Global Shrink Sleeve Applicator Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

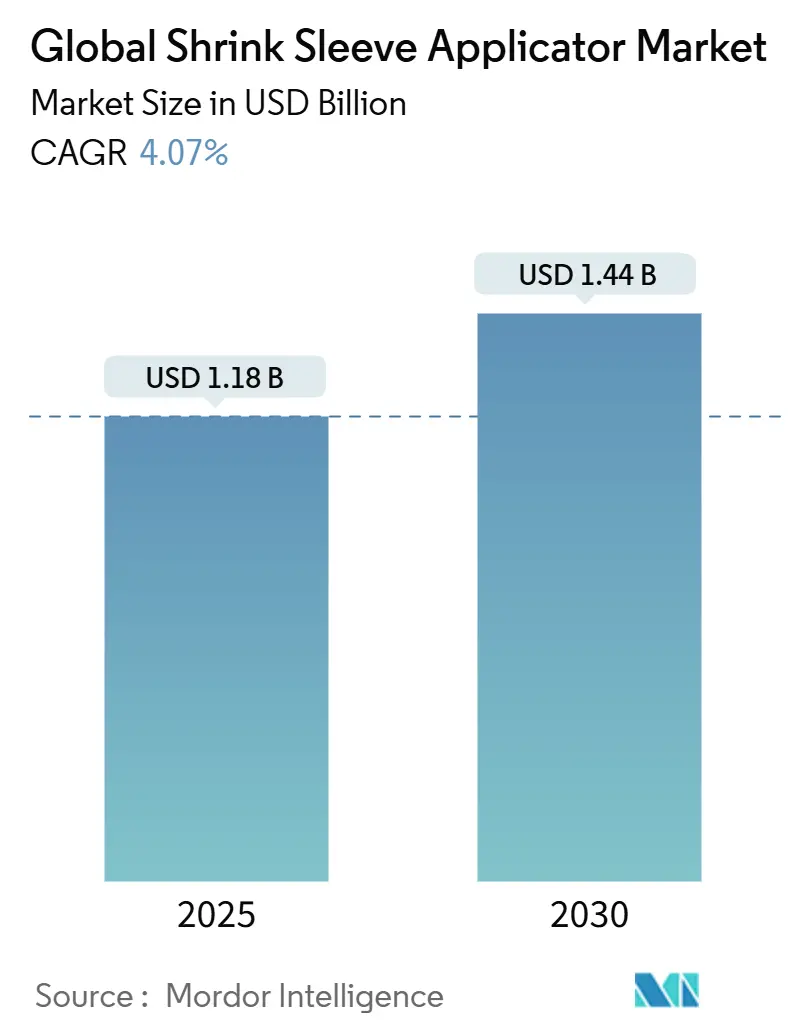

| Market Size (2025) | USD 1.18 Billion |

| Market Size (2030) | USD 1.44 Billion |

| Growth Rate (2025 - 2030) | 4.07% CAGR |

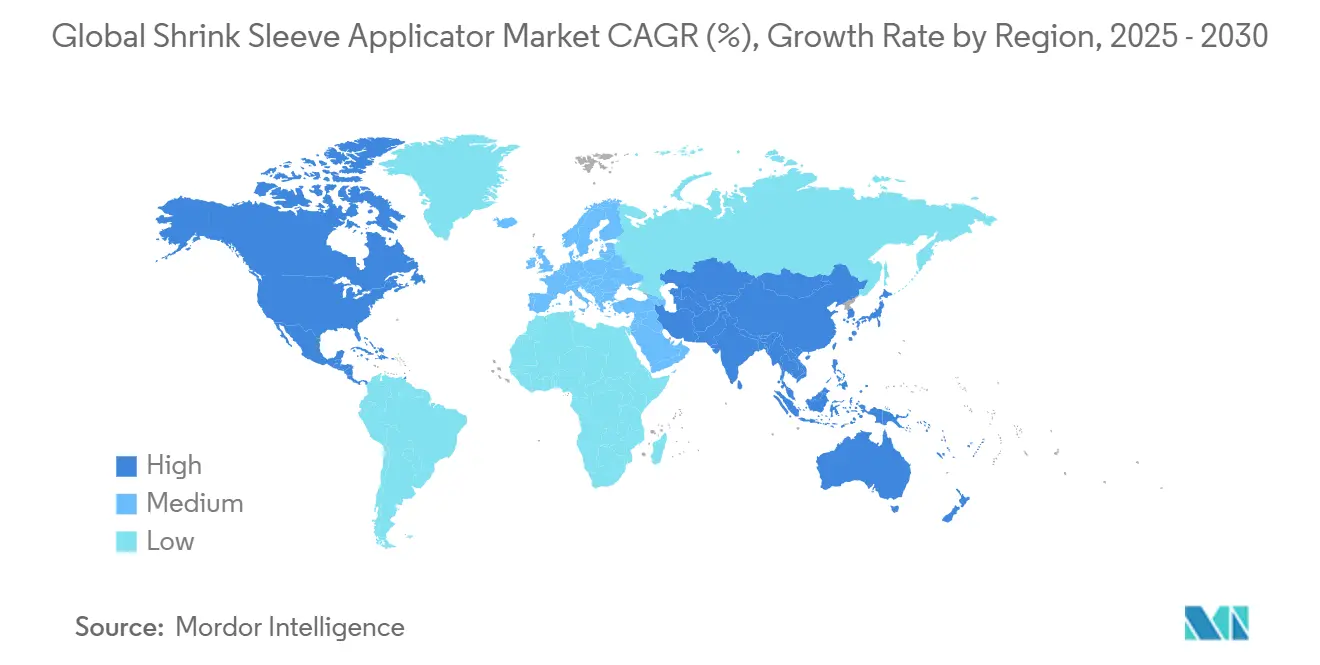

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

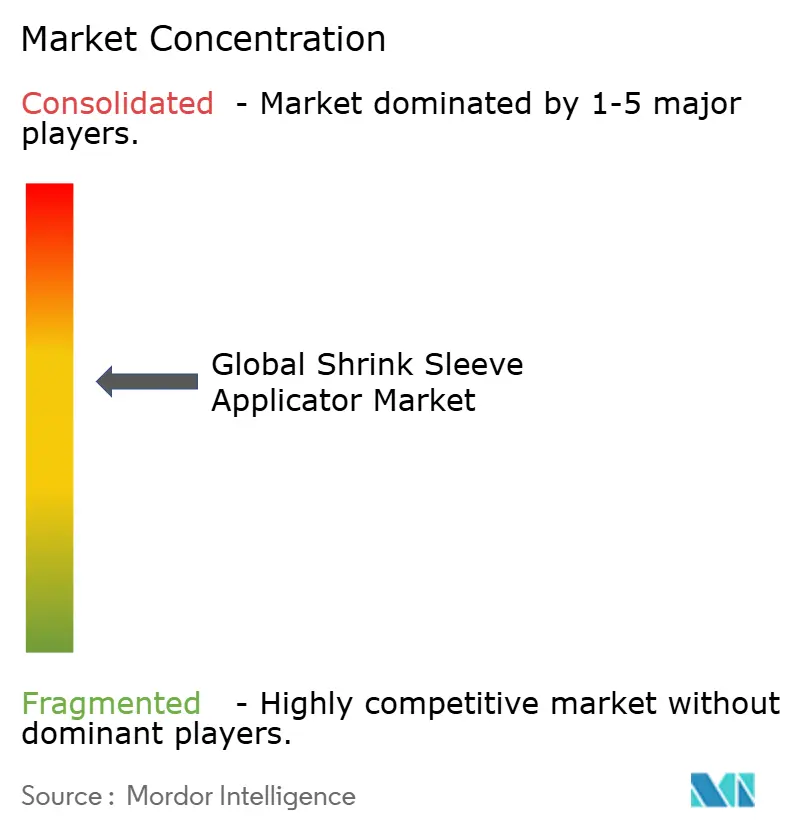

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Shrink Sleeve Applicator Market Analysis by Mordor Intelligence

The shrink sleeve applicator market stood at USD 1,183.68 million in 2025 and is on track to reach USD 1,442.28 million by 2030, advancing at a 4.07% CAGR. Rising regulatory stringency in pharmaceuticals, SKU proliferation in craft beverages, and retailers’ preference for multi-pack displays are steering demand away from basic equipment toward digitally enabled, high-speed rotary and hybrid systems. Producers are prioritizing fully integrated automation that embeds vision inspection and predictive maintenance, both to offset labor shortages and to improve overall equipment effectiveness. A parallel push toward eco-designed, floatable PET-G sleeves is reshaping material handling requirements, prompting machinery suppliers to redesign heat tunnels and servo controls for lower shrink temperatures. High-volume co-packers are also accelerating investment in applicators rated above 600 BPM to maximize asset turns while maintaining tight quality tolerances. Competitive dynamics remain technology-led rather than price-driven, with modularity, change-over speed, and data connectivity emerging as core differentiators in the shrink sleeve applicator market.

Key Report Takeaways

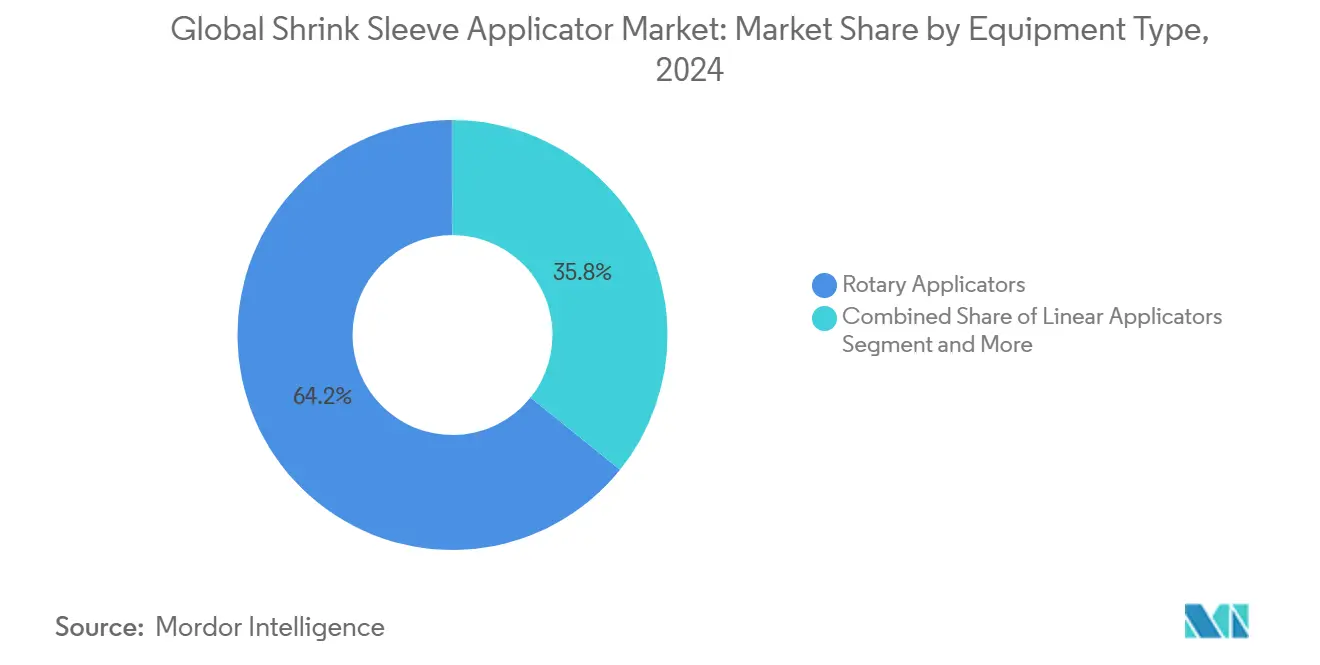

- By equipment type, rotary applicators captured 64.23% of the shrink sleeve applicator market share in 2024.

- By automation level, fully automated units held 81.92% share of the shrink sleeve applicator market size in 2024 and post a 5.03% CAGR to 2030.

- By sleeve application type, multi-pack and promotional sleeves led with 58.4% revenue share in 2024; full-body sleeves register the fastest 4.68% CAGR to 2030.

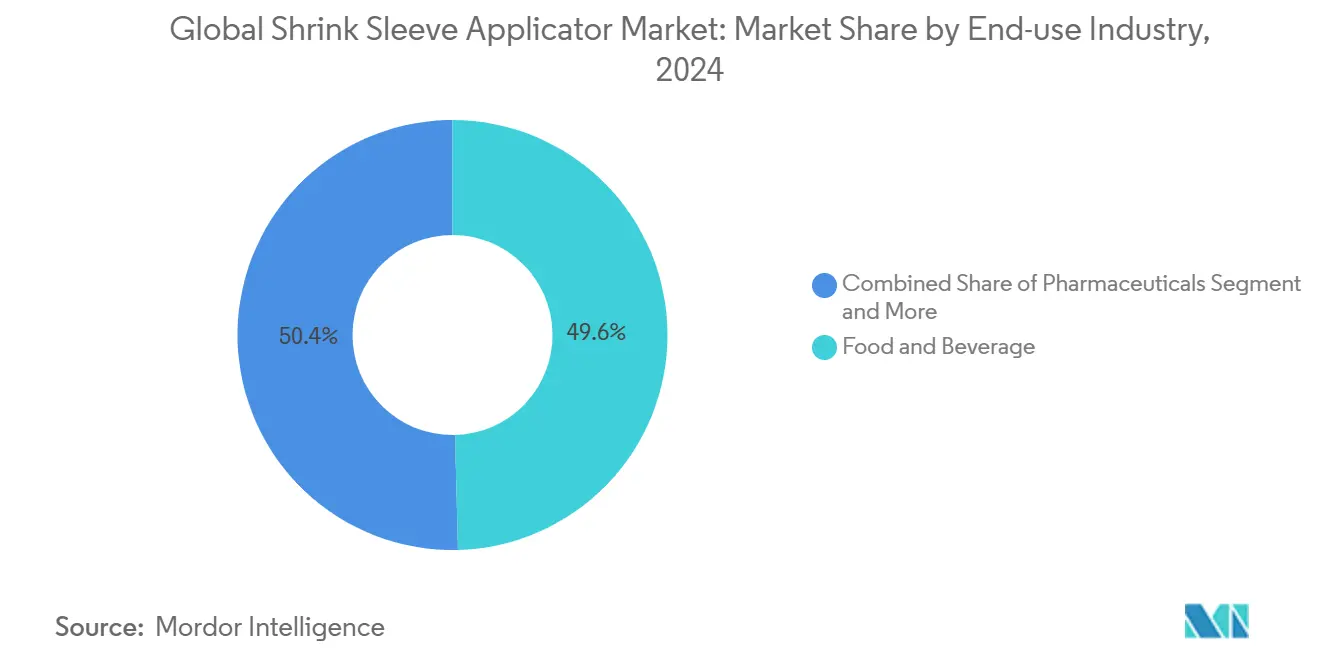

- By end-use industry, food & beverage commanded 49.6% of the shrink sleeve applicator market size in 2024, while pharmaceuticals expand at the leading 4.81% CAGR through 2030.

- By production-speed capacity, lines exceeding 600 BPM held 41.3% share of the shrink sleeve.

- By geography, North America controlled 34.4% of the shrink sleeve applicator market in 2024; Asia-Pacific is the fastest climber at 5.67% CAGR through 2030.

Global Shrink Sleeve Applicator Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tamper-evident demand in pharma | +1.2% | North America and EU-centric, global roll-out | Medium term (2–4 years) |

| Craft beverage SKU surge | +0.8% | North America and Europe, rising in Asia-Pacific | Short term (≤ 2 years) |

| High-speed rotary adoption by co-packers | +0.9% | Global, led by North America | Medium term (2–4 years) |

| Brand shift to floatable PET-G sleeves | +0.6% | EU-driven, global uptake | Long term (≥ 4 years) |

| In-line digital inspection for OEE | +0.5% | Developed markets first, then global | Medium term (2–4 years) |

| Predictive maintenance integration | +0.4% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising demand for tamper-evident packaging in pharmaceuticals

Drug producers now specify applicators that can place security bands compliant with U.S. DSCSA and EU FMD standards, forcing machinery builders to engineer precision band control, servo-driven mandrels, and integrated vision inspection. Thermo Fisher Scientific’s patented cold-chain tamper-evident carton and Pack Leader USA’s SL series showcase how equipment must guarantee band accuracy without damaging sensitive vials. The pharmaceutical segment’s 4.81% CAGR to 2030 underpins continued capital spending on these high-spec lines, reinforcing security as a decisive driver within the shrink sleeve applicator market.

Surge in craft-beverage SKUs requiring short-run, full-body decoration

Seasonal launches and limited-edition labels push breweries toward shrink sleeves that deliver 360-degree graphics even at low volumes. Tripack’s modular HSA-250 and HSA-405 lines, rated up to 500 packages per minute, enable sub-five-minute changeovers critical for micro-run economics. Digital printing’s falling unit cost further accelerates adoption, extending the driver to premium food niches and reinforcing flexible equipment demand across the shrink sleeve applicator market.

Adoption of higher-speed rotary systems by co-packers

Outsourced packers running diverse SKU portfolios view >600 BPM rotary units as the clearest path to asset utilization gains. Krones passed the 1,000-unit milestone for its Sleevematic platform in 2025, supplying a unit for Acqua Sant’Anna that illustrates persistent demand for continuous-motion architecture. Servo-driven turret designs cut changeovers from hours to minutes, making rotary solutions a cornerstone of co-packer competitiveness.

Brand-owner shift to eco-friendly, floatable PET-G sleeves

European recycling mandates favor floatable labels that detach in sink/float systems. TOPAS Advanced Polymers’ cyclic olefin copolymer and Impact Sleeves’ Eco-Sleeve require applicators calibrated for lower heat shrink and tighter tension control[1]TOPAS Advanced Polymers, “Floatable COC Label Material,” topas.com. Brands such as Premier Protein already cite 35% plastic savings from new perforated sleeves, making sustainability a structural growth driver for the shrink sleeve applicator market.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Label-visibility rules limiting sleeve coverage | -0.4% | Global, jurisdiction-specific | Short term (≤ 2 years) |

| High capital outlay of premium applicators | -0.7% | Emerging markets most affected | Medium term (2–4 years) |

| PVC film recycling incompatibility | -0.3% | EU-led, spreading worldwide | Long term (≥ 4 years) |

| Sleeve material price volatility | -0.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Label-visibility regulations limiting sleeve coverage

FDA and EU labeling rules mandate unobstructed nutrition and warning panels, forcing brands to reserve clear windows or reduce sleeve length. Applicator suppliers answer with advanced registration controls, yet creative latitude shrinks and overall sleeve square-meter demand softens, tempering full-body adoption in the shrink sleeve applicator market.

Capital-intensive nature of high-speed applicators

Fully loaded rotary lines can exceed USD 500,000, creating adoption hurdles for SMEs in cost-sensitive regions. MULTIVAC’s EUR 100 million German plant expansion spotlights the heavy investment required to build next-generation systems. Leasing models exist, but added usage fees dilute long-term ROI, slowing penetration in developing economies.

Segment Analysis

By Equipment Type: Rotary throughput, linear agility

Rotary units held 64.23% share thanks to steady >800 container-per-minute capability, a figure that equates to roughly 25% of the overall shrink sleeve applicator market size for high-volume food and beverage use. Axon’s SLX platform combines servo turrets and smart sensors to maintain registration at those speeds[2]Axon, “SLX High-Speed Shrink Sleeve Applicator,” axon.com. Linear machines, though smaller, post a 7.04% CAGR as co-packers accept marginally lower throughput in exchange for a narrower footprint and easier maintenance. Hybrid frames that accept rotary or linear heads on a common chassis provide transitional flexibility for plants phasing in automation.

Continued PETG migration calls for tunnel redesigns that moderate temperature while preserving shrink ratios. Specialty band applicators, essential for pharma neck-bands, secure a steady niche shielded from volume-based price erosion. Given these dynamics, machinery builders expect the rotary subset of the shrink sleeve applicator market to widen its absolute revenue lead yet cede incremental growth share to compact linear and hybrid models over the forecast horizon.

By Automation Level: Fully automated dominance

Fully automated systems captured 81.92% of the 2024 shrink sleeve applicator market share, and the category expands 5.03% annually as producers weave in AI vision and closed-loop tension control. Smart dashboards recording OEE in real time enable maintenance teams to switch from reactive to predictive workflows. LinkedData’s deployment of OT/IT analytics for Amcor illustrates how live telemetry justifies the higher capex. Semi-automated lines—typically manual feed plus automated sleeve drop—serve firms migrating from legacy manual tables; that slice remains relevant in lower-volume personal-care plants.

On fully automated platforms, camera arrays tie directly into servo adjustments, trimming waste below 1%. Markem-Imaje’s CoLOS Vision exemplifies AI-driven label verification for pharmaceutical batches. With labor scarcity unlikely to ease, end-users view autonomous operation not as a luxury but as an operational prerequisite, cementing its status as the primary value pool inside the shrink sleeve applicator market.

By Sleeve Application Type: Promotional bundles headline volume

Multi-pack sleeves supplied 58.4% of volume in 2024, underlining retailers’ appetite for club packs and BOGO promotions. Because each machine cycle encloses multiple primary packages, multi-packs slash per-unit material cost, sustaining high asset utilization. Full-body sleeves, while only 360-degree in coverage, account for the strongest 4.68% CAGR as brand managers leverage billboard-like graphics. Here, the shrink sleeve applicator market size for full-body decoration is expected to climb to USD 445 million by 2030 at current forecasts.

Neckbands, mandated for premium spirits and over-the-counter drugs, maintain steady uptake tied directly to regulatory enforcement. Partial sleeves and “label” bands occupy cost-sensitive niches where on-shelf differentiation is secondary to clear-panel visibility requirements. Applicator OEMs increasingly offer quick-swap mandrels permitting any of the above sleeve formats on a single frame, an approach that de-risks equipment selection for co-packers serving multiple application types.

By End-Use Industry: Food and beverage rules, pharma rises

Food and beverage plants represented 49.6% of the shrink sleeve applicator market in 2024, undergirded by soda, water, and RTD coffee lines seeking high-speed graphics. Yet pharma’s 4.81% CAGR means its slice could approach 15% of total demand by 2030, powered by serialization laws and anti-counterfeiting drives. Multi-Color Corporation’s tactile varnish sleeves in personal care show how cosmetics leverage decoration depth for shelf appeal.

Industrial chemicals adopt sleeves for secondary containment and compliance icons that withstand abrasion. Tripack’s automotive kits show how label durability and chemical resistance guide equipment specification. With pharmaceutical quality parameters permeating adjacent sectors, cross-industry standardization pressures will likely tighten applicator tolerances—even in mainstream food uses—across the shrink sleeve applicator market.

By Production-Speed Capacity: 600 BPM plus for top tier

Lines capable of >600 BPM held 41.3% of 2024 revenue and advance at 5.19% CAGR as bottlers chase cost per thousand containers. Automated vision lifts defect detection from 50% manual accuracy to 90%, enabling ultra-high-speed throughput without yield loss automate.org. The 301–600 BPM bracket supports regional soda and personal-care fillers balancing capex with line versatility. Sub-300 BPM categories retain importance among craft beverage and pilot facilities but account for a shrinking share of the shrink sleeve applicator market size as scale economics tilt toward faster lines.

AI-enabled condition monitoring is already bundled into many >600 BPM units, notifying maintenance teams before bearing or knife failures run scrap rates. That digital overlay reinforces the speed hierarchy: the faster the line, the higher the return on uptime analytics, cementing the premium tier’s growth trajectory.

Geography Analysis

North America’s 34.4% share in 2024 mirrors its deep co-packing network and strong regulatory emphasis on tamper evidence. ProMach’s 2024–25 acquisition spree, from HMC Products to Sentry Equipment, points to a strategy of end-to-end line integration that feeds further demand for embedded shrink-sleeve modules[3]ProMach, “Acquisition of Sentry Equipment,” promachbuilt.com. U.S. beverage sites gravitate toward rotary applicators exceeding 800 BPM, whereas Mexican fillers prefer compact linear units to keep capex low yet comply with U.S. export labeling. Canadian OTC pharma firms leverage harmonized standards to deploy identical applicator SKUs across border plants, driving batch consistency. Sustainability imperatives spur trials of floatable sleeves, prompting OEMs to add lower-temperature tunnels for PET-G films across the region.

Asia-Pacific advances at a market-leading 5.67% CAGR on the back of consumer packaged goods volume growth and rising automation budgets in China, India, and Vietnam. Fuji Seal International’s USD 52 million North Carolina plant underscores confidence in NA; nevertheless, its Thai subsidiary has doubled capacity to cater to APAC brands that now specify OEE monitoring and rapid-switch mandrels. Pharmaceutical production clusters in India and Indonesia demand precise tamper bands, encouraging local integrators to license foreign servo tech instead of importing entire frames. As sustainability rules tighten, early-stage trials of de-inkable sleeves in Japan signal upcoming upgrades in tunnel heating profiles for regional converter lines, expanding the shrink sleeve applicator market.

Europe remains steady due to replacement cycles and green directives. MULTIVAC’s EUR 100 million German expansion earmarks RandD for energy-efficient tunnels and IoT analytics . EU policy banning non-recyclable PVC labels from 2027 accelerates PET-G adoption, compelling existing lines to retrofit nip-roll and blade systems. Germany and Italy supply most of the continent’s applicators, exporting digital-ready models to Central Europe’s beverage producers upgrading for DRS compliance. UK craft distillers meanwhile adopt semi-auto bands, blending heritage branding with modest chunks of the broader shrink sleeve applicator market.

Competitive Landscape

The market shows moderate fragmentation: the top five suppliers collectively hold roughly 45%, justifying a concentration score of 6. Krones, Fuji Seal International, and Sleever International occupy the premium tier, each bundling applicators with inspection cameras, tunnel ovens, and MES connectors. These firms stress service contracts and spare-part subscriptions that can represent 20% of total five-year customer spend, shifting revenue mix toward recurring flows.

Mid-tier challengers such as Axon, Tripack, and PDC International target craft beverage and personal-care niches, touting modularity and fast changeovers. Patent filings highlight ongoing advances in multi-layer shrink films and AI control loops; for instance, Sealed Air’s 65% free-shrink multilayer substrate pushes machinery redesign for lower temperature differential.

Supply disruptions and PVC volatility force OEMs to develop sleeve-agnostic mandrel sets and dynamic tensioners. Vendors slow to offer sustainability-ready designs risk share erosion, especially in Europe where brand owners treat recyclability compliance as a vendor pre-qualification filter. The shift to data-centric selling also advantages manufacturers with native OPC UA integration, positioning them for Industry 4.0 line contracts.

Global Shrink Sleeve Applicator Industry Leaders

Krones AG

Fujiseal International

Pack Leader Machinery Inc.

Axon Corporation

Sleever International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: ProMach acquired Sentry Equipment and Erectors, broadening conveyor and container handling depth.

- May 2025: Krones posted 2024 revenue of EUR 5.29 billion, up 12.1%, and guided 7–9% growth for 2025.

- April 2025: Krones showcased upgraded PET bottle recycling at PRSE 2025, reinforcing its circular-economy offering.

- February 2025: ProMach formed a Wine and Spirits Solutions Group to tailor integrated lines for distillers.

Global Shrink Sleeve Applicator Market Report Scope

The Shrink Sleeve Applicator Market is segmented by Equipment Type, End-user Vertical, and Geography. The shrink sleeve applicator, also known as heat shrink sleeving labeler, has specifically been designed to make packaging systematic and enhance labeling performance as pack per minute ratios. The shrink sleeve applicators are used in different industries like food, cosmetics, pharmaceuticals, etc.

| Rotary Applicators |

| Linear Applicators |

| Hybrid / Modular Applicators |

| Specialty Band Applicators |

| Manual |

| Semi-automated |

| Fully Automated |

| Full-body Sleeves |

| Neckband / Tamper-evident Bands |

| Multi-pack / Promotional Sleeves |

| Partial / Label Sleeves |

| Food and Beverage |

| Pharmaceuticals |

| Personal Care and Cosmetics |

| Chemicals and Industrial |

| ≤100 BPM |

| 101–300 BPM |

| 301–600 BPM |

| >600 BPM |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics | ||

| Rest of Europe | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| By Equipment Type | Rotary Applicators | ||

| Linear Applicators | |||

| Hybrid / Modular Applicators | |||

| Specialty Band Applicators | |||

| By Automation Level | Manual | ||

| Semi-automated | |||

| Fully Automated | |||

| By Sleeve Application Type | Full-body Sleeves | ||

| Neckband / Tamper-evident Bands | |||

| Multi-pack / Promotional Sleeves | |||

| Partial / Label Sleeves | |||

| By End-use Industry | Food and Beverage | ||

| Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| Chemicals and Industrial | |||

| By Production-Speed Capacity | ≤100 BPM | ||

| 101–300 BPM | |||

| 301–600 BPM | |||

| >600 BPM | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics | |||

| Rest of Europe | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Nigeria | |||

| Rest of Africa | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

Key Questions Answered in the Report

What is the current size of the shrink sleeve applicator market?

It was valued at USD 1,183.68 million in 2025.

How fast is the shrink sleeve applicator market expected to grow?

The forecast CAGR is 4.07% between 2025 and 2030.

Which equipment type dominates sales?

Rotary systems held 64.23% market share in 2024 due to high-speed capability.

Which end-use industry offers the highest growth?

Pharmaceutical packaging leads with a 4.81% CAGR to 2030, driven by tamper-evident regulations.

Page last updated on: