Forestry Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.41 Billion |

| Market Size (2031) | USD 13.58 Billion |

| Growth Rate (2026 - 2031) | 3.54% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

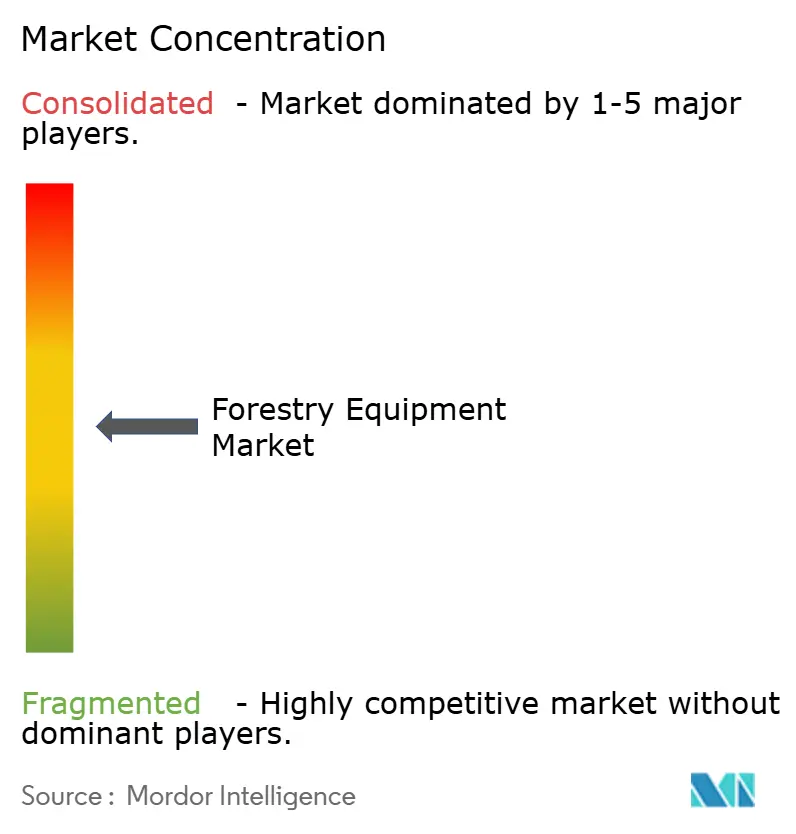

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Forestry Equipment Market Analysis by Mordor Intelligence

The Forestry Equipment Market size is expected to grow from USD 10.98 billion in 2025 to USD 11.41 billion in 2026 and is forecast to reach USD 13.58 billion by 2031 at 3.54% CAGR over 2026-2031.

Demand growth is shaped by stricter emission rules, rapid mechanization in emerging economies, and rising post-wildfire salvage volumes. Large operators are testing hybrid fleets to comply with carbon caps, yet most small and mid-sized contractors keep refurbishing diesel machines to contain capital costs. Rental fleets are expanding quickly because contractors prefer paying for short-term use rather than locking scarce cash into ownership. Technology is a decisive differentiator as leading manufacturers deploy telematics, AI-assisted controls, and predictive maintenance to reduce downtime and offset a widening skilled-operator gap.

Key Report Takeaways

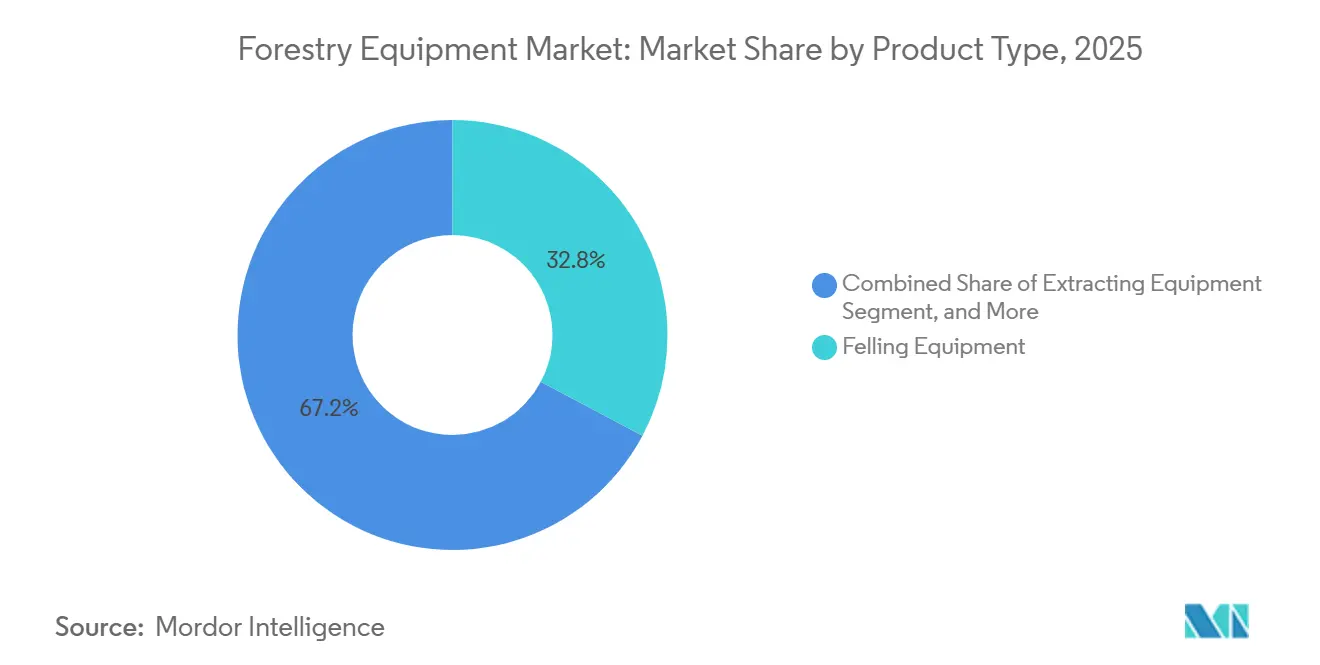

- By product type, felling equipment commanded 32.76% of the forestry equipment market share in 2025, while other forestry equipment (loaders, mulchers, and others) is projected to advance at a 4.31% CAGR through 2031.

- By power source, diesel systems held 62.07% of the forestry equipment market share in 2025, whereas electric-powered units are forecast to grow at a 4.52% CAGR to 2031.

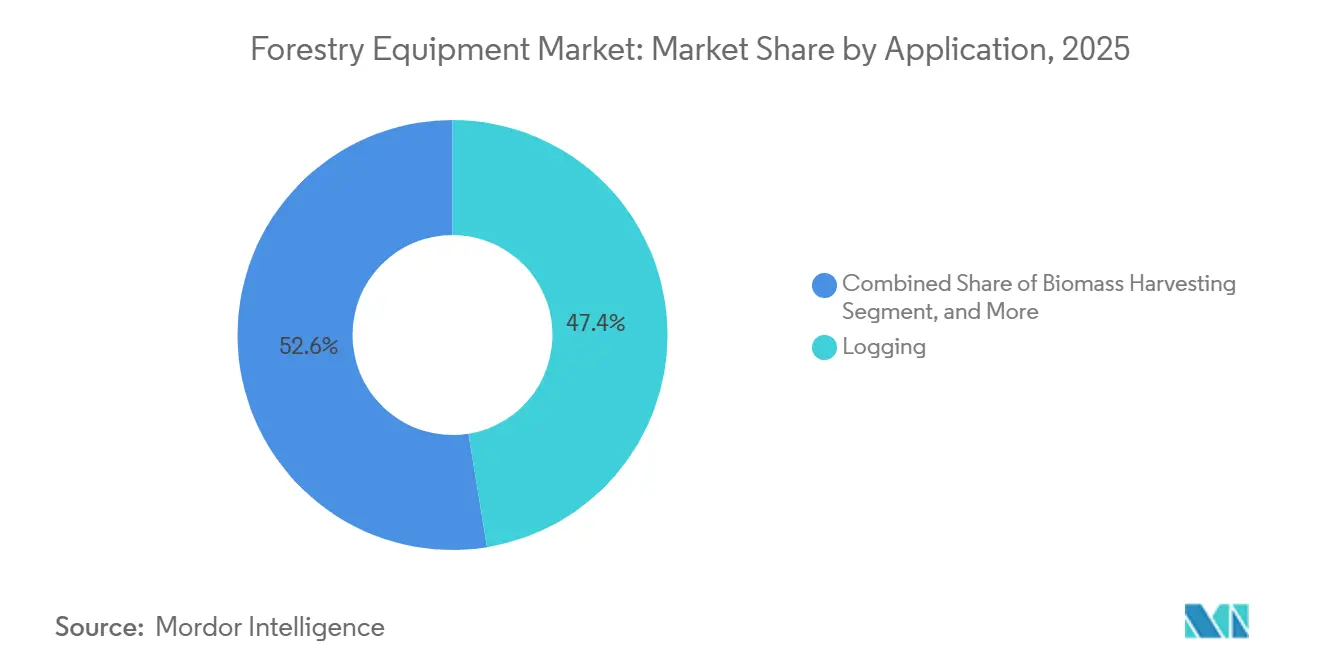

- By application, logging led with 47.43% revenue share in 2025, and biomass harvesting is forecast to expand at a 4.71% CAGR to 2031.

- By end-user, commercial logging companies accounted for 53.21% share of the forestry equipment market size in 2025, whereas rental service providers are expected to record the fastest 4.49% CAGR through 2031.

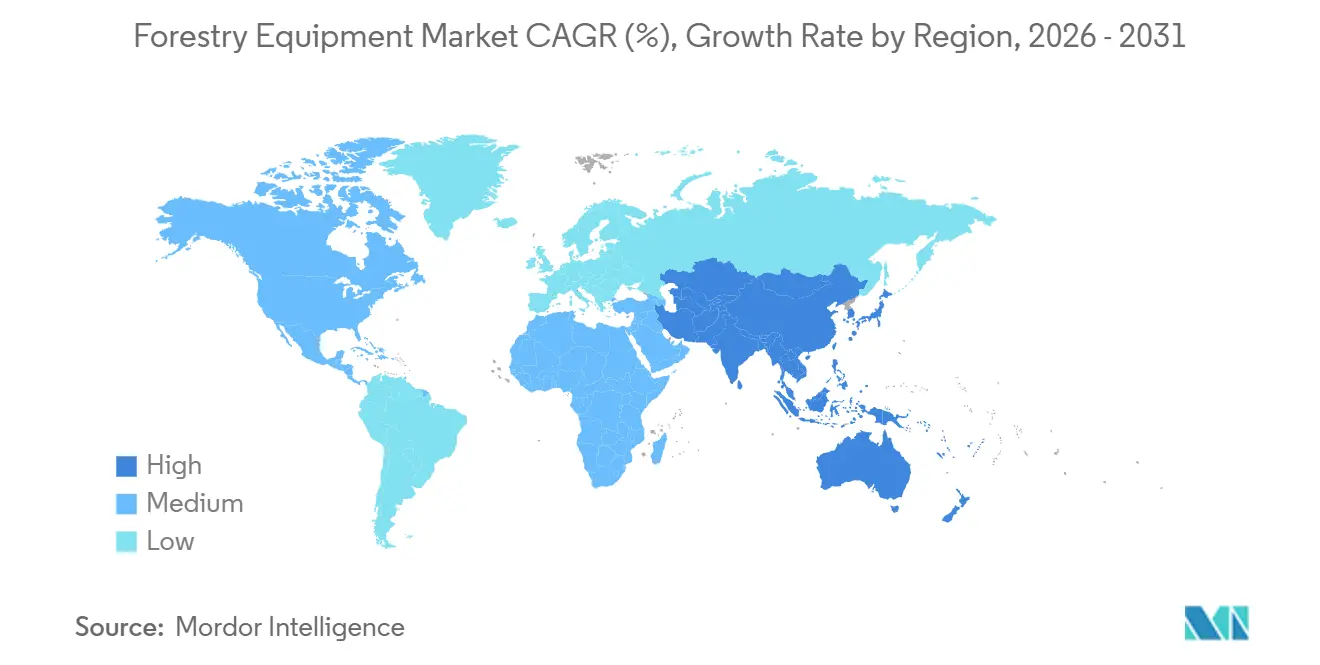

- By geography, North America dominated with 39.32% of global demand in 2025, while Asia-Pacific is projected to post the highest 4.57% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Forestry Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Mechanised Selective Logging | +0.8% | North America and Europe | Medium term (2–4 years) |

| Adoption of Electric and Hybrid Forestry Machinery | +0.6% | North America and Europe, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Expansion of Biomass and Bioenergy Projects | +0.9% | Europe, North America, Asia-Pacific | Medium term (2–4 years) |

| Government Incentives for Precision and Sustainable Forestry | +0.5% | North America, Europe, Australia, New Zealand | Short term (≤ 2 years) |

| Integration of Telematics and AI Fleet Optimisation | +0.4% | Global | Medium term (2–4 years) |

| Post-Wildfire Salvage Harvesting Needs | +0.3% | North America, Australia, Mediterranean Europe | Short term (≤ 2 |

| Source: Mordor Intelligence | |||

Rising Demand for Mechanised Selective Logging

Labor shortages and stricter habitat rules are steering selective logging away from chainsaw crews toward harvesters and forwarders that minimize residual stand damage. Oregon’s 80-year Elliott State Research Forest permit highlights this shift because managers must thin steep slopes without harming protected bird habitats. Komatsu’s 951XC-1 harvester, released in 2025, uses advanced hydraulics to precisely buck logs on uneven ground, reducing waste and increasing fiber yield. Institutional timberland investors such as Stafford Capital Partners prioritize certification-compliant mechanization to lock in predictable returns across 6.3 million acres. While small contractors still run skidders and chainsaws, rising insurance costs and safety regulations continue to tilt economics toward integrated machines that cut cycle times and reduce labor intensity.

Increasing Adoption of Electric and Hybrid Forestry Machinery

Volvo showcased the first electric articulated dump trucks in 2025, framing a long-range transition to zero-emission haulage. Adoption of deep-forest tasks remains cautious because charging points are scarce beyond 50 kilometers from the grid, and diesel generators undermine emission gains. Nonetheless, European and Californian mandates force pilot programs, with Volvo trialing 5G-controlled electric loaders in Scandinavian forests. Surveys indicate 77% of operators still trust hydraulic diesels over electric-hydraulic hybrids, forecasting a multi-stage path in which hybrids bridge technology gaps until batteries store more energy per kilogram. Government subsidies covering battery packs and fast chargers shorten payback for fleet owners operating near mills, helping the segment outpace the overall forestry equipment market.

Expansion of Global Biomass and Bioenergy Projects

Bioenergy programs in the European Union and the United States are boosting demand for chippers, grinders, and debarkers that convert low-grade timber into uniform fuel. Terex CBI’s 6800CT grinder processes standing deadwood at an Arizona biomass plant, demonstrating how salvage material can be converted into renewable heat and power. The U.S. Department of Energy projects forest biomass supply could double to 62.7 million tonnes annually in mature markets, sustaining a 4.71% CAGR for biomass harvesting gear. Morbark’s 2355 Flail Chiparvestor offers 1,200 HP capacity and integrated dirt separators to boost chip quality. Even where pulp mills close, redirected slash fuels distributed boiler networks, keeping demand buoyant despite cyclic lumber prices.[1]Kate Freund, “Record of Decision for Elliott State Research Forest,” U.S. Fish and Wildlife Service, fws.gov

Government Incentives for Precision and Sustainable Forestry

Oregon deployed USD 26.6 million in Urban and Community Forestry grants during 2024-2025 to fund workforce programs, LiDAR mapping, and telematics-ready machinery.[2]Oregon Department of Forestry, “Urban and Community Forestry Subaward Programs,” oregon.gov Europe links subsidy eligibility to ISO 14001 and FSC compliance, accelerating purchases of Stage V harvesters with remote diagnostics. New Zealand’s Precision Silviculture Programme lifted LiDAR use to 93% by 2025, cutting waste and reducing fuel burn. These schemes temper capital barriers, letting mid-tier contractors trial Komatsu’s Smart Forestry suite, which wires machine health data to cloud dashboards for real-time optimization. Regional priorities differ: North America rewards emission cuts, whereas Asia-Pacific backs simple mechanization to replace manual labor, so manufacturers tailor features to local funding rules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Expenditure for Advanced Machines | -0.6% | Global, particularly affecting small to medium operators | Short term (≤ 2 years) |

| Shortage of Skilled Heavy-Equipment Operators in Rural Areas | -0.5% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Limited Charging Infrastructure in Remote Forest Regions | -0.4% | Global, with highest impact in North America and Nordic countries | Long term (≥ 4 years) |

| Volatility of Global Timber Prices Impacting CAPEX Cycles | -0.3% | Global, with particular sensitivity in commodity-dependent regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure for Advanced Machines

Electric harvesters cost 30-50% more than diesel peers, putting ownership out of reach for many small firms. Morbark’s 2355 Flail Chiparvestor, weighing 115,200 pounds, lists above USD 1 million, restricting sales to large loggers and rental companies.[3]Morbark, “2355 Flail Chiparvestor,” morbark.com Smart controls and Stage V after-treatment add USD 50,000-100,000 to Komatsu excavators. Regions with high interest rates, notably parts of Asia-Pacific and South America, face steeper hurdles because shorter loan tenures inflate monthly outlays. Consequently, many operators sweat older fleets longer, boosting demand for parts and rebuilds instead of new units.

Shortage of Skilled Heavy-Equipment Operators in Rural Areas

A projected 700,000-person deficit in qualified operators by 2031 squeezes utilization across North American and European forests. Retirements outpace apprenticeships, and younger workers choose urban logistics roles. Vendors respond with automation: John Deere’s autonomous articulated dump truck uses terrain memory to run without a driver on mapped routes.[4]Heavy Equipment Guide, “2025 Top Introductions,” heavyequipmentguide.ca Link-Belt’s Payload Assist app sends load tickets to smartphones, simplifying recordkeeping. Yet remote forests still lack reliable data coverage, limiting the benefit of connected tech. Wage premiums of 20-30% persist, elevating cost structures until autonomous systems mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Growing Demand for Multi-Role Machines

Felling equipment controlled 32.76% of the forestry equipment market share in 2025. Harvesters, feller bunchers, and swing machines dominate both cut-to-length and whole-tree systems, with Komatsu’s TN785D improving slope stability to unlock steep-terrain fiber. Extracting gear, mainly forwarders and skidders, remains indispensable because it bridges the stump and landing. On-site processors, such as chippers and delimbers, become relevant when biomass plants pay for uniform chips. Separately sold parts and attachments deliver recurring margins, as OEMs guarantee chain and bar supply for decades.

Other forestry equipment (loaders, mulchers, and others) is poised to grow fastest at a 4.31% CAGR through 2031, boosting the market for loaders, mulchers, and ancillary assets. Bobcat’s 32-item attachment range turns compact skid-steers into land-clearing specialists. Rayco’s T415 mulcher tackles firebreaks, pipeline corridors, and right-of-way clearing with 415 HP hydrostatic power. Tigercat’s reinforced H-Series feller-bunchers extend machine life, helping contractors capture value through harsher cycles. Versatility drives investment as contractors seek assets that pivot between logging, land clearing, and infrastructure jobs to maximize uptime.

By Power Source: Diesel Dominance Meets Early Electrification

Diesel units retained 62.07% forestry equipment market share in 2025 because remote fuel delivery systems, technician familiarity, and robust torque keep them indispensable. Caterpillar’s FM528 GF/LL integrates efficient diesels that meet Stage V while maintaining the ruggedness demanded by steep-slope thinnings. Petrol models, mainly chainsaws, fill portable needs.

Electric-powered machines are forecast to post a 4.52% CAGR, yet their advance hinges on batteries and charging. Volvo’s A30 and A40 Electric articulated dump trucks headline this frontier, but viable ranges stay near 50 kilometers unless mobile battery banks are financed. Hybrids that capture brake energy stand as stop-gaps, shaving fuel during idle or low-load cycles without range anxiety. Surveys reveal that most operators still rate hydraulic reliability above electric drives, signaling a decade-long transition toward parity.

By Application: Core Logging Steady, Bioenergy Lifts Growth

Logging absorbed 47.43% of 2025 demand as managed forests maintain stable harvest schedules supported by long-term permits such as the 83,326-acre Elliott State plan. Land clearing accompanies roadway, pipeline, and agricultural projects, while fire management upsizes mulcher fleets following severe wildfire seasons. Forest road construction continues, although conservation caps, such as the 40-mile limit in Elliott State, constrain hard infrastructure.

Biomass harvesting will grow at a 4.71% CAGR, outpacing conventional logging. Terex CBI’s ChipMax 364T whole-tree chipper, transportable without special permits, supports high-volume power producers. Morbark’s 50/48X drum chipper processes entire trees into boiler-ready chips, aligning with European feed-in tariffs for renewable heat. Where pulp mills shutter, low-grade timber diverts into energy loops, preserving equipment utilization even when sawlog prices soften.

By End-User: Capital-Light Models Gain Favor

Commercial logging companies held 53.21% share of forestry equipment market size in 2025, operating 10-50-unit fleets focused on utilization and total cost of ownership. TIMOs mandate telematics reporting to validate ESG metrics across multi-country portfolios, reinforcing demand for smart machines. Government agencies procure niche gear for fire mitigation and habitat work, often funded by stimulus grants.

Rental service providers will expand fastest at 4.49% CAGR. United Rentals and Sunbelt stock specialized harvesters and mulchers, letting contractors match fleet scale to episodic jobs like post-wildfire salvage. Telematics supports pay-per-hour billing and predictive maintenance, ensuring uptime vital for short contract windows. Younger entrepreneurs favor asset-light models, reinforcing rental momentum across mature and emerging regions.

Geography Analysis

North America generated 39.32% of 2025 revenue, cementing the region’s leadership. Extensive pine plantations in the U.S. South, mechanized Douglas fir stands in the Pacific Northwest, and salvage programs in western states provide a balanced demand base. Canadian loggers invest in steep-slope harvesters to reach fire-prone interior forests, while Mexico’s community forestry programs opt for compact loaders and chainsaws. Manufacturers strengthen local assembly: Volvo expanded U.S. capacity in 2025, and John Deere launched L-III skidders optimized for dense hardwood tracts.

Europe emphasizes compliance with emissions standards and ecosystem services. Germany and France push Stage V harvesters integrated with LiDAR silviculture planning, while Sweden’s biomass-for-district-heat sector fuels grinder uptake. Russia retains vast unrealized potential, but infrastructure and geopolitics slow mechanization. The forestry equipment market size for European biomass harvesting keeps growing as carbon pricing rewards renewable fuels.

Asia-Pacific is set to post a 4.57% CAGR through 2031. China scales up subsidies for forest harvesters, India modernizes plantation management, and Australia pivots toward fuel-reduction equipment after repeated bushfires. New Zealand logging firms, already early adopters of telematics, now trial hybrid forwarders on radiata pine slopes. Southeast Asian exporters mechanize selectively to satisfy certification audits, driving sales of mid-sized skidders and rough-terrain loaders. Elsewhere, South America’s eucalyptus plantations in Brazil and Argentina quicken harvester demand to lift pulpwood yields, while Africa’s nascent sectors in South Africa adopt cost-efficient cut-to-length systems as mills expand.

Competitive Landscape

Deere, Caterpillar, Komatsu, and Volvo anchor the market with broad portfolios, global dealer coverage, and captive finance. Komatsu’s Smart Forestry suite blends telematics, AI, and inventory data to cut downtime by 20% for early adopters, while Deere’s autonomous truck prototype illustrates progress toward driverless timber transport. Nordic specialists Ponsse and Tigercat concentrate on purpose-built harvesters and forwarders, earning strong loyalty where uptime in cold, remote forests is critical.

Niche players enlarge white-space segments. Terex CBI leverages interchangeable rotors to switch from mulch to chip modes fast, appealing to contractors juggling biomass and land-clearing contracts. Morbark positions lifetime parts availability as a hedge against second-hand price erosion, and Rayco markets multi-head mulchers for storm cleanup and firebreak creation. Bobcat and Kubota expand compact equipment with forestry-grade attachments, challenging full-size OEMs on small-site agility.

Rental channel concentration shifts bargaining power. United Rentals demands OEM-installed telematics for fleet-wide dashboards, steering product roadmaps. Digital services emerge as the next battleground: Link-Belt’s payload app, Morbark’s Integrated Control System, and Komatsu’s Intelligent Machine Control 3.0 all promise lower cost per cubic meter. Consolidation remains measured, leaving room for regional champions, yet technology costs spur partnerships between sensor startups and legacy manufacturers keen to accelerate automation.

Forestry Equipment Industry Leaders

Deere & Company

Caterpillar Inc.

Komatsu Ltd.

Ponsse Oyj

Tigercat Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Volvo Construction Equipment confirmed U.S. plant expansion is on schedule, with pilot assembly of electric loaders slated for Q4 2026.

- October 2025: John Deere introduced the L-III skidders featuring enhanced fuel efficiency and in-cab comfort upgrades.

- September 2025: Komatsu launched the 951XC-1 harvester with precision hydraulics tailored for selective cutting in high-value stands.

- July 2025: Komatsu rolled out the TN785D swing machine designed for slopes exceeding 30 degrees.

Global Forestry Equipment Market Report Scope

The Forestry Equipment Market Report is Segmented by Product Type (Felling Equipment, Extracting Equipment, On-Site Processing Equipment, Separately Sold Parts and Attachments, Other Forestry Equipment), Power Source (Diesel, Petrol/Oil, Electric, Hybrid, Other), Application (Logging, Land Clearing, Forest Fire Management, Forest Road Construction, Biomass Harvesting, Other), End-User (Commercial Logging Companies, Timberland Investment Managers, Government Forestry Agencies, Individual Contractors and Small Operators, Rental Service Providers), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Felling Equipment | Chainsaws |

| Harvesters | |

| Feller Bunchers | |

| Extracting Equipment | Forwarders |

| Skidders | |

| Other Extracting Equipment | |

| On-Site Processing Equipment | Chippers and Grinders |

| Delimbers and Slashers | |

| Other On-Site Processing Equipment | |

| Separately Sold Parts and Attachments | Saw Chain, Guide Bars, Discs, and Teeth |

| Harvesting and Other Cutting Heads | |

| Other Separately Sold Parts and Attachments | |

| Other Forestry Equipment | Loaders |

| Mulchers | |

| Other Forestry Equipment |

| Diesel-Powered Equipment |

| Petrol / Oil-Powered Equipment |

| Electric-Powered Equipment |

| Hybrid-Powered Equipment |

| Other Power Source |

| Logging |

| Land Clearing |

| Forest Fire Management |

| Forest Road Construction |

| Biomass Harvesting |

| Other Application |

| Commercial Logging Companies |

| Timberland Investment Managers |

| Government Forestry Agencies |

| Individual Contractors and Small Operators |

| Rental Service Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Felling Equipment | Chainsaws |

| Harvesters | ||

| Feller Bunchers | ||

| Extracting Equipment | Forwarders | |

| Skidders | ||

| Other Extracting Equipment | ||

| On-Site Processing Equipment | Chippers and Grinders | |

| Delimbers and Slashers | ||

| Other On-Site Processing Equipment | ||

| Separately Sold Parts and Attachments | Saw Chain, Guide Bars, Discs, and Teeth | |

| Harvesting and Other Cutting Heads | ||

| Other Separately Sold Parts and Attachments | ||

| Other Forestry Equipment | Loaders | |

| Mulchers | ||

| Other Forestry Equipment | ||

| By Power Source | Diesel-Powered Equipment | |

| Petrol / Oil-Powered Equipment | ||

| Electric-Powered Equipment | ||

| Hybrid-Powered Equipment | ||

| Other Power Source | ||

| By Application | Logging | |

| Land Clearing | ||

| Forest Fire Management | ||

| Forest Road Construction | ||

| Biomass Harvesting | ||

| Other Application | ||

| By End-User | Commercial Logging Companies | |

| Timberland Investment Managers | ||

| Government Forestry Agencies | ||

| Individual Contractors and Small Operators | ||

| Rental Service Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of the forestry equipment market by 2031?

The market is projected to reach USD 13.58 billion by 2031.

Which product segment is forecast to grow fastest through 2031?

Other forestry equipment such as loaders and mulchers is set to expand at a 4.31% CAGR.

Why are rental service providers gaining share?

High capital costs and volatile timber prices push contractors toward flexible rental agreements, driving a 4.49% CAGR for this segment.

How quickly are electric-powered forestry machines growing?

Electric units are projected to register a 4.52% CAGR, outpacing the overall market but from a small base.

Which region will post the highest growth rate to 2031?

Asia-Pacific is expected to lead with a 4.57% CAGR as China and India mechanize large state forests.

What technology trends are shaping future equipment design?

Telematics, AI-driven fleet optimization, and hybrid or electric drivetrains are key areas of innovation among leading OEMs.

Page last updated on: