Europe Surveillance Camera Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

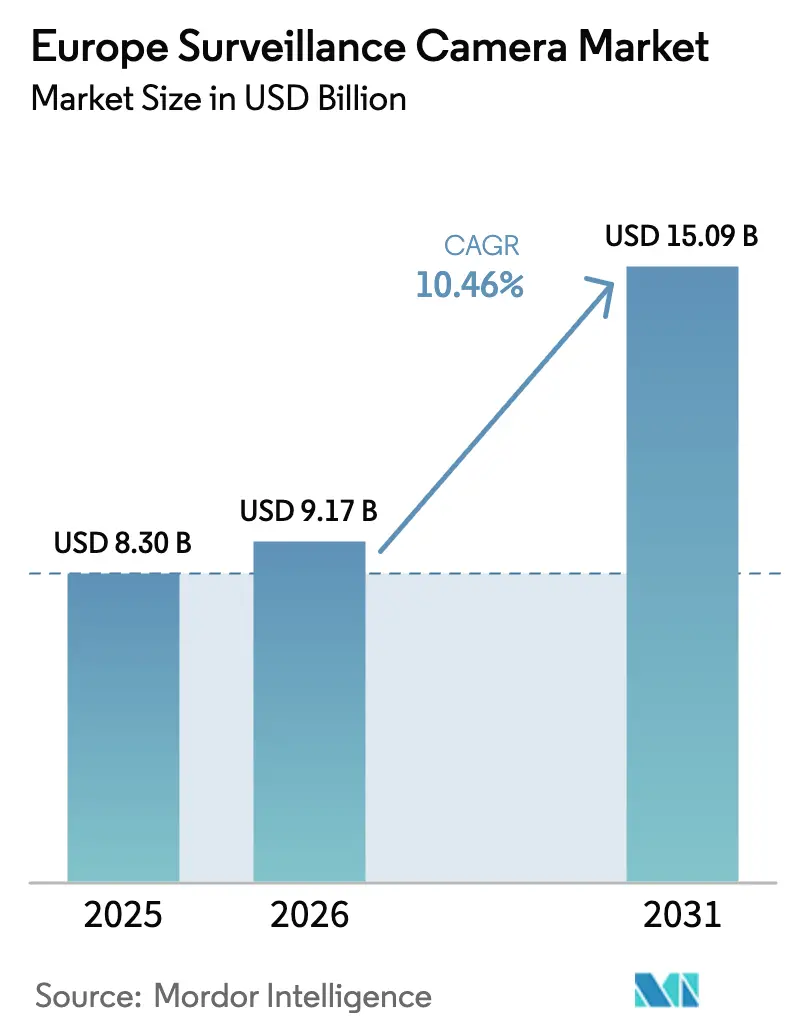

| Base Year Market Size (2025) | USD 8.30 Billion |

| Market Size (2026) | USD 9.17 Billion |

| Market Size (2031) | USD 15.09 Billion |

| Growth Rate (2026 - 2031) | 10.46% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Surveillance Camera Market Analysis by Mordor Intelligence

The Europe Surveillance Camera market size was valued at USD 8.30 billion in 2025 and estimated to grow from USD 9.17 billion in 2026 to reach USD 15.09 billion by 2031, at a CAGR of 10.46% during the forecast period (2026-2031). IP-based equipment already represents 68% of installed units and underpins most smart-city, retail analytics, and critical-infrastructure projects. Government authorities remain the largest customers and hold a 29% share thanks to city-wide CCTV networks, while transportation hubs are now procuring 4K/8K vision systems that feed predictive-maintenance algorithms. Fixed-box cameras dominate day-to-day monitoring, yet ruggedised outdoor variants—already 57% of shipments—are expanding quickly as municipalities harden public spaces against vandalism and weather. Wired Power-over-Ethernet links account for 61% of current deployments, but 5G-enabled wireless nodes are scaling faster because they eliminate trenching costs and support UHD backhaul. Country demand is led by the United Kingdom at 23% of regional revenue, whereas France is poised for the fastest growth as Olympic-driven crowd-management pilots spur large-scale rollouts.

Key Report Takeaways

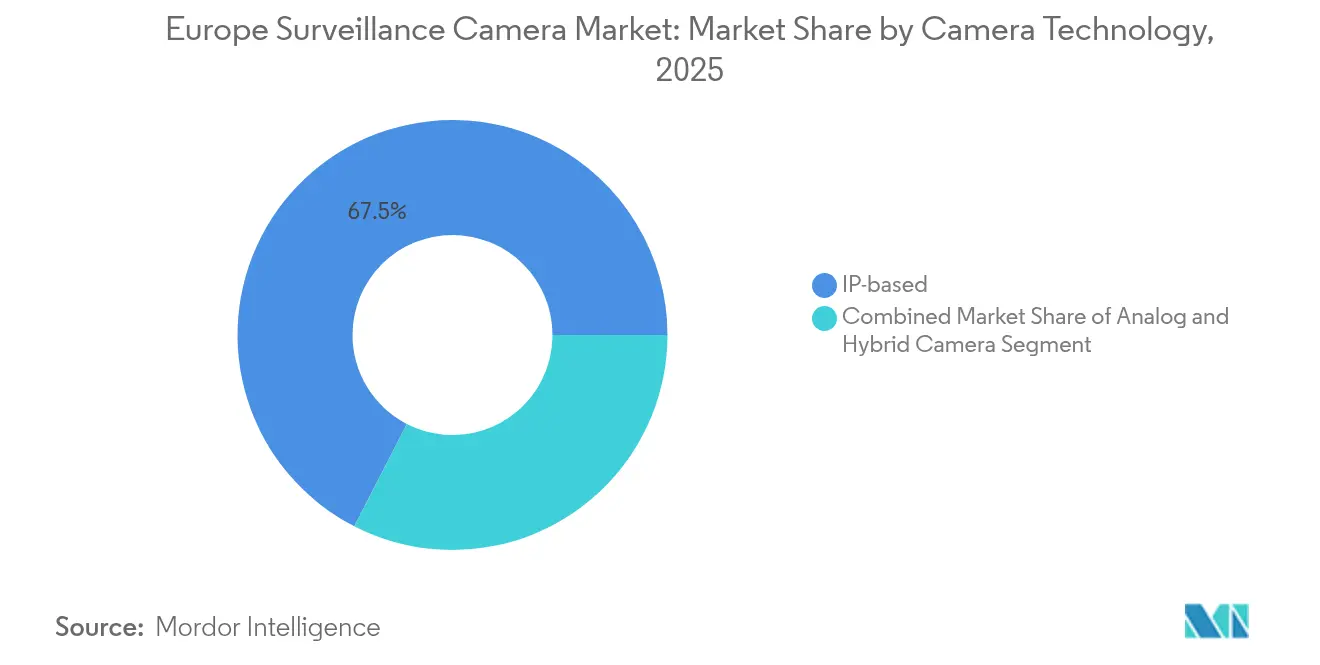

- By camera technology, IP-based systems led with 67.45% of Europe Surveillance Camera market share in 2025; hybrid architectures are projected to grow at an 11.05% CAGR to 2031.

- By end-user vertical, Government & Public Safety held 28.55% of Europe Surveillance Camera market share in 2025, while Transportation & Logistics is set for a 12.31% CAGR through 2031.

- By resolution, Full-HD (1080p) captured 46.05% share of the Europe Surveillance Camera market size in 2025; 4K & above formats are expected to climb at a 13.18% CAGR.

- By connectivity, wired (PoE/Ethernet) solutions dominated with a 60.25% share in 2025; wireless links will advance at a 13.95% CAGR to 2031.

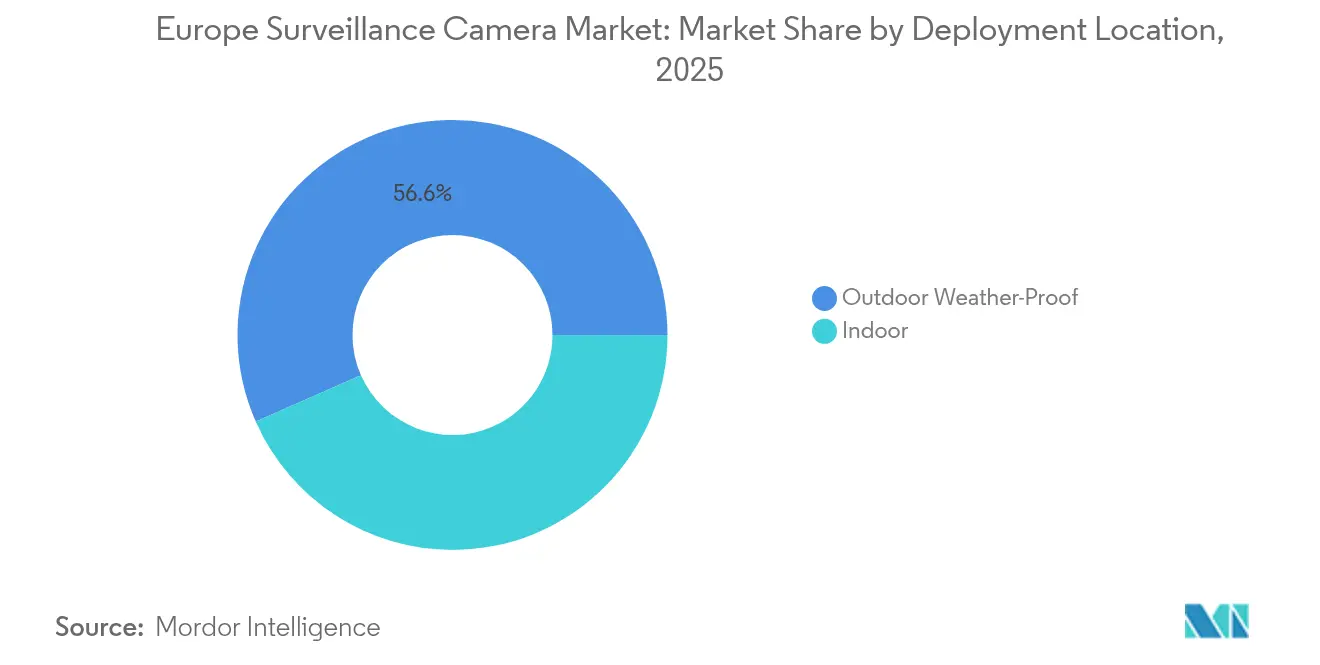

- By deployment location, outdoor systems represented 56.60% of units in 2025, and outdoor-ruggedised models are forecast to grow at a 12.15% CAGR.

- By camera form-factor, fixed-box designs held 41.40% share in 2025, whereas thermal & dual-spectral models are tracking a 13.55% CAGR.

- By country, the United Kingdom generated 22.70% of regional revenue in 2025; France is predicted to expand at a 13.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe contributes to a system defined not by any single geography but by the interaction of many. The global surveillance camera market data by Mordor Intelligence represents that combined structure.

Europe Surveillance Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Smart-City Surveillance Projects Accelerating IP Camera Installations | +2.3% | Western Europe and Nordic countries | Medium term (2-4 years) |

| GDPR-Compliant Edge Analytics Driving Upgrade Cycles | +1.8% | EU-wide, especially Germany, France, Benelux | Short term (≤ 2 years) |

| Adoption of 4K/8K Ultra-HD Cameras in Nordic Ports & Airports | +1.2% | Nordic cluster and major EU hubs | Medium term (2-4 years) |

| Shift from Capex to Surveillance-as-a-Service among European SMEs | +1.7% | EU-wide, strongest in UK, Germany, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU smart-city surveillance projects accelerating IP camera installations

Municipal initiatives earmark surveillance as a core pillar of digital-twin programmes. České Budějovice integrated 170+ Axis and Genetec units to manage traffic flows and emergency response, illustrating how open-platform devices feed transport, environmental and safety dashboards.[1]Axis Communications, “Axis Launches All-in-One Outdoor Bullet Camera,” securityworldmarket.comNordic capitals extend this model with 5G backbone networks that enable real-time AI analytics, turning cameras into multi-purpose sensors. Project tenders increasingly specify ONVIF-compliant streams and encrypted edge storage, nudging buyers toward IP hardware and supporting the 68% Europe Surveillance Camera market share already held by the category.

GDPR-compliant edge analytics driving upgrade cycles

The European Data Protection Supervisor’s 2024 report flags rising scrutiny of AI-enabled video, prompting organisations to replace record-only devices with edge-intelligent cameras that redact personal identifiers before export.[2]European Data Protection Supervisor, “Annual Report 2024,” edps.europa.eu Vendors bundle on-device anonymisation and metadata search that satisfy auditors yet retain operational insight, shortening refresh cycles—especially in Germany and France where fines can reach 4% of turnover for violations. This regulatory push aligns with the 14.17% wireless growth outlook, as bandwidth-efficient edge processing makes untethered deployments commercially viable.

Adoption of 4K/8K ultra-HD cameras in Nordic ports & airports

Axis’s Q1809-LE delivers 8K imagery for long-range harbour oversight, and similar UHD devices are deployed in the 5G-LOGINNOV project at Hamburg and Koper to link video with predictive-maintenance algorithms. Operators gain forensics-grade footage and asset-tracking analytics, fuelling a 13.35% CAGR for 4K-and-above units and raising storage requirements that favour edge compression chips supplied by hybrid camera lines.

Shift from capex to Surveillance-as-a-Service among European SMEs

Genetec’s SaaS platform unifies video, access and occupancy metrics under subscription pricing, trimming upfront spend for retailers combating shrinkage. SMEs adopt managed services to secure automatic firmware updates and cyber-insurance compliance, supporting a 12.57% CAGR in Transportation & Logistics as warehouses embrace pay-as-you-go scalability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter EU AI-Act limits on biometric surveillance | –1.6% | EU-wide, led by Germany, Netherlands, Nordics | Short term (≤ 2 years) |

| Supply-chain dependence on non-EU chipsets inflating lead-times | –1.2% | EU-wide, higher impact in Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter EU AI-Act limits on biometric surveillance

The March 2024 AI Act bans untargeted facial scraping and confines biometric identification to limited law-enforcement use cases. Integrators must shelve or re-engineer facial analytics within public-space designs, dampening demand for premium algorithms embedded in thermal & dual-spectral models—although these cameras still post a 13.80% CAGR by pivoting toward industrial inspection and emissions monitoring.

Supply-chain dependence on non-EU chipsets inflating lead-times

DIGITALEUROPE cites a high supply-risk score for AI-grade semiconductors, with lead times exceeding 40 weeks.[3]DIGITALEUROPE, “Analysis of the EU’s Positioning in Critical Technology Value Chains,” digitaleurope.org Eastern European installers, operating on slimmer budgets, substitute lower-spec components, curbing premium ASP growth across the Europe Surveillance Camera market. European fabricators are pursuing design-for-manufacture alliances to shorten supply loops, yet near-term constraints persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By : IP dominance consolidates while hybrid bridges legacy gaps

IP-based units captured 67.45% Europe Surveillance Camera market share in 2025, anchored by open APIs and ONVIF conformity that simplify integration with VMS and access-control suites. Hybrid analog-IP converters, growing at 11.05% CAGR, address cost-sensitive campuses that cannot decommission coax infrastructure yet crave edge analytics. Vendors differentiate through secure boot, certificate-based authentication and chip-level TPMs. Chinese entrants compress pricing, compelling European incumbents to package analytics subscriptions with hardware to protect margins.

Second-order effects include higher demand for switch upgrades and PoE+ injectors, as 4K bandwidth exceeds legacy network capacity. Cyber-insurance premiums are also shaping purchase criteria; policies increasingly require firmware-signed cameras, favouring brands with mature patch cadences. These dynamics reinforce IP’s lead while hybrid retains relevance in phased conversion roadmaps.

By Camera Form-Factor: Fixed-box ubiquity versus thermal innovation

Fixed-box designs delivered 41.40% Europe Surveillance Camera market share in 2025 by providing predictable framing at a modest cost. Their rectangular housings simplify pole or façade mounting, making them the default choice for parking, campus corridors and cash-desk zones. Ruggedised variants with integrated heaters dominate the 56.60% outdoor deployment share, with IP66/67 ratings now standard. Thermal & dual-spectral units, although niche, are forecast to post a 13.55% CAGR as energy and petrochemical sites adopt optical-gas-imaging for methane-leak compliance.

Hybrid visual-thermal models also aid railways in detecting human presence on tracks, a use case attracting EU safety grants. Form-factor choice is therefore increasingly linked to vertical-specific KPIs rather than universal security metrics.

By Resolution: Full-HD leads but 4K momentum accelerates

Full-HD maintains 46.05% Europe Surveillance Camera market share because it balances clarity with storage efficiency on existing NVR arrays. Compression algorithms such as H.265+ allow 30 days retention without major disk upgrades, aligning with regulatory evidence-keeping mandates. Nonetheless, 4K & above segments are surging at a 13.18% CAGR. Ports, stadiums and border crossings require pixel density to enable zone cropping and digital PTZ across wide areas.

Higher resolution drives adjacent demand for SSD-based appliances and AI-optimised GPUs, reaffirming vendor moves toward full-stack offerings that bundle storage, analytics and cyber-hygiene dashboards.

By Connectivity: Wired reliability versus wireless agility

Wired PoE/Ethernet carries 60.25% share thanks to dependable power delivery and predictable latency, essentials for government-grade infrastructure and 24/7 industrial lines. Yet wireless nodes, growing at 13.95% CAGR, unlock heritage sites and temporary venues where trenching is impractical. Companies incorporate WPA3 encryption and SIM-based authentication to satisfy insurers, aligning with the cyber-resilience requirements coming into force.

Site architects now specify dual-path connectivity, one wired, one LTE/5G, to ensure failover, highlighting convergence rather than outright substitution.

By Deployment Location: Outdoor share climbs on ruggedised demand

Outdoor placements reached 56.60% in 2025, reflecting broader city-wide security investment. The outdoor-ruggedised sub-class, forecast at 12.15% CAGR, integrates self-cleaning lenses, salt-fog coatings and wide operating-temperature ranges.

Europe Surveillance Camera market share for indoor cameras remains steady in retail and healthcare, where privacy-masking and occupancy analytics generate operational value. Vendors tie environmental sensors (PM2.5, CO₂, decibels) to outdoor housings, feeding municipal dashboards and justifying budget under sustainability line-items.

By End-User Industry: Government leadership meets logistics acceleration

Government & Public Safety commands 28.55% Europe Surveillance Camera market share, anchored in city surveillance, border control and law-enforcement facilities. However, Transportation & Logistics will outpace all sectors at a 12.31% CAGR, driven by port automation mandates and airport capacity upgrades.

Railway operators pair UHD cameras with LiDAR to detect track obstructions, integrating feeds into maintenance-of-way software platforms. Logistics warehouses employ edge-vision to reduce forklift collisions and optimise inventory-slotting, linking surveillance ROI directly to operational KPIs.

Geography Analysis

The United Kingdom, holding 22.70% Europe Surveillance Camera market share in 2025, blends vast legacy CCTV stock with aggressive uptake of cloud-native VMS. Financial districts deploy AI-enabled anomaly detection to safeguard trading floors, while councils migrate control rooms onto hybrid-cloud infrastructure. UK public acceptance of surveillance remains comparatively high, yet the Information Commissioner’s Office enforces strict footage-retention limits that nudge buyers toward edge redaction.

Germany prioritises privacy-by-design, pushing vendors to insert on-sensor blurring and audit trails. Preparations for the UEFA 2024 Championship accelerated stadium and border deployments, showcasing 4K crowd-density analytics. Manufacturing clusters integrate cameras with MES and SCADA, transforming surveillance into a quality-control asset.

France, forecast to grow at a 13.90% CAGR, leverages Olympics-funded pilots to validate AI video for abandoned-object detection and queue management. Paris metro extensions embed cameras in platform-edge doors to monitor passenger flow, signalling city-wide analytics adoption post-Games.

The surveillance camera market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Latin America and Asia. This is complemented by country-specific insights for France, United Kingdom, Mexico, India, Japan, China, and Brazil, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

Europe Surveillance Camera market competition spans optics specialists, AI software vendors and cloud-service providers. Hikvision’s 31.19% revenue jump confirms persistent price leadership. Axis Communications emphasises secure-element chips and open-source firmware to differentiate on cyber posture. Bosch’s marketing of Sony imaging modules aligns superior sensor performance with in-house analytics, broadening portfolio depth.

Milestone Systems’ merger with Arcules combines on-prem resilience and cloud scalability, illustrating platform consolidation. Genetec’s SaaS suite transforms perpetual-license revenues into predictable ARR, locking in clients through API ecosystems. Hanwha Vision’s sustainability strategy, documented under ISO 14001, positions the brand with EU-Green-Deal procurement criteria.

Niche players exploit vertical gaps; Teledyne FLIR focuses on methane-leak detection, while Avigilon integrates body-worn camera feeds with fixed infrastructure for police forces. Cyber-resilience regulation is a rising moat—manufacturers with certified secure-boot chains will likely capture premium segments once the Cyber Resilience Act applies.

Europe Surveillance Camera Industry Leaders

Eagle Eye Networks

Bosch Security Systems GmbH

Axis Communications AB

Milestone Systems

Mobotix AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Milestone Systems merged with Arcules, enabling customers to toggle workloads between on-prem NVRS and cloud hot tiers.

- February 2025: Bosch announced EUR 44.5 billion (USD 47.9 billion) European revenue and strategic acquisitions to deepen security-technology capabilities.

- January 2025: Genetec showcased Security Centre SaaS at PropTech Connect in London, positioning unified cloud services as a hedge against fragmented point solutions.

- December 2024: Hanwha Vision published its sustainability report, highlighting low-power AI cameras and ISO-14001 certification.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study frames the Europe surveillance camera market as revenue generated from newly shipped analog, IP, and hybrid cameras, both fixed and PTZ, sold to residential, commercial, industrial, and public sector users across all 27 EU nations plus the UK, Norway, and Switzerland.

Scope exclusion: recorders, VMS software, cabling, and cloud storage services fall outside this camera-only baseline.

Segmentation Overview

- By Camera Technology

- Analog

- IP-based

- Hybrid

- By Camera Form-Factor

- Fixed Box

- PTZ (Pan-Tilt-Zoom)

- Thermal and Dual-Spectral

- Fisheye and 360°

- By Resolution

- HD (≤720p)

- Full-HD (1080p)

- 4K and Above

- By Connectivity

- Wired (PoE/Ethernet)

- Wireless (Wi-Fi/Cellular)

- By Deployment Location

- Indoor

- Outdoor Weather-Proof

- By End-User Industry

- Government and Public Safety

- Banking and Financial Services

- Healthcare and Pharmaceuticals

- Transportation and Logistics

- Industrial and Manufacturing

- Education Institutions

- Retail and Malls

- Corporate/Enterprise Campuses

- Residential and Smart Homes

- By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Nordics

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

To close gaps, we interview camera OEM product managers, regional distributors, systems integrators, and facilities chiefs in the UK, Germany, and France.

Their insights on average selling prices, feature adoption curves (AI analytics, 4 K, PoE++), and channel mark-ups allow us to calibrate desk findings and test early model outputs before locking assumptions.

Desk Research

Mordor analysts first sift through open data sets such as Eurostat crime statistics, EU GDPR enforcement logs, and government tenders published on TED, as these reveal volume pull from city-wide safety projects.

Trade bodies like the European Security Industry Association, CENELEC technical committees, and transport authorities publishing CCTV deployment counts enrich the understanding of installed base trends.

Company 10-Ks, investor decks, and import-export filings retrieved via D&B Hoovers and Dow Jones Factiva provide model-level shipment clues, while Questel patent analytics help gauge the speed of edge AI innovation.

The sources cited here are illustrative; many more public and subscription references are cross-checked to corroborate each data point.

Market-Sizing & Forecasting

We begin with a top-down construct that aligns EU manufacturing output and CN import volumes with channel inventories, which are then multiplied by validated ASP bands to derive 2025 revenue.

Select bottom-up checks, sampled supplier roll-ups and smart-city tender audits, fine-tune the totals.

Key model drivers include new dwellings completed, retail floor space additions, public safety CAPEX, average camera ASP erosion, and GDPR-related retrofit rates.

A multivariate regression links these drivers to historic sales, after which scenario analysis adjusts for currency swings and AI Act compliance costs.

Where bottom-up gaps appear (e.g., gray market inflows), we apply bounded error ranges agreed during expert calls.

Data Validation & Update Cycle

Outputs pass three-layer reviews: automated variance scans, peer analyst scrutiny, and senior lead sign-off.

We refresh models annually and trigger interim updates when policy shifts or supply shocks move baseline assumptions; a final validation occurs just before report release to ensure clients receive the freshest view.

Why Mordor's Europe Surveillance Camera Baseline Stands Solid

Published estimates often diverge because firms track different hardware bundles, ASP ladders, or refresh less frequently. Mordor's disciplined camera-only scope, annual refresh, and dual-path modeling create a dependable yardstick for planners.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.30 B (2025) | Mordor Intelligence | - |

| USD 5.28 B (2024) | Regional Consultancy A | Broader video surveillance scope excludes only monitors, lowering denominator |

| USD 7.42 B (2024) | Trade Journal B | Older price deck not adjusted for 2025 ASP rises and currency shifts |

The comparison shows that once differing scopes and pricing refresh cycles are reconciled, Mordor's figure offers the balanced middle ground purchasers can rely on for strategy setting.

Key Questions Answered in the Report

What is the current size of the Europe Surveillance Camera market?

The market stands at USD 9.17 billion in 2026 and is projected to reach USD 15.09 billion by 2031.

Which camera technology dominates today?

IP-based systems control 67.45% of Europe Surveillance Camera market share, reflecting widespread integration into smart-city and enterprise platforms.

Which segment is growing fastest between 2026 and 2031?

Wireless connectivity solutions top the growth chart with a 13.95% CAGR, followed closely by 4K & above resolutions at 13.18% CAGR.

Why is Transportation & Logistics viewed as a high-growth vertical?

Port and airport modernisation projects require UHD cameras and AI analytics, propelling the sector at a 12.31% CAGR.

How much of the market does the United Kingdom hold?

The UK accounted for 22.70% of Europe Surveillance Camera market revenue in 2025, supported by extensive legacy CCTV and rapid cloud adoption.

What resolution category leads the market today?

Full-HD (1080p) remains the largest resolution class with 46.05% share, although 4K & above is accelerating quickly.

How is GDPR influencing camera design?

GDPR drives adoption of edge-analytics cameras that anonymise data on-device, reducing compliance risk and boosting refresh rates across Europe.

Page last updated on: