Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

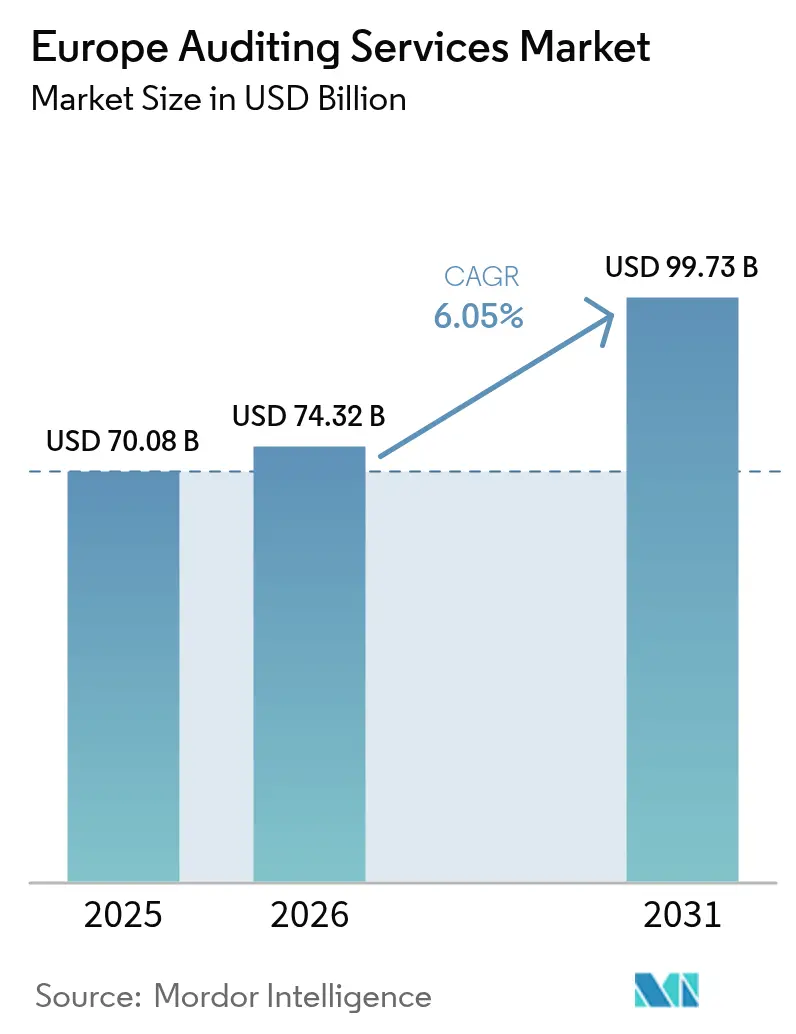

| Base Year Market Size (2025) | USD 70.08 Billion |

| Market Size (2026) | USD 74.32 Billion |

| Market Size (2031) | USD 99.73 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Auditing Services Market Analysis by Mordor Intelligence

Europe auditing services market size in 2026 is estimated at USD 74.32 billion, growing from 2025 value of USD 70.08 billion with 2031 projections showing USD 99.73 billion, growing at 6.05% CAGR over 2026-2031. Mandatory rotation rules, real-time assurance adoption, and ESG-linked assurance mandates are the strongest drivers shaping the European auditing services market. Accelerating automation of compliance tasks frees auditors to focus on judgment-based procedures, while AI-enabled anomaly detection expands population testing and improves fraud detection accuracy. Digital-first small and mid-sized businesses are surpassing statutory audit thresholds, further enlarging the European auditing services market as these companies require their first external audit engagements. Simultaneously, information-system audit demand is rising because regulators now view cyber resilience as an intrinsic aspect of financial reporting integrity. The European auditing services market is also benefiting from the Corporate Sustainability Reporting Directive, which opens entirely new assurance revenue streams related to carbon accounting and social-impact metrics. Overall, firms that fuse proprietary analytics with human expertise are positioned to capture outsized gains, even as talent scarcity and liability inflation temper headline growth.

Key Report Takeaways

- By type, external audit services retained 71.92% of Europe auditing services market share in 2025, while internal audit outsourcing is expanding at an 7.78% CAGR through 2031.

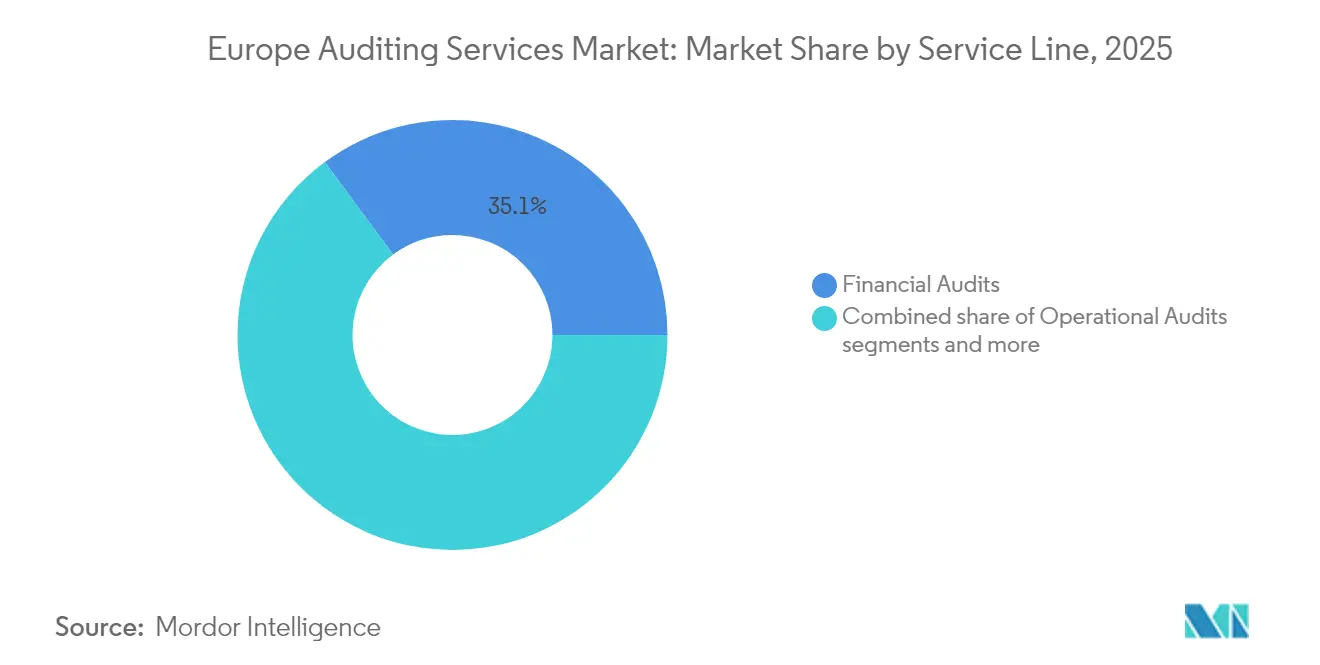

- By service line, financial audits accounted for 35.12% of the Europe auditing services market size in 2025, and information-system audits are forecast to grow at a 13.08% CAGR to 2031.

- By end-user, banking, Financial Services, and Insurance segment held 30.78% of the Europe auditing services market size in 2025; IT & Telecom is projected to increase at a 12.35% CAGR through 2031.

- By geography, the United Kingdom commanded 29.12% Europe auditing services market share in 2025, while the BENELUX region is advancing at an 7.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Auditing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to continuous auditing & real-time assurance solutions | +1.2% | Global, strongest in UK & Germany | Medium term (2-4 years) |

| Mandatory rotation & tendering rules amplify audit churn | +1.8% | Europe-wide, particularly strong in EU core | Long term (≥ 4 years) |

| Digital-first SMBs entering statutory-audit bracket | +0.9% | Global, with early gains in BENELUX, NORDICS | Short term (≤ 2 years) |

| EU Green Deal driving ESG-linked audit demand | +1.4% | Europe-wide, spill-over to UK | Medium term (2-4 years) |

| Cloud-native ERP penetration enables remote audit delivery | +0.8% | Global | Short term (≤ 2 years) |

| AI-powered anomaly detection raises audit scope | +1.1% | Global, strongest in Switzerland, UK | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift to Continuous Auditing & Real-Time Assurance Solutions

Continuous monitoring platforms allow 100% transaction testing instead of sampling, sharply enhancing fraud-risk coverage across the European auditing services market[1]Grant Thornton, “AI in Audit: European Deployment Report,” Grant Thornton Global, grantthornton.global. . Mid-tier networks that deploy standardized analytics quickly gain credibility among mid-market issuers. Big Four firms are revamping legacy systems, yet partner consensus requirements slow enterprise-wide rollouts, creating competitive white space. Real-time dashboards enable boards to identify control breaches within hours rather than weeks, which strengthens governance effectiveness. Audit fees increasingly incorporate subscription pricing tied to data-stream connections instead of hourly billing. The transition also requires reskilling auditors to interpret algorithmic alerts and to evaluate AI model governance. As a result, technology fluency becomes a core competency across the European auditing services industry.

Mandatory Rotation & Tendering Rules Amplify Audit Churn

Statutory rotation mandates generate predictable retender cycles that inject an estimated EUR 2.3 billion in contestable fees into the European auditing services market[2]Financial Reporting Council, “Audit Quality Review,” FRC, frc.org.uk. . Mid-tier networks with sector specialism and competitive rates capitalize on these openings to penetrate large-cap rosters. However, winning new mandates demands upfront investment in bid teams and onboarding capacity, which strains cash flows when talent costs are rising. Incumbents defend positions by bundling multidisciplinary services and highlighting institutional knowledge accumulated over prior audit cycles. Regulators closely monitor fee negotiations to ensure auditor independence, sometimes disallowing ancillary consulting, which reshapes revenue mixes. Rotation also prompts companies to reassess internal control maturity, indirectly lifting demand for pre-transition readiness reviews. Overall, enforced churn diversifies the European auditing services market yet raises compliance complexity for issuers.

Digital-First SMBs Entering Statutory-Audit Bracket

E-commerce and SaaS scale-ups in the NORDICS and BENELUX are surpassing revenue or headcount thresholds that trigger statutory audit, broadening the European auditing services market [3]Nordic Innovation, “Technology Sector Audit Requirements,” Nordic Innovation, nordicinnovation.org. . Founders favor cloud-native audit portals that integrate directly with ERP data lakes, reducing PBC (prepared-by-client) friction. Audit engagement letters increasingly bundle tax compliance and cyber-risk diagnostics as startups seek one-stop governance solutions. Mid-tier auditors gain an advantage by offering agile workflows, while larger firms compete through brand credibility when companies prepare for IPOs. The influx of first-time audit clients increases the volume of smaller engagements, prompting firms to automate low-complexity tasks for cost efficiency. Over time, scaling SMBs evolve into mid-cap clients, creating lifetime value potential across the European auditing services market. This driver, therefore, supports sustainable revenue expansion beyond macroeconomic cycles.

EU Green Deal Driving ESG-Linked Audit Demand

The Corporate Sustainability Reporting Directive requires limited assurance in 2025, escalating to reasonable assurance by 2028, which injects new service lines into the European auditing services market[4]PwC, “ESG Assurance Services in Europe,” PwC, pwc.com.. Auditors must validate carbon footprints, supply-chain labor practices, and biodiversity impacts, calling for multidisciplinary teams that blend accountants, engineers, and environmental scientists. Big Four firms have built dedicated ESG hubs across 15 European countries, signaling significant investment. Mid-tier networks partner with niche consultancies to fill capability gaps, accelerating M&A activity. Pricing models remain nascent because market participants debate engagement scoping and liability caps for non-financial misstatements. Early-mover issuers that voluntarily seek assurance gain investor trust, setting peer pressure across industries. Over the next decade, ESG validation could rival financial audit revenues within the European auditing services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Auditor talent crunch and escalating wage inflation | -1.5% | Europe-wide, particularly acute in UK & Germany | Short term (≤ 2 years) |

| Rising liability caps & litigation risk | -0.8% | Europe-wide, with spillover effects from US litigation | Medium term (2-4 years) |

| Blockchain-enabled self-assurance threatens fee pools | -0.3% | Global, early adoption in financial services | Long term (≥ 4 years) |

| SME cost-sensitivity limits advisory cross-sell | -0.6% | Europe-wide, particularly in Southern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Auditor Talent Crunch and Escalating Wage Inflation

Qualified auditor supply lags demand by double-digit percentages, pushing senior-staff wages up 23% in 2024 and squeezing engagement margins across the European auditing services market. Firms respond with hybrid work models and accelerated promotion pathways, yet these perks sometimes dilute mentoring rigor. Scarcity is most acute in IT audit and ESG assurance, where interdisciplinary expertise is required. Recruitment of overseas professionals faces immigration friction, especially post-Brexit, compounding shortages in the United Kingdom. High attrition also erodes institutional memory, raising the cost of maintaining audit quality controls. Automation offsets some resource gaps, but clients remain cautious when junior teams run critical procedures. Unless training pipelines expand, talent deficits could slow delivery timelines and jeopardize fee recovery across the European auditing services industry.

Rising Liability Caps & Litigation Risk

Professional indemnity premiums have climbed 18% annually since 2024 amid headline audit failures, lifting fixed-cost structures within the European auditing services market. Legislative debates on joint-and-several liability intensify risk perception among insurers, who expand exclusions for technology-related errors. Smaller networks face disproportionate pricing, making it tougher to bid for large-cap audits that require EUR 100 million coverage. Some firms create captive insurance vehicles, but regulators scrutinize self-insurance for solvency adequacy. Higher deductible layers encourage extensive use of forensic tools to pre-empt claims, raising audit execution costs. Meanwhile, clients negotiate clawback clauses that transfer part of litigation exposure back to firms. Unless liability reforms offer balanced protections, expanding risk premiums could curb competitive entry and reinforce concentration in the European auditing services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: External Audit Dominance Amid Internal Growth

External audit engagements generated 71.92% of 2025 revenue, confirming statutory compliance as the anchor of the European auditing services market. Mandatory filing deadlines and investor pressure ensure relatively inelastic demand, which supports predictable cash flows for audit networks. Nonetheless, internal audit outsourcing is accelerating at an 7.78% CAGR, reflecting board-level appetite for independent assessments of operational controls without staff overhead. Mid-tier firms leverage sector-specific teams to win managed-service contracts from mid-market enterprises that seek scalability. Simultaneously, Big Four incumbents spin out dedicated internal audit units to avoid independence conflicts with external audit clients while capturing incremental wallet share. Technology deployment, such as continuous control monitoring, allows providers to run lean resource models that improve profitability. Consequently, internal audit gains prominence within the European auditing services market as governance expectations widen beyond financial reporting. This convergence also creates cross-referral pathways, as external auditors recommend internal audit enhancements to improve overall assurance ecosystems.

Internal audit growth alters pricing architecture, shifting from time-and-materials to subscription models tied to the number of control tests or business processes covered. Firms that package risk analytics dashboards with quarterly committee briefings secure multi-year contracts that stabilize utilization rates. Meanwhile, external audit fee pressure rises because tender processes emphasize cost competitiveness amid rotation rules. Pairing both services grants providers negotiation leverage, allowing cross-subsidization strategies. Regulators, however, enforce independence safeguards that limit simultaneous provision to the same client, which nudges the Europe auditing services market toward clearer internal-external delineation. Over the forecast horizon, hybrid sourcing models, where companies keep strategic internal audit planning in-house but outsource execution, are likely to expand. This blend maximizes governance depth while containing payroll costs, underlining the complementary growth trajectories of both audit types.

By Service Line: Financial Audits Lead While Tech Audits Surge

Financial audits delivered 35.12% of the total 2025 revenues and remain the reputational foundation of the European auditing services market. They enable cross-selling into advisory, tax, and transaction services, reinforcing client stickiness. However, information-system audits are projected to advance at a 13.08% CAGR, outpacing all other service lines as cyber-risk monitoring becomes integral to financial reliability. Regulators emphasize IT general controls and data-integrity validations, compelling auditors to integrate security engineers into field teams. Big Four firms deploy proprietary code-review tools that scan ERP customization layers, while mid-tier networks partner with cybersecurity boutiques for niche expertise. The escalating reliance on cloud architectures extends audit scope to third-party service organizations, increasing engagement complexity.

Compliance audits and operational audits continue to address sector-specific regulations, such as Solvency II in insurance and GMP in pharmaceuticals. Investigation audits, though smaller in volume, command premium fees during fraud crises, boosting margins. Strategy consultancies pressure advisory lines but remain valuable when bundled with assurance mandates. Over time, service-line convergence is expected, as clients request integrated audit opinions covering financial statements, IT controls, and ESG metrics within a single engagement. Such integration necessitates multidomain frameworks, pushing firms to invest in unified data platforms to handle heterogeneous evidence sets. The service-mix evolution thus redefines capability priorities throughout the European auditing services market.

By End-User Industry: BFSI Leads While Tech Accelerates

The Banking, Financial Services, and Insurance sector generated 30.78% of audit demand in 2025 because prudential oversight requires extensive assurance on credit risk models and capital adequacy. Complex financial instruments further heighten reliance on valuation specialists, sustaining fee density. Yet IT & Telecom audit expenditure is forecast to climb at a 12.35% CAGR as digital platforms, 5G rollouts, and artificial intelligence systems invite heightened regulatory scrutiny over data privacy and algorithmic fairness. Audit firms must now validate software life-cycles, data-governance frameworks, and ethical-AI controls alongside traditional financial reconciliations. This trend broadens talent requirements within the European auditing services market, blending technologists with CPAs.

Manufacturing entities contribute steady revenue via supply-chain transparency and carbon-footprint verification. Energy & Utilities engagements rise as renewable integration and carbon trading proliferate, demanding audits of power-purchase agreements and emissions registries. Government & Public Sector audits remain sizable but constrained by public-budget cycles, while Healthcare & Life Sciences audits expand modestly amidst clinical-trial digitization. Cross-industry divergence in growth rates compels firms to pursue industry-centric go-to-market strategies rather than monolithic service models. Consequently, resource allocation aligns with sectors undergoing the fastest transformation, reinforcing the structural shift toward technology-intensive engagements across the Europe auditing services market.

Geography Analysis

United Kingdom maintains 29.12% market share in 2025 despite Brexit-related regulatory divergence, benefiting from London's financial center status, complex corporate structures, and sophisticated audit requirements that command premium fees, while BENELUX emerges as the fastest-growing region at 7.74% CAGR driven by regulatory harmonization and cross-border M&A activity. Germany represents the second-largest market with strong industrial audit demand, complex corporate governance requirements, and substantial mid-market audit opportunities that benefit both Big Four and mid-tier firms. France demonstrates steady growth through corporate governance reforms and ESG reporting requirements that create additional audit scope and advisory opportunities.

The BENELUX region's exceptional growth reflects economic integration benefits, with Netherlands serving as a European headquarters location for multinational corporations requiring sophisticated audit services, while Belgium's position as an EU administrative center creates demand for regulatory compliance and government audit services. NORDICS shows solid growth driven by sustainability leadership, technology adoption, and transparent governance practices that create demand for ESG assurance and technology audit services. Spain and Italy represent substantial markets with growth opportunities in mid-market audit services and regulatory compliance verification, while Rest of Europe captures emerging markets in Central and Eastern Europe where economic development drives increasing audit requirements and regulatory sophistication.

NORDIC markets exhibit 7.12% CAGR growth through 2031, catalyzed by technology entrepreneurship and leadership in climate transparency. Sweden and Denmark drive renewable-energy audit demand, while Finland’s gaming industry necessitates IP-valuation expertise. Spain and Italy offer emerging upside linked to EU recovery-fund projects that mandate stringent audit oversight. However, economic volatility and complex labor regulations temper near-term momentum. Rest-of-Europe territories, including Central and Eastern European economies, deliver moderate growth but serve as cost-efficient delivery centers for large networks. Overall, capturing geographic growth within the Europe auditing services market requires balancing local regulatory fluency with pan-European delivery infrastructure.

Competitive Landscape

The European auditing services market is highly concentrated, with the Big Four firms dominating the vast majority of audit revenues, indicating a near-monopolistic structure. PwC maintains a leadership position, followed closely by Deloitte, EY, and KPMG. However, competition among these giants is increasingly shaped by capability differentiation rather than a focus on retaining market share. Major investments in AI-driven analytics, ESG capabilities, and blockchain-secured audit documentation reflect this shift. Notable moves include PwC’s launch of a Europe-wide ESG Center of Excellence and Deloitte’s expansion of its proprietary Cortex platform, enabling advanced journal-entry testing.

Mid-tier audit networks, while much smaller in overall market share, are successfully targeting niche areas to win new mandates. Firms like BDO and Grant Thornton appeal to specialized client groups through focused strategies in family-owned enterprises and private equity, respectively. The merger of Mazars and FORVIS has created a larger player capable of challenging the dominance of the Big Four. Baker Tilly’s recent acquisitions in France and Spain highlight a broader trend of consolidation to build scale and fund tech upgrades. Regulatory emphasis on audit quality over firm size has allowed these challengers to compete on effectiveness, subtly diversifying the competitive landscape.

Future competitiveness in the sector is increasingly tied to strategic partnerships and talent innovation. Alliances with cloud providers, cybersecurity experts, and ESG consultants are shaping next-generation audit offerings. Deloitte’s collaboration with Google Cloud supports advanced AI-powered risk tools, while RSM’s work with Microsoft focuses on audit solutions for small and mid-sized businesses. Firms are also intensifying recruitment efforts, offering benefits like tuition-free master’s programs in data science to attract top talent. Growing litigation risks are prompting joint legal defense arrangements, showing that technology, specialization, and talent development are now more critical than sheer market size.

Europe Auditing Services Industry Leaders

PwC

Deloitte

EY

KPMG

BDO

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Auditstage, a Brussels-based AuditTech startup, raised EUR 750,000 (USD 880,350) in pre-seed funding led by Smartfin to develop AI-powered audit collaboration platforms featuring automated confirmations and data preparation capabilities, signaling venture capital interest in audit technology innovation.

- March 2025: KPMG announced the consolidation of its European national partnerships into larger regional entities to streamline governance, strengthen cross-border service delivery, and improve audit quality consistency across jurisdictions, representing a significant organizational restructuring initiative.

- January 2025: Baker Tilly International reported record global revenues of USD 5.62 billion for 2024, with EMEA representing the fastest-growing region at 13% growth, driven by expansion in Belgium, France, Germany, Italy, the Netherlands, Poland, Spain, and the UK markets.

- December 2024: KPMG Belgium published guidance on generative AI implementation for internal audit teams, featuring prompt engineering techniques and Retrieval-Augmented Generation technology to enhance audit efficiency and knowledge management capabilities.

Europe Auditing Services Market Report Scope

Auditing services examine and evaluate an organization's financial records and transactions, ensuring accuracy and compliance with relevant laws and regulations. Audits are typically conducted by independent, qualified professionals known as auditors. The European auditing services market is segmented by type, service line, and country. By type, the market is segmented into internal audit and external audit. The market is segmented by service line into operational audits, financial audits, advisory and consulting, investigation audits, information system audits, compliance audits, and other service lines (information technology (IT) audits, etc). The market is segmented by country: the United Kingdom and Ireland, Germany, France, Italy, Netherlands, Spain, and the Rest of Europe). The report offers market size and forecasts for the Europe auditing services market in value (USD) for all the above segments.

By Type

| Internal Audit |

| External Audit |

By Service Line

| Operational Audits |

| Financial Audits |

| Compliance Audits |

| Other Service Lines (Investigation Audit, Information System Audit, etc) |

By End-User Industry

| BFSI |

| Manufacturing |

| Government & Public Sector |

| Healthcare & Life Sciences |

| IT & Telecom |

| Energy & Utilities |

| Other Industries |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Type | Internal Audit |

| External Audit | |

| By Service Line | Operational Audits |

| Financial Audits | |

| Compliance Audits | |

| Other Service Lines (Investigation Audit, Information System Audit, etc) | |

| By End-User Industry | BFSI |

| Manufacturing | |

| Government & Public Sector | |

| Healthcare & Life Sciences | |

| IT & Telecom | |

| Energy & Utilities | |

| Other Industries | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

How fast is the Europe auditing services market expected to grow through 2031?

It is projected to expand at a 6.05% CAGR, moving from USD 74.32 billion in 2026 to USD 99.73 billion by 2031.

Which service line is growing quickest in European audit engagements?

Information-system audits are forecast to rise at a 13.08% CAGR because cyber resilience is now integral to financial-reporting integrity.

What segment holds the largest Europe auditing services market share today?

External audit services command 71.92% of revenues owing to statutory compliance demands.

Which end-user vertical is set to post the highest audit-spend growth?

IT & Telecom audit demand is expected to climb at a 12.35% CAGR as regulators tighten oversight of platform companies.

Who are the dominant players in European audit services?

PwC, Deloitte, EY, and KPMG collectively hold 97% of audit revenues, reflecting extreme market concentration.

Why is ESG assurance significant for audit firms?

The Corporate Sustainability Reporting Directive mandates limited assurance from 2025 and reasonable assurance by 2028, creating new revenue streams for firms with sustainability expertise.

Page last updated on: