Flexible Foam Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

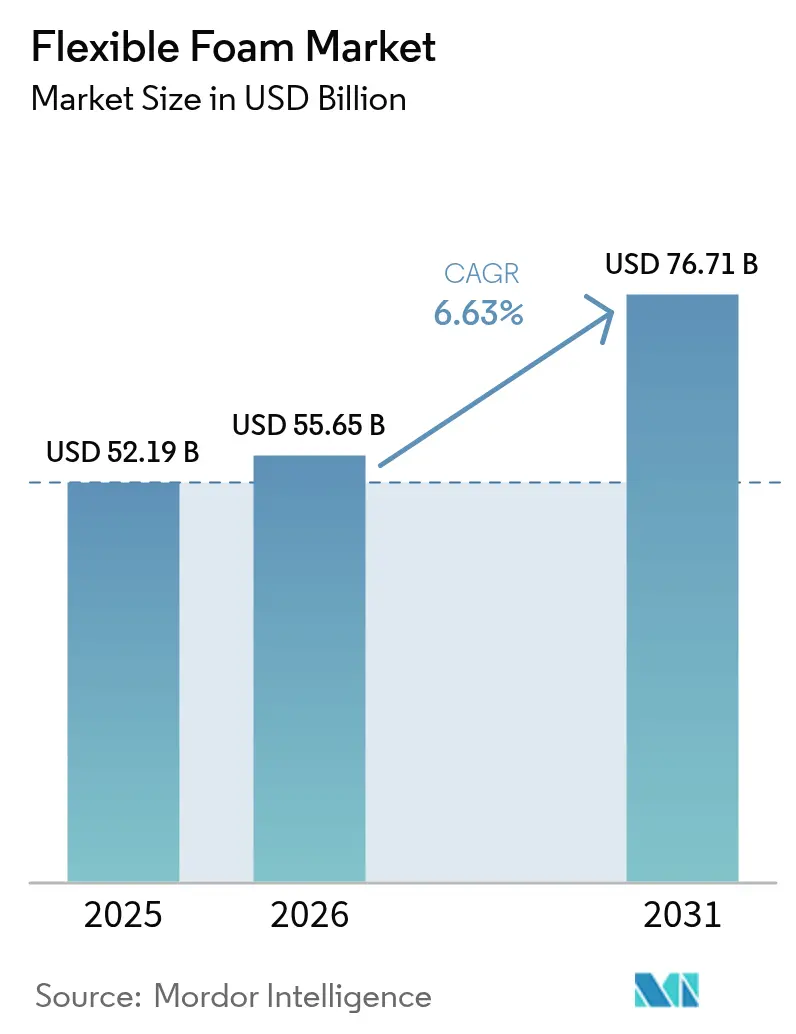

| Market Size (2026) | USD 55.65 Billion |

| Market Size (2031) | USD 76.71 Billion |

| Growth Rate (2026 - 2031) | 6.63% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexible Foam Market Analysis by Mordor Intelligence

Flexible Foam market size in 2026 is estimated at USD 55.65 billion, growing from 2025 value of USD 52.19 billion with 2031 projections showing USD 76.71 billion, growing at 6.63% CAGR over 2026-2031.

Rising e-commerce packaging volumes, lightweighting imperatives in automotive seats, and a broad push toward sustainable chemistry underpin this expansion. Polyurethane maintains clear leadership thanks to its tunable density profiles, while carbon-capture polyol technologies and graphene-enhanced formulations illustrate ongoing performance gains. Asia-Pacific’s manufacturing depth and domestic consumption growth secure its position as the largest regional contributor. Meanwhile, strategic acquisitions signal a maturing competitive landscape that prizes vertical integration and omnichannel reach.

Key Report Takeaways

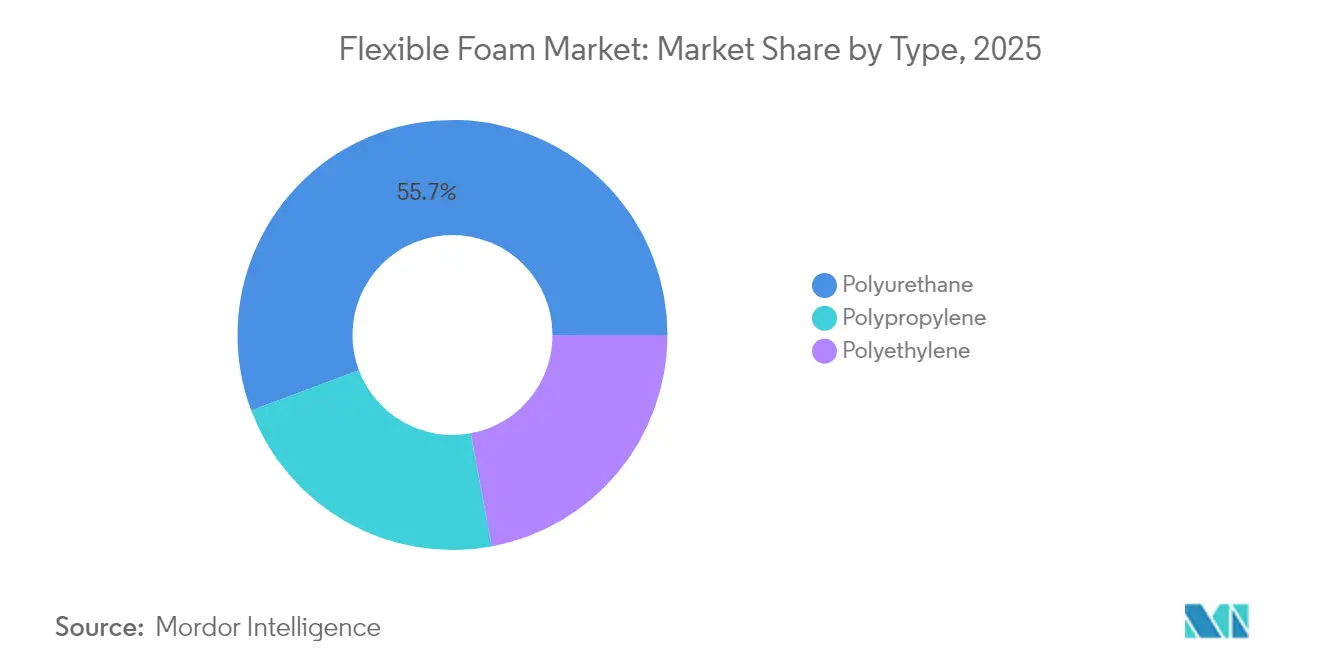

- By type, polyurethane foam led with 55.72% of flexible foam market share in 2025; the type is forecast to expand at a 7.34% CAGR through 2031.

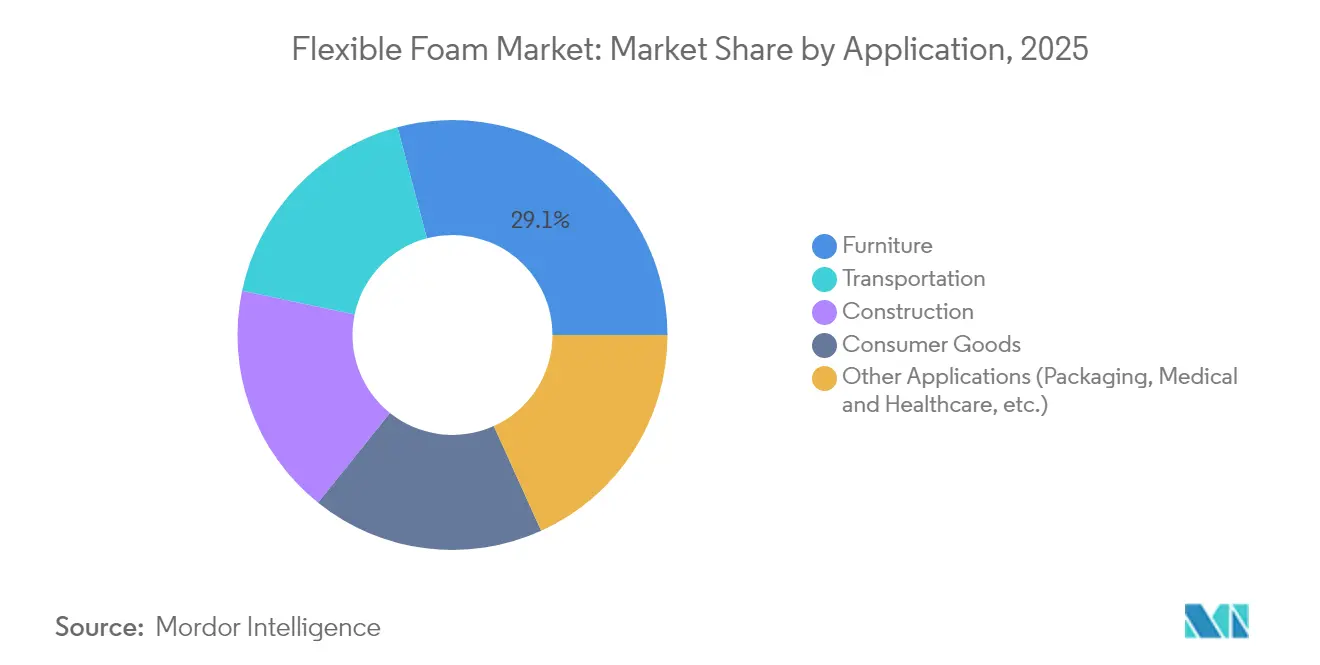

- By application, furniture accounted for a 29.12% share of the flexible foam market size in 2025, while other applications such as packaging, medical, and healthcare are advancing at an 7.62% CAGR through 2031.

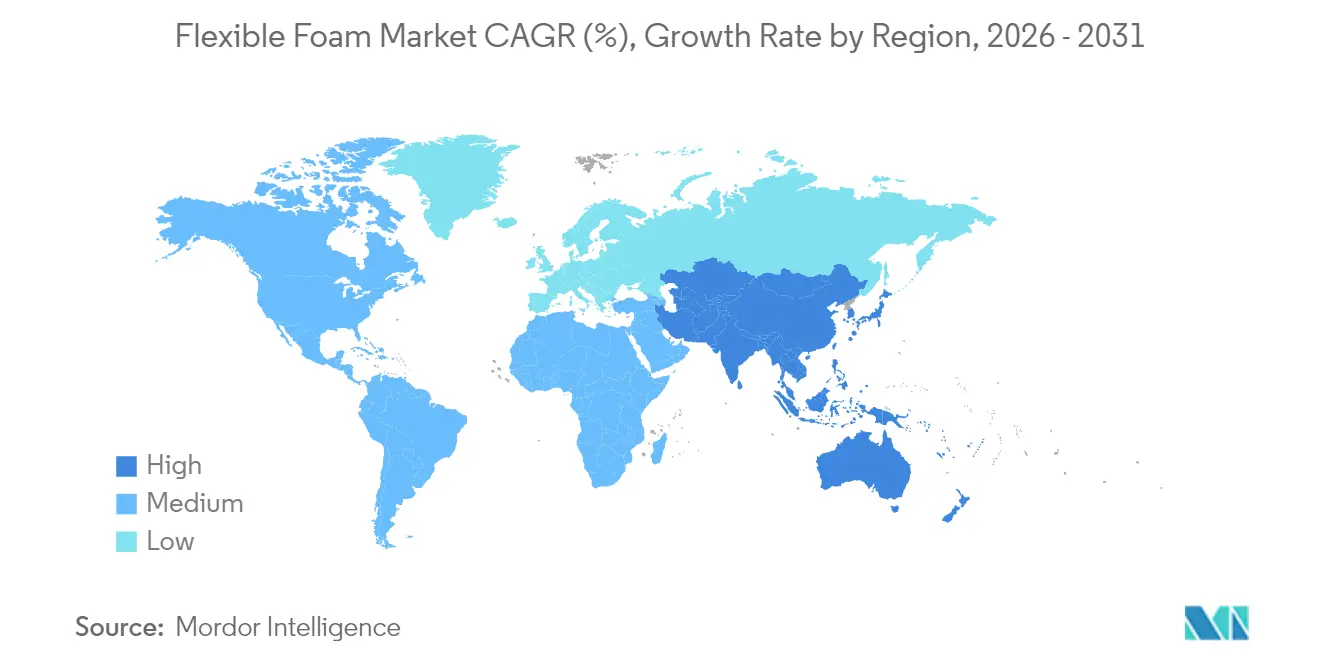

- By geography, Asia-Pacific captured 45.60% revenue share in 2025; the region is projected to register the fastest 7.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flexible Foam Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging E-Commerce Packaging Demand | +1.8% | Global, with APAC and North America leading | Short term (≤ 2 years) |

| Furniture and Bedding Refresh Cycles in Mature Economies | +1.2% | North America and EU primarily | Medium term (2-4 years) |

| Lightweight Automotive Seating and NVH Requirements | +1.5% | Global, concentrated in automotive hubs | Medium term (2-4 years) |

| Adoption of CO₂-Based Polyols and Circular Foam Chemistries | +0.9% | EU and North America early adoption, global expansion | Long term (≥ 4 years) |

| Bed-In-A-Box Mattress Logistics Boom | +1.1% | North America and EU mature markets, APAC emerging | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging E-Commerce Packaging Demand

Protective packaging needs for fragile electronics and premium direct-to-consumer deliveries are driving polyurethane foam volumes. The global packaging foam segment is set to move from USD 12.22 billion in 2025 to USD 15.36 billion by 2034, a 4.68% CAGR, underscoring polyurethane’s shock-absorption advantage. Asia-Pacific leads this shift as device makers specify custom foam inserts for smartphones and tablets. Retailers differentiate through elevated unboxing experiences that rely on flexible foam solutions. Extended Producer Responsibility rules in Europe, however, push producers to design recyclable formats that may limit traditional formulations. Manufacturers with circular chemistries stand to win share as compliance deadlines near.

Furniture and Bedding Refresh Cycles in Mature Economies

Remote-work investments and wellness centricity are shortening furniture replacement timelines in developed markets. European furniture production rose 1.5% over the first four months of 2025 versus 2024, signaling continued recovery[1]Globalwood, “European Furniture Production Update,” globalwood.org . Consumers demand premium seating and bedding that blend ergonomics with low-VOC profiles. Foam manufacturers able to deliver breathability, antimicrobial additives, and precision zoning capture premium margins. Yet spending remains sensitive to mortgage rates and housing turnover, potentially tempering growth in periods of macro stress.

Lightweight Automotive Seating and NVH Requirements

Automakers target 50 miles-per-gallon fleet averages by 2025, spurring adoption of low-density polyurethane that trims seat weight by over 10% while meeting crash norms. Ford’s graphene-enhanced foam elevates compression strength 20% and boosts sound absorption 25% without mass penalties. Electric vehicle uptake amplifies the need for NVH damping formerly masked by engine noise. Covestro’s Bayfit SA platform extends to hoodliners and floor modules that pair acoustic gains with biocircular feedstocks. The segment nevertheless rides cyclical production swings and chip-related disruptions.

Adoption of CO₂-Based Polyols and Circular Foam Chemistries

Covestro’s cardyon® process upcycles captured CO₂ into polyol chains containing up to 20% carbon dioxide, cutting fossil inputs and energy intensity. Recticel’s KAPUA® replaces one-seventh of petroleum with CO₂-based intermediates while retaining OEKO-TEX® credentials. INOAC’s ECOLOCEL® reaches 50% plant content, proving bio-derived feedstocks can meet mattress resilience criteria. Early adopters gain regulatory headroom and brand advantage, though R&D costs and supply-chain recertification moderate near-term uptake.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Isocyanate and Polyol Feedstock Prices | -1.4% | Global, with regional supply chain variations | Short term (≤ 2 years) |

| Stricter VOC / Flame-Retardant Regulations | -0.8% | EU and North America leading, global adoption | Medium term (2-4 years) |

| Transition to Halogen-Free FR Systems Raises Cost And Complexity | -0.6% | Global, with varying compliance timelines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Isocyanate and Polyol Feedstock Prices

MDI and TDI swings compress margins when pass-through pricing lags. BASF lifted select diols by USD 0.08-0.10 lb in April 2025 amid crude volatility. Dow’s closure of an Argentina polyols site illustrates supply-demand imbalances that ripple through regional costs. U.S. consumption hit 434.9 million lb for pure MDI and 482.9 million lb for TDI in 2023, highlighting the market’s raw-material exposure. Contract structures that lock in index-based formulas help larger processors mitigate shocks but smaller converters remain vulnerable.

Stricter VOC / Flame-Retardant Regulations

New York bans intentional use of flame retardants in upholstered items from December 2024, prompting reformulation toward barrier fabrics and graphite-infused foams. EPA health assessments and California TB117-2013 push industry to low-smolder yet chemical-lean solutions. Europe’s REACH now requires special training for diisocyanate handling above 0.1% content, elevating compliance overhead. Producers investing early in halogen-free systems gain market access while others risk penalties and lost business.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Polyurethane Dominance Drives Innovation

Polyurethane held 55.72% of flexible foam market share in 2025 on the strength of its cost-to-performance balance. Polyester grades deliver durability for load-bearing mats while polyether variants retain hydrolytic stability in comfort seating. The segment is projected to post a 7.34% CAGR through 2031, cementing its role in the flexible foam market even as CO₂-based chemistries gain ground. Ford’s graphene-enhanced seat cushions demonstrate how nano-fillers can push compression strength up 20% while trimming weight 10%.

Polyethylene and polypropylene foams trail but carve niches in moisture-proof packaging and automotive headliners. Cross-linked polyethylene offers closed-cell moisture resistance, whereas non-cross-linked grades provide economical cushioning. Polypropylene’s recyclability and chemical inertia secure opportunities in under-hood thermal shields. Together, alternative resins broaden the flexible foam market by enabling applications unsuited to polyurethane’s thermoset nature.

By Application: Furniture Leadership Faces Emerging Competition

Furniture retained a 29.12% share of the flexible foam market size in 2025, benefiting from heightened home-office spending. Nonetheless, packaging, medical, and healthcare collectively display the fastest 7.62% CAGR to 2031 as brand owners seek tailored cushioning and infection-control solutions. Mattress manufacturers experiment with phase-change microcapsules and zoned firmness to capture premium tiers, while hospital beds require anti-microbial, low-VOC pads to comply with tightening indoor-air mandates.

Transportation and construction follow, fueled by electric-vehicle NVH mitigation and retro-fit insulation mandates. Consumer goods, from athletic footwear to personal-care applicators, rely on foam’s softness and rebound to differentiate. The shifting mix signals that future volume gains may outpace furniture, redefining where manufacturers allocate capacity and R&D funds within the flexible foam market.

Geography Analysis

Asia-Pacific controlled 45.60% of 2025 revenue and is projected to expand at a 7.35% CAGR through 2031, underscoring its central role in the flexible foam market. China’s entrenched supply base partners with India’s USD 87 billion petrochemical build-out, while ASEAN nations benefit from “China + 1” diversification. Sekisui Chemical’s new INR 500 million Pune site signals ongoing localization for automotive seating foams.

North America maintains technological leadership despite cyclical dips in bedding and vehicle output. The U.S. leverages abundant natural gas feedstock, and Mexico now ranks as the fourth-largest polyurethane consumer thanks to near-shoring EV assembly. Regulations favor low-VOC and circular feedstocks, creating pull-through for CO₂-based polyols.

Europe balances stringent environmental rules with innovation incentives. Dow’s strategic review of its European polyurethane chain shows profitability strains amid high energy costs. Yet the bloc leads in circular foam adoption, driven by the 2024 Packaging and Packaging Waste Regulation mandating recyclability. South America and Middle East and Africa add incremental demand as infrastructure programs specify energy-efficient insulation, though currency volatility tempers investment.

Competitive Landscape

The flexible foam market remains highly fragmented but is moving toward strategic clustering. Tempur Sealy’s USD 5 billion Mattress Firm acquisition and Leggett & Platt’s USD 1.25 billion Elite Comfort Solutions deal highlight vertical integration aimed at controlling both branded bedding and specialty foam inputs[2]Tempur Sealy International, “Mattress Firm Acquisition,” tempursealy.com . Carpenter Co.’s EUR 656 million take-over of Recticel’s Engineered Foams business extends capacity in technical laminates, though UK regulators are scrutinizing competition impacts.

Global chemical majors—BASF, Covestro, Dow—command advantage through end-to-end supply chains and deep R&D pipelines. They focus on CO₂-based polyols, bio-attributed MDI, and digitalized production lines that cut scrap and CO₂. Regional converters differentiate on speed, service, and specialized formulations such as halogen-free acoustic foams. Product innovation around nanomaterial reinforcement and closed-loop recycling aims to defend margins in commodity segments. Compliance infrastructure has become a gating factor: smaller firms face hurdles meeting REACH diisocyanate rules, potentially accelerating consolidation in the flexible foam market.

Flexible Foam Industry Leaders

Carpenter Co

Covestro AG

Woodbridge

Greiner AG

SEKISUI CHEMICAL CO., LTD

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Dow commenced production of VORANOL WK5750 at its Freeport polyol plant. The new polyether polyol flexible foam product offers enhanced reactivity, optimal viscosity, and maintains high purity and quality standards.

- September 2024: BASF and Future Foam have started commercial production of flexible foam for the bedding industry using 100% domestically produced Biomass Balance (BMB) Lupranate® T 80 toluene diisocyanate (TDI). BASF manufactures the TDI at its Verbund production facility in Geismar, Louisiana.

Global Flexible Foam Market Report Scope

Flexible foam is used to cushion a wide range of consumer and commercial products, such as furniture, carpet cushions, transportation, bedding, packaging, textiles, and fibers. The market is segmented by type, application, and geography. By type, the market is segmented into polyurethane, polyethylene, and polypropylene. By application, the market is segmented into construction, consumer goods, furniture, transportation, and other applications. The report also covers the market size and forecasts for the flexible foam market in 15 countries across major regions. For each segment, market sizing and forecasts have been done on the basis of revenue (USD million).

| Polyurethane | Polyester |

| Polyether | |

| Polyethylene | Cross-linked |

| Non-cross-linked | |

| Polypropylene |

| Furniture |

| Transportation |

| Construction |

| Consumer Goods |

| Other Applications (Packaging, Medical and Healthcare, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Polyurethane | Polyester |

| Polyether | ||

| Polyethylene | Cross-linked | |

| Non-cross-linked | ||

| Polypropylene | ||

| By Application | Furniture | |

| Transportation | ||

| Construction | ||

| Consumer Goods | ||

| Other Applications (Packaging, Medical and Healthcare, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current flexible foam market size?

The flexible foam market size stands at USD 55.65 billion in 2026 and is forecast to reach USD 76.71 billion by 2031.

Which region leads the flexible foam market?

Asia-Pacific leads with 45.60% 2025 revenue share and is projected to post a 7.35% CAGR through 2031.

Why is polyurethane foam dominant in the flexible foam market?

Polyurethane offers versatile density control, strong strength-to-weight ratios, and ongoing innovation such as graphene reinforcement and CO₂-based polyols.

How are sustainability trends affecting flexible foam production?

Manufacturers are investing in CO₂-capture polyols, bio-based feedstocks, and recycling to meet tightening VOC and flame-retardant regulations.

What impact do raw-material price swings have on flexible foam producers?

Volatility in MDI and TDI prices can compress margins when converters cannot promptly pass costs to customers, especially in commodity furniture foam.

Page last updated on: