Foldable Smartphone Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

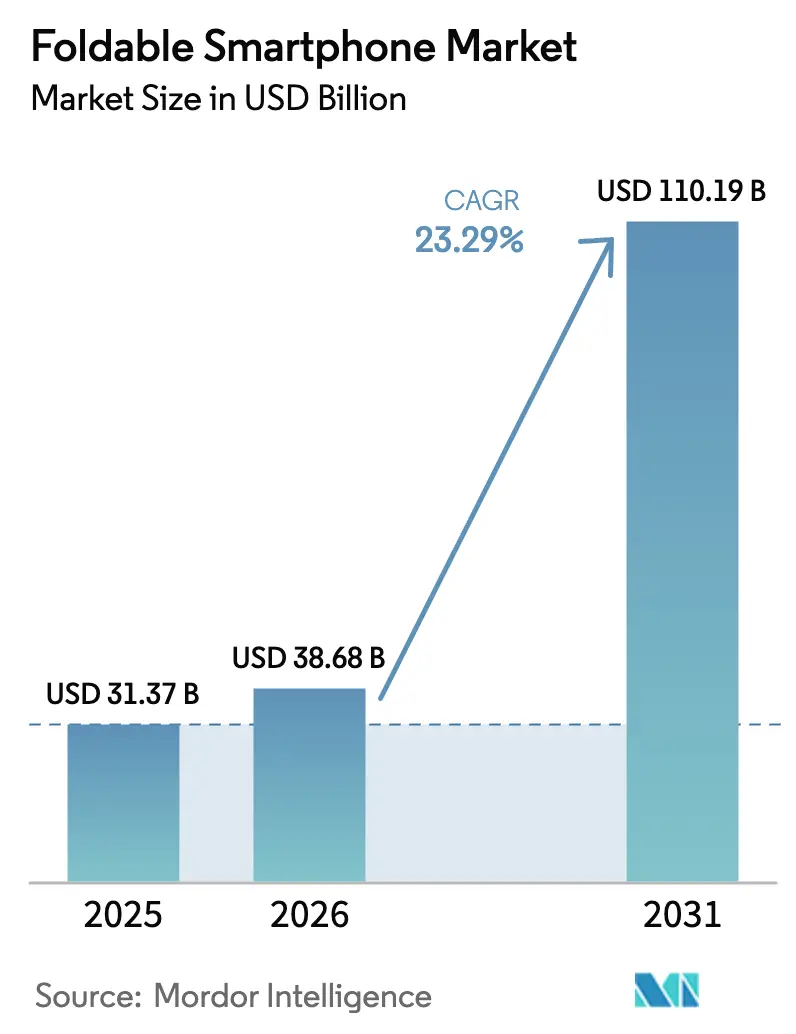

| Market Size (2026) | USD 38.68 Billion |

| Market Size (2031) | USD 110.19 Billion |

| Growth Rate (2026 - 2031) | 23.29% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

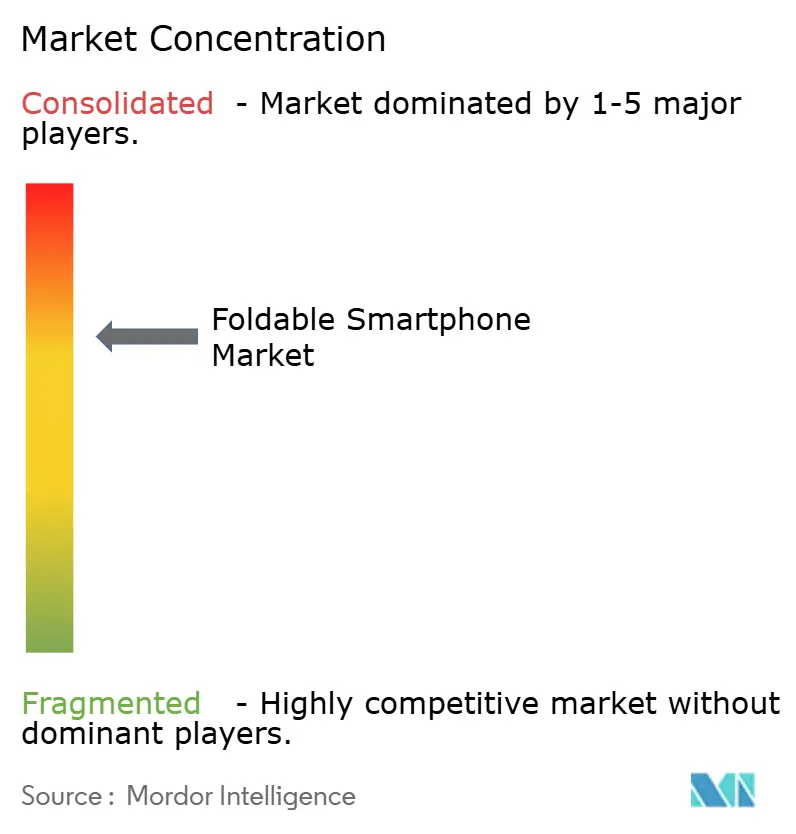

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Foldable Smartphone Market Analysis by Mordor Intelligence

The Foldable Smartphone Market size is expected to increase from USD 31.37 billion in 2025 to USD 38.68 billion in 2026 and reach USD 110.19 billion by 2031, growing at a CAGR of 23.29% over 2026-2031. Ultra-thin-glass (UTG) yields surpassed 85% in 2025, panel prices declined by 30% between 2024 and 2025, and carrier subsidies paired with 5G unlimited-data plans pulled premium devices below the USD 1,500 threshold, lowering adoption friction across consumer and enterprise segments. Enterprise deployments doubled in logistics and field-service verticals, while book-style models captured 62.31% of 2025 revenue and 7-8 inch screens secured 44.34% share as users replaced tablets with split-screen workflows. Asia-Pacific led with 54.84% of global revenue, Middle East demand rose fastest at a 23.43% CAGR, and North America plus Europe remained premium strongholds for Samsung’s Galaxy Z series even as Chinese challengers expanded via e-commerce. Form-factor innovation now spans rollable and slide-out concepts, and enterprise uptake at 26.19% CAGR signals that productivity gains, not just consumer enthusiasm, will shape the next replacement cycle.

Key Report Takeaways

- By form factor, book-style devices led with 62.31% revenue share in 2025; rollable and slide-out designs are set to post the fastest 24.21% CAGR through 2031.

- By screen size, the 7-8 inch category contributed 44.34% of 2025 revenue, whereas displays above 8 inches are forecast to expand at 25.76% CAGR to 2031.

- By price range, units priced between USD 1,500-1,999 are advancing at the quickest 26.52% CAGR even though models priced USD 1,000-1,499 accounted for 48.51% of 2025 revenue.

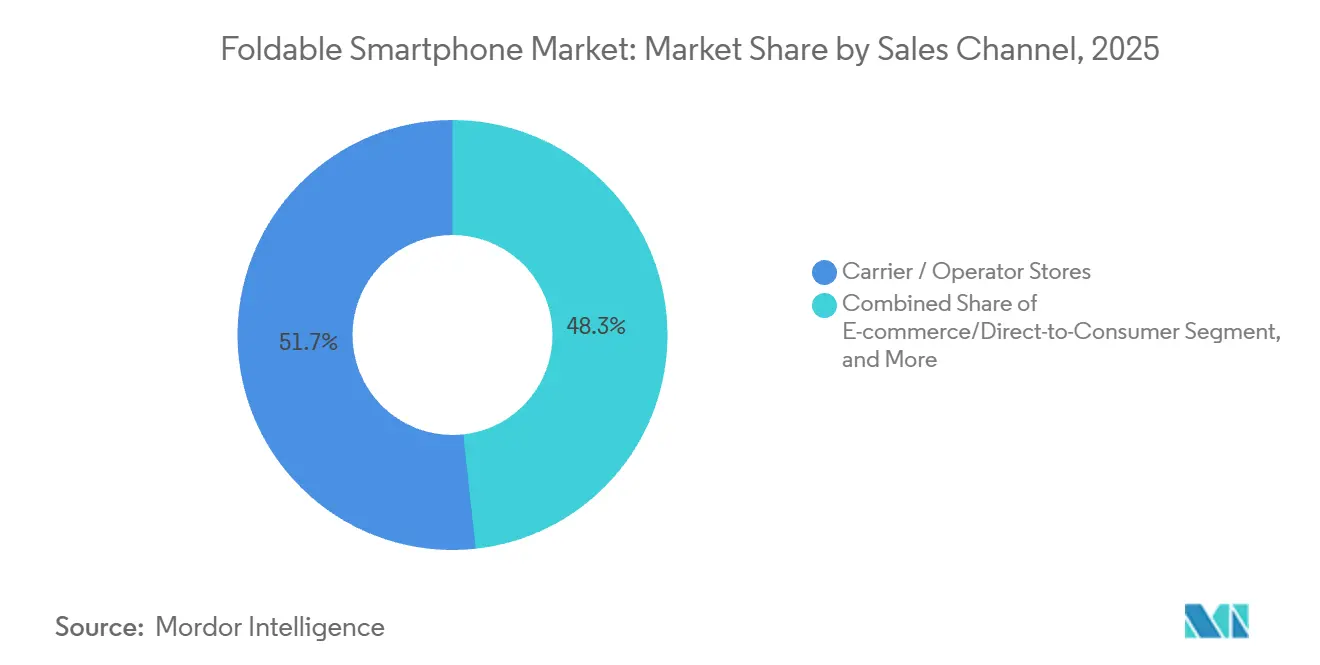

- By sales channel, carrier and operator stores commanded 51.73% of 2025 sales, yet e-commerce and direct-to-consumer channels are growing at 24.32% CAGR through 2031.

- By end user, consumers delivered 72.46% of 2025 revenue, but enterprise purchases are accelerating at a 26.19% CAGR on demonstrated 22% productivity gains in pilot programs.

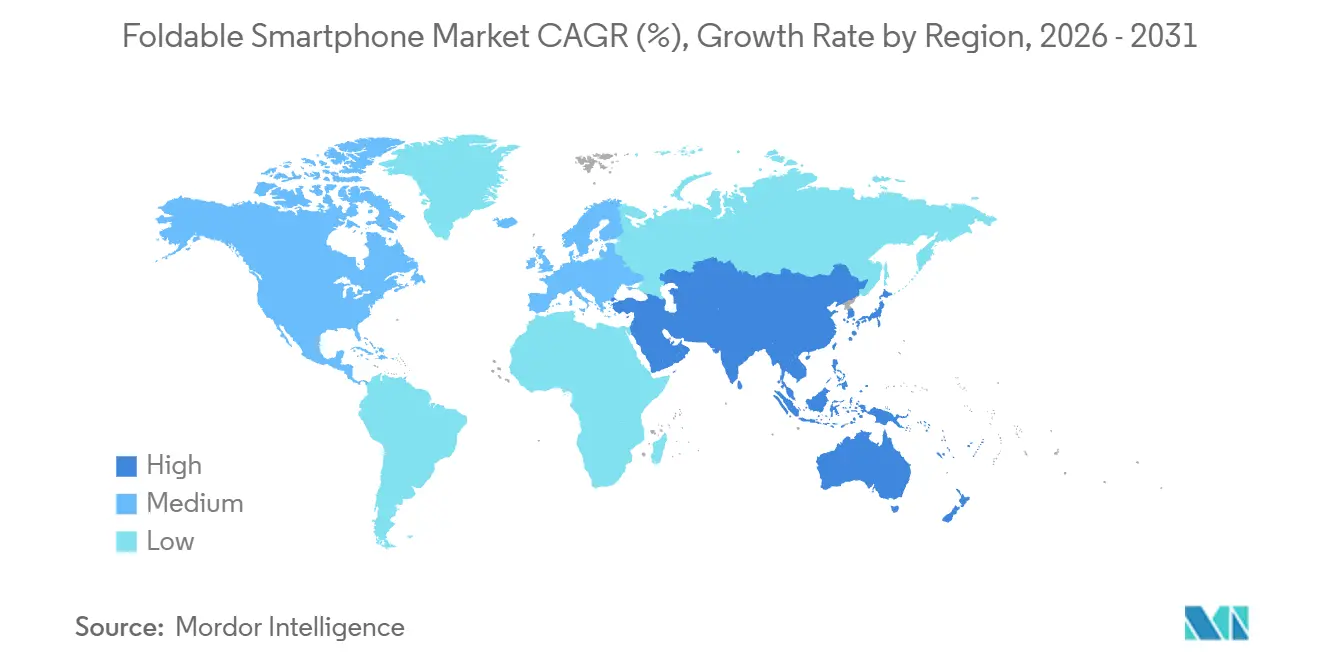

- By geography, Asia-Pacific controlled 54.84% of 2025 revenue, while the Middle East is the fastest-growing region at 23.43% CAGR for the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Foldable Smartphone Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Advancements in Ultra-Thin Glass Yield Rates | +4.2% | Global, with manufacturing concentrated in South Korea, China | Medium term (2-4 years) |

| Carrier Subsidization Strategies for Premium 5G Plans | +3.8% | North America, Europe, Middle East | Short term (≤ 2 years) |

| Enterprise Demand for Foldables to Support Field-Productivity Apps in Logistics Sector | +3.5% | Global, early adoption in North America, Asia-Pacific logistics hubs | Medium term (2-4 years) |

| Content-Streaming Partnerships Requiring Wider Aspect Ratios | +2.1% | Global, led by North America and Europe content consumption | Medium term (2-4 years) |

| Declining Per-Unit Cost of Flexible AMOLED Panels | +4.9% | Global, supply concentrated in South Korea, China | Short term (≤ 2 years) |

| Emergence of Foldable-Specific Mobile Gaming Titles Monetized via In-App Purchases | +2.3% | Asia-Pacific core, spill-over to North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Advancements in Ultra-Thin Glass Yield Rates

Ultra-thin-glass yield improvements from 60% in 2023 to 85% in 2025 cut scrap costs and enabled sub-USD 1,000 models for emerging markets without eroding gross margins. Samsung Display and Corning achieved 30 micrometer substrates via precision chemical etching, reducing dependence on polyimide films that scratch easily. As yields approach 90% by 2027, the cost gap between foldable and conventional flagship displays is projected to shrink below 15%, paving the path for broader adoption.

Declining Per-Unit Cost of Flexible AMOLED Panels

A 30% price drop between 2024 and 2025 followed BOE and Visionox capacity expansions that added 50,000 m² of Gen-6 OLED lines and Samsung Display’s low-temperature polycrystalline oxide licensing program. Cheaper panels now support 120 Hz and HDR10+ on mid-tier devices, absorb tariff volatility, and align with EU energy directives, as OLED manufacturing consumes 40% less energy than LCD.[1]International Energy Agency, “Energy Efficiency in Electronics Manufacturing,” iea.org

Carrier Subsidization Strategies for Premium 5G Plans

North American and European operators embed foldables into unlimited-data bundles, offering as much as USD 1,000 in trade-in credits that halve upfront costs. Middle East carriers mirror the model to attract high-income subscribers, although sustained subsidy spending strains margins and is expected to taper after 2027.

Enterprise Demand for Foldables to Support Field-Productivity Apps in Logistics Sector

Deployments doubled in 2025; DHL reported 22% faster inventory audits using 5,000 Galaxy Z Fold5 units, and Microsoft built Dynamics 365 features that exploit dual-screen workflows. Recurring managed-service contracts boost OEM revenue beyond hardware sales, though cost-sensitive industries still balk at USD 1,500 price tags.

Restraints Impact Analysis of Foldable Smartphone Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sub-200k Cycle Hinge Durability Concerns in Humid Tropics | -2.8% | Southeast Asia, South Asia, Sub-Saharan Africa, Latin America | Short term (≤ 2 years) |

| Limited App Optimization for Multi-Window Foldable UI | -2.3% | Global, most acute in markets with fragmented app ecosystems | Medium term (2-4 years) |

| Supply-Chain Bottlenecks for UTG and Hinge Components (Post-2023 Taiwan Quake) | -1.9% | Global, manufacturing concentrated in Taiwan, South Korea | Short term (≤ 2 years) |

| Volatile Import Tariffs on Flexible OLED Components in Key Emerging Markets | -1.6% | India, Brazil, Southeast Asia, Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sub-200k Cycle Hinge Durability Concerns in Humid Tropics

Field reports from Indonesia and coastal India show hinges failing within 18 months, three times the claim-rate of temperate markets, due to corrosion from sustained 80% humidity. OEMs face elevated warranty costs and explore sealed or coated mechanisms that increase weight and bill-of-materials.

Volatile Import Tariffs on Flexible OLED Components in Key Emerging Markets

India’s 2025 duty exemptions on batteries and displays dropped component costs 12%, but Brazil’s 60% electronics import levy and Nigeria’s FX caps still constrain retail affordability.[2]Government of India Ministry of Finance, “Import Duty Exemptions Notification,” finmin.nic.in

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Foldable Smartphone Market Segment Analysis

By Form Factor:

Rollables Challenge Book-Style DominanceBook-style units held 62.31% of 2025 foldable smartphone market share, anchored by Samsung’s Galaxy Z Fold line and Huawei’s Mate X series. Rollable displays from OPPO and Motorola, growing at 24.21% CAGR, promise crease-free expansion from 6.7 inches to 7.4 inches without added thickness, positioning the foldable smartphone market for another wave of form-factor disruption.

Folding clamshells, prized for pocketability, sustain demand among fashion-forward buyers, while outward-fold designs remain niche due to screen-protection challenges. Tri-fold prototypes hint at future 10-inch displays that could further enlarge the foldable smartphone market size for productivity-oriented professionals.

By Screen Size:

Larger Displays Drive Tablet ReplacementThe 7-8 inch bracket generated 44.34% of 2025 revenue as customers used single devices to replace tablets, and models exceeding 8 inches are slated for a 25.76% CAGR to 2031. These gains underline a strategic pivot within the foldable smartphone market toward bigger canvases that accommodate side-by-side applications.

Clamshells below 6.9 inches endure for portability, but enterprise buyers gravitate to 7-8 inch devices where foldable smartphone market size expansion aligns with ERP and video-conferencing use cases. Screen-ratio experimentation, such as 21:9 unfolded versus 25:9 folded, aims to balance usability and thickness.

By Price Range:

Mid-Premium Segment Expands FastestUnits priced USD 1,000-1,499 delivered 48.51% of 2025 revenue, yet the USD 1,500-1,999 tier is advancing at 26.52% CAGR as OEMs integrate periscope lenses, titanium frames, and IP68 sealing without breaching USD 2,000. This “premiumization with accessibility” tightens the gap between foldables and slate flagships within the foldable smartphone market.

Devices above USD 2,000 remain limited to Samsung’s and Huawei’s highest-end entries, while sub-USD 1,000 concepts from TECNO and OnePlus indicate looming price compression that could broaden foldable smartphone market penetration.

By Sales Channel:

E-Commerce Erodes Carrier DominanceCarrier stores still accounted for 51.73% of 2025 sales, but direct-to-consumer websites and marketplaces are scaling at 24.32% CAGR as brands leverage online trade-ins, extended warranties, and virtual try-on tools.

Carrier lock-ins dominate in regions with heavy subsidies like North America, whereas price transparency and flash sales drive Asia-Pacific’s e-commerce leadership, reshaping revenue streams inside the foldable smartphone market.

By End User:

Enterprise Adoption AcceleratesConsumers generated 72.46% of 2025 revenue, but business deployments are climbing at a 26.19% CAGR after documented 22% efficiency gains in warehouse audits, steering the foldable smartphone market toward recurring service models.

Government pilots in Singapore and the U.S. Veterans Affairs hint at future public-sector demand once security certifications mature, gradually shifting foldable smartphone market size contributions from pure hardware to managed mobility.

Geography Analysis

APAC Foldable Smartphone Market

Asia-Pacific captured 54.84% of 2025 revenue, as Huawei, Honor, Xiaomi, and Oppo shipped over 8 million units in three quarters despite chipset supply constraints, underscoring how local ecosystems power foldable smartphone market leadership. China’s Mate XT tri-fold sold out at CNY 19,999 (USD 2870.78), South Korea enjoys high per-capita uptake, and India’s tariff relief in March 2025 trimmed costs, though price remains a hurdle for mass buyers. Southeast Asia’s rising incomes and carrier subsidies are widening the foldable smartphone market, yet hinge failures in humid climates are tempering momentum.

Saudi Arabia Foldable Smartphone Market

The Middle East exhibits the highest CAGR of 23.43%, propelled by Vision 2030 digitization targets and zero-down carrier bundles that place USD 1,800 devices within the reach of affluent consumers. Saudi Arabia’s Public Investment Fund earmarked USD 500 million for digital government services, creating procurement opportunities that will expand the foldable smartphone market across the enterprise and public sectors.[3]Saudi Arabia Public Investment Fund, “Annual Report 2025,” pif.gov.sa

North America, Europe, LATAM and Africa Foldable Smartphone Market

North America accounts for roughly 22% of 2025 revenue; Samsung’s 64% share is maintained through partnerships with Verizon, AT&T, and T-Mobile, though Google’s Pixel 9 Pro Fold launches at USD 1,799 with limited channel reach. Europe mirrors this premium profile, while Latin America and Africa collectively stay below 5% share because of tariffs and currency risk, suggesting future growth will depend on local assembly and enterprise seeding.

Regulatory Landscape

The regulatory environment for foldable smartphones is tightening around durability, repairability, and interoperability, with the European Union providing the clearest device-specific anchors. Regulation (EU) 2023/1670 sets ecodesign requirements that explicitly cover foldable smartphones, with provisions effective from June 20, 2025, including minimum durability-type tests (for example, drop testing and scratch resistance thresholds) and related labeling rules. These requirements flow into hinge design, cover-screen protection, and the validation protocols that OEMs and ODMs use.

Charging and radio compliance continue to shape global product configurations. In the EU, Directive (EU) 2022/2380 and related measures require USB Type-C for wired-charging-capable mobile phones (including foldables) and alignment with relevant USB and power delivery specifications, which pushes OEMs toward harmonized charging hardware across regions. In the United States, foldables operate under FCC equipment authorization requirements in 47 CFR Part 2, and device-specific procedural actions have occurred, including an FCC temporary waiver granted to Samsung Electronics in October 2024 for certain foldable models. This also highlights the role of RF compliance workflows during rapid iteration cycles.

Value Chain Analysis

The foldable smartphone value chain starts with advanced materials and display sub-systems, then concentrates into specialized midstream processing and high-precision assembly. Upstream inputs include flexible AMOLED stacks and ultra-thin glass (UTG) supply, where base materials are sourced from companies such as Corning and SCHOTT, while finishing and strengthening are handled by UTG specialists including Dowoo Insys and Lens Technology. Components then move into precision module builds, where foldable designs depend on tightly controlled alignment and bonding processes (often cited at micrometer-level repeatability) to integrate UTG, flexible OLED, touch layers, and protective films without compromising fold performance.

Midstream and downstream participants include hinge module suppliers and device assemblers, followed by distribution through carrier/operator stores and direct-to-consumer e-commerce channels. Hinges require bespoke mechanical engineering and increasingly complex fabrication methods, including 3D-printing-enabled approaches in some supplier ecosystems. In the foldable hinge supply base, the names cited include Shin Zu Shing, Amphenol, KH Vatech, and S-connect. On the OEM side, the supply chain is shaped by sourcing decisions and platform dependencies, with Samsung Display positioned as a pivotal foldable OLED supplier and deep mass production experience. The 2026 context around Apple-related foldable specification finalization and supplier alignment also points to how major entrants can pull upstream capacity, qualification, and component standardization into longer-cycle supply agreements.

Competitive Landscape

Foldable smartphone market concentration is moderate. Samsung, Huawei, and Motorola shipped 80% of 2025 units, yet shares are fragmenting as Honor, Xiaomi, Oppo, and vivo expand abroad. Samsung’s vertical integration secures 40% gross margins, Huawei’s domestic resurgence leverages tri-fold innovation and nationalism, and Motorola’s sub-USD 1,000 Razr targets style-centric buyers.

Patent portfolios diverge: Samsung files for under-display cameras plus S Pen-ready hinges, OPPO pursues rollable technology, and Apple’s out-fold concepts signal future disruption once display reliability meets Cupertino’s tolerances. White-space opportunities lie under USD 800 and in enterprise-grade devices with enhanced stylus and desktop modes.

BOE’s USD 2.8 billion OLED expansion prepares a shift from component supplier to white-label OEM, potentially reshaping supply dynamics. Meanwhile, TECNO and OnePlus aim at emerging markets, and Google’s second-generation Pixel Fold deepens the Android tight-integration play. Competitive intensity will hinge on hinge durability, software optimization, and AI-powered multitasking that maximizes foldable real estate.

Foldable Smartphone Industry Leaders

Samsung Electronics Co. Ltd.

Huawei Technologies Co. Ltd.

Motorola Mobility LLC (Lenovo Group Limited)

Xiaomi Corp.

Oppo Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Foldable Smartphone Market Companies Covered in this Report

- Samsung Electronics Co. Ltd.

- Huawei Technologies Co. Ltd.

- Motorola Mobility LLC (Lenovo)

- Xiaomi Corp.

- Oppo Co. Ltd.

- vivo Communication Technology Co. Ltd.

- Royole Corp.

- Honor Device Co. Ltd.

- TCL Technology Group Corp.

- ZTE Corporation

- Google LLC

- Microsoft Corp.

- Sony Corp.

- LG Electronics Inc.

- Apple Inc.

- TECNO Mobile Ltd.

- OnePlus Technology (Shenzhen) Co. Ltd.

- Energizer Holdings Inc.

- Sharp Corp.

- BOE Technology Group Co. Ltd.

- Visionox Technology Inc.

- Kyocera Corp.

Market Opportunities and Future Outlook

Opportunities are opening where foldables can move from novelty hardware to quantified productivity and durability-driven replacement, especially in enterprise and carrier-led channels. Enterprise pilots provide a concrete demand signal: deployments doubled in 2025 in logistics and field service, and DHL cited 22% faster inventory audits using 5,000 Galaxy Z Fold5 units. Microsoft also added Dynamics 365 features designed around dual-screen workflows. That mix creates whitespace for OEMs and software partners to package foldable-specific workflows (multi-window, stylus and desktop modes, device management) as managed offerings rather than one-time premium hardware sales.

Material and mechanical refinement is becoming a visible commercial lever, supporting premium pricing and broader acceptance in harsh-use conditions that previously drove warranty and churn. In July 2026, Samsung introduced Flex Titanium technology for foldable displays, highlighting a titanium-alloy film approach aimed at improving durability and reducing crease visibility, which aligns with consumer and enterprise pain points around hinge and display longevity. Cost-down progress in the component base is also measurable in the market context, with flexible AMOLED panel prices declining 30% between 2024 and 2025 and UTG yields surpassing 85% in 2025. At the same time, distribution is shifting as e-commerce and direct-to-consumer channels scale alongside carrier trade-in credits that have brought premium devices below the USD 1,500 psychological threshold in some bundles.

Recent Industry Developments in Foldable Smartphone Market

- July 2026: Samsung introduced Flex Titanium technology for foldable displays, highlighting a titanium-alloy film approach to improve structural rigidity and reduce crease visibility in upcoming foldable devices. The announcement shifts differentiation toward materials engineering to address durability concerns that elevate warranty costs and slow adoption in humid and high-use environments.

- June 2026: Samsung foldable models for its next cycle cleared key regulatory steps, including BIS certification in India and FCC certification in the United States for select devices referenced in public reporting. These approvals support synchronized multi-region launch planning and reduce time-to-shelf risk for carrier and retail partners that rely on predictable flagship release windows.

- July 2025: Samsung launched the Galaxy Z Fold6 and Galaxy Z Flip6 with hinges rated for 500,000 folds while maintaining flagship pricing at USD 1,799. The higher durability specifications at a steady price point increased competitive pressure on rivals to match hinge reliability without pushing devices beyond the mid-premium affordability boundary created by trade-in and subsidy programs.

Foldable Smartphone Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers factory-built handheld foldable smartphones where the main display bends, folds, or rolls and still operates as a full touchscreen phone with a mobile operating system. The market size is presented in value terms and reflects sales into both consumer and enterprise channels across geographies.

Scope exclusions: Larger foldable tablets and laptops, and rugged industrial handheld devices are excluded from the market numbers.

Segments Covered in This Report

- By Form Factor

- Clamshell (Vertical Fold)

- Book-Style (Horizontal Fold)

- Outward Fold

- Rollable/Slide-out

- By Screen Size

- Less than Equal 6.9 inch

- 7 - 8 inch

- Greater than to 8 inch

- By Price Range

- Less than USD 1,000

- USD 1,000 - 1,499

- USD 1,500 - 1,999

- Greater than equal USD 2,000

- By Sales Channel

- Carrier/Operator Stores

- Consumer Electronics and Specialty Retail

- E-commerce/Direct-to-Consumer

- By End User

- Consumer

- Enterprise/Corporate

- Government and Defense

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Australia and New Zealand

- Rest of Asia Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market frame and build an initial dataset before interviews began. We referenced public source types such as national telecom and ICT regulators, customs and trade statistics for handset and component flows, and ITU country indicators for mobile adoption, along with WTO datasets for tariff and trade context. Technical grounding was also supported through patent databases and peer-reviewed papers covering foldable display materials, hinge reliability, and UTG progress.

On the market side, inputs were checked using company filings and earnings transcripts, investor presentations, official product launch disclosures, and reputable press coverage that tracks shipments and pricing trends. A paid subscription for company financials and intelligence helped align disclosed revenue ranges with modeled volume and ASP assumptions. This list is illustrative only, and additional sources were reviewed for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with handset ecosystem participants, including device brands, component and display supply chain contacts, carriers and retailers, and repair and after-sales specialists who see real failure rates. This step was used to stress-test adoption assumptions by region, confirm realistic ASP movement by form factor, and check how quickly new designs, including rollable models, are likely to be commercialized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | APAC: 46% |

| Mid tier: 56% | Functional/Unit leaders: 32% | EMEA: 29% |

| Smaller Players: 19% | Managers: 55% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down reconstruction of the demand pool where overall smartphone shipments and upgrade cycles are filtered through foldable penetration by region, then converted into value using form factor level ASPs. After the top-down estimate is set, we corroborate totals using selective bottom-up approximations, such as sampled model lineups multiplied by expected unit mix and channel pricing, followed by distributor and carrier checks where available.

Key inputs that shape the model include foldable shipment run rates, average selling price spreads between book-style and clamshell designs, display panel and UTG cost direction, carrier subsidy intensity, and replacement and repair patterns that affect repeat purchases. When a data gap appears, assumptions are first bounded using the nearest comparable series (for example, premium smartphone pricing bands and launch cadence), then adjusted based on expert feedback so the final numbers stay realistic.

For forecasting, scenario analysis is used around a base case, because adoption can swing with component yields, pricing steps, and consumer confidence. The scenarios are anchored on what interviewees expect for model launches, availability in carrier channels, and how quickly durability concerns are being addressed.

Data Validation & Update Cycle

Outputs are checked against independent signals such as reported shipment commentary, major launch timing, and observed price movement, then variances are reviewed until the underlying drivers are clearly explained. We also run currency and inflation consistency checks so year-on-year changes are not created by conversion timing alone.

Before sign-off, the work goes through multiple analyst reviews, and outlier changes trigger re-contact with sources to confirm what shifted in the market. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is done so clients receive the most current view.

Mordor Intelligence's Foldable Smartphone Market Sizing Compared With Other Published Estimates

Different published market sizes for foldable smartphones often disagree because product scope and the value build-up are not handled in the same way. The largest differences usually come from how each study treats form factors, which price points are used for ASPs, and how quickly assumptions are refreshed when a new model cycle hits.

The main gap comes from whether rollable and dual-screen foldable designs are counted as part of foldables today, and Mordor Intelligence treats them as included only when they are commercially sold as factory-built phones with full touchscreen and mobile-OS functionality, rather than being inferred from flexible-display activity.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 31.37 B (2025) | |

| Global Consultancy A | USD 34.65 B (2024) | Uses a different base year and may emphasize flip and fold models with limited clarity on enterprise channel revenue and how pricing is normalized across regions. |

| Market Research Publisher B | USD 29.64 B (2025) | Relies heavily on a units times ASP build-up with less visibility into ASP step-downs over a model cycle, and may leave out newer form factors such as rollable devices. |

Across the three figures, the spread is mainly explained by what gets counted as a foldable phone versus an adjacent flexible-display product, and by how ASP progression is handled year to year. By keeping the scope tied to commercially sold foldable smartphones and validating pricing and adoption assumptions with real channel feedback, our estimate stays traceable to a repeatable set of inputs.

Key Questions Answered in the Report

What CAGR is forecast for the foldable smartphone market through 2031?

The foldable smartphone market is projected to grow at a 23.29% CAGR between 2026 and 2031.

Which form factor currently leads revenue?

Book-style models held 62.31% revenue share in 2025.

Which region is expanding fastest?

The Middle East is poised for the highest 23.43% CAGR through 2031.

How big is enterprise demand relative to consumers?

Enterprises accounted for 27.54% of 2025 revenue and are growing at a 26.19% CAGR, outpacing consumer growth.

What price segment shows the quickest growth?

Devices priced USD 1,500-1,999 are expanding at a 26.52% CAGR.

Which companies dominate shipments?

Samsung, Huawei, and Motorola together shipped 80% of units in 2025.

Page last updated on: