Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

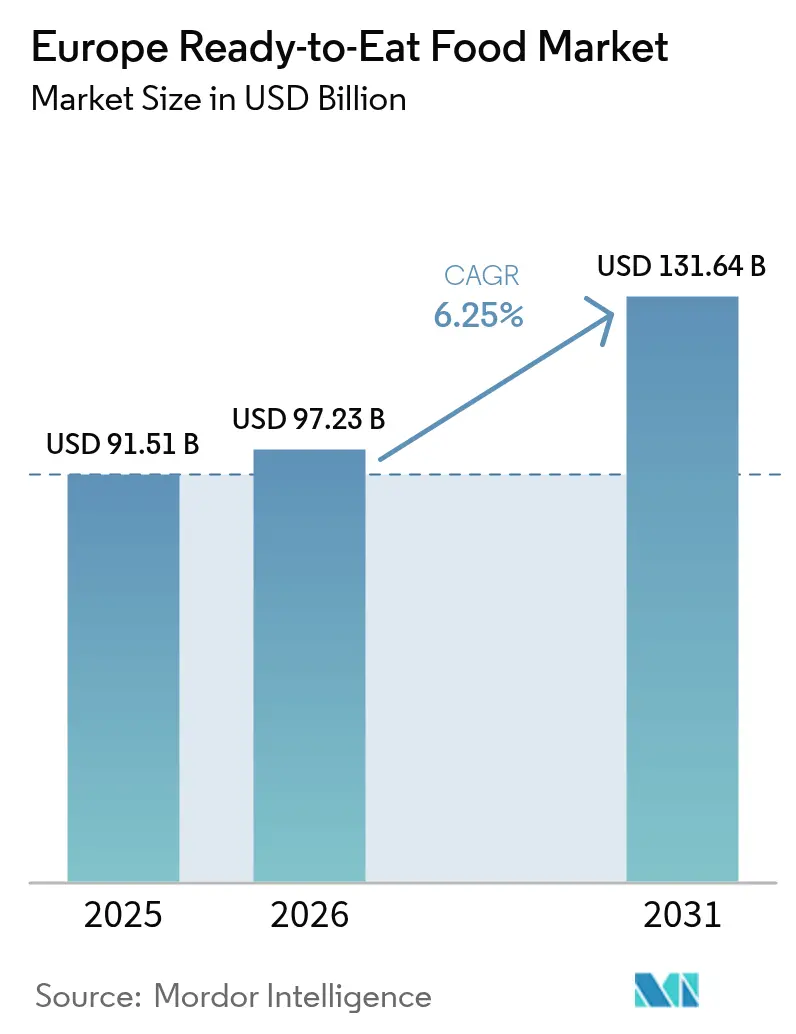

| Base Year Market Size (2025) | USD 91.51 Billion |

| Market Size (2026) | USD 97.23 Billion |

| Market Size (2031) | USD 131.64 Billion |

| Growth Rate (2026 - 2031) | 6.25% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Ready-to-Eat Food Market Analysis by Mordor Intelligence

The Europe ready to eat food market size is expected to grow from USD 91.51 billion in 2025 to USD 97.23 billion in 2026 and is forecast to reach USD 131.64 billion by 2031 at 6.25% CAGR over 2026-2031. Factors such as urbanization, an uptick in single-person households, and a surge in dual-income families are reshaping dining habits. This shift is driving a heightened demand for premium, portion-controlled convenience products that prioritize both flavor and nutritional clarity. Innovations in packaging, especially Modified Atmosphere Packaging (MAP), are not only broadening distribution channels but also minimizing waste by prolonging the shelf life of both chilled and shelf-stable products. As consumers become more discerning about ingredient sourcing and processing, there's a notable shift towards plant-based and organic alternatives, further fueling value growth. The e-commerce boom, initially spurred by the pandemic, has solidified its presence, making online grocery shopping the fastest-growing channel and intensifying competition in logistics. On the supply front, Europe's food-processing hubs are witnessing a surge in automation investments, enabling major players to safeguard their margins amidst escalating energy and labor costs.

Key Report Takeaways

- By product type, ready meals led with 36.12% revenue share in 2025, while meat products are projected to expand at a 7.2% CAGR through 2031.

- By category, conventional offerings held 77.95% of the European ready-to-eat food market share in 2025, whereas organic/clean-label lines record the fastest 7.68% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets commanded 61.15% of the 2025 value, while online retail stores registered an 7.85% CAGR through 2031.

- By geography, Germany captured 18.32% of 2025 revenue; Poland posts the quickest 6.68% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Ready-to-Eat Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising number of single-person households and dual-income families | +0.9% | Germany, France, United Kingdom. | Medium term (2-4 years) |

| Advancements in shelf-stable and chilled packaging technology | +0.8% | European Union-wide, led by Germany and Netherlands | Long term (≥ 4 years) |

| Demand for plant-based and alternative protein meals | +1.1% | Northern Europe, expanding south | Medium term (2-4 years) |

| Growth in the food processing industry | +0.9% | Germany, France, Italy, Poland | Long term (≥ 4 years) |

| Product innovation and flavor diversification | +0.7% | Germany, United Kingdom., France, Nordics | Short term (≤ 2 years) |

| Changing consumer lifestyles | +0.8% | Urban centers across Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising number of single-person households and dual-income families

The growing number of single-person households in Europe is reshaping the ready-to-eat (RTE) food market, boosting demand for single-serve and individually portioned meals. Eurostat data shows that between 2015 and 2024, single-person households without children in the European Union increased by 16.9%, compared to a 5.8% rise in all households [1]Source: Eurostat, "Household composition statistics', ec.europa.eu. This demographic shift has driven consistent demand for portion-controlled, shelf-stable products that help reduce food waste while providing restaurant-quality experiences at home. The trend is further supported by the rise of dual-income families. In 2024, Eurostat reported that 57.8% of European Union households had all adults employed, either part-time or full-time [2]Source: Eurostat, "Household composition statistics', ec.europa.eu. This reduces available cooking time and increases the willingness to pay a premium for convenience without sacrificing nutritional quality. Furthermore, smaller households spend more per capita on premium ready meals than traditional family units, driving not only volume growth but also product sophistication. Companies that offer single-serve formats and position their products as premium are well-placed to capture significant value in this expanding market segment.

Advancements in shelf-stable and chilled packaging technology

Technological advancements in Modified Atmosphere Packaging (MAP) are transforming supply chains and market reach for European ready-to-eat meal producers. These innovations extend product shelf life by 2 to 5 times compared to traditional packaging methods. Advanced gas-flush systems, which precisely balance CO2, N2, and O2, now preserve product integrity for weeks instead of days. This enables manufacturers to serve wider geographic markets while significantly reducing food waste across the value chain. The technology is particularly impactful for meat products and fresh pasta segments, where extended shelf life facilitates export opportunities and supports premium market positioning by maintaining visual appeal and nutritional value. European packaging machinery suppliers report a rapid increase in MAP adoption as producers seek to differentiate themselves through extended freshness claims. Implementation costs are offset by simplified logistics and expanded market access.

Demand for plant-based and alternative protein meals

The plant-based segment holds a premium position in the European ready-to-eat (RTE) food market by attracting consumers focused on health, sustainability, and innovative, experience-driven food options. These plant-based RTE products are priced higher than conventional alternatives, reflecting consumers' willingness to pay more for health benefits, clean-label ingredients, and sustainable sourcing. This trend allows manufacturers to achieve higher profit margins, particularly as demand for "better-for-you" and eco-conscious products grows, especially among affluent urban populations. According to the Good Food Institute, in 2024, approximately 40% of adults in Germany and the United Kingdom plan to increase their consumption of plant-based foods. Health considerations drive 48% of this shift, followed by environmental concerns at 29%, and animal welfare at 25% [3]Source: Good Food Institute, "State of the Industry 2024", gfi.org. The segment also gains momentum from European Union sustainability frameworks that promote plant-forward nutrition, aligning policies to support market growth. Food technologists are accelerating innovation cycles, developing protein-rich formulations from pea, soy, and other novel ingredients to deliver sensory experiences comparable to traditional meat. Distribution partnerships with mainstream retailers are helping plant-based ready meals transition from niche to mainstream, with major supermarket chains dedicating more shelf space to meet the growing demand for sustainable and convenient food options.

Growth in the food processing industry

The European ready-to-eat (RTE) food market is experiencing robust growth, driven by the modernization of the food processing industry. Investments in automation, advanced packaging, sensor technology, and innovative sterilization processes are enabling companies to enhance production volumes while improving efficiency, consistency, and safety. These advancements allow manufacturers to expand their product portfolios, reduce costs, and comply with the strict quality and traceability standards demanded by modern European consumers. This wave of modernization is particularly beneficial for RTE producers. By utilizing automated portioning, packaging, and quality control systems, they are effectively addressing increasing demand while maintaining profitability. However, the industry is undergoing consolidation as smaller producers face challenges in meeting the capital requirements for competitive manufacturing. This shift creates opportunities for well-capitalized companies to strengthen their market position through superior operational performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-processed food scrutiny creates reformulation pressure | -0.5% | European Union-wide, varied by member state | Medium term (2-4 years) |

| Perceived lack of freshness and quality | -0.4% | Germany, France, Nordics | Short term (≤ 2 years) |

| Heightened nutritional-transparency expectations | -0.4% | European Union-wide, health-driven consumers | Medium term (2-4 years) |

| Premium pricing vulnerability amid economic headwinds | -0.6% | Eastern Europe, during downturns | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ultra-processed food scrutiny creates reformulation pressure

Growing consumer awareness of the health risks associated with ultra-processed foods is driving regulatory momentum across European markets. However, the likelihood of comprehensive legislation remains low despite increasing pressure. The European Food Safety Authority (EFSA) continues to prioritize novel food assessments and nutritional transparency, adding complexity to compliance for ready-to-eat food manufacturers, particularly those with extensive ingredient lists or reliance on processing aids. At the same time, consumer advocacy groups are using the NOVA classification system to influence purchasing behavior, compelling companies to invest in reformulating products to reduce processing intensity while preserving taste and shelf stability. This regulatory uncertainty is challenging for companies, as it extends innovation timelines and raises development costs while they navigate evolving compliance requirements and maintain competitive positioning.

Premium pricing vulnerability amid economic headwinds

Economic challenges are impacting the European ready-to-eat (RTE) food market. Premium pricing, a key feature of RTE products, is increasingly deterring price-sensitive consumers. Consequently, category growth is slowing, and many consumers are turning to more affordable alternatives, such as private labels and discount brands. This trend is particularly evident during periods of inflation, rising living costs, or economic uncertainty. RTE products are generally priced at 2-3 times the cost of home-cooked meals, creating a significant affordability gap during economic downturns or inflationary cycles. In Eastern Europe, for example, consumers exhibit heightened price sensitivity toward premium ready meals. This forces manufacturers to navigate the challenge of maintaining margins while preserving sales volumes. The situation is further aggravated by elevated energy prices, which remain higher than pre-2022 levels. This not only increases production costs but also reduces consumer purchasing power across the value chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ready Meals Retain Lead while Meat Options Accelerate

Ready meals contributed 36.12% of total revenue in 2025, emphasizing their popularity among time-constrained consumers. With brands introducing seasonal flavors and diverse cuisines, the European ready-to-eat food market is expected to grow steadily. Birds Eye’s Mediterranean pasta range showcases the industry's move toward vegetable-focused options that combine indulgence with health benefits. Additionally, meat products, growing at a 7.2% CAGR (2026-2031), benefit from their high-protein appeal and advanced MAP solutions that preserve freshness and color. Fitness-focused consumers in markets like Germany and the U.K. increasingly prefer macro-labeled packaging, driving greater household adoption.

Instant breakfasts and soups continue to experience stable demand, supported by innovative sachet designs. Baked goods are adapting to the clean-label trend by replacing preservatives with natural enzymes. The "other" category, which primarily includes plant-based and ethnic specialties, acts as an incubator for niche concepts that could transition to mainstream retail. Across all segments, companies navigate EFSA’s novel food pathway, weighing dossier costs against the advantages of being a first mover.

By Category: Conventional Lines Large but Organic Momentum Builds

Conventional SKUs continue to dominate 77.95% of shelf space in 2025, primarily due to their affordability and well-established supply chains. However, the European ready-to-eat food market is experiencing a significant transformation. Organic and clean-label alternatives are gaining traction, growing at a compound annual growth rate (CAGR) of 7.68% (2026-2031) and commanding a price premium of 15-25%. To strengthen their sustainability credentials and compete with national brands, continental retailers are increasingly focusing on private-label organic products. Producers are addressing consumer concerns by reducing the use of E-numbers, simplifying ingredient lists, and prominently displaying European Union organic logos to build trust and confidence among shoppers.

In response to this shift, conventional operators are adapting by simplifying recipes, lowering sodium levels, and leveraging economies of scale to maintain their position in entry-level price tiers. Although the costs associated with organic certification and the scarcity of raw materials can drive up margins for organic products, consumers are willing to pay the premium, associating it with trustworthiness and environmental responsibility. As a result, the market accommodates both segments: price-sensitive households tend to prefer conventional options, while more affluent consumers gravitate toward clean-label alternatives. Together, these dynamics are driving the overall growth of the European ready-to-eat food market.

By Distribution Channel: Digital Grocery Gains Sustain Momentum

Supermarkets and hypermarkets contributed 61.15% of the turnover in 2025, capitalizing on in-store merchandising to meet immediate consumption needs. Their scale enables supermarkets to secure favorable pricing from suppliers, allowing them to provide promotions or value packs. This approach makes ready-to-eat (RTE) foods more accessible to a wider audience. However, online retail is the fastest-growing segment in Europe's ready-to-eat food market, with a notable 7.85% CAGR (2026-2031). Pure-play platforms and omnichannel grocers enhance the shopping experience through subscription replenishments, bundled deals, and transparent search filters, which streamline the discovery of niche SKUs. Additionally, improvements in cold-chain reliability, supported by insulated totes and time-slot deliveries, have significantly narrowed the quality gap with traditional brick-and-mortar stores.

Convenience stores continue to play a key role in providing quick meals and late-night options. At the same time, foodservice outlets and vending machines expand their presence in workplaces and universities. Manufacturers are designing pack sizes to suit specific channels: family multipacks for hypermarkets, single-serve pouches for e-commerce, and heat-to-eat trays for petrol forecourts. As retailer demands for promotional funding increase, direct-to-consumer pilots are becoming more attractive for their ability to capture data and manage margins effectively.

Geography Analysis

Germany holds an 18.32% market share in 2025, reflecting its position as Europe's largest consumer base. With advanced food processing capabilities and high disposable incomes, Germany leads in premium ready-to-eat consumption. The country excels in the organic and clean-label segments, with consumers willing to pay 20-30% more for products that meet sustainability and health standards. Its robust logistics infrastructure and strong retail partnerships ensure efficient distribution across the DACH region. Additionally, compliance with EFSA guidelines supports product innovation, particularly in novel foods and nutritional claims.

Poland is emerging as Europe's fastest-growing ready-to-eat market, with a projected 6.68% CAGR through 2031. This growth is driven by rapid urbanization, rising disposable incomes, and younger consumers adopting Western European consumption patterns. Significant foreign direct investments in food processing and retail modernization further enhance product availability and quality. In contrast, France, Italy, and Spain, as mature markets, are shaped by distinct regional preferences. These preferences influence product development, particularly in ethnic cuisines and traditional flavors that appeal to local tastes. These markets remain resilient by focusing on premium positioning and health-conscious innovations aligned with Mediterranean dietary traditions. The United Kingdom continues to maintain a strong market presence despite post-Brexit trade challenges. Companies have adapted supply chains and regulatory processes to serve this critical consumer base. In the Nordics, countries like Sweden play a significant role in premium and sustainable segments, with consumers driving advancements in plant-based alternatives and eco-friendly packaging. The Netherlands and Belgium leverage their strategic locations and advanced cold-chain logistics to act as key distribution hubs for Northern Europe. Meanwhile, Eastern European countries, such as the Czech Republic and Hungary, are showing growth potential as economic development accelerates the adoption of convenience foods, following patterns seen in Western Europe.

Competitive Landscape

The European ready-to-eat food market is moderately fragmented. Established multinational players hold a significant market presence but are increasingly challenged by regional specialists and emerging plant-based disruptors. The market's concentration is largely due to the capital-intensive nature of modern food processing, cold-chain distribution, and the need for regulatory compliance. These factors create barriers, favoring well-capitalized incumbents with established retail ties. Strategic maneuvers highlight a trend towards portfolio diversification, spanning product categories, geographic markets, and price points, all aimed at aligning with shifting consumer preferences while leveraging operational scale advantages.

Technology adoption stands out as a pivotal competitive edge. Leading firms are channeling investments into automated production lines, cutting-edge packaging systems, and data analytics. These advancements not only facilitate personalized product development but also optimize the supply chain. Key players like McCain Foods Limited, Nomad Foods Ltd, Dr. Oetker KG, Kraft Heinz Company, and Nestlé SA are honing in on packaging. For them, packaging is crucial in preserving product quality, vitamin content, taste, texture, color, and shelf-life. Given the industry's high profitability, manufacturers are crafting robust competitive strategies, heightening the competition among them. Product innovation has become the primary strategy for these major players, aiming to solidify their foothold in the market.

There's a burgeoning interest in premium ethnic cuisines, functional nutrition, and eco-friendly packaging innovations that not only address environmental concerns but also uphold product integrity. In January 2025, merger and acquisition activity underscored this trend, with Valeo Foods making headlines through its EUR 200 million acquisition of I.D.C. Holding. Such moves highlight the industry's consolidation as firms chase scale advantages and broader geographic footprints. Meanwhile, emerging disruptors are capitalizing on direct-to-consumer channels and subscription models. By sidestepping traditional retail gatekeepers, they're fostering brand loyalty through tailored offerings and a sustainability stance that resonates with eco-conscious consumers.

Europe Ready-to-Eat Food Industry Leaders

-

McCain Foods Limited

-

Nestlé S.A.

-

Nomad Foods Ltd

-

The Kraft Heinz Company

-

Dr. Oetker KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Batchelors, a brand under Premier Foods introduced its "Meals in Minutes" range of ambient ready meals in select Sainsbury's stores. These meals, priced at GBP 3.50 for 300ml pouches, are designed to appeal to busy professionals seeking convenient options with enhanced flavors. This initiative highlights Premier Foods' efforts to broaden its demographic reach beyond the traditional instant meal categories.

- March 2025: Mars Food and Nutrition expanded its ambient ready meal portfolio by launching 14 new SKUs under the Ben's Original and Dolmio brands. The company introduced three HFSS-compliant ranges, priced at approximately GBP 3 for 250g pouches, in major retailers such as Sainsbury's, Morrisons, and Iceland. This initiative highlights Mars' commitment to offering healthier formulations while maintaining its focus on convenience.

- February 2025: Chefees, a Malaysian brand specializing in frozen meal kits entered the United Kingdom market. The brand provides flash-frozen recipe boxes with a freezer shelf life exceeding one year. For its United Kingdom operations, Chefees has partnered with Oaklands International for logistics and aims to secure retail listings with leading chains, Waitrose and Sainsbury's.

- January 2025: Kitchen Joy introduced its Thai ready meals range at Tesco United Kingdom, featuring takeout-inspired packaging, which underscores the growth of ethnic-flavored chilled ready meals and retailer-driven innovation in convenience positioning.

Europe Ready-to-Eat Food Market Report Scope

Ready-to-eat foods are pre-cooked, pre-cleaned, mostly packaged, and ready for consumption without prior preparation or cooking. They are highly preferred for the convenience they offer.

The European ready-to-eat food market is segmented into type, distribution channel, and geography. Based on type, the market is segmented into instant breakfast/cereals, instant soups frozen snacks, meat snacks, ready meals, and instant noodles. Based on distribution channels, the market is segmented into hypermarkets/supermarkets, convenience stores/grocery stores, online retail stores, and other distribution channels. The report gives a detailed analysis of emerging economies in the European region, namely the United Kingdom, Germany, Spain, France, Italy, Russia, and the Rest of Europe.

For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

Product Type

| Instant Breakfast / Cereals |

| Instant Soups and Snacks |

| Ready Meals |

| Baked Goods |

| Meat Products |

| Other Product Types |

Category

| Conventional |

| Organic/Clean Label |

Distribution Channels

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Retail Channels |

Countries

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Russia |

| Sweden |

| Belgium |

| Poland |

| Netherlands |

| Rest of Europe |

| Product Type | Instant Breakfast / Cereals |

| Instant Soups and Snacks | |

| Ready Meals | |

| Baked Goods | |

| Meat Products | |

| Other Product Types | |

| Category | Conventional |

| Organic/Clean Label | |

| Distribution Channels | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Retail Channels | |

| Countries | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

How big is the Europe ready-to-eat food market in 2026?

The Europe ready to eat food market size is USD 97.23 billion in 2026.

What is the expected growth rate for ready meals through 2031?

Ready meals are forecast to advance at a 6.25% overall CAGR, while meat products lead segment growth at 7.2%.

Which country dominates sales today?

Germany holds 18.32% of total 2025 revenue, leveraging high purchasing power and advanced processing capacity.

Which distribution channel is expanding fastest?

Online retail stores post the highest 7.85% CAGR as shoppers migrate to digital grocery platforms.

Page last updated on: