Emollient Esters Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

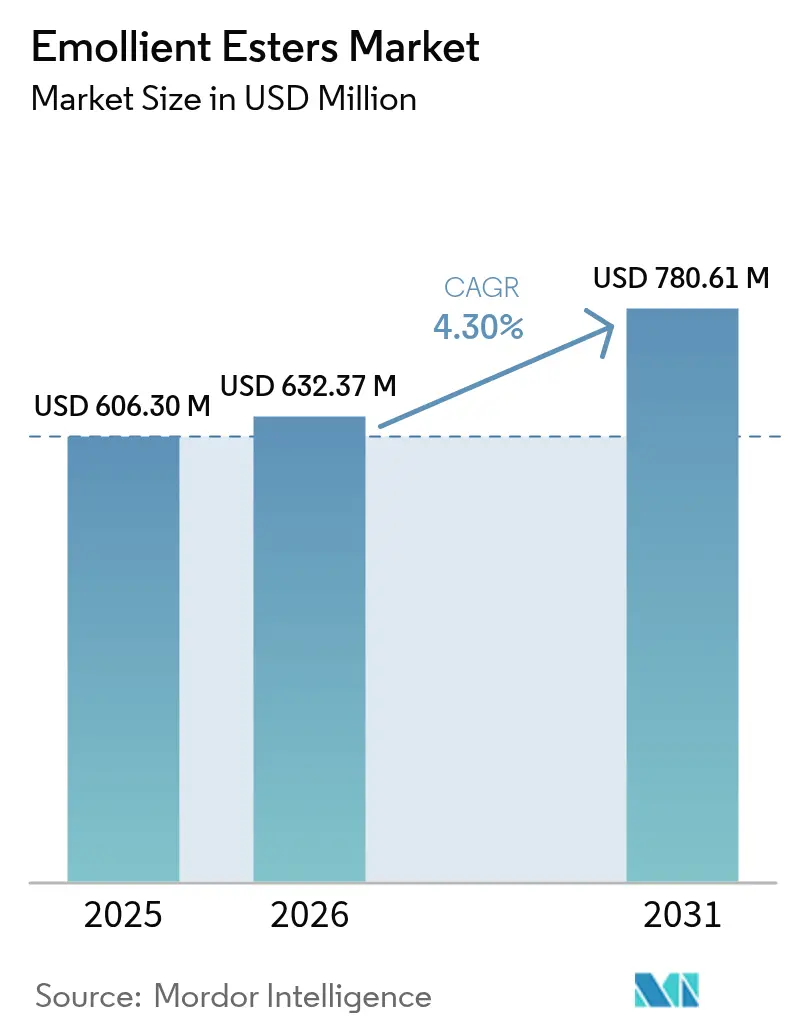

| Market Size (2026) | USD 632.37 Million |

| Market Size (2031) | USD 780.61 Million |

| Growth Rate (2026 - 2031) | 4.30% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Emollient Esters Market Analysis by Mordor Intelligence

The emollient esters market size was valued at USD 606.30 million in 2025 and estimated to grow from USD 632.37 million in 2026 to reach USD 780.61 million by 2031, at a CAGR of 4.30% during the forecast period (2026-2031). Growth stems from rising demand for multifunctional, sustainably produced esters, wider adoption of enzymatic synthesis, and premiumization trends across personal care categories. Asia-Pacific’s large production base and fast-growing beauty industry accelerate regional consumption, while REACH-driven European reformulations raise demand for high-purity, bio-based grades. Manufacturers gain pricing power through differentiated carbon-reduction technologies, although volatile vegetable-oil feedstock prices continue to pressure margins. Regulatory calls for microplastic-free formulations further boost natural and up-cycled esters, pushing the emollient esters market toward value-oriented specialty solutions rather than high-volume commoditized grades.

Key Report Takeaways

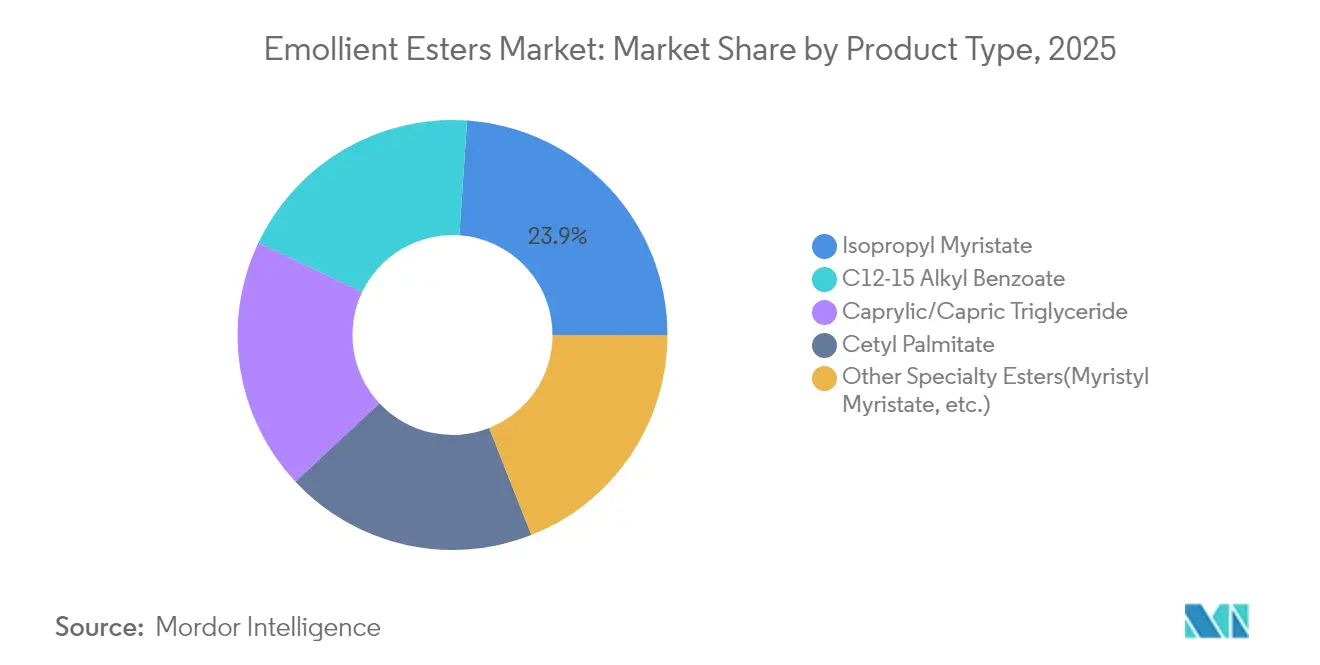

- By product type, isopropyl myristate led with 23.92% of emollient esters market share in 2025; caprylic/capric triglyceride is projected to advance at a 5.38% CAGR through 2031.

- By source, plant-derived grades held 70.35% of the emollient esters market share in 2025, while up-cycled feedstocks are set to grow the fastest at 5.65% CAGR to 2031.

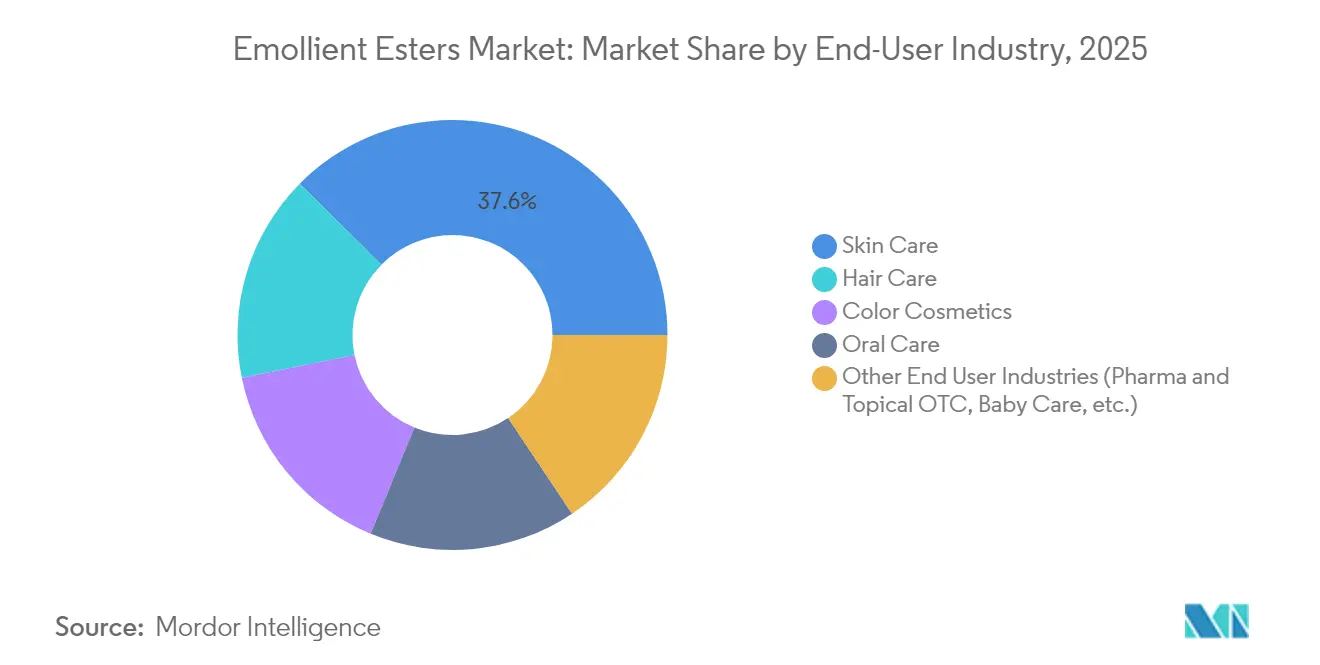

- By end-user industry, skin care accounted for 37.58% share of the emollient esters market size in 2025 and is expanding at a 5.76% CAGR through 2031.

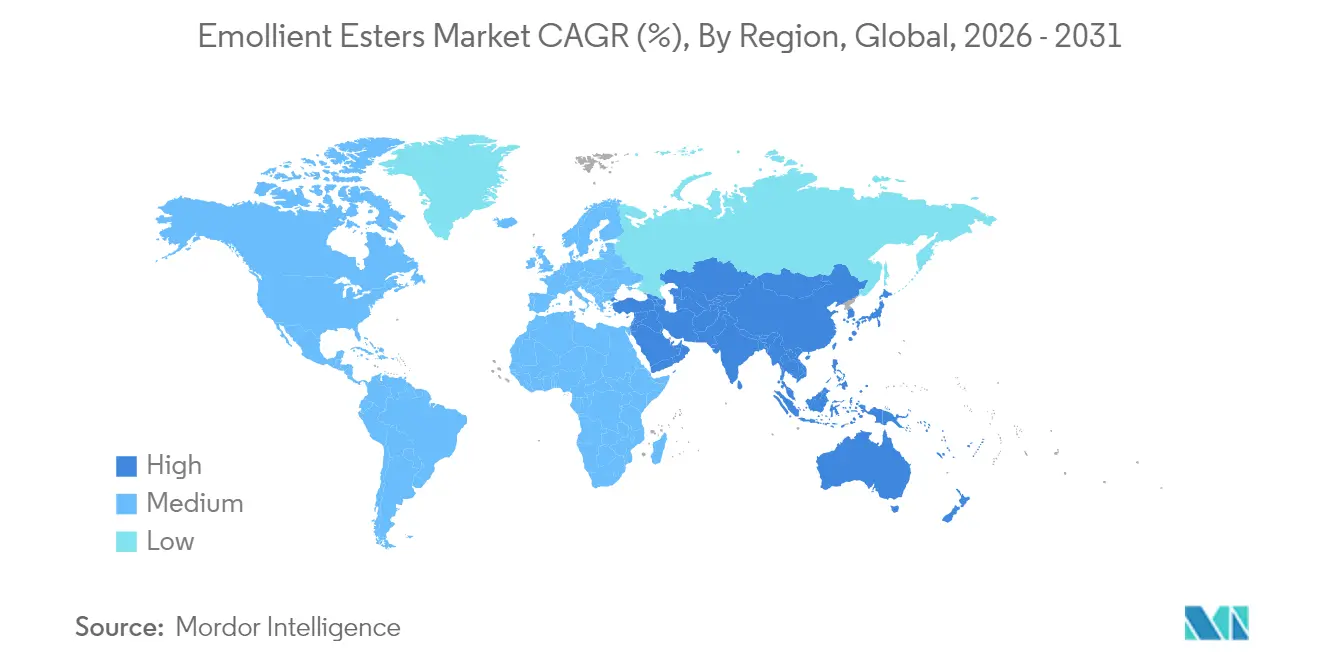

- By geography, Asia-Pacific captured 34.62% of 2025 revenue and is expected to register the highest regional CAGR of 5.05% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Emollient Esters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for personal care & cosmetic products | +1.2% | Global, with strongest impact in Asia-Pacific | Medium term (2-4 years) |

| Rising preference for naturally derived emollient esters | +0.9% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Growth in dermatology & topical-pharma formulations | +0.7% | Global, led by developed markets | Medium term (2-4 years) |

| Expansion of premium beauty brands in emerging economies | +0.8% | Asia-Pacific, Latin America, MEA | Medium term (2-4 years) |

| Shift toward solid & water-free beauty formats boosting high-melting esters | +0.5% | Global, early adoption in Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Personal Care & Cosmetic Products

E-commerce penetration in tier-2 cities accounts for 55% of prestige beauty sales, broadening access to premium formulations[1]Business Standard, “China’s cosmetics retail climbs,” business-standard.com. Gen Z and millennial consumers favor clinically backed ingredients, sustaining demand for caprylic/capric triglyceride and other multifunctional esters. The result is consistent volume growth and improved average selling prices across the global emollient esters market.

Rising Preference for Naturally Derived Emollient Esters

Plant-based grades already dominate but continue to gain share as leading suppliers launch biodegradable, sustainably sourced lines, such as BASF’s new portfolio of natural betaines. Evonik’s enzymatic routes achieve full-scale CO₂ reductions, aligning with brand pledges for climate neutrality[2]Evonik Industries, “Evonik opens sustainable cosmetic ester plant in Steinau,” evonik.com. With REACH restrictions tightening, bio-based esters enjoy regulatory advantages, reinforcing their long-term growth trajectory within the emollient esters market.

Growth in Dermatology & Topical-Pharma Formulations

Cosmeceutical demand elevates performance standards for penetration enhancers and barrier-repair agents. Patent activity for fatty-acid esters as anti-Malassezia actives underscores expanding therapeutic utility. Brands willing to pay for clinically proven functionality boost the value mix of the emollient esters market.

Expansion of Premium Beauty Brands in Emerging Economies

Asia-Pacific’s USD 190 billion beauty sector is growing 6.7% annually to 2027, with premium segments capturing the lion’s share. Cross-border e-commerce delivers international brands into new cities, while local manufacturers co-develop upscale SKUs that rely on high-purity esters for texture and sensorial performance. This trend supports a positive price–mix for suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in fatty-acid & alcohol feedstock prices | -0.8% | Global, particularly impacting Asia-Pacific producers | Short term (≤ 2 years) |

| Stringent REACH & global cosmetic-safety regulations | -0.4% | Europe leading, with global spillover effects | Medium term (2-4 years) |

| Rising substitution by silicone-free texturizers & polymers | -0.3% | North America & Europe, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Fatty-Acid & Alcohol Feedstock Prices

Palm-oil-derived alcohol costs rose 12% in 2024, while cocoa products doubled on adverse weather, squeezing margins for ester producers dependent on these commodities. Smaller firms lacking hedging capacity face liquidity pressure, prompting investment in diversified feedstocks and enzymatic processes that tolerate variable raw-material inputs, yet near-term profitability remains vulnerable.

Stringent REACH & Global Cosmetic-Safety Regulations

The European Commission’s ban on synthetic polymer microparticles adds reformulation burdens and testing costs[3]Publications Office of the European Union, “Restrictions on synthetic polymer microparticles,” eur-lex.europa.eu. REACH dossiers demand high data fees, especially punitive for low-volume specialty esters. As the highest standard migrates worldwide, suppliers must budget for universal compliance, marginally restraining the emollient esters market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Specialty Esters Drive Innovation

Isopropyl myristate retained 23.92% of 2025 revenue, anchoring the emollient esters market through its broad utility in skin, hair, and color cosmetics. Caprylic/capric triglyceride’s 5.38% CAGR demonstrates a migration toward multifunctional ingredients that combine emolliency with antimicrobial action. Its popularity supports premium shelf prices and improved profitability for formulators relying on a single ingredient to deliver multiple claims.

Enzymatically produced specialty esters enable up to 60% lower carbon footprints, letting suppliers capture brand sustainability budgets. Novel C12-15 alkyl benzoate grades tailor spreading profiles for sun care, while cetyl palmitate gains relevance in solid moisturizers. Patent filings for ultra-long-chain sugar alcohol esters indicate an innovation pipeline geared toward stability and bioactivity improvements that will diversify product offerings within the emollient esters market.

By Source: Circular Economy Reshapes Supply Chains

Plant-derived grades secured a 70.35% share in 2025 on entrenched palm and coconut oil supply chains. Up-cycled oils, however, are growing 5.65% annually as processors valorize waste streams such as olive-pomace fractions into market-ready esters without additional land use. Brands value the lower environmental footprint and story-rich positioning.

Petrochemical esters remain essential in applications requiring tight viscosity tolerances, yet shrinking acceptance underscores a structural shift. Regulatory incentives favor bio-content, while supply-chain-risk mitigation pushes users to blend multiple source types. These changes diversify procurement strategies across the emollient esters market.

By End-User Industry: Skin Care Segment Drives Premium Growth

Skin care’s 37.58% share of 2025 sales and 5.76% CAGR confirm its position as the largest and fastest growth engine within the emollient esters market. Anti-aging serums, barrier-repair creams, and derma-cosmetics integrate high-performance esters that justify premium price positioning. Hair care follows, employing emollients for conditioning and cuticle protection, especially in sulfate-free shampoos that require extra sensorial agents.

Color cosmetics leverage esters for pigment wetting and texture control, with solid lipstick sticks and waterless foundations embodying rising demand for high-melting wax esters. Oral care and pharma applications, though smaller, seek clinical purity grades, providing a price premium and stable demand arc important to suppliers’ portfolio balance.

Geography Analysis

Asia-Pacific captured 34.62% of 2025 revenue and is forecast for a 5.05% CAGR. Domestic investments such as Evonik’s enzymatic line elevate regional self-sufficiency, shorten lead times, and reduce import tariffs, strengthening competitiveness across the emollient esters market.

North America exhibits mature but innovation-driven demand. Consumers pay premiums for natural, traceable ingredients, encouraging suppliers to widen bio-based offerings. Regulatory clarity by the FDA plus state-level disclosures increase documentation needs, giving technologically advanced producers an edge. Mexico’s rising contract manufacturing base benefits from near-shoring dynamics and preferential trade agreements with the United States, underpinning future growth.

Europe’s stringent environmental framework drives market evolution. REACH pushes reformulations toward low-carbon and microplastic-free esters. Germany, France, the United Kingdom, and Italy house sophisticated laboratories focused on sensory innovation and green chemistry, fostering high-value downstream demand.

South America shows early-stage expansion led by Brazil’s increasing disposable income and local beauty entrepreneurship.

The Middle East and Africa remain small yet promising, especially in Saudi Arabia and South Africa where retail modernization and social-media exposure stimulate upmarket personal care adoption.

Regulatory Landscape

In the European Union, emollient esters supplied into cosmetics are governed by Regulation (EC) No 1223/2009, with 2025-2026 updates tightening ingredient compliance. Regulation (EU) 2026/909 (adopted 27 April 2026) amended the cosmetics framework for the permitted use of specific substances. The related Omnibus VIII changes introduced new CMR-linked restrictions, with a compliance and product-withdrawal deadline of 1 May 2026. For ester suppliers, this lifts demand for high-purity grades and toxicology packages that help downstream brands and contract manufacturers during reformulation cycles. In the United States, the Modernization of Cosmetics Regulation Act of 2022 (MoCRA) expanded FDA oversight through facility registration and strengthened expectations for safety substantiation and recordkeeping, including FDA authority to access certain safety and adverse-event related records during inspections. In China, the National Medical Products Administration (NMPA) continues to enforce the Cosmetics Supervision and Administration Regulation (CSAR) framework, including registration or filing pathways for new cosmetic ingredients and a post-market safety monitoring period (typically three years) before inclusion in the Inventory of Existing Cosmetic Ingredients in China (IECIC), with NMPA Announcement No. 61 of 2025 updating IECIC-related matters. Together, these regimes increase documentation, traceability, and change-control requirements for globally supplied emollient ester portfolios.

Value Chain Analysis

The emollient esters value chain begins with oleochemical feedstocks, mainly fatty acids and fatty alcohols derived from palm, coconut, and other vegetable oils, and extends through esterification, purification, and blending into cosmetic-grade ingredients. Producers increasingly use enzymatic synthesis alongside conventional chemical catalysis to improve purity and reduce byproducts, which supports premium personal-care applications and increases the need for globally aligned compliance documentation. Integrated chemical and oleochemical assets give cost and supply advantages for large suppliers, for example BASF leverages its integrated complex at Ludwigshafen, while specialty players differentiate through lipid technology, application labs, and bio-based sourcing strategies. Midstream activities include tolling, packaging, and quality systems aligned with cosmetic GMP expectations, followed by distribution through direct supply agreements and specialty chemical distributors into brand owners, contract manufacturers, and formulators. In Europe, industry bodies such as EFfCI and APAG (Oleochemicals Europe) shape technical expectations and harmonization priorities, while logistics and cluster concentration can add lead-time risk. Capacity constraints in German chemical clusters, including Ludwigshafen and Marl, and corridor dependencies such as Rotterdam-to-Ludwigshafen movements can affect lead times for ester intermediates. Downstream demand also reflects formulation shifts toward silicone alternatives, microplastic-free concepts, and traceable, plant-derived or circular-feedstock claims, which raises the value of consistent performance data and transparent sourcing.

Competitive Landscape

The global emollient esters market exhibits moderate fragmentation. Major players like BASF, Evonik, and Croda utilize strategies such as backward integration, multi-site production, and expansive technical service teams to clinch large-volume contracts. Mid-tier companies are carving niches for themselves. The presence of patent portfolios centered on solvent-free methodologies and long-chain sugar alcohol esters underscores a fierce R&D competition. Strategic moves like BASF's distribution partnership with Azelis in July 2025 and Eternis Fine Chemicals' acquisition of Sharon Personal Care in 2024 highlight a trend of consolidation. These maneuvers aim to bolster regional presence and deepen technical expertise. Together, these strategies drive product innovation and enhance supply security in the emollient esters market.

Emollient Esters Industry Leaders

The Lubrizol Corporation

Croda International Plc

Stepan Company

BASF

Evonik Industries AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A gap is emerging for bio-based and circular-feedstock emollient esters that let brands meet stricter compliance and sustainability screens without giving up sensorial performance, particularly in skin care and sun care where spreading, pigment wetting, and UV-filter solubility matter. Regulatory pressure in Europe, including the 1 May 2026 Omnibus VIII compliance timeline tied to the EU cosmetics framework, is driving reformulation activity and favors suppliers that can provide high-purity alternatives with complete safety documentation, traceable sourcing, and fit-for-purpose performance data for dermocosmetic and premium beauty lines. Investment and capability buildouts also show where suppliers are prioritizing resources. Evonik inaugurated a dedicated plant for sustainable cosmetic emollients at Steinau, Germany (September 2024), supporting enzymatic esterification routes aligned with carbon-reduction targets, and it expanded innovation-facing infrastructure with a beauty science and innovation center in Shanghai (June 2026) to shorten development cycles with regional customers. Circular inputs are being industrialized through programs such as the Bunge and Olleco joint venture announced in June 2025 to collect and reprocess used cooking oil in Europe, supporting up-cycled ester value propositions and reducing reliance on virgin vegetable oils. These steps create opportunities for suppliers to differentiate via low-temperature biocatalytic production, provide audit-ready documentation for multi-region compliance, and support regionally delivered technical services that speed adoption across fast-moving personal-care innovation pipelines.

Recent Industry Developments

- July 2026: BASF inaugurated a new production plant in Dusseldorf, Germany, for specialty emollients used in skin care and sun protection. The commissioning expands local supply for European customers and supports faster qualification of new grades amid ongoing reformulation work. The move also reinforces BASF's position in higher-value cosmetic ingredient manufacturing rather than commodity ester supply.

- June 2025: Bunge and Olleco announced a joint venture to collect and reprocess used cooking oil in Europe, enabling circular feedstocks for ester production. The collaboration strengthens sustainable sourcing and expands upcycled ester propositions for brands seeking lower environmental footprints. It aligns with EU circular economy initiatives and supports traceable, compliant supply chains.

- September 2024: Evonik inaugurated a new production plant for sustainable cosmetic emollients at its Steinau site in Germany, using an enzymatic process to reduce the climate footprint. The added capacity strengthened availability of specialty ester emollients aligned with renewable sourcing and sustainability claims. It raised the benchmark for process technology and documentation demanded by brands pursuing cleaner, lower-impact formulations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of emollient ester ingredients sold for use in personal care, cosmetics, and similar topical formulations, where they are added to improve skin feel, spreadability, and conditioning.

Scope exclusions: We exclude non-ester emollients and adjacent inputs such as silicones, mineral oils, fatty alcohols (non-esters), and fatty acids.

Segmentation Overview

- By Product Type

- Isopropyl Myristate

- C12-15 Alkyl Benzoate

- Caprylic/Capric Triglyceride

- Cetyl Palmitate

- Other Specialty Esters(Myristyl Myristate, etc.)

- By Source

- Plant-derived

- Petrochemical-derived

- Up-cycled / By-product-derived

- By End-User Industry

- Skin Care

- Hair Care

- Color Cosmetics

- Oral Care

- Other End-User Industries (Pharma & Topical OTC, Baby Care, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with building the demand context for emollient esters using public statistics and technical references, then checking how that demand translates into ingredient consumption. We draw on US FDA cosmetics guidance and ingredient resources, EU Cosmetics Regulation information (including CosIng), and International Trade Centre trade statistics for relevant chemical categories.

We also review open publications and associations that reflect formulation and ingredient trends, such as Personal Care Products Council materials, Cosmetics Europe resources, and peer-reviewed journal articles on ester chemistry and sensory performance. Company annual reports, investor presentations, and product brochures are used to understand capacity additions, product positioning, and typical end-use exposure. Where needed, paid subscriptions are used for company financials and intelligence, patent databases, and shipment-level import-export checks to keep assumptions anchored. These sources are illustrative, and many other references were used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work focuses on validating what is hard to see in public data, such as how ester types are chosen in formulations, how pricing moves with feedstock cycles, and how demand differs by region and application. We speak with a mix of ingredient suppliers, distributors, contract manufacturers, and downstream formulators, and then we confirm key assumptions across APAC, EMEA, and the Americas before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 13% | APAC: 51% |

| Mid tier: 58% | Functional/Unit leaders: 36% | EMEA: 30% |

| Smaller Players: 15% | Managers: 51% | Americas: 19% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where personal care and cosmetic output, formulation intensity, and region-level adoption of ester-based emollients are used to reconstruct the addressable demand pool, which is then priced using observed average selling price ranges. To keep the totals realistic, we check selective bottom-up approximations such as sampled supplier revenue splits, distributor channel checks, and a simple volume times ASP view for the most common ester families.

Key inputs that shape the model include the share of leave-on versus rinse-off products, the typical ester loading rates by formulation type, feedstock-linked price movement (fatty acids and fatty alcohols), the pace of natural and biodegradable ingredient substitution, and regional mix shifts led by skin care growth. Forecasting is done using scenario analysis, since pricing and mix can change when feedstock costs move quickly or when regulatory and claim trends shift purchasing behavior. When a direct data point is missing for a country or product niche, we bridge the gap using proxy indicators such as cosmetics production, trade flow direction, and expert-validated penetration ranges, and then we re-test the implied per-capita consumption before sign-off.

Data Validation & Update Cycle

Outputs are validated through multiple checks that look for mismatches between modeled demand and independent signals such as ingredient trade direction, announced capacity changes, and pricing ranges discussed by market participants. If an anomaly shows up, we review the assumption behind it, and then initiate follow-up outreach to re-confirm the variable that moved.

A multi-step internal review is completed before publication so that arithmetic, unit logic, and regional splits stay consistent across the model. Reports are refreshed annually, and interim updates are made when there are material events such as major feedstock shocks, supply disruptions, or notable regulatory shifts. Right before delivery, we run a fresh pass to ensure clients receive the most current view available.

Mordor Intelligence's Emollient Esters Market Size Compared Against Other Published Estimates

Published market numbers for emollient esters can look quite different, even when they appear to refer to the same ingredient space, because scope, pricing logic, and the year used for the base value are not always aligned. Differences also come from how firms treat neighboring ingredients, and whether values represent neat ingredient sales or broader formulation-level spending.

The biggest gap drivers in this market usually start with what is counted as an emollient ester versus a wider emollients basket, and then extend to how feedstock-linked ASP changes are applied through the forecast. Some estimates also shift the base year, use a more aggressive substitution story for natural emollients, or convert currencies using different timing, which changes the headline even if volumes are similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 632.37 M (2026) | |

| Global Consultancy A | USD 690.00 M (2026) | This figure appears to fold a broader emollients basket into the total, where silicones and other non-ester emollients are partially included, and then a single blended price path is applied across regions. |

| Industry Association B | USD 580.00 M (2025) | This estimate is anchored to an earlier base year and tends to rely on member-reported volumes with limited normalization for distributor markups and regional pricing dispersion. |

The spread in values is largely explained by whether adjacent emollient chemistries are included, and by how base-year pricing and currency timing are handled before the forecast is extended. Keeping the count limited to neat fatty acid and fatty alcohol esters used as emollient inputs, and then cross-checking totals with trade and pricing signals, is the approach applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current Emollient Esters Market size?

The emollient esters market size reached USD 632.37 million in 2026 and is projected to hit USD 780.61 million by 2031, reflecting a 4.30% CAGR.

Which region leads global demand?

Asia-Pacific commands the largest share at 34.62% in 2025 and is also the fastest-growing region, expected to record a 5.05% CAGR through 2031.

Which product category is expanding the fastest?

Caprylic/capric triglyceride is the fastest-growing product, forecast to rise at 5.38% annually to 2031 due to its multifunctional benefits.

What impact do feedstock price swings have on producers?

Volatile palm and coconut oil prices can compress margins by as much as 0.8 percentage points on forecast CAGR, prompting diversification and enzymatic processes to mitigate risk.

How are regulations shaping product development?

Stricter REACH and microplastic bans require reformulation toward biodegradable, bio-based esters, raising compliance costs but opening premium opportunities for sustainable suppliers.

Page last updated on: