Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

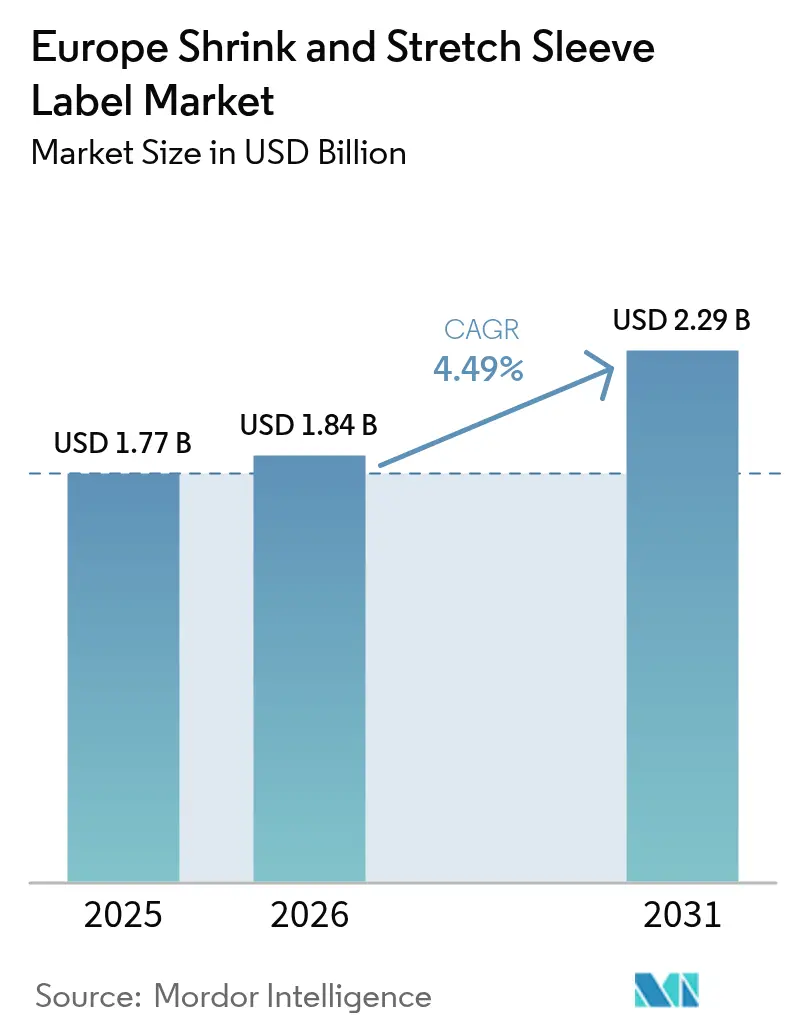

| Base Year Market Size (2025) | USD 1.77 Billion |

| Market Size (2026) | USD 1.84 Billion |

| Market Size (2031) | USD 2.29 Billion |

| Growth Rate (2026 - 2031) | 4.49% CAGR |

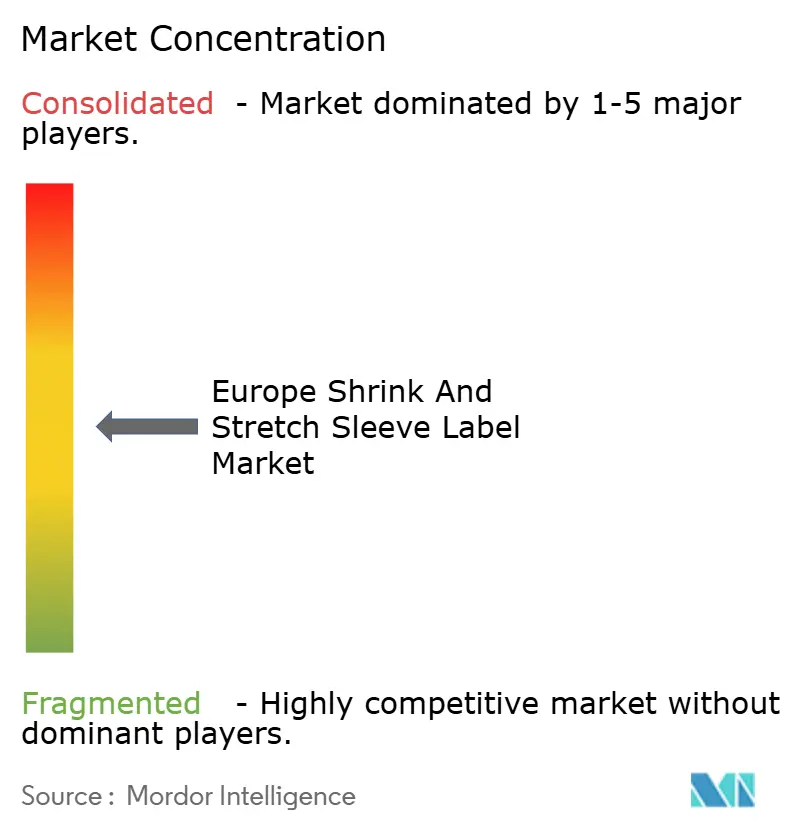

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Shrink And Stretch Sleeve Label Market Analysis by Mordor Intelligence

The Europe shrink and stretch sleeve label market size is projected to be USD 1.77 billion in 2025, USD 1.84 billion in 2026, and reach USD 2.29 billion by 2031, growing at a CAGR of 4.49% from 2026 to 2031. The steady expansion reflects rising demand for full-body branding across beverages and personal care, rapid integration of inline digital presses that enable micro-segmented campaigns, and material innovations that ease compliance with the European Union’s Packaging and Packaging Waste Regulation. Growth is tempered, however, by escalating virgin PET-G and PVC resin prices and by tougher recyclability rules that compel converters to redesign sleeve constructions. Heat-shrink formats remain dominant in volume terms, yet stretch sleeves are gaining traction in deposit-return schemes because they peel away cleanly, while recyclable polyolefin shrink films are emerging as credible PET-G substitutes in dairy and juice. Country dynamics diverge: Germany leads on account of dense bottling infrastructure and early digital-printing adoption, whereas Poland is the fastest grower thanks to cost-competitive greenfield capacity and proximity to Central European beverage hubs.

Key Report Takeaways

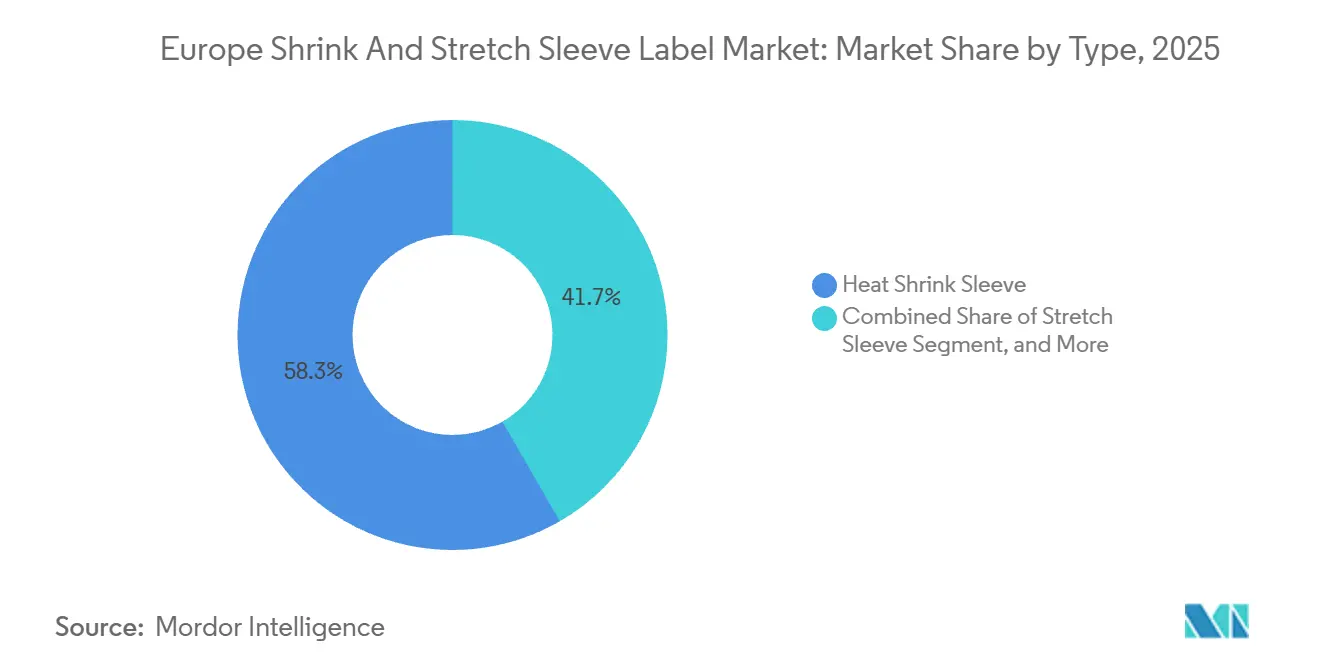

- By type, heat-shrink sleeves held 58.32% of the Europe shrink and stretch sleeve label market share in 2025, while stretch sleeves are projected to post the highest CAGR at 5.65% through 2031.

- By material, PET-G accounted for 46.23% of the Europe shrink and stretch sleeve label market size in 2025; polyethylene-based films are forecast to record the quickest expansion at 5.83% between 2026 and 2031.

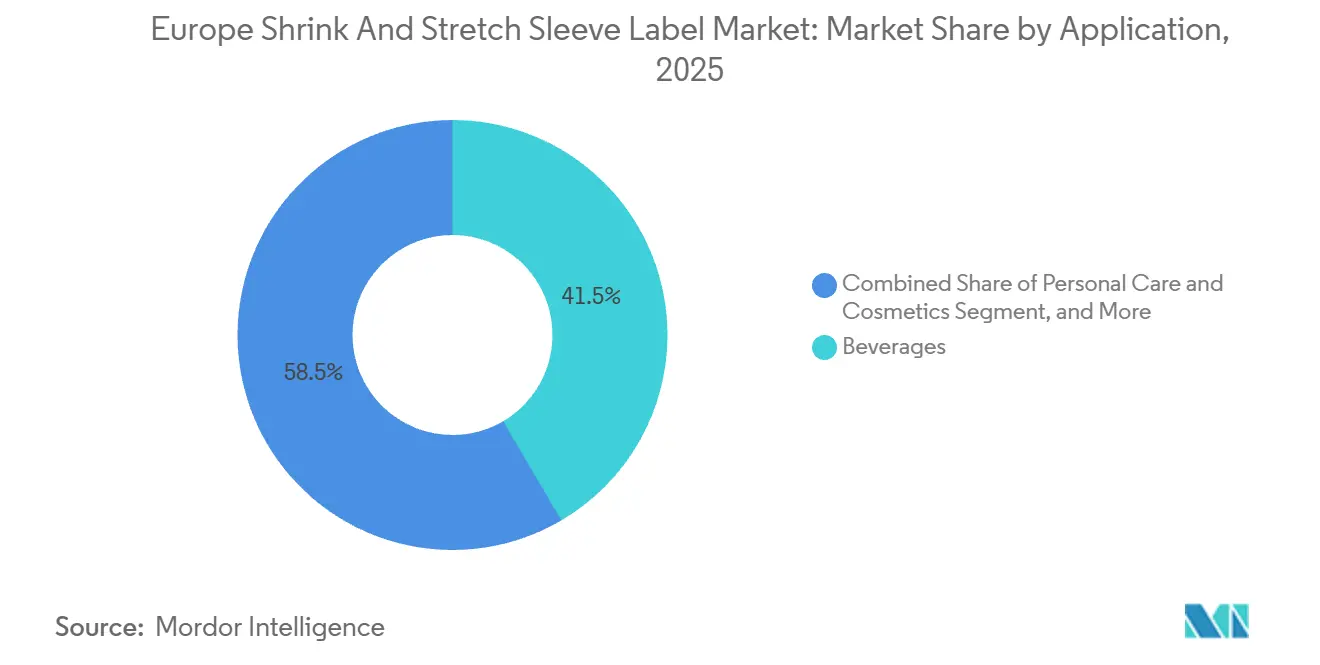

- By application, beverages led with 41.54% market share in 2025, whereas personal care and cosmetics is anticipated to advance at a 6.12% CAGR during the outlook period.

- By printing technology, flexography dominated with 48.61% share in 2025, but digital printing is expected to grow the fastest at 5.91% to 2031.

- By Country, Germany captured 21.34% of market share in 2025; Poland is projected to register the highest national CAGR at 5.57% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Shrink And Stretch Sleeve Label Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand to Increase On-Shelf Appeal | +1.2% | Germany, France, United Kingdom, Italy, Netherlands | Medium term (2-4 years) |

| Need for Tamper-Evident Protection | +0.9% | Germany, France, United Kingdom, Poland, Spain | Short term (≤ 2 years) |

| Shift Toward 360° Branding Surfaces | +1.1% | France, United Kingdom, Italy, Spain, Netherlands | Medium term (2-4 years) |

| Adoption of Recyclable Polyolefin Shrink Films | +0.8% | Germany, Netherlands, Poland, Rest of Europe | Long term (≥ 4 years) |

| Inline Digital Printing Integration | +0.7% | Germany, France, Italy, United Kingdom | Medium term (2-4 years) |

| Lithium-Metal Additive Inks Enabling Ultra-Thin Sleeves | +0.4% | Germany, France, Poland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand to Increase On-Shelf Appeal

Eye-tracking research shows that 64% of European shoppers decide within three seconds which beverage to pick, underscoring how full-body sleeves elevate shelf impact.[1]Fraunhofer Institute for Industrial Engineering, “Consumer Eye-Tracking Study 2025,” iao.fraunhofer.de The label’s 360° canvas lets brands combine vivid graphics, sustainability claims, and QR-enabled promotions without disrupting visual flow. Luxury shampoo makers in France and Italy transitioned from paper labels to heat-shrink sleeves in 2025, unlocking room for multilingual text and premium finishes. Perrier’s holographic limited edition boosted impulse sales by 17% in French hypermarkets the same year.[2]Nestlé S.A., “Perrier Fines Bulles Limited Edition Launch,” nestle.com Private-label chains such as Lidl mimic these premium cues with low-cost flexo-printed sleeves, intensifying competition for consumer attention. As e-commerce platforms favor products that photograph well in 360°, brand owners continue to treat sleeves as an investment in conversion and loyalty rather than a mere cost line.

Need for Tamper-Evident Protection

EU food-contact rules coming into force by 2027 oblige liquid dairy and infant-nutrition packs to display verifiable integrity seals. Shrink sleeves with perforated tear bands meet that need without secondary over-wraps. After a 2024 methanol poisoning incident, Eastern European distilleries adopted full-body sleeves with tear strips in spirits above 20% alcohol, following new safety decrees in Poland and Slovakia. Pharmaceutical packers in Germany and the Netherlands now wrap clinical-trial vials in coded sleeves that align with EU track-and-trace law. Huhtamaki’s ISO-16495-certified sleeve for aseptic juice, launched in Spain in late 2025, shows how tamper evidence and child resistance converge in a single construction. As regulators tighten integrity demands, tamper-evident sleeves shift from value-add to baseline expectation.

Shift Toward 360° Branding Surfaces

The EU Green Claims Directive requires more space for substantiation, so labels must house up to 18% extra compliance text versus 2024.[3]European Commission, “Green Claims Directive,” ec.europa.eu Seamless sleeve graphics counter that space crunch. Garnier migrated its European shampoo line to PET-G sleeves in 2025, embedding a 12-language ingredient list and blockchain-verified sustainability score. Craft breweries embrace digitally printed sleeves to rotate collectible artwork monthly, sparking social-media sharing. Coca-Cola Europacific Partners paired Fanta cans with AR-enabled sleeves in Germany that drove 2.3 million app downloads in eight weeks. Retailers reward such high-information designs with prominent facings, reinforcing the branding cycle.

Adoption of Recyclable Polyolefin Shrink Films

The PPWR stipulates that all packs be recyclable or reusable by 2030, a rule that exposes PET-G sleeves to float-sink contamination risks. Innovia Films’ cavitated PE sleeve floats away from PET flakes during caustic wash, as proven in a six-month Arla Foods dairy pilot that cut contamination below 0.5%. Amcor invested EUR 45 million (USD 50.9 million) in 2025 to retrofit its Ghent plant for mono-material PE sleeves, anticipating surcharges on non-recyclable formats. EPR fee structures in France and Italy already penalize non-recyclable sleeves by up to EUR 0.08 per unit, driving brand owners toward polyolefin options. Although PE’s lower clarity challenges premium beverages, co-extrusion and surface-treatment advances continue to narrow the aesthetics gap.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter EU Plastics-Packaging Waste Directives | -0.8% | Germany, France, Netherlands, Poland, Rest of Europe | Short term (≤ 2 years) |

| Rising Prices of Virgin PET-G and PVC Resins | -0.6% | Germany, Italy, France, Spain, United Kingdom | Short term (≤ 2 years) |

| Limited Recycling Streams for Multi-Layer Films | -0.4% | Germany, Netherlands, France, Belgium | Medium term (2-4 years) |

| Sleeve Removal Bottlenecks in EU Deposit-Return Schemes | -0.3% | Germany, Netherlands, Poland, Rest of Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter EU Plastics-Packaging Waste Directives

Germany’s VerpackG amendment introduces a tiered EPR fee on sleeves thicker than 40 microns or printed with non-detectable inks, raising unit costs by EUR 0.05-0.12 from January 2026. A draft EU act floats a 30% recycled-content mandate for PET-G sleeves by 2028, yet the current high-intrinsic-viscosity rPET supply is insufficient. Uncertainty over “recyclable in practice” metrics stalls converter investment, while small Southern European firms risk exit because funding mono-material lines is capital-intensive.

Rising Prices of Virgin PET-G and PVC Resins

Spot PET-G reached EUR 1,850 per metric ton in January 2026, 9% above 2025, on outages at Eastman and Indorama glycolysis units. PVC climbed 14% to EUR 1,320 on tight ethylene dichloride supply and higher energy tariffs. Mid-tier converters operating long-term contracts at 2024 price baselines have seen 200-300 basis-point margin compression. Mondi blamed resin inflation for 60% of its 2025 European margin decline, prompting a pivot toward recycled-content substrates. Without hedging tools for specialty resins, converters pass costs downstream or lose share to vertically integrated rivals able to offset resin swings internally.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Stretch Sleeves Gain Traction In Deposit Systems

Heat-shrink sleeves commanded 58.32% share of the Europe shrink and stretch sleeve label market in 2025, reflecting their compatibility with complex bottle shapes and high-speed tunnels. Stretch equivalents are forecast to expand at 5.65% to 2031 as Germany and the Netherlands penalize labels that hinder bottle recycling, making peelable, adhesive-free sleeves attractive. In 2025 Sleever International installed a stretch applicator rated at 36,000 bottles per hour, closing the speed gap with heat-tunnel systems. Full-body shrink formats continue to serve premium spirits and cosmetics, while multi-pack bundling sleeves remain mainstream in carbonated sodas.

Deposit-return economics amplify stretch demand; operators incur fewer wash-cycle rejects and score higher rPET purity. Conversely, heat-shrink sleeves retain a material-cost edge, at EUR 0.02-0.04 per unit against EUR 0.05-0.07 for stretch. As DRS penalties intensify, however, brand owners increasingly treat higher stretch-sleeve costs as compliance insurance. The interplay between recyclability fees and line-speed economics will keep both formats relevant, bifurcating adoption by regulatory stringency and price sensitivity.

By Material: PET-G Dominance Faces Polyolefin Challenge

PET-G delivered unsurpassed clarity and shrink uniformity, securing 46.23% share in 2025. Yet the Europe shrink and stretch sleeve label market size for polyethylene films is rising at 5.83% thanks to float-sink separability and lower EPR fees. Klöckner Pentaplast’s 35% rPET-content film, launched in 2025, helps brand owners inch toward recycled-content pledges. OPP and OPS stay relevant for bundling sleeves that need rigidity, but their recyclability weaknesses expose them to substitution pressure.

Dow’s Affinity elastomers now enable PE films to achieve up to 60% shrink while maintaining gloss comparable to PET-G. PVC’s exit accelerates under Scandinavian bans, shrinking its addressable pool to specialty applications. Polypropylene serves hot-fill beverages where high shrink temperature is tolerable. By 2027 polyolefins are likely to overtake PET-G in dairy and water, while PET-G remains entrenched in premium graphic-intensive SKUs that prize optical brilliance.

By Application: Personal Care Outpaces Beverages In Growth

Beverages accounted for 41.54% of market share in 2025, underscoring how full-body sleeves combine tamper-evidence with a marketing canvas. Nevertheless, personal care and cosmetics will register the strongest 6.12% CAGR through 2031, reflecting luxury brands’ shift to seam-free, 360° storytelling. Coca-Cola Europacific Partners extended sleeve use across Fanta and Sprite in Germany and Poland, embedding NFC tags that raised repeat-purchase rates by 11%.

Food sleeves cover dairy tubs, sauces, and ready meals, but feel growing pressure from refill schemes. Other uses, from automotive fluids to household cleaners, are small yet gain share, as chemical-resistant PVC sleeves satisfy CLP labeling requirements. The result is a bifurcation; beverages drive volume, while personal care generates value, ensuring converters calibrate press fleets for both high-speed flexo runs and short-run digital cosmetics variants.

By Printing Technology: Digital Gains Share In Short-Run Cosmetics

Flexography kept 48.61% share in 2025 because plate costs amortize efficiently on runs above 100,000. Digital, growing 5.91%, excels below 50,000 units where plate-free workflows shine. HP Indigo WS6800 presses installed in France and Italy allow 1,200-dpi resolution at 40 m/min, letting cosmetic brands localize artwork for specific retailers without incurring cylinder charges.

Rotogravure still rules mega-volume carbonated drinks thanks to ink density and tonal stability, whereas screen printing lives in premium spirits that need tactile metallic layers. LED-UV flexo units cut energy 40% and reduce turnaround, blurring speed advantages. Hybrid lines that combine flexo base layers with digital variable data position converters to capture both mainstream beverage orders and cosmetics’ long-tail SKUs.

Geography Analysis

Germany generated 21.34% of the Europe shrink and stretch sleeve label market revenue in 2025 as global converters clustered around its dense bottling ecosystem and early deposit-return adoption. VerpackG’s new EPR tiers raise demand for PE sleeves and for laser-perforated designs now trialed by Fraunhofer IVV, which detach reliably during industrial washes. Poland is projected to climb at a 5.57% CAGR toward 2031, buoyed by greenfield flexo and gravure capacity in Silesia that serves Czech, Slovak, and Hungarian beverage hubs at substantially lower labor cost.

France and the United Kingdom form mature but regulation-intensive markets. France’s AGEC law targets 10% reusable packaging by 2027, prompting beverage fillers to explore refillable PET and glass that could shrink sleeve volumes. The UK’s post-Brexit EPR scheme, effective October 2025, levies up to GBP 0.10 (USD 0.13) per non-recyclable sleeve, nudging brands toward polyolefins.

Southern nations reveal mixed trajectories; Spain’s 2025 packaging-waste act bans non-recyclable sleeves on bottles above 1 liter by 2028, while Italy’s laxer pace preserves PVC in wine sleeves until EPR fees double in 2027. The Netherlands represents the DRS vanguard with 12,000 reverse-vending machines, driving stretch-sleeve penetration for rapid manual removal. Eastern markets such as Romania and Bulgaria lag two years behind Western recyclability timelines, creating pockets where conventional PET-G still thrives.

Regulatory Landscape

At the EU level, the Packaging and Packaging Waste Regulation, Regulation (EU) 2025/40 (PPWR), entered into force on 11 February 2025 and applies from 12 August 2026. It tightens design-for-recycling expectations for packaging components such as shrink and stretch sleeves. Under the PPWR framework, converters and brand owners need to show that sleeves do not hinder collection, sorting, and mechanical recycling, which increases the value of mono-material polyolefin sleeves, detectable inks, and constructions that can be removed or separated in established recycling processes.

Implementation detail is also moving through EU acts and deadlines that shape compliance programs and documentation. In June 2026, the European Commission adopted Commission Implementing Decision (EU) 2026/1425 (30 June 2026), setting rules for calculating, verifying, and reporting recycled plastic content data for single-use plastic beverage bottles. This raises verification rigor across bottle ecosystems where sleeves function as part of the overall packaging system. The PPWR also mandates implementing acts by 12 August 2026 for harmonised packaging labelling specifications, supporting more consistent sorting guidance across Member States and increasing the premium on sleeve solutions aligned with harmonised recyclability and labeling rules.

Value Chain Analysis

The value chain begins with polymer and additive suppliers that feed PET-G, PVC, and polyolefin film structures, alongside inks, coatings, and adhesives designed for shrink performance and detectability in sorting. Converters then extrude or source films, print using flexo, gravure, or digital methods, and finish sleeves (seaming, perforation, RFID or variable-data integration). Applicator and shrink-tunnel equipment providers influence line speed and energy use, and they also affect how practical peelable or stretch formats are on production lines.

Demand is concentrated among beverage and personal care brand owners and co-packers that specify sleeve material, artwork, and compliance attributes, with retail and e-commerce shaping SKU proliferation that favors short-run and variable-data printing. Downstream, waste management operators and DRS systems are increasingly setting sleeve specifications by requiring separation that is clean for PET and that does not compromise rPET quality. PPWR, Regulation (EU) 2025/40, applying from 12 August 2026, reinforces coordination across the value chain around traceability, harmonised labeling, and recyclability evidence, pulling converters closer to brand owners and recyclers to validate wash performance and sortability. As a result, material compatibility documentation becomes more central, including recycled-content accounting where applicable, and it favors suppliers that can support solutions end-to-end, from film selection through applicator setup to recycling validation.

Competitive Landscape

Market concentration is moderate with players like Amcor, CCL Industries, Huhtamaki, Fuji Seal, and others. Competition pivots on technology breadth; brand owners seek partners that can extrude recyclable films, print both flexo and digital, and install applicators. Amcor’s 2025 purchase of Capsule for USD 150 million strengthened its mono-material PE know-how and added three Indigo presses to its European fleet. Huhtamaki captured market share in tamper-evident sleeves after releasing an ISO 16495-compliant juice carton solution.

Mid-tier disruptors exploit incumbents’ slower reaction to sustainability mandates. Sleever International markets energy-free stretch applicators that sidestep heat tunnels, enticing beverage fillers aiming to cut scope-2 emissions. Multi-Color Corporation leverages digital presses to service cosmetics SKUs that traditional gravure economics cannot support. Mondi filed a patent for water-soluble sleeve adhesive, addressing a critical DRS barrier and signaling intent to integrate deeper into beverage loops.

Strategic differentiation now resides in circularity credentials as much as in cost leadership. Converters that secure ISO 14021 certification for recycled-content claims, align with CEN/TC 261 protocols, and maintain traceable chain-of-custody programs become preferred vendors. As EPR tariffs tighten, vertically integrated firms able to internalize resin volatility gain resilience, suggesting gradual consolidation but still leaving room for agile innovators that target high-margin niches such as ultra-thin lithium-ink sleeves for battery packs.

Europe Shrink And Stretch Sleeve Label Industry Leaders

CCL Industries Inc.

Fuji Seal International Inc.

Amcor PLC

Multi-Color Corporation

Klöckner Pentaplast GmbH and Co. KG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

PPWR (Regulation (EU) 2025/40), applying from 12 August 2026, creates clearer whitespace for sleeve constructions that demonstrate compatibility with established recycling pathways and harmonised labeling requirements. This is supporting investment and product development focused on floatable polyolefin sleeves, wash-off or clean-release chemistries, and constructions intended to reduce contamination in PET streams, especially for beverages subject to deposit-return schemes where removal performance directly affects rPET purity.

Smart and data-enabled sleeves also represent a tangible opportunity as policy and brand programs place greater emphasis on digital packaging information and traceability. Company actions show this direction: in February 2026, Sleever launched INVENTRA RFID integrated into shrink sleeves for identification and traceability use cases. In May 2026, UPM introduced the UPM ProCycle portfolio focused on packaging recyclability and clean release during mechanical recycling. These initiatives support converters that can pair compliant materials with digital printing and embedded features, enabling short-run personalization while meeting tighter EU documentation and verification expectations.

Recent Industry Developments

- June 2026: CCL Industries completed its acquisition of Sleever International. The deal expands CCLs capabilities in shrink sleeve technologies and application equipment. It strengthens integrated offerings for brand owners seeking decoration performance and recyclability outcomes across Europe.

- October 2025: Amcor acquired Capsule for USD 150 million, adding mono-material PE know-how and three HP Indigo presses to its European network. The acquisition broadened Amcors ability to supply recycle-ready sleeve structures. It also supports short-run, high-variation labeling programs alongside mainstream beverage volumes.

- January 2024: CCL Industries opened a sustainable sleeve label hub in Dornbirn, Austria, featuring EcoFloat decoration technology. The facility investment increased local capacity for floatable, recycling-aligned sleeve solutions. It reflects how European brand owners have pushed for designs that separate more cleanly in PET recycling streams.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers the value of shrink and stretch sleeve labels used to decorate, protect, and identify consumer and industrial products across Europe, where the sleeve is applied around the container or pack and then shrunk or stretched to fit.

Scope exclusions: We exclude non-sleeve labeling formats (such as pressure-sensitive labels and in-mold labels) and any label demand outside Europe.

Segmentation Overview

- By Type

- Heat Shrink Sleeve

- Stretch Sleeve

- Full-Body Sleeve

- Multi-Pack/Bundling Sleeve

- Other Types

- By Material

- Polyvinyl Chloride (PVC)

- Polyethylene Terephthalate Glycol-Modified (PET-G)

- OPP (Oriented Polypropylene) and OPS (Oriented Polystyrene)

- Polyethylene (PE)

- Polypropylene (PP)

- Other Materials

- By Application

- Food

- Beverages

- Personal Care and Cosmetics

- Other Applications

- By Printing Technology

- Flexographic Printing

- Rotogravure Printing

- Digital Printing

- Others Printing Technologies

- By Country

- Germany

- France

- United Kingdom

- Italy

- Poland

- Netherlands

- Spain

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping the sleeve label value chain, from film and labelstock through printing and converting, then into key end uses like beverages, food, and personal care. We use public sources to anchor the model inputs, including packaging and labeling guidance from the European Commission, Eurostat manufacturing and trade series for plastics and printed products, and harmonized customs statistics to sanity-check import and export flows.

To keep assumptions realistic, we also review sustainability and recycling position papers from industry associations, packaging waste and EPR-related publications from national authorities, and peer-reviewed articles on shrink-film materials and wash-off behavior. Company annual reports, investor presentations, and credible press are used to understand capacity additions, technology shifts (flexographic, rotogravure, and digital), and pricing direction. Where public disclosures are thin, we reference a paid subscription source for company financials and news selectively to close gaps. These are illustrative examples of desk inputs, and other sources were consulted for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work is used to confirm what desk inputs cannot fully show, especially how sleeve demand shifts by country, application, and printing route, and how pricing changes get passed through. We speak with participants across the chain, including converters, film suppliers, and packaging buyers in beverages and personal care, and we include a mix of European geographies so the model does not overfit to one large market.

Where numbers vary, we revisit assumptions with follow-up questions so the final totals stay tied to purchase behavior and realistic conversion yields.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 13% | |

| Mid tier: 51% | Functional/Unit leaders: 31% | |

| Smaller Players: 14% | Managers: 56% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where packaging and converting activity in Europe is reconstructed into an addressable sleeve label demand pool, and then filtered by sleeve adoption in key applications. Once that ceiling is formed, we corroborate it using selective bottom-up approximations, including converter revenue sampling by sleeve activity, channel checks on typical project sizes, and a few ASP times volume calculations for representative container groups.

The model is shaped using practical variables that interviewees can validate, such as sleeve usage intensity in beverages versus food, the split between shrink and stretch sleeves, film and ink cost movements that influence finished sleeve pricing, and the printing technology mix (flexographic, rotogravure, digital) that changes unit economics. We also incorporate regulatory packaging requirements that can affect material choice and label redesign cycles. When data is missing for smaller countries, gaps are handled by applying country-level beverage and packaged goods output signals with conservative sleeve penetration ranges, then correcting through primary feedback.

Forecasting uses scenario analysis supported by near-term indicators, including packaged beverage output, private-label activity, and capacity additions in converting, followed by a normalization of input cost assumptions. We keep one central case as the published forecast, while downside and upside cases are used internally to check that the CAGR remains consistent with what market participants see in their order books.

Data Validation & Update Cycle

Validation is done through a set of checks that a junior analyst can repeat, where we compare implied sleeve spending per unit output in beverages and personal care against what buyers report. We also test whether country totals align with trade and production signals. Outliers are flagged, then assumptions like adoption rates, ASP steps, and printing mix are reviewed again before internal sign-off.

We re-check year-to-year movements so they match known developments, such as major packaging regulation milestones, resin price spikes, or major capacity changes that can temporarily distort pricing. Reports are refreshed annually, and where a material event occurs, interim updates are made so the market numbers do not lag reality. Before delivery, a final pass is completed to ensure the latest publicly available signals and interview feedback are included.

Mordor Intelligence's Europe Shrink and Stretch Sleeve Label Market Size Versus Other Published Estimates

Published market sizes for sleeve labels in Europe often do not match, mainly because researchers group products differently and they also choose different timing for pricing and currency conversion. The same market can look larger when adjacent packaging services are counted, or smaller when only one sleeve type or a narrower geography is included.

The biggest gap drivers here usually come from whether multi-pack and bundling sleeves are counted with full-body sleeves, how materials (PVC, PET-G, OPP/OPS, and others) are translated into finished label value, and whether growth is projected from a steady base case or from an aggressive recovery path. Differences can also come from refresh cadence, because rapid changes in resin-linked pricing can shift the value outcome even when volumes are stable, and these mechanics explain why numbers spread across sources.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.77 B (2025) | |

| Regional Consultancy A | USD 2.74 B (2022) | Uses a Western Europe-only geography and appears to fold a wider packaging services scope into the sleeve label total, while also using an earlier price base year that can inflate value when resin costs were elevated. |

| Industry Research Publisher B | USD 3.30 B (2024) | Presents a broader heat-shrink focus that likely mixes sleeve packaging and label value together, and relies on high-level regional shares rather than country and application checks, which can overstate Europe when adoption rates are generalized. |

The table shows that scope and value construction choices explain most of the spread, especially around whether bundling sleeves and packaging services are treated as label value and how pricing is time-aligned. By keeping the calculation tied to sleeve label demand in Europe and cross-checking application-level adoption and pricing steps, the spread is narrowed in a way that stays repeatable for an analyst, a modeling choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the projected revenue for Europe shrink and stretch sleeve label market by 2031?

The market is forecast to reach USD 2.29 billion by 2031, reflecting a 4.49% CAGR from 2026.

Which sleeve type is growing fastest across European deposit-return systems?

Stretch sleeves, thanks to their peel-off design that prevents PET contamination, are projected to grow at 5.65% through 2031.

Why are polyolefin shrink films gaining popularity with beverage brands?

Polyolefin sleeves meet PPWR recyclability rules because they float away from PET flakes, lowering EPR fees and preserving rPET quality.

How is digital printing changing sleeve-label supply?

HP Indigo and similar presses remove plate costs, enabling run lengths as low as 500 units and supporting hyper-localized cosmetic launches.

Which country offers the highest growth opportunity for converters?

Poland is expected to lead with a 5.57% CAGR to 2031, supported by new greenfield capacity and regional beverage demand.

What material challenges confront premium graphic-heavy sleeves?

Virgin PET-G costs rose 9% year-on-year, and recyclability rules push brands to find polyolefin films that match PET-Gs clarity without cost spikes.

Page last updated on: