Left Atrial Appendage Devices Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

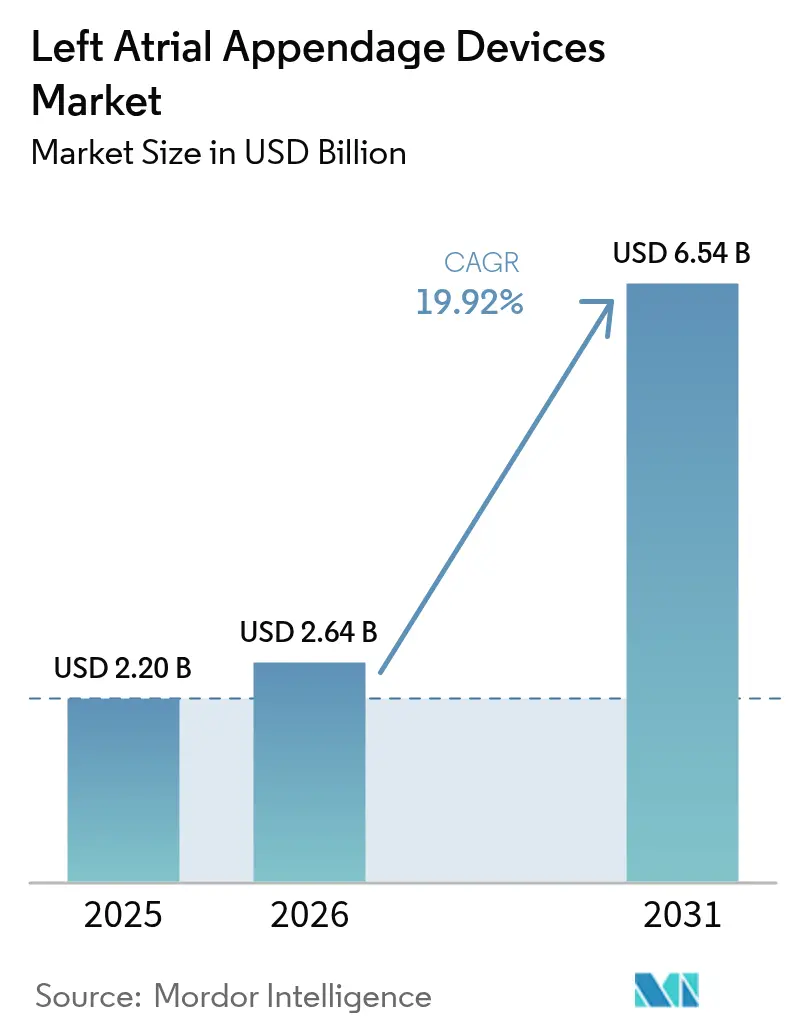

| Market Size (2026) | USD 2.64 Billion |

| Market Size (2031) | USD 6.54 Billion |

| Growth Rate (2026 - 2031) | 19.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Left Atrial Appendage Devices Market Analysis by Mordor Intelligence

The left atrial appendage devices market size was valued at USD 2.2 billion in 2025 and estimated to grow from USD 2.64 billion in 2026 to reach USD 6.54 billion by 2031, at a CAGR of 19.92% during the forecast period (2026-2031). Solid clinical evidence, especially the 8.5% versus 18.1% major bleeding differential reported in the OPTION trial, is redefining stroke-prevention therapy for atrial fibrillation patients.[1]American College of Cardiology, “OPTION Trial Results Show Reduced Bleeding in LAAC Patients,” acc.org Growth is further fueled by an aging population with higher arrhythmia prevalence, expanding ambulatory surgical center (ASC) capabilities, and new U.S. MS-DRG codes that bundle left atrial appendage closure with catheter ablation, making combined procedures financially attractive for hospitals. Oligopolistic competition centers on technological differentiation rather than price, illustrated by Boston Scientific’s 24% WATCHMAN franchise growth in Q1 2025 and ongoing launches of polymer-coated iterations that cut device-related thrombosis. Strategic M&A, including Johnson & Johnson’s USD 400 million Laminar acquisition and Edwards Lifesciences’ USD 1.2 billion twin buy-out of JenaValve and Endotronix—signals consolidation around complementary structural-heart platforms. Consequently, the left atrial appendage devices market benefits from scale-driven R&D investment, broader regulatory pathways, and deepening clinical data that lower adoption hurdles worldwide.

Key Report Takeaways

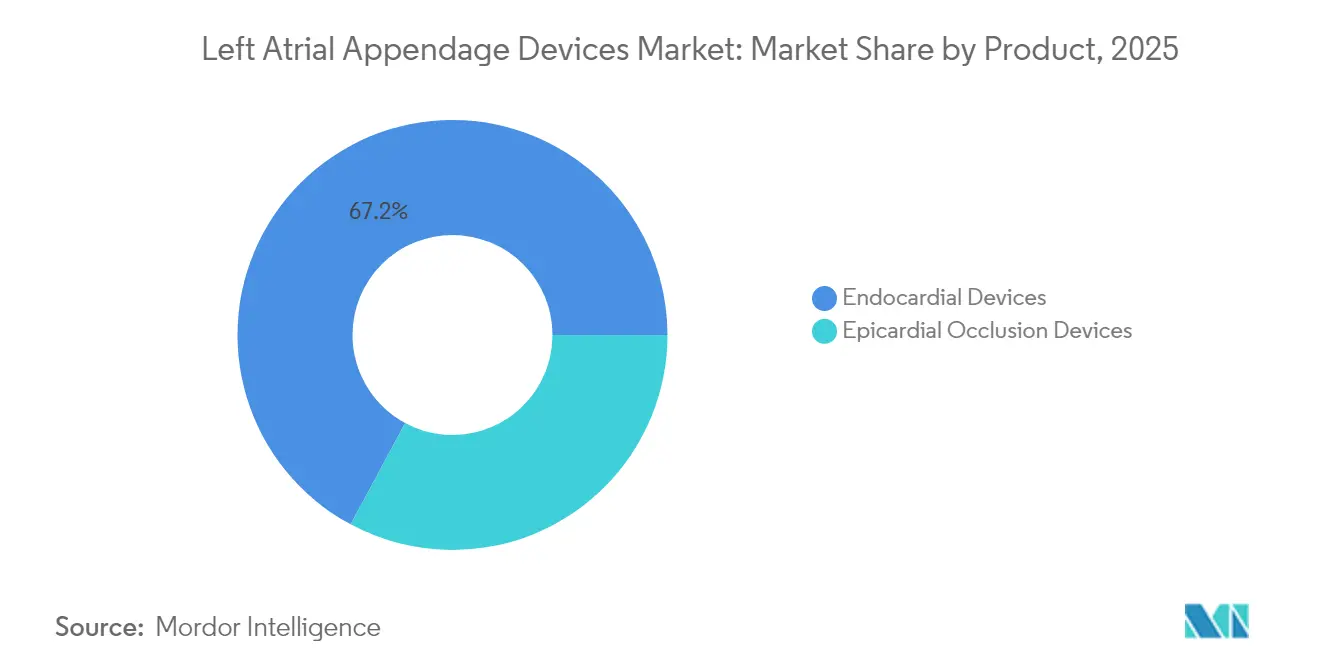

- By product type, endocardial devices led with 67.15% of left atrial appendage devices market share in 2025, whereas epicardial systems are projected to expand at an 18.55% CAGR through 2031.

- By access approach, transcatheter techniques commanded 80.55% share of the left atrial appendage devices market size in 2025, while minimally-invasive surgical methods are racing ahead at an 17.95% CAGR.

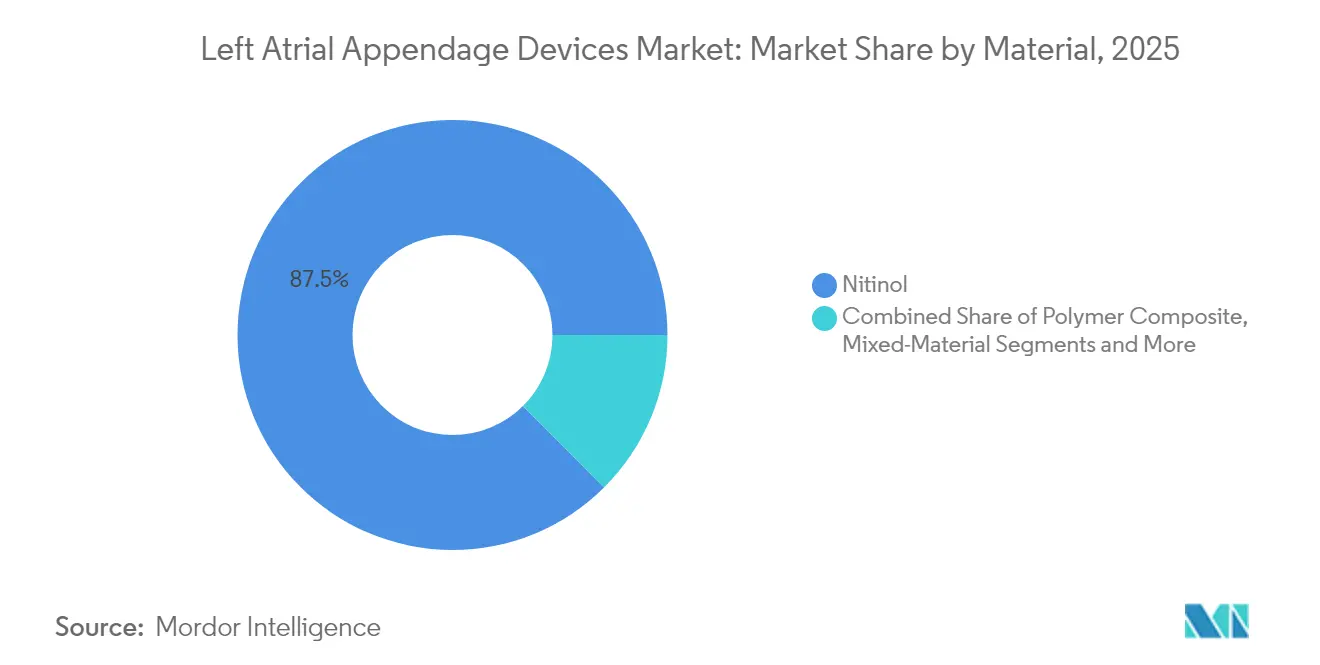

- By material, nitinol devices contributed 87.45% of the 2025 left atrial appendage devices market size; polymer composites are set to grow at a 19.35% CAGR to 2031.

- By end user, tertiary hospitals held 70.55% revenue share of the left atrial appendage devices market in 2025, yet ASCs display the fastest momentum with a 16.85% CAGR.

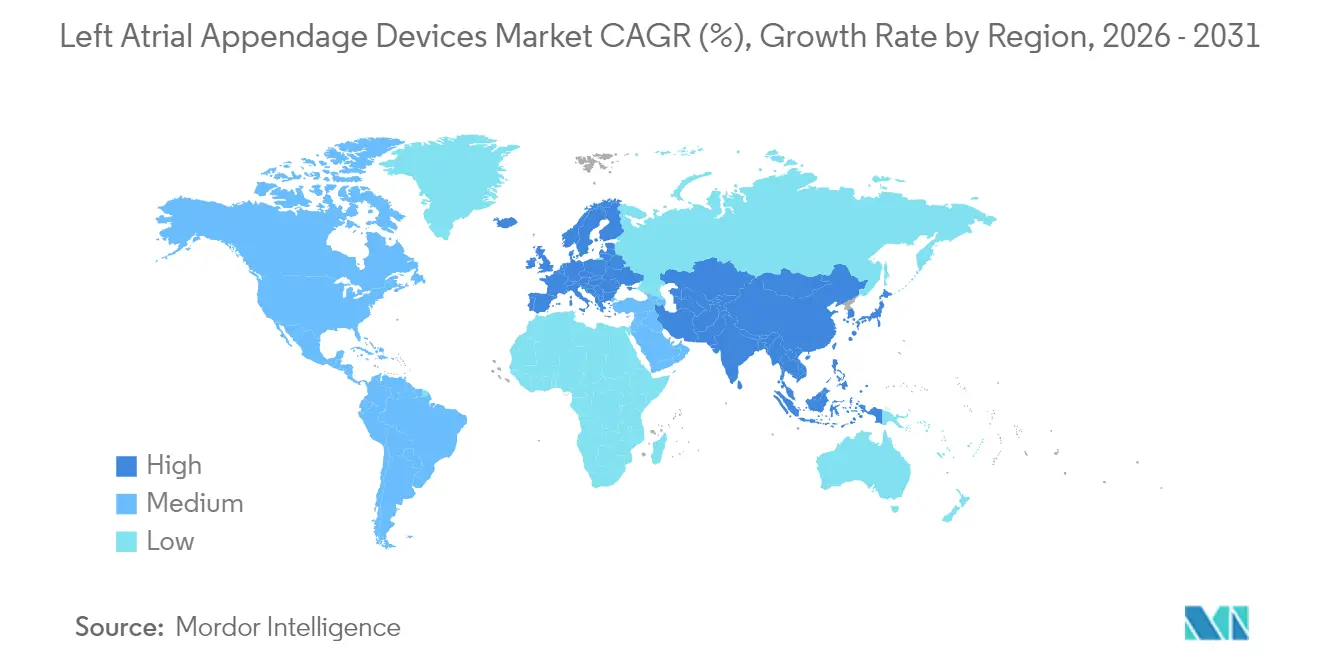

- By geography, North America dominated with 39.15% left atrial appendage devices market share in 2025, whereas Asia-Pacific is forecast to rise at a 13.85% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Left Atrial Appendage Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of atrial fibrillation | +4.20% | Global (peak in North America & Europe) | Long term (≥ 4 years) |

| Adoption as alternative to anticoagulation | +3.80% | North America & Europe, expanding into Asia-Pacific | Medium term (2–4 years) |

| Technological advances in occlusion/imaging | +3.10% | Global, spearheaded by U.S. R&D hubs | Medium term (2–4 years) |

| Expanding reimbursement in US/EU/JP | +2.90% | Core markets of the United States, Europe, Japan | Short term (≤ 2 years) |

| ASC-based structural-heart programs | +2.70% | Primarily North America, nascent uptake in Western Europe | Medium term (2–4 years) |

| Advanced imaging & computational modeling | +2.10% | Global, concentrated within tertiary centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Atrial Fibrillation (AF)

Escalating global AF prevalence of 2.1% overall in South Korea and 8.7% in patients older than 70 enlarges the pool of candidates for mechanical stroke-prevention therapy.[2]Robert J. Russo, “Device-Related Thrombus and Pericardial Effusion After Left Atrial Appendage Closure,” JACC Advances, jaccadvances.org In parallel, improved diagnostics boost case identification in developing economies, broadening the left atrial appendage devices market. Older populations, especially in Europe, double AF prevalence roughly every decade after age 55, sustaining procedural demand well into the 2030s. Moreover, adherence issues with long-term anticoagulation continue to surface, encouraging physicians to opt for a one-time implant. Payers are observing lower hospitalization frequency linked to device-based therapy, validating economic utility. Collectively, these demographic and economic shifts assure long-run expansion of the left atrial appendage devices market.

Growing Adoption as Alternative to Long-Term Anticoagulation

OPTION trial data showing a near-60% reduction in major bleeding is reshaping treatment algorithms. As more than 500,000 implants globally confirm safety, cardiologists increasingly position LAAC ahead of lifelong medication for high bleeding-risk patients. Health economists highlight downstream savings from fewer bleed-related admissions and no INR monitoring, attracting insurers. Public awareness campaigns by leading centers position LAAC as a definitive solution, further propelling the left atrial appendage devices market. Industry pipelines now include devices sized for challenging anatomies, reinforcing therapy suitability across broader cohorts. Together, evidence, economics, and device evolution accelerate preference for implant-based stroke prevention.

Technological Advancements in Occlusion & Imaging Systems

WATCHMAN FLX Pro integrates a polymer HEMOCOAT finish and more visible markers that improve placement precision. Computational modeling and AI-enhanced CT planning streamline sizing and sheath selection, cutting procedure times by up to 20%. Image-guided delivery systems are migrating from tertiary centers to community hospitals, democratizing access. New 40 mm device iterations accommodate appendages previously managed surgically, broadening market scope. Developers are co-designing devices with pulsed-field ablation catheters to enable same-session rhythm control and stroke protection. These innovations sustain pricing power and support value-based purchasing strategies that favor the left atrial appendage devices market.

Expanding Reimbursement Coverage

The 2025 CMS MS-DRG 317 code covers combined ablation plus LAAC and offers hospitals full payment parity, spurring same-day dual interventions. Germany and France already reimburse LAAC nationally, while Spain and Italy moved toward broader coverage after cost-utility studies. In Japan, device-level coverage for stroke prevention aligns with fiscal pressure to curb long-term anticoagulant subsidies. Private payers follow government leads, easing approval pathways. Overall, payment certainty eliminates a key bottleneck, pushing the left atrial appendage devices market into mainstream cardiovascular care.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Device & Procedure Cost | -2.10% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Risk Of Device-Related Thrombus & Pericardial Effusion | -1.80% | Global, varies by operator experience | Short term (≤ 2 years) |

| Limited Operator Training & Steep Learning Curve | -1.40% | Global, concentrated in community hospitals | Medium term (2-4 years) |

| Supply-Chain Volatility For Nitinol Components | -1.20% | Global, most impact in high-volume markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Device & Procedure Cost

Despite long-term economic merits, the roughly USD 20,000 all-in procedural bill including device, imaging, and physician fees—limits adoption in self-pay markets. Emerging economies face currency-exchange volatility that inflates imported device prices. Government tenders often prioritize acute coronary supplies over preventive implants, delaying uptake. Manufacturers offer risk-sharing contracts, but budget-constrained hospitals still hesitate. As domestic manufacturing develops in China and India, device ASPs may ease, yet short-to-mid-term growth remains tempered outside reimbursement-rich regions of the left atrial appendage devices market.

Risk of Device-Related Thrombus & Pericardial Effusion

Registry data show a 1.3% device-related thrombus (DRT) incidence, necessitating transient anticoagulation that partially offsets bleeding-risk claims.[3]Yeong-Dae Kim, “Atrial Fibrillation Epidemiology in a Korean Nationwide Cohort,” Journal of Korean Medical Science, pmc.gov Pericardial effusion rates decline with operator experience, yet remain a deterrent for hospitals new to structural-heart programs. Training programs and enhanced visualization markers are mitigating these issues, but publicized adverse events continue to influence conservative physicians. Consequently, some centers restrict LAAC to high-risk cohorts, moderating near-term procedure growth in sections of the left atrial appendage devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Endocardial Dominance Faces Epicardial Innovation

Endocardial devices contributed USD 1.48 billion, or 67.15%, of the 2025 left atrial appendage devices market size, anchored by WATCHMAN, Amplatzer Amulet, and LAmbre implants. Procedural familiarity and catheter lab availability keep endocardial implants firmly entrenched. However, AtriCure’s AtriClip portfolio is advancing at an 18.55% CAGR, making epicardial clips the fastest-rising alternative. Surgeons appreciate clip-based closure that leaves no intraluminal implant, freeing patients from any antiplatelet regimen. Over time, convergent hybrid devices combining endocardial reach with epicardial sealing may emerge, underscoring coexistence rather than displacement within the left atrial appendage devices market.

Shifting practice also stems from surgical efficiency. During valve or coronary bypass operations, clips are deployed within 90 seconds, adding negligible OR time. Meta-analyses reveal 98% complete closure with clips versus variable endocardial seal rates, especially in chicken-wing anatomies. Still, endocardial products hold broader reimbursement support and fit percutaneous workflows, which is crucial for ASC settings. Device developers are now co-sponsoring trials that directly compare the two approaches, helping clinicians stratify patients and sustaining a balanced share across the left atrial appendage devices market.

By Access Approach: Transcatheter Leadership Challenged by Surgical Innovation

Transcatheter delivery owned 80.55% of 2025 revenue thanks to widespread cath-lab infrastructure. Operators value femoral-vein entry, familiar sheath systems, and same-day discharge. Yet minimally invasive thoracoscopic approaches are climbing at an 17.95% CAGR. Robot-assisted thoracoscopic clip placement now finishes inside 45 minutes with minimal postoperative pain, making it appealing for patients requiring no foreign material in the atrium.

Open-heart access retains a niche for concomitant cardiac surgery but lacks growth impetus. Meanwhile, hybrid cath-lab/OR suites are being built so hospitals can switch access routes mid-procedure if imaging reveals unsuitable anatomies. Boston Scientific’s OPTION-A study in Asia-Pacific confirms investment in diversified techniques, reinforcing flexibility within the left atrial appendage devices market.

By Material: Nitinol Supremacy Faces Polymer Challenge

Nitinol’s shape-memory and radial strength qualities justify its 87.45% 2025 share due to its superelasticity, which eases recapture-and-re-deploy maneuvers, vital for complex lobes. Even so, polymer composites are climbing at 19.35% CAGR. Early data on polyethylene terephthalate (PET) mesh frameworks show faster endothelialization and lower DRT, convincing risk-averse physicians.

Manufacturers now combine nitinol frames with polymer surfaces, delivering best-of-both hybrids. Boston Scientific’s HEMOCOAT is one such example, featuring a chromatophore-inspired hydrophilic layer that lowers platelet adhesion. Should supply shortages or cost spikes hit nickel-titanium alloys, polymer alternatives could accelerate, adding resilience to the left atrial appendage devices market supply chain.

By End User: Hospital Dominance Yields to ASC Growth

Tertiary hospitals accounted for 70.55% of 2025 revenue, reflecting broad device inventories, imaging equipment, and on-call surgical backup. ASCs, however, are expanding at 16.85% CAGR. Favorable CMS site-of-service differentials allow physician-owned centers to capture margin, and lean staffing models halve facility costs. Device makers supply turnkey training, cloud-based echo interpretation, and on-demand proctorship to de-risk first cases. Specialty heart clinics bridge the two ends, running weekday LAAC lists while routing complex anatomies to tertiary centers, keeping the broader left atrial appendage devices market accessible.

Patient satisfaction plays a key role. Surveys reveal 94% of ASC patients prefer outpatient implants to hospital stays, citing quicker mobility and lower infection anxiety. Meanwhile, hospitals defend volume through same-day discharge protocols and bundled procedures such as ablation-plus-LAAC, adding value that ASCs cannot yet replicate for higher-risk cohorts.

Geography Analysis

North America attained a 39.15% of the 2025 left atrial appendage devices market share, buoyed by Medicare and private-payer coverage. Device maker field-training keeps more than 3,000 implanters active, spreading access beyond metropolitan hubs. New MS-DRG codes have already boosted combined ablation-LAAC case volumes by 12% over the 2024 baseline. Canada’s single-payer system rolled out national coverage in late 2024, widening referral funnels, while Mexico shows early momentum through medical tourism packages that undercut U.S. prices.

Europe’s mixed public-insurance systems create patchy but steady adoption. Germany leads with nearly 150 implanting centers, whereas the United Kingdom’s NHS budgets slow uptake despite favorable NICE guidance. France, Italy, and Spain unlocked broader coverage in late 2024, kick-starting double-digit growth. Clinician networks such as EuroACT share best practices, improving consistency across borders and sustaining expansion inside the left atrial appendage devices market.

Asia-Pacific outpaces all regions at a 13.85% CAGR. China’s National Medical Products Administration (NMPA) cleared two domestic devices in 2024, sparking price competition that could drive penetration in tier-2 cities. Japan’s seasoned electrophysiology community leverages generous reimbursement, making the country a bellwether for broader APAC adoption. India’s private hospitals serve rising middle-class demand, though government insurance remains limited. Australia, South Korea, and Singapore form regional training hubs, exporting expertise to neighbors. Overall, demographic aging and economic ascent ensure APAC’s pivotal role in the future left atrial appendage devices market.

Competitive Landscape

Boston Scientific anchors the market with its WATCHMAN franchise, capturing a leading share and posting 24% YoY revenue growth in Q1 2025. The firm’s successive FLX and FLX Pro launches showcase polymer enhancements and broader size matrices, keeping a first-mover advantage. AtriCure dominates epicardial territory; its AtriClip suite delivered record sales after the FLEX-Mini launch in February 2025, buoyed by surgeon preference for clip-based closure in operating rooms. Abbott, while historically focused on Amplatzer Amulet, intensified R&D in pulsed-field ablation-compatible occluders, aiming at dual-therapy platforms.

Consolidation remains a strategic theme. Johnson & Johnson MedTech’s USD 400 million Laminar buy brings a rotational appendage elimination system into its Biosense Webster electrophysiology empire, creating synergy around combined ablation and occlusion solutions. Edwards Lifesciences’ USD 1.2 billion acquisitions of JenaValve and Endotronix extend its transcatheter valve pedigree to adjacent structural-heart indications. Teleflex’s planned EUR 760 million purchase of BIOTRONIK’s vascular arm will hand it European distribution muscle and diversified cath-lab tools.

Competitive battlegrounds now revolve around evidence generation and geographic reach. Ongoing OPTION-A and OPTION-M trials in APAC and Latin America provide localized data that unlock regulatory approvals and physician confidence. Manufacturers invest in remote proctoring and AI-driven echo support to court community hospitals and ASCs. As a result, price competition remains subdued; instead, device makers differentiate on coating technologies, sheath profiles, and integrated software—factors sustaining premium ASPs across the left atrial appendage devices market.

Left Atrial Appendage Devices Industry Leaders

Articure

Boston Scientific Corporation

Johnson & Johnson

Abbott Laboratories

Lifetech Scientific

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Boston Scientific initiated the OPTION-A clinical trial in Asia-Pacific, pairing FARAPULSE PFA ablation with WATCHMAN FLX for single-session AF management.

- March 2025: Boston Scientific led a USD 175 million funding round in 4C Medical Technologies, advancing transcatheter mitral repair.

- February 2025: Teleflex agreed to acquire BIOTRONIK’s Vascular Intervention business for EUR 760 million (USD 820 million), closing by Q3 2025.

- February 2025: AtriCure launched AtriClip FLEX-Mini and cryoSPHERE+ within the United States market.

Global Left Atrial Appendage Devices Market Report Scope

As per the scope of the report, the left atrial appendage is a microscopic ear-shaped sac located in the upper changer of the heart. Left atrial appendage are medical devices that are used for preventing the risk of heart stroke in the body.

The left atrial appendage devices market is segmented by product type (endocardial and epicardial), end user (hospitals, ambulatory surgical centers, and others), and geography (North America, Europe, Asia-Pacific and Rest of the World). The report offers the value (in USD million) for the above segments.

| Endocardial Occlusion Devices |

| Epicardial Occlusion Devices |

| Transcatheter |

| Minimally-Invasive Surgical |

| Open Surgical |

| Nitinol |

| Polymer Composite |

| Mixed-Material |

| Tertiary Care Hospitals |

| Ambulatory Surgical Centers |

| Specialty Heart Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Endocardial Occlusion Devices | |

| Epicardial Occlusion Devices | ||

| By Access Approach | Transcatheter | |

| Minimally-Invasive Surgical | ||

| Open Surgical | ||

| By Material | Nitinol | |

| Polymer Composite | ||

| Mixed-Material | ||

| By End User | Tertiary Care Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Heart Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the left atrial appendage closure market?

The market stands at USD 2.64 billion in 2026 and is projected to hit USD 6.54 billion by 2031, reflecting a 19.92% CAGR.

Which device type holds the largest market share?

Endocardial occluders dominate with a 67.15% share, thanks to robust evidence and widespread catheter-lab infrastructure.

Which region is growing the fastest?

Asia-Pacific leads growth with a 13.85% CAGR, propelled by improving healthcare access and aging demographics.

How has reimbursement influenced adoption in the United States?

CMS’s new MS-DRG 317 now pays hospitals for same-session ablation and LAAC, boosting combined procedure volumes and broadening patient eligibility.

Why are ambulatory surgical centers important for future growth?

ASCs offer lower overheads and patient-preferred outpatient care, expanding procedural capacity and supporting a 16.85% CAGR within this setting.

Page last updated on: