High-temperature Insulation Materials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

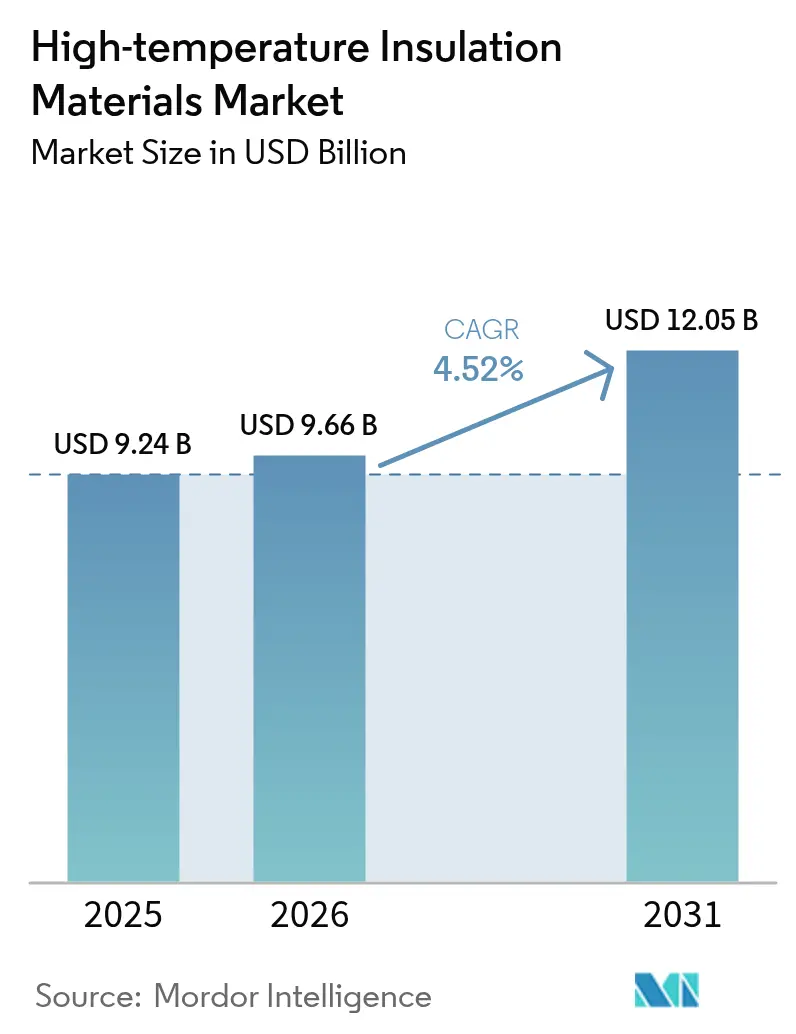

| Market Size (2026) | USD 9.66 Billion |

| Market Size (2031) | USD 12.05 Billion |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High-temperature Insulation Materials Market Analysis by Mordor Intelligence

The High-temperature Insulation Materials Market size is expected to grow from USD 9.24 billion in 2025 to USD 9.66 billion in 2026 and is forecast to reach USD 12.05 billion by 2031 at 4.52% CAGR over 2026-2031. The current market size reflects steady demand growth as energy-intensive industries pursue operational efficiency and lower emissions. Tight building-energy codes, rapid petrochemical and metals capacity additions in Asia-Pacific, and expanding green hydrogen electrolyser installations form the backbone of demand. Manufacturers continue to prioritize non-combustible and low-biopersistent alternatives that satisfy stricter occupational exposure limits. At the same time, vertical integration strategies and regional capacity expansions are helping large suppliers shield themselves from raw-material price swings and logistics bottlenecks. While alumina, silica, and zirconia pricing remains volatile, the economic payback from lower fuel use and maintenance costs keeps adoption on an upward trajectory.

Key Report Takeaways

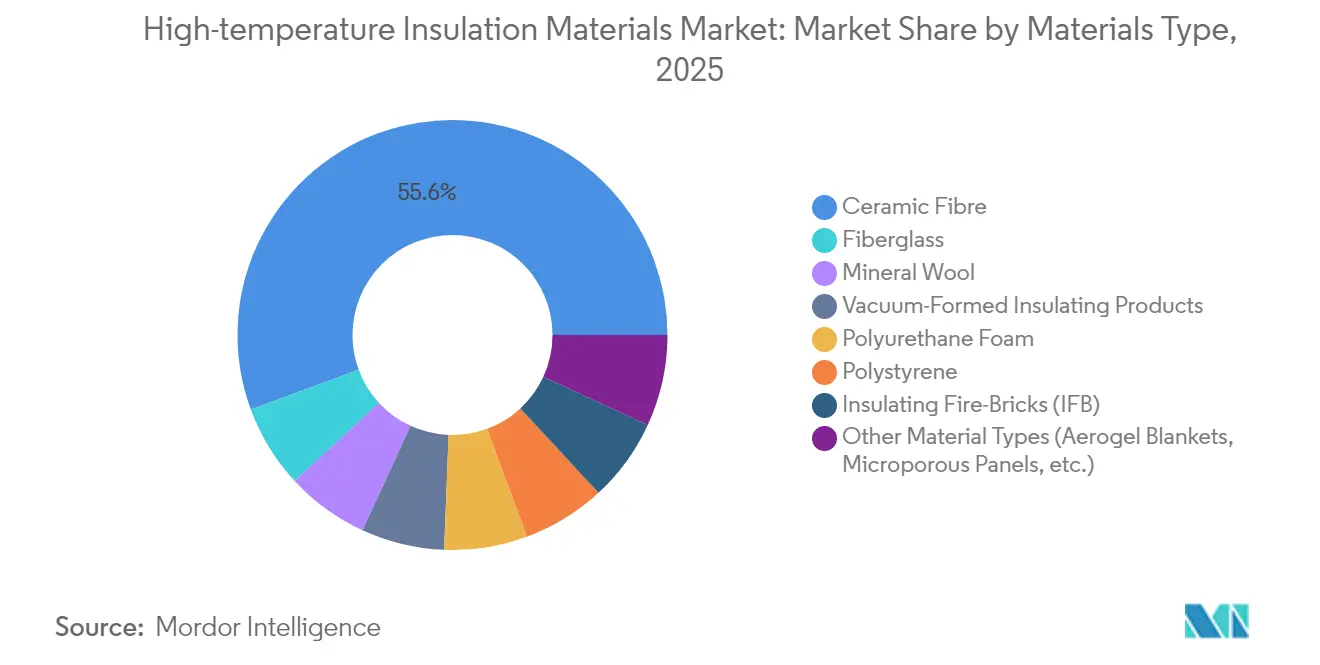

- By material type, ceramic fibre led with 55.63% of high-temperature insulation materials market share in 2025; other material types, including aerogel blankets and microporous panels, are projected to advance at 6.01% CAGR to 2031.

- By application, industrial equipment accounted for 42.98% share of the high-temperature insulation materials market size in 2025, while dedicated insulation applications are expanding at a 5.67% CAGR through 2031.

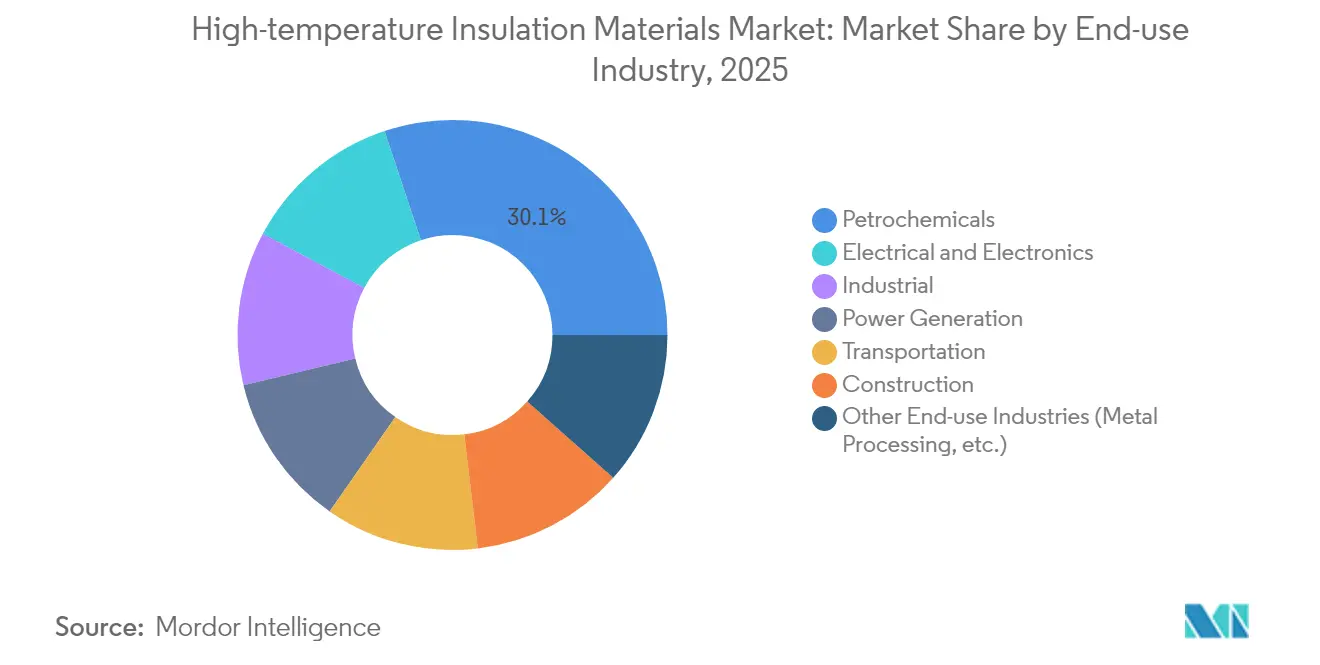

- By end-use industry, the petrochemicals segment held 30.12% revenue share in 2025; electrical and electronics is the fastest-growing end user at 5.71% CAGR to 2031.

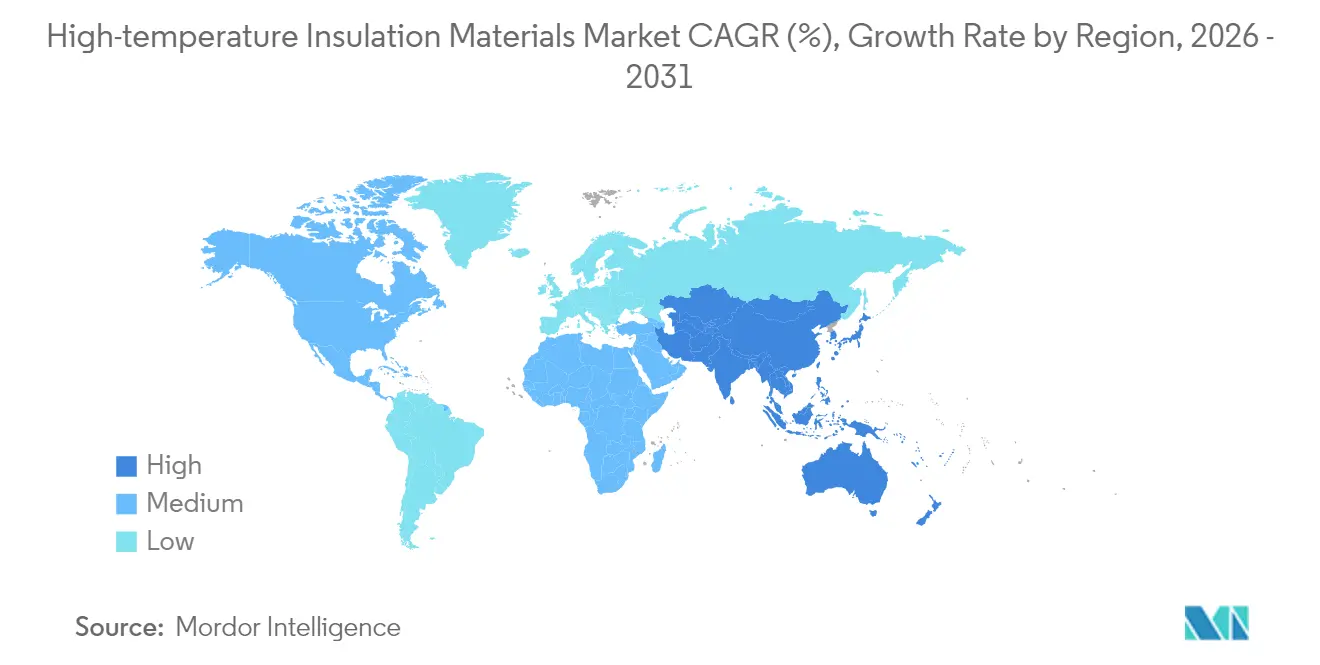

- By geography, Asia-Pacific captured 47.08% of 2025 revenue and is forecast to post a 5.44% CAGR, the highest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of High-temperature Insulation Materials Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for Energy-Efficient Industrial Furnaces | +1.2% | Global focus in Asia-Pacific and Europe | Medium term (2-4 years) |

| Tightening Building-Energy Codes Requiring High-Temperature Insulation | +0.8% | North America & EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Rapid Capacity Build-Out in Asian Petro-Chem and Metal Sectors | +1.5% | Asia-Pacific core, spill-over to MEA | Short term (≤ 2 years) |

| Green-Hydrogen Electrolyser Adoption needs High Temperature Lining | +0.7% | Europe and North America, emerging Asia-Pacific | Long term (≥ 4 years) |

| Growing Lightweight, Durable Insulation Material Demand | +0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Energy-Efficient Industrial Furnaces

Industrial furnace builders face stricter energy-performance rules under the 2024 International Energy Conservation Code, which lowered allowable heat loss and tightened air-leakage rates. Operators specify ceramic fibre blankets and microporous panels that endure 1,000°C service without compromising fuel economy. Typical energy savings approach 30% over legacy linings, improving payback despite higher capital cost. Integrating smart thermal management systems with advanced insulation materials enables predictive maintenance and optimized energy consumption, positioning high-temperature insulation as a critical component in Industry 4.0 transformation strategies. [1]International Code Council, “2024 International Energy Conservation Code,” iccsafe.org.

Tightening Building-Energy Codes Requiring High-Temperature Insulation

The same 2024 International Energy Conservation Code (IECC) revision also sharpened commercial building shell requirements, magnifying interest in continuous insulation and thermal-bridge mitigation. European Union Fit-for-55 directives demand complementary heat- and fire-resistant solutions in industrial facilities, increasingly favoring materials that combine thermal performance with fire safety, driving demand for non-combustible options like mineral wool and ceramic fiber systems. Building owners face escalating energy costs and carbon pricing mechanisms that make high-performance insulation economically attractive over building lifecycles. The convergence of energy efficiency mandates and fire safety requirements creates a sweet spot for high-temperature insulation materials that can address both regulatory imperatives simultaneously.

Rapid Capacity Build-Out in Asian Petro-Chem and Metal Sectors

Asia-Pacific's industrial expansion continues at an unprecedented scale, with China and India leading massive capacity additions in petrochemicals and steel production. China's heavy industry expansion, while supporting clean technology manufacturing, creates parallel demand for thermal management solutions in aluminum and steel production facilities. These assets rely on refractory linings that withstand intense thermal cycling while reducing fuel intensity. Specifications increasingly call for premium ceramic fibres and vacuum-formed shapes that shorten heat-up cycles and extend maintenance intervals. Middle-East complexes replicate these standards to meet export market emissions rules, further widening regional material demand.

Green-Hydrogen Electrolyser Adoption Needs High-Temperature Lining

The global transition to green hydrogen production creates new demand vectors for specialized high-temperature insulation materials. Solid oxide electrolysis cells (SOECs) operate at temperatures between 500-900°C, requiring advanced thermal management solutions that can maintain efficiency while preventing heat loss. High-temperature steam electrolysis systems offer 35% lower electricity requirements than conventional low-temperature electrolysis, making thermal insulation critical for economic viability. Manufacturers, therefore, incorporate refractory ceramic fibre boards and microporous tiles to retain heat while safeguarding personnel from surface temperatures. Thermal-energy-storage blocks in emerging heat batteries for renewables likewise use similar high-temperature insulation to store heat beyond 1,000°C, underscoring cross-sector synergy.

Restraints Impact Analysis of High-temperature Insulation Materials Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Occupational Exposure Limits on Synthetic Vitreous Fibres | -0.9% | Global; stricter in Europe & North America | Medium term (2-4 years) |

| Volatile Alumina and Silica Prices Squeeze Converter Margins | -0.6% | Global, affecting Asia-Pacific processing hubs | Short term (≤ 2 years) |

| Supply-Chain Risk for High-Purity Zirconia Precursors | -0.4% | Global; high China dependency | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Occupational Exposure Limits on Synthetic Vitreous Fibres

Regulatory authorities worldwide are tightening occupational exposure limits for synthetic vitreous fibers, with OSHA maintaining permissible exposure limits of 0.2 fibers per cubic centimeter for refractory ceramic fibers [2]Occupational Safety and Health Administration, “Safety and Health Topics: Refractory Ceramic Fibers,” osha.gov. The Health and Safety Executive in the UK has classified refractory ceramic fiber as a category 2 carcinogen, necessitating stringent control measures under COSHH regulations that increase handling costs and limit application flexibility. European legislation increasingly favors low-biopersistent alternatives, driving market share gains for alkaline earth silicate fibers despite their higher costs and slightly reduced temperature capabilities. The regulatory trend toward biosoluble fibers creates opportunities for innovative manufacturers while constraining traditional ceramic fiber applications. Compliance costs and liability concerns are pushing industrial users toward alternative materials, even when performance trade-offs exist. The long-term trajectory suggests continued regulatory pressure that will reshape the competitive landscape in favor of companies with strong low-biopersistent fiber portfolios.

Volatile Alumina and Silica Prices Squeeze Converter Margins

Raw material price volatility significantly impacts high-temperature insulation manufacturers, with alumina and silica representing 40-60% of production costs for ceramic fiber products. Zirconium dioxide prices have fluctuated between USD 3,755-6,067 per metric ton, creating margin pressure for manufacturers of premium refractory products. Supply chain disruptions and geopolitical tensions have exacerbated price volatility, with China's dominance in refractory mineral supply creating concentration risks for global manufacturers. The strategic nature of these materials means price fluctuations often reflect broader economic and political dynamics rather than pure supply-demand fundamentals. Manufacturers are responding through vertical integration strategies and long-term supply agreements, but smaller players face particular vulnerability to price spikes. The development of alternative raw material sources and recycling technologies offers potential mitigation, but implementation timelines extend beyond the immediate forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

High-temperature Insulation Materials Market Segment Analysis

By Material Type:

Ceramic Fibre Retains Leadership as Alternatives ScaleCeramic fibre held 55.63% of 2025 revenue owing to its 1,260°C service limit, low density, and adaptability into blankets, modules, and boards. This leadership is anchored in asset-heavy industries, such as steel, non-ferrous metals, and petrochemicals, where downtime costs dwarf material prices. The high-temperature insulation materials market size for ceramic fibre is expected to post steady single-digit growth as new capacities in Asia-Pacific come on stream.

Other material types, such as aerogel composites and microporous panels, are the fastest-growing group at 6.01% CAGR. Weight-sensitive end uses value aerogels’ sub-0.020 W/m·K (Watt per metre Kelvin) conductivity combined with fiber reinforcement that boosts handling strength. Regulatory-driven migration to low-biopersistent chemistries accelerates alkaline earth silicate wool uptake, especially in Europe. Polycrystalline wool supports specialized duties above 1,500°C, while vacuum-formed shapes address complex geometries that would require costly on-site gunning or ramming. The high-temperature insulation materials industry continues to refine sintering additives and fiber diameters to balance shot content, strength, and thermal shock resistance.

By Application:

Industrial Equipment Dominates, Insulation Retrofits AccelerateIndustrial equipment accounted for 42.98% of 2025 revenue, reflecting the indispensability of reliable refractory linings in furnaces, kilns, and heaters. Process licensors impose exacting thermal-efficiency benchmarks; thus, furnace Original Equipment Manufacturers (OEMs) specify multilayer ceramic fibre and microporous systems to minimize shell temperatures and enhance operator safety. Equipment makers also integrate laminated insulation packs that simplify lining replacement during annual shutdowns, curbing unplanned outages.

Pure insulation retrofits represent the quickest-rising use case at 5.67% CAGR as facility owners respond to updated energy codes and carbon-pricing schemes. The high-temperature insulation materials market size for building retrofits is set to widen as governments fund industrial decarbonization grants. Thin, flexible blankets support tight spaces behind cladding panels while maintaining non-combustibility ratings. Fire-barrier assemblies combine mineral wool and ceramic fibre layers to meet insulation and flame-spread criteria. Cross-sector synergies emerge as technology proven in process equipment migrates into high-rise mechanical rooms and district-heating distribution lines.

By End-Use Industry:

Petrochemicals Steady, Electronics Momentum BuildsPetrochemicals maintained a 30.12% share in 2025, underpinned by the sheer number of fired heaters, crackers, and reformers that require refractory upkeep. Operators mandate long campaigns between turnarounds, driving adoption of fiber modules that slash installation time and maintain uniform heat profiles. Upgraded steam crackers now pursue lower-carbon intensity, increasing demand for multilayer insulation packages that tolerate hydrogen-rich combustion.

Electrical and electronics applications, such as semiconductor fabs, lithium-ion gigafactories, and electric vehicle (EV) power electronics, are the fastest-growing at 5.71% CAGR. Cleanrooms demand particulate-free insulation, favoring low-dust ceramic fibre boards in high-temperature diffusion furnaces. Power chip sintering presses operate near 900°C, relying on stable insulation to prevent thermal runaway. The high-temperature insulation materials market share for electronics remains modest today, yet expands rapidly as device thermal loads climb and fabs proliferate across Asia-Pacific and North America.

Geography Analysis

APAC High-temperature Insulation Materials Market

Asia-Pacific had a 47.08% market share in 2025 and is projected to advance at a 5.44% CAGR. China’s ongoing capacity additions in steel, aluminum, and chemicals sustain bulk demand, while India’s National Infrastructure Pipeline and expanding hydrogen plans reinforce long-term growth. Southeast Asian nations add petrochemical and renewables assets that likewise require refractory linings. Policymakers increasingly enforce energy-efficiency norms, shifting purchasing toward low-conductivity fibre modules and aerogels.

North America High-temperature Insulation Materials Market

North America ranks second by value. Federal clean energy credits and state-level carbon caps make retrofit insulation economically attractive in refineries, liquidated natural gas (LNG) terminals, and pulp mills. The region’s reshoring of semiconductor and battery manufacturing raises consumption of ultra-clean insulation boards and fiber-reinforced aerogels. Robust industrial safety enforcement also accelerates adoption of alkaline earth silicate wool.

Europe High-temperature Insulation Materials Market

Europe remains technology-focused, leveraging its stringent environmental rules and carbon-border adjustments to champion low-biopersistent materials. European Union (EU) Green Deal investments spur renovation of existing industrial assets with multilayer linings that marry insulation and fire-containment. Innovative pilot projects in concentrated solar power and thermal energy storage adopt advanced ceramics, broadening application footprints.

Value Chain Analysis

The value chain starts with upstream extraction and beneficiation of mineral inputs (alumina and silica for ceramic fibers, and zirconia-bearing precursors for premium grades), along with binders, reinforcements, and packaging materials. These inputs move to midstream producers that melt, fiberize, calcine, or sinter and then convert outputs into blankets, modules, boards, papers, gaskets, insulating firebricks (IFBs), and engineered microporous or vacuum-formed shapes. To protect delivered insulation costs, suppliers typically tighten control over upstream sourcing and regional logistics, particularly given volatility in alumina, silica, and zirconia-linked feedstocks and the risk of freight disruption.

Downstream, products reach furnace OEMs, EPC contractors, and end users through a mix of direct sales and specialist distributors or fabricators, with heavy emphasis on furnace and high-temperature industrial equipment maintenance during turnarounds. Installation and aftermarket services, including lining design, prefabrication, anchoring systems, and on-site fitting, account for a meaningful portion of delivered value where downtime avoidance is critical. Standards and industry bodies influence specifications and compliance across the chain, including ISO/TC 163/SC 3 and ASTM International for test methods and system guidance. In parallel, ECFIA stewardship initiatives such as CARE (Controlled And Reduced Exposure) shape handling practices and product selection toward low-biopersistent alternatives in regulated workplaces.

Competitive Landscape

The high-temperature insulation materials market exhibits moderate consolidation with established multinational corporations, such as Morgan Advanced Materials, Alkegen, Saint-Gobain, and Luyang Energy-saving Materials Co., Ltd., competing alongside specialized regional manufacturers. They devote significant R&D resources to super-wool and hybrid aerogel platforms, preparing for stricter exposure limits. Product differentiation revolves around fiber chemistry, shot content, and module anchoring designs that speed installation. Vendors also integrate digital monitoring infrared cameras, embedded thermocouples to showcase insulation performance, and support warranty programs. Partnerships with furnace Original Equipment Manufacturers (OEMs) and Engineering, Procurement, and Construction (EPC) contractors deepen preferred-supplier status, while vertical integration into alumina and silica mining helps limit raw-material risk.

High-temperature Insulation Materials Industry Leaders

Morgan Advanced Materials

Luyang Energy-saving Materials Co., Ltd.

Saint-Gobain

Alkegen

ROCKWOOL A/S

- *Disclaimer: Major Players sorted in no particular order

High-temperature Insulation Materials Market Companies Covered in this Report

- 3M

- Alkegen

- Almatis

- Aspen Aerogels, Inc.

- BNZ Materials,Inc.

- Cabot Corporation

- Carlisle Companies Inc.

- Dyson Technical Ceramics

- Etex Group

- ISOLITE

- Knauf Insulation

- Luyang Energy-saving Materials Co., Ltd.

- M.E. Schupp Industriekeramik Gmbh

- Morgan Advanced Materials

- NUTEC Incorporated

- Pacor Inc.

- Pyrotek

- Rath-Group

- ROCKWOOL A/S

- Saint-Gobain

Read Analysis of High-temperature Insulation Materials Companies

Market Opportunities and Future Outlook

White-space is emerging in higher-performance, lower-thickness insulation systems for industrial furnaces, petrochemical heaters, and high-temperature process lines, where operators focus on fuel savings and lower shell temperatures while maintaining uptime. The publication of ISO 18959:2025 (requirements for factory-made rigid nano-microporous insulation for industrial applications from 100 degrees C to 1,150 degrees C) supports more standardized procurement of nano-microporous products. ASTM C1696-26 updates system-level guidance for industrial thermal insulation across a wide temperature range. Together, these standards-based anchors and the ongoing shift away from higher-exposure synthetic vitreous fibers in regulated environments create openings for suppliers with low-biopersistent fiber portfolios, cleaner boards for electronics fabrication environments, and engineered multilayer packages that shorten turnaround time.

On the supply side, capacity and technology investments provide concrete signals that manufacturers are aligning with energy-efficiency and decarbonization requirements. In April 2026, ROCKWOOL broke ground on a USD 175 million manufacturing facility in Washington (United States) using proprietary electric melting technology, and in March 2026 MAB Group announced a new rock wool plant project in Hungary backed by HIPA support. In North America, Knauf Insulation expanded its Shelbyville, Indiana footprint with investments that include new blowing wool and pipe insulation capacity tied to 2026 commissioning, reinforcing localization of insulation supply for building and industrial channels. These announcements point to opportunity areas around regionalized sourcing, electric-melting and lower-CO2 production routes, and product positioning that connects fire performance and energy efficiency to increasingly formalized classification and test regimes, including the EU Delegated Regulation (EU) 2026/557 on fire resistance performance classes for construction products.

Recent Industry Developments in High-temperature Insulation Materials Market

- June 2026: Saint-Gobain completed the divestment of its high-temperature industrial insulation textile businesses H.K.O. Isolier- und Textiltechnik GmbH (Germany) and Deltec (France) to a fund managed by DUBAG Group. The transaction supports Saint-Gobain's portfolio optimization under its Lead and Grow strategy and refocuses resources toward core construction and performance solutions, while transferring specialized industrial textile insulation capacity to a dedicated financial sponsor.

- March 2026: Morgan Advanced Materials and RHI Magnesita announced commercial availability of a jointly developed Advanced Insulation System for steel treatment ladles, targeting applications such as torpedo cars, tundishes, and ladles in Europe and CIS markets. The collaboration combines refractory and insulation know-how to improve thermal performance in harsh steelmaking duties, reinforcing solution-led selling and raising the bar for engineered, application-specific insulation packages.

- October 2024: Carlisle Companies Inc. agreed to acquire the expanded polystyrene (EPS) insulation segment of PFB Holdco, Inc. The deal broadens Carlisle's insulation portfolio and distribution reach, adding scale in polymer insulation categories that compete for portions of the broader insulation spend alongside high-temperature solutions in construction and industrial envelopes. The acquisition expands Carlisle's polymer insulation capabilities, supporting deeper market access in building envelopes and accelerating its diversification into value-added polymer products.

High-temperature Insulation Materials Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the market covers insulation materials designed to operate reliably at elevated temperatures, primarily to reduce heat loss, protect equipment, and improve process safety in industrial settings.

Scope exclusions: We exclude low-temperature building insulation and any labor-only installation services unless they are bundled with material supply pricing.

Segments Covered in This Report

- By Material Type

- Fiberglass

- Ceramic Fibre

- Mineral Wool

- Alkaline Earth Silicate (AES)

- Aluminum Silicate Wool (ASW) or Refractory Ceramic Fibre (RCF)

- Polycrystalline Wool or Fibre (PCW)

- Long Fibre

- Vacuum-Formed Insulating Products

- Polyurethane Foam

- Polystyrene

- Insulating Fire-Bricks (IFB)

- Other Material Types (Aerogel Blankets, Microporous Panels, etc.)

- By Application

- Insulation

- Industrial Eqipment

- Other Applications (Building and Fire-Protection, etc.)

- By End-use Industry

- Petrochemicals

- Industrial

- Power Generation

- Transportation

- Electrical and Electronics

- Construction

- Other End-use Industries (Metal Processing, etc.)

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- NORDIC Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research builds the starting market structure, so the later modeling is anchored to real industrial activity rather than stated opinions. We reference public sources such as industrial production and energy data from the US Energy Information Administration, manufacturing indicators from the Federal Reserve, trade and product flow statistics from UN Comtrade, and factory output releases from OECD and national statistics offices.

To tighten the use-case mapping, we also review technical and standards information from bodies such as ISO and ASTM, plus peer-reviewed papers that report typical service temperature ranges and replacement behavior in furnaces and kilns. Company annual reports, investor presentations, and credible trade press are used to understand capacity changes and pricing direction. Where needed, paid subscriptions for company financials and shipment-level import and export data are used to cross-check supply exposure, and this desk list is illustrative since many additional sources were reviewed for collection, clarification, and validation.

Primary Interviews and Surveys

Primary interviews and surveys are used to pressure-test desk assumptions on how materials are specified, how often they are replaced, and what price points are realistic across temperature ranges. We speak with a mix of producers, distributors, EPC and maintenance stakeholders, and end users in process industries across key regions, so the demand pool and pricing logic can be adjusted where secondary data is thin.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 12% | APAC: 49% |

| Mid tier: 61% | Functional/Unit leaders: 33% | EMEA: 33% |

| Smaller Players: 14% | Managers: 55% | Americas: 18% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where industrial heat-intensive activity is reconstructed into an addressable insulation demand pool, then translated into value using typical consumption patterns and price bands. We start from indicators that track where high-temperature insulation is actually used, then narrow it using application intensity and practical replacement behavior.

Key inputs in the model include crude steel output and capacity utilization, cement and glass production trends, refinery and petrochemical operating rates, furnace and kiln maintenance cycles, and import and export movements for relevant insulation material categories. To keep the value layer realistic, price assumptions are structured by temperature capability and material family, then checked against interview-based ranges, recent input-cost direction, and observed procurement practices. Results are corroborated with selective bottom-up approximations, such as sampled volume times average selling price checks and channel feedback, and gaps are handled by applying conservative penetration rates where visibility is limited.

For forecasting, scenario analysis is used around industrial output, energy price sensitivity, and maintenance spending, followed by smoothing of near-term volatility so the curve does not overreact to a single year. Assumptions are reviewed with primary respondents to confirm that demand drivers and pricing progression remain plausible under base-case conditions.

Data Validation & Update Cycle

Validation is done through multiple checks so the final number remains consistent with independent signals. We compare outputs against industrial production benchmarks, trade flows, and known capacity additions, and then review any large variances by revisiting the specific assumption that created the swing.

Before sign-off, the model goes through step-by-step analyst reviews, including arithmetic checks, unit consistency checks, and logic checks on price and volume movement by region. When a key input changes materially, or when interviews flag a new pricing or substitution shift, the relevant assumptions are re-contacted and revalidated. The report is refreshed annually, with interim updates triggered by material events, and a final pre-delivery pass is done so clients receive the latest view available at the time of release.

Mordor Intelligence's High Temperature Insulation Materials Market Estimate Compared With Other Published Estimates

Published market values for high-temperature insulation materials often do not align, even when studies appear to be describing the same category. Differences typically come from how each study sets the temperature threshold, whether adjacent refractory or installation spend is blended in, and how prices are normalized across regions and years.

A refresh-led gap also shows up in the details, because currency conversion timing and the way average selling prices are rolled forward can change the reported value even if volumes are similar. By rechecking price bands and demand signals during each annual refresh, and by aligning currency timing to the stated year rather than a mixed average, Mordor Intelligence reduces swings that can result from one-off inflation spikes and delayed updates.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.24 B (2025) | |

| Industry Research Publisher A | USD 7.64 B (2024) | Uses an earlier base year and a different time window, which can pull down value if pricing is not updated to the same currency timing. The scope presentation suggests broader temperature bands and end-use mapping, but the price normalization method is not clearly shown. |

| Industry Research Publisher B | USD 6.90 B (2025) | Anchors the 2025 value to a lower stated market size and applies a higher long-run CAGR to 2034, which can indicate a different base-case stance. The published summary does not fully clarify whether adjacent refractory linings or installation-related spend is included, which can change the boundary materially. |

Overall, the spread is mainly explained by timing and boundary choices, followed by how price progression is handled across regions. With clearer year alignment, repeatable demand indicators, and visible price logic tied to temperature capability, the sizing steps remain easier to audit and reproduce for planning discussions.

Key Questions Answered in the Report

What is the current value of the high-temperature insulation materials market?

The High-temperature Insulation Materials Market is worth USD 9.66 billion in 2026 and is forecast to grow to USD 12.05 billion by 2031 at a 4.52% CAGR.

Which material type holds the largest share of the high-temperature insulation materials market?

Ceramic fibre leads with 55.63% revenue share in 2025 due to its versatility and temperature resistance.

Why is Asia-Pacific the dominant region in the high-temperature insulation materials market?

Massive petrochemical, metals, and electronics capacity expansions combined with stricter energy-efficiency mandates drive 47.08% of global demand and the fastest regional CAGR of 5.44%.

How are regulations influencing product development in this market?

Tighter occupational exposure limits are steering R&D toward low-biopersistent alkaline earth silicate fibres and fiber-reinforced aerogels that maintain performance while improving worker safety.

Page last updated on: