Expandable Graphite Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Volume (2026) | 89.12 kilotons |

| Market Volume (2031) | 129.20 kilotons |

| Growth Rate (2026 - 2031) | 7.71% CAGR |

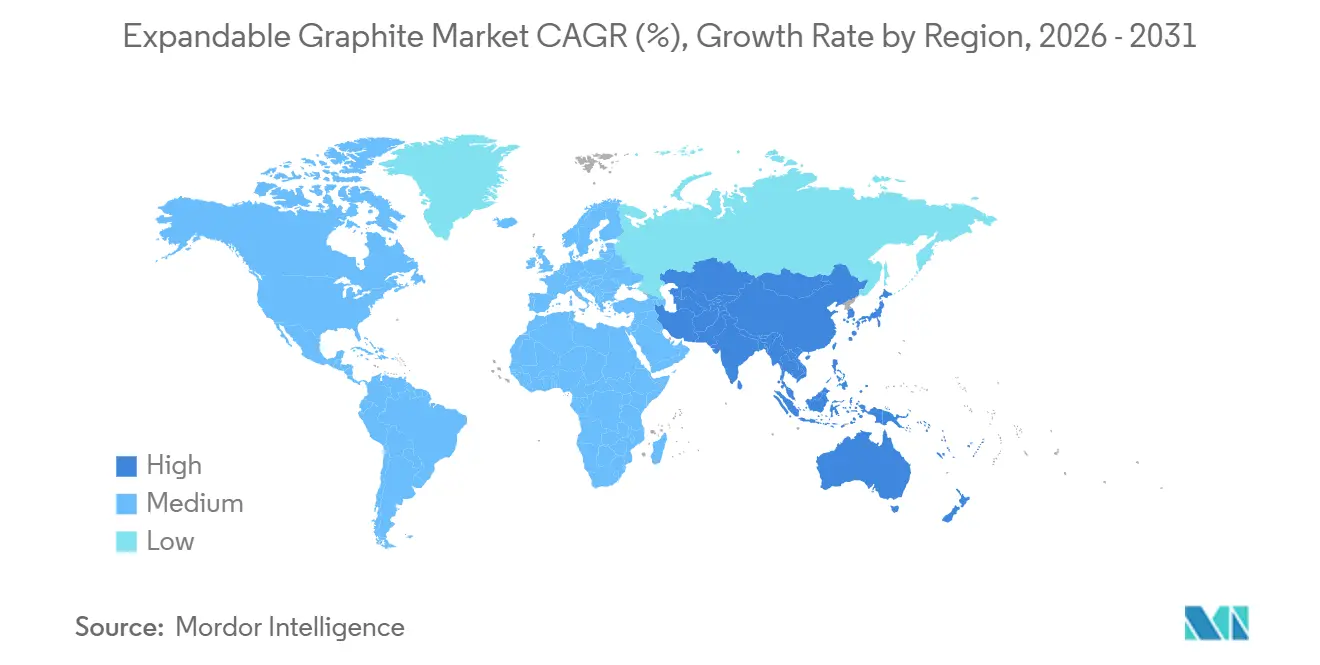

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

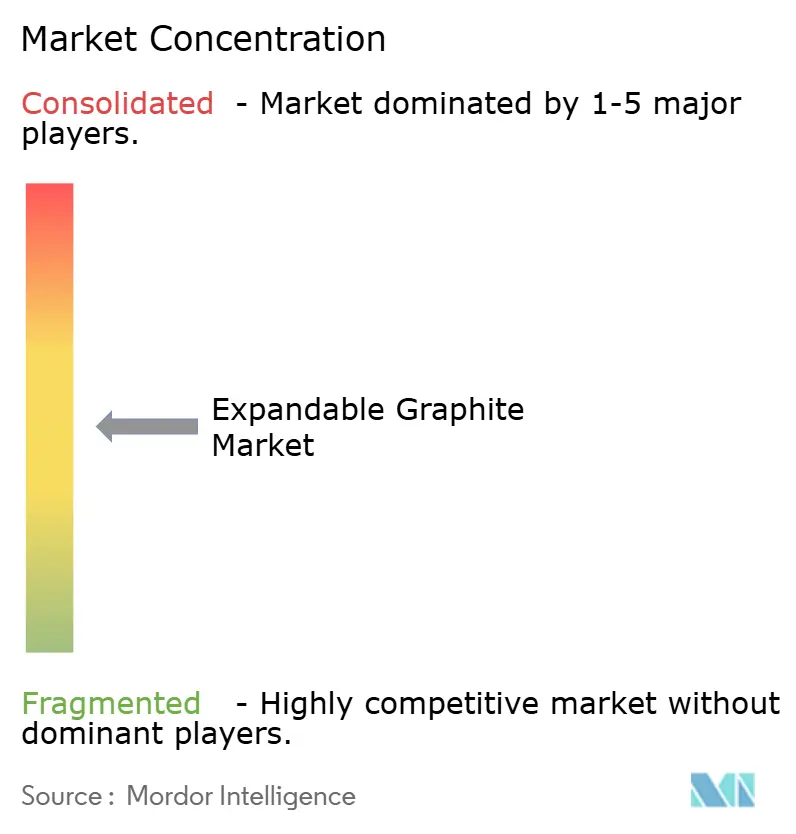

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Expandable Graphite Market Analysis by Mordor Intelligence

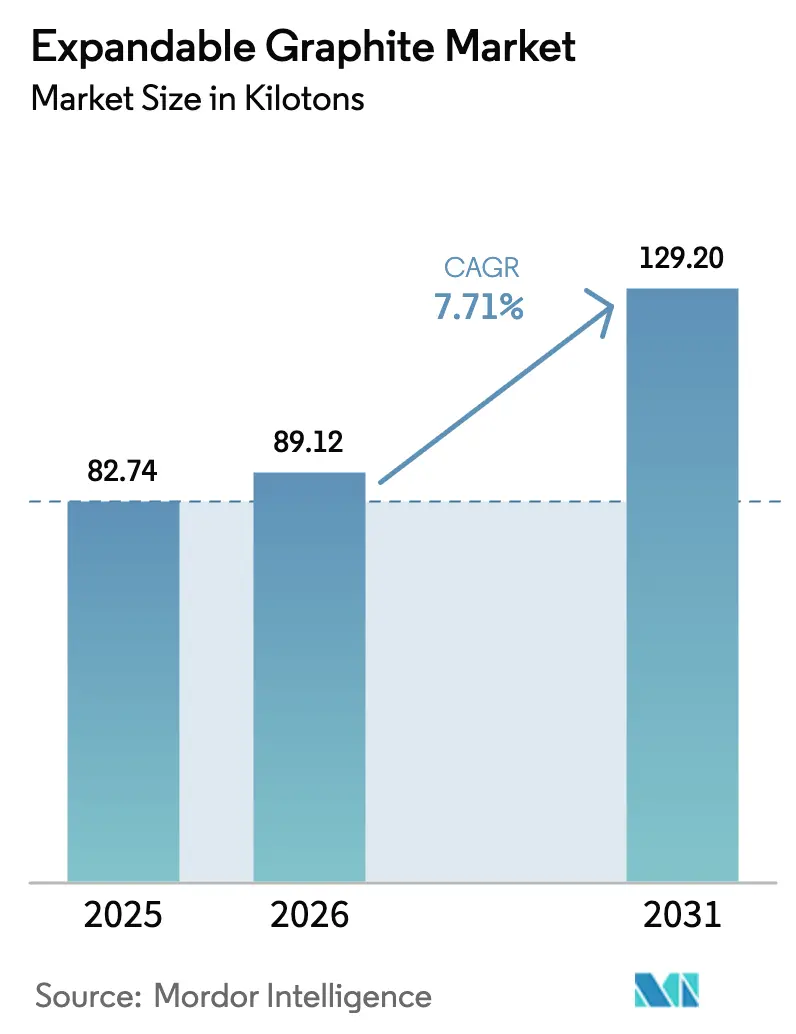

The Expandable Graphite Market size is expected to grow from 82.74 kilotons in 2025 to 89.12 kilotons in 2026 and is forecast to reach 129.20 kilotons by 2031 at a 7.71% CAGR over 2026-2031. Robust demand for halogen-free flame-retardant systems in electronics housings and high-rise construction, coupled with surging electric-vehicle (EV) battery thermal-management requirements, underpins this growth trajectory. Regulatory actions such as the European Chemicals Agency’s 2024 restriction on hexabromocyclododecane accelerate substitution toward expandable graphite char formers. Meanwhile, the International Energy Agency highlighted a 40% jump in battery-grade graphite demand in 2023, confirming the structural pivot from refractory uses to energy-storage and electronics applications. China’s December 2023 export controls on natural graphite further tightened global feedstock availability, prompting automakers and battery manufacturers to finance ex-China purification hubs that comply with the Inflation Reduction Act sourcing rules. Together, these shifts reinforce the positive outlook for the expandable graphite market.

Key Report Takeaways

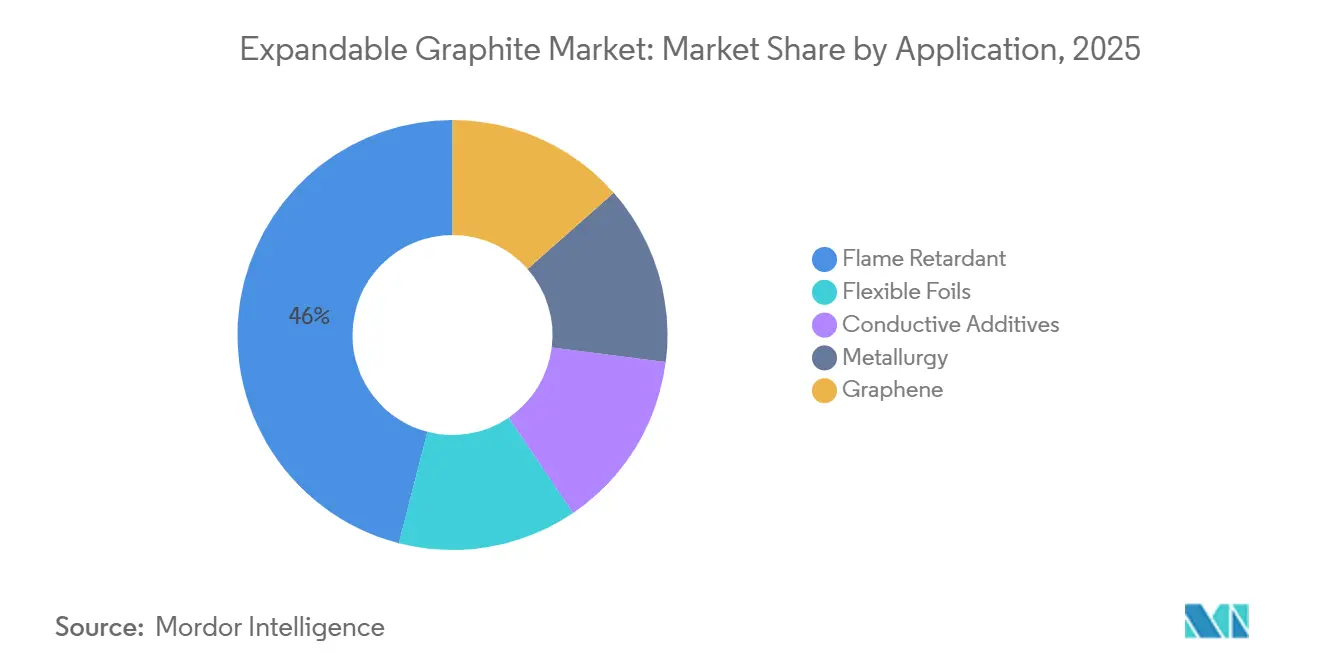

- By application, flame retardants led the expandable graphite market with 45.97% of the market share in 2025, and this segment is expected to advance at an 8.05% CAGR through 2031.

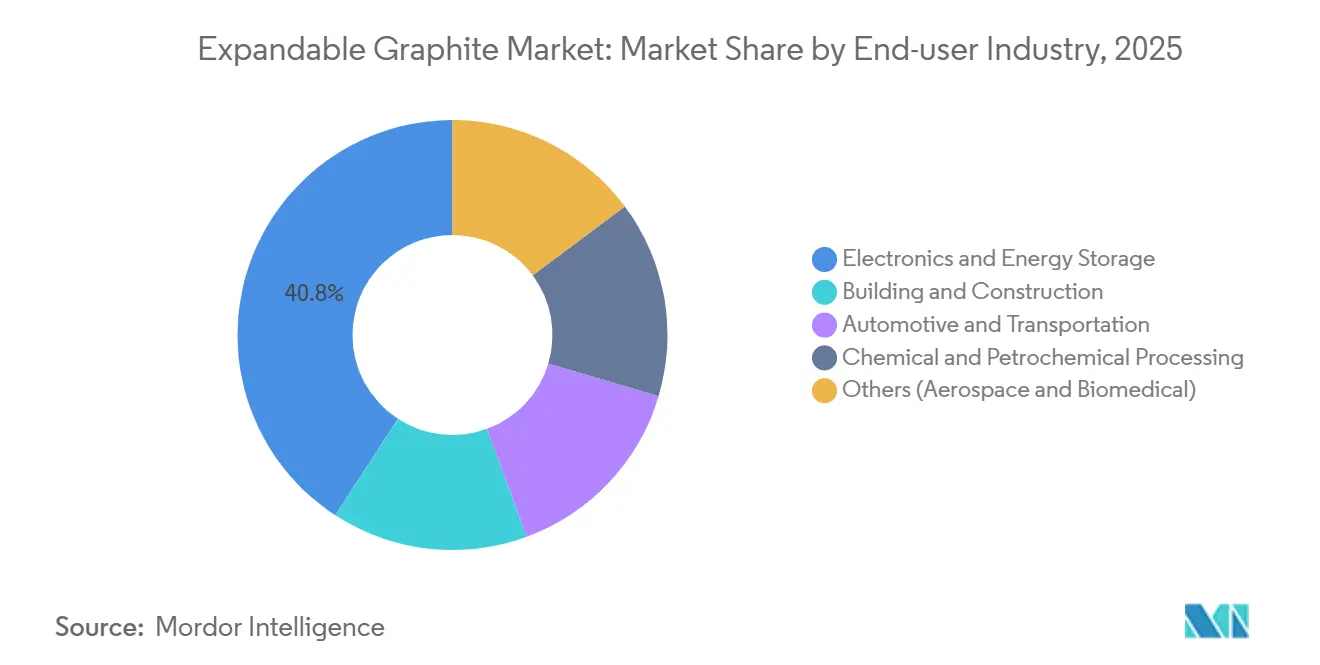

- By end-use industry, electronics and energy storage commanded a 40.82% share of the expandable graphite market size in 2025 and are expected to expand at an 8.46% CAGR through 2031.

- By region, the Asia-Pacific captured 57.51% of the volume in 2025 and is expected to register the fastest regional CAGR of 8.19% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Expandable Graphite Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Halogen-free flame-retardant adoption surge | +1.8% | Global, led by EU and North America | Medium term (2–4 years) |

| EV battery and thermal-management boom | +2.3% | Asia-Pacific core, spill-over to North America and EU | Long term (≥ 4 years) |

| Tightening global fire-safety codes | +1.2% | Global, strongest in EU and select Asia-Pacific markets | Short term (≤ 2 years) |

| Demand for high-conductivity foils in electronics | +1.5% | China, Japan, South Korea, United States | Medium term (2–4 years) |

| Next-generation intumescent products for 3D-printed parts | +0.9% | United States, Germany, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Halogen-free Flame-retardant Adoption Surge

Regulators on both sides of the Atlantic are phasing out brominated and chlorinated additives. The European Chemicals Agency finalized REACH Annex XVII restrictions on HBCDD in 2024, compelling formulators to pivot toward intumescent systems in polystyrene foams and polyurethane coatings[1]European Chemicals Agency, “Annex XVII Restriction on Hexabromocyclododecane,” echa.europa.eu. Similar momentum in California’s Proposition 65 list and ongoing US EPA reviews drives North American electronics OEMs toward expandable graphite grades that deliver expansion ratios above 250 mL/g. Because most REACH provisions entered force in mid-2024, demand for synergistic blends of expandable graphite and ammonium polyphosphate is now ramping quickly, particularly in wire-and-cable insulation and printed-circuit-board laminates. Germany and the Netherlands have already banned halogenated flame retardants in public infrastructure, yet cost-sensitive Southern European markets still favor legacy additives, suggesting a multi-year conversion window.

EV Battery and Thermal-management Boom

EV battery packs produce localized heat fluxes that aluminum or copper spreaders cannot dissipate without unacceptable mass penalties. Compressing expandable graphite into flexible foils achieves thermal conductivities above 300 W/m·K at densities below 1.9 g/cm³, supporting thinner interfaces between cylindrical or prismatic cells[2]SGL Carbon, “SIGRAFLEX Thermal Management Materials,” sglcarbon.com. The International Energy Agency projects that battery-grade graphite demand will quadruple by 2040 under net-zero scenarios, with thermal-management applications capturing an increasing slice. Automakers are qualifying expandable-graphite foils for cell-to-pack architectures in 800-volt systems, while Western OEMs finance domestic purification capacity, Graphite One’s Ohio facility is a prime example, to align with US sourcing incentives. This convergence of battery and thermal-management supply chains positions the expandable graphite market for durable expansion.

Tightening Global Fire-safety Codes

The International Code Council’s 2024 update to the International Building Code tightened flame-spread and smoke-development requirements for structures exceeding 75 ft, mandating intumescent coatings on steel columns and doors. Coatings loading 15%–20% expandable graphite can double fire-resistance ratings from 60 min to 120 min, meeting the revised thresholds without increasing dry-film thickness. Enforcement is rigorous in Singapore and Hong Kong, but less consistent in emerging Southeast Asian cities, resulting in uneven near-term uptake. The European Union’s Construction Products Regulation likewise requires CE marking and harmonized test reports, favoring suppliers that already possess ISO 9001 and EN 13501 data.

Demand for High-conductivity Foils in Electronics

Proliferation of 5G base stations, edge servers, and foldable phones intensifies thermal challenges in compact footprints. Flexible graphite foils manufactured through intercalation, high-temperature expansion, and calendaring offer in-plane conductivity above 400 W/m·K and can be die-cut to fit complex geometries. Japan’s graphite-sheet market grew from USD 200 million in 2022 to an estimated USD 400 million by 2030, reflecting strong domestic handset and semiconductor output. Semiconductor packaging already specifies graphite foils between chiplets and integrated heat spreaders, while synthetic foils command premium pricing because of lower thermal-expansion mismatch with silicon.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply constraints in jumbo-flake graphite | -1.1% | Global, acute in battery-grade processing | Short term (≤ 2 years) |

| Price volatility of flake and reagents | -0.8% | Asia-Pacific, North America | Medium term (2–4 years) |

| Stricter wastewater and acid-emission rules | -0.6% | North America, EU, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Constraints in Jumbo-flake Graphite

Expandable graphite relies on +80 mesh jumbo flake, which represents less than 15% of natural-graphite output and commands premiums of 30%–50% over finer grades. China dominates reserves in Heilongjiang and Inner Mongolia, yet environmental inspections and output quotas capped production growth below 5% after 2024. The United States remains fully import-reliant, sourcing 43% of its supply from China in 2024. New capacity in Mozambique’s Balama and Tanzania’s Epanko projects offers alternatives, but logistics challenges, port congestion, and irregular rail services inflate costs by up to 15%, constraining supply for flame-retardant and foil producers.

Price Volatility of Flake and Intercalation Reagents

A steep 2023 price drop for flake graphite, followed by stabilization near USD 1,100 per tonne in 2024, sowed procurement uncertainty. Intercalation uses sulfuric or nitric acid, commodities whose prices correlate with refinery capacity; Asian sulfuric-acid prices spiked 20% in mid-2024 after outages in South Korea. Large integrated players that secure captive acid or synthetic-graphite routes mitigate exposure, but most mid-tier firms absorb volatility through inventory adjustments. Absent a liquid futures market, expandable-graphite buyers rely on fixed-price contracts that merely redistribute, rather than remove, price risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Flame Retardants Drive Volume, Foils Capture Premium

Flame-retardant compounds accounted for 45.97% of the 2025 volume and are projected to expand at 8.05% to 2031. This dominant position stems from regulatory bans on brominated additives and the ability of expandable graphite to deliver intumescence at 15%–25% loading levels, easily achieving UL 94 V-0 ratings. Flexible foil applications, while representing a smaller slice of the expandable graphite market size, command 3–5 times higher pricing because of demanding purity and calendaring specifications. Foil growth lags at roughly 6.5% but benefits from rising EV thermal-management and semiconductor packaging deployments.

Conductive additives for lithium-ion electrodes and polymer composites are the fastest-growing niche, driven by energy-storage expansion and a need for lightweight conductive fillers in electric-vehicle components. Metallurgy applications, once the primary outlet for natural graphite, now contribute a modest share as steelmakers shift to synthetic carbons with tighter particle-size distributions. Experimental graphene production from expandable graphite remains commercially immature because yields are below 10% and solvent costs are high.

By End-use Industry: Electronics and Energy Storage Outpace Construction

Electronics and energy storage absorbed 40.82% of 2025 demand and will advance at an 8.46% CAGR through 2031, a trend rooted in 5G rollouts, battery proliferation, and device miniaturization that mandates advanced thermal-interface materials. Building and construction records a slower CAGR, reflecting cyclical residential activity and uneven adoption of halogen-free coatings outside Northern Europe.

Automotive and transportation applications are expanding as Euro 7 emission norms and EV platform shifts prioritize lightweight, high-temperature gasket solutions that include flexible graphite. Chemical processing remains a stable but low-growth end-market characterized by long replacement cycles in refineries and petrochemical plants. Aerospace and biomedical opportunities are still embryonic, yet could accelerate once additive-manufactured parts and implantable devices clear regulatory hurdles.

Geography Analysis

Asia-Pacific commanded 57.51% of 2025 volume and is forecast to grow at 8.19% to 2031, cementing its leadership in the expandable graphite market. Qingdao’s cluster of Heilong, Jinhui, Yanxin, and Mingheda leverages proximity to jumbo-flake mines and mature sulfuric-acid supply chains, producing as much as 70% of global expandable-graphite output. China’s December 2023 export license regime incentivized local offtake, tightened external supply, and nudged Western buyers to diversify. Japan and South Korea focus on high-purity foils; Japan’s graphite-sheet market will double to USD 400 million by 2030 as smartphone and semiconductor output climbs. India’s Production-Linked Incentive scheme spurs Tirupati Graphite’s Sagar project, aimed at 10,000 tonnes per year by late 2026.

North America's market share should grow substantially as OEMs align with the Inflation Reduction Act sourcing rules. Graphite One’s USD 435 million Ohio processing plant, set for late 2026 completion, targets 25,000 tonnes of synthetic anode and expandable graphite, leveraging an 85-acre site with multimodal logistics. Although Canada investigates Quebec and Ontario deposits, commercial extraction remains years away, preserving near-term import reliance. Mexico’s automotive wire-harness market illustrates demand growth for halogen-free flame retardants in the regional supply chain.

Europe’s market share volume is led by Germany, France, and the United Kingdom. The EU Construction Products Regulation mandates EN 13501-certified intumescent coatings, elevating barriers for entrants lacking accredited test data. Scandinavian retrofit subsidies for energy-efficient buildings drive halogen-free insulation uptake, whereas Southern Europe remains price sensitive. Eastern European demand rises in renewable-energy cable installations financed by EU cohesion funds.

Competitive Landscape

The Expandable Graphite market is moderately concentrated. SGL Carbon and NeoGraf use in-house synthetic-graphite routes to sidestep jumbo-flake shortages, sustaining gross margins 5–8 percentage points above competitors reliant on merchant feedstock. Chinese firms compete on cost; however, new wastewater rules and export licensing narrow their traditional advantage. Government-backed entrants add competitive pressure. The US Department of Defense funded feasibility studies for domestic intercalation under the Defense Production Act, and Graphite One’s Ohio complex illustrates this policy-driven capacity build-out.

Expandable Graphite Industry Leaders

SGL Carbon

NeoGraf Solutions LLC

Nacional de Grafite

Yichang Xincheng Graphite Co., Ltd.

Qingdao Jinhui Graphite Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Australian mining firm International Graphite teamed up with Arctic Graphite and Graphite Investment Partners (GIP) to set up a state-of-the-art expandable graphite production facility in Germany. Scheduled to commence operations in 2027, the facility is expected to produce 3,000 tons annually.

- January 2025: Evion, an Australian graphite producer, in collaboration with Indian firm Metachem Manufacturing, announced the inaugural shipments of its expandable graphite, set for this month in Pune, India.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the expandable graphite market as all grades of natural-flake graphite that have been chemically intercalated to expand at temperatures above 250 C and are then sold for downstream use in flame-retardant plastics, flexible foils, conductive additives, metallurgy aids, and graphene precursors.

Scope exclusion: synthetic or isotropic graphite that is expanded only for battery anode material is not counted in this scope.

Segmentation Overview

- By Application

- Flame Retardant

- Flexible Foils

- Conductive Additives

- Metallurgy

- Graphene

- By End-use Industry

- Building and Construction

- Electronics and Energy Storage

- Automotive and Transportation

- Chemical and Petrochemical Processing

- Others (Aerospace, Biomedical)

- By Geography

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed mine managers in Heilongjiang, flame-retardant compound formulators in Germany, electronics thermal-foil converters in South Korea, and procurement leads at North American gasket makers. Their insights validated dosage rates, regional price spreads, and realistic adoption curves that secondary sources alone could not reveal.

Desk Research

We built the baseline with open data drawn from tier-1 sources such as China Customs export statistics for flake graphite, Eurostat flame-retardant chemical trade tables, the U.S. Geological Survey Mineral Commodity Summaries, and fire-safety building code updates from the EU and China. Company 10-Ks, investor decks, patent families accessed through Questel, and periodic price assessments from Asian Metal added cost and capacity context. In parallel, production quotas and license data released by China's Ministry of Commerce after the December 2023 export-permit rule were trended to map likely supply tightening.

These references illustrate the breadth of desk work; dozens of additional public records, trade journals, and paid databases were reviewed to corroborate every datapoint.

Market-Sizing & Forecasting

We anchored demand by reconstructing production and trade flows (top-down) before cross-checking with sampled converter throughput and average selling price x volume roll-ups (bottom-up). Key model inputs include: a) new floor-space completions subject to non-halogen fire codes, b) average expandable-graphite loading per m2 of insulation board, c) consumer-electronics thermal-foil shipments, and d) export-permit approval rates. A multivariate regression links these drivers to historical volume, while scenario analysis adjusts for substitute flame retardants and price elasticity. Data gaps in small-flake metallurgy use were bridged through ratio analysis against output.

Data Validation & Update Cycle

Every draft output passes three-layer variance checks, peer review, and senior sign-off. Models are refreshed yearly, with interim updates triggered by events such as regulatory bans or major mine restarts. A last-minute sweep is completed before client delivery to ensure the freshest view.

Why Mordor's Expandable Graphite Baseline Earns Trust

Published figures often diverge because firms mix value and volume, bundle adjacent graphite grades, or rely on untested cost mark-ups.

Key gap drivers include differing scope (some omit conductive additives), currency and ASP assumptions, refresh cadence, and whether China's export-license rule is fully factored into 2025 supply.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 88.06 kilotons (2025) | Mordor Intelligence | - |

| USD 0.29 billion (2025) | Global Consultancy A | Revenue only; excludes metallurgy and graphene niches |

| USD 353.19 million (2024) | Trade Journal B | Uses mixed expanded + intercalated powders; unclear geographic split |

| USD 235.95 million (2024) | Industry Association C | Omits Asia small-flake segment; relies on pre-ban Chinese export data |

Taken together, the comparison shows that Mordor's disciplined scope definition, dual-track sizing logic, and annual refresh yield a balanced baseline that decision-makers can replicate and audit with confidence.

Key Questions Answered in the Report

What is the current size of the expandable graphite market?

What is the current size of the expandable graphite market?

Which application segment leads demand for expandable graphite?

Which application segment leads demand for expandable graphite?

Why is Asia-Pacific dominant in expandable graphite supply?

Why is Asia-Pacific dominant in expandable graphite supply?

How are EV trends influencing expandable graphite use?

How are EV trends influencing expandable graphite use?

What regulatory actions are driving halogen-free adoption?

What regulatory actions are driving halogen-free adoption?

Page last updated on: