Application | Drilling | |

| Well Workover and Intervention | ||

| Blowout Preventer Control Units | ||

| Hydraulic Fracturing Units | ||

| Other Upstream Operations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| Norway | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the oil & gas accumulator market?

The Oil And Gas Accumulator Market is valued at USD 658.55 million in 2026 and is forecast to reach USD 826.09 million by 2031 at a CAGR of 4.62% over 2026-2031.

Which region shows the fastest growth for oil & gas accumulator market sales?

The Middle East & Africa region is projected to grow at a 6.08% CAGR through 2031, driven by large gas projects in Saudi Arabia and the UAE.

Why are metal bellows accumulators gaining popularity?

Metal bellows units withstand 20,000 psi pressures and sour-gas corrosion better than bladder designs, making them ideal for deep-HPHT developments like Chevron’s Anchor field.

How do API 16D regulations affect demand?

API 16D mandates sufficient accumulator capacity for rapid BOP closure, leading operators to purchase larger, redundant systems with enhanced monitoring.

Will electrification reduce future accumulator demand?

All-electric subsea BOPs lower hydraulic volumes, but hybrid architectures still require accumulators for emergency shutdown, sustaining a niche yet critical demand segment.

What is the main restraint on short-term growth?

Oil-price volatility limits drilling budgets, causing operators to defer premium equipment upgrades and extend existing accumulator lifespans.

Page last updated on: