Europe Wire and Cable Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

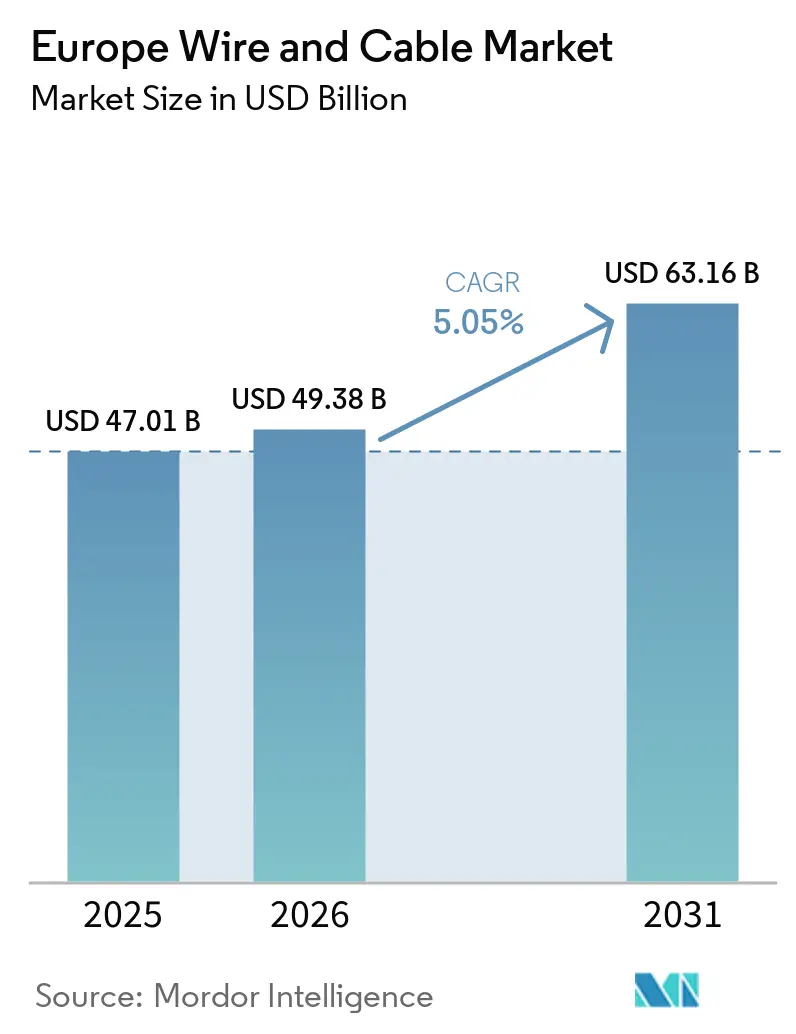

| Base Year Market Size (2025) | USD 47.01 Billion |

| Market Size (2026) | USD 49.38 Billion |

| Market Size (2031) | USD 63.16 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Wire and Cable Market Analysis by Mordor Intelligence

The Europe wire and cable market size is expected to be USD 47.01 billion in 2025, USD 49.38 billion in 2026, and reach USD 63.16 billion by 2031, growing at a CAGR of 5.05% from 2026 to 2031. Cable demand is pivoting toward extra-high-voltage subsea links and hybrid fiber systems as offshore wind, data-center build-outs, and pan-European grid upgrades displace the traditional dominance of commodity low-voltage products. HVDC projects such as TenneT’s Aurora Line, alongside ENTSO-E’s 108-gigawatt cross-border target, are accelerating specifications that emphasize 320-525 kilovolt ratings and polyethylene insulation certified for 50-year subsea service. At the same time, the construction sector’s retrofits sustain a sizable base for low-voltage energy cables, although its share is sliding as modular wiring grows. Fiber-optic demand is surging as 5G densification and hyperscale cloud nodes drive operators to pre-buy ribbon fiber and blown-fiber solutions, compressing lead times and pushing specialty telecom manufacturers toward dedicated lines. Commodity metal volatility remains a headline risk such as copper’s 2025 spot range of USD 8,500-10,200 per metric ton squeezed margins on fixed-price contracts, prompting manufacturers to hedge aggressively or shift to aluminum alloys.

Key Report Takeaways

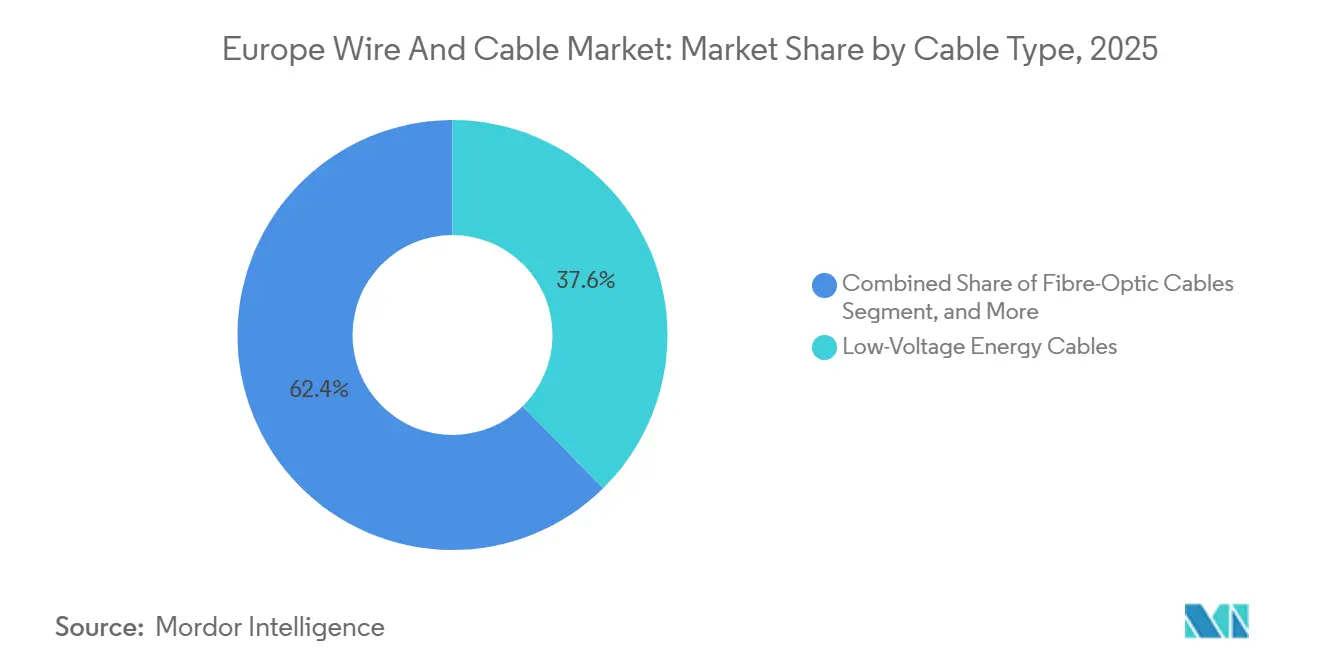

- By cable type, low-voltage energy cables led with 37.63% of Europe wire and cable market share in 2025, while fiber-optic cables are forecast to post a 5.99% CAGR through 2031.

- By voltage rating, cables at or below 1 kilovolt accounted for 39.62% share of the Europe wire and cable market size in 2025, whereas above-150-kilovolt systems are projected to expand at a 6.03% CAGR over 2026-2031.

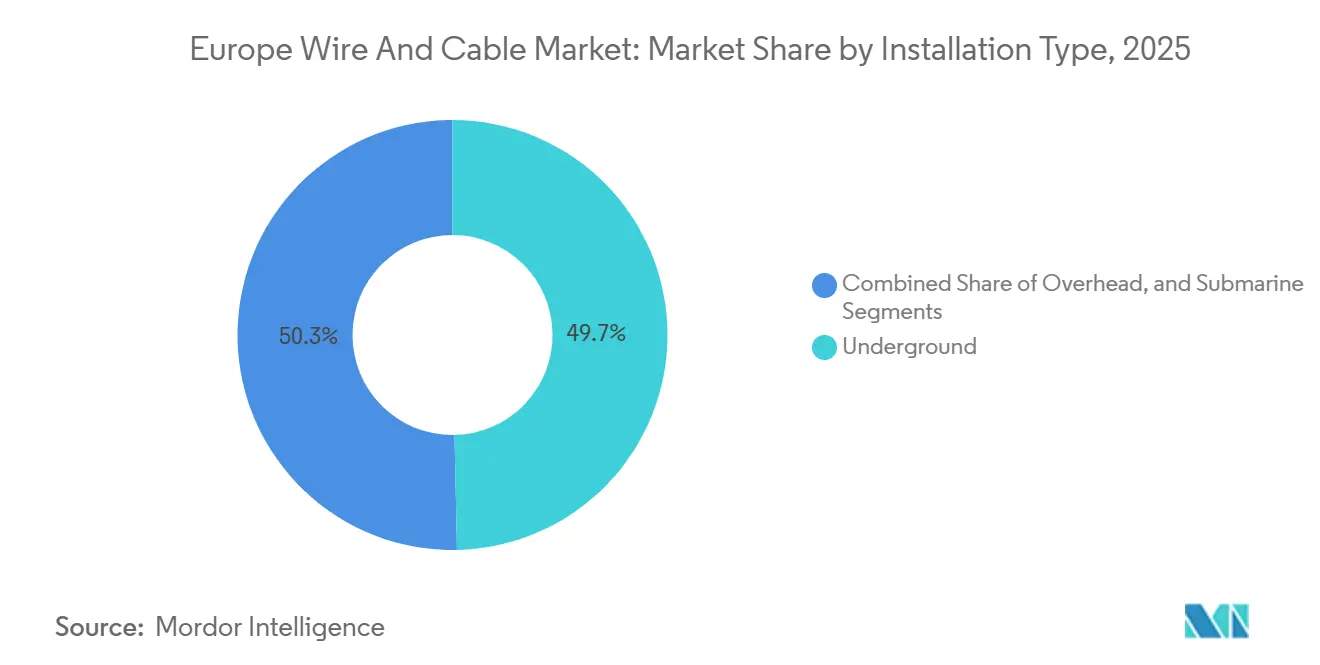

- By installation type, underground deployments held 49.72% of the Europe wire and cable market size in 2025 and submarine cables are advancing at a 6.34% CAGR through 2031.

- By conductor material, copper retained 57.62% share of the Europe wire and cable market size in 2025, but aluminum-alloy conductors are set to grow at 6.76% CAGR.

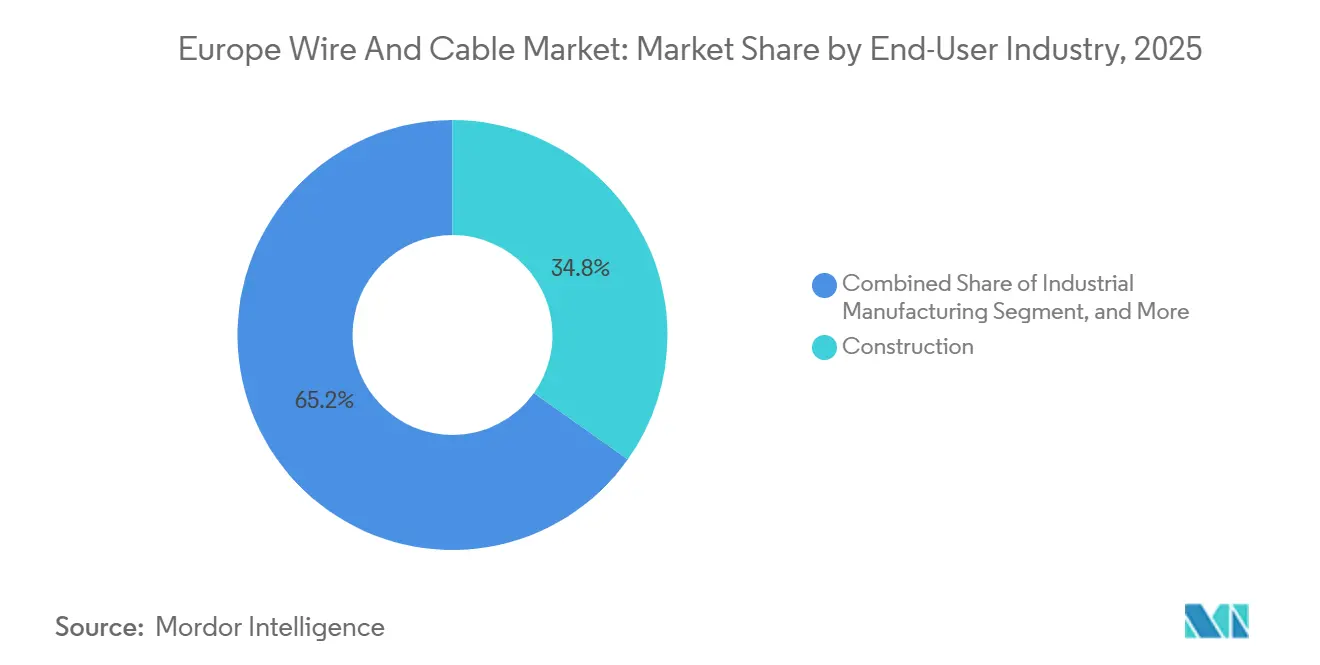

- By end-user industry, construction dominated with 34.84% of Europe wire and cable market share in 2025, while telecommunications and data centers are rising at a 6.56% CAGR.

- By geography, Germany commanded 29.40% of 2025 revenue of Europe wire and cable market, whereas Poland records the fastest outlook at a 6.90% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global valuation is built by aggregating outputs from multiple regions, with Europe forming one of the important contributors. Mordor Intelligence's global wire and cable market size report represents that cumulative total.

Europe Wire and Cable Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Renewable-Power Cable Demand | +1.2% | Germany, Netherlands, Denmark, Poland, United Kingdom, Belgium, France | Long term (≥ 4 years) |

| Grid-Modernization and HV Upgrade Programs | +1.0% | Germany, France, Italy, Spain, Poland | Medium term (2-4 years) |

| 5G and Fiber-to-the-Home Rollout | +0.7% | Germany, France, Spain, Poland, Netherlands | Short term (≤ 2 years) |

| EU Recovery Fund-Fueled Undergrounding | +0.6% | Italy, Spain, Poland, Greece, Portugal, France, Germany | Medium term (2-4 years) |

| EV-Charging-Infrastructure Fire-Safety Cables | +0.4% | Germany, France, Netherlands, Norway, Sweden, United Kingdom | Short term (≤ 2 years) |

| EU Digital Product Passport Traceability | +0.2% | Pan-European starting in Germany, France, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Renewable-Power Cable Demand

Offshore wind’s expansion is reshaping requirements for the Europe wire and cable market. The North Sea Wind Power Hub feasibility update outlines 180 gigawatts of artificial-island capacity that will need more than 3,000 kilometers of 320-kilovolt export cable, a specification only a handful of suppliers can meet.[1]North Sea Wind Power Hub, “Feasibility Study Update 2024,” NORTHSEAWINDPOWERHUB.EU Denmark’s Bornholm Energy Island alone will secure EUR 650 million (USD 709 million) in contracts by 2030, requiring polyethylene insulation certified for 50 years subsea.[2]Danish Energy Agency, “Bornholm Energy Island Project,” ENS.DK Onshore solar farms in Spain and Italy add medium-voltage volume, yet the highest inflection point lies in hybrid renewable-plus-storage arrays that require low-smoke, halogen-free, fire-resistant cables that meet IEC 60332. With transmission operators pre-booking capacity years in advance, leading manufacturers such as Prysmian, Nexans, and NKT are stretching lead times, while niche suppliers of specialty insulation capture premium margins. Sustained order backlogs confirm that renewables will underpin cable demand beyond 2030, cushioning the sector against construction cyclicality.

Grid-Modernization and HV Upgrade Programs

Transmission system operators have earmarked EUR 584 billion (USD 637 billion) for reinforcement through 2030, with Germany’s Amprion alone planning EUR 42 billion (USD 45.8 billion) in underground HVDC corridors that quintuple per‐kilometer cable costs but sidestep permitting delays. France’s RTE is replacing 1,200 kilometers of 225 kilovolt lines with cross-linked polyethylene variants by 2028, while Spain and Italy channel recovery funds into medium-voltage undergrounding. The strategic result is a steady pull on capacity across the Europe wire and cable market, locking in large contracts years before installation. Utilities are aggregating demand into multi-year frameworks, incentivizing manufacturers to expand extra-high-voltage lines and prioritize long-lead insulation materials. If supply tightens, smaller projects risk slippage, creating a bifurcated market in which large interconnectors progress while municipal upgrades wait.

5G and Fiber-to-the-Home Rollout

Fiber household penetration reached 56% in 2025 and still trails the European Commission’s 95% gigabit aspiration, requiring another 2.8 million kilometers of cable by 2030.[3]European Commission, “Gigabit Infrastructure Act Progress Report 2025,” EC.EUROPA.EU Germany earmarked EUR 12 billion (USD 13.1 billion) for subsidies that have driven blown-fiber deployments, able to cut installation time by 40%. Hyperscale data centers in Frankfurt, Amsterdam, and Dublin consumed around 180,000 kilometers of multi-mode fiber in 2025, pushing suppliers to dedicate production solely for cloud operators. Mobile carriers are densifying 5G small cells, each of which requires fiber backhaul, lifting metro-area demand by up to 30%. These converging trends are elevating fiber optics from a telecom niche to a fundamental pillar of the Europe wire and cable market, set to outgrow every other cable type through 2031.

EU Recovery Fund-Fueled Undergrounding

The EUR 750 billion (USD 818 billion) NextGenerationEU package diverted a substantial slice to green grid projects, compressing typically scattered undergrounding programs into a tight 2024-2026 window. Italy’s plan allocates EUR 5.9 billion (USD 6.44 billion) for medium-voltage lines in seismic zones, while Spain’s program supports 1,200 kilometers of 20 kilovolt cables in rural districts. Poland allocates EUR 1.8 billion (USD 1.96 billion) toward undergrounding urban infrastructure to replace aging overhead infrastructure. Because subsidies expire if projects are not contracted by mid-2026, distribution operators have accelerated tender schedules, straining factory output and bringing production slots forward. The surge temporarily inflates backlog visibility for manufacturers, yet once funds sunset, demand could normalize, reopening capacity for private industrial customers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Copper and Aluminum Prices | -0.8% | Pan-European, with acute impact in Germany, Italy, France, Spain | Short term (≤ 2 years) |

| High Underground and Subsea Installation Costs | -0.6% | United Kingdom, Germany, Netherlands, Denmark, Belgium for subsea; Italy, Spain for underground | Medium term (2-4 years) |

| Tightened EU PFAS Restrictions on Fluoropolymers | -0.3% | Pan-European, phased enforcement starting 2026 | Long term (≥ 4 years) |

| Baltic Sea Security Risks Elevating Insurance Costs | -0.2% | Finland, Sweden, Poland, Germany, Denmark, Estonia, Latvia, Lithuania | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Copper and Aluminum Prices

Copper’s 2025 spot range erased as much as half of gross margin on low-voltage fixed-price deals, forcing larger manufacturers to hedge and smaller players to absorb hits or renegotiate. Prysmian absorbed a EUR 180 million (USD 196 million) hedge loss, illustrating the scaling difficulty of commodity exposure. While aluminum alloy offers 92% of copper’s conductivity at one-third the cost, larger cross-sections and heavier armoring limit its universal substitution. As price swings remain unpredictable, forward-buying and material diversification are now routine boardroom topics across the Europe wire and cable industry.

High Underground and Subsea Installation Costs

Average subsea installation expenses reached EUR 1.8 million (USD 1.96 million) per kilometer in 2025, doubling in rocky seabeds.[4]Nexans, “Subsea Cable Installation Costs,” NEXANS.COM Insurance premiums spiked 15-20% after Baltic sabotage incidents severed Estlink 2 and adjoining optical fibers. Urban trenching costs near EUR 1.2 million (USD 1.31 million) per kilometer once archaeological and traffic constraints are met, and Italy’s seismic codes add another 15% for flexible conduits. These economics slow adoption in budget-sensitive municipalities, tempering the submarine segment’s otherwise promising growth trajectory in the Europe wire and cable market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cable Type: Fiber Optics Extend Growth Leadership

Fiber-optic cables recorded the fastest expansion within the Europe wire and cable market, growing at a 5.99% CAGR through 2031. Low-voltage energy products preserved a dominant 37.63% share in 2025, but shifting building codes and pre-wired modular construction are curbing their growth. The Europe wire and cable market size attributable to fiber optics is expected to exceed USD 11 billion by 2031, spurred by mandatory gigabit coverage and hyperscale data centers. Energy cables will still serve residential retrofits, yet the value pool is migrating to ribbon fiber, loose-tube outdoor variants, and specialty fire-resistant designs rated to IEC 60332.

Premium subsea HVDC systems further narrow supplier pools, channeling orders to vertically integrated giants with extrusion capacity for 320-640 kilovolt polymer-insulated cores. Signal and control cables see stable industrial demand, particularly in rail electrification and factory automation, but remain a mid-single-digit niche. Specialty halogen-free cables for EV charging stations are capturing high-margin demand as urban parking regulations tighten across Germany and France, adding resilience to the segment mix.

By Voltage Rating: Ultra-High Voltage Captures Premium Share

Cables above 150 kilovolts post the strongest 6.03% CAGR as grid planners favor HVDC corridors to ship offshore wind to inland load centers. The Europe wire and cable market share for sub-1 kilovolt lines stood at 39.62% in 2025, yet utilities' focus on transmission expansion directs capex toward 220-525 kilovolt specifications. Cross-linked polyethylene insulation is displacing legacy oil-filled designs in the 36-150 kilovolt band, which maintains a stable mid-30s share.

While household electrification moderates in Western Europe, the 1-35 kilovolt category benefits from solar-farm connections that each require up to 12 kilometers of feeder cable. EU TEN-E rules favor interconnectors above 220 kilovolts for subsidies, steering incremental funds to the ultra-high-voltage end. Suppliers capable of producing 525 kilovolt P-Laser or equivalent solid-dielectric designs command pricing power and extended backlogs.

By Installation Type: Submarine Systems Accelerate

Underground cabling accounted for 49.72% of 2025 demand, striking a balance between urban resilience and manageable installation costs. Submarine deployments will expand at a 6.34% CAGR, catalyzed by North Sea and Baltic offshore projects that require 50-year design life and robust armoring against trawler gear. Overhead replacements persist in rural zones but are largely restricted to refurbishment programs instead of new builds as public opposition and visual-impact concerns mount.

Next-generation cable-laying vessels such as Nexans Aurora improve installation speed and lower risk, yet geopolitical tensions in the Baltic Sea inflate insurance by up to 20%, feeding directly into project budgets. Groundbreaking micro-trenching and horizontal directional drilling modes are shaving urban underground installation costs by up to 40%, making buried lines more attractive on a lifecycle basis than overhead schemes prone to weather outages.

By Conductor Material: Aluminum Alloys Outpace Copper

Aluminum-alloy variants are projected to grow at 6.76% CAGR through 2031, gaining share in overhead and submarine segments of the Europe wire and cable market. The extended rally in copper prices above USD 9,000 per metric ton encouraged transmission operators to specify aluminum alloys for lines above 150 kilovolts. Still, copper holds a 57.62% share owing to low-voltage applications where conductor cross-section is constrained, and contractors are accustomed to copper’s mechanical handling.

Alloy 8000-series strands deliver nearly identical conductivity at a third of the metal cost, though thicker insulation and armoring increase the overall cable diameter by about 10-15%. Sustainability metrics add momentum such as aluminum production emits 40% less CO₂ per kilogram than copper, an advantage utilities now count toward net-zero commitments. As carbon reporting tightens, material substitution could accelerate despite aluminum’s higher resistive losses on long runs.

By End-User Industry: Telecom and Data Centers Surge Ahead

Telecommunications and data centers are the fastest-growing end-user vertical, poised for a 6.56% CAGR as cloud providers lock in fiber and power cable volumes years in advance. Construction led with 34.84% of the Europe wire and cable market size in 2025, but its trajectory moderates as Western housing plateaus and renovation overtakes new build. Utilities and power infrastructure maintain a mid-20s share on the back of grid-modernization budgets, while industrial automation’s migration to wireless protocols tempers its reliance on cables.

Hyperscale expansions in the Frankfurt-Amsterdam-Dublin corridor alone consumed 180,000 kilometers of fiber in 2025, pushing manufacturers to reserve capacity exclusively for cloud operators. EV charging infrastructure also underpins specialty fire-resistant cable demand, with Germany’s 1 million public charging points target equating to a 50,000-60,000 kilometer requirement for halogen-free cable.

Geography Analysis

Germany retained a 29.40% share of the Europe wire and cable market in 2025, driven by reinforcement of the Energiewende, entrenched industrial wiring needs, and an outsized share of continental data-center traffic. Amprion’s EUR 42 billion (USD 45.8 billion) HVDC program pushes underground volumes, and TenneT’s 525 kilovolt Aurora Line provides follow-on orders as renewables saturate alternating-current corridors. Copper and polymer supply bottlenecks slightly slowed project schedules, yet German suppliers capitalize on geographic proximity and familiarity with compliance to defend market share.

Poland ranks as the fastest-growing geography, projected to grow at 6.90% CAGR through 2031. EU cohesion funds subsidize distribution upgrades, and NKT’s 180-kilometer Gennaker subsea export route unlocks Baltic wind resources, channeling heavy HVDC investment toward Polish yards. The national broadband plan’s 95% fiber target will need 150,000 kilometers of fiber, further lifting demand. Domestic producers are expanding extrusion lines to hedge currency moves and shorten import cycles.

France, the United Kingdom, Italy, and Spain each hold mid-single-digit slices but host pivotal projects. France’s 1,200 kilometer undergrounding initiative sustains steady cross-linked polyethylene intake, while the United Kingdom’s offshore pipeline, including Dogger Bank phases, keeps submarine backlogs healthy. Italy’s seismic retrofitting incentives continue to favor flexible conduits, and Spain’s rural electrification supports medium-voltage tenders, particularly at Iberdrola. Smaller markets such as Netherlands and Belgium exceed weight in specialty halogen-free and sensor-embedded cable niches thanks to tunnel and shipbuilding regulations that require extended fire integrity.

Coverage of the wire and cable market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for North America and South America, alongside detailed country-level intelligence for India and Mexico, each shaped by local operating conditions.

Competitive Landscape

The Europe wire and cable market is moderately concentrated around Prysmian, Nexans, and NKT, whose vertical integration spans polymer compounding, conductor drawing, and turnkey subsea installation. Prysmian’s 525 kilovolt P-Laser series transmits 2 gigawatts over 200 kilometers with under 3% loss, commanding a EUR 4.5 million (USD 4.91 million) per-kilometer premium for high-efficiency interconnectors. Nexans Aurora, a DP3-class vessel, enables single-lift installation of 70-ton segments, cutting offshore campaign durations and locking in multi-year capacity for North Sea developers. NKT’s focus on the Baltic Sea, highlighted by the completed Gennaker route, demonstrates turnkey competence under geopolitical pressure.

Fragmentation endures in low-voltage and specialty categories where regional players such as Helukabel, Lapp, Tratos, and Brugg Kabel leverage shorter lead times and local compliance expertise. Fire-resistant products for EV charging and tunnel safety, halogen-free hospital wiring, and sensor-embedded cables for real-time strain monitoring represent profitable micro-segments outsiders often overlook. Standards IEC 60840 and IEC 62067 act as gatekeepers for high-voltage entrants, though digital-twin-based type testing is beginning to compress certification timelines. Material innovation is a rising differentiator, with Prysmian’s microcapsule self-healing insulation patent suggesting 60-year lifespans that could reset total-cost-of-ownership benchmarks and prompt licensing deals or parallel chemistry R&D among rivals.

Geopolitical disruptions such as the 2024 Baltic sabotage led some utilities to diversify away from single-source suppliers, opening doors for mid-tier firms like Hellenic Cables and TKF to capture contingency contracts. Commodity hedging strategies, supply-chain transparency mandated by EU Digital Product Passports, and ESG scoring are additional vectors through which challengers can erode incumbent share in selected segments.

Europe Wire and Cable Industry Leaders

Prysmian S.p.A.

Nexans S.A.

NKT A/S

Leoni AG

TELE-FONIKA Kable S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Prysmian secured a EUR 850 million (USD 927 million) order for 240 kilometers of 320 kilovolt subsea cable for Poland’s Baltica 2 wind farm, Europe’s largest single cable contract to date.

- January 2026: Nexans committed EUR 120 million (USD 131 million) to add 50,000 kilometers of annual HVDC capacity at Halden, Norway, with completion slated for Q3 2027.

- November 2025: NKT delivered 180 kilometers of 220 kilovolt cable for Poland’s Gennaker route, the first large-scale Baltic export system.

- September 2025: TenneT awarded a EUR 680 million (USD 742 million) consortium contract for the Aurora Line extension, adding 200 kilometers of 525 kilovolt subsea cable by 2029.

Europe Wire and Cable Market Report Scope

The Europe Wire and Cable Market Report is Segmented by Cable Type (Low-Voltage Energy Cables, Medium-Voltage Cables, High-Voltage and EHV Cables, Fiber-Optic Cables, Signal and Control Cables, Specialty/Fire-Resistant Cables), Voltage Rating (Less or Equal to 1 kV, 1-35 kV, 36-150 kV, Above 150 kV), Installation Type (Overhead, Underground, Submarine), Conductor Material (Copper, Aluminum, Aluminum-Alloy), End-User Industry (Construction, Power Infrastructure and Utilities, Telecommunications and Data Centers, Industrial Manufacturing, Transportation, Other End-User Industries), and Geography (United Kingdom, Germany, France, Italy, Spain, Switzerland, Belgium, Netherlands, Poland, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Low-Voltage Energy Cables |

| Medium-Voltage Cables |

| High-Voltage and EHV Cables |

| Fiber-Optic Cables |

| Signal and Control Cables |

| Specialty / Fire-Resistant Cables |

| Less or Equal to 1 kV |

| 1–35 kV |

| 36–150 kV |

| Above 150 kV |

| Overhead |

| Underground |

| Submarine |

| Copper |

| Aluminum |

| Aluminum-Alloy |

| Construction (Residential and Commercial) |

| Power Infrastructure and Utilities |

| Telecommunications and Data Centers |

| Industrial Manufacturing |

| Transportation (Rail, EV, Marine) |

| Other End-User Industries |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Switzerland |

| Belgium |

| Netherlands |

| Poland |

| Rest of Europe |

| By Cable Type | Low-Voltage Energy Cables |

| Medium-Voltage Cables | |

| High-Voltage and EHV Cables | |

| Fiber-Optic Cables | |

| Signal and Control Cables | |

| Specialty / Fire-Resistant Cables | |

| By Voltage Rating | Less or Equal to 1 kV |

| 1–35 kV | |

| 36–150 kV | |

| Above 150 kV | |

| By Installation Type | Overhead |

| Underground | |

| Submarine | |

| By Conductor Material | Copper |

| Aluminum | |

| Aluminum-Alloy | |

| By End-User Industry | Construction (Residential and Commercial) |

| Power Infrastructure and Utilities | |

| Telecommunications and Data Centers | |

| Industrial Manufacturing | |

| Transportation (Rail, EV, Marine) | |

| Other End-User Industries | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Switzerland | |

| Belgium | |

| Netherlands | |

| Poland | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current and projected Europe wire and cable market size?

The Europe wire and cable market size stands at USD 49.38 billion in 2026 and is forecast to reach USD 63.16 billion by 2031, reflecting a 5.05% CAGR (Mordor Intelligence).

Which segment is growing fastest in the Europe wire and cable market?

Submarine cable installations are the fastest, advancing at a 6.34% CAGR on the back of North Sea and Baltic offshore wind export routes (Mordor Intelligence).

Why are aluminum-alloy conductors gaining share?

Aluminum-alloy strands cost roughly one-third of copper and emit 40% less CO₂ during production, prompting utilities to specify them for new overhead and some subsea lines despite larger cross-section requirements (Mordor Intelligence).

How does the 5G rollout influence cable demand?

5G densification needs dense fiber backhaul, driving additional orders for ribbon and blown-fiber cables that elevate fiber optics to the quickest-expanding cable type in the region (Mordor Intelligence).

What are the main risks to Europe’s submarine cable projects?

Elevated installation costs and higher insurance premiums driven by Baltic Sea security incidents have added up to 20% to project budgets, potentially delaying tender timelines (Mordor Intelligence).

Which countries will lead growth through 2031?

Poland leads with a 6.90% CAGR as cohesion funds, HVDC interconnectors, and nationwide fiber targets compress decades of infrastructure investment into a single decade.

Page last updated on: