Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.53 Billion |

| Market Size (2026) | USD 2.57 Billion |

| Market Size (2031) | USD 2.76 Billion |

| Growth Rate (2026 - 2031) | 1.44% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Soup Market Analysis by Mordor Intelligence

The European soup market size was valued at USD 2.53 billion in 2025 and estimated to grow from USD 2.57 billion in 2026 to reach USD 2.76 billion by 2031, at a CAGR of 1.44% during the forecast period (2026-2031). While shelf-stable canned soups remain the most common product type, there is a noticeable shift toward chilled and plant-based soup options, which are priced higher and driving value growth. Retailers are increasingly discontinuing slower-selling products and pushing for recyclable packaging to meet the European Union’s 2030 circular economy goals. This has prompted manufacturers to adopt pouch packaging more quickly. In Southern and Eastern Europe, consumers are more price-sensitive, which limits the demand for premium products. However, in Northern Europe, the growing popularity of flexitarian diets, which involve reducing meat consumption, has increased demand for vegetarian soup options. The market is moderately fragmented, with private-label brands offering similar flavors to established brands at lower prices. This competition is forcing major players to stand out by focusing on transparent ingredient sourcing and eco-friendly packaging solutions.

Key Report Takeaways

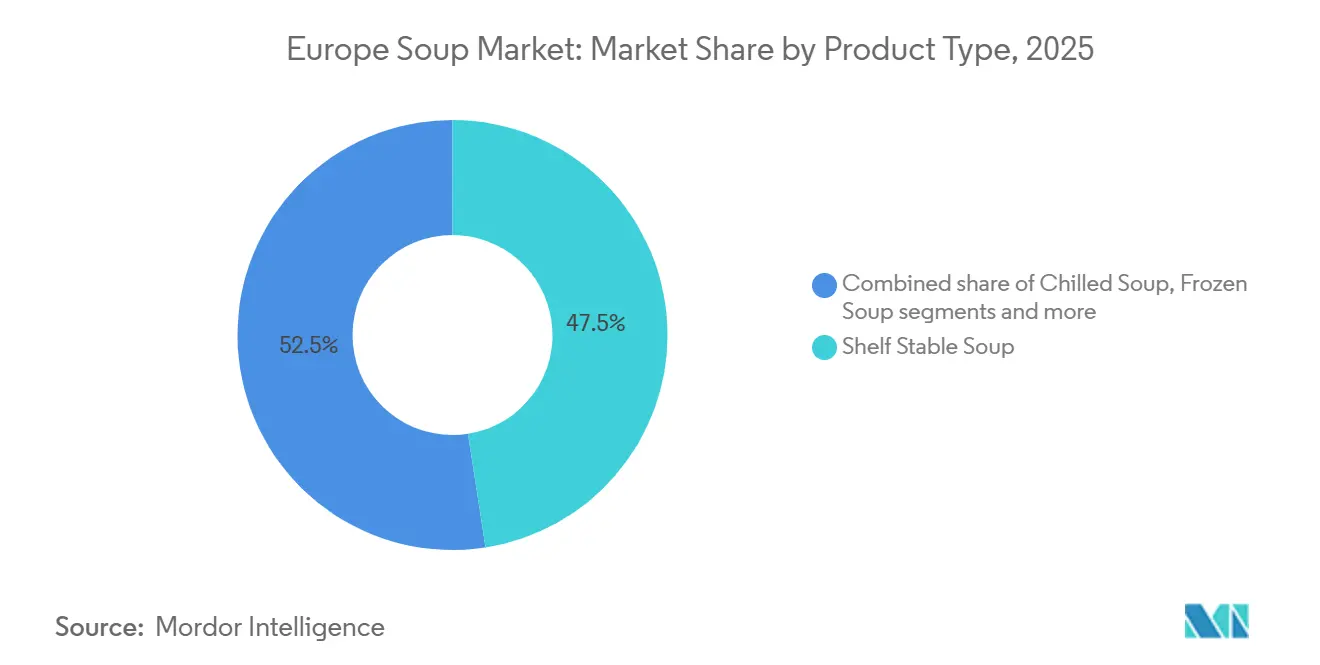

- By product type, shelf-stable canned soups dominated the market in 2025, accounting for 47.54% of the market share. In contrast, chilled soup is forecast to expand at a 3.54% CAGR through 2031, outpacing all other formats.

- By category, non-vegetarian variants held 65.72% of the European soup market share in 2025, while vegetarian lines are set to grow at a 3.02% CAGR to 2031.

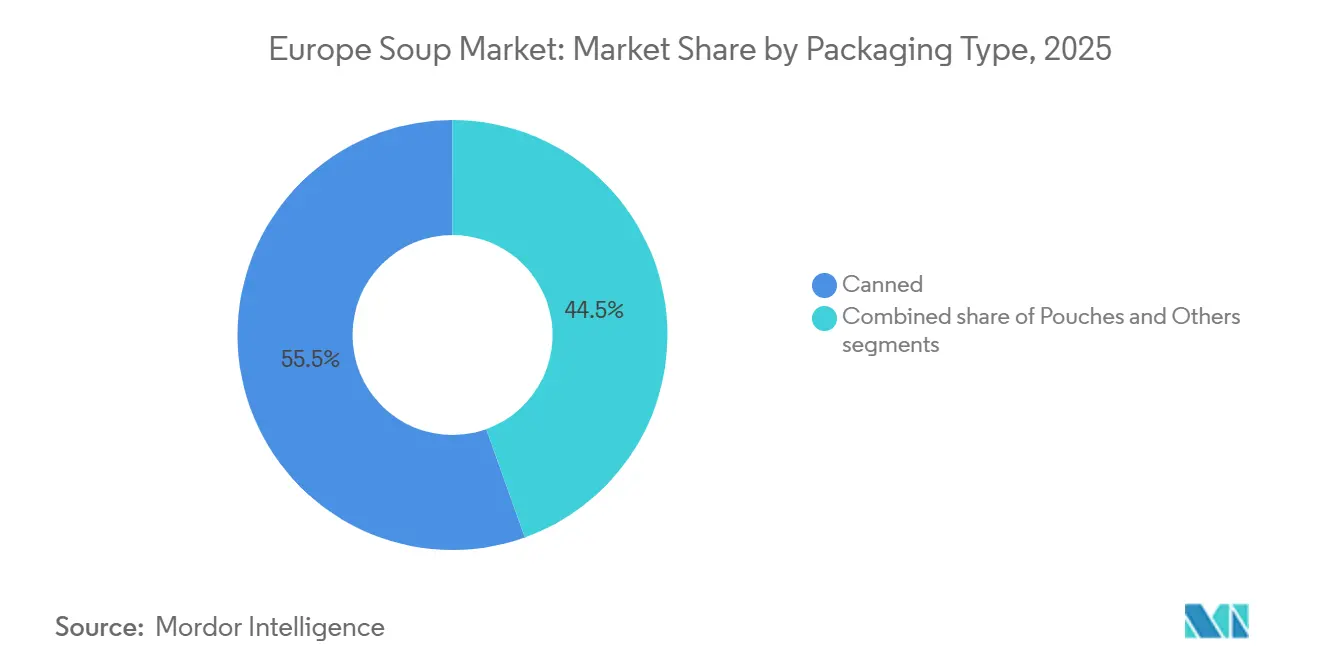

- By packaging type, cans accounted for 55.48% of the European soup market size in 2025; pouches represented the fastest-growing pack type, advancing at a 2.56% CAGR from 2026 to 2031.

- By distribution channel, supermarkets and hypermarkets accounted for 43.85% of sales in 2025; however, online retail is projected to rise at a 3.05% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Soup Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for convenient and ready-to-eat foods | +0.3% | Concentration in United Kingdom, Germany, France | Medium term (2-4 years) |

| Growth in plant-based and vegan soup offerings | +0.2% | Western Europe (United Kingdom, Netherlands, Sweden), expanding to Poland | Long term (≥ 4 years) |

| Premiumisation and gourmet product demand | +0.2% | United Kingdom, Switzerland, Netherlands, urban centers across Germany and France | Medium term (2-4 years) |

| Shift toward clean-label and transparent products | +0.15% | Europe-wide, driven by regulatory harmonization | Long term (≥ 4 years) |

| Innovation in packaging functionality and sustainability | +0.15% | Europe-wide, accelerated in Germany, France, Netherlands due to PPWR compliance | Short term (≤ 2 years) |

| Growth of seasonal and limited-edition launches | +0.1% | United Kingdom, Germany, seasonal peaks in Q4 | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing demand for convenient and ready-to-eat foods

The demand for convenient meal options is driving the European soup market, as busy lifestyles and shifting work habits leave consumers with less time to prepare meals. As more people return to office routines, the demand for convenient lunch options, such as soup, has steadily increased. According to the Agriculture and Horticulture Development Board UK, soup consumption rose by 0.1% in March 2025, reflecting this trend[1]Source: Agriculture and Horticulture Development Board, "Consumer Cooking Trends: Healthy and Convenient Meals on the Rise", ahdb.org.uk. Ready-to-eat soups, such as ambient and chilled varieties that can be heated in minutes, are becoming a popular choice for busy weekdays. These soups offer a simple, portion-controlled alternative to takeout or frozen meals. Both private-label retailers and well-known brands are expanding their soup offerings to meet this demand. Innovations in packaging, such as resealable caps and portable designs, are making soups even more appealing for quick desk lunches or on-the-go consumption.

Growth in plant-based and vegan soup offerings

The growth of plant-based and vegan soup options is driving the European soup market as more people adopt flexitarian, vegetarian, and vegan diets. This trend is particularly pronounced in Germany, which has the largest vegetarian population in Europe and over 1.5 million vegans, according to ProVeg as of April 2024[2]Source: ProVeg Organization, "Capture Europe’s Biggest Flexitarian Audience By Understanding German Consumers", proveg.org. To meet this demand, brands are introducing innovative plant-based soups that cater to both health-conscious and convenience-focused consumers. For example, Heinz UK launched its creamy tomato soup with beans and sausages in 2023, which combines plant-based protein with familiar flavors to appeal to a wider audience. Plant-based soups are gaining popularity due to their environmental benefits, such as lower carbon emissions compared to animal-based soups. Improvements in taste and texture are also encouraging more consumers, especially those who are environmentally conscious or looking for protein-rich options, to try these products.

Innovation in packaging functionality and sustainability

Packaging innovation is playing a significant role in transforming the European soup market as both regulations and consumer preferences push for more sustainable and user-friendly options. The European Union Packaging and Packaging Waste Regulation, which came into effect in January 2025, prohibits the use of per- and polyfluoroalkyl substances and requires all packaging to be recyclable by 2030[3]Source: European Commission, "Packaging Waste", environment.ec.europa.eu. This has led brands and manufacturers to move away from traditional multilayer laminates, which are more difficult to recycle. In response, companies are introducing advanced packaging solutions. For example, Gualapack’s Pouch5, launched in 2024, is a mono-material pouch that is compatible with standard form-fill-seal machines and meets curbside recycling requirements in countries such as Italy and Spain. Similarly, Amcor’s Liquiflex AmPrima, which debuted in 2025, removes aluminum barriers while maintaining oxygen resistance, making it suitable for shelf-stable soups.

Shift toward clean-label and transparent products

The shift toward clean-label and transparent products is a key factor driving the European soup market. Consumers and regulators are increasingly focusing on simpler and more natural ingredient lists. In response, many manufacturers are reformulating their recipes to comply with stricter additive and nutrition guidelines set by the European Food Safety Authority. This has led to the removal of artificial colors, flavor enhancers, and high sodium content from many products. Countries like Germany and France are particularly focused on transparency, with consumers favoring brands that clearly display the sources of their ingredients and processing details. This is often done through scannable QR codes or clear labels on packaging. While reformulating products to meet clean-label standards can increase production costs, surveys conducted in 2025 revealed that European consumers are willing to pay a premium for products that are free from additives and have transparent labeling.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from alternative meal solutions | -0.2% | United Kingdom, Germany, France, urban centers with high meal-kit penetration | Medium term (2-4 years) |

| Perception of processed foods as less healthy | -0.25% | Europe-wide, particularly acute in Germany, France, Netherlands | Long term (≥ 4 years) |

| High price sensitivity in staple food categories | -0.15% | Poland, Spain, Italy, Southern and Eastern Europe | Short term (≤ 2 years) |

| Taste and texture compromises from health reformulation | -0.1% | Higher impact in markets with established taste preferences (United Kingdom, Germany) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Perception of processed foods as less healthy

The belief that processed foods are less healthy is limiting the growth of the European soup market. Increasing scientific studies and public health recommendations are making consumers more cautious about industrially processed products. For instance, a 2024 British Medical Journal review highlighted that consuming large amounts of ultra-processed foods is linked to higher risks of heart disease and overall mortality. Similarly, findings from the European Prospective Investigation into Cancer and Nutrition study, published in The Lancet, supported these concerns across Europe, drawing attention to products such as canned and dehydrated soups. Even when manufacturers reformulate their products, many soups still face challenges in overcoming the negative perception associated with industrial processing methods, such as high-temperature sterilization and spray-drying.

Competition from alternative meal solutions

Growth in the European soup market is being limited by competition from other convenient meal options. Consumers are increasingly opting for alternatives that directly replace soup in their meal choices. For example, meal-kit providers like HelloFresh and Gousto are gaining popularity in the United Kingdom, with plans to serve millions of households by 2025. These services offer pre-portioned ingredients for easy meal preparation, providing the same convenience as soup but with a perception of higher value. Supermarket chilled-meal sections have expanded significantly since 2024, offering ready-to-eat options that compete with soup. Quick-commerce apps deliver hot restaurant meals in under 15 minutes, further reducing the appeal of soup as a quick weeknight meal option. Younger consumers, especially those under 35, tend to view soup as a seasonal comfort food rather than an everyday option.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chilled Formats Redefine Premium Positioning

Shelf-stable canned soups dominated the European soup market in 2025, accounting for 47.54% of the market share. These soups are popular due to their long shelf life, affordability, and easy availability, making them a convenient choice for households. They are especially favored by consumers who prefer stocking up on ready-to-eat meals for quick and hassle-free meal preparation. Dry soup sachets and frozen soups make up the rest of the market, appealing to those who value portability, cost-effectiveness, or extended storage options. Their strong presence in supermarkets, discount stores, and private-label offerings further boosts their demand across the region.

The chilled soup segment is projected to grow at a compound annual growth rate (CAGR) of 3.54% from 2026 to 2031, emerging as the fastest-growing product category in Europe. This growth is driven by increasing consumer demand for fresh, minimally processed foods with shorter ingredient lists. Chilled soups are often marketed as premium, clean-label, or chef-inspired alternatives to traditional canned soups, appealing to health-conscious and quality-focused consumers. These products are gaining popularity in urban areas and among higher-income consumers, as they are willing to pay more for healthier and fresher options. Retailers are also expanding shelf space for chilled soups to meet this growing demand.

By Category: Vegetarian Variants Gain Share Amid Flexitarian Adoption

In 2025, non-vegetarian soups made up 65.72% of the European soup market, highlighting the region's strong preference for chicken, beef, and seafood-based broths. These soups are popular due to their rich flavors and association with traditional home-cooked meals, especially in Southern and Eastern Europe. Many consumers view meat-based soups as comforting and nutritious, making them a staple in both retail and foodservice channels. Products like canned and chilled soups, as well as those served in restaurants, continue to rely heavily on animal-protein ingredients, ensuring this segment remains dominant.

Vegetarian soups are expected to grow at a 3.02% CAGR through 2031, driven by the increasing popularity of plant-based and health-conscious eating habits. Increasing numbers of consumers are adopting flexitarian diets, which focus on reducing meat consumption while incorporating more plant-based foods. Vegetarian soups, made with ingredients such as legumes, vegetables, and alternative proteins, are gaining popularity due to their perceived health benefits and affordability. Additionally, their lower production costs compared to meat-based soups allow brands to offer competitive pricing, appealing to budget-conscious and environmentally aware shoppers.

By Packaging Type: Pouches Gain Ground on Sustainability Mandates

Cans accounted for 55.48% of the European soup market in 2025, primarily due to their durability, long shelf life, and strong consumer trust. Metal cans are widely recycled across Europe, supported by efficient recycling systems, which adds to their appeal as a sustainable option. These characteristics make cans a popular choice for large-scale manufacturers and private-label brands. Their affordability and easy availability in supermarkets and hypermarkets ensure they remain a dominant packaging format in the market.

Pouches are expected to grow at a 2.56% CAGR from 2026 to 2031, becoming the fastest-growing packaging format in the European soup market. This growth is driven by advancements in recyclable and mono-material pouch designs, which align with the European Union’s sustainability goals for 2030. Pouches are lightweight, easy to store, and often feature resealable closures, making them convenient for consumers. Their eco-friendly nature and space-saving design are increasingly appealing to both environmentally conscious shoppers and brands looking to meet sustainability standards.

By Distribution Channel: Online Retail Captures Convenience-Driven Demand

Supermarkets/hypermarkets dominated the European soup market in 2025, holding a 43.85% share. These stores attract a large number of customers due to their convenience and variety. They provide ample shelf space for both well-known brands and private-label soups, making it easy for shoppers to compare options. Promotions such as discounts, multipack offers, and eye-catching in-store displays encourage customers to make bulk purchases or make impulse buys. As a result, supermarkets and hypermarkets remain the leading sales channels for soups across the region.

Online retail is projected to grow at a 3.05% CAGR from 2026 to 2031, emerging as the fastest-growing distribution channel for soups in Europe. The convenience of subscription services and personalized product recommendations has made online platforms increasingly popular for purchasing pantry staples, such as soup. Quick-commerce services, offering rapid delivery that can be as fast as minutes, have made online shopping more appealing for both planned purchases and last-minute needs. This shift in consumer behavior is driving the growth of online retail, making it a crucial channel for the expansion of the soup market.

Geography Analysis

The United Kingdom held 27.49% of Europe’s soup market in 2025, driven by high per-capita consumption and a strong presence of chilled soup options. Seasonal product launches and the growth of private-label offerings in major retail chains have helped maintain steady demand among households. However, younger consumers are gradually moving toward alternative meal options, which has slowed the frequency of soup purchases. In other major markets, such as Germany, France, and Italy, overall soup consumption remains stable. Growth in these countries is primarily fueled by product improvements, such as better packaging, reformulated recipes, and premium positioning, rather than attracting new consumers.

Poland is the fastest-growing soup market in Europe, with a projected CAGR of 3.23% through 2031. Factors such as urbanization, rising disposable incomes, and the expansion of modern retail formats are making soups a more common meal choice. The availability of a wider range of ambient and chilled soups in discount and convenience stores has made these products more accessible, especially in urban areas. While affordability continues to be a key factor, improving living standards are encouraging consumers to opt for higher-quality and more convenient soup options. This shift is helping drive the market’s growth in Poland.

In the rest of Europe, soup consumption patterns vary based on lifestyle, climate, and income levels. Southern countries like Spain experience strong seasonal demand for soups, particularly during colder months. Meanwhile, Northern and Western European markets are seeing a growing preference for organic, vegetarian, and health-focused soups. High-income countries such as Switzerland are driving demand for premium and functional soup products, including those with added nutrients or unique blends. Standardized food and labeling regulations across Europe are enabling manufacturers to introduce products in multiple countries more efficiently, supporting regional market expansion.

Competitive Landscape

The European soup market consists of a mix of large multinational companies, regional players, and smaller niche brands, making it moderately fragmented. Global companies benefit from their large-scale operations, strong marketing strategies, and extensive retail networks. However, regional brands and private-label products also hold a significant share of shelf space in many countries, ensuring no single company dominates the market. This competitive landscape drives companies to continually innovate, introducing new flavors and formats while maintaining competitive pricing to attract consumers.

Smaller, local, and premium-focused brands are gaining prominence by addressing the growing demand for chilled, clean-label, and plant-based soups. These brands often use direct-to-consumer sales channels, collaborate with foodservice providers, and leverage social media to engage with urban and younger consumers. They differentiate themselves by offering innovative packaging, emphasizing freshness, and using simple, natural ingredient lists. These strategies help them stand out in the crowded market, appealing to consumers who prioritize health, quality, and sustainability in their food choices.

Private-label soups, particularly in Western Europe, add to the competition by offering a wide range of affordable and premium options under retailer brands. To remain competitive, branded manufacturers are focusing on seasonal product launches, promoting sustainability, enhancing nutritional content, and positioning their products as premium offerings. Additionally, larger companies are actively acquiring regional and specialty soup brands to expand their product portfolios and strengthen their market presence. This trend highlights the fragmented nature of the market and the ongoing efforts by companies to capture a larger share of consumer demand.

Europe Soup Industry Leaders

-

Unilever plc

-

The Kraft Heinz Company

-

GB Foods SA

-

Premier Foods plc

-

Baxters Food Group Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Soul Kitchen, a United Kingdom-based female-founded food brand, introduced a new range of single-serve, clean-label soups designed to cater to modern workplaces, micro-markets, and the travel sector.

- September 2025: Dozz introduced an innovative soup format to the United Kingdom market, offering chilled ready-to-drink (RTD) soup packaged in aluminum cans. This innovative approach aimed to cater to the growing demand for convenient.

- September 2025: Bol Foods introduced its latest product innovation to the United Kingdom market: the protein Thai green noodle power soup. This new offering highlighted the brand's commitment to catering to health-conscious consumers by combining high-protein content with bold, authentic flavors.

- March 2024: Unilever received a binding offer from Sill Entreprises, a prominent French food and beverage company, to acquire its Knorr liquid soups business in France. This potential acquisition aligned with Sill Entreprises' strategy to expand its portfolio in the soup market.

Europe Soup Market Report Scope

The European soup market refers to the production, sale, and consumption of packaged and ready-to-serve soup products across European countries through retail and online channels. The European soup market is segmented by product type, category, packaging type, distribution channel, and country. Based on the product type, the market is classified into dry soup, shelf-stable soup, chilled soup, and frozen soup. Based on the category, the market is segmented into vegetarian soup and non-vegetarian soups. Based on the packaging type, the market is segmented into canned, pouches, and others. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, online retail stores, and others. Based on country, the market is segmented into the United Kingdom, Germany, France, Italy, Spain, the Netherlands, Sweden, Poland, Switzerland, and the Rest of Europe. The market forecasts are provided in terms of value (USD).

By Product Type

| Dry Soup |

| Shelf Stable Soup |

| Chilled Soup |

| Frozen Soup |

By Category

| Vegeterian Soup |

| Non-Vegeterian Soup |

By Packaging Type

| Canned |

| Pouches |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Others |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Sweden |

| Poland |

| Switzerland |

| Rest of Europe |

| By Product Type | Dry Soup |

| Shelf Stable Soup | |

| Chilled Soup | |

| Frozen Soup | |

| By Category | Vegeterian Soup |

| Non-Vegeterian Soup | |

| By Packaging Type | Canned |

| Pouches | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Others | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Switzerland | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe soup market in 2026?

The Europe soup market size reached USD 2.57 billion in 2026 and is forecast to rise steadily through 2031.

Which product format is growing fastest across the region?

Chilled soup is the fastest-growing product format, projected to expand at a 3.54% CAGR from 2026 to 2031.

What share do vegetarian SKUs hold and how fast are they expanding?

Vegetarian recipes made up 34.28% of 2025 sales and are on a 3.02% CAGR trajectory as flexitarian diets normalize.

Which country will add the most incremental value by 2031?

Poland is set for the fastest expansion at a 3.23% CAGR, driven by discount-banner growth and urban income gains.

Page last updated on: