Fire Alarm Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 36.75 Billion |

| Market Size (2031) | USD 51.35 Billion |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

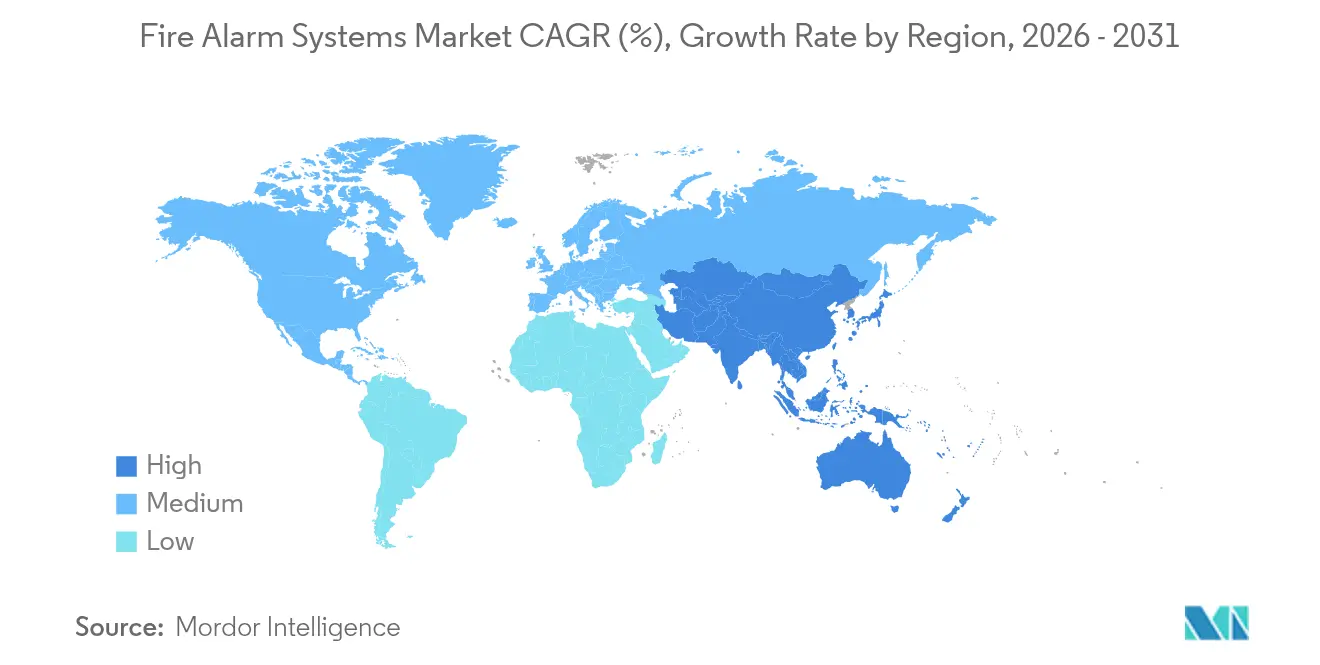

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

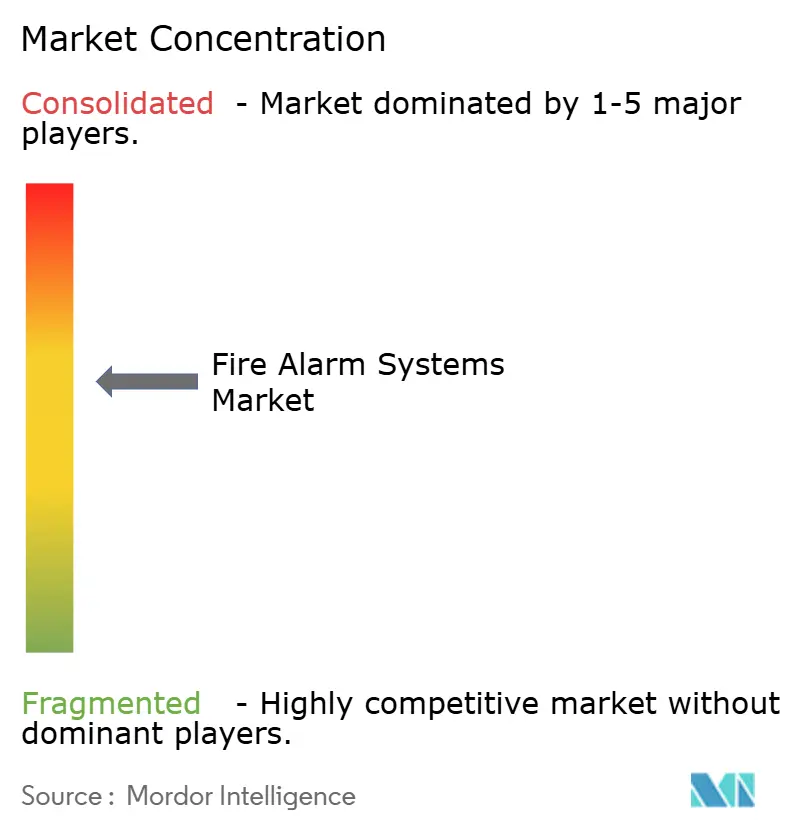

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fire Alarm Systems Market Analysis by Mordor Intelligence

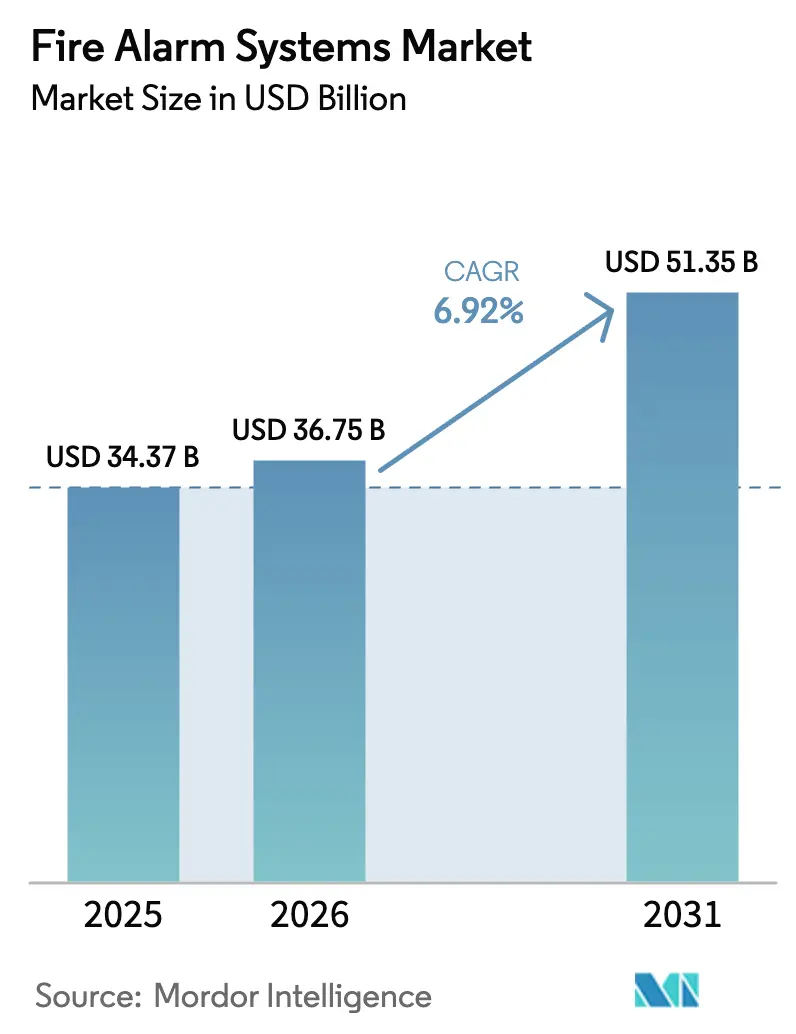

The fire alarm systems market size was valued at USD 34.37 billion in 2025 and estimated to grow from USD 36.75 billion in 2026 to reach USD 51.35 billion by 2031, at a CAGR of 6.92% during the forecast period (2026-2031). Strong code enforcement, the spread of smart-building projects, and a broad transition from hard-wired conventional panels to connected, addressable platforms sustained this growth path during 2024 and 2025. Commercial developers favored networkable systems that integrate with wider building-management software, while data-center operators and battery-storage owners demanded specialized detection and suppression that protect sensitive electronics. Rapid code revisions, such as NFPA 72 (2025), introduced cybersecurity obligations, thermal-imaging detection, and acoustic leak sensing, forcing vendors to redesign products and installers to upskill. Private-equity funds accelerated roll-ups to create national service platforms, a response to the technician shortage that lifted labour costs but widened aftermarket revenue opportunities. Regionally, spending momentum shifted toward the Asia-Pacific, while North America maintained scale advantages through earlier adoption of smart-facility retrofits.

Key Report Takeaways

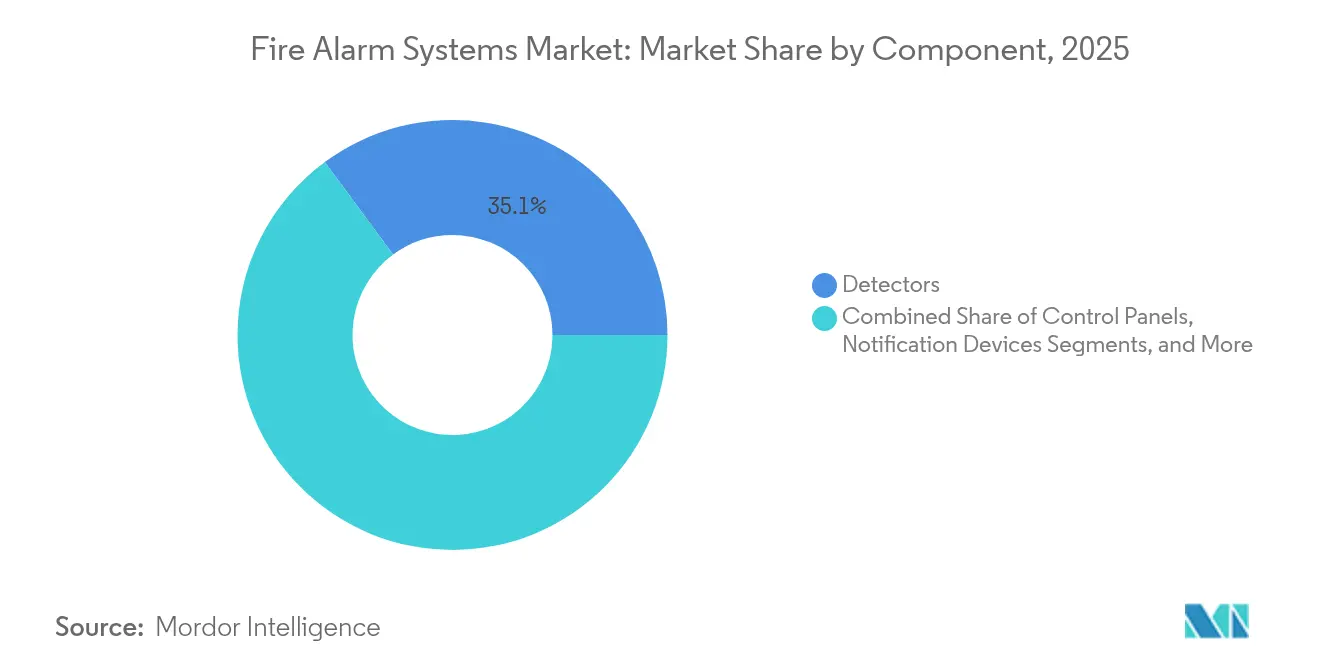

- By component, detectors accounted for 35.12% of the fire alarm systems market in 2025, are expected to advance at 8.07% CAGR through 2031.

- By system type, addressable fire alarm systems led the fire alarm systems market, accounting for a 64.12% market share in 2025. Meanwhile, hybrid systems are projected to grow at a 10.03% CAGR through 2031.

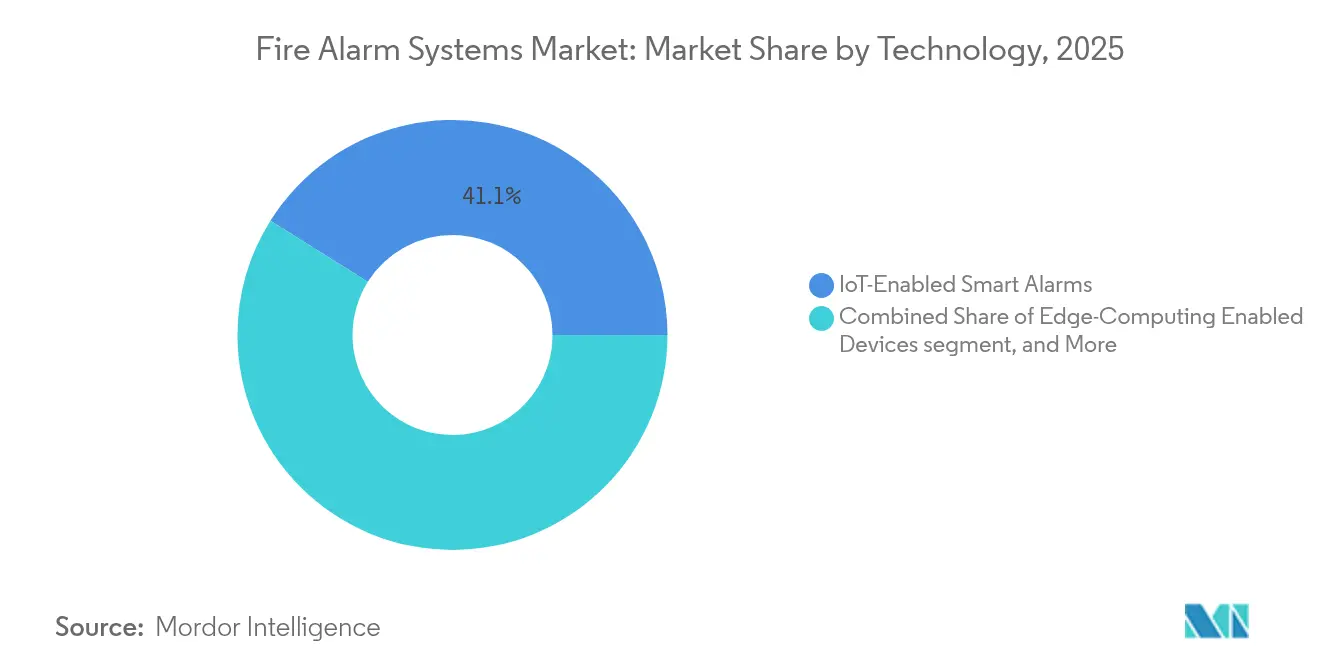

- By technology, IoT-enabled smart alarms accounted for 41.08% of the market in 2025, whereas AI-based analytics and predictive detection posted the fastest growth at 8.31% over the forecast period.

- By end-user industry, the commercial segment accounted for 48.05% of the fire alarm systems market size in 2025; the transportation and infrastructure segment is expected to advance at a 8.88% CAGR through 2031.

- By geography, North America held 40.02% of the fire alarm systems market size in 2025, whereas the Asia-Pacific region is forecast to post the fastest regional CAGR of 9.42% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fire Alarm Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global fire-safety regulations and codes | +1.8% | North America, EU | Medium term (2-4 years) |

| Acceleration of commercial real estate and smart-building construction | +1.5% | Asia-Pacific, North America | Long term (≥ 4 years) |

| Migration from conventional to addressable and networked systems | +1.2% | Global | Medium term (2-4 years) |

| Rapid expansion of data centres and Li-ion battery storage facilities | +1.0% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| NFPA 915-driven remote inspection and predictive maintenance adoption | +0.8% | North America, expanding global | Medium term (2-4 years) |

| Private-equity consolidation is accelerating product innovation | +0.6% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Global Fire-Safety Regulations and Codes

Code revisions shaped demand during 2024–2025. The 2025 update of NFPA 72 made cybersecurity controls, acoustic leak detection, and thermal-imaging capabilities mandatory for new addressable panels, following federal alerts that exposed buffer-overflow flaws that hackers could exploit in legacy systems.[1]Cybersecurity and Infrastructure Security Agency, “Siemens Desigo Fire Safety UL and Cerberus PRO Vulnerabilities,” cisa.gov European EN 54 standards moved in parallel, shifting certification from component-level to full-system testing to assure functional integrity. In North America, UL 217 and UL 268 smoke-alarm rules suppressed kitchen nuisance alarms, compelling residential builders to specify new sensor algorithms. As a result, the fire alarm systems market experienced a surge in retrofit orders, particularly on healthcare and education campuses, where “Restricted Audible Mode Operation” became mandatory for patient- and student-sensitive zones.

Acceleration of Commercial Real Estate and Smart Building Construction

Developers prioritized digital readiness even amid material-cost inflation. Fire alarm platforms with open APIs linked to energy dashboards, visitor management, and security video feeds, creating a single pane of glass for facility operators. Edge computers inside new panels processed smoke-sensor data locally, trimming latency for suppression commands while reserving the cloud for fleet-wide analytics. Wireless detectors and annunciators were chosen for retrofit towers where conduit labour had become cost-prohibitive, cutting installation time by up to 35%. Even with supply bottlenecks, contractors kept adoption high because smart-ready projects earned higher lease rates, reinforcing the upward trajectory of the fire alarm systems market.

Migration from Conventional to Addressable and Networked Systems

End users migrated quickly once they witnessed the operational gains from pinpoint location data and false-alarm suppression. Addressable loops used micro-current signalling that accepted both wired and EN 54-25 wireless devices, allowing phased upgrades without pulling new copper. Large universities swapped out conventional zone systems for networked platforms that supported voice evacuation, elevator recall, and HVAC smoke control in a single logic table. Rising copper prices during 2024 also swung cost-benefit analyses toward wireless, further reinforcing the fire alarm systems market’s switch to digital architectures.

Rapid Expansion of Datacenters and Li-ion Battery Storage Facilities

Server-dense halls and battery farms imposed new risk profiles. NFPA began drafting NFPA 800 to codify Li-ion safety across manufacturing and storage, pushing integrators to add early off-gas detection and gaseous suppression rather than water sprinklers. Data-centre clients demanded aspirating detectors tuned for low-airflow liquid-cooling corridors and mandated shutdown interfaces that isolate racks within seconds. Vendors responded with high-sensitivity laser sampling units and redundant network cards that maintain alarm integrity across dual paths. These specialized needs bolstered premium revenue streams within the fire alarm systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront installation and retrofitting costs | -1.2% | Global | Short term (≤ 2 years) |

| Nuisance/false-alarm frequency and associated fines | -0.8% | Dense urban areas, South Korea | Medium term (2-4 years) |

| Shortage of certified technicians for advanced systems | -0.6% | North America, Europe | Medium term (2-4 years) |

| Cyber-vulnerabilities in cloud-connected alarm networks | -0.4% | Global critical infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Installation and Retrofitting Costs

Addressable technology and specialty detectors carried price premiums of 15-25% over conventional gear through 2025. Retrofit projects in hospitals and heritage sites faced extra hurdles such as asbestos abatement and infection-control partitions, doubling labour hours. The technician shortfall, half of North American service firms reported vacancies amplified wage benchmarks and stretched project timelines. Small enterprises delayed upgrades or opted for the lowest-cost, limited-feature panels, creating a bifurcated demand curve inside the broader fire alarm systems market.

Nuisance/False-Alarm Frequency and Associated Fines

False dispatches remained a sore point despite algorithmic advances. Restaurants incurred escalating penalties when cooking aerosols triggered county fire-department rollouts, prompting brand chains to pilot AI-enhanced optical scattering detectors that differentiate steam from fire particles. Municipalities in Seoul and Singapore hiked repeat-offender fines, nudging owners toward multi-criteria sensors that blend smoke, heat, and CO signatures. Although these devices lowered nuisance trips by roughly 55%, their higher per-unit cost slowed adoption among price-sensitive segments of the fire alarm systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Detectors Drive Innovation Through IoT Integration

Detectors accounted for 35.12% of the fire alarm systems market in 2025 and are projected to grow at an 8.07% CAGR through 2031. Platform makers embedded micro-fog smoke, rate-of-rise heat, CO, and air-quality chambers in one housing, allowing algorithms to cross-reference signals and silence spurious alarms. Cloud-linked detectors streamed self-diagnostic data, giving service firms advance notice of contamination or impending battery depletion. As IoT frameworks mature, detectors become addressable nodes that feed real-time status into digital twins, a capability prized by pharmaceutical plants pursuing zero-downtime goals.

Control panels followed a parallel path of innovation. New boards incorporated dual IP ports, LTE failover, and TPM chips that meet NFPA 72 cyberhardening guidance. Power-supply modules switched to lithium-ion backup packs rated for 24-hour standby, halving rack footprint. Notification appliances utilized low-profile LED strobes and intelligible voice horns to comply with accessibility regulations. As accessories such as BACnet gateways and PoE switch racks are sold alongside every panel, the component mix becomes a system-level package that expands the average selling price, reinforcing growth within the fire alarm systems market.

By System Type: Addressable Platforms Command the Modern Build

Addressable fire alarm systems accounted for 64.12% of the fire alarm systems market share in 2025, a dominance that deepened as price gaps narrowed, while hybrid systems are set to expand at a 10.03% CAGR through 2031. Builders preferred them for precise point identification and for remote service functions that cut truck rolls by 20%. Modular addressable loops accepted wireless translators, creating hybrid topologies suited to phased renovations.

Conventional panels retained footholds in low-rise retail and rural warehouses, yet their share slid each year as copper costs rose. Voice evacuation systems, once a niche technology, gained mainstream traction after the NFPA introduced Restricted Audible Mode Operation to reduce patient stress in hospitals. This pushed panel makers to bundle audio amplifiers and prerecorded message libraries. In parallel, wireless-only systems blossomed in historic buildings where drilling masonry is restricted, delivering the fastest incremental revenue segment of the fire alarm systems market.

By Technology: AI and Edge Computing Redefine Detection

IoT-Enabled Smart Alarms accounted for 41.08% of the market in 2025. However, AI-based analytics and predictive detection experienced the fastest growth, with an 8.31% increase during the forecast period. IoT-connected architectures dominated the fire alarm systems market in 2025, driven by decreasing sensor module costs and enterprise requirements for unified facility dashboards. Additionally, edge-compute gateway boards integrated into panels now process smoke-pattern vectors and execute suppression commands locally, meeting latency requirements in data-center hot aisles.

Machine-learning models trained on thousands of real event waveforms reduced the incidence of false alarms and improved early warning in smolder tests. Cloud telemetry enabled service aggregators to benchmark fleets, identifying geographical clusters of nuisance alarms and incorporating that insight into firmware updates. Research into in-panel AI continued to accelerate, and predictive analytics that flag wiring degradation days ahead of failure are forecast to transition from beta pilots to broad release by 2027, introducing a new premium tier within the fire alarm systems industry.

By End-User Industry: Transport Infrastructure Sprints Ahead

The commercial segment remained the largest revenue contributor to the fire alarm systems market, accounting for 48.05% of the market share in 2025. The transportation and infrastructure sectors are projected to grow at a 8.88% CAGR through 2031. Office towers and big-box retail chains have commissioned addressable devices that integrate with access control and HVAC smoke purge systems, meeting tenant demands for integrated safety dashboards.

Transportation hubs and tunnels delivered the steepest growth curve. Projects such as the USD 85.5 million overhaul of Detroit Metropolitan Airport’s roadway tunnels specified multi-criteria detectors with water-mist suppression interfaces. Rail operators across Europe specified linear heat-sensing cables and redundant panel architecture for underground stations, further propelling the fire alarm systems market. Industrial plants upgraded to explosion-proof units in chemical and battery-manufacturing lines, while data-centre developers insisted on high-sensitivity aspirating systems. Each vertical imposed unique performance and certification thresholds, motivating vendors to build broad, configurable portfolios.

Geography Analysis

North America retained leadership in the fire alarm systems market, accounting for 40.02% of 2025 revenue. Adoption remained high because existing stock replaced legacy panels to comply with NFPA 72 cyber provisions and UL nuisance-alarm rules. Service companies widened e-learning programs to close talent gaps, and private-equity backed roll-ups stitched regional contractors into nationwide compliance networks. Municipal incentive funds for school retrofits hinged on voice evacuation and network supervision supported baseline demand.

Asia-Pacific delivered the fastest expansion, clocking a 9.42% CAGR to 2031. Urban infrastructure projects in India, Indonesia, and Vietnam specified addressable systems with seismic-resistant enclosures. Japanese regulators advanced guidelines urging cybersecurity safeguards for connected building subsystems; while not yet codified nationally, the stance spurred early uptake of encrypted panel communications. South Korean research institutes demonstrated AI smoke algorithms that trimmed false dispatches in high-rise kitchens, catalysing local vendor investment in embedded analytics.

Europe posted steady mid-single-digit growth after EN 54 revisions compelled whole-system certification, elevating barriers for low-cost imports. German factories automated compliance logs to satisfy workplace inspectors, expanding sales of panels equipped with digital event-report exports. Meanwhile, mergers accelerated as UK and Nordic service firms dove into cross-border acquisitions, drawn by predictable code-driven maintenance fees. The resulting scale increased bargaining power on component sourcing, curbing inflationary pressure, and safeguarding margin in the region’s portion of the fire alarm systems market.

Competitive Landscape

During 2024 and 2025, the competitive field transitioned from moderately fragmented to consolidating. APi Group’s purchase of Endeavor Fire Protection widened national reach, while Johnson Controls published a hardening guide that set a de facto standard for cyber-secure panel deployments, differentiating its portfolio.[4]AZoSensors, “AI-Powered Fire Detection Drastically Reduces False Alarms,” azosensors.com Honeywell and Siemens adapted by embedding secure bootloaders and TLS-encrypted cloud links into flagship control units.

Technology leadership focused on AI-enabled multisensor detectors and predictive maintenance dashboards. Start-ups licensed false-alarm-reduction algorithms to large OEMs, while edge-analytics specialists partnered with panel makers to host containerized models on board. Vendors also diversified into lithium-ion battery risk mitigation, unveiling gas-detection arrays that sense HF plumes seconds before thermal runaway escalates.

Recurring revenue strategies drove M&A. Inspection, testing, and monitoring contracts generated annuities that appealed to private-equity investors seeking cash-flow stability. The shortage of certified technicians justified digital work-order platforms and AR-based remote assistance, allowing consolidators to leverage scarce expertise across broader footprints. As a result, service bundling tightened customer lock-in and raised switching costs, cementing share positions in the fire alarm systems market.

Fire Alarm Systems Industry Leaders

Honeywell International Inc.

Johnson Controls International plc

Siemens Aktiengesellschaft

Robert Bosch GmbH

Eaton Corporation plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: WAGNER Group announced 12% sales growth on the back of advanced detection exports to Europe.

- February 2025: Korea’s Electronics and Telecommunications Research Institute unveiled an AI detector algorithm that slashes false alarms in clean rooms.

- January 2025: Ramtech rolled out an EN 54-25-compliant wireless evacuation system for heritage retrofits across Europe.

- January 2025: Johnson Controls reported a record USD 31.8 billion backlog with elevated demand for data-center cooling and connected fire panels.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the fire-alarm systems market as the sale value of dedicated detection, control, notification, and power-supply hardware whose primary purpose is to sense fire indicators and audibly or visually alert occupants, maintenance teams, or remote monitoring centers. The scope tracks revenues from new-build and retrofit projects across commercial, industrial, residential, infrastructure, and government facilities, measured at factory gate prices.

Scope exclusion: suppression equipment, standalone security sensors, and software-only monitoring platforms are not included.

Segmentation Overview

- By Component

- Detectors

- Control Panels

- Notification Devices

- Power Supplies

- Accessories

- By System Type

- Conventional Fire Alarm Systems

- Addressable Fire Alarm Systems

- Hybrid Systems

- Wireless Fire Alarm Systems

- Voice Evacuation Systems

- By Technology

- IoT-Enabled Smart Alarms

- AI-Based Analytics and Predictive Detection

- Cloud-Connected Monitoring Platforms

- Edge-Computing Enabled Devices

- By End-User Industry

- Commercial

- Industrial

- Residential

- Government and Institutional

- Transportation and Infrastructure

- Energy and Utilities

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured discussions with regional fire-code inspectors, systems integrators, OEM product managers, and facilities directors across North America, Europe, Asia-Pacific, and the Middle East. These interviews validated retrofit ratios, detector mix shifts, and realistic pricing corridors, filling gaps left by fragmented secondary data and sharpening our assumptions before model finalization.

Desk Research

We built the foundational dataset by screening non-paywalled tier-1 sources such as NFPA and OSHA code updates, Eurostat construction output, United Nations Comtrade shipment lines for HS-8531/8531.20 parts, and building permit dashboards from the US Census and Japan MLIT. Fire-incident statistics from the International Association of Fire & Rescue Services, along with patent analytics from Questel, allowed us to size installed bases and technology migration curves. Company 10-Ks, investor decks, and major trade-show releases rounded out average selling price (ASP) and channel margin trends. The sources cited above are illustrative; several additional public and subscription databases informed granular country splits.

Market-Sizing & Forecasting

A top-down construct, starting with new-floor-space completions, retrofit rates, and detector density mandates, establishes the demand pool, which is then cross-checked through sampled ASP × unit roll-ups from supplier disclosures. Key variables feeding the model include: (1) annual commercial floor-space additions, (2) percentage of smart addressable panel adoption, (3) average detector ASP movements, (4) regulatory compliance deadlines, and (5) insurance-driven retrofit penetration. Multivariate regression with ARIMA error correction projects each driver, while sampled supplier roll-ups flag outliers for adjustment. Where bottom-up estimates are thin, for example in smaller emerging markets, controlled interpolation anchored to regional trade data bridges the gaps.

Data Validation & Update Cycle

Outputs pass variance checks against independent indicators, after which senior reviewers audit formula logic. Reports refresh annually; however, material code revisions or merger events trigger mid-cycle re-runs so clients always receive the most current baseline.

Why Our Fire Alarm Systems Baseline Commands Reliability

Published figures can diverge because firms mix suppression gear, apply different ASP ladders, or freeze models for years. By aligning scope strictly with detection-centric hardware, updating inputs every twelve months, and stress-testing variables with practitioners, Mordor minimizes such drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 34.37 B (2025) | Mordor Intelligence | - |

| USD 34.44 B (2023) | Global Consultancy A | Uses historic exchange rates and omits retrofit discounting |

| USD 43.43 B (2024) | Industry Journal B | Bundles suppression cylinders and service contracts into revenue pool |

| USD 51.63 B (2025) | Regional Consultancy C | Applies list-price ASPs and counts ancillary wiring accessories |

The comparison shows that differences stem mainly from scope creep and pricing assumptions. Because Mordor's model ties each dollar to audited variables and a clearly documented refresh cadence, decision-makers gain a balanced, transparent baseline they can replicate and defend.

Key Questions Answered in the Report

What is the current value of the fire alarm market?

It stood at USD 36.75 billion in 2026 and is forecast to reach USD 51.35 billion by 2031.

Which system type dominates the fire alarm market?

Addressable platforms held 64.12% fire alarm market share in 2025 due to pinpoint incident location and diagnostic features.

Why are data centers buying specialized fire detection?

High-density servers and lithium-ion batteries create unique fire risks, so operators specify aspirating smoke detectors and gas suppression systems compliant with emerging NFPA guidelines.

How are new regulations influencing product design?

NFPA 72 (2025) requires cybersecurity, acoustic leak detection, and thermal imaging, driving manufacturers to incorporate secure processors and advanced sensing modules.

What restrains adoption in emerging economies?

High upfront installation costs and limited pools of certified technicians slow deployment, especially for advanced addressable systems.

Which region is growing the fastest and why?

Asia-Pacific shows the highest CAGR at 9.42%, propelled by urban megaprojects and early moves to embed smart-building technology in new construction.

Page last updated on: