Sharps Containers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

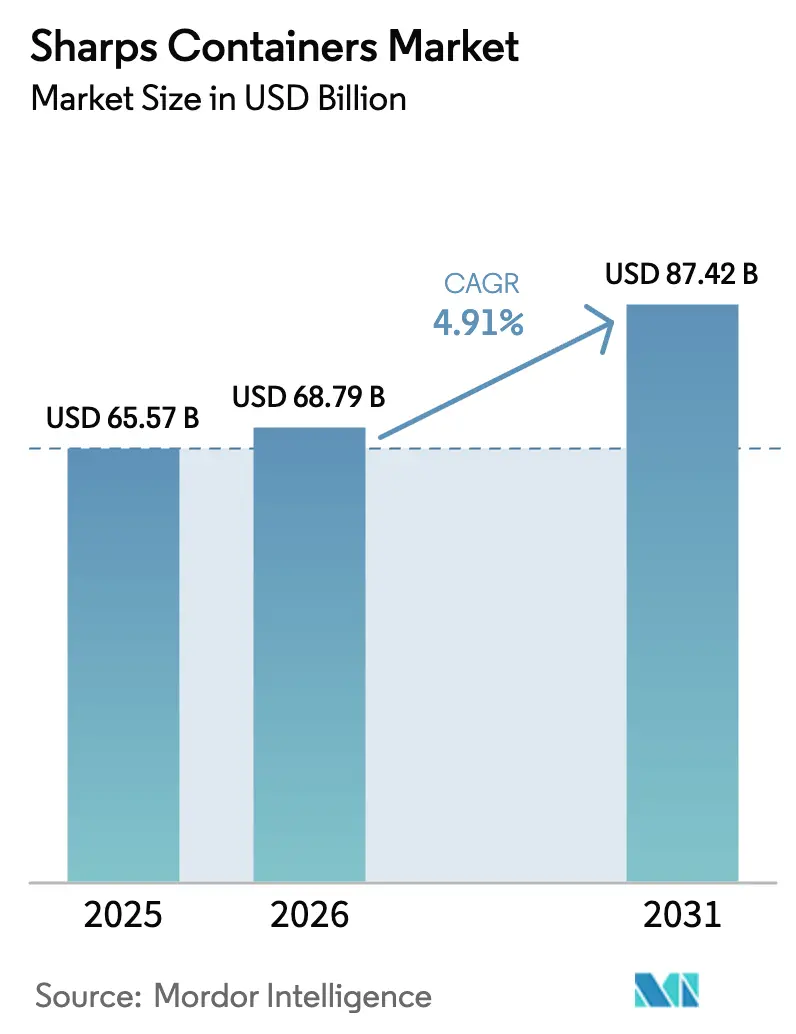

| Market Size (2026) | USD 68.79 Billion |

| Market Size (2031) | USD 87.42 Billion |

| Growth Rate (2026 - 2031) | 4.91% CAGR |

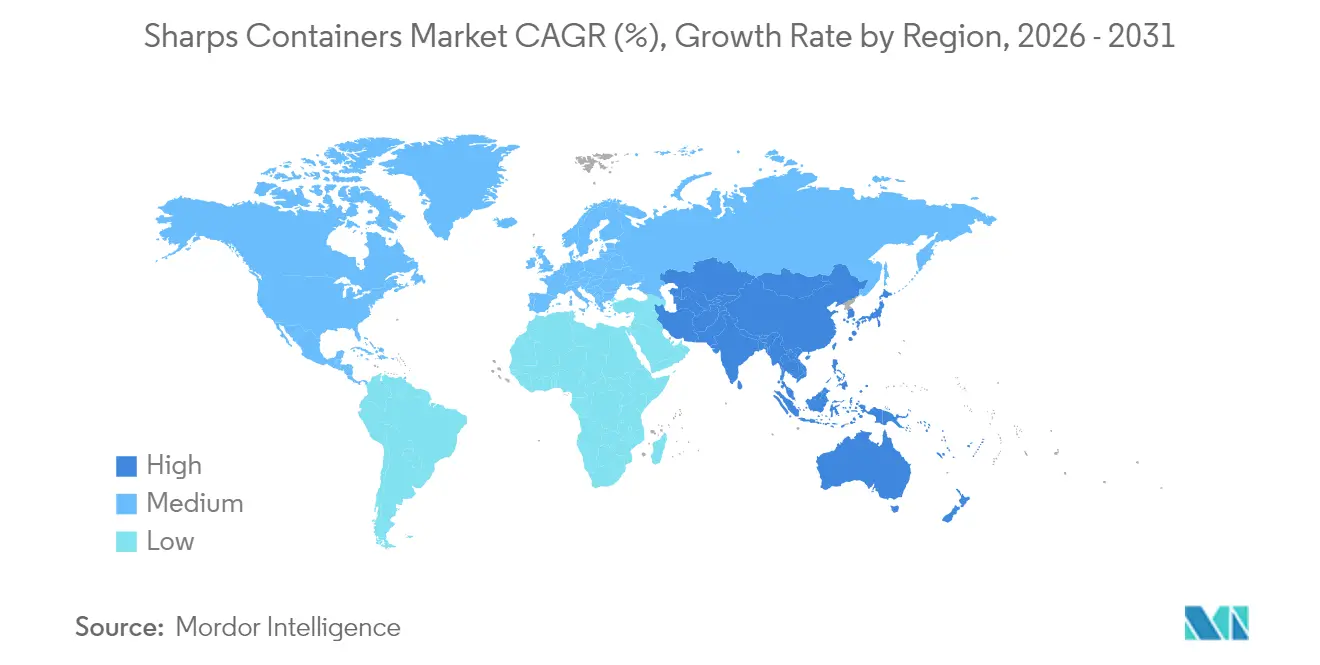

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

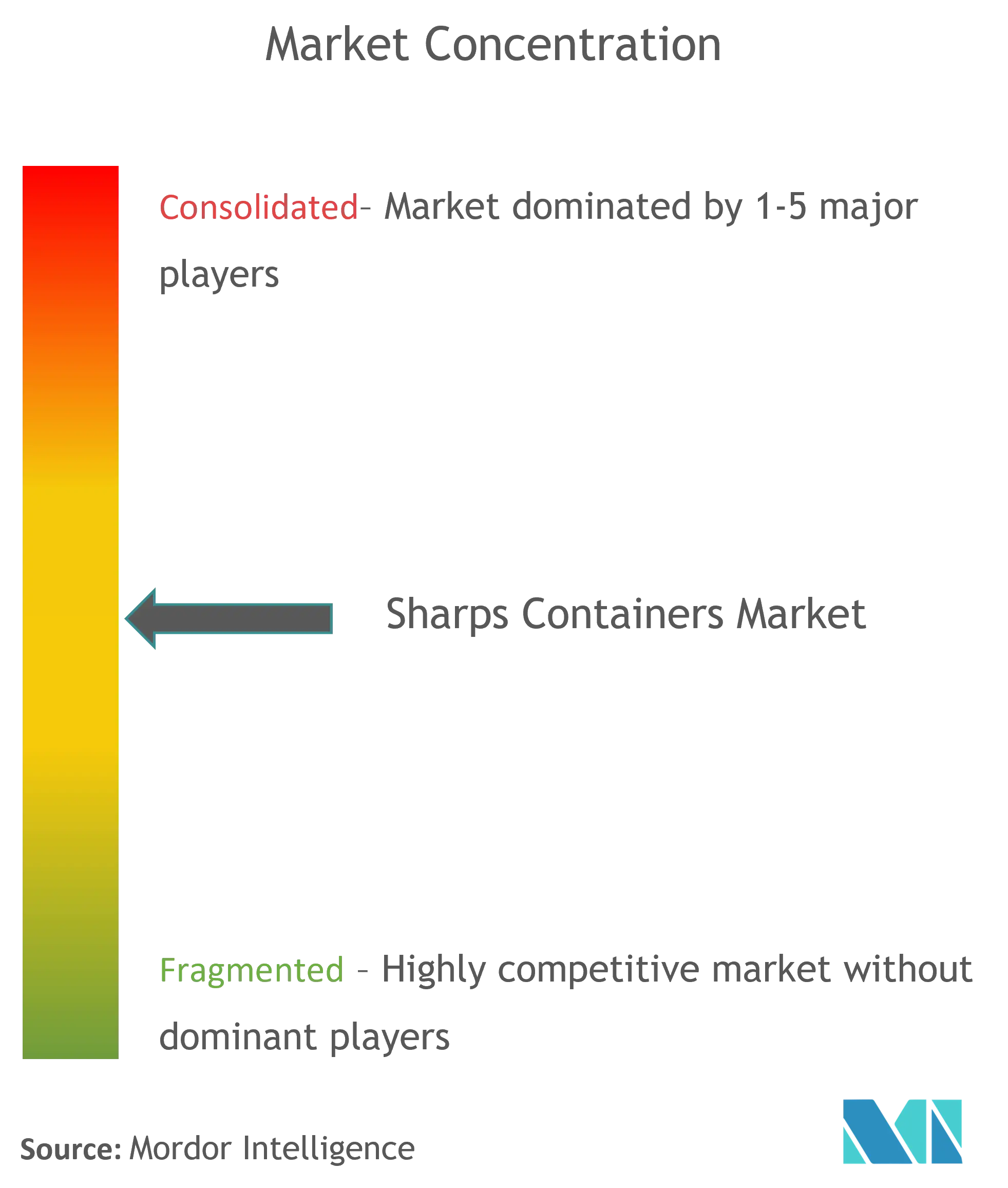

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sharps Containers Market Analysis by Mordor Intelligence

The sharps containers market size was valued at USD 65.57 million in 2025 and estimated to grow from USD 68.79 million in 2026 to reach USD 87.42 million by 2031, at a CAGR of 4.91% during the forecast period (2026-2031). North America remains the revenue anchor, while Asia-Pacific delivers the steepest growth slope. Regulatory tightening, chronic-disease-driven injectable therapy demand, and the pivot toward reusable systems shape competitive positioning. Suppliers are now differentiating on lifecycle compliance, safety engineering, and environmental credentials rather than on container volumes or price alone. Sustainability targets, home-care expansion, and digital procurement are restructuring value creation across the sharps containers market.

Key Report Takeaways

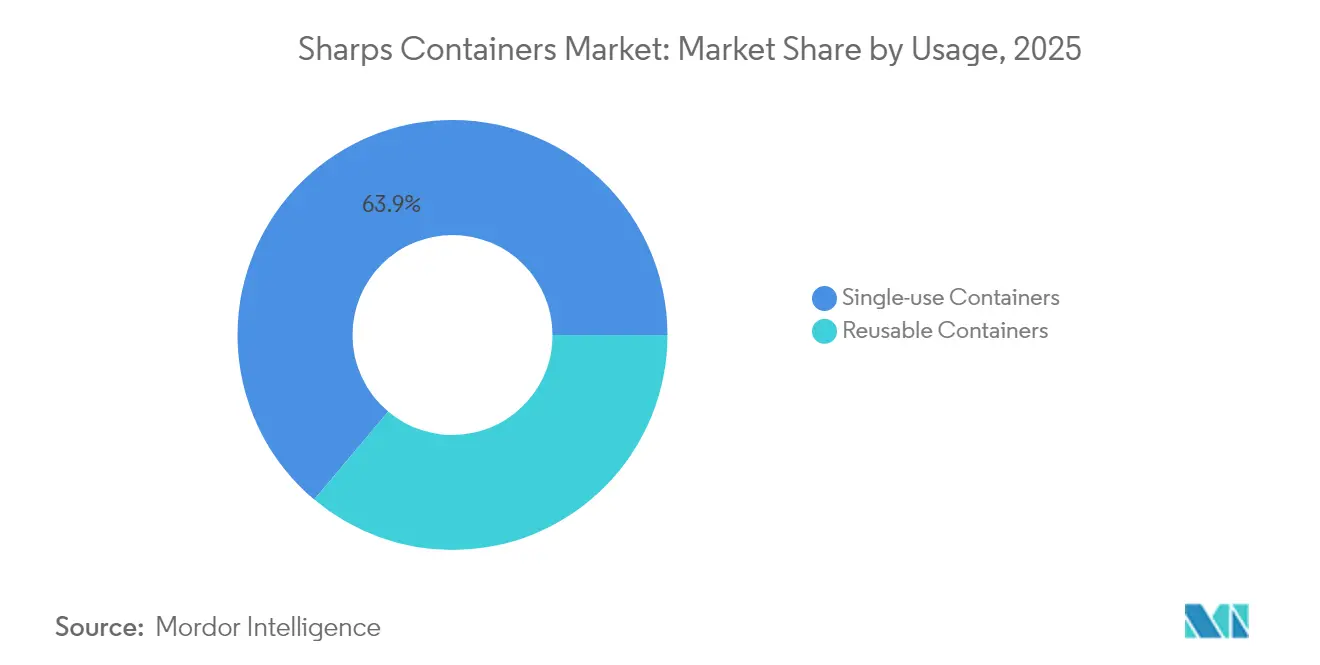

- By usage, single-use systems led with 63.88% revenue share in 2025; reusable solutions are forecast to expand at a 6.28% CAGR through 2031.

- By type, multipurpose designs held 41.90% of the sharps containers market share in 2025, while patient-room units are set to grow fastest at 6.57% CAGR to 2031.

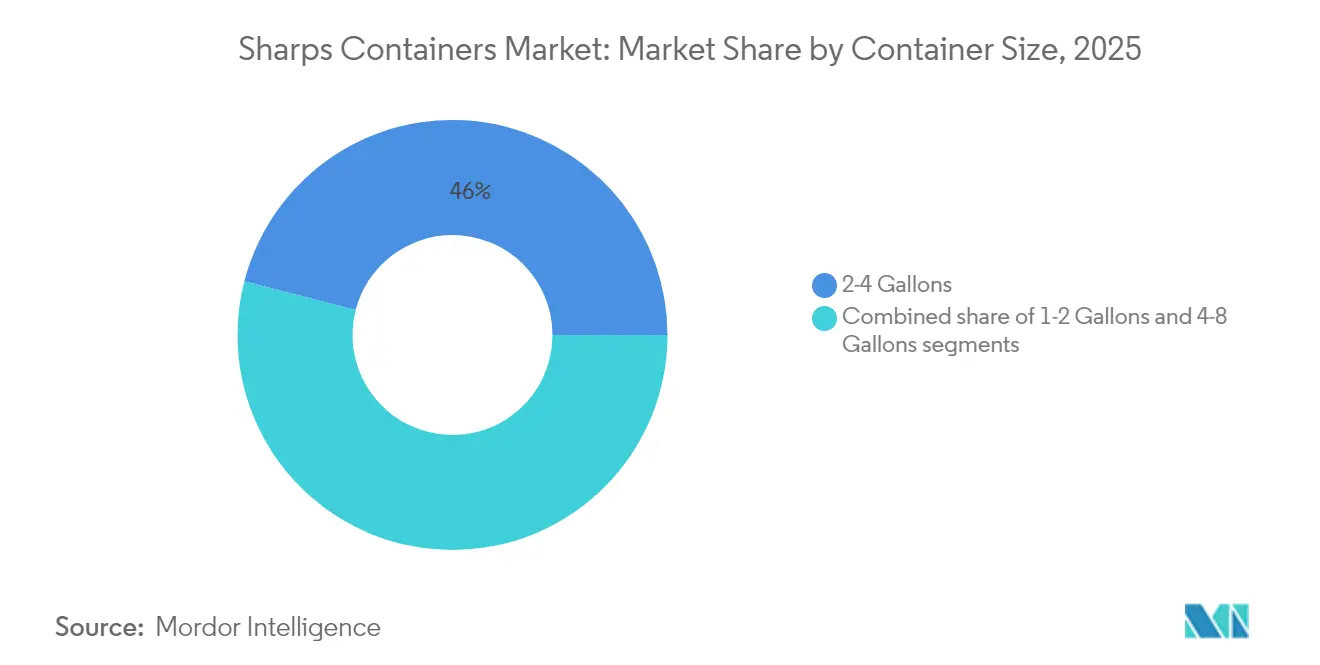

- By container size, the 2-4 gallon band captured 45.98% share of the sharps containers market size in 2025; the 4-8 gallon band will advance at 6.78% CAGR over 2026-2031.

- By distribution channel, direct sales accounted for 50.92% of 2025 revenue; online sales are projected to post a 7.11% CAGR through 2031.

- Geographically, North America led with 35.12% revenue in 2025; Asia-Pacific is forecast to post a 5.44% CAGR, the fastest worldwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sharps Containers Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Healthcare Waste Management Regulations | +1.2% | North America, EU, global roll-out | Long term (≥ 4 years) |

| Growing Healthcare Service Utilization Worldwide | +0.9% | Global; strongest in Asia-Pacific | Medium term (2–4 years) |

| Increasing Prevalence Of Chronic Diseases Requiring Injectable Therapies | +1.1% | Developed economies, expanding globally | Long term (≥ 4 years) |

| Rising Adoption Of Reusable And Eco-Friendly Sharps Disposal Solutions | +0.7% | North America, EU, early adoption in Asia-Pacific | Medium term (2–4 years) |

| Rapid Expansion Of Healthcare Infrastructure In Emerging Markets | +0.8% | Asia-Pacific core, spill-over to Middle East & Africa | Short term (≤ 2 years) |

| Technological Advancements In Safety And Tracking Of Sharps Containers | +0.5% | North America, EU, gradual Asia-Pacific penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Healthcare Waste Regulations

OSHA, FDA, and state-level rule changes, such as Michigan’s 18-month storage allowance for containers < 75% full and Ohio’s pathway for controlled container reuse, require continuous compliance investments. The forthcoming EU Packaging and Packaging Waste Regulation extends recyclability mandates while maintaining patient-safety exemptions, aligning environmental goals with infection-control imperatives. Large vendors leverage compliance expertise to consolidate regional share, while smaller providers exit or partner for scale.

Growing Healthcare Service Utilization Worldwide

Hospital outpatient shifts and home-care therapy growth are accelerating container demand in smaller formats. U.S. hospitals still generate more than 29 lb of waste per occupied bed daily, with sharps a key infectious fraction. Asia-Pacific bed additions and specialty-pharmacy expansion reinforce baseline volume growth.

Increasing Prevalence of Chronic Diseases Requiring Injectable Therapies

The CDC counts 76.4% of U.S. adults with at least one chronic condition in 2025, sustaining high injectable drug volumes[1]Centers for Disease Control and Prevention, “Guidelines for Safe Work Practices in Human and Animal Medical Diagnostic Laboratories,” cdc.gov. GLP-1 pen usage for diabetes and obesity multiplies single-patient sharps waste streams and prompts pharmacy collection programs.

Rising adoption of reusable and eco-friendly sharps disposal solutions

Daniels Health reports 90% CO₂-equivalent reductions and 7,000 lb annual plastic savings per 100 occupied beds when hospitals switch to its Sharpsmart system. ESG-driven procurement increasingly stipulates lifecycle impact metrics, spurring conversion from disposable to reusable systems.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Operational Challenges In Segregation And Collection Of Sharps Waste | -0.8% | Global, most pronounced in developing regions | Medium term (2–4 years) |

| High Cost Of Compliance For Healthcare Facilities | -0.6% | Global, with varying impact by healthcare system maturity | Long term (≥ 4 years) |

| Limited Waste Management Infrastructure In Developing Regions | -0.7% | Developing regions | Long term (≥ 4 years) |

| Supply Chain Disruptions And Raw Material Price Volatility | -0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Operational challenges in segregation and collection

A Portuguese microbiology lab found sharps misclassification in 2.79% of daily waste, heightening exposure risks and disposal costs. Similar findings across emerging markets reveal skills gaps that drive training and technology spending.

High cost of compliance for healthcare facilities

U.S. hospitals spend an estimated USD 760 billion-935 billion annually on waste-related activities, with documentation and audit overhead accounting for a meaningful share. Smaller clinics increasingly outsource to integrated providers to mitigate fixed-cost pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Usage: Reusable Systems Challenge Disposable Dominance

Single-use units kept a 63.88% revenue lead in 2025. However, reusable formats are projected to grow at 6.28% CAGR, supported by lifecycle cost modeling and ESG scoring. Daniels Health documents up to 87% cuts in container-related needlestick injuries after reusable adoption. Large hospital networks account for most conversions, aligning with volume thresholds that justify processing infrastructure. The sharps containers market size for reusable formats is expected to surpass USD 34.1 million by 2031 alongside regulatory credits tied to carbon disclosure.

Reusable penetration faces logistics hurdles in small practices, yet service providers now offer regional processing hubs and RFID-enabled asset tracking to close capability gaps. As public sustainability reporting frameworks such as GRI expand into healthcare, reusable share gains will accelerate.

By Type: Patient-Room Containers Drive Point-Of-Care Efficiency

Multipurpose containers held 41.90% revenue in 2025. Patient-room designs will register the fastest gains at 6.57% CAGR thanks to bedside care models. Horizontal entry lids, clear fill windows, and wall-mount frames reduce transport steps and injury exposure. Clinical evidence links immediate disposal at the use site with reduced needlestick events, reinforcing procurement preference.

Engineered features now include passive overfill locks and tamper-evident seals to satisfy OSHA’s secure-closure criteria. Suppliers offering modular mounting kits capture incremental revenue from retrofit projects in existing wards.

By Container Size: Mid-Range Capacity Optimizes Handling Efficiency

The 2-4 gallon class commanded 45.98% of revenue in 2025. Yet high-acuity departments increasingly favor 4-8 gallon vessels, propelling a 6.78% CAGR. Larger bins cut change-out labor and support RFID-based route optimization. Conversely, 1-2 gallon units defend share in home infusion and ambulatory surgery centers where storage footprints are constrained.

Hospitals adopt mixed-size strategies mapped to procedural throughput analytics. The sharps containers market share held by 4-8 gallon models is forecast to climb to 32.40% by 2031, reshaping SKU portfolios.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Direct contracts still deliver 50.92% of 2025 revenue, driven by consultative selling. Online platforms will grow at 7.11% CAGR as group purchasing organizations automate reorder workflows. Henry Schein’s marketplace expansion to 8,000 non-clinical SKUs exemplifies the pivot to e-procurement convenience. Vendor portals now integrate SDS libraries and compliance dashboards, embedding value beyond price.

Geography Analysis

North America generated 35.12% of 2025 revenue and posts stable low-single-digit growth under mature OSHA-FDA oversight. Hospitals deploy smart fill-level telemetry and statewide rule updates, such as Michigan’s storage-period extension, to fine-tune collection logistics. The sharps containers market size in the region reached USD 24.15 million in 2026 and is projected at USD 30.66 million by 2031.

Asia-Pacific is the sprint leader with 5.44% CAGR. China and India’s hospital bed expansions, coupled with 774 metric-ton daily biomedical waste peaks, strain existing disposal capacity and unlock demand for compliant sharps solutions. Government funding for waste-treatment plants and private-hospital chains catalyze procurement cycles. Cross-border suppliers partner with local collectors to navigate evolving licensing norms.

Europe maintains moderate growth as the EU’s 2025/40 packaging regulation incentivizes recyclable and reusable medical packaging while retaining infection-control provisions. Scandinavian and UK health systems highlight 90% CO2 reductions from reusable programs, setting reference benchmarks for continental tenders.

South America, Middle East, and Africa show heterogeneous patterns. Gulf Cooperation Council hospitals pursue JCI accreditation, lifting demand for UN-rated containers, while parts of Africa face capacity shortfalls that delay market development.

Mordor Intelligence provides coverage of the sharps containers market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The sharps containers market is moderately consolidated. Waste Management’s USD 7.2 billion purchase of Stericycle formed a vertically integrated leader with national hauling, treatment, and mail-back services, unlocking over USD 125 million annual synergies. Daniels Health remains the reference brand for engineered reusable systems, operating automated washlines across five continents. BD supports containers through its Medication Delivery franchise and invests USD 2.5 billion in U.S. device capacity to secure syringe supply, indirectly boosting disposal volumes[3]BD Increases Domestic Production to Support U.S. Health Care Need for Syringes,” news.bd.com.

Disruptors such as Sharps Technology target prefillable syringe niches and home-care mail-back kits. Regional service specialists bundle container leasing with route-based pickup to protect share against the WM-Stericycle behemoth. Competitive success now hinges on proof-of-injury reduction, Scope 3 emission reporting, and digital traceability integration rather than on container commoditization.

Sharps Containers Industry Leaders

Stericycle

Sharps Compliance, Inc.

Becton, Dickinson & Co.

Daniels Health

Cardinal Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Henry Schein reported USD 3.168 billion Q1 net sales with 3% constant-currency growth in global medical distribution.

- November 2024: WM closed the USD 7.2 billion Stericycle acquisition, forming the largest integrated medical-waste platform.

- August 2024: BD agreed to acquire Edwards Lifesciences’ Critical Care Product Group for USD 4.2 billion, expanding its Medical segment.

- June 2024: Sharps Technology secured a five-year USD 200 million syringe sales pact, funding U.S. production scaling.

- May 2024: BD unveiled a USD 2.5 billion five-year U.S. manufacturing investment plan covering container-compatible devices.

Global Sharps Containers Market Report Scope

As per the scope of the report, a sharps container is a hard plastic container utilized for the disposal of hypodermic needles and other sharp medical items, including IV catheters and disposable scalpels, in a safe manner. The containers are frequently sealable, self-locking, and robust, thereby blocking waste from penetrating the container's surfaces. The sharps containers market is segmented by usage (single-use containers, and reusable containers), type (patient room containers, phlebotomy containers, and multipurpose containers), container size (1-2 gallons, 2-4 gallons, and 4-8 gallons), distribution channel (direct sale, online sale, and retail sale), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Single-Use Containers |

| Reusable Containers |

| Patient-Room Containers |

| Phlebotomy Containers |

| Multipurpose Containers |

| 1-2 Gallons |

| 2-4 Gallons |

| 4-8 Gallons |

| Direct Sale |

| Online Sale |

| Retail Sale |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Rest of the World |

| By Usage | Single-Use Containers | |

| Reusable Containers | ||

| By Type | Patient-Room Containers | |

| Phlebotomy Containers | ||

| Multipurpose Containers | ||

| By Container Size | 1-2 Gallons | |

| 2-4 Gallons | ||

| 4-8 Gallons | ||

| By Distribution Channel | Direct Sale | |

| Online Sale | ||

| Retail Sale | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Rest of the World | ||

Key Questions Answered in the Report

What is the current value of the global sharps containers market in 2026?

The market stands at USD 68.79 million in 2026.

Why are reusable sharps containers gaining share so quickly?

Reusable systems cut carbon emissions by up to 90% and reduce needlestick injuries by about 87%, giving hospitals both ESG and safety payoffs that offset processing costs.

Which region will post the fastest revenue growth?

Asia-Pacific is projected to expand at 5.44% CAGR, powered by hospital infrastructure investment and rising injectable therapy volumes in China and India.

How is digital procurement affecting distribution channels?

Online platforms are forecast to grow at 7.11% CAGR as health systems automate reorder workflows and integrate compliance documentation, eroding purely direct-sales reliance.

What impact did Waste Management’s acquisition of Stericycle create?

The USD 7.2 billion deal formed a single entity handling more than half of North American regulated medical waste, raising competitive scale thresholds for smaller service providers.

Are container size preferences changing?

Yes. High-acuity departments are rotating to 4-8 gallon bins for labor efficiency, while home-care and ambulatory centers still favor 1-2 gallon formats for space optimization.

Page last updated on: