Financial Crime And Fraud Management Solutions Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

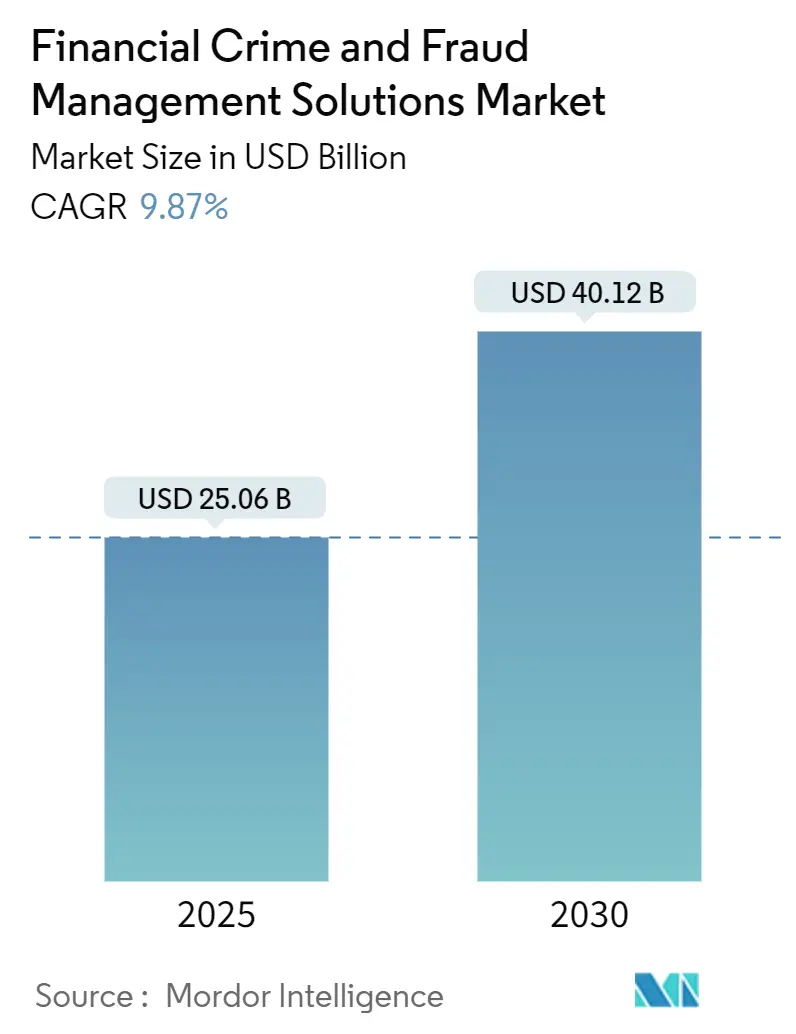

| Market Size (2025) | USD 25.06 Billion |

| Market Size (2030) | USD 40.12 Billion |

| Growth Rate (2025 - 2030) | 9.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Financial Crime And Fraud Management Solutions Market Analysis by Mordor Intelligence

The Financial crime and fraud management solutions market size stands at USD 25.06 billion in 2025 and is forecast to reach USD 40.12 billion by 2030, exhibiting a 9.87% CAGR through the period. Digital payments are scaling at record speed, instant‐settlement rails are irrecoverable once posted, and institutions are under mounting pressure to replace batch screening with real-time analytics. Regulatory reforms such as the EU’s 6AMLD and the United States’ Section 314(b) expansion are pushing banks toward unified compliance engines. Cloud delivery lowers up-front costs and accelerates access to AI toolkits, while behavioral biometrics and consortium data sharing curb false positives far more effectively than static rules. M&A activity is accelerating as incumbents acquire AI-native specialists to fill technology gaps and secure larger data networks.

Key Report Takeaways

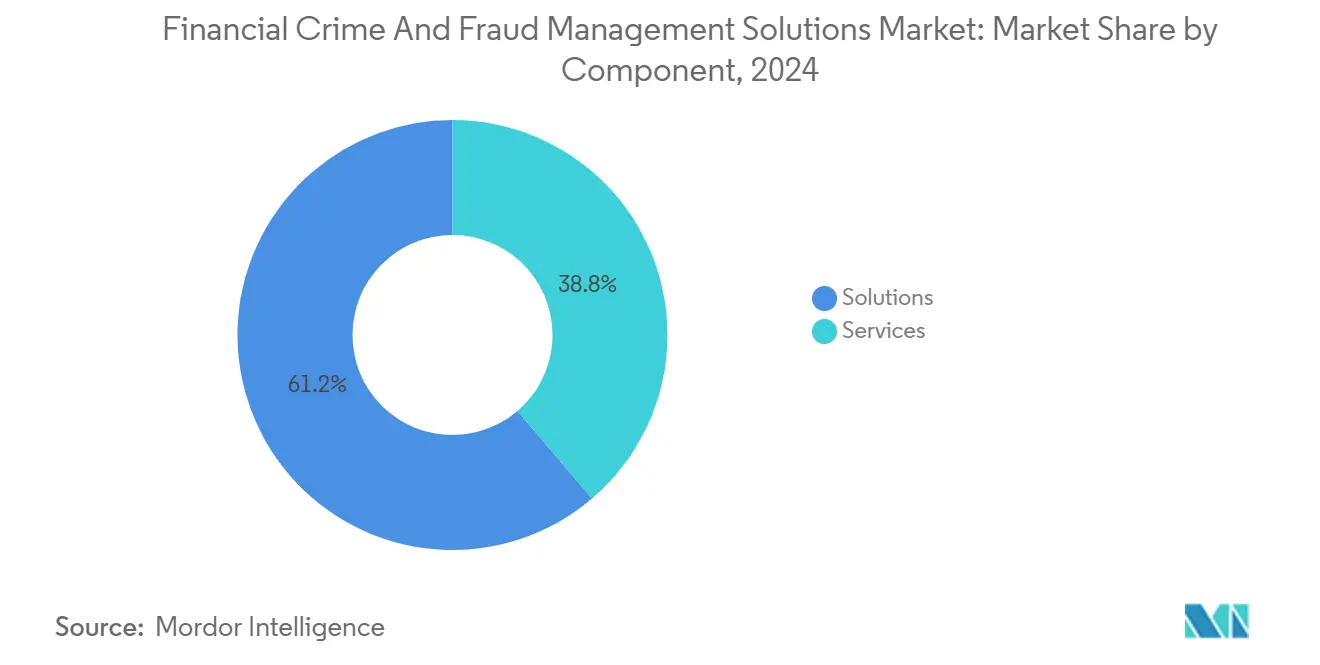

- By component, solutions commanded 61.24% of the Financial crime and fraud management solutions market share in 2024; services are projected to expand at an 11.23% CAGR to 2030.

- By deployment mode, on-premises held 56.57% of the Financial crime and fraud management solutions market size in 2024, while cloud is advancing at an 11.46% CAGR through 2030.

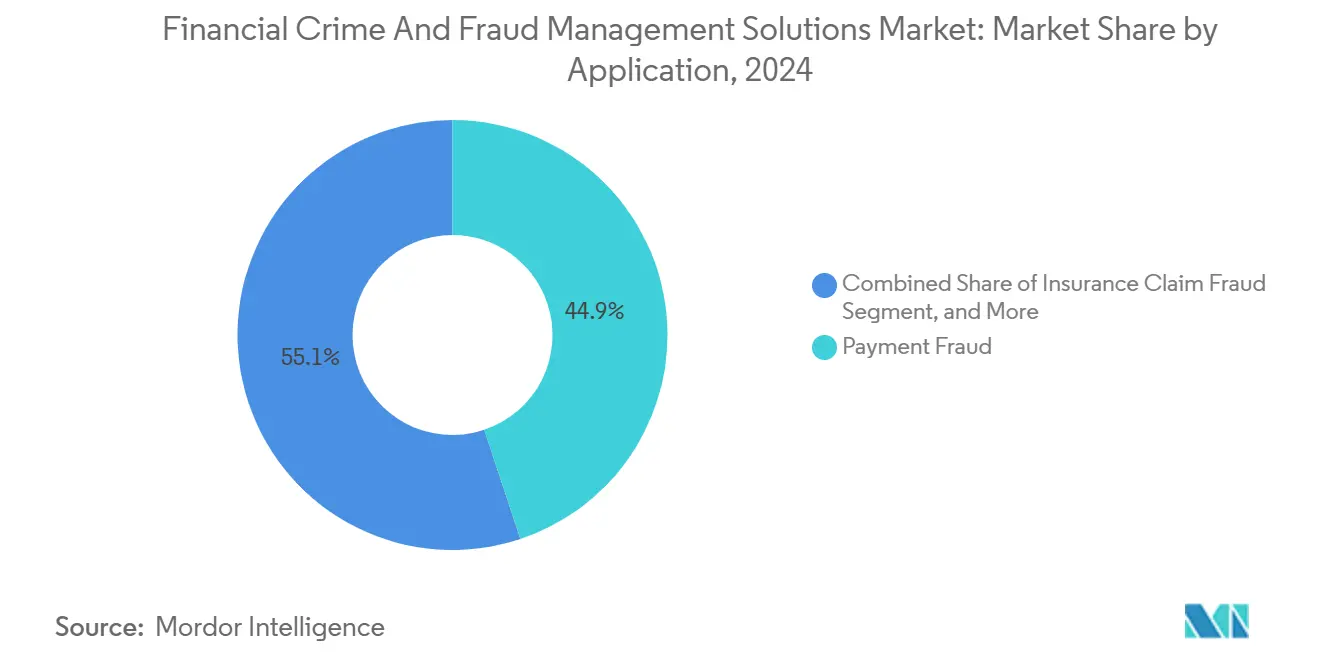

- By application, payment fraud accounted for a 44.87% share of the Financial crime and fraud management solutions market size in 2024, and identity theft and account takeover are rising at a 9.98% CAGR through 2030.

- By end-user, BFSI led with 36.34% revenue share in 2024; FinTech and payment processors record the highest projected 10.13% CAGR to 2030.

- By geography, North America captured 34.79% of the Financial crime and fraud management solutions market share in 2024, whereas Asia-Pacific is set to grow at a 10.31% CAGR over the forecast horizon.

Global Financial Crime And Fraud Management Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing digital payment volumes | +2.1% | Asia-Pacific, North America | Medium term (2-4 years) |

| Increasing regulatory stringency (AML/KYC) | +1.8% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Adoption of AI/ML-based real-time analytics | +2.3% | North America, Europe | Short term (≤ 2 years) |

| Growth of embedded finance ecosystems | +1.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Convergence of fraud, AML and cyber-security stacks | +1.2% | Developed markets | Long term (≥ 4 years) |

| Rise of Banking-as-a-Service | +1.0% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Digital Payment Volumes

Instant-payment transactions in the United States are on track to hit 7.4 billion in 2025, a 43.4% CAGR that outstrips card growth.[1]Nasdaq Verafin, “The Evolution of Instant Payments Infographic,” verafin.com The irrevocable nature of real-time rails compresses decision windows from minutes to milliseconds, exposing the Financial crime and fraud management solutions market to urgent demand for streaming analytics. Authorized push-payment fraud surged 27% between 2022 and 2024 as criminals exploited speed advantages. ISO 20022 messages add richer context that improves model accuracy, yet require scalable data pipelines.

Increasing Regulatory Stringency (AML/KYC)

Europe’s 6AMLD lifted compliance workloads by 15-20%, driving automation of sanctions screening and customer due diligence.[2]LexisNexis Risk Solutions, “Top Financial Crime Compliance Trends in 2025,” lexisnexis.com U.S. regulators expanded Section 314(b) to cover additional payment types, widening the scope of information sharing obligations. Asian regulators are tightening KYC for digital wallets, compelling banks to deploy unified risk platforms capable of handling instant and batch flows without latency penalties.

Adoption of AI/ML-Based Real-Time Analytics

Generative AI agents launched by NICE Actimize in 2025 cut investigation times while lowering false positives below 5%.[3]NICE Actimize, “Xceed AI Agents Press Release,” niceactimize.com BioCatch’s Trust Network shares behavioral signals across multiple banks and achieves 80% accuracy on previously unseen scam patterns. Consortium intelligence from 650 million counterparties enables institutions to flag mule accounts in milliseconds.

Growth of Embedded Finance Ecosystems

Embedded finance handled USD 2.6 trillion in 2024 transactions, turning fraud prevention into a decisive buying criterion for Banking-as-a-Service partners. Alloy and Unit21 integrate risk scoring directly into BaaS workflows, providing real-time monitoring across multiple brands on a single ledger. TransPecos Banks cut fraud-ops expenditures by 40% after deploying specialist tools optimized for distributed journeys.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High false-positive costs and alert fatigue | -1.4% | North America, Europe | Short term (≤ 2 years) |

| Talent shortage in fraud analytics | -0.9% | Global | Medium term (2-4 years) |

| Privacy-by-design and data-sovereignty barriers | -0.7% | Europe | Long term (≥ 4 years) |

| Sophistication of cross-channel mule networks | -0.8% | Developed payment markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High False-Positive Costs and Alert Fatigue

Legacy rule engines trigger false positives on more than 95% of alerts, costing between USD 50 and USD 200 per case and overwhelming investigators. Customer friction from unnecessary holds drives attrition rates up to 15%. Cloud-native AI models that ingest behavioral and consortium data have pushed false positives below 10%, releasing capacity for genuine threat hunting.

Talent Shortage in Fraud Analytics

The global shortfall of 4 million cybersecurity specialists is acute in fraud analytics, where cross-disciplinary skills in data science and compliance are uncommon. Banks in major hubs report six-month hiring cycles and 20-30% pay premiums for senior analysts. Institutions counter the gap through managed detection services and academic partnerships, yet near-term capacity constraints remain a drag on Financial crime and fraud management solutions market adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solution Suites Underpin Adoption

Solutions generated the bulk of demand, capturing 61.24% of the Financial crime and fraud management solutions market size in 2024. Unified platforms that blend transaction monitoring, behavioral biometrics, and case management appeal to buyers seeking tight data correlation. Vendors are packaging fraud, AML, and sanctions screening into single stacks to simplify integration.

Services represent the agility layer. Managed detection and response is growing at 11.23% CAGR as banks outsource alert triage to round-the-clock specialist teams. Consulting engagements focus on tuning AI models to local regulations, ensuring that Financial crime and fraud management solutions market deployments meet audit expectations without escalating false positives.

By Deployment Mode: Cloud Gains Critical Mass

On-premises installations still accounted for 56.57% of the Financial crime and fraud management solutions market size in 2024, reflecting legacy infrastructure and data-residency rules. However, cloud deployments are scaling at an 11.46% CAGR as regulators offer clearer guidance on outsourcing and as models that require GPU acceleration become cost-prohibitive on-site.

Hybrid architectures balance latency and sovereignty. Sensitive identity graphs remain in private data centers while anomaly scoring runs on public cloud clusters. This middle ground supports the Financial crime and fraud management solutions market shift toward real-time analytics without wholesale system rip-and-replace.

By Application: Payment Fraud Still Leads, but Identity Threats Surge

Payment fraud held a 44.87% share in 2024 as criminals pivoted to instant rails, where chargeback protections are absent. Real-time behavioral analytics and device intelligence are, therefore, core purchase criteria.

Identity theft and account takeover are growing fastest at a 9.98% CAGR, fueled by synthetic IDs and credential stuffing spikes. Vendors are layering behavioral biometrics and federated identity signals to recognize anomalies even when static data is compromised, boosting uptake across the Financial crime and fraud management solutions market.

By End-user Industry: FinTech Outpaces Traditional Banking

BFSI remained the anchor customer set, representing 36.34% of 2024 revenue. Banks integrate fraud, AML, and cyber telemetry to reduce overhead from siloed programs.

FinTech and payment processors, however, are expanding at a 10.13% CAGR as their transaction counts multiply. These agile firms demand API-first offerings that embed compliance directly into checkout flows, widening the total addressable scope for the Financial crime and fraud management solutions market well beyond incumbent banking cohorts.

Geography Analysis

North America contributed the largest slice at 34.79% in 2024 on the back of robust information-sharing frameworks, early ISO 20022 migration, and high-velocity instant-payment adoption. Regulatory pilots that promote data collaboration between banks and fintechs further enlarge the Financial crime and fraud management solutions market in the region.

Asia-Pacific is the fastest climber with 10.31% CAGR, propelled by financial-inclusion agendas and rampant smartphone penetration. Countries such as India are codifying stricter KYC for digital wallets, compelling providers to embed risk scoring at onboarding rather than after suspicious activity surfaces.

Europe maintains strong momentum. GDPR and 6AMLD heighten the need for privacy-by-design solutions that localize data while still supporting cross-border sanctions obligations. Local cloud zones and confidential computing are therefore central to European procurement decisions within the Financial crime and fraud management solutions market.

Competitive Landscape

The sector exhibits moderate concentration. NICE Actimize, FICO, and LexisNexis Risk Solutions retain scale advantages through broad product suites and deep regulatory content. Visa’s USD 1.1 billion purchase of Featurespace and Permira’s acquisition of BioCatch underscore investor appetite for AI-centric engines. Vendors increasingly differentiate on network effects: the wider the consortium data, the higher the detection lift. BioCatch’s launch of a behavior-sharing trust network with Australian banks exemplifies this flywheel.

Disruptors such as Riskified and Sift laser focus on eCommerce abuse and digital-platform fraud. In parallel, Fiserv’s FIUSD stablecoin introduces on-chain fraud controls, signaling converging payments and Web3 security. Success factors, therefore, hinge on cloud-native design, explainable AI, and the depth of intelligence partnerships.

Incumbents respond with accelerated R&D. NICE Actimize channeled USD 50 million into generative AI agents that summarize unstructured evidence for analysts. Mastercard joined forces with Feedzai to apply network-level signals to scam interdiction. These maneuvers illustrate how rapidly the Financial crime and fraud management solutions market is moving toward real-time, consortium-based defense models.

Financial Crime And Fraud Management Solutions Industry Leaders

NICE Ltd. (NICE Actimize)

Fair Isaac Corporation (FICO)

RELX PLC – LexisNexis Risk Solutions

ACI Worldwide Inc.

SAS Institute Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: NICE Actimize released its 2025 Fraud Insights Report, confirming scams as the top attempted fraud method.

- June 2025: Fiserv launched FIUSD, a bank-friendly stablecoin with embedded fraud controls.

- June 2025: Mastercard expanded its partnership with Fiserv to roll out FIUSD across its network.

- May 2025: BioCatch launched the BioCatch Trust Network with five Australian banks.

Global Financial Crime And Fraud Management Solutions Market Report Scope

| Solutions |

| Services |

| On-premises |

| Cloud |

| Payment Fraud |

| Identity Theft and Account Take-over |

| Insurance Claim Fraud |

| Money Laundering and Terrorist Financing |

| Internal/Employee Fraud |

| Banking, Financial Services and Insurance (BFSI) |

| FinTech and Payment Processors |

| eCommerce and Retail |

| Healthcare |

| Government and Public Sector |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Solutions | ||

| Services | |||

| By Deployment Mode | On-premises | ||

| Cloud | |||

| By Application | Payment Fraud | ||

| Identity Theft and Account Take-over | |||

| Insurance Claim Fraud | |||

| Money Laundering and Terrorist Financing | |||

| Internal/Employee Fraud | |||

| By End-user Industry | Banking, Financial Services and Insurance (BFSI) | ||

| FinTech and Payment Processors | |||

| eCommerce and Retail | |||

| Healthcare | |||

| Government and Public Sector | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the Financial crime and fraud management solutions market in 2025?

It is valued at USD 25.06 billion and is projected to expand at a 9.87% CAGR to USD 40.12 billion by 2030.

Which region grows fastest for fraud management platforms?

Asia-Pacific leads with a 10.31% CAGR thanks to rapid digital payment adoption and evolving KYC rules.

What segment shows the highest market share today?

Solutions account for 61.24% of revenue as institutions favor integrated detection suites.

Why are false positives a major restraint?

Legacy rule engines flag more than 95% benign alerts, driving up investigation costs and customer attrition.

How is AI improving fraud detection accuracy?

Generative and machine-learning models cut false positives below 10% by combining behavioral biometrics with consortium intelligence.

Page last updated on: