Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

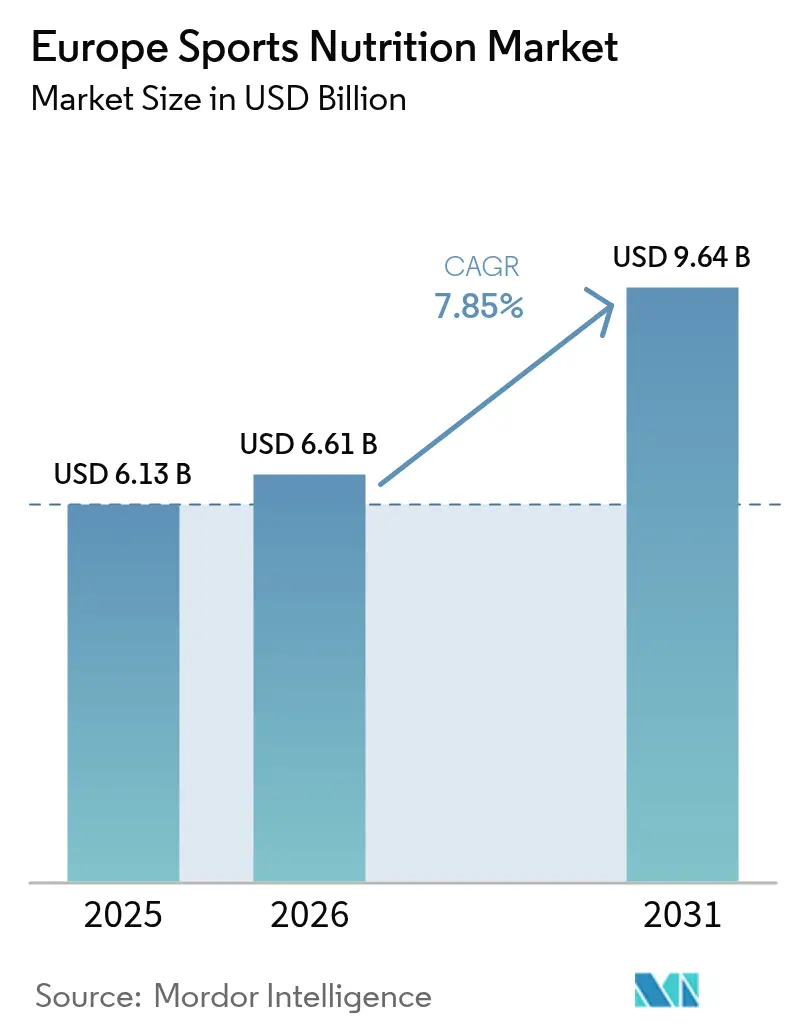

| Base Year Market Size (2025) | USD 6.13 Billion |

| Market Size (2026) | USD 6.61 Billion |

| Market Size (2031) | USD 9.64 Billion |

| Growth Rate (2026 - 2031) | 7.85% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Sports Nutrition Market Analysis by Mordor Intelligence

The Europe sports nutrition market size is expected to grow from USD 6.13 billion in 2025 to USD 6.61 billion in 2026 and is forecast to reach USD 9.64 billion by 2031 at 7.85% CAGR over 2026-2031. The robust outlook reflects a broadening consumer base that now includes millennials, Gen Z, and active seniors who integrate performance products into daily wellness routines. The rising popularity of gym memberships, recreational activities, and endurance sports is driving the demand for performance-enhancing nutritional supplements such as pre-workouts and protein products. Product innovations, including ready-to-drink formats, bars, and clinically tested ingredients, improve convenience and effectiveness, appealing to a broader range of consumers. Additionally, sports nutrition is increasingly being used by non-athletes for general wellness, weight management, and healthy aging, thereby expanding its consumer base. Fitness culture investments, a shift toward plant-based, clean-label ingredients, and omnichannel retail advances also reinforce consumption momentum. Meanwhile, intensified enforcement against counterfeit goods bolsters consumer trust and favors compliant brands.

Key Report Takeaways

- By product type, Sports Protein Products led with 68.24% of Europe sports nutrition market share in 2025. Sports Non-Protein Products are forecast to expand at an 8.35% CAGR through 2031, the fastest among product segments.

- By distribution channel, Online Retail Stores held 56.31% of the Europe sports nutrition market size in 2025. Supermarkets and Hypermarkets record the highest projected CAGR at 9.35% through 2031.

- By geography, the United Kingdom accounted for a 32.06% share of the Europe sports nutrition market size in 2025. Germany posts the quickest national growth pace with a 10.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Sports Nutrition Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health and fitness consciousness among Millennials and Gen Z | +1.8% | Germany, Netherlands, Sweden | Medium term (2-4 years) |

| Expansion of plant-based and clean-label formulations | +1.5% | Germany, France, Netherlands | Long term (≥ 4 years) |

| Premiumisation of protein snacks and RTD beverages | +1.2% | UK, Germany, France, Italy | Medium term (2-4 years) |

| Rising participation in fitness activities and sports | +1.0% | Germany, Sweden, Netherlands | Long term (≥ 4 years) |

| Influence of social media and fitness influencers | +0.9% | UK, Germany, France | Short term (≤ 2 years) |

| Demand for personalized nutrition and niche products | +0.8% | UK, Germany, Switzerland, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising health and fitness consciousness among millennials and gen Z

Demographic transformation drives market expansion as younger consumers integrate sports nutrition into daily wellness routines rather than limiting usage to athletic performance. This generational shift creates sustained demand beyond traditional gym-centric consumption patterns. Growing participation in gym workouts, outdoor sports, yoga, and fitness challenges is driving consistent demand for performance-enhancing and recovery products. Sport England reported that 6,695,500 individuals attended fitness classes in England during the 2023-2024 period [1]Source: Sport England, "Active Lives Adult Survey November 2023-24", sportengland.org. Millennials and Gen Z are fueling the need for products designed to meet their specific dietary preferences and health goals, fostering innovation and diversification within the market. The World Health Organization's 2024 report highlighting potential savings of EUR 8 billion annually through increased physical activity reinforces policy support for fitness initiatives, creating favorable conditions for market growth. Social media amplifies this trend, with studies demonstrating that influencer trustworthiness and content quality significantly enhance exercise intentions and supplement purchasing behavior among younger consumers.

Expansion of plant-based and clean-label formulations

The European Food Safety Authority streamlined approvals for novel proteins, including duckweed, crickets, and soy leghemoglobin, during 2024-2025, promoting ingredient diversification. As consumers increasingly prioritize products with a reduced environmental impact, manufacturers are shifting towards plant-based formulations due to their lower carbon emissions compared to animal-based proteins. Improved processing technologies are enhancing the taste, texture, and digestibility of plant-based sports nutrition products, addressing previous consumer concerns and boosting adoption. Plant-based protein consumption in Europe now exceeds 1.1 million tonnes annually [2]Source: European Vegetable Protein Association, "Industry and Market", euvepro.eu, with soy and pea proteins leading in commercial applications, according to the European Vegetable Protein Association. The regulatory framework is evolving, with EFSA's updated guidance for novel food applications, effective February 2025, streamlining market entry for innovative protein sources while upholding safety standards.

Premiumization of protein snacks and RTD beverages

Consumers are increasingly willing to pay a premium for products that offer enhanced functionality and convenience. In 2024, Abbott's Ensure brand achieved a significant milestone, exceeding USD 3 billion in global sales. This success, driven by a 9% organic growth in its adult nutrition portfolio, highlights the brand's ability to meet the needs of an aging population. Innovation has expanded beyond traditional protein powders to include ready-to-drink beverages, functional snacks, and specialized formulations designed for specific health outcomes. The approval of glucosyl hesperidin for use in functional drinks, such as energy and sports beverages, with a maximum limit of 525 mg/L, creates opportunities for premium product differentiation. European consumers are increasingly seeking products that combine convenience with scientific validation, fueling demand for clinically-tested ingredients and transparent labeling. Additionally, premium positioning is strengthened by regulatory compliance advantages. Stricter health claims requirements from the European Food Safety Authority (EFSA) favor established brands with strong scientific substantiation.

Rising participation in fitness activities and sports

Emerging fitness trends, including strength training, HIIT, group classes, and outdoor sports, are driving the need for customized nutrition solutions tailored to diverse energy and recovery requirements. Fitness has become integral to wellness and a dynamic social lifestyle, fostering consistent engagement. Group fitness classes and community-focused workouts enhance motivation and adherence, highlighting the growing demand for sports nutrition to support energy and recovery. According to the German Olympic Sports Federation, Germany had 11.3 million fitness sports members [3]Source: German Olympic Sports Federation, "Deutscher Olympischer Sportbund - Bestandserhebung 2024", dosb.de. Infrastructure investments are accelerating participation growth. In 2023, European governments spent EUR 67.6 billion on recreational and sporting services, maintaining a consistent 0.8% share of total government expenditure, as per Eurostat [4]Source: Eurostat, "Government expenditure on recreational and sporting services", ec.europa.eu. WHO data from 2023 shows that 45% of EU citizens did not meet adequate physical activity levels, presenting opportunities for intervention. Policy measures promoting health-enhancing physical activities are further driving the supplement market's growth. Fitness trends like high-intensity interval training, functional fitness, and personalized training services are creating specific nutritional demands, fostering product innovation and market segmentation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EFSA claims approval process | -1.4% | European Union | Long term (≥ 4 years) |

| High cost and variability of raw materials | -1.1% | Europe-based manufacturers | Medium term (2-4 years) |

| Intense competition and market saturation | -0.8% | United Kingdom, Germany, France | Short term (≤ 2 years) |

| Prevalence of counterfeit and substandard products | -0.6% | Cross-border e-commerce | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent EFSA Claims approval process

Regulatory complexities create barriers that benefit established players while hindering innovation for smaller firms. The European Food Safety Authority requires extensive scientific evidence for health claims, yet cognitive benefits of creatine remain unapproved despite increasing consumer interest. Post-Brexit regulatory divergence adds to the challenge, as companies must navigate separate approval processes for the UK and EU, leading to higher compliance costs that disproportionately affect smaller enterprises. The Netherlands' proposed notification system for food supplements, modeled after Belgium and Romania, reflects growing regulatory scrutiny across EU member states. EFSA's updated guidance, effective February 2025, aims to enhance the quality of novel food applications but also extends assessment timelines. An EU task force working to harmonize maximum permitted levels across member states offers potential for regulatory streamlining, though implementation remains uncertain.

High cost and variability of raw materials

Food production costs across Europe have risen sharply due to a doubling of agricultural input and energy prices amid ongoing supply chain disruptions. The Russia-Ukraine conflict has further heightened raw material volatility, particularly for protein ingredients sourced from the affected regions. According to the European Central Bank, food inflation peaked at 15% in March 2023. Processed foods, which constitute 75% of food expenditure, have faced persistent pressure from escalating energy costs. Addressing infrastructure gaps in alternative proteins will require significant investments, with projections highlighting the need for substantial funding by 2030 to scale production facilities for plant-based and cultivated proteins. Rising protein ingredient costs are compelling manufacturers to navigate pricing strategies carefully, balancing them against consumer price sensitivity in highly competitive segments. To mitigate input cost pressures, companies like Glanbia are implementing multi-year transformation programs aimed at achieving annual cost savings of at least USD 50 million by 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protein Dominance Faces Non-Protein Innovation

Sports Protein Products represented 68.24% of the Europe sports nutrition market in 2025, anchored by whey and casein powders widely accepted among gym users. This dominance stems from a robust demand for protein supplements, which are pivotal for muscle recovery, maintenance, and overall fitness, resonating with both athletes and fitness aficionados. However, sports non-protein products are on a growth trajectory, boasting an impressive 8.35% CAGR through 2031, underscoring a burgeoning consumer interest in specialized ergogenic aids. While whey retains its lead due to taste and bioavailability, plant-based alternatives are gaining momentum, championed by sustainability and allergen-friendly labels.

Leading the non-protein demand are creatine, branched-chain amino acids, and colostrum. Meanwhile, ready-to-drink hybrids, merging protein with electrolytes, cater to convenience-seeking consumers and expand usage scenarios. Premium ready-to-drinks (RTDs) are making a mark on upscale shelves, harnessing glucosyl hesperidin for its vascular and energy benefits. With a growing emphasis on consumer education, brands are diversifying their offerings in terms of textures and delivery formats, further propelling the expansion of Europe's sports nutrition market size.

By Distribution Channel: Digital Transformation Meets Retail Renaissance

In 2025, online retail stores dominated the European sports nutrition market, claiming a 56.31% share. This surge was spearheaded by category specialists and major e-commerce players. Digital shoppers, drawn by transparent reviews and dynamic pricing, find loyalty nurtured through diverse product assortments. E-commerce platforms boast a vast array of offerings, spotlighting niche items like vegan proteins and allergen-free bars, often absent from brick-and-mortar stores. Leveraging advanced data analytics and focused digital marketing, these platforms provide tailored recommendations, guiding consumers to products that align with their dietary needs and fitness aspirations.

Meanwhile, supermarkets and hypermarkets are witnessing the fastest growth, posting a notable CAGR of 9.35%. This growth is bolstered by strategic aisle expansions, the introduction of private labels, and the allure of impulse purchases. Physical stores capitalize on the advantage of product sampling and cross-category bundling, effectively increasing basket values. Specialist stores, revered for their niche expertise, offer in-person consultations that resonate with dedicated athletes. At the same time, convenience stores tap into the on-the-go snacking trend, prominently featuring chilled ready-to-drinks (RTDs). Other channels, including gyms, vending machines, and pharmacies, leverage their trusted status to distribute compliant goods. Notably, a wave of fitness center consolidations in Germany is amplifying gym-based sales, seamlessly merging professional coaching with supplement promotions. This diversification across retail channels underscores the resilience and expansive reach of the European sports nutrition market.

Geography Analysis

In 2025, the United Kingdom holds a 32.06% share of Western Europe's market, highlighting its well-established consumer behaviors and strong distribution networks. UK consumers exhibit a preference for premium products, demonstrate strong brand loyalty, and possess a high level of education, all of which drive demand for higher-value formulations. Germany, with a dynamic market projected to grow at a 10.05% CAGR through 2031, is undergoing a transformation fueled by increasing health awareness, a rise in fitness club memberships, and the rapid adoption of vegan and plant-based products. France and Italy maintain significant market positions by capitalizing on their traditional retail strengths and rapidly integrating e-commerce. In contrast, Spain is experiencing growing market penetration among younger demographics, heavily influenced by social media-driven fitness trends. In 2023, EU governments allocated EUR 67.6 billion to recreational and sporting services, with Hungary, Finland, and Sweden leading at 0.7% of their budgets, reflecting strong policy support for market growth, according to Eurostat.

Nordic countries, led by Sweden, exhibit premium market characteristics, including high per-capita consumption and advanced regulatory frameworks that benefit established brands. The Netherlands leads in innovation, promoting proposed food supplement notification systems and actively engaging in EU protein diversification initiatives. Belgium acts as a regulatory testing ground, with its food supplement notification requirements providing valuable insights for broader EU harmonization. Meanwhile, Eastern European countries such as Poland and Russia are emerging as key markets for fitness culture adoption, despite facing significant regulatory complexities.

Cross-border enforcement initiatives highlight the success of regulatory coordination. For instance, OLAF operations targeting counterfeit products linked to major sporting events resulted in the seizure of over 630,000 items, as reported by the European Anti-Fraud Office in 2024. These actions enhance the competitive position of compliant market participants while building consumer trust in legitimate distribution channels. Additionally, regional regulatory harmonization efforts, such as the EU task force's work on standardizing maximum permitted levels, indicate progress toward unified market conditions. This development could reduce compliance challenges and support seamless cross-border expansion strategies.

Regulatory Landscape

Sports nutrition products in Europe generally fall under horizontal EU food law rather than a dedicated sports-food regime, so compliance depends on whether a product is positioned as a conventional food, fortified food, or food supplement. Core requirements include Food Information to Consumers rules under Regulation (EU) No 1169/2011 (labeling, allergens, and nutrition declaration), with supplement-specific provisions anchored in Directive 2002/46/EC (harmonized lists of permitted vitamins and minerals, while maximum amounts are still largely set at Member State level). For enriched formats such as RTDs and bars, formulation and labeling can also intersect with EU rules on the addition of vitamins, minerals, and certain other substances.

Claims and ingredient authorization are key gating factors for premium and science-led positioning. Health and nutrition claims used in labeling and advertising must comply with Regulation (EC) No 1924/2006 and rely on EFSA scientific assessment and EU authorization, which increases substantiation and dossier quality requirements versus many non-EU markets. Novel ingredients, including alternative proteins used in sports nutrition innovation, require pre-market assessment under the EU novel foods framework. EFSA guidance updates effective February 2025 reinforced application expectations while aiming to improve submission quality and process clarity.

Competitive Landscape

Market concentration remains moderate, with competitive dynamics fragmented as leading players employ diverse strategies to capitalize on growth opportunities. Glanbia enhances its portfolio by strategically discontinuing e-commerce operations like Body and Fit and the SlimFast brand, while focusing on strengthening its core brand, Optimum Nutrition. The company's multi-year transformation program, targeting USD 50 million in annual cost savings by 2027, highlights the industry's emphasis on improving operational efficiency amidst rising raw material costs. Abbott's nutrition segment, which achieved 9% organic growth, demonstrates its effective premium positioning, particularly as aging demographics increasingly intersect with sports nutrition demands.

Companies are driving innovation by streamlining regulatory pathways, creating competitive advantages. They are investing in novel food applications and validating health claims to support premium pricing strategies. The European Commission's 2024 approval of five novel food substances, including protein concentrate from Lemna species and beta-glucan from Euglena gracilis, reflects a regulatory openness to innovation, favoring companies with strong research and development capabilities.

Major players such as Glanbia PLC, PepsiCo Inc., Nestle SA, The Hut Group, and Abbott Laboratories prioritize quality as a key element of brand positioning. The market's competitive environment includes both regional and international players. As a result, these leading companies are diversifying their portfolios to stand out through product innovations, strategic partnerships, mergers and acquisitions, and market expansions. White-space opportunities are emerging in areas like personalized nutrition, plant-based formulations, and targeting specific demographics. At the same time, regulatory actions against counterfeit products are strengthening the market positions of legitimate players by building consumer trust and enforcing distribution channel verification requirements.

Europe Sports Nutrition Industry Leaders

-

Glanbia PLC

-

PepsiCo Inc.

-

Nestle SA

-

Abbott Laboratories

-

The Hut Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A visible whitespace in Europe sits at the intersection of regulatory navigation and ingredient innovation, where brands that can support substantiated claims and complete novel food dossiers can differentiate more consistently. Industry advocacy has intensified around practical reforms, including the European Specialist Sports Nutrition Alliance (ESSNA) publishing a 2024 manifesto for the 2024-2029 policy term. It calls for a more streamlined novel foods approval system and more harmonized enforcement across Member States. In parallel, unresolved discussions around maximum permitted levels (MPLs) for vitamins and minerals remained a central topic through 2025 in industry coverage, which continues to drive demand for compliant reformulation, pan-European label architectures, and country-specific portfolio planning.

Europe also continues to attract investments aimed at shortening lead times and improving control over quality, formats, and fulfillment, aligning with demand for RTD beverages and everyday wellness usage. Glanbia has referenced ongoing capacity expansions in Europe during its Q1 2026 update. GymBeam reported 2025 revenue of EUR 232 million (ex VAT) alongside a manufacturing acquisition (KAJA Food) and an automated logistics hub near Milan using AutoStore robots, reflecting scale economics in cross-border DTC and marketplace distribution. Portfolio and channel consolidation also creates openings for specialist and retailer brands to broaden ranges in high-velocity formats. Lactalis acquisition of the UK active nutrition brand Protein Works in June 2026 (following Protein Works investment in a vertically integrated UK hub near Liverpool) reflects continued M&A appetite for established digital brands with manufacturing depth and export potential.

Recent Industry Developments

- July 2026: THG (Myprotein) and Nichols announced a partnership to launch a ready-to-drink Myprotein Clear Whey Protein Water range in the United Kingdom, with a planned market rollout in September 2026. The partnership extends Myprotein beyond powders and snacks into branded RTD hydration-adjacent protein, a format that supports higher purchase frequency and convenience-led use cases. It also pairs an established sports nutrition brand with a UK beverage player to accelerate route-to-market and cold-chain execution.

- May 2026: PepsiCo expanded Gatorade in Italy with Glacier Freeze Zero Zuccheri, entering the zero-sugar functional sports drink segment in the country. This adds competitive pressure in mainstream retail and convenience channels where sugar-reduction claims and everyday hydration positioning influence shopper choice. The launch underscores continued product renovation by large beverage groups to defend share against smaller functional and wellness beverage entrants.

- October 2024: Glanbia, through its Optimum Nutrition brand, launched Optimum Nutrition Protein Hot Chocolate across the United Kingdom and Europe, offering 20 grams of protein per serving with hydrolyzed whey concentrate. The product broadens consumption occasions into hot beverages, supporting premiumization and seasonality resilience beyond traditional shakes. It also reinforces the strategy of established brands using flavor-led innovation while keeping protein delivery central to positioning.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the Europe sports nutrition market includes packaged sports drinks, sports foods, and sports supplements that are bought to support exercise performance, recovery, and everyday active wellness, and it is measured in value terms in USD across European countries.

Scope exclusions: We exclude general functional foods and beverages that are not marketed or used as sports nutrition, along with prescription nutrition and clinical enteral nutrition.

Segmentation Overview

-

By Product Type

-

Sports Protein Products

- Protein/Energy Bars

-

Sports Protein Powder

-

Whey and Casein Powder

- Concentrate

- Isolate

- Others

- Plant-Based Protein Powder

- Other Sports Protein Powders

-

Whey and Casein Powder

- Sports Protein RTD

-

Sports Non-Protein Products

- Creatine

- BCAA

- Others

-

Sports Protein Products

-

By Distribution Channel

- Supermarkets / Hypermarkets

- Convenience Stores

- Specialist Stores

- Online Retail Stores

- Other Distribution Channels (Gyms, Vending, Pharmacies)

-

By Geography

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Sweden

- Belgium

- Poland

- Netherlands

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand pool and the selling environment in Europe, then adding checks on what is allowed to be sold and how it is labeled. Public sources such as Eurostat, national statistics offices, and EU food safety and labeling pages are used to validate population, income, health, and trade signals that can move category demand. We also review sources such as UN Comtrade, customs releases, and selected peer reviewed nutrition and sports science journals to ground ingredient adoption and usage patterns.

On top of this, we use company annual reports, investor presentations, and brand announcements to understand category priorities and route to market shifts, particularly for online and modern retail. Where helpful, we reference paid subscriptions for company financials and intelligence, news and financials, patent databases, and import and export shipment level data to confirm timelines, product pipelines, and the direction of cross border flows. These examples are not exhaustive, and many other public and paid sources were consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure test the market boundary, pricing logic, and the split between sports drinks, sports foods, and sports supplements across major European countries. We speak with a mix of brand and channel stakeholders, ingredient ecosystem participants, and category specialists, then we re check key assumptions with follow up questions when a country level trend looks out of line. Coverage is spread across Europe so that large markets and smaller, fast moving markets are both reflected in the final sizing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 13% | |

| Mid tier: 61% | Functional/Unit leaders: 40% | |

| Smaller Players: 14% | Managers: 47% |

Market-Sizing & Forecasting

Sizing is built using a top down approach where consumption demand is reconstructed from country level category penetration, active lifestyle participation, and retail channel mix, and then values are converted using typical pack sizes and observed price bands. To keep the model realistic, we also create selective bottom up approximations using sampled brand line pricing, channel checks for online versus offline shares, and supplier side volume cues where they are available, and then use these results to adjust totals that look too high or too low.

Inputs that meaningfully move the Europe sports nutrition market include sports and gym participation trends, the share shift toward online retail, the pace of ready to drink and bar format adoption, average selling price movement by format, and regulatory and labeling changes that affect claims and ingredient usage. Forecasts are developed using scenario analysis, with the base case anchored to these variables and stress tested with primary feedback on price elasticity and promotional intensity. When a bottom up check has gaps, we fill them with conservative assumptions tied to nearby countries with similar channel structure, and we review the impact before it is accepted.

Data Validation & Update Cycle

Outputs are triangulated against multiple independent signals such as trade movement direction, observed pricing ranges, and country level category growth narratives from interviews. Variance checks are run to catch odd jumps by country or by product group, and those cases trigger a re check of the underlying drivers. In certain situations, we also do a short re contact with a respondent to confirm what changed.

Before sign off, the model and assumptions go through a multi step analyst review so arithmetic, scope, and country splits are consistent across the workbook and the written analysis. The report is refreshed on an annual cycle, with interim updates when major events occur, for example a large labeling change or a sudden shift in distribution. Right before delivery, a final pass is completed to ensure the latest available public data and market signals are reflected.

Mordor Intelligence's Europe Sports Nutrition Market Sizing Compared With Other Published Estimates

It is common to see different market sizes for Europe sports nutrition because each study draws the boundary in its own way and then uses different price and channel assumptions. Differences can also come from the year used as the base, whether value is reported at retail or closer to manufacturer selling prices, and how quickly currency and inflation changes are refreshed.

By tracking format level pricing and channel mix shifts across key European countries, Mordor Intelligence keeps the total focused on sports drinks, sports foods, and sports supplements sold for performance and active wellness, rather than folding in adjacent weight management or general functional nutrition baskets.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.13 B (2025) | |

| Global Consultancy A | USD 17.64 B (2025) | Uses a wider category set that appears to include meal replacements and weight loss products, which expands the counted demand pool beyond typical sports nutrition purchases. |

| Industry Publisher B | USD 7.23 B (2025) | Likely applies broader inclusion for product forms and functions and may use different price point assumptions, which can lift value even when volumes are similar. |

The spread is mainly explained by what gets counted inside the category and where the price is taken in the value chain. When scope is kept tight to sports nutrition and pricing is checked by format and channel, the total becomes easier to trace back to simple, repeatable drivers across Europe.

Key Questions Answered in the Report

What is the current valuation of the Europe sports nutrition market?

The market is valued at USD 6.61 billion in 2026 and is projected to reach USD 9.64 billion by 2031.

Which product segment is growing fastest across Europe?

Sports Non-Protein Products, including creatine and BCAA blends, lead with an 8.35% CAGR through 2031.

Why is Germany the fastest-growing national market?

Germany benefits from rising gym memberships, government support for alternative proteins, and a 10.05% CAGR outlook.

How are new protein sources entering the market?

EFSA approvals for duckweed, house crickets, and mealworm larvae enable novel, sustainable protein formulations.

Page last updated on: